How to Compare College Financial Aid Letters Side by Side

The core strategy for accurately comparing financial aid offers is to standardize each award letter by identifying the comprehensive Cost of Attendance (COA) and subtracting only "gift aid" (grants and scholarships) to calculate the true "Net Price." To make an authentic apples-to-apples comparison of actual out-of-pocket expenses, families must systematically strip away loans and work-study from the "awarded" column, as these represent money that must eventually be repaid with interest or earned through labor. By calculating the Net Price independently, students can cut through institutional marketing jargon and accurately project their long-term financial obligations.

The High Stakes of Decoding Award Letters

For millions of high school seniors and their families, the euphoria of receiving a college acceptance letter is often swiftly followed by the profound confusion and anxiety of deciphering the accompanying financial aid award letter. In theory, this document is intended to be a transparent consumer counseling tool that helps families understand exactly how much a year of higher education will cost and how it can be financed 1. In practice, however, these letters frequently serve as highly engineered marketing and recruitment documents designed by enrollment managers to make an institution appear far more affordable than the underlying arithmetic suggests 1. The design of many financial aid award letters is driven primarily by the college's pecuniary interests, focusing on maximizing yield rates rather than protecting the student's long-term financial best interests 1.

The stakes of misunderstanding these documents are exceptionally high, carrying consequences that can echo throughout a student's adult life. Confusing award letters routinely disguise interest-bearing loans as "discounts," "awards," or "financial assistance," leading families to mistakenly assume their financial need has been fully met 2. Consequently, students and their parents unknowingly commit to tens of thousands of dollars in unexpected intergenerational debt 33. A comprehensive analysis conducted by the New America Foundation and uAspire, which performed a quantitative analysis of over 11,000 financial aid award letters and a qualitative review of 515 unique institutional letters, revealed a staggering lack of consistency and transparency across the higher education sector 34. The researchers found that financial aid is often fundamentally insufficient to cover the cost of college; for example, students who receive a federal Pell Grant are still left to cover a significant gap averaging nearly $12,000 per year 4.

Because financial aid frequently falls short, clear communication is essential, yet the uAspire/New America study exposed pervasive obfuscation 4. The study found that 70% of the analyzed letters grouped all forms of aid together, failing to provide definitions to indicate how grants (free money), loans (borrowed money), and work-study (earned money) differ mechanically and financially 3. Furthermore, 50% of the letters failed to specify clear next steps, such as how a student might go about declining an unwanted loan 3.

Without mandatory federal standardization - though tools like the Department of Education's College Financing Plan offer voluntary templates - institutions are largely free to use technical jargon, obscure bottom-line calculations, and omit critical living expenses 15. If families do not approach these documents with a forensic level of scrutiny, they risk making one of the largest financial decisions of their lives based on data that is, at best, opaque and, at worst, actively misleading.

What is the true cost of attendance?

To accurately evaluate any financial aid offer, the analyst must first establish the total cost of the education being offered. Every award letter should theoretically begin with a clear, unambiguous articulation of the Cost of Attendance (COA) 68. The COA is a federally recognized metric that represents the institution's estimated total cost for one year of enrollment, serving as the "sticker price" before any financial aid is applied 97. However, the uAspire and New America study found that more than one-third of institutions omit complete cost information from their award letters entirely, leaving students with no baseline to contextualize the aid they are being offered 48. Without a clearly stated COA, a $20,000 scholarship exists in a vacuum; it is highly valuable if the COA is $25,000, but dangerously inadequate if the COA is $75,000.

