What to Know About Student Loans and College Costs in 2026

In 2026, the landscape of American higher education is defined by a striking paradox: while the actual net price of tuition is falling for many families due to record institutional discounting, the rules for financing that education have become radically more restrictive. The recently enacted One Big Beautiful Bill Act (OBBBA) imposes strict new federal borrowing caps and phases out popular income-driven repayment plans, just as federal student loan interest rates reach their highest levels in over a decade. For prospective students and their families, navigating this environment requires looking past published sticker prices, aggressively planning for new borrowing limits, and preparing for the return of federal taxes on canceled student debt.

The True Cost of College: Sticker Price vs. Net Price

When evaluating the financial burden of a four-year degree, the most pervasive mistake families make is anchoring their financial decisions to the published "sticker price." The sticker price functions much like the manufacturer's suggested retail price on a vehicle - a starting point that very few consumers actually pay.

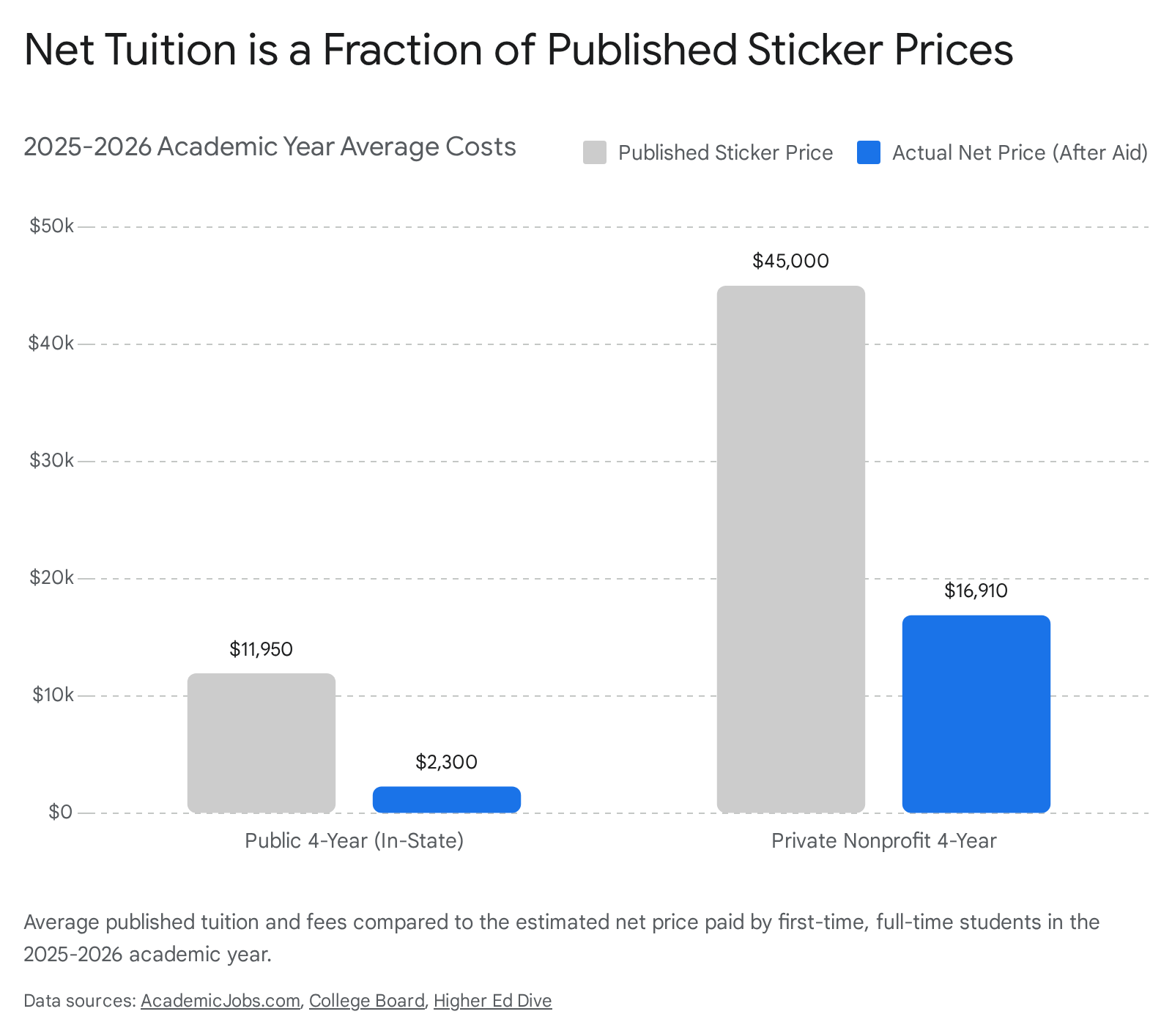

For the 2025 - 2026 academic year, the average published tuition and fees reached $11,950 for in-state public universities and $45,000 for private nonprofit institutions 112. However, the metric that dictates a student's true financial obligation is the net price. This figure represents the actual amount paid out-of-pocket after subtracting grants, scholarships, and institutional financial aid 14.

Driven by intense enrollment competition and robust financial assistance pools, the average net tuition at public four-year institutions has plunged. Adjusted for inflation, the average net tuition paid by first-time, full-time in-state students has fallen to an estimated $2,300 for the 2025 - 2026 academic year, representing a dramatic 48% decline from its 2012 peak of $4,450 113. Private nonprofit institutions mirror this trajectory. These schools increasingly rely on heavy institutional discounting - often offering average tuition discounts exceeding 50% - to remain competitive with heavily subsidized public flagship universities 24. Consequently, the average net tuition at private colleges has dropped to $16,910 in constant 2025 dollars, down from nearly $20,000 two decades prior 113.

How Family Income Dictates Actual Costs

The divergence between sticker price and net price is heavily influenced by a family's financial background. Elite private schools, which boast massive endowments, frequently deploy need-based aid so aggressively that they become cheaper for low-income applicants than their local state universities 24. Conversely, high-earning families are routinely expected to pay the full published cost.

A 2026 analysis of federal College Scorecard data spanning thousands of four-year schools illustrates this precise stratification. The data reveals a consistent pattern where the actual financial burden scales steeply alongside household earnings.

| Family Income Bracket | Typical Net Price per Year (Private Nonprofit) |

|---|---|

| $0 to $30,000 | $5,000 to $15,000 4 |

| $30,001 to $48,000 | $10,000 to $20,000 4 |

| $48,001 to $75,000 | $15,000 to $30,000 4 |

| $75,001 to $110,000 | $25,000 to $40,000 4 |

| $110,001 and above | $35,000 to $55,000 4 |

Families making decisions based solely on the published sticker price run the risk of making an $80,000 mistake over four years by artificially limiting their search to schools with lower advertised rates, missing out on institutions that offer superior internal grants 4.

The Hidden Non-Tuition Costs and Campus Inflation

While net tuition is demonstrably falling, the broader Cost of Attendance (COA) continues to strain household budgets. The COA encompasses everything required to live and study for a year, including housing, food, transportation, and personal expenses. By 2026, non-tuition costs account for more than 50% of a student's total budget at many public universities 2.

On-campus room and board alone routinely runs between $10,000 and $18,000 per year, while textbooks, specialized software, and personal expenses add an additional $3,000 to $6,000 annually 45. When these indirect expenses are aggregated, the total cost of attendance for public four-year institutions reaches approximately $38,700 annually for in-state students, while private nonprofit colleges demand an average of $56,600 8.

Furthermore, families must account for compounding tuition inflation over a four-year degree timeline. While the staggering double-digit tuition hikes of the 1980s have subsided, modern college costs still reliably increase at roughly 3% to 5% per year 48. A school charging a net price of $15,000 during a student's freshman year will likely charge over $17,200 by their senior year. Over four years, a standard 4% annual tuition increase adds roughly $3,000 to $5,000 to the total cost relative to holding tuition flat 4. Forecasting the true economic cost requires multiplying the first-year net cost by a minimum of 1.15 to account for this inflationary tail risk.

State-by-State Tuition Differences and Regional Reciprocity

The baseline cost of higher education varies sharply depending on where a student claims residency. Because public institutions are heavily subsidized by local taxpayer dollars, they extend significantly lower tuition rates to in-state residents while charging a premium to non-residents.

The national average out-of-state tuition at public four-year institutions sits at roughly $29,000 to $31,000, creating a massive gap compared to the $11,000 in-state average 596. At highly sought-after flagship universities, this differential is even more pronounced. For example, the University of Michigan charges non-residents upward of $63,000 in out-of-state tuition, while the University of Virginia charges roughly $60,900 6. Even within the boundaries of in-state tuition, geographic disparity is vast. Florida offers the lowest average yearly in-state tuition at just $4,540 to $4,836, while states in New England charge steep premiums, with Vermont leading the nation at over $17,600 to $19,200 for in-state public tuition 56.

Regional Exchange Programs

To mitigate the out-of-state tuition penalty, families increasingly rely on regional reciprocity agreements. These coalitions allow students to cross state lines without absorbing the full financial shock of non-resident pricing.

The Western Undergraduate Exchange (WUE), operated by the Western Interstate Commission for Higher Education, spans 16 western states and strictly caps out-of-state tuition at 150% of the destination institution's in-state rate 96. In the 2023 - 2024 academic year alone, students utilizing the WUE saved over $559 million in collective tuition costs 6. Similarly, the Midwest Student Exchange Program (MSEP) covers nine midwestern states, offering comparable 150% caps at public institutions and 10% base tuition reductions at participating private colleges, resulting in average individual savings of over $7,200 annually 6.

The Expansion of State "Promise" Programs

Rather than merely discounting tuition, several state legislatures have pushed forward with aggressive "free college" or "promise" programs designed to retain local talent and shield lower-income families from the student debt crisis.

New Mexico's Opportunity Scholarship has emerged as one of the most generous and universal programs in the country 1112. The state covers 100% of tuition and fees for any resident attending a public college or university within the state. Crucially, the New Mexico model features no family income limit; students only need to maintain a 2.5 GPA to retain the funding through both associate and bachelor's degrees 1112.

Other states maintain highly effective, though income-restricted, models. New York's Excelsior Scholarship covers total tuition at City University of New York (CUNY) and State University of New York (SUNY) schools for families earning up to $125,000 annually 11. California's College Promise guarantees two full years of community college tuition for first-time students regardless of income, while programs in states like Michigan target adults over the age of 25 returning to community college to acquire high-demand vocational certificates 11.

Is the Return on Investment Still Worth It?

As the cost of attendance climbs, skepticism regarding the intrinsic value of a college degree has intensified. However, comprehensive economic data overwhelmingly suggests that higher education remains a mathematically sound investment, provided students are strategic about their fields of study and the amount of debt they leverage.

According to 2025 research from the Federal Reserve Bank of New York, acquiring a bachelor's degree yields a 12.5% increase in lifetime earnings compared to halting education at a high school diploma 7. This return sits well above the 8% threshold traditionally considered necessary for a sound financial investment 7. Across their entire careers, individuals holding a bachelor's degree earn approximately 67% more than their peers who possess only a high school education 8.

Despite this broad macroeconomic advantage, the Return on Investment (ROI) of higher education is deeply fragmented. A 2026 longitudinal study scoring 1,665 four-year institutions on financial ROI found that only 18% of schools were rated as "Strong" or "Exceptional." Conversely, 42% of institutions scored as "Poor" 15. At schools in the bottom decile, graduates routinely face debt-to-income ratios exceeding 1.0, meaning they enter the workforce owing more in student loan principal than they can expect to earn in their entire first year of employment 15.

The Deciding Factors: Major and Institution Type

The specific field of study is the most significant variable in determining a student's future financial security. A comprehensive analysis by the Foundation for Research on Equal Opportunity (FREOPP), which estimated the ROI for over 53,000 distinct degree and certificate programs, revealed that degrees in engineering, computer science, and nursing reliably generate lifetime earnings exceeding $500,000 above the median baseline 9. In contrast, degrees in the fine arts, general education, and psychology frequently offer minimal to zero net financial return when factoring in the cost of borrowing and the opportunity cost of lost wages while in school 9.

The type of institution also plays a critical role in the ROI calculation. While prestigious private universities often dominate public perception, public universities are projected to surpass private colleges in median financial ROI by 24% over the coming decade 10. This shifting dynamic is not necessarily indicative of superior educational quality at public schools, but rather a reflection of the math surrounding initial debt loads. Because the baseline tuition at public institutions is structurally lower, students graduate with significantly less debt, allowing their early-career salaries to compound into wealth rather than being siphoned off by high-interest loan servicing.

The 2026-2027 FAFSA Rollout and Aid Application Changes

The gateway to all federal and institutional financial aid is the Free Application for Federal Student Aid (FAFSA). Following several tumultuous years marked by delayed rollouts and severe software glitches, the Department of Education stabilized the system for the 2026 - 2027 academic cycle. The department successfully launched the new FAFSA application on September 24, 2025, beating the congressionally mandated October 1 deadline and completing the earliest launch in the program's history 11122021.

The modernized system benefits from rigorous beta testing conducted in the late summer of 2025. Over 14,000 students successfully submitted forms during this phase, with the platform reporting a 95% to 97% user satisfaction rating and no critical software bugs 111220. The updated form cuts wait times and streamlines the complex verification process 1121. Rather than requiring students to manually collect and input their parents' sensitive tax details, the 2026 - 2027 system allows applicants to simply invite a parent, guardian, or spouse via email. The contributor receives a secure code linking them directly to the form, drastically reducing manual entry errors 1121. Early data indicates these improvements are driving higher completion rates; in states like Alabama, FAFSA completion among high school seniors jumped to 60% early in the cycle, an improvement of three percentage points over the previous year 11.

New Asset Exemptions Under the OBBBA

The FAFSA calculation formula has also been meaningfully altered by the recent passage of the One Big Beautiful Bill Act (OBBBA). In a significant win for rural families and entrepreneurs, the law institutes new asset exemptions that protect specific types of generational wealth from penalizing a student's financial aid eligibility.

Beginning with the 2026 - 2027 aid year, the Student Aid Index (SAI) calculation completely excludes the net worth of family farms on which the family resides, family-owned businesses with fewer than 100 full-time employees, and family-controlled commercial fishing businesses 2213. By removing these often illiquid assets from the calculation, students from agricultural and small business backgrounds will likely qualify for larger federal and state grant packages than in previous cycles.

Federal Student Loan Interest Rates Hit Recent Highs

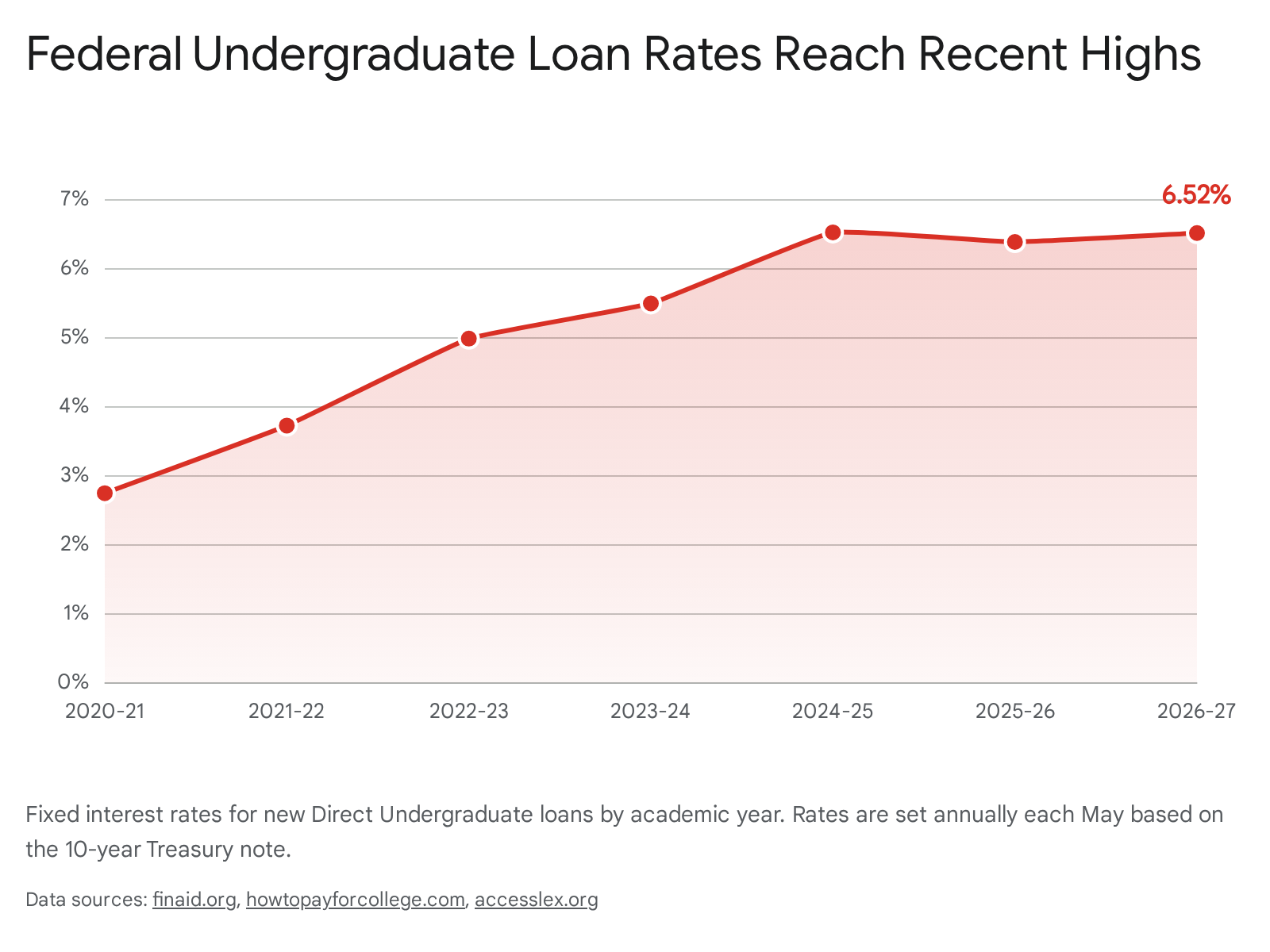

While the application process has smoothed out, the actual cost of borrowing has surged. Borrowers taking out new federal student loans for the 2026 - 2027 academic year face some of the highest fixed borrowing costs seen since the late 2000s 14.

Federal student loan interest rates are not determined arbitrarily by the Department of Education. Instead, Congress mandates that rates be recalculated every spring based on the high yield of the final 10-year Treasury note auction held in May, plus a fixed statutory percentage markup that varies by the specific loan type 14152616. Because the broader macroeconomic environment has sustained higher baseline borrowing costs, the May 2026 Treasury auction yielded 4.47%, a measurable increase from the 4.34% yield recorded the previous year 151718.

Consequently, all new federal student loans disbursed between July 1, 2026, and June 30, 2027, will carry higher fixed interest rates. Once a federal loan is disbursed, that specific rate is locked in for the life of the loan; it will not fluctuate with future market changes 14161819.

For the 2026 - 2027 academic year, Direct Subsidized and Unsubsidized loans for undergraduates sit at 6.52% 141617.

Direct Unsubsidized loans for graduate students have breached the eight-percent mark, landing at 8.07% 161718. The most expensive federal options, Parent PLUS and Graduate PLUS loans (where still applicable), now carry an imposing 9.07% fixed interest rate 14161718.

The Hidden Penalty of Origination Fees

The quoted interest rate does not reflect the total cost of federal borrowing. The Department of Education continues to assess mandatory upfront origination fees, which are deducted proportionately from each loan disbursement before the funds ever reach the university 1431. For standard undergraduate and graduate direct loans, the fee is currently set at 1.057% 141719. For PLUS loans, the government seizes a much larger 4.228% fee upfront 14171931. This means a parent borrowing $20,000 will instantly lose nearly $850 to fees but will still accrue interest on and be required to repay the full $20,000 principal.

Federal student loan rates are applied uniformly to all borrowers regardless of their credit score, income, or financial history 142618. While this universality protects lower-income families who might otherwise be denied credit, it presents a significant disadvantage for highly creditworthy borrowers. Graduate students and parents with excellent credit profiles may increasingly find that private student loans offer interest rates well below the 8% or 9% federal threshold, particularly when factoring in the absence of private origination fees 14261718. However, pivoting to the private market requires sacrificing critical federal safety nets, including access to income-driven repayment frameworks and loan forgiveness programs.

The OBBBA: Radical New Limits on Federal Borrowing

For decades, higher education financing was defined by the federal government's willingness to lend almost unlimited amounts of money to graduate students and parents. Through the PLUS loan programs, borrowers could legally take out federal debt up to the total Cost of Attendance minus any other financial aid received, effectively allowing students to finance luxury apartments and exorbitant private school tuitions entirely with taxpayer-backed loans 1920.

That era officially ends on July 1, 2026.

Passed in July 2025 as part of a sweeping budget reconciliation package, the One Big Beautiful Bill Act (OBBBA) fundamentally restructures federal financial aid 202122. Aiming to curb a national student debt crisis that has ballooned to over $1.6 trillion, the legislation imposes strict new annual and lifetime borrowing caps 20212324. While these changes shield taxpayers, they leave many incoming graduate students and parents scrambling to cover immediate funding gaps.

The End of Unlimited Grad PLUS and Parent PLUS Borrowing

The most aggressive policy shift in the OBBBA is the total elimination of the Graduate PLUS loan program for new borrowers beginning July 1, 2026 22131720212526. Without Grad PLUS, new graduate students are restricted entirely to Direct Unsubsidized loans. These are now strictly capped at an annual limit of $20,500, with an aggregate graduate borrowing limit of $100,000 20212527.

Recognizing that certain degrees require vastly more capital, the law creates a new statutory distinction between "graduate" and "professional" students. Students enrolled in specifically designated professional programs - such as Medicine (M.D., D.O.), Law (J.D.), Dentistry (D.D.S.), and Veterinary Medicine (D.V.M.) - are granted a higher annual borrowing limit of $50,000, capped at an aggregate of $200,000 20212527. However, even these expanded limits fall drastically short of the total cost of attendance at most elite medical and law schools, virtually guaranteeing that future doctors and lawyers will be forced into the private, credit-based lending market 1820.

Parent PLUS loans survived the legislative culling but were heavily restricted. Parents of dependent undergraduates may no longer borrow up to the total cost of attendance. Instead, Parent PLUS loans are now capped at an annual maximum of $20,000 per dependent student, with a hard lifetime aggregate limit of $65,000 per student 131720242526. This cap applies regardless of whether previous loans have been repaid or discharged 24.

Finally, the OBBBA institutes a sweeping, absolute lifetime federal borrowing limit. Across all loan types - undergraduate, graduate, and professional - a single student may not borrow more than $257,500 in federal student debt over the course of their life 13212427.

| Borrower Type | Federal Loan Limits (Pre-July 2026 Rules) | Federal Loan Limits (Effective July 1, 2026) |

|---|---|---|

| Dependent Undergraduate | $31,000 aggregate | $31,000 aggregate (Unchanged) 28 |

| Independent Undergraduate | $57,500 aggregate | $57,500 aggregate (Unchanged) 28 |

| Parent PLUS (Per Student) | Up to total Cost of Attendance (No cap) | $20,000 annually / $65,000 lifetime limit 13202426 |

| Graduate Student | $138,500 aggregate / Grad PLUS up to COA | $20,500 annually / $100,000 aggregate limit (Grad PLUS eliminated) 20252627 |

| Professional Student (Med, Law) | Varies / Grad PLUS up to COA | $50,000 annually / $200,000 aggregate limit 20212527 |

| Absolute Lifetime Limit | None | $257,500 across all degree levels combined 13212427 |

(Note: Under the OBBBA, loan limits for both undergraduate and graduate students will now be heavily prorated if a student is enrolled less than full-time 13242628.)

The "Legacy" Exception for Current Borrowers

To prevent immediate disruption for students mid-way through their degrees, the OBBBA includes a transitional "legacy provision" (sometimes referred to as the limited exception). If a student or parent received a federal loan prior to July 1, 2026, and remains enrolled in that same credentialed program, they are grandfathered into the old borrowing rules 1724252627.

Under this exception, a parent can continue pulling unlimited Parent PLUS loans, and a graduate student can continue utilizing Grad PLUS loans to cover the full cost of attendance, for up to three academic years or until the student completes the specific program, whichever occurs first 1724252627. However, legacy status is highly volatile. A borrower permanently loses access to these old rules if the student takes a leave of absence, withdraws for a term, or changes their degree program 24.

The End of SAVE and the Launch of the Repayment Assistance Plan (RAP)

Simultaneous with the borrowing overhaul, the mechanisms for repaying federal student debt have been completely rewritten. For years, the Department of Education offered a dizzying array of Income-Driven Repayment (IDR) plans - such as IBR, ICR, PAYE, and REPAYE - each with distinct mathematical formulas and timelines.

In 2023, the Biden administration attempted to streamline this with the SAVE (Saving on a Valuable Education) plan, which offered wildly lower monthly payments and accelerated forgiveness 4129. However, after a prolonged legal battle with Republican-led states, the Eighth Circuit Court of Appeals ruled the SAVE plan unlawful in March 2026 29303145. Consequently, the 7.5 million borrowers enrolled in SAVE - who spent nearly two years in an administrative forbearance accumulating interest without earning credit toward forgiveness - have received mass warnings from the Department of Education 293145. These borrowers are required to transition out of SAVE and into a different, legally authorized repayment plan by late 2026, or they will be automatically defaulted into standard 10-year repayment 30314532.

Understanding the New Repayment Assistance Plan (RAP)

To replace the fractured system of legacy IDR plans, the OBBBA created a single, consolidated income-driven option launching on July 1, 2026: the Repayment Assistance Plan (RAP) 132229303334. For any new federal student loan disbursed on or after that date, borrowers will only have two repayment choices: a tiered Standard Repayment Plan (spanning 10 to 25 years based on total debt) or the new RAP 221322272830333435.

RAP introduces entirely new mathematical mechanics that borrowers must carefully model before enrolling: * Income Calculation: Unlike older plans that based payments on "discretionary income" (which shielded earnings up to a certain percentage of the federal poverty line), RAP calculates payments directly based on a borrower's Adjusted Gross Income (AGI) 2833343651. * Payment Tiers: Borrowers will pay between 1% and 10% of their AGI toward their loans each month, scaling with their income level, with a hard minimum payment of $10 per month 2228333537. * Dependent Deductions: To account for family size, RAP subtracts only a flat $50 per dependent child from the calculated monthly payment. This is generally far less generous to large families than the poverty-line exclusions utilized in older plans 2233343537. If a borrower is married and files taxes separately, their spouse's AGI and dependents are strictly excluded from the calculation 22. * No Maximum Payment Cap: In a massive departure from legacy IDR plans, RAP features no upper limit on monthly payments 222835. Under the old IBR plan, if a borrower's income skyrocketed, their required payment was legally capped at whatever the 10-year standard payment would have been. Under RAP, if a borrower's AGI spikes, their monthly payment will scale up indefinitely, meaning high earners could pay substantially more under RAP than under a standard amortization schedule 223553. * The Negative Amortization Shield: To counterbalance the lack of a payment cap, RAP introduces a powerful interest subsidy. If a borrower's required income-based payment is mathematically too small to cover the interest that accrued that month, the federal government pays the difference 225338. This guarantees that a borrower's total outstanding principal balance will never grow larger than the day they entered the program, completely eliminating the terrifying "runaway interest" scenario that trapped previous generations 2238.

The tradeoff for this interest subsidy is time. While legacy IDR plans offered total balance forgiveness after 20 or 25 years, RAP demands a grueling 30 years (360 qualifying months) of repayment before any remaining debt is canceled by the government 22283435515355.

The 2028 Transition Deadline for Legacy Borrowers

Borrowers who possess loans disbursed prior to July 1, 2026, are not immediately forced into RAP. They retain the right to utilize older, legacy IDR plans, most notably Income-Based Repayment (IBR) 22132233343655. Because IBR preserves a maximum payment cap and offers forgiveness in 20 to 25 years, it remains the most stable and legally protective path for existing borrowers 22333555.

However, the OBBBA mandates that the Department of Education completely phase out alternative legacy plans like PAYE and ICR 2232333436. Borrowers currently utilizing those plans, or borrowers exiting the defunct SAVE program, face a critical deadline. They must proactively switch their loans into IBR or a standard plan before July 1, 2028. Any borrower who fails to act before that date will be automatically swept into the new 30-year RAP system 2213223032333436.

| Feature | Legacy IBR (Loans Pre-July 2026) | New RAP (Loans On/After July 2026) |

|---|---|---|

| Payment Formula | 10% or 15% of discretionary income 335155 | 1% to 10% of Adjusted Gross Income (AGI) 22283351 |

| Maximum Payment Cap | Capped at 10-Year Standard amount 335153 | No cap. Payments scale indefinitely with income 22283553 |

| Interest Subsidy | Limited to first 3 years (subsidized loans only) 38 | 100% subsidy on unpaid interest; balance will never grow 2238 |

| Time to Forgiveness | 20 or 25 years 33355155 | 30 years (360 months) 222834355355 |

| Future Availability | Closed to new borrowing after July 2026. Transition deadline is July 2028. 22133334 | Mandatory for all new income-driven borrowers starting July 2026. 2213223334 |

The Return of the "IDR Tax Bomb" in 2026

For decades, borrowers targeting long-term debt forgiveness faced a terrifying caveat: the IRS viewed canceled debt as taxable income. During the pandemic, Congress temporarily neutralized this threat via the American Rescue Plan Act (ARPA) of 2021, which made all federal student loan forgiveness entirely tax-free at the federal level 55394041424344.

However, that vital borrower protection was always temporary. The ARPA provision officially expired on December 31, 2025, and lawmakers declined to extend it during the drafting of the OBBBA 554041424344.

Consequently, beginning January 1, 2026, any student loan balance forgiven under an Income-Driven Repayment plan (whether that is legacy IBR or the new RAP) will once again be treated by the IRS as taxable "cancellation of debt" income 30554041424344. Financial planners refer to this looming liability as the "IDR tax bomb" 4043.

The mechanics are severe: if a borrower reaches the end of their 25- or 30-year repayment term and has a $60,000 remaining balance discharged, the federal government essentially treats that event as if the borrower was handed a $60,000 cash bonus. The lender will issue an IRS Form 1099-C (Cancellation of Debt), and the borrower must report that $60,000 on their 1040 tax return 414344. Because the United States utilizes a progressive tax system, this phantom income is stacked on top of the borrower's actual salary, frequently pushing them into a much higher tax bracket and generating a massive, immediate federal tax bill - potentially costing thousands or tens of thousands of dollars in a single year 40414344.

Borrowers who established eligibility for forgiveness before the end of 2025 but whose paperwork was delayed will retain their tax-free status, provided they kept dated documentation 4041. For everyone else, advanced tax planning - such as increasing withholdings, making estimated payments, or setting aside dedicated savings - is now a mandatory component of utilizing an IDR plan 41.

The Exceptions: PSLF and Insolvency

There are two primary ways to escape the IDR tax bomb. First, borrowers who can mathematically prove to the IRS that they were functionally "insolvent" (meaning their total liabilities exceeded their total assets) at the exact moment the debt was canceled may qualify to have the tax burden waived 55.

More reliably, Public Service Loan Forgiveness (PSLF) remains entirely tax-free under federal law 55404142. Established by Congress in 2007, PSLF operates on a separate legal statute from standard IDR forgiveness 2340. Borrowers who make 120 qualifying monthly payments while employed full-time by a U.S. federal, state, local, or tribal government, or a qualifying 501(c)(3) nonprofit organization, will have their remaining balances discharged without generating a Form 1099-C or any subsequent tax liability 23554045. Additionally, specialized programs like Teacher Loan Forgiveness, which offers up to $17,500 in relief for educators in low-income schools, also remain tax-exempt 55.

Status of Broad Student Loan Forgiveness

Beyond the structured pathways of PSLF and IDR, the dream of broad, universal student loan forgiveness has effectively died in the courts. In 2022, the Biden-Harris administration announced a sweeping initiative to cancel $10,000 to $20,000 in federal student debt for borrowers earning under $125,000 annually 39636446.

However, following swift legal challenges, the U.S. Supreme Court explicitly struck down the one-time cancellation program in June 2023, ruling the executive branch lacked the authority to erase the debt without congressional approval 3964. While the administration subsequently attempted to implement relief through the aforementioned SAVE plan, that avenue has also been permanently blocked by the judiciary in 2026 303145. Moving forward, borrowers must assume that no broad, executive-ordered debt jubilee is coming. Erasing student loans in 2026 and beyond requires strict adherence to the 10-year PSLF track, surviving the 30-year RAP timeline, or aggressive, traditional principal repayment.

Bottom line

The 2026 higher education market requires borrowers to execute a level of strategic financial planning previously reserved for corporate accounting. Do not let published sticker prices deter applications, as robust institutional discounting has driven actual net tuition down significantly for most income brackets. However, relying on federal student loans to bridge the remaining gaps is no longer a simple endeavor; the OBBBA's strict lifetime borrowing caps, the elimination of Grad PLUS loans, and federal interest rates hovering between 6.5% and 9% mean families can no longer borrow their way out of expensive tuition choices. Legacy borrowers must proactively lock into legacy repayment plans like IBR before the 2028 transition deadline, while new borrowers must carefully model whether the negative amortization protections of the new 30-year RAP plan outweigh the return of the IRS tax bomb upon forgiveness.