How Your FAFSA Data Becomes a Financial Aid Letter

Your FAFSA data undergoes a highly secure, multi-stage digital journey involving the IRS, federal processing systems, and college financial aid offices to determine your financial need. After calculating your Student Aid Index (SAI), the government securely transmits your file to colleges, which then blend federal, state, and institutional funds into a personalized aid letter. Throughout this pipeline, strict federal laws dictate exactly who can see your tax information and how it can be legally used.

The Intake: Identity, Contributors, and the IRS Connection

The moment you begin your Free Application for Federal Student Aid (FAFSA), you are entering a highly regulated data ecosystem. Following the passage of the FAFSA Simplification Act and the Fostering Undergraduate Talent by Unlocking Resources for Education (FUTURE) Act, the application is no longer a standalone, self-reported form 12. Today, it acts as a collaborative, multi-party data-gathering engine.

To understand what happens to your data, you must first understand how it is collected. A major shift in recent years is the introduction of the term "contributor" 3. A contributor is anyone required to provide personal information, financial data, a signature, and legal consent on a student's FAFSA. Depending on the student's dependency status and family situation, contributors can include the student, a spouse, a biological or adoptive parent, or even the spouse of a remarried parent (a stepparent) 34. Notably, non-adoptive grandparents, legal guardians, and foster parents are not considered contributors 4.

Each contributor must create their own Federal Student Aid (FSA) ID and log into the system separately to complete their specific section of the form 34. The system uses sophisticated matching protocols to ensure that the contributor's name, date of birth, and Social Security Number perfectly align with the data on file 4. Once these contributors are authenticated, the FAFSA initiates its most critical backend process: fetching federal tax data.

