Merit vs. Need-Based Aid: What's the Difference

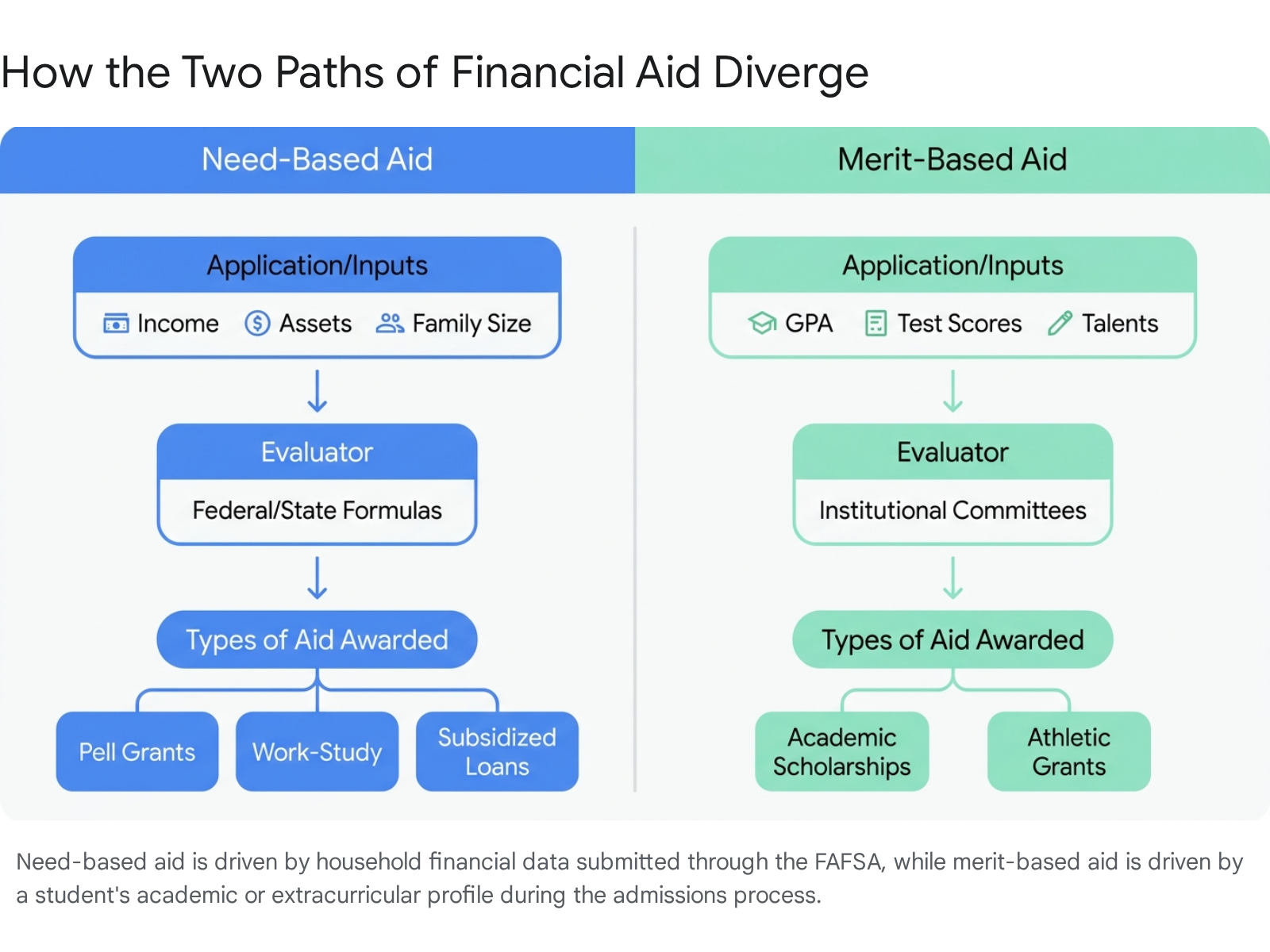

Need-based financial aid is awarded based on a family's calculated ability to pay for college, while merit-based aid rewards a student's academic, athletic, or artistic achievements regardless of household income. Most students combine both types of funding to cover the rising sticker price of higher education, utilizing federal and state grants alongside institutional scholarships to significantly reduce their out-of-pocket costs.