When the COA is provided, it is critical to distinguish between direct costs and indirect costs to understand what is actually owed to the bursar versus what must be budgeted for daily survival.

| Cost Category | Expense Type | Description and Billing Mechanism | Risk of Institutional Underestimation |

|---|---|---|---|

| Direct Costs | Tuition and Fees | The baseline, non-negotiable cost of academic instruction, facility maintenance, and mandatory campus services. Billed directly by the institution. | Low. These are fixed, published rates that colleges cannot easily manipulate without regulatory scrutiny 712. |

| Direct Costs | Room and Board (On-Campus) | The cost of housing and meal plans, specifically for students who choose to reside in on-campus dormitories and utilize university dining facilities 129. | Low to Moderate. Institutions may default to listing the cheapest, most restrictive room and meal plan, which may not be realistic for all students 710. |

| Indirect Costs | Books and Supplies | The estimated annual cost of required textbooks, laboratory materials, software licenses, and personal computers 711. | High. 62% of surveyed students felt that institutional estimates for books and supplies were unrealistically low 1. |

| Indirect Costs | Transportation | Travel expenses for commuting to campus daily or flying home during holidays for residential students 912. | High. Almost three-quarters (73%) of respondents in a major survey felt colleges underestimated transportation expenses 1. |

| Indirect Costs | Personal Expenses | Everyday living costs, including toiletries, laundry, entertainment, clothing, dependent care, and required student health insurance 1213. | High. These figures are highly subjective, and colleges frequently minimize them to artificially deflate the overall COA 1213. |

A common deceptive practice among some institutions is to list only direct costs on the award letter, making the college appear significantly cheaper 811. For example, a college might prominently display a direct cost of $35,000 for tuition and housing, while quietly omitting the $4,000 to $6,000 historically required for books, travel, and personal expenses. This systemic understatement of indirect costs forces students to rely on unexpected mid-semester borrowing or excessive work hours, which can ultimately derail their academic progress. Families must proactively seek out the full, unabridged COA - often found buried on the college's website or via the National Center for Education Statistics' College Navigator tool - to ensure they are comparing comprehensive budgets 1415.

What is the difference between grants, loans, and work-study?

Once the true COA is established, the next analytical step is to decode the components of the financial aid package itself. Financial aid is generally broken down into three distinct categories. Understanding the mechanical and financial boundaries between these categories is the single most important skill in evaluating an award letter, as mixing these categories leads to severe financial miscalculations 1020.

| Aid Bucket | Common Terminology | Financial Mechanism and Long-Term Implications |

|---|---|---|

| Free Money | Grants, Scholarships, Fellowships, Tuition Waivers, Pell Grants, FSEOG | Also known as "gift aid," this is capital that does not need to be repaid 1120. It functions as a true, permanent discount on the sticker price of the college. Grants are typically need-based, while scholarships are often merit-based, awarded for academic, athletic, or artistic achievement 621. |

| Earned Money | Federal Work-Study (FWS), Campus Employment | Also known as "self-help aid," this represents an opportunity to earn funds through part-time employment 616. Crucially, these funds do not reduce the upfront tuition bill. The student must secure a job, work the hours, and receive a bi-weekly paycheck, which is intended to subsidize indirect personal expenses 612. |

| Borrowed Money | Federal Direct Subsidized Loans, Federal Direct Unsubsidized Loans, Parent PLUS Loans, Private Loans | Also known as "self-help aid," this is capital that must be repaid with interest 711. While loans provide critical cash-flow assistance, they are a financing mechanism, not a discount 1117. Subsidized loans defer interest while the student is enrolled, whereas unsubsidized loans accrue interest immediately 621. |

The primary danger in reviewing these categories arises when institutions deliberately utilize opaque or highly abbreviated terminology. Without mandatory standardization, financial aid letters are frequently packed with technical jargon that even families with extensive experience in consumer finance find baffling 8. In the comprehensive New America and uAspire study, researchers documented an astonishing 136 different terms used by colleges to describe a standard Federal Direct Unsubsidized Loan 3.

Shockingly, 24 of those 136 terms did not even include the word "loan" 421. A family might review their letter, see a line item for "Fed Direct Unsub L" or "L. Stafford" for $5,500, and mistakenly assume it is a proprietary institutional grant 311. Any item bearing the terms "Sub," "Unsub," "Stafford," "Direct," "Promissory Note," or simply the abbreviation "L." indicates borrowed money that carries long-term financial consequences and origination fees 92418. Analysts and families must manually comb through the document, identify every line item, and explicitly cross out the word "Award" if it is attached to a loan, reclassifying it as consumer debt.

