5 Ways the Global Energy Transition Could Look by 2040

By 2040, the global energy transition will likely diverge into one of five distinct pathways: a sluggish baseline driven by current policies, a middle-road trajectory based on stated government pledges, an aggressive net-zero mobilization, a development-focused universal access surge, or a high-growth, fossil-fueled economic boom. The scenario that ultimately materializes will depend entirely on how swiftly nations can resolve severe bottlenecks in grid infrastructure, scale up long-duration energy storage, and redirect capital flows toward the Global South. These models provide critical insights into how investment decisions and policy frameworks implemented today will dictate global energy security and climate resilience over the next two decades.

Decoding the Models: Why Scenarios Matter

Energy transition scenarios are not crystal balls or definitive forecasts of the future. Rather, they are sophisticated, data-driven frameworks designed to explore the cascading consequences of different policy choices, technological breakthroughs, and macroeconomic investment flows 123. They provide a common, rigorous backdrop against which policymakers, grid operators, and institutional investors can evaluate the resilience of their long-term strategies and stress-test their assumptions about the future of global energy markets 12.

The global energy landscape is currently defined by sharp, unprecedented contradictions. On one hand, global investments in clean energy technologies, particularly solar photovoltaics (PV) and grid-scale battery storage, have reached record highs 45. Electrification spending is accelerating rapidly, with global investment in electricity grids and end-use electrification now outpacing capital expenditures in traditional oil and gas supply for the first time in history 36. On the other hand, the absolute global consumption of oil, natural gas, and coal has simultaneously reached record highs, driven by a post-pandemic economic rebound, surging energy demand in emerging markets, and the persistent rigidity of legacy fossil fuel infrastructure 3.

Furthermore, new geopolitical fractures, sustained inflation, and emerging supply chain vulnerabilities - particularly regarding critical minerals like copper, lithium, and rare earth elements - have elevated energy security from an environmental concern to a matter of acute national and economic security 378. The International Energy Agency (IEA) has noted that energy security tensions currently apply to more fuels and technologies simultaneously than at any point since the 1973 oil shock 7.

To untangle these complex variables and understand where the world will realistically be in 2040, analysts rely on two primary types of models: exploratory scenarios and normative scenarios 12. Exploratory scenarios track where current or stated policies will lead if left unchanged. Normative scenarios work backward from a specific, desired endpoint - such as limiting global warming to 1.5°C or achieving universal electricity access - to determine exactly what technological and financial milestones must be achieved by 2040 to make that future possible 13. The following five scenarios synthesize the leading integrated assessment models from the IEA's World Energy Outlook, the International Renewable Energy Agency's (IRENA) World Energy Transitions Outlook, and the Intergovernmental Panel on Climate Change's (IPCC) Shared Socioeconomic Pathways to outline the distinct futures available to the global economy.

Scenario 1: The "Current Policies" Baseline (A Sluggish Shift)