The FA-DDX: The Federal Tax Information Pipeline

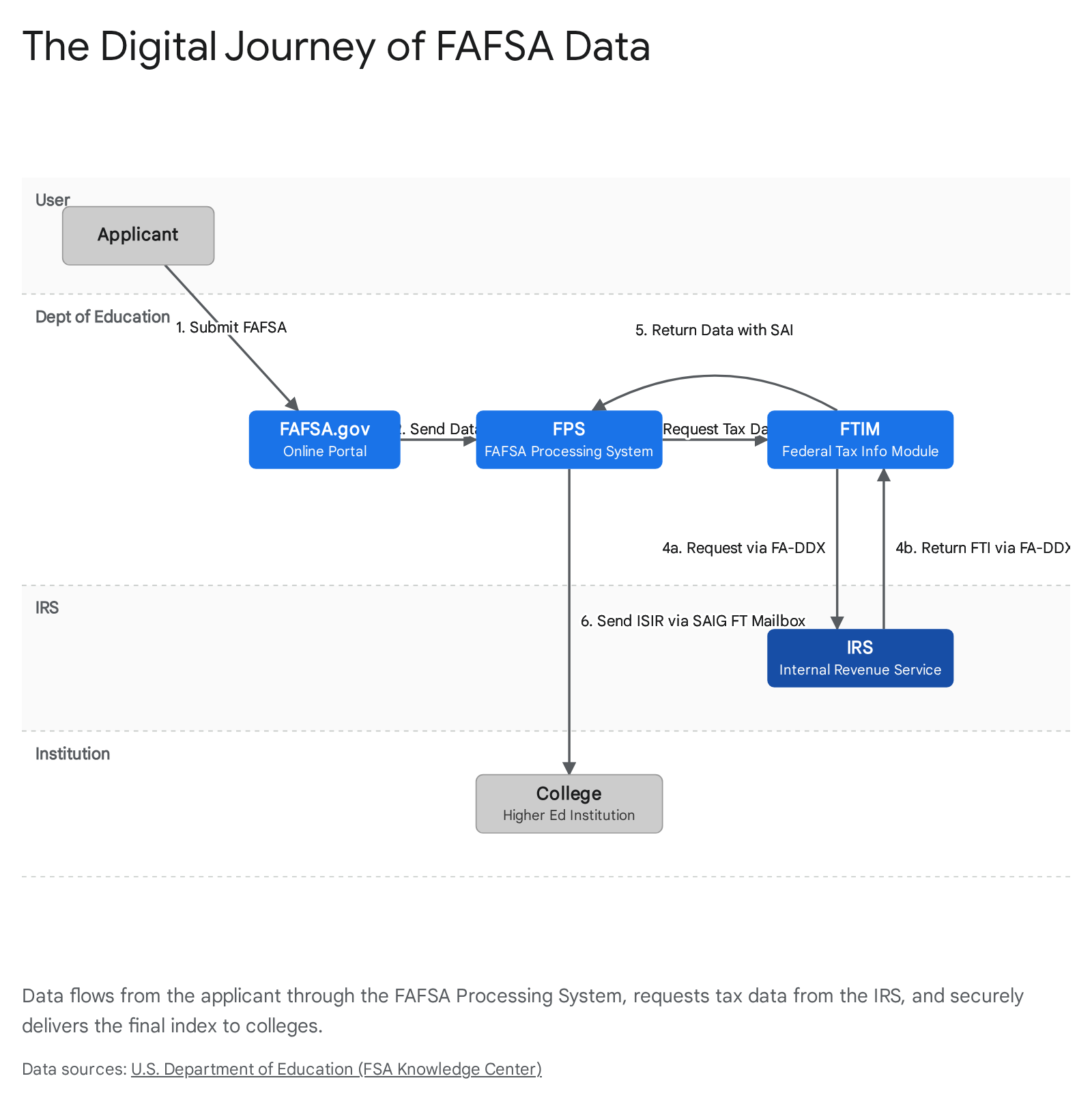

In the past, applicants either manually typed their tax data into the FAFSA or utilized the IRS Data Retrieval Tool (DRT) to port the information over. While the DRT was a step forward, it still required users to manually leave the FAFSA site, log into the IRS, and initiate the transfer 5.

Today, that entire mechanism has been replaced by the FUTURE Act Direct Data Exchange (FA-DDX) 15. Think of the FA-DDX as an automated, highly secure, windowless tunnel connecting the U.S. Department of Education directly to the Internal Revenue Service (IRS).

When a contributor logs in, they are required to provide formal "consent and approval" 1. This is not a mere terms-of-service checkbox; it is a legally binding authorization that allows the Department of Education to use the contributor's personal identifiers to ping the IRS, retrieve specific tax elements, and pull them directly into the application's backend 13.

The exact Federal Tax Information (FTI) pulled by the FA-DDX includes a highly specific set of data points necessary for the federal aid formula: * Tax year and filing status * Adjusted Gross Income (AGI) * Number of dependents or exemptions * Income earned from work and federal taxes paid * Education tax credits * Untaxed portions of Individual Retirement Account (IRA) distributions and pensions * Tax-exempt interest * Schedule C net profit or loss 45.

Once this data lands in the FAFSA system, it is permanently locked. The FA-DDX transferred values cannot be manually edited by the student or the parent 5. If the IRS states that your Adjusted Gross Income was $54,118, that is exactly what the FAFSA will use to calculate your aid - even if you believe there was an error 5. If a user needs to correct this information, they cannot do it on the FAFSA itself; they must file an amended tax return with the IRS, wait for the IRS to process the amendment, and then update the FAFSA 5.

This tradeoff guarantees data fidelity. By locking the data, the government prevents applicants from accidentally (or intentionally) altering their income to qualify for more aid 5. It also drastically reduces the amount of paperwork colleges must verify later in the process.

There are, however, exceptions to this seamless process. The FA-DDX cannot be used if the parents of a dependent student are married but file separate tax returns, if a parent's marital status has changed since the end of the tax year, if the family filed a foreign tax return, or if the tax filer was the victim of IRS-related identity fraud 6710. In these specific edge cases, the system requires the contributor to manually enter their tax data or provide an IRS Tax Return Transcript directly to the college 610.

Crucially, providing consent for the FA-DDX is mandatory. If any required contributor - including the student - refuses to provide consent, the FAFSA is immediately flagged as incomplete, and the student becomes entirely ineligible for federal and state student aid 118. There are no exceptions to this rule, even if the contributor did not earn enough money to be required to file taxes. In non-filing cases, consent simply allows the IRS to officially confirm to the Department of Education that no tax return exists 8.