Calculating the "Net Price": The Only Metric That Matters

With the total Cost of Attendance identified and the aid stringently categorized into Free Money, Earned Money, and Borrowed Money, families must perform their own calculations to determine the actual affordability of the institution. Financial aid letters frequently highlight a "Net Cost" or "Out-of-Pocket Cost" at the very bottom of the page, but this figure is often mathematically engineered to be highly misleading 26.

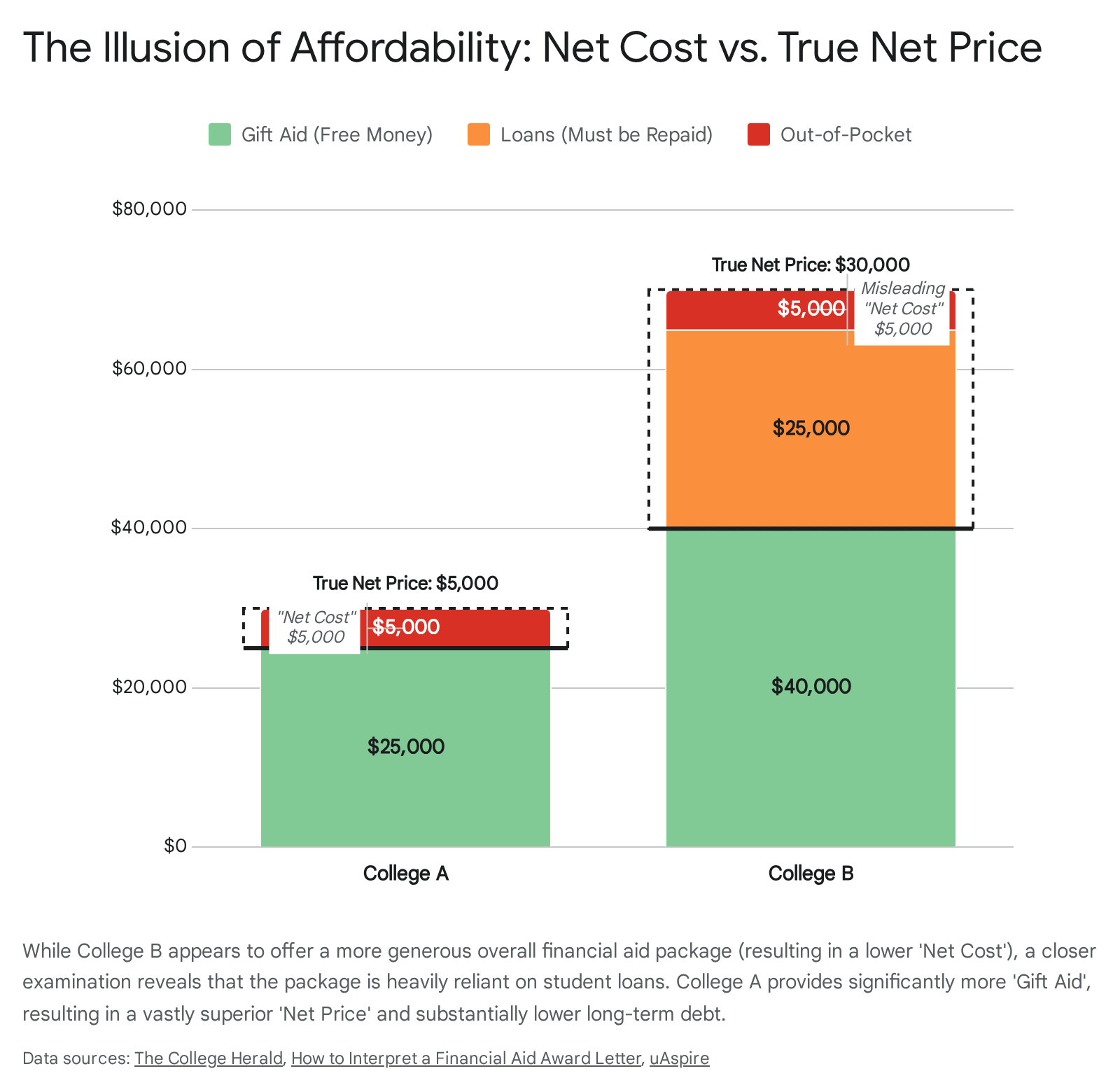

The concept of Net Cost is traditionally defined by institutions as the Total Cost of Attendance minus the entire financial aid package 1211. Because the entire financial aid package usually includes thousands of dollars in student loans, parent loans, and prospective work-study earnings, the Net Cost presents an artificially deflated number. For instance, a college might proudly boast a Net Cost of $0 on its award letter, but this mathematical zero is only achieved because the institution has aggressively packaged $5,500 in student loans and a $25,000 Parent PLUS loan into the award 2619. Loans absolutely do not cut college costs; they merely spread out the costs over time while compounding the financial burden through interest accrual 1117.

The only mathematically accurate and ethically sound metric for comparing the affordability of different institutions is the Net Price 1114.

The operative formula is straightforward but essential: Total Cost of Attendance (Direct + Indirect Costs) - Gift Aid (Grants & Scholarships) = Net Price. 1213

The Net Price represents the actual quantum of money the family must cover out of their own resources - whether through current income, liquidation of 529 savings accounts, or by making the conscious, informed decision to take on debt 1128.

Consider a practical example of two highly competitive offers, as illustrated by the data in the chart above. College A has a total COA of $30,000. They offer a $25,000 grant and no loans, leaving an apparent gap of $5,000. The Net Price is $5,000. College B has an exorbitant COA of $70,000. They offer a $40,000 grant, but also package $30,000 in student and parent loans. College B's award letter prominently displays a "Net Cost" of $0, making it seem like a full ride 26.