The Foundations of Financial Aid

Paying for a college education is rarely accomplished with a single check. Instead, higher education funding relies on a highly layered strategy drawing from four primary sources: the federal government, state governments, the colleges themselves, and private organizations 11. Navigating this complex landscape requires understanding the two fundamental philosophies that dictate how this money is distributed: need and merit.

Need-based financial aid is fundamentally designed to bridge the gap between what a family can reasonably afford and the actual cost of attendance 1. Its primary goal is educational equity, ensuring that students from low- and middle-income backgrounds have access to higher education 2. Eligibility is determined through a strict formulaic analysis of a family's income, assets, and household size, largely agnostic of the student's high school grades or extracurricular talents 123.

Merit-based financial aid, conversely, operates as both a reward system and an institutional enrollment strategy. It is granted primarily based on a student's personal accomplishments, such as academic excellence, athletic prowess, community leadership, or artistic talent 1. A student's financial background is entirely irrelevant to pure merit aid. Assuming that financial need is not a secondary condition of the specific scholarship, a student from a wealthy family with extensive assets is just as entitled to a merit-based academic award as a student with limited resources 2.

While need-based aid relies heavily on federal and state taxpayer funds, the vast majority of merit aid is distributed directly by the colleges and universities themselves. Institutions deploy these funds strategically to attract high-performing students who will improve the school's academic profile, ensure specific enrollment goals are met, or fill vital roles in campus organizations and athletic teams 47. For the modern college student, affordability usually requires stacking both types of aid; very few students cover their entire tuition bill with just one form of support 14.

The Mechanics of Need-Based Aid

The universal gateway to need-based financial aid in the United States is the Free Application for Federal Student Aid (FAFSA). Colleges, state governments, and the federal Department of Education all rely on the data submitted through the FAFSA to determine a student's eligibility for a wide array of need-based grants, subsidized loans, and work-study programs 85.

The Transition to the Student Aid Index (SAI)

Historically, processing the FAFSA produced a metric known as the Expected Family Contribution (EFC). However, following the FAFSA Simplification Act, the EFC was officially replaced by the Student Aid Index (SAI) beginning with the 2024 - 2025 academic year 1011. The SAI is intended to be a more accurate representation of the metric's true purpose. The old EFC nomenclature often confused families, who erroneously believed the figure represented their exact tuition bill. The SAI, by contrast, is explicitly an index number used by colleges to calculate the depth of a student's financial need and build an appropriate aid package 116.

The transition to the SAI introduced significant changes to the underlying mathematics of student aid. Most notably, while the old EFC bottomed out at zero, the SAI can drop to a negative number, going as low as -$1,500 1011. This negative range allows financial aid offices to more precisely identify students with the deepest, most severe financial need, helping schools prioritize the distribution of limited campus-based aid and state grants 116.

The formula weighs several elements: parent income, parent assets, student income, and student assets 13. Allowances against parent income include federal tax liability, payroll taxes, an employment expense allowance, and an Income Protection Allowance (IPA) based on family size. For a family of four, the IPA is roughly $44,880 13. After these allowances, the remaining "available income" is assessed at progressive rates ranging from 22% to 47% 13. Student assets are assessed much more heavily, at a rate of 20% of their value, meaning every $1,000 sitting in a student's personal bank account increases the family's expected ability to pay by $200 13.

The most controversial change introduced by the SAI formula was the elimination of the "sibling discount." Under the previous EFC system, families with multiple children in college at the same time saw their expected contribution divided among the enrolled students 116. The SAI does not adjust for multiple students in college, meaning middle-class families with overlapping college students experienced a significant reduction in their calculated need-based aid eligibility 117.