The Backend Engine: FPS and FTIM

Once the FAFSA is submitted with all necessary signatures and IRS consent approvals, it leaves the public-facing website and plunges into the Department of Education's vast backend processing environment. This is where raw data is transformed into a standardized metric of financial need.

For decades, millions of FAFSA applications were processed by an aging mainframe known as the Central Processing System (CPS). However, the implementation of the FAFSA Simplification Act demanded a modern, more agile architecture. Starting with the 2024-2025 financial aid cycle, the legacy CPS was officially decommissioned and replaced by a modernized cloud-based infrastructure called the FAFSA Processing System (FPS) 91015.

The transition to the FPS was not merely a software upgrade; it was a fundamental architectural shift dictated by strict federal privacy laws. Because the FA-DDX brings highly sensitive raw tax data into the Department of Education's ecosystem, the IRS mandated rigorous cybersecurity protections. To meet these standards, the Department of Education had to build an entirely separate, heavily fortified digital vault known as the Federal Tax Information Module (FTIM) 1011.

When your FAFSA arrives at the FPS, the system separates your self-reported demographic data from your financial needs. The FPS sends a request to the FTIM, which securely interfaces with the IRS via the FA-DDX to retrieve your tax data 1011. The FTIM acts as a walled garden; it houses your tax data, performs the complex algorithmic math required to determine your financial need, and then passes only the final calculated results back to the broader FPS 11. This ensures that your raw tax data is never unnecessarily exposed to other government databases.

Calculating the Student Aid Index (SAI)

Inside the FTIM, your data is run through a complex, congressionally mandated formula to generate your Student Aid Index (SAI) 111718. Introduced during the recent simplification overhaul, the SAI officially replaced the long-standing Expected Family Contribution (EFC) 17.

The shift from EFC to SAI was heavily lobbied for by financial aid advocates because the term "Expected Family Contribution" was profoundly misleading. Families frequently assumed the EFC was the exact dollar amount they would be forced to pay out of pocket, which was rarely the case. The SAI is rebranded to clarify its true purpose: it is simply an eligibility index number that colleges use to rank a student's financial strength against the rest of the applicant pool 171812.

Beyond the name change, the transition to the SAI brought significant mathematical alterations to how your family's data is evaluated. Some changes expanded aid eligibility, while others tightened loopholes for wealthier families.

| Feature | Expected Family Contribution (EFC) | Student Aid Index (SAI) |

|---|---|---|

| Minimum Value Limit | Floored at $0. A student with zero income and a student in deep poverty both received a 0, making it hard for colleges to differentiate. | Can drop to -$1,500. This allows college financial aid offices to explicitly identify and target emergency grants to students with the most extreme financial need 1314. |

| The Sibling Discount | The final EFC was divided by the number of children a family had enrolled in college simultaneously, drastically lowering the expected contribution 17. | Removed entirely. Having multiple children in college no longer mathematically reduces the SAI 1314. |

| Family Farms & Small Businesses | Assets from small family businesses (under 100 employees) and family farms were completely excluded from the calculation 17. | The net worth of all businesses and farms must now be reported as an asset (excluding the specific value of the primary residence located on the farm) 13. |

| Grandparent 529 Plans & Cash Gifts | Financial support from extended family, including 529 plan distributions from grandparents, had to be reported as untaxed student income, penalizing the student 14. | Cash support and grandparent-owned 529 plans are no longer reported, protecting students from losing aid due to outside help 14. |

| Income Protection Allowance | Shielded a modest amount of parental and student income from the formula. | Significantly increases the income protection allowance, shielding a greater amount of parental income - especially for single parents 14. |

Once the FTIM calculates this SAI, it passes the index number, along with a determination of whether the student qualifies for a maximum, minimum, or calculated Federal Pell Grant, back to the main FAFSA Processing System 111214. At this point, your raw data has been successfully synthesized into actionable financial aid metrics.

Splitting the Data: ISIRs and Submission Summaries

After the FPS finishes its internal checks and calculations, it does not send the same information to everyone. The system splits the data, generating two distinct output documents: a highly redacted version for the student and a comprehensively detailed version for the colleges 915.

The FAFSA Submission Summary (For the Student)

Shortly after submission, the student receives an email notifying them that their FAFSA has been processed. They are directed to log into StudentAid.gov to view their FAFSA Submission Summary, a document that replaced the old Student Aid Report (SAR) 91516.

The Submission Summary is designed to be consumer-friendly. It provides an overview of the information the student originally provided, displays the calculated Student Aid Index (SAI), indicates estimated Federal Pell Grant eligibility, and highlights any data inconsistencies or missing signatures that require immediate correction 1524.

Crucially, to protect against identity theft and unauthorized viewing, the FAFSA Submission Summary will not display the raw Federal Tax Information pulled from the IRS via the FA-DDX 1517. For example, a student looking at their summary will not be able to see their parent's exact Adjusted Gross Income or taxes paid. Instead, the document will simply show a status indicator confirming that the tax data was successfully retrieved and transferred from the IRS 11.

The ISIR (For the College)

While the student receives the summary, the backend system simultaneously generates an Institutional Student Information Record (ISIR). The ISIR is the master output document of the financial aid world 1827. It is a massive, highly detailed, fixed-length electronic data file that contains every piece of information required for a college to package an aid offer 2719.

The ISIR contains the student's demographic data, the SAI, the results of various federal eligibility matches (such as checks against Department of Homeland Security and Social Security Administration databases), and the student's National Student Loan Data System (NSLDS) financial aid history, which shows how much federal aid the student has borrowed in the past 151920.

Unlike the student's summary, the ISIR does contain the raw Federal Tax Information (FTI) imported from the IRS 19. Because this tax data is legally protected under the Internal Revenue Code, the Department of Education mandates strict data labeling protocols. Specific fields on the ISIR that contain tax data or intermediate values derived from tax data (specifically ISIR Fields 306-321) must be explicitly flagged with the label "CUI//SP-TAX" (Controlled Unclassified Information/Specified Tax) 113031. This specialized label is hardcoded into the data file and follows the tax information wherever it is stored or accessed, serving as a constant legal reminder to the college that this data must be safeguarded under the highest federal cybersecurity standards 30.

The Department of Education securely transmits this ISIR to the state higher education agency of the student's home state and to every specific college or university the student listed on their FAFSA 151832. (Students can list up to 20 colleges on the modern online FAFSA 9).

Delivery to the Colleges: The SAIG Network

How exactly does a college receive your ISIR? Due to the sensitive nature of the data, the Department of Education does not use standard email or simple web portals to deliver these files. Colleges must establish and maintain connectivity to a secure federal intranet known as the Student Aid Internet Gateway (SAIG) 3321.

The SAIG is the primary routing system and secure pipeline through which institutions exchange financial aid data with federal systems 2122. To connect to it, a college's IT department and financial aid administrators use specialized federal software, most commonly EDconnect (a PC-based application) or TDClient (a mainframe/midrange application used for automated, high-volume file transfers) 193321.

Every college is assigned specific electronic mailboxes on the SAIG network, which serve as secure routing addresses 21. Before the 2024-2025 cycle, colleges used a primary "TG Mailbox" (identified by a code starting with "TG") for all financial aid data 19. However, the introduction of the FA-DDX and the inclusion of raw IRS tax data forced the government to heighten security 33.

Starting in the 2024-2025 award year, every college was required to establish a completely new, parallel "FT Mailbox" (identified by a code starting with "FT") 192122. This FT Mailbox is designed exclusively to receive ISIRs and any other files containing Federal Tax Information 1922. This strict separation ensures that highly sensitive tax data does not mingle with standard operational data and is protected by Federal Information Processing Standards (FIPS) advanced encryption 19.

In addition to receiving ISIRs through the SAIG, colleges also use this secure pipeline to connect to the Common Origination and Disbursement (COD) system 33. Once a college decides to award a student a Pell Grant or a Direct Federal Student Loan, the financial aid office uses the SAIG to send "origination" files to the COD system, essentially asking the federal government to draw down the actual funds from the U.S. Treasury and disburse them to the student's campus account 33.

The Processing Crisis: Normal Timelines vs. The 2024-2025 Delays

Understanding the backend plumbing of the FAFSA is critical to understanding why the financial aid system occasionally breaks down.

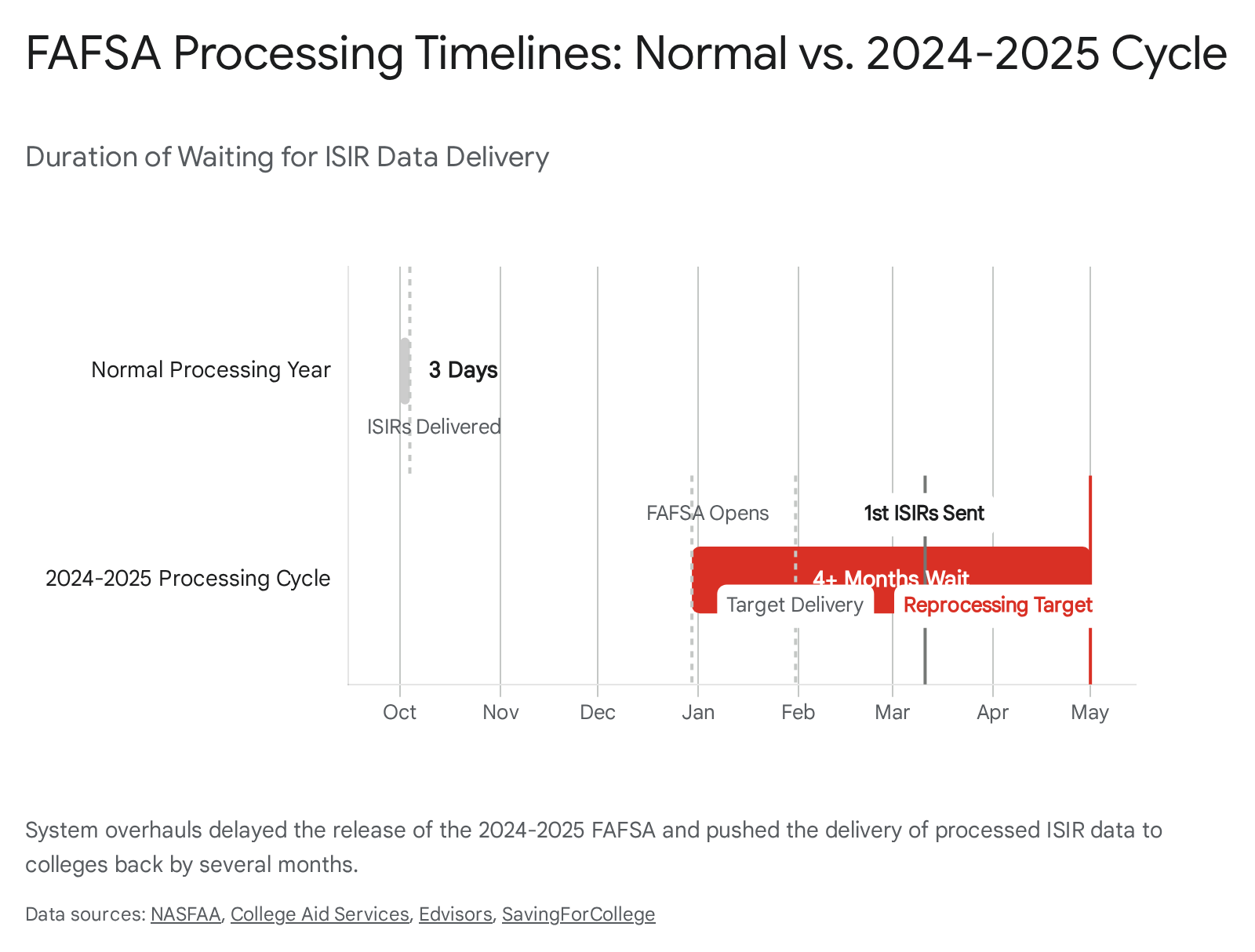

In a normal processing year, the FAFSA opens on October 1st 2338. Once a student submits their application online, the turnaround is remarkably fast. The application travels through the FPS, pings the IRS, calculates the SAI, generates the ISIR, and drops the file into the college's SAIG FT Mailbox within one to three days 322339. Paper forms generally take 7 to 10 days to process 39. Because the data arrives in early October, colleges have months to carefully verify the data, model their institutional budgets, and build comprehensive financial aid packages that are mailed to students by early spring.

However, the rollout of the redesigned 2024-2025 FAFSA caused a historic systemic crisis, pushing the delivery of ISIR data to colleges back by several months and drastically shortening the window students had to make enrollment decisions 4024.

The problems began with the launch date. Due to the sheer complexity of replacing the legacy CPS with the new FPS and building the FTIM to IRS specifications, the Department of Education delayed the release of the FAFSA from October 1, 2023, to late December 2023 - a period the Department called a "soft launch" 233842. Even after the form launched, the Department announced it would not begin processing any of the submitted applications or sending any ISIRs to colleges until March 2024, leaving millions of applications sitting dormant in a backlog 232443.

When the Department finally began transmitting ISIRs in mid-March, a cascade of severe calculation errors in the new formula algorithms were discovered, impacting massive swaths of the applicant pool: * The Inflation Table Error: The Department failed to update the supporting data tables used in the SAI calculation to account for recent inflation, an oversight that legally threatened $1.8 billion in federal aid before it was caught and patched 43. * The Dependent Asset Error: A vendor programming error caused the FPS to ignore the reported assets of dependent students (such as investments and cash accounts) when calculating the SAI, resulting in artificially low SAIs and inaccurate ISIRs being sent to colleges 2526. * Tax Data Discrepancies: Roughly 20% of FAFSA forms experienced errors transferring IRS data, including inconsistencies in education tax credit data and issues with amended tax returns 4647. * Missing Family Size: A glitch allowed some applications to be submitted with missing family size information, resulting in the system generating an ISIR with a blank SAI 48.

Because of these errors, the Department of Education had to halt, patch the software, and manually reprocess hundreds of thousands of ISIRs, sending updated files to colleges throughout April and May of 2024 254627.

A subsequent investigation by the Government Accountability Office (GAO) revealed the root causes of the crisis. The GAO found that the Office of Federal Student Aid (FSA) had failed to fully implement performance monitoring approaches for its contractors, deployed systems with incomplete contractual requirements, lacked specialized training for key oversight staff, and relied on testing environments that lacked vital information 28.

The real-world impact of these backend failures was severe. Because colleges did not receive accurate ISIRs until late spring, they could not load the data into their software systems to model budgets or generate aid letters 29. This compressed the decision-making window, forcing many colleges to push their traditional May 1st commitment deadlines to June 24. Preliminary data from the National Student Clearinghouse Research Center indicated that the chaotic rollout contributed to a steep decline in college freshmen enrollment for the 2024-2025 academic year, with the steepest drops observed among minority students and those attending public four-year institutions 53.

Verification: The Audit Phase

Once a college successfully downloads your ISIR into its local financial aid software, the data enters a critical quality-control phase. Before a college can offer you a single dollar of federal aid, it must check to see if your application has been flagged for "verification."

Verification is a routine federal audit process mandated by the Department of Education to ensure that the information submitted on the FAFSA is accurate 1524. It is not necessarily an accusation of wrongdoing; the FPS algorithm flags applications randomly or based on conflicting data patterns 1024. If your application is selected, your FAFSA Submission Summary will note it, and your ISIR will display an asterisk (*) next to your Student Aid Index 24.

When flagged, the student is placed into a specific Verification Tracking Group, which dictates exactly what the college's financial aid administrators must double-check 10.

- Standard Verification (V1): Focuses heavily on financial data. Historically, this meant the student had to track down physical W-2s and order IRS Tax Transcripts to prove their income 24.

- Custom Verification (V4): Focuses primarily on identity and the statement of educational purpose, ensuring the person applying is who they say they are 10.

- Aggregate Verification (V5): A comprehensive audit that combines the requirements of both V1 and V4, scrutinizing both financial data and identity .

Historically, the V1 financial verification process was a massive administrative burden that delayed aid for low-income students. However, the introduction of the FA-DDX has revolutionized this step. Because your tax data is now piped directly from the IRS into the FAFSA via a secure federal integration, the Department of Education automatically considers any FA-DDX imported data to be fully "verified" for Title IV aid purposes 210.

Today, if you use the FA-DDX, the financial aid office does not need to ask you for a tax transcript 1011. Financial verification now largely focuses on edge cases: families who manually entered their data, students whose parents filed separate returns, or discrepancies in the reported "family size" 61011.

If a student refuses to comply with the verification requests, the financial aid office is legally prohibited from disbursing any federal Title IV funds . Furthermore, if the documentation reveals that a student engaged in intentional fraud to receive aid, the college is required by federal regulations to refer the case to the Office of Inspector General .

To help colleges manage the compressed timeline during the 2024-2025 crisis, the Department of Education issued broad waivers, drastically reducing the overall percentage of students selected for verification to speed up processing. They also suspended routine program reviews, allowing financial aid offices to prioritize packaging aid over conducting audits 3031.

Building the Financial Aid Package

With a valid, fully verified ISIR on file, the financial aid office transitions from data processing to financial modeling. This is where your federal index is translated into actual money.

The foundation of every financial aid package is a simple, federally mandated equation: Cost of Attendance (COA) - Student Aid Index (SAI) = Financial Need 1232.

The Cost of Attendance is a comprehensive estimate calculated by the college that includes tuition, fees, housing, food, books, transportation, and miscellaneous personal expenses for the academic year 12. If a university's COA is $50,000 and your SAI is 10,000, your demonstrated financial need at that specific institution is $40,000.

The financial aid administrator's job is to attempt to fill that $40,000 gap by stacking different layers of funding 58.

- Federal Aid (The Foundation): The administrator first looks at your federal eligibility. If your SAI is low enough, the federal system guarantees you a Pell Grant 1258. Depending on the college's federal allocations, the administrator may also stack on a Federal Supplemental Educational Opportunity Grant (FSEOG) and Federal Work-Study funds 1258. Finally, they will add Direct Subsidized and Unsubsidized student loans to the package 12.

- State Aid (The Regional Support): Because state higher education agencies also receive your ISIR, they use your SAI to award state-funded grants (such as the Washington College Grant or New York's TAP) 5833. The financial aid office integrates these state awards into your institutional package.

- Institutional Aid (The Differentiator): This is where colleges differ wildly. The college uses its own endowment, tuition revenue, and budget allocations to award need-based grants and merit-based scholarships 3258.

Because state and federal funding partnerships vary drastically across the country, and because colleges have vastly different endowment sizes and enrollment goals, two different universities can receive the exact same ISIR for you but offer completely different financial aid packages 3260.

Unless a college is one of the rare institutions that guarantees to "meet 100% of demonstrated need," they are not legally obligated to fill your entire financial gap 32. Financial aid administrators use complex software models to distribute their limited institutional budget based on the college's strategic goals - whether that means attracting higher-scoring students, balancing out-of-state demographics, or prioritizing specific academic majors 3261.

When analyzing aid letters, families will typically encounter one of several distinct institutional packaging strategies:

| Packaging Strategy | How the College Awards Aid | Implications for the Student |

|---|---|---|

| Institutional Commitment Package | Uses massive institutional endowment grants to keep out-of-pocket costs extremely low, replacing student loans with grant aid. | Usually restricted to highly selective, wealthy colleges. Students see "no loan" or "100% full need met" guarantees 62. |

| Upfront Discount Package | Deploys a mix of federal aid and multiple internal scholarships early in the admissions cycle to reduce the "sticker shock." | Provides a clear picture of costs early on, though the final package may still leave a moderate funding gap the student must cover 62. |

| Heavy Borrowing Package | Relies almost entirely on standard federal aid (Pell Grants and basic federal loans) because the institution lacks the budget for internal scholarships. | Leaves a massive financial gap that families are forced to fill by taking on high-interest private student loans or federal Parent PLUS loans 62. |

| Low-Cost, High-Quality Package | Focuses on keeping the baseline Cost of Attendance (tuition) inherently low rather than offering large discounts. | Typical of community colleges and in-state public universities. Relies heavily on state and federal aid to cover the modest costs 62. |

Once the software finishes blending these federal, state, and institutional funds, the financial aid office generates the official aid offer letter, delivering the final verdict on what your education will actually cost.

