How and When to Appeal a Financial Aid Offer

If a college financial aid package falls short of what a student requires to attend, families have the legal right to request a formal reconsideration through a process known as a financial aid appeal. Success hinges on a family's ability to provide concrete documentation of recent financial hardships not captured by tax records, or their ability to tactfully leverage a better financial aid offer from a competing institution. While large public universities often have strict budgetary limits, private colleges frequently possess the endowment flexibility to negotiate and increase their grant offerings.

The Disconnect Between Tax Data and Financial Reality

To understand why financial aid appeals exist and why they are frequently successful, one must first understand how colleges initially determine a student's ability to pay. The foundation of the American financial aid system rests heavily on the Free Application for Federal Student Aid (FAFSA) and, for many private institutions, the College Board's CSS Profile 11.

When families complete these standardized forms, the data collected is based on a "prior-prior year" methodology 1. For example, a student applying for financial aid for the 2025 - 2026 academic year is required to submit federal tax information from the 2023 calendar year 3. While utilizing historical tax data allows families to complete their applications earlier in the admissions cycle using finalized tax returns, it creates a significant structural flaw: the data is essentially two years out of date by the time the student sets foot on campus 12.

Over the course of two years, a family's financial stability can drastically deteriorate. The standardized formulas cannot predict a sudden corporate layoff, a devastating medical diagnosis, a divorce, or the death of a primary wage earner. Because the automated system is inherently rigid, the U.S. Department of Education provides a legal mechanism for colleges to bridge the gap between two-year-old tax data and a family's present-day financial reality.

The Statutory Power of Professional Judgment

Financial aid administrators at colleges and universities are not simply processing machines; they are granted significant discretionary authority by the federal government. This authority is codified in Section 479A of the Higher Education Act and is officially referred to as "Professional Judgment" (PJ) 3.

Professional judgment allows a financial aid administrator to evaluate a student's unique situation on a case-by-case basis and manually adjust the underlying data elements used to calculate their federal and institutional aid eligibility 3. By altering specific financial inputs - such as removing a lost job's income from the calculation or increasing the student's designated Cost of Attendance (COA) to account for unusual medical bills - the administrator can generate a new, lower Student Aid Index (SAI), which subsequently unlocks additional grant money and subsidized loans 347.

Recent legislation has actually strengthened this process. Under the FAFSA Simplification Act, the Department of Education explicitly mandates that institutions must publicly post information regarding the ability to request a professional judgment review on their websites 38. Furthermore, institutions are strictly prohibited from maintaining a blanket policy that denies all appeal requests; they must consider all documented inquiries 38.

The use of this mechanism is widespread. Recent surveys conducted by the National Association of Student Financial Aid Administrators (NASFAA) indicate that approximately 26 percent of collegiate financial aid offices have reported an increase in professional judgment requests over the past year 5. This rise is attributed to lingering economic volatility, broader awareness of the appeals process, and the recent federal mandates requiring colleges to proactively advertise the option 5.

The FAFSA Simplification Act formally bifurcates professional judgment into two distinct categories: "Special Circumstances" and "Unusual Circumstances" 38. Understanding the difference is critical for families preparing to submit an appeal.

Special Circumstances: Appealing the Financial Data

"Special Circumstances" refer exclusively to financial situations that justify altering the data elements in a student's cost of attendance or their Student Aid Index calculation 3. When a family experiences a tangible loss of income or an unexpected, unavoidable expense, they are filing a special circumstances appeal 36.

However, financial aid administrators are heavily regulated and subject to federal audits. They cannot grant an appeal simply because a family feels that college is too expensive, or because the family wishes to avoid taking out student loans 711. The financial hardship must be non-discretionary, meaning the family had no reasonable control over the financial burden. The following scenarios outline the most common and legitimate grounds for a special circumstances appeal.

Involuntary Job Loss and Income Reductions

The most frequently approved financial aid appeals involve the sudden loss of employment 77. If a parent or an independent student is laid off, fired, or experiences a severe, involuntary reduction in their working hours after the base tax year, the financial aid office can manually adjust the FAFSA to reflect the family's projected current-year income rather than their past income 13.