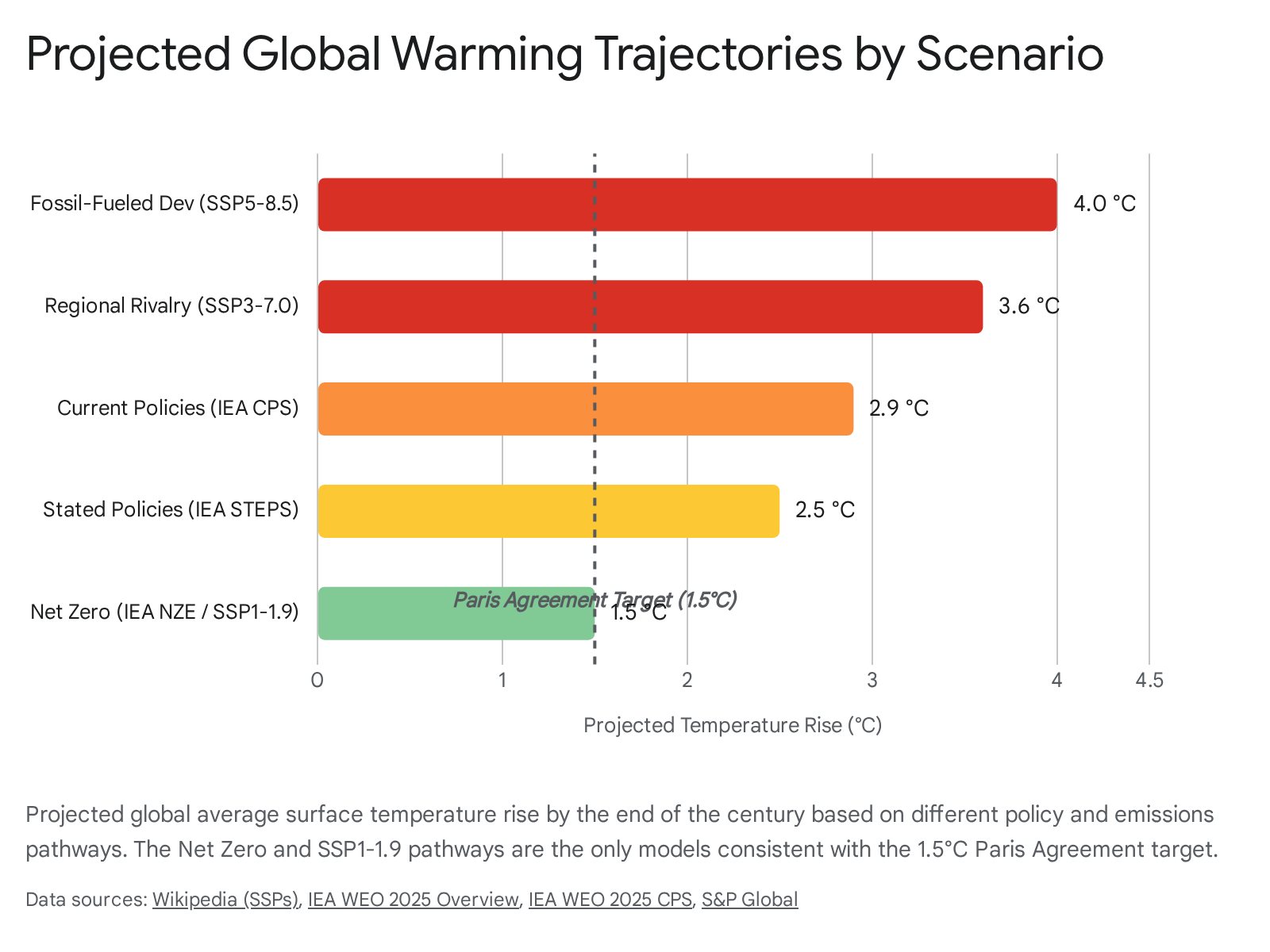

The first major scenario explores a world that proceeds entirely on the momentum of existing legislation, assuming no new governmental interventions, subsidies, or carbon taxes are enacted between now and 2040. Known formally as the Current Policies Scenario (CPS) by the IEA, and conceptually aligned with the IPCC's Shared Socioeconomic Pathway 3 (SSP3-7.0), this is an unmitigated baseline pathway 389. It is characterized by stubbornly high greenhouse gas emissions, a deeply entrenched reliance on fossil fuels, and a fragmentation of international climate cooperation in favor of domestic security priorities 91010.

The Energy Mix and Unyielding Fossil Fuel Dominance

In this baseline scenario, the global push for a fully electrified, zero-carbon energy system fails to gain broad, unified momentum. While total final energy consumption continues to rise by roughly 1.3% annually over the next decade - driven by global industrial output, expanding appliance ownership in developing nations, and rising demands for mobility - energy efficiency gains remain disappointingly modest 11.

Because nations focus heavily on domestic energy security and regional rivalry rather than collaborative environmental concerns, the transition from fossil fuels is severely delayed 912. Global demand for oil climbs steadily, defying peak-demand predictions to reach an estimated 113 to 114 million barrels per day (mb/d) by 2050 1114. This sustained, massive oil appetite is underpinned by the heavy road transport sector, aviation, and a booming petrochemical industry, particularly in emerging market and developing economies (EMDEs) where alternative feedstocks are unavailable or cost-prohibitive 11.

Similarly, natural gas demand surges in the CPS framework. Driven by rising supply needs in Asia and the Middle East, global natural gas consumption rises to 5,600 billion cubic meters by mid-century, met by expansive new liquefied natural gas (LNG) infrastructure and international pipeline networks from Russia to China 11.

While coal use is projected to eventually decline in China prior to 2030, this reduction is counterbalanced by increasing, robust coal consumption across India and Southeast Asia 1113. Consequently, coal remains the single largest source of global power generation well into the 2030s 11. By 2100, under the broader SSP3-7.0 socioeconomic assumptions, the total primary energy supply could grow to an immense 1,200 exajoules (EJ) per year, with the energy mix remaining fundamentally dominated by fossil fuels 10.

The Climate and Geopolitical Fallout

Under the CPS, the adoption of clean technologies stalls in regions that lack robust, sustained policy support. Outside of early-adopter markets like China and the European Union, the global share of electric vehicles (EVs) in total car sales plateaus at around 40% after 2035 311. Annual solar PV capacity additions stall at roughly 540 gigawatts (GW) leading up to 2035, largely because power grids remain underdeveloped, inflexible, and fundamentally incapable of handling further integration of variable renewable generation 311.