The Ironclad Rules of Data Privacy: Who Can Actually See Your Data?

A lingering concern for many families who submit the FAFSA is privacy. Because the modern FA-DDX pulls highly sensitive tax data directly from the IRS, applicants frequently worry about who on a college campus has access to their financial background.

The reality is that FAFSA data is governed by an extraordinarily strict, overlapping web of federal privacy laws. College financial aid administrators do not view all data equally. Instead, they manage three distinct categories of data, each with its own legal framework 63:

| Data Category | What It Includes | Governing Law |

|---|---|---|

| Federal Tax Information (FTI) | Raw IRS data imported via the FA-DDX (e.g., AGI, taxes paid, untaxed pensions). | Internal Revenue Code (IRC) 6103 6334. |

| FAFSA Data | Self-reported demographics, plus derived indices like the SAI and Pell Grant eligibility status. | Higher Education Act (HEA) Section 483 6334. |

| Non-FAFSA Data | Institutional records, local scholarships, internal unmet need calculations, and academic records. | Family Educational Rights and Privacy Act (FERPA) 63. |

The golden rule for college administrators is that when these data types overlap, the most restrictive law applies 3063. Because the Internal Revenue Code (IRC) carries severe civil and criminal penalties for unauthorized disclosure, FTI is protected with absolute rigidity.

By law, your FTI can only be used and disclosed strictly for the "application, award, and administration of student financial aid programs" 346535. Colleges must apply the principle of "least privilege," ensuring that raw tax data is cordoned off and accessible only to specific financial aid personnel whose core job is to calculate and disburse funding 63.

This means your raw tax data cannot be casually shared across campus. Your academic advisor, your professors, the admissions office, and even the college's institutional research department are legally barred from accessing your FTI 3435.

If a college wants to use your data for broader student success initiatives - for example, an academic advisor wanting to know if you are Pell-eligible so they can refer you to a free textbook program - they cannot look at your raw tax data. They are only allowed to view "derived" FAFSA data (like your SAI or Pell status), and only if you provide explicit, written consent authorizing that specific disclosure 3435. Mass consent forms or blanket authorizations tucked into enrollment agreements are prohibited; consent must be gathered on a specific, case-by-case basis 6335.

The strictness of the IRC also creates massive hurdles for internal college research. While universities are permitted to use anonymized demographic FAFSA data to study campus trends regarding attendance, persistence, and graduation rates without student consent, they are absolutely prohibited from using FTI for research purposes - even if the data is stripped of identifying information 303334.

Furthermore, these privacy laws shield students from external investigations. Subpoenas from local or state law enforcement investigations do not override the Internal Revenue Code. If an investigator demands a student's file from a college, the financial aid office is required to heavily redact all FTI before handing over the records; investigators must subpoena the IRS directly to obtain tax records 31.

These restrictions have had unintended consequences, particularly for college access organizations. For decades, federal TRIO programs (which provide mentoring and support to low-income, first-generation students) utilized FAFSA data to identify and assist vulnerable students 36. However, under the new FUTURE Act interpretations, unless a specific TRIO program is actively determining a student's eligibility for a monetary grant, its counselors are completely barred from accessing FTI or FAFSA data without the student's explicit, written consent 433. TRIO advocates are currently lobbying Congress to amend the law to allow access for non-monetary support programs 36.

Bottom line

The transition of your data from a FAFSA submission to a final financial aid letter is a highly automated, deeply regulated process designed to pull exact tax metrics directly from the IRS and translate them into a standardized index of financial need. While the transition to the modernized FAFSA Processing System caused historic delays and severe algorithmic errors during the 2024-2025 cycle, the underlying architecture ensures that your sensitive tax information is protected by the strictest federal privacy laws and used exclusively for awarding aid. Ultimately, while your federal data sets your baseline eligibility, the specific college you choose relies on its own budget and strategic goals to determine exactly how much funding you will receive.