To successfully prosecute this type of appeal, families must provide an airtight paper trail. Administrators will typically require a formal termination or layoff notice from the former employer, the final pay stub showing year-to-date earnings, and any initial eligibility determination letters from the state unemployment compensation office 1489. Furthermore, the family must provide a written, good-faith estimate of their anticipated income for the remainder of the calendar year, accounting for any severance pay or unused vacation payouts 139. If a parent lost a job but was quickly rehired at a similar salary, the appeal will likely be denied, as the overall annual income remains largely unchanged.

Exceptional Medical and Dental Emergencies

Routine healthcare costs, health insurance premiums, and elective procedures are generally factored into the standard formula used to determine financial aid. In fact, the federal methodology includes an automatic "Income Protection Allowance" (IPA), which assumes that roughly 11 percent of a family's basic living allowance goes toward standard medical care 3.

However, if a family is burdened by catastrophic, out-of-pocket medical or dental expenses that far exceed standard allowances - such as the costs associated with cancer treatments, unexpected surgeries, or managing a chronic disability - these costs can be grounds for an appeal 14810. To win a medical appeal, the family must prove that the expenses were not reimbursed by insurance. Required documentation typically includes itemized hospital billing statements, receipts for paid medical debts, and a copy of the payment agreement with the health organization 138. If a severe medical condition required significant travel, meticulously documented expenses for gas, lodging, and food related to that travel can sometimes be factored into the appeal 13.

Life Transitions: Divorce, Separation, and Death

The financial landscape of a family changes instantly in the event of a divorce, legal separation, or the death of a parent. If these events occur after the FAFSA has been filed, the surviving or custodial parent can immediately petition the financial aid office to remove the deceased or absent spouse's income and assets from the application 810.

In the case of death, administrators will request a death certificate and documentation of the deceased parent's year-to-date earnings 89. For divorce or separation, colleges generally require a copy of the legal divorce decree or separation agreement, which outlines child support and alimony 89. If the parents are informally separated without legal documentation, many colleges will accept alternative evidence of separate living accommodations, such as utility bills or lease agreements in the non-custodial parent's name at a different address 1389. It is important to note that if parents consider themselves separated but continue to reside in the exact same household, financial aid administrators will typically consider the appeal invalid, as the household income structure has not functionally split 13.

One-Time Financial Anomalies (The "Income Spike")

Occasionally, a family's tax returns will show an artificially inflated income due to a one-time financial anomaly. Common examples include withdrawing from a retirement account to pay for a sudden emergency, receiving a lump-sum severance package, cashing in an inheritance, or receiving a divorce settlement 148.

If these funds were used to pay off medical debts or were rolled over into another protected account (like a Roth IRA rollover), they make the family look vastly wealthier on paper than they actually are. Families can appeal to have these one-time spikes excluded from the need analysis calculation. To do so, they must provide documentation of the origin of the one-time income and clear verification of how the funds were ultimately used or relocated 811.

The Boundaries of an Appeal: What Administrators Will Not Consider

While financial aid administrators have broad authority, their flexibility has hard limits. Professional judgment is designed to assist families facing unavoidable hardships, not to subsidize lifestyle choices or consumer debt 912.

Colleges will almost universally reject appeals based on the following circumstances: * High consumer debt, including credit card balances and personal loans 911. * Auto loans and car insurance payments 11. * Personal bankruptcy proceedings 911. * Loss of home equity or standard home maintenance 11. * Voluntary private secondary school tuition for younger siblings 11. * Vacation expenses or voluntary tithing to religious organizations 3.

To clarify the boundaries of the appeals process, the table below summarizes the difference between a valid, non-discretionary special circumstance and an invalid, discretionary financial choice.

| Category of Appeal | Valid Special Circumstances (Likely Approved) | Invalid Circumstances (Almost Certainly Denied) |

|---|---|---|

| Employment & Income | Involuntary layoff, permanent disability, or permanent closure of the employer's business. | Voluntary resignation to seek a new career; minor fluctuations in freelance income. |

| Household Structure | Legal divorce, death of a wage earner, or documented physical separation into two distinct households. | Parents who claim to be separated but still reside under the same roof sharing expenses. |

| Medical Costs | Out-of-pocket costs for severe illnesses, chronic disability management, or emergency surgeries. | Routine dental cleanings, elective cosmetic procedures, or minor copays fully covered by the standard income allowance. |

| Housing & Assets | Catastrophic home repairs due to natural disasters (e.g., burst pipes flooding a home). | Standard mortgage payments, optional kitchen renovations, or losses in the stock market. |

Unusual Circumstances: Dependency Overrides

The second branch of professional judgment is classified under the FAFSA Simplification Act as "Unusual Circumstances" 3. This is entirely separate from appealing financial data; instead, it involves appealing the student's legal dependency status.

For the purposes of financial aid, the vast majority of undergraduate students under the age of 24 are considered "dependent," meaning the federal formula demands that their parents' financial information and signatures be included on the FAFSA 8. However, the law recognizes that in severe cases, obtaining parental information is either impossible or dangerous for the student.

Financial aid administrators possess the authority to execute a "dependency override," unilaterally reclassifying a dependent student as an independent student 37. If an override is granted, the parents' income and assets are completely stripped from the calculation, and the student's financial aid is assessed solely on their own income, which typically results in maximum grant eligibility 6.

When Dependency Overrides Are Granted

Dependency overrides are reserved for extreme, highly sensitive situations. According to Department of Education guidelines, valid unusual circumstances include: * Human trafficking 38. * Refugee or asylee status where parents remain in a dangerous foreign nation 38. * Severe parental abuse, neglect, or physical abandonment 38. * Parental incarceration or institutionalization 38. * Students who are unaccompanied homeless youth or at risk of becoming homeless 320.

Because these situations involve legal and physical safety, administrators require corroborating evidence. Students are typically asked to provide third-party documentation, such as letters from high school guidance counselors, social workers, law enforcement officers, clergy members, or court records detailing the estrangement or abuse 7. The FAFSA Simplification Act specifically directs institutions to process these independence determinations as quickly as practicable, mandating a decision no later than 60 days after the student enrolls 3. Once a student is granted an adjustment for unusual circumstances, they are presumed to be independent for all subsequent award years at that institution, saving them from having to re-prove their trauma annually 3.

When Dependency Overrides Are Denied

It is crucial to understand that federal guidelines explicitly forbid administrators from granting a dependency override for routine family friction. An administrator cannot and will not grant an override simply because the student's parents refuse to contribute financially to their college education 3. Furthermore, an override will not be granted just because the parents refuse to fill out the FAFSA form, nor because the parents do not claim the student as a dependent on their federal tax returns 3. Even if a student currently lives alone and supports themselves entirely through a full-time job, they remain a dependent in the eyes of the Department of Education until they reach age 24, marry, join the military, or have dependents of their own, unless a documented history of abuse or abandonment exists 38.

The Competitive Appeal: Negotiating Merit and Yield

While special and unusual circumstances rely heavily on demonstrating severe financial or personal hardship, there is an entirely different avenue for appealing a financial aid package: the competitive appeal 21. This approach relies less on a family's financial distress and more on the college's desperate need to secure high-quality students.

Higher education is fundamentally a business, and colleges are acutely focused on their "yield rate" - the percentage of admitted students who ultimately choose to enroll 13. Over the past two decades, shifting demographics, an increase in the number of applications students submit, and widespread skepticism regarding the value of a degree have driven average yield rates down severely. From 2007 to 2017, the average college yield rate plummeted by nearly 15 percentage points, stabilizing in the low 30 percent range 13.

To combat this, colleges use predictive data modeling and targeted financial aid to incentivize their most desired applicants 13. If a student receives an impressive financial aid package from one institution but prefers another, they can often leverage the competing offer to spark a bidding war 123.

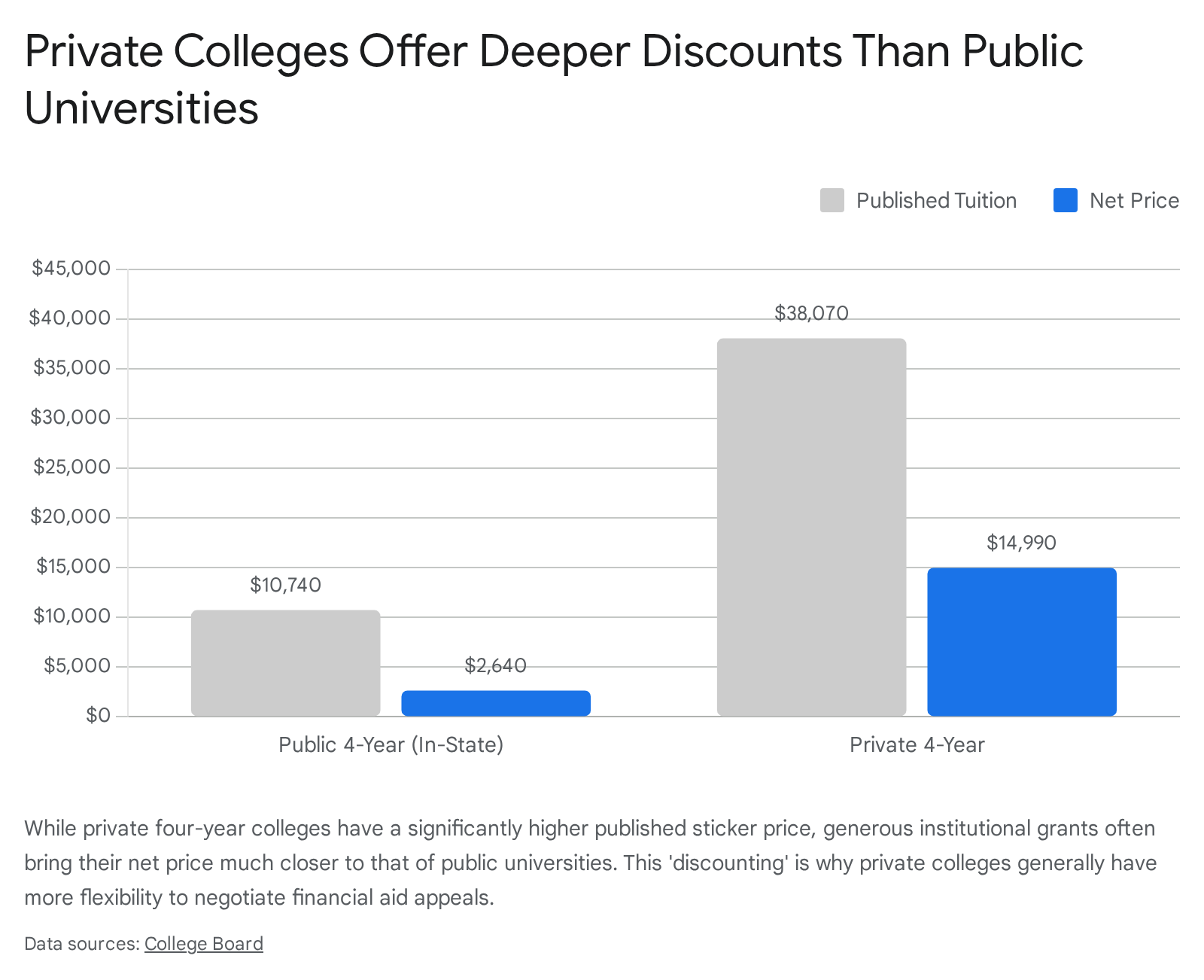

The Divide Between Public and Private Institutions

A family's leverage in a competitive appeal is almost entirely dependent on whether they are negotiating with a public state university or a private college.

Public Universities: State-funded institutions generally operate with rigid formulas tied directly to state appropriations and federal guidelines 212425. Because their published tuition - the "sticker price" - is already heavily subsidized by taxpayers for in-state residents, their financial aid offices have very little discretionary institutional grant money 2124. If a student approaches a massive public university asking them to match a private school's offer, the appeal will likely fail. As one industry expert notes, competitive appeals at public institutions have a success rate of roughly 25 percent, and often only yield minimal increases 225.

Private Colleges: Conversely, private, non-profit institutions are funded by substantial endowments and charge a much higher initial sticker price 2414. However, very few students actually pay that price. To remain competitive, private colleges engage in aggressive "tuition discounting." According to the National Association of College and University Business Officers, private institutions offered average tuition discounts exceeding 50 percent for the 2024 - 2025 academic year 13. Because these discounts are funded by discretionary endowment pools, financial aid officers at private colleges have tremendous flexibility to adjust merit scholarships and institutional grants to win over an applicant 251427. Competitive appeals at middle-tier private colleges are highly successful, with some estimates citing a 75 percent success rate, often yielding an additional $3,000 to $5,000 per year 221.

Executing an "Apples to Apples" Comparison

To effectively negotiate, families must ensure they are making an "apples to apples" comparison 21. Financial aid administrators are trained to see through poorly constructed leverage.

First, the competing offers must be from peer institutions. A financial aid office at a highly selective Ivy League university will not be swayed by a massive merit scholarship from a non-selective regional college 2115. To generate genuine leverage, the competing offer must come from a school of similar prestige, size, or ranking 15.

Secondly, families must negotiate based on the "net price," not the gross scholarship amount. Financial aid award letters can be notoriously confusing, sometimes burying high-interest Parent PLUS loans within the "award" section to make the package look more generous than it is 2125. When comparing offers, families must subtract all free money (grants and scholarships) from the total cost of attendance (tuition, fees, room, and board) to find the net price 29.

For instance, if College A costs $50,000 and offers $15,000 in grants, the net cost is $35,000. If College B costs $40,000 and offers $10,000 in grants, the net cost is $30,000 29. Even though College A offered a larger raw scholarship, College B is the objectively cheaper option. A student would then approach College A, present College B's award letter, and politely ask if College A can find an additional $5,000 in institutional aid to match the net price of their competitor 2329.

Families must also be wary of "front-loaded" packages. Some colleges offer massive grants for the freshman year to secure enrollment, but require a 3.7 GPA to renew the scholarship in subsequent years 2125. When negotiating, it is vital to ensure that any additional aid offered is renewable for all four years of study.

The FAFSA Simplification Act and the Rollout Crisis

Any discussion of financial aid appeals in the current era must address the seismic shifts caused by the FAFSA Simplification Act. Passed by Congress in 2020 and fully implemented for the 2024 - 2025 award year, this legislation represented the largest overhaul of the federal student aid system in over thirty years 30163233.

While the goal was to streamline the process by pulling tax data directly from the IRS via the FUTURE Act Direct Data Exchange, the transition was disastrous 43017. The software rollout was plagued by technical glitches, delayed openings, math formula errors, and a severe backlog in processing 1735.

For families seeking an appeal, the FAFSA Simplification Act introduced two massive hurdles: drastic changes to the underlying math formula, and chaotic administrative timelines.

The Shift from EFC to SAI

The legislation eliminated the longstanding "Expected Family Contribution" (EFC) and replaced it with the "Student Aid Index" (SAI) 420. While the SAI can drop as low as -$1,500 (allowing states to better target the neediest students), the new formula quietly eliminated several provisions that middle-class families previously relied upon 18.

The most controversial change was the elimination of the sibling discount. Historically, a family's EFC was divided by the number of children they had enrolled in college simultaneously 20. Under the new SAI formula, having multiple children in college yields no automatic benefit 2032. Furthermore, families who own small businesses or family farms are now required to report the net value of those assets, which were previously shielded 2032.

These legislative changes caused thousands of families to see a massive, unexpected drop in their financial aid eligibility. Fortunately, the Department of Education explicitly noted that financial aid administrators are permitted to use professional judgment to account for these exact losses. Administrators can manually adjust an applicant's COA or SAI elements to reflect the financial burden of paying for multiple college tuitions simultaneously 419.

To understand if a family has grounds to appeal based on formula changes, the following table summarizes the key structural differences introduced by the FAFSA Simplification Act.

| Metric | Previous Rules (Expected Family Contribution) | New Rules (Student Aid Index) |

|---|---|---|

| Minimum Value | $0 | -$1,500 (Allows for prioritization of the neediest applicants) 18. |

| Siblings in College | Total contribution divided by number of enrolled children. | No automatic division. (Can be appealed via Professional Judgment) 2019. |

| Small Businesses & Farms | Assets excluded if fewer than 100 employees. | Net worth of business/farm must be reported as an asset 2032. |

| Pre-Tax Retirement | Employee contributions added back to adjusted gross income. | Contributions no longer added back, naturally lowering the SAI 20. |

| Asset Reporting Threshold | Required for families with an AGI above $50,000. | Increased to $60,000 AGI (Fewer families must report savings/investments) 20. |

Navigating System Delays and Deadlines

The botched rollout of the 2024 - 2025 FAFSA caused a ripple effect of delays. The form, which traditionally opens on October 1, did not soft-launch until December 30, and was immediately hobbled by virtual waiting rooms and system crashes 1735. Due to a massive formula error discovered late in the cycle - which would have shortchanged students by $1.8 billion - colleges did not receive Institutional Student Information Records (ISIRs) until mid-March, months later than usual 3320.

As a result, college financial aid offices experienced unprecedented strain. A NASFAA survey revealed that 72 percent of institutions experienced severe processing delays and unresponsiveness from the federal government, and nearly half of all aid offices faced severe resource and staffing shortages 214022. This administrative chaos forced many universities to push their traditional May 1 commitment deadlines to June or July 3323.

For families filing appeals, this chaos demands immense patience but also presents an opportunity for grace. Many colleges recognize that the technical difficulties are the fault of the Department of Education, not the student. If a student missed a state or institutional priority deadline because of a verifiable FAFSA system error, they should immediately contact the financial aid office to request a deadline extension; many institutions are granting leniency specifically because of the modernization issues 202444.

Step-by-Step Guide to Filing a Successful Appeal

Navigating the financial aid appeal process requires organization, a respectful tone, and adherence to protocol. Complaining directly to an admissions counselor or sending angry emails to the financial aid inbox will likely backfire. To maximize the chances of a favorable professional judgment review, families should follow a strict, strategic methodology.

Step 1: Initiate Contact and Learn the Protocol

Do not immediately draft a letter and send it blindly. The first step is always to contact the specific institution's financial aid office via phone or email to inquire about their unique appeals process 141025.

Every college operates under different administrative systems. Some universities require students to log into a specialized financial aid portal and complete a proprietary "Special Circumstances Appeal Form" 6712. Others may require a specific institutional dependency override worksheet, while smaller colleges might simply ask for an emailed letter. Failing to follow the institution's designated procedure guarantees a delay 71446.

If the student is selected for federal verification - a routine audit process where the school must verify the accuracy of the FAFSA data - that verification must be entirely completed before a financial aid administrator is legally allowed to process a professional judgment adjustment 26.

Step 2: Gather Comprehensive Documentation

As established, administrators cannot act without a paper trail. If the appeal is based on financial hardship, families must compile copies (never originals) of tax returns, W-2s, termination letters, medical bills, and unemployment benefit statements 131425.

If the appeal is competitive, the student must generate high-quality PDF copies of the competing financial aid award letters 2327. The documentation should be organized logically so the administrator can immediately locate the pertinent figures.

Step 3: Draft a Student-Led Letter

The appeal letter itself should ideally be authored by the student. Admissions and financial aid officers appreciate students who take ownership of their collegiate journey, and a polite request from an aspiring freshman is generally received better than a demanding email from a frustrated parent 1.

The letter should be professional, concise (no longer than one to two pages), and structured logically 1427: 1. The Opening (Gratitude and Identification): Begin by stating the student's full name, student ID number, and the specific academic year in question. Express genuine gratitude for the offer of admission and the initial financial aid package 142527. 2. The Context (The Pivot): Clearly state that the family's financial situation has materially changed since the FAFSA was filed, or that a competing offer has made the current package financially unfeasible. Keep the explanation factual and devoid of excessive emotional pleading 71427. 3. The Evidence (The Numbers): Detail the specific financial changes. Use exact dollar amounts and percentages to illustrate the impact. Explicitly reference the attached supporting documents (e.g., "As demonstrated in the attached termination letter, our household income has decreased by $40,000") 71425. 4. The Ask (The Specific Request): Politely request a "reconsideration" or a "professional judgment review" of the award package. If a specific dollar amount is needed to make attendance possible, state that amount clearly. Reiterate that the institution remains the student's absolute top choice and that they are eager to enroll if the financial gap can be bridged 142125.

Step 4: Follow Up Respectfully

Once the appeal form, the letter, and the supporting documents are submitted, patience is required. The appeals process can take several weeks, particularly during the chaotic spring enrollment season 710. If two weeks pass without an acknowledgment, the student should send a polite follow-up email or call the office to confirm that the materials were received and to inquire if the committee requires any additional information 727.

Throughout the process, it is critical to have a backup plan. Appeals are never guaranteed, and families should actively research alternative funding options, outside scholarships, and more affordable fallback institutions while waiting for the committee's final verdict 71110.

Debunking Common Financial Aid Myths

Every year, thousands of students leave federal and institutional aid on the table because they fall victim to pervasive myths about how college funding works. Clearing up these misconceptions is vital for families navigating the appeals process.

Myth: Appealing for more money will cause the college to revoke my admission. This is entirely false. A college will never rescind an offer of admission simply because a family asked for more financial assistance. The admissions department and the financial aid department operate independently 221. Furthermore, federal law requires colleges to maintain a process for financial aid appeals 2. An offer of admission is generally only revoked for severe academic fraud, undisclosed criminal disciplinary history, or a catastrophic drop in high school grades during the senior year 492851.

Myth: My parents make too much money, so appealing is pointless. There is no hard income cutoff to qualify for federal or institutional student aid 293054. The need analysis formula takes into account family size, the age of the oldest parent, state taxes, and the cost of the specific institution 3054. Even if a family's income is too high to qualify for a federal Pell Grant, filing the FAFSA and appealing a hardship could still unlock access to low-interest, subsidized federal loans, federal work-study programs, or need-based institutional grants funded directly by the college 295431.

Myth: Financial aid is only for straight-A students and elite athletes. While merit-based scholarships certainly exist, they represent a fraction of the overall financial aid landscape. The vast majority of the funds disbursed annually - which routinely exceeds $185 billion across federal, state, and private sources - is awarded strictly on the basis of demonstrated financial need, completely independent of a student's high school GPA 293032. As long as a student meets the basic requirements for admission and maintains satisfactory academic progress, they are eligible for federal need-based aid 3032.

Myth: Only ethnic minorities qualify for financial aid. This is a persistent and legally inaccurate myth. The overwhelming bulk of federal, state, and institutional aid is strictly tied to financial need, not race or ethnicity. In fact, the Free Application for Federal Student Aid (FAFSA) does not even collect data regarding an applicant's ethnicity 3032.

Bottom line

A financial aid award letter is an opening offer, not an absolute final verdict. By utilizing the federal provision of professional judgment, administrators have the authority to increase aid packages for families facing legitimate, documented financial hardships, or to negotiate with highly desired applicants wielding competitive offers. While success requires meticulous documentation, an understanding of the difference between public and private college budgets, and a polite, student-led approach, the potential reward of securing thousands of dollars in additional educational funding is well worth the administrative effort.