Correcting the Course: The 2026 FAFSA Rollout

The initial rollout of the simplified FAFSA for the 2024 - 2025 cycle was widely considered a disaster, plagued by severe technical glitches, unfathomable delays, and a catastrophic failure to properly process applications for students whose parents lacked Social Security numbers 1516. The chaotic launch left millions of students waiting months for financial aid offers, and an estimated 25% of students reported that the rollout issues negatively affected their ability to stay enrolled 1689.

To prevent a repeat of this scenario, the Department of Education implemented a phased rollout for subsequent years. For the 2026 - 2027 academic year, driven by the bipartisan FAFSA Deadline Act, the application successfully launched on time on October 1, 2025 810. The new system features real-time identity verification, eliminating the previous multi-day waiting periods for account setup, and allows most applicants to receive immediate confirmation of their SAI and Pell Grant eligibility without delay 101112.

The One Big Beautiful Bill Act (OBBBA) Adjustments

The 2026 - 2027 FAFSA cycle also incorporates new formula adjustments dictated by the One Big Beautiful Bill Act (OBBBA), passed in July 2025 1213. These changes drastically alter how certain assets and incomes are treated in the need-based calculation:

- Restored Asset Exemptions: A major win for middle-class families, the new formula excludes the net worth of family-owned businesses (with 100 or fewer full-time employees) and family farms on which the family resides from the SAI asset calculation 101213.

- Foreign Income Inclusion: Any foreign earned income exclusion amounts reported on tax returns will now be added back into a family's Adjusted Gross Income (AGI) when determining Pell Grant eligibility, impacting families who live or work abroad 101323.

- Prior Tax Year Shift: The 2026 - 2027 application requires applicants to provide 2024 prior-year tax information, establishing a more up-to-date financial profile 12.

Federal Need-Based Programs

Once a student's SAI is calculated, it acts as the master key to unlock federal need-based assistance. The cornerstone of the federal system is the Federal Pell Grant. Designed for undergraduate students with exceptional financial need, the Pell Grant is considered the foundation of a financial aid package because, unlike a loan, it generally does not have to be repaid 4623.

For the 2026 - 2027 award year (running from July 1, 2026, through June 30, 2027), the maximum Federal Pell Grant is officially fixed at $7,395, with a minimum award amount of $740 231415. However, the OBBBA legislation introduced strict new eligibility caps. Students with an SAI equal to or greater than twice the maximum Pell Grant amount - specifically, an SAI of $14,790 or higher - are now explicitly blocked from receiving any Pell Grant funds 132315. This establishes a hard ceiling that did not exist under previous regulations, though a narrow exception remains for certain dependents of deceased servicemembers and public safety officers 2315.

Furthermore, beginning in July 2026, students who receive full-ride scholarships that cover their direct costs (tuition, fees, room, and board) will no longer be eligible for Pell Grants 10. This regulation is designed to prevent the stacking of federal need-based funds on top of comprehensive institutional merit awards, redirecting federal dollars to students with unmet expenses 10.

Beyond grants, federal need-based aid includes the Federal Work-Study program, which provides subsidized part-time campus jobs, and Direct Subsidized Loans 16. Unlike standard unsubsidized loans, the federal government pays the interest on subsidized loans while the student remains enrolled at least half-time, making them a highly desirable form of debt 16.

It is worth noting that the OBBBA also fundamentally changed federal borrowing limits. While undergraduate subsidized and unsubsidized loan limits remain mostly intact, the legislation introduced severe new annual and lifetime borrowing caps for graduate students, health professionals, and Parent PLUS borrowers, effectively phasing out unlimited federal graduate lending 16. "Legacy borrowers" - those who had a loan disbursed in their current program prior to July 1, 2026 - are permitted to continue using the old federal loan limits for up to three academic years, provided they maintain continuous enrollment 16.

The Reality of Merit-Based Aid and Tuition Discounting

While the federal government dominates the need-based landscape, institutional aid - the money that colleges provide directly to their students out of their own coffers - dominates the merit space. Over the past decade, institutional grants have surged, growing by 31% to a massive $82.8 billion in the 2023 - 2024 academic year 27. Today, institutional grants account for roughly 52% of all grant aid received by undergraduate and graduate students combined 27.

Merit aid is frequently misunderstood by the general public as a rare reward reserved strictly for valedictorians, perfect SAT scorers, and elite athletes. While those students certainly receive scholarships, the reality is that merit aid at the vast majority of private universities functions as a sophisticated enrollment and pricing strategy known as "tuition discounting" 71718.

Because the exorbitant sticker price of private colleges can easily deter applicants, institutions offer so-called merit scholarships to systematically lower the actual cost for the majority of their accepted students. This strategy entices students to enroll who might otherwise choose a cheaper public university, helping the private college hit its tuition revenue targets and shape the demographics and academic metrics of its incoming freshman class 719.

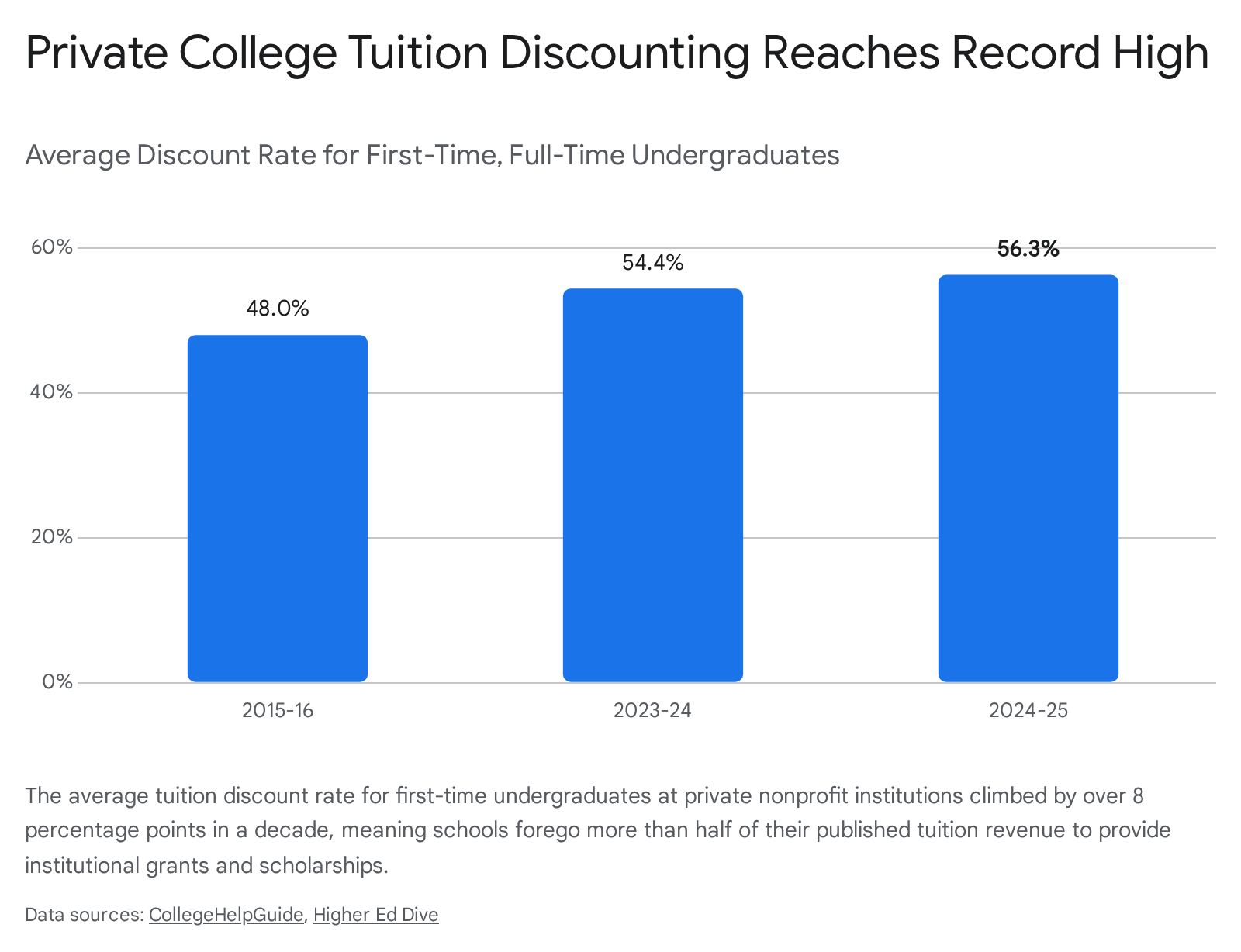

Data from the National Association of College and University Business Officers (NACUBO) reveals the sheer scale of this practice. For the 2024 - 2025 academic year, the average tuition discount rate for first-time, full-time undergraduates at private nonprofit colleges reached a record high of 56.3% 202122.

This metric indicates that for every dollar of tuition these institutions charge on paper, they immediately give back roughly 56 cents in the form of institutional grants and scholarships 2122.

Consequently, approximately 90% of first-time undergraduates at participating private institutions received some form of institutional aid 2234. The current system of setting college prices has been criticized by higher education economists as broken and confusing, because the published "sticker price" is an increasingly poor indicator of what students actually pay 1723. If a family writes off a private college solely based on its published tuition without seeing their discounted financial aid package, they may be making a $30,000 mistake 20.

This discounting strategy comes at a severe cost to the institutions themselves. Colleges fund these discounts primarily through "undedicated sources" - meaning they simply go without the tuition revenue they claimed to charge - as well as drawing from institutional reserves and endowment earnings 1722. Because discount rates are rising faster than tuition increases, net tuition revenue (the actual cash colleges take in) was projected to decline by 0.8% in the 2024 - 2025 academic year 2234. At private colleges that recently announced closures, the average discount rate was routinely exceeding 65%, underscoring the precarious financial tightrope many tuition-dependent schools walk 23.

Public universities, traditionally reliant on a low-tuition, low-aid model, are rapidly adopting private-sector discounting strategies to combat demographic shifts and enrollment challenges. Between 2014 and 2022, the percentage of first-time, full-time undergraduates receiving institutional grant aid at public four-year institutions increased from 49% to 62%, with average public discount rates rising from 24% to 31% 3624. During this transition, merit-based aid at public institutions grew by 38%, vastly outpacing a meager 4% growth in need-based institutional grants, indicating a shift toward competitive enrollment tactics rather than equity-based funding 24.

How Need and Merit Intersect in College Admissions

When applying to college, a family's financial need can occasionally impact their actual chances of admission, depending entirely on the institution's stated policy. The admissions landscape is divided into two primary camps: need-blind and need-aware.

Need-Blind Admissions

Need-blind admissions means that a college evaluates a student's application strictly on academic and personal merit, entirely without seeing their financial aid forms or considering their ability to pay 3839. The admissions committee does not know if the applicant requires a full ride or can pay the $80,000 yearly sticker price in cash 39. Need-blind admission is considered the gold standard of equity in higher education.

However, only a small fraction of elite schools - typically the wealthiest private universities like Harvard, MIT, Princeton, Yale, and Stanford - can afford to operate truly need-blind policies while simultaneously guaranteeing to meet 100% of an admitted student's demonstrated financial need 383940. Most of these institutions reserve this policy exclusively for domestic students (U.S. citizens and permanent residents) 38.

Need-Aware Admissions

Need-aware (or need-sensitive) admissions means the university actively factors a student's financial situation and ability to pay into the final admissions decision 740. While colleges still focus heavily on academic merit, a need-aware school with a finite financial aid budget may ultimately favor a full-paying student over a high-need student if both applicants are on the borderline of acceptance 73825.

For domestic students, being need-aware rarely means the school routinely rejects qualified applicants simply because they are poor. Need is usually only a "tip factor" among many, and the vast majority of admitted students at need-aware schools still receive substantial financial aid packages 3825.

International students, however, face distinctly tougher odds. As non-U.S. citizens, they are ineligible for federal financial aid, meaning the university itself must cover the entirety of their tuition gap out of its own budget 40. Consequently, almost all U.S. colleges are need-aware for international applicants 38. Even at need-blind schools, international applicants face challenges related to "yield protection" - colleges prefer to admit students they believe will actually enroll, and some institutions may subtly favor international applicants who have the demonstrated financial resources to easily secure a visa and attend 40.

State-Sponsored Aid Systems

State governments provide the third major pillar of financial aid, appropriating an estimated $133.1 billion for higher education overall in the 2026 fiscal year 2627. Of that total state support, roughly 12.9% (or over $17 billion) was allocated specifically to student financial aid 2627.

State-level aid has become increasingly crucial as public university net tuition revenues fluctuate. According to the State Higher Education Executive Officers Association (SHEEO), state public financial aid reached an all-time high of $1,271 per full-time equivalent (FTE) student in 2025, a 5.1% increase over the prior year 2829. However, this aid varies wildly by geography, ranging from a meager $44 per student in Montana to $3,662 per student in New Mexico 28.

State financial aid programs generally fall into two distinct ideological camps. Forty-nine of the 100 largest state financial aid programs disburse funds strictly based on financial need (often using the FAFSA's SAI metric), ensuring taxpayer dollars support low-income residents. Conversely, seventeen major state programs use purely merit-based criteria, focusing aid on students matriculating directly from high school who meet specific GPA or standardized test requirements 5.

Southern states have heavily favored merit-based models, often funding them through state lotteries, to keep high-achieving local students from leaving the state for college. Other states are moving toward "Promise" programs, which function as last-dollar need-based grants.

Comparing Notable State Aid Programs

| State | Program Name | Primary Type | Key Eligibility Requirements | Funding Coverage |

|---|---|---|---|---|

| Georgia | HOPE Scholarship | Merit | 3.0 high school GPA; 4 rigor credits (e.g., AP/IB/Dual Enrollment). | Significant portion of in-state public tuition; fixed amount for private colleges. |

| Georgia | Zell Miller Scholarship | Merit | 3.7 high school GPA; 1200 SAT or 26 ACT. | Full standard in-state public tuition (fees and housing excluded). |

| Florida | Bright Futures | Merit | High GPA, standardized test thresholds, and documented volunteer service hours. | Up to 100% of tuition at in-state public universities. |

| Minnesota | North Star Promise | Need | Adjusted Gross Income below $80,000; FAFSA completion. | Tuition-free at MN public and tribal colleges after other grants are applied. |

| New York | Excelsior Scholarship | Need/Hybrid | Family income up to $125,000; must live/work in NY after graduation. | Tuition-free at SUNY/CUNY public colleges (housing excluded). |

| Louisiana | TOPS (Taylor Opportunity) | Merit | Specific core GPA and minimum ACT scores across tiered award levels. | Covers tuition at LA public institutions up to set legislative amounts. |

Sources: 4647304950

State aid programs often operate on a "last-dollar" basis. This means the state will only cover the remaining tuition costs left over after a student's federal Pell Grants and institutional scholarships have already been applied to the bill 4630.

Macroeconomic Trends in College Funding

The interplay of merit and need-based aid operates against a backdrop of severe macroeconomic pressure on both students and institutions. As of the third quarter of 2025, total U.S. student loan debt reached an astounding $1.833 trillion, spread across 42.8 million federal borrowers carrying an average balance of $39,547 2734.

While the headline numbers suggest widespread access to capital, the burden of repayment is not distributed equally. According to Federal Reserve data, roughly 20% of borrowers who are currently required to make payments reported being behind or in collections in late 2024 51. Difficulties with student loan payments are highly correlated with the type of institution attended: 35% of borrowers who attended private for-profit institutions were behind on payments, compared to just 16% of those who attended public universities and 15% at private nonprofits 51.

Colleges themselves are facing severe inflationary pressures that complicate their ability to offer aid. The Higher Education Price Index (HEPI) - which tracks the specific costs of running a university - has outpaced the general Consumer Price Index in nine of the past eleven years 34. In fiscal year 2025, faculty salaries, which constitute 35% of the HEPI index, grew by 4.3%, the highest rate since tracking began in 1998 34.

To survive these rising costs without pricing students out entirely, universities lean heavily on direct federal funding. Beyond student financial aid, the federal government is a massive revenue source for institutional operations, primarily through research grants from agencies like the National Institutes of Health (NIH) and the National Science Foundation (NSF) 31. At elite research universities like Johns Hopkins and MIT, federal funding accounts for over 40% of their total institutional revenue 31. If federal student aid or research grants were cut, public universities would be forced to rely on increased state investment, while private institutions would likely raise tuition for higher-income students to replace the lost revenue, further exacerbating the cycle of high prices and deep discounts 31.

Debunking Common Financial Aid Myths

The sheer complexity of the FAFSA, institutional discounting, and state policies generates pervasive misconceptions. Unfortunately, these myths frequently deter middle-class families from applying for aid, causing them to miss out on vital funding.

Myth: "We make too much money to qualify for aid." There is no absolute income cut-off to qualify for federal student aid 353. Eligibility depends on a matrix of factors including family size, the number of dependents, and asset types. Furthermore, because many colleges require a completed FAFSA before they will consider students for merit-based scholarships, affluent families who skip the application process out of an assumption of ineligibility often leave thousands of dollars of non-need-based institutional aid on the table 35455.

Myth: "Private colleges are always more expensive than public universities." While the published sticker price of a private college is almost always higher, their massive tuition discounting practices and deep institutional endowments routinely yield a lower net price for the student 854. Institutions like Bridgewater College or the University of Tulsa automatically consider applicants for generous merit scholarships that can bring the net cost well below the out-of-state tuition of public flagship universities 56.

Myth: "Applying for financial aid hurts my admission chances." For the vast majority of applicants, checking the box indicating they will apply for financial aid does not harm their admissions chances. The majority of U.S. colleges practice need-blind admissions for domestic students 5455. Even at need-aware schools, financial need is typically only considered at the very margins for borderline candidates 25.

Myth: "Only straight-A students get merit aid." Because merit aid is primarily used as a tuition discounting tactic to boost baseline enrollment, a student certainly does not need a 4.0 GPA or a perfect ACT score to receive institutional scholarships. Colleges regularly award merit aid for leadership, community service, geographic diversity, legacy status, and specialized extracurricular talents 1854.

Myth: "The government decides how much aid I get." The federal government uses the FAFSA to determine a student's Student Aid Index (SAI) and their eligibility for federal Pell Grants and loans. However, the government does not mandate what the college must give. Each college's financial aid office ultimately decides how much institutional grant aid to offer based on its own internal budget, endowment resources, and enrollment goals 55.

Bottom line

Merit-based financial aid primarily functions as a sophisticated enrollment strategy used by colleges to attract talented students and meet revenue targets, while need-based aid is a formulaic federal and state system meant to bridge the wealth gap and ensure educational access. Because private colleges discount their tuition by an average of 56.3%, the published sticker price is rarely an accurate reflection of what families actually pay. To maximize funding, students must submit the FAFSA annually regardless of their household income, as it serves as the mandatory gateway not only to federal grants and subsidized loans, but also to millions of dollars in institutional merit scholarships.