If a family only looks at the bottom line provided by the institutions, College B appears to be the superior financial decision. However, calculating the true Net Price reveals a starkly different reality: College A costs $5,000, while College B costs $30,000 ($70,000 COA minus $40,000 in free money). College B is simply expecting the student and their parents to borrow the massive $30,000 difference 26. By relying solely on rigorous Net Price calculations, families can safely ignore the marketing spin, strip away the illusion of affordability, and make financially sound, apples-to-apples comparisons 2020.

Navigating Misleading Practices and Common Misconceptions

Even armed with the correct Net Price formula, analysts and families must remain hyper-vigilant against several pervasive and highly deceptive practices employed by financial aid offices. These practices are designed to make enrollment appear more financially palatable in the short term, often at the expense of the student's long-term financial viability.

Treating Parent PLUS Loans as "Awards"

One of the most predatory practices identified by higher education researchers is the inclusion of Federal Direct Parent PLUS loans as standard line items in a student's financial aid package 24. In the New America study, nearly 15% of the analyzed letters packaged Parent PLUS loans as an "award," deliberately making the financial aid package appear far more generous than it really was 33.

This packaging strategy is profoundly misleading for several structural reasons. First, unlike undergraduate Stafford loans (which are tightly capped annually and require no credit check), Parent PLUS loans are taken out entirely by the parents, meaning the parent bears full legal and financial responsibility for repayment 119. Presenting intergenerational debt as a student award obscures liability. Second, Parent PLUS loans require an adverse credit history check; a parent with a recent bankruptcy, foreclosure, or severe delinquency may be summarily denied, rendering the carefully constructed aid package suddenly tens of thousands of dollars short with no immediate recourse 219. Third, PLUS loans inherently carry significantly higher interest rates and origination fees compared to standard undergraduate student loans 19. Presenting a $30,000 Parent PLUS loan alongside a $5,000 Pell Grant under the broad, comforting umbrella of "Financial Assistance" obscures the massive debt burden the family is being asked to shoulder 219.

Misunderstanding the Mechanics of Federal Work-Study

Federal Work-Study (FWS) is frequently misunderstood by first-time college applicants and their families, a confusion exacerbated by poor institutional communication. Seven in ten schools that offered work-study in the New America study failed to explain what the program actually was or how it differed materially from other types of aid 3. When an award letter includes a line item for "$3,000 in Federal Work-Study," families consistently and mistakenly assume this amount will be directly credited against the upcoming semester's tuition bill by the bursar's office 6.

In reality, a work-study award merely indicates that the student has federal authorization to apply for specific subsidized jobs on or near campus 6. The money is not guaranteed, and it is never deducted from direct costs. The student must actively hunt for a job, navigate the interview process, work the necessary hours alongside their academic schedule, and will eventually receive the funds gradually via a standard bi-weekly paycheck 6. Consequently, work-study funds should be mentally allocated exclusively toward paying for ongoing indirect costs - such as pizza, laundry, transportation, and personal supplies - rather than upfront direct costs like tuition and housing 6. Subtracting a prospective work-study allocation from the immediate tuition bill will result in a dangerous cash shortfall when the payment deadline arrives.

The "Front-Loading" of Grants

A particularly insidious tactic utilized by roughly half of all four-year colleges involves the "front-loading" of grants 1117. Front-loading occurs when an enrollment management algorithm offers a highly generous mix of grants and scholarships to an incoming freshman as a lure to secure their initial enrollment, only to drastically reduce that free money in the sophomore, junior, and senior years 1730.

This practice is effectively a bait-and-switch pricing model 1121. The resulting financial gap in subsequent years is typically filled by larger student loan requirements, trapping students who are already academically integrated into the institution and highly reluctant to transfer 1121. Unexpected price increases inequitably accrue to lower-income students, resulting in severe nonmonetary costs, ranging from chronic anxiety over money to an increased risk of dropping out entirely 21.

To detect front-loading before committing, families must aggressively scrutinize the terms and conditions of all institutional scholarships. Are they guaranteed for all four years? What specific GPA or credit-hour minimum must be maintained to renew them? 30 Furthermore, savvy applicants can utilize federal tools like the Department of Education's College Navigator to compare the average grant amount awarded specifically to first-year students versus the average grant amount awarded to the overall undergraduate population 22. A significant mathematical drop-off strongly indicates a systemic pattern of front-loading 22.

The Trap of Scholarship Displacement

Another critical misconception involves the treatment of outside, private scholarships (e.g., money won from the Rotary Club, corporate sponsors, or local foundations). Students labor under the assumption that winning a $5,000 private scholarship will automatically lower their Net Price by $5,000. However, due to federal over-award regulations and institutional policies known as "scholarship displacement," this is not always the case 1121.

If a student's total aid exceeds their demonstrated financial need, the financial aid office is required to reduce the aid package 21. Ideally, the college will reduce the student's loan burden or work-study expectation first 11. However, many institutions will systematically reduce their own institutional grants by the exact amount of the private scholarship won, leaving the student's Net Price completely unchanged despite their hard work in securing outside funding 1133. Families must explicitly ask the financial aid office about their scholarship displacement policies before assuming private awards will improve their bottom line 33.

Recent Developments: The 2024-2025 FAFSA Rollout Crisis

The landscape of higher education finance is currently experiencing a period of unprecedented structural volatility. The passage of the FAFSA Simplification Act represented the most significant overhaul of federal student aid processes in decades, fundamentally rewriting the formulas that govern eligibility 2324. However, the rollout of these changes created systemic chaos that continues to affect the timeline and formatting of recent award letters.

The rollout of the newly redesigned FAFSA for the 2024-2025 academic year was marred by severe technical glitches and catastrophic processing delays 2526. While the application traditionally opens seamlessly on October 1st of each year, the complex new form was delayed until late December 2023 2638. Subsequent calculation errors discovered by the Department of Education meant that colleges did not receive accurate Institutional Student Information Records (ISIRs) until mid-March or April of 2024 3940. This truncated timeline paