How Colleges Build Your Financial Aid Package

When a college financial aid office builds your package, administrators follow a highly regulated, step-by-step sequence to bridge the gap between the school's cost and your family's ability to pay. They act as financial architects, starting with foundational federal grants, layering on state and institutional funds, and finally adding work-study and student loans to meet your demonstrated need. Because most colleges operate with limited budgets, however, the resulting package often leaves a financial gap that families must ultimately cover out of pocket.

The Financial Aid Formula: Calculating Your Need

Before a single dollar is awarded, the financial aid office must determine exactly how much assistance you legally qualify to receive. This process, traditionally known in higher education administration as "packaging," is designed to ensure that need-based aid does not exceed your actual financial need, and that your total financial assistance does not exceed the school's total cost of attendance 1.

To achieve this, administrators utilize a standard federal equation: Cost of Attendance (COA) - Student Aid Index (SAI) - Other Financial Assistance (OFA) = Financial Need 12.

Understanding the components of this formula is critical to understanding how decisions are made behind the closed doors of the financial aid office:

- Cost of Attendance (COA): This is the school's full sticker price for the academic year. It includes direct costs that you pay to the university (such as tuition, mandatory fees, on-campus housing, and meal plans) as well as estimated indirect costs (such as textbooks, supplies, transportation, and personal daily expenses) 34. Because COA includes these indirect lifestyle costs, the total figure is often significantly higher than the actual bill you receive from the bursar's office.

- Student Aid Index (SAI): This is a federal index number calculated from the tax and demographic data you submit on your financial aid application. The SAI represents a baseline measurement of your family's financial strength 25.

- Other Financial Assistance (OFA): This includes outside funding you bring to the table before the school builds its package, such as private scholarships, community foundation grants, or employer tuition assistance 1.

If a university has a Cost of Attendance of $50,000 and your Student Aid Index is 15,000, your demonstrated financial need is $35,000. The financial aid office's primary objective is to build a package of grants, work-study, and subsidized loans that meets as much of that $35,000 as possible, without exceeding it 16.

The Shift from EFC to the Student Aid Index (SAI)

For decades, the financial aid system relied on a metric called the Expected Family Contribution (EFC). However, following the passage of the FAFSA Simplification Act, the Department of Education overhauled the application process for the 2024 - 2025 academic year, officially replacing the EFC with the Student Aid Index (SAI) 256.

This was not merely a name change; it fundamentally altered how financial aid offices calculate need and package awards. The new formula introduced several major shifts that administrative software systems had to accommodate:

The Introduction of the Negative SAI

Under the old system, the EFC could never drop below zero. The new SAI, however, can drop as low as -1,500 25. This negative number was designed to give financial aid administrators a clearer, more nuanced picture of the nation's lowest-income students. Theoretically, this allows schools to identify and prioritize their most vulnerable applicants for limited institutional funds or specialized state grants 7.

However, the Department of Education instituted a strict rule for how this negative number is processed in the administrative workflow. When packaging federal need-based aid - such as Federal Supplemental Educational Opportunity Grants (FSEOG) or Federal Work-Study - aid offices are legally required to convert any negative SAI to a zero 12. A negative SAI does not artificially increase a student's eligibility for non-need-based aid, nor does it allow the school to award federal aid that exceeds the student's Cost of Attendance 27.

Elimination of the Sibling Discount

One of the most consequential changes for middle-class families was the elimination of the "sibling discount" in the federal need analysis 589. Previously, if a family had multiple children enrolled in college at the same time, the federal formula divided the parents' expected contribution by the number of enrolled students, significantly increasing each child's aid eligibility 911.

Under the new SAI rules, the number of family members in college is no longer a factor in the standard federal calculation 2. Consequently, families with two or more enrolled students may see their SAI skyrocket compared to their old EFC, reducing their eligibility for federal, state, and institutional need-based aid 6911. Financial aid officers anticipate an ongoing surge in appeals from families negatively impacted by this specific change 9.

Inclusion of Small Businesses and Family Farms

The FAFSA Simplification Act also altered which assets are protected. Previously, families who owned small businesses (with fewer than 100 employees) or family farms that served as their primary residence could exclude the net worth of those assets from the FAFSA 811. The new regulations eliminate this exclusion. The net worth of these businesses and farms must now be reported as assets, which raises the family's SAI and subsequently reduces their calculated financial need 611.

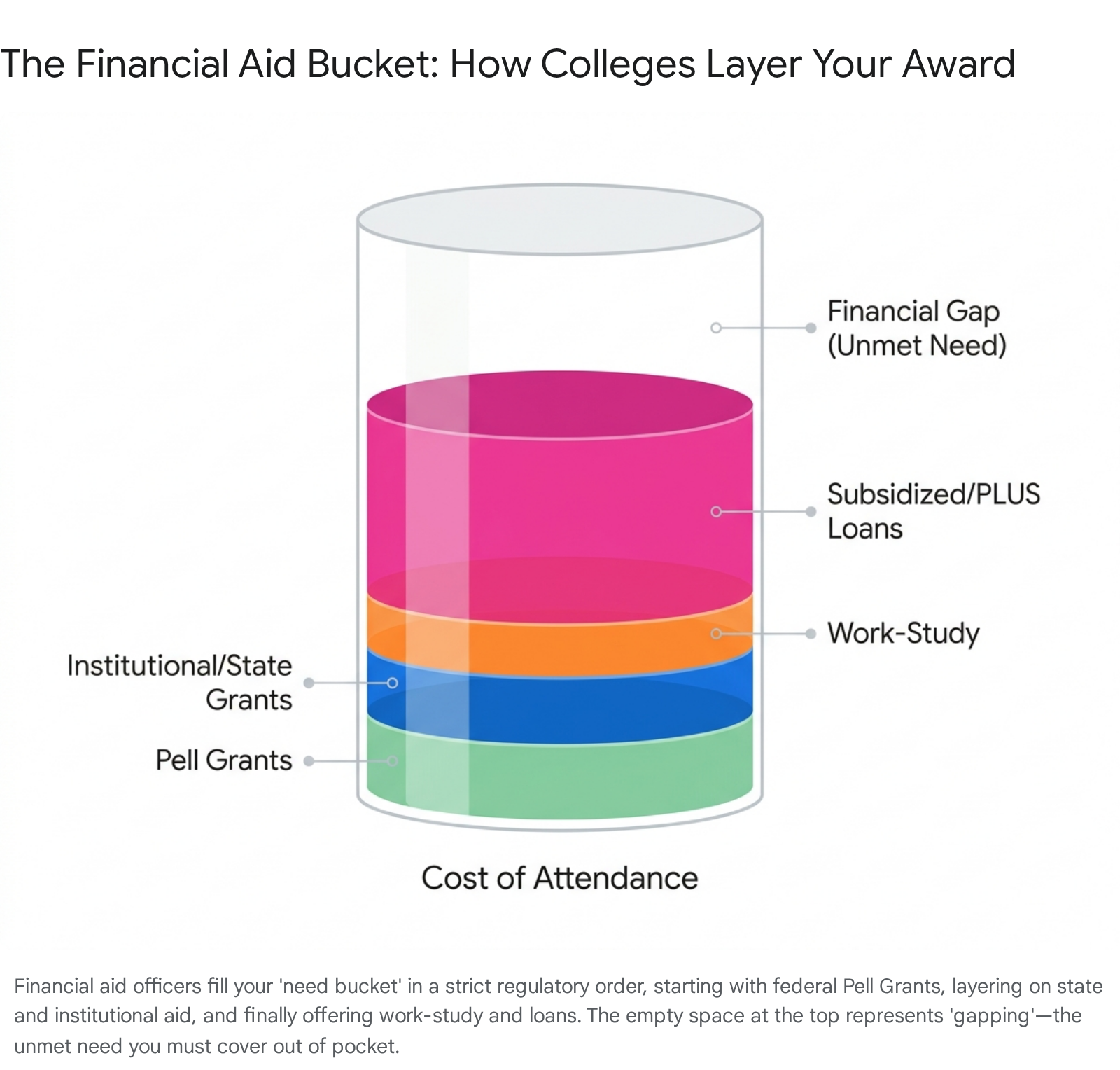

The "Bucket Filling" Administrative Workflow

Financial aid professionals frequently rely on the metaphor of "bucket filling" to explain the complex administrative process of building an award package 1011.

Once you submit your application, the federal processor generates an Institutional Student Information Record (ISIR) and sends it to the colleges you listed. When a college's financial aid office receives your ISIR, it is loaded into the school's Student Information System (SIS) - software platforms like Banner, EDExpress, or specialized commercial vendors 1012.

These software systems are configured to automate the packaging process based on the school's unique financial philosophy, but they must fill your financial "bucket" in a strict, federally mandated hierarchical sequence 101213.

Step 1: Federal Pell Grants (The Foundation)

Pell Grants are always considered the first source of aid in a student's package 110. Because the Federal Pell Grant is an entitlement program - meaning the federal government guarantees the funds for any eligible low-income student - the school does not have to worry about depleting a finite budget.

The financial aid software automatically determines Pell eligibility by comparing the student's SAI, household size, and the federal poverty guidelines 126. Before finalizing this foundational layer, the software pings the federal Common Origination and Disbursement (COD) system to ensure the student has not exceeded their Lifetime Eligibility Used (LEU) limit, which is currently capped at 600% (the equivalent of six years of full-time funding) 114.

Step 2: State and Institutional Grants (The Next Layer)

Once the Pell Grant is applied, the software calculates the remaining unmet need. If the college possesses its own institutional grant money or administers state-funded grants, these funds are added next 1015.

This is where institutional philosophy dictates the software's behavior. Because institutional funds are finite, administrators must program their systems to distribute money strategically. Some schools choose to give a higher proportion of grant assistance to beginning freshmen, who may face steeper hurdles adjusting to campus life, while increasing the proportion of loans in subsequent years 10. Other schools distribute funds as an equal percentage of every eligible student's need, or they prioritize early applicants on a first-come, first-served basis 110.

Step 3: Campus-Based Aid (FSEOG and Work-Study)

After institutional grants are applied, the office looks to "Campus-Based" federal aid, which primarily includes the Federal Supplemental Educational Opportunity Grant (FSEOG) and Federal Work-Study (FWS) 12.

Unlike Pell Grants, Campus-Based aid is severely limited. The Department of Education gives each college a fixed annual allocation for these programs. Once the school's budget is exhausted, no more awards can be made, even to highly eligible students 1018. Federal rules dictate that schools must include a student's estimated Pell Grant eligibility as part of their Other Financial Assistance (OFA) before they can calculate eligibility for Campus-Based awards 1.

It is crucial to understand how Federal Work-Study functions administratively. If a financial aid office awards you $3,000 in work-study, that amount reduces your official unmet need on paper 1920. However, that $3,000 is not credited to your bursar's account to pay your upfront tuition bill. Instead, you must secure an eligible job (on or off campus), work the hours, and earn the money via a standard paycheck throughout the semester to help cover your indirect costs like textbooks and living expenses 111920. If you do not work the hours, you do not receive the money.

Step 4: Federal Direct Subsidized Loans

If a student still exhibits unmet need after all grants and work-study have been exhausted, the financial aid office will offer a Federal Direct Subsidized Loan 1. For these need-based loans, the federal government pays the accruing interest while the student is enrolled in school at least half-time.

Because subsidized loans represent a superior borrowing option, federal packaging rules require that a financial aid administrator must evaluate eligibility for Campus-Based funds and originate any eligible Direct Subsidized Loans before they can offer a student an Unsubsidized Loan 1.

Step 5: Non-Need-Based Aid (Filling the Rest of the COA)

Once a student's purely "need-based" eligibility is met (or if a high-income student had no need to begin with), the financial aid office will offer non-need-based aid to help the family cover their Student Aid Index. This layer primarily consists of Federal Direct Unsubsidized Loans and Parent PLUS Loans, as well as specialized programs like the TEACH Grant 1.

Eligibility for non-need-based aid is simply calculated by subtracting any Other Financial Assistance (including the need-based aid already awarded) from the total Cost of Attendance 1. While any eligible student can qualify for an Unsubsidized Loan regardless of their family's income or SAI, the critical difference is that interest begins accruing on these loans the moment the funds are disbursed to the school 16.

Navigating Regulatory Compliance and Overawards

Financial aid administrators are heavily audited to ensure compliance with Title IV federal regulations. One of the most complex daily tasks in a financial aid office is preventing and resolving "overawards."

The golden rule of financial aid packaging is twofold: 1. A student's need-based aid cannot exceed their demonstrated financial need. 2. A student's total financial assistance (including loans) cannot exceed their Cost of Attendance 110.

An overaward typically occurs when a student secures an outside scholarship (like a $5,000 award from a local rotary club or employer) and reports it to the school after their financial aid package has already been built 11017.

If you bring a $5,000 private scholarship to a package that is already fully meeting your financial need, the financial aid office cannot simply stack the new money on top of your existing awards. By federal law, they are required to adjust your package downward to eliminate the $5,000 overaward 110.

Typically, administrators will reduce your self-help aid first, canceling your work-study allotment or reducing your federal student loans 16. This is highly beneficial to the student. However, if your need was already being met entirely by institutional grants, the school may be forced to reduce your institutional grant money to make room for the outside scholarship in your budget 1618. In this scenario, your hard-won private scholarship essentially subsidizes the university's budget rather than lowering your out-of-pocket costs.

Federal vs. Institutional Methodology

When calculating your need, not all colleges view your family's financial reality through the same lens. The administrative software used by financial aid offices generally operates on one of two distinct mathematical formulas: the Federal Methodology (FM) or the Institutional Methodology (IM) 2419.

Public universities and the vast majority of private colleges rely solely on the data submitted via the FAFSA, utilizing the Federal Methodology. This formula, strictly standardized by Congress, takes a relatively straightforward approach, focusing primarily on the income of the custodial parent(s) and specific liquid assets 1920.

However, roughly 250 highly selective private institutions - along with certain competitive scholarship programs - require applicants to submit a secondary application called the CSS Profile, which utilizes the Institutional Methodology 241920. Administered by the College Board, the IM gives financial aid officers much wider latitude to dig into a family's underlying financial strength before they award their own highly valuable institutional endowment funds 19.

Comparing Financial Aid Formulas

The differences between the two methodologies can result in a family receiving a vastly different calculation of their ability to pay depending on which forms a college requires 2721.

| Financial Component | FAFSA (Federal Methodology) | CSS Profile (Institutional Methodology) |

|---|---|---|

| Primary Users | All institutions receiving federal aid (public and private) 1921. | Approximately 250 selective, private colleges with large endowments 1921. |

| Home Equity | Completely ignored. The primary residence is not counted as a liquid asset 2421. | Counted as an asset. Often capped by the institution at 2 to 3 times the family's annual income 242021. |

| Non-Custodial Parent | Ignored. Only the parent providing the most financial support files the form 111920. | Counted. Most IM schools require a separate application and financial disclosure from the non-custodial parent 1920. |

| Paper Financial Losses | Counted. Depreciation, capital losses, and business losses lower the family's adjusted income 2420. | Ignored. Financial aid administrators add these "paper losses" back into the family's available income pool 2420. |

| Small Family Businesses | Counted as an asset (newly implemented under FAFSA simplification) 61120. | Counted as an asset, often scrutinized more deeply for retained earnings and equity 2029. |

| Cost to Apply | Free to complete and submit 21. | $25 initial fee, plus $16 per additional school (fee waivers automatically granted for low-income students) 1921. |

Because the Institutional Methodology captures heavy assets like home equity and forces the inclusion of non-custodial parent income in cases of divorce, middle-class and upper-middle-class families often find that their calculated need under the CSS Profile is significantly lower than their federal FAFSA index 1927.

However, there is a strategic caveat: if an institution uses the CSS Profile to award its own money, but the Federal Methodology generates a higher SAI for a specific student, some colleges are known to "anchor" their award to the less generous federal number, requiring savvy families to actively request that the school honor their own Institutional Methodology 30.

Why Packages Fall Short: The Reality of "Gapping"

If your financial aid forms show that your family has $20,000 in demonstrated financial need, it is logical to expect an award package worth exactly $20,000. Unfortunately, higher education finance rarely works that way. If a university offers you a financial aid package that is less than your demonstrated need, you have been "gapped" 6313222.

Gapping is rarely a clerical error; it is a calculated mathematical reality of institutional budgets. The vast majority of colleges simply do not have the endowment funds required to meet 100% of the demonstrated need for every single student they accept 632. Therefore, financial aid offices and enrollment managers must strategically leverage their limited institutional grants to meet their enrollment goals.

Instead of spreading their money equally, schools often offer larger, gap-free aid packages to highly sought-after students - such as academic high-achievers or those with unique talents - using need-based aid as a de facto merit incentive 631. Meanwhile, average applicants who fall lower on the admissions priority list are offered admission but are given a package with a massive financial gap 631.

When you are gapped, the financial aid office has already maxed out your eligibility for federal student loans 3222. Therefore, families cannot rely on standard federal borrowing to bridge the divide. They must cover the gap through out-of-pocket cash, current student income, high-interest private student loans, or federal Parent PLUS loans 33222.

Public vs. Private College Packaging Priorities

Only a tiny fraction of the nation's colleges - roughly 80 elite institutions, including the Ivy League and highly selective liberal arts colleges like Amherst and Pomona - guarantee to meet 100% of demonstrated financial need for all admitted students 342324. Some of these institutions, possessing multi-billion-dollar endowments, even pledge to meet that full need without inserting student loans into the package 2324.

For instance, the "NYU Promise" guarantees that New York University will meet 100% of demonstrated need for all first-year undergraduates, additionally pledging that families with an income under $100,000 (and typical assets) will pay zero tuition 1618.

Beyond that elite tier, public and private colleges employ vastly different operational strategies when building aid packages:

| Feature | Public Universities | Private Universities |

|---|---|---|

| Funding Source | Rely heavily on state government appropriations and taxpayer subsidies to keep operational costs down 252639. | Rely primarily on tuition revenue, private donations, and institutional endowments 252639. |

| Sticker Price | Significantly lower, especially for in-state residents 2539. | Significantly higher, often double or triple the public in-state rate 3927. |

| Packaging Strategy | Relies on lower upfront tuition costs combined with federal aid and state-funded grants (like the Cal Grant or NY TAP) 2526. | Utilizes a high-tuition, high-discount model. Private schools offer massive institutional grants to offset their high prices (averaging a 52-56% "tuition discount" rate) 2741. |

| Average Net Cost | Generally the lowest option, though out-of-state public tuition can still result in severe gapping 3942. | Can frequently match or even beat public school net prices for specific students due to aggressive merit and need-based institutional grants 439. |

Behind the Scenes: Administrative Chaos in 2024-2025

Behind the polished award letters sent to students, the modern financial aid office is a labyrinth of compliance, data processing, and workflow management 12. In a normal operational year, the workflow is highly automated, minimizing the time between a student submitting a FAFSA and the software generating an award letter 1028.

However, the implementation of the FAFSA Simplification Act threw this administrative workflow into historic chaos during the 2024 - 2025 cycle 29. The new form, designed to be shorter and directly linked to IRS data, was delayed by months, launching in late December rather than the traditional October 1 timeline 62930. When applicant data finally began flowing to colleges, mathematical errors in the federal formula meant hundreds of thousands of records were incorrect, forcing the Department of Education to reprocess the data and further delaying financial aid offers nationwide 2930.

The Burden of Manual Keystroke Processing

The most severe operational blow to financial aid administrators was the suspension of "batch corrections." Normally, if a financial aid office needs to update FAFSA data for hundreds of students (due to verification or professional judgment appeals), administrators upload a single batch file via the Electronic Data Exchange (EDE) to update the federal system instantly 463148.

Due to ongoing technical failures, the Department of Education announced that batch processing functionality would not be available at all for the 2024 - 2025 cycle, pushing its release to the first quarter of 2025 463148.

This catastrophic software failure forced financial aid staff across the country to log into the federal portal and submit corrections manually, keystroke-by-keystroke, for thousands of individual student files 48. For administrative staff, this turned an automated process that normally takes minutes into weeks of grueling manual data entry, leading to acute burnout and severe processing delays 48.

A July 2025 survey conducted by the National Association of Student Financial Aid Administrators (NASFAA) found that 72% of institutions reported persistent processing delays due to federal system breakdowns 32. More alarmingly, the operational strain impacted actual enrollment, with 51% of institutions reporting heightened student confusion and some universities being forced to rescind work-study or grant awards due to processing errors 3233.

Appealing the Package: Professional Judgment and Negotiation

Because the FAFSA relies on tax data from the "prior-prior" year (for instance, using 2022 tax returns for the 2024 - 2025 school year), the financial snapshot it provides is often deeply outdated 3452. If the financial aid package generated by the office leaves you with an unmanageable gap, the initial offer is not necessarily final. You have the right to formally appeal.

When communicating with the office, financial aid administrators advise against using words like "negotiate," "bargain," or "haggle" 355455. Aid officers view their work as applying objective criteria governed by strict federal compliance, not haggling over a price 35. Instead, the office processes these requests through two main, formal avenues: Professional Judgment and Competitive Matching.

Professional Judgment (Special Circumstances)

The Higher Education Act of 1965 grants financial aid administrators the legal authority to exercise "Professional Judgment." This regulatory power allows an administrator to manually override specific data elements on a student's FAFSA to ensure the resulting SAI better reflects the family's current financial reality 343637.

A successful Professional Judgment review typically requires a severe, documented change in circumstances. Administrators will commonly approve appeals for: * Recent job loss, long-term unemployment, or significant reductions in work hours or overtime 353839. * The death, divorce, or legal separation of parents since the FAFSA was originally filed 353839. * Extraordinary, unreimbursed medical or dental expenses. (Offices usually require these out-of-pocket expenses to exceed a specific threshold, such as $3,000, before they will adjust the formula) 343839. * The sudden loss of untaxed income, such as the cessation of child support or Social Security benefits 3438.

To process this, the office requires a formal appeal letter accompanied by concrete, third-party evidence - such as employer termination letters, extensive medical receipts, or finalized divorce decrees 343538.

If the financial aid committee approves the appeal, they will execute a data review to lower your SAI, or they will execute a cost-of-attendance adjustment to increase your overall student budget 353637. Either action forces the software to generate a higher level of demonstrated financial need, allowing the school to offer more grants or subsidized loans. Crucially, Congress delegated this authority exclusively to the aid administrators; their decisions made via Professional Judgment are final and cannot be overridden by the university president or appealed to the U.S. Department of Education 343637.

Competitive Matching (Merit Appeals)

If your family has not experienced a severe financial hardship, you may still be able to secure more funding through a merit-based appeal. This strategy is highly effective at private universities that actively fight to protect their enrollment yields 6040.

If you receive a stronger financial aid offer from a comparable peer institution, you can share that competing award letter with the financial aid or admissions office 356040. Administrators are more likely to entertain a match if the competing school is a direct academic rival, and if the student's profile (GPA, test scores, or unique talents) makes them an attractive candidate 6040.

When submitting a competitive appeal, experts recommend structuring your communication precisely: open by expressing gratitude for the initial offer, state the exact dollar amount of the gap you need closed using the competing letter as proof, and explicitly confirm that you will commit to enrolling if the school can match the competing package 525440.

Bottom line

When a financial aid office builds your package, administrators execute a highly regulated, automated sequence that layers federal, state, and institutional funds to meet your calculated need. However, due to finite institutional budgets, the vast majority of students are still "gapped" and forced to find alternative funding to cover the true cost of attendance. While families have the right to appeal an insufficient package through a Professional Judgment review if their finances have drastically changed, the overall financial aid system remains heavily strained by recent federal software overhauls and manual processing delays that continue to challenge both administrators and applicants.