The environmental consequences of this sluggish transition are severe and compounding. Annual global energy-related carbon dioxide (CO2) emissions remain high, approaching 40 gigatonnes per year in the early 2030s and plateauing near that level through 2050 11. The total accumulation of greenhouse gases in this scenario sets the world on course for a global average surface temperature rise of roughly 2.9°C to 3.0°C by 2100 1114. Furthermore, the SSP3-7.0 socio-economic framework suggests that as temperatures rise, the associated physical climate damages - such as extreme weather events, agricultural disruptions, and coastal flooding - will severely hinder overall economic growth, human capital development, and global stability 91015.

Scenario 2: The "Stated Policies" Trajectory (The Middle Road)

The second scenario provides a more dynamic, optimistic reading of the current energy landscape. It assumes that governments will successfully implement all the energy, climate, and related industrial policies that have already been announced or put forward, even if those policies are not yet formally codified into strict legal mandates 1813. This middle-road pathway is captured by the IEA's Stated Policies Scenario (STEPS) and mirrors essential elements of IRENA's Planned Energy Scenario (PES) 81316.

Peak Fossil Fuels and Renewable Ascendance

The defining macroeconomic feature of the Stated Policies scenario by 2040 is that it marks the definitive peak and plateau of the global fossil fuel era. In this projection, aggregate global coal demand peaks before 2030 13. Oil demand levels off at approximately 102 mb/d around 2030 before beginning a slow, structural decline, heavily displaced by the rapid electrification of passenger transport 313. By 2035, over 840 million electric vehicles will be on the road globally, displacing roughly 10 mb/d of oil demand, predominantly concentrated in Asia and Europe 13.

Natural gas, long touted by industry advocates as a universal "bridge fuel" to a low-carbon future, sees a more complex trajectory. Driven by massive, ongoing expansions in LNG export capacity in the United States and Qatar, global gas demand continues to grow by nearly 1% annually into the 2030s 1314. The sheer volume of this incoming LNG supply is expected to put significant downward pressure on global gas prices, incentivizing continued use in industrial sectors and power generation before demand finally flattens out 14.

The combination of a peaking fossil fuel sector and the rapid scaling of clean energy means that, from the 2030s onward, renewables in aggregate will meet nearly all additional global energy demand 13. Under IRENA's PES modeling, the share of renewable energy in global power generation rises from roughly 28% in 2020 to 46% in 2030, eventually passing 70% by 2050 1718. The global electricity grid expands significantly to accommodate this shift, with electricity use rising four times faster than overall energy demand leading up to 2035 13.

The Implementation Gap and Lingering Climate Risk

Despite this rapid technological shift, the "Stated Policies" scenario ultimately falls short of international climate targets. Clean energy deployment, while highly impressive in absolute terms, remains unevenly distributed across geographic regions. Furthermore, emerging low-emission fuels like green hydrogen, liquid biofuels, and biogases struggle to capture significant market share without deeper, structural policy interventions and massive subsidies 13.

Consequently, while energy-sector CO2 emissions peak in the near term at just over 38 gigatonnes, their subsequent decline is too slow to meet the Paris Agreement goals 313. Emissions fall to approximately 35 Gt by the mid-2030s, keeping the world on a trajectory toward 2.4°C to 2.5°C of warming by 2100 1419. This scenario highlights a crucial, unavoidable reality for 2040: existing technological momentum and current government targets are sufficient to permanently disrupt legacy fossil fuel markets, but they are insufficiently ambitious to avert dangerous, irreversible climate change 818.

Scenario 3: The "Net Zero" 1.5°C Pathway (Rapid Decarbonization)

The Net Zero pathway is a strictly normative scenario. Rather than projecting forward based on current trends or policies, it establishes a firm, non-negotiable endpoint - achieving global net-zero CO2 emissions by 2050 and limiting warming to 1.5°C - and works backward to determine exactly what must happen by 2040 to make that reality possible 1310. Modeled comprehensively as the IEA's Net Zero Emissions by 2050 (NZE) Scenario, IRENA's 1.5°C Scenario, and the IPCC's SSP1-1.9, this represents the most ambitious, structurally disruptive, and capital-intensive pathway 122021.

Total System Transformation

Achieving the Net Zero scenario requires an almost total elimination of unabated fossil fuel consumption by mid-century 10. By 2040, the global energy mix will have undergone a radical, fundamental transformation. Under IRENA's 1.5°C Scenario, the share of renewable energy in total final energy consumption (TFEC) must surge to 91% by 2050, up from just 28% in 2020 1722. Overall, clean energy would account for 90% of total energy demand, with the remaining fossil fuels either fully abated through widespread carbon capture technologies or offset entirely by atmospheric carbon removals 23.

This aggressive pathway relies heavily on two foundational pillars: unprecedented energy efficiency improvements across all sectors and the massive, accelerated electrification of end-use sectors like heating, heavy industry, and transport 2024. Electricity becomes the undisputed predominant global energy carrier, growing by more than 50% by 2035 compared to today 317. To meet this surging demand, power generation must increase more than threefold, driven almost entirely by low-emission sources 17.

The Capital and Infrastructure Mandate

The primary barrier to realizing the 1.5°C scenario is not technological feasibility, but rather the sheer speed of execution and the mobilization of astronomical capital flows. IRENA estimates that keeping the 1.5°C target alive requires tripling global renewable power capacity to over 11,000 GW by 2030 521. This undertaking requires cumulative investments in renewable power generation, grid flexibility, and energy efficiency totaling an astounding $31.5 trillion between 2024 and 2030 alone 2125. Across the broader economy, cumulative clean energy and infrastructure investments could reach $60 trillion by 2050 10.

Under the Net Zero pathway, global warming is projected to peak slightly above 1.5°C (reaching roughly 1.65°C) around 2040 or 2050, before slowly declining as active CO2 removal measures successfully scale up 114. However, as the IEA and IRENA continuously caution in their latest reports, the world is currently far off track from achieving this scenario 5621. Delayed policy action and sluggish deployment in the early 2020s have resulted in higher peak warming estimates, meaning that staying within the remaining carbon budget will now require increasingly steep, potentially economically disruptive emissions cuts in the 2030s 136.

Scenario 4: The "Universal Access" Scenario (The Global South Surge)

Historically, mainstream energy transition scenarios have been critiqued for focusing predominantly on the rapid decarbonization of wealthy, high-emitting Western nations, while sidelining the critical development needs of emerging economies. The fourth scenario specifically addresses this developmental deficit in the Global South. Modeled uniquely in the IEA's newly introduced Accelerating Clean Cooking and Electricity Services Scenario (ACCESS), this normative pathway illustrates the precise energy shifts required to achieve universal access to electricity by 2035 and universal clean cooking by 2040 1626.

The Scale of the Inequality Challenge

Today, the global energy system is defined by stark, persistent inequalities. Modern end-use energy consumption per capita in the United States routinely ranges from 154 to 194 gigajoules (GJ), while in Africa, it languishes at a mere 10 to 13 GJ per capita 27. Approximately 730 million people currently live without basic electricity access, and nearly 2 billion continue to rely on unsafe, polluting biomass, wood, and charcoal for daily cooking needs 61426.

In the ACCESS scenario, the center of gravity for global energy demand shifts decidedly away from the West and toward India, Southeast Asia, and Sub-Saharan Africa 1428. As urbanization, industrialization, and digital infrastructure rapidly expand, emerging markets witness an unprecedented surge in electricity demand 626. In India, for example, energy demand is projected to increase dramatically, overtaking the European Union to become the world's third-largest energy consumer by 2030 29. Concurrently, however, solar power is projected to witness exponential growth, potentially matching or exceeding coal's historically dominant share in India's power generation mix by 2040 29.

Leapfrogging via Distributed Renewables and Targeted Finance

Achieving universal access by 2040 does not entail repeating the centralized, fossil-heavy grid development model utilized by the West in the 20th century. Instead, the ACCESS pathway relies heavily on "leapfrogging" technologies, specifically decentralized renewable energy - such as solar microgrids - and the strategic expansion of liquid petroleum gas (LPG) as a highly effective transitional clean cooking fuel 36. Africa possesses immense, largely untapped renewable potential; detailed geographic research indicates that 76% of Africa's total electricity needs could be met entirely by renewables by 2040, predominantly through a mix of hydropower and high-irradiance solar PV 630.

However, unlocking this optimistic scenario requires a fundamental, structural realignment of global development finance. Currently, Sub-Saharan Africa is home to roughly 20% of the global population and the vast majority of those without electricity, yet the region receives a disproportionately low 2% of global clean energy investment 26. Public and development finance for African energy projects has actually fallen by approximately one-third over the past decade 4. The IEA estimates that bridging this gap and achieving the ACCESS goals will require a dedicated, sustained annual investment of $15 billion specifically targeted at universal electricity access in Africa 26. If this capital is successfully unlocked, the ACCESS scenario presents a 2040 where rapid socio-economic development and poverty alleviation are achieved without triggering a commensurate explosion in global carbon emissions.

Scenario 5: The "Fossil-Fueled Development" Pathway (High Growth)

The final prominent scenario, modeled comprehensively by the IPCC as Shared Socioeconomic Pathway 5 (SSP5-8.5), is a "high-challenge" baseline known as "Taking the Highway" or "Fossil-Fueled Development" 915. Unlike the fragmented, slow-growth world depicted in the SSP3-7.0 regional rivalry baseline, this scenario features highly integrated global markets, rapid technological progress, and robust investments in human capital and education. However, this global economic super-cycle is powered almost exclusively by the aggressive, unmitigated exploitation of abundant fossil fuel resources 910.

High Growth, Extreme Vulnerability

In the SSP5-8.5 scenario, the global economy embraces highly energy-intensive, materially consumptive lifestyles. While innovation yields vast improvements in health, education, and raw GDP growth, it is fundamentally decoupled from environmental sustainability. Global CO2 emissions are projected to triple by 2075 under this pathway, resulting in a staggering estimated temperature increase of 2.4°C by the 2041 - 2060 period alone, and pushing well past 4.0°C by the end of the century 910.

This scenario represents a dangerous, potentially terminal paradox for 2040: human society will appear incredibly wealthy and technologically advanced on paper, but it will be highly exposed to catastrophic, compounding physical climate risks. S&P Global estimates that unmitigated, high-emission climate trajectories could result in up to $25 trillion in direct climate-related physical impacts 10. By 2040, the increasing frequency of extreme weather events, accelerating sea-level rise, and unlivable heat waves would begin to structurally undermine the very economic growth and infrastructure that fossil fuel exploitation initially generated 15. Due to the sheer scale of emissions and the resulting catastrophic radiative forcing, climate scientists generally regard SSP5-8.5 as an absolute worst-case baseline, demonstrating the severe perils of prioritizing short-term economic output over long-term planetary stability 931.

Scenario Comparison Matrix

The following table summarizes the key metrics, milestones, and projected climate outcomes of the five major transition scenarios projected for 2040 and beyond.

| Scenario Archetype | Primary Models | Baseline Narrative | Projected Warming by 2100 | Key 2040/2050 Energy Milestones |

|---|---|---|---|---|

| 1. Current Policies | IEA CPS, IPCC SSP3-7.0 |

Stagnant climate action; high geopolitical rivalry; continued heavy fossil fuel dependence. | ~2.9°C - 3.6°C | Oil demand reaches 113 mb/d; global EV adoption plateaus at 40%; coal remains dominant. |

| 2. Stated Policies | IEA STEPS, IRENA PES |

Moderate transition; existing pledges implemented; renewables grow but fossil fuels plateau. | ~2.4°C - 2.5°C | Oil peaks around 2030; EVs hit 50% market share by 2035; renewables cross 70% in power sector. |

| 3. Net Zero 1.5°C | IEA NZE, IRENA 1.5°C |

Aggressive decarbonization; massive clean energy investment; rapid, mandated fossil phase-out. | ~1.5°C | Clean energy meets 90% of total demand; immense grid modernization; $60T total investment. |

| 4. Universal Access | IEA ACCESS | Focus on socio-economic development in the Global South via decentralized renewables. | Variable (aligns with mitigation efforts) | Universal electricity by 2035; universal clean cooking by 2040; $15B/yr deployed in Africa. |

| 5. Fossil-Fueled Dev. | IPCC SSP5-8.5 | Unprecedented economic growth driven entirely by unmitigated fossil fuel exploitation. | ~4.0°C+ | CO2 emissions triple by 2075; extreme physical climate damages counteract economic gains. |

Critical Bottlenecks to 2040: The Grid Infrastructure Crisis

Regardless of which scenario ultimately unfolds, the journey to 2040 faces several severe, systemic physical bottlenecks. The energy transition is no longer merely a question of generating clean power; it is fundamentally a logistics challenge concerning transmission, storage, and material supply chains.

The 80-Million-Kilometer Problem

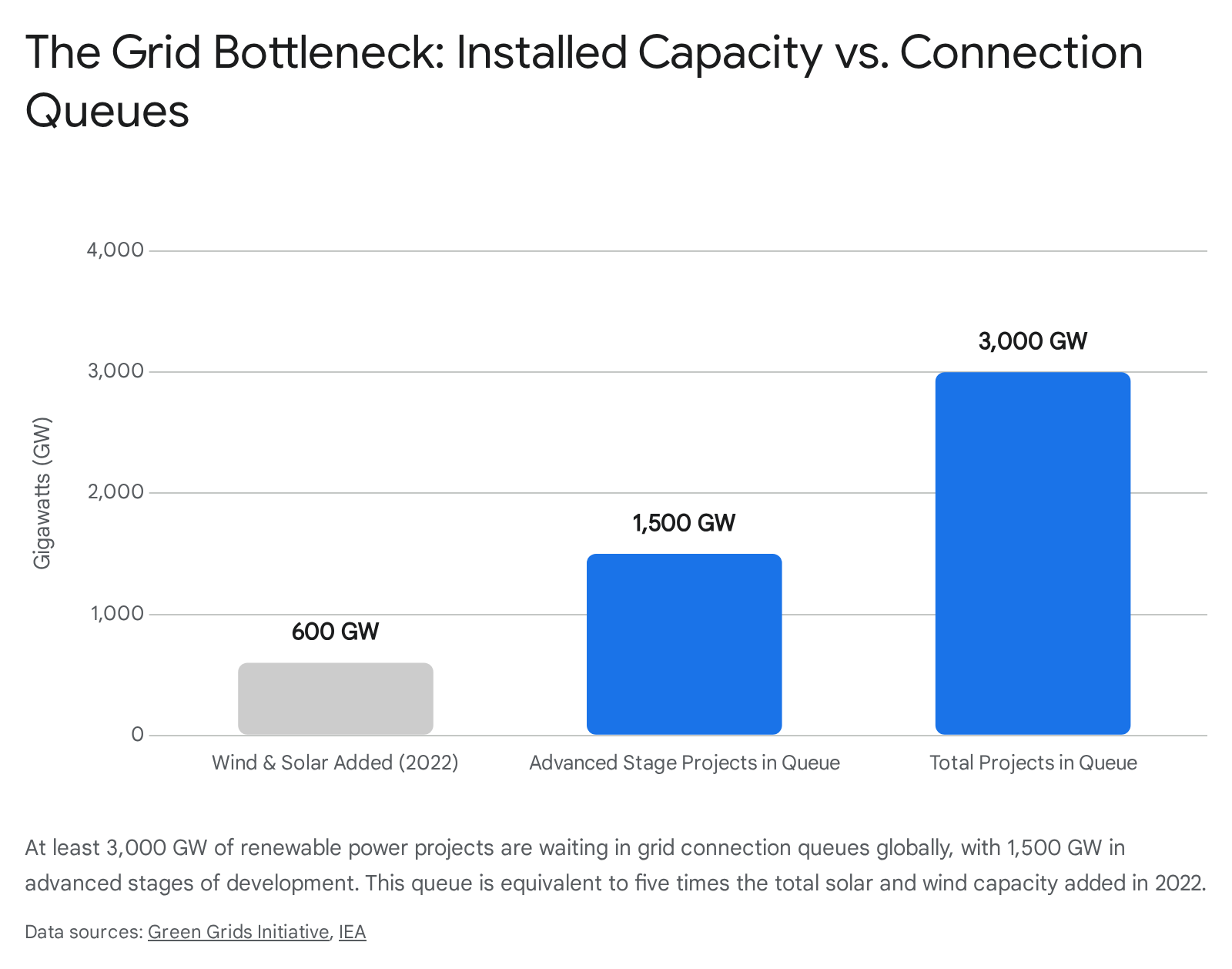

The most critical physical barrier to the 2040 energy transition is the global electricity grid. For more than a century, power grids were designed and optimized to transmit stable, centralized fossil-fuel power to end-users 3233. Today, they must be completely re-architected to handle decentralized, intermittent power flowing from thousands of dispersed wind and solar farms.

The IEA has bluntly warned that "grids risk becoming the weak link of clean energy transitions" 3334. Across the globe, there are currently at least 3,000 GW of renewable power projects waiting in grid connection queues - a massive backlog equivalent to five times the total amount of solar and wind capacity added worldwide in 2022 3234. Of these queued projects, 1,500 GW are in advanced stages of development but remain paralyzed by a lack of transmission capacity 3234.

Connecting these projects and meeting national climate goals will require adding or refurbishing an estimated 80 million kilometers of power lines by 2040. To put this in perspective, this is the equivalent of rebuilding the entire existing global power grid from scratch within a single generation 323335.

The Cost of Grid Delays

Delays in grid investment are actively threatening the Net Zero scenario. The IEA modeled a "Grid Delay Case" to explore the impacts of limited investment and slow modernization. The results indicate that stalled grid deployments would substantially increase reliance on fossil fuels, adding 58 gigatonnes of cumulative CO2 emissions from the power sector by 2050 - equivalent to the total global power sector CO2 emissions from the past four years combined 34.

To succeed, annual global investment in power grids must nearly double from current stagnant levels to over $600 billion per year by 2030, with a heavy emphasis on digitalizing distribution grids to handle variable loads and expanding grid interconnections across borders 3233. Furthermore, grid expansion is highly material-intensive. Meeting these targets will require over double the annual copper and aluminum supply relative to 2021 levels, placing immense strain on global mining supply chains and escalating geopolitical competition for critical minerals 836. Grids must also be fortified against an increasing array of non-traditional threats, including a recent tripling in cyberattacks against utility infrastructure and the rising severity of extreme weather events that have impacted hundreds of millions of families 839.

Critical Bottlenecks to 2040: Long-Duration Energy Storage (LDES)

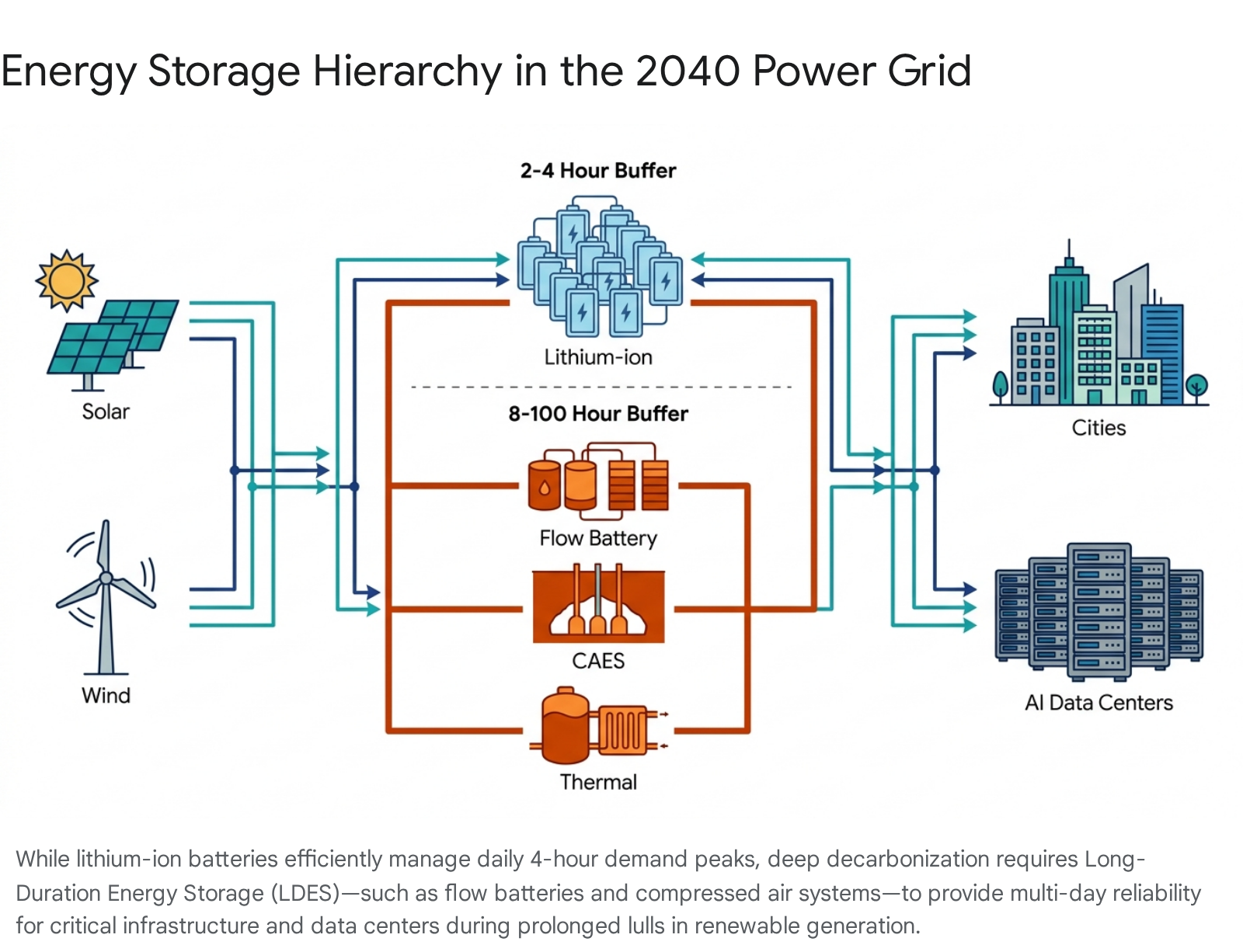

Because wind and solar power are inherently intermittent - generating electricity only when the wind blows or the sun shines - the grid of 2040 requires massive reservoirs of stored energy to maintain frequency regulation and prevent catastrophic blackouts. The global grid-scale energy storage market is expanding rapidly, projected to grow at a 30.9% compound annual growth rate (CAGR), surging from $7.51 billion in 2024 to $28.73 billion by 2029 4037.

Currently, the market is dominated by lithium-ion battery energy storage systems (BESS). Lithium-ion is highly efficient, modular, and currently cost-effective for short-duration storage, typically acting as a 2-to-4-hour buffer to smooth out daily supply fluctuations (e.g., absorbing excess solar power at noon and discharging it into the grid during the evening demand peak) 37383940.

However, deep decarbonization requires power grids to survive multi-day lulls in renewable generation, severe winter storms, and the continuous, 24/7 power demands of industrial facilities and artificial intelligence (AI) data centers. The power demands from data centers alone are forecast to increase by 50% by 2026, representing a massive strain on grid reliability 34142.

This necessitates Long-Duration Energy Storage (LDES) - systems capable of discharging power competitively for 8, 24, or even 100 hours 404247. Because scaling lithium-ion for multi-day storage is prohibitively expensive, the industry is racing to commercialize alternative, heavy-duty chemistries and mechanical systems. By 2040, a resilient grid will likely rely on a hybrid ecosystem including several emerging technologies.

LDES Technologies Shaping the 2040 Grid

To understand how the grid will stabilize variable renewables, it is necessary to examine the specific LDES technologies competing for market share.

| Storage Technology | Mechanism & Chemistry | Grid Duration | Current Commercial Status & Challenges |

|---|---|---|---|

| Lithium-ion BESS | Electrochemical cells using lithium, nickel, manganese, and cobalt. | 2 - 4 hours | Dominant. Highly scalable and bankable, but cost-prohibitive for multi-day storage. 373940 |

| Flow Batteries | Liquid electrolytes (iron, zinc, vanadium) pumped through a membrane. | 8 - 24+ hours | Emerging. Decouples power from capacity. Scaling up, but lacks the mature economies of scale of lithium-ion. 404748 |

| Compressed Air (CAES) | Compresses air into underground geological caverns; releases to turn turbines. | 12 - 24+ hours | Proven but Constrained. Offers lowest levelized cost at scale, but entirely dependent on suitable underground geology. 4037 |

| Thermal / Gravity | Heats molten salts or lifts heavy weights using excess power; releases kinetically. | 8 - 16 hours | Pilot Stage. Can leverage existing infrastructure (e.g., retired mine shafts), but round-trip efficiency requires optimization. 4037 |

Despite the promise of alternative chemistries, lithium-ion's massive manufacturing scale currently gives it a persistent edge even in the 8-to-12-hour inter-day market, where it accounts for 70% of planned projects targeting operations by 2030 40. Unseating lithium-ion for true multi-day storage will require robust policy support - such as the UK's cap-and-floor subsidy scheme for LDES - to provide revenue guarantees and derisk early-stage commercial deployments 4048.

Critical Bottlenecks to 2040: The Transport Sector Transition

The final major variable dictating the 2040 energy mix is the speed at which the global transportation fleet electrifies. Across all IEA scenarios, oil demand from passenger vehicles faces intense downward pressure as alternatives scale 313. At the COP26 climate summit, more than 30 nations - alongside major automakers like Ford, General Motors, and Volvo - signed declarations committing to transition to 100% zero-emission new car and van sales globally by 2040, and by no later than 2035 in leading markets 43.

Diverging Regional Strategies

However, the path to 2040 is becoming increasingly fragmented by regional economics, consumer behavior, and divergent industrial policies. In China, battery electric vehicles (BEVs) and plug-in hybrids are surging past 50% market share, driven by aggressive industrial policy, deep domestic battery supply chains, and highly affordable models 5051.

In contrast, the United States has seen near-term growth momentum slow in 2026 due to persistent charging infrastructure anxiety, political uncertainty regarding federal EV mandates, high interest rates, and consumer preferences for larger, range-heavy vehicles 52. In response, the IEA revised down its EV growth projections for advanced economies in its latest STEPS modeling 3.

Meanwhile, Japan is pioneering a distinctly alternative strategy. With the lowest BEV uptake among advanced economies, Japanese automakers (like Toyota and Honda) are heavily prioritizing hybrid electric vehicles (HEVs) 51. This strategy is designed to mitigate supply chain risks associated with raw battery minerals and leverage existing fueling infrastructure, though it fundamentally relies on a much slower, prolonged phase-out of internal combustion engines, putting it at odds with aggressive Net Zero pathways 51.

Despite these near-term market frictions and policy divergences, industry analysts forecast that the long-term macroeconomic trend is highly resilient. Global EVs are broadly expected to account for roughly 80% of all global vehicle sales by 2040, fundamentally severing the passenger transport sector's century-long reliance on petroleum 5052.

Bottom line

By 2040, the global energy transition will not be a singular, uniform event, but rather a complex spectrum of outcomes defined by infrastructure execution, capital allocation, and political will. While technological momentum and shifting market economics have effectively guaranteed the end of the unabated fossil-fuel growth era, current trajectory models - like the Stated Policies Scenario - still project a dangerous 2.5°C of global warming. Achieving a stabilized, net-zero future requires immediate, unprecedented global capital deployment to unblock 80 million kilometers of grid transmission queues, successfully commercialize non-lithium long-duration energy storage, and aggressively finance clean energy infrastructure in the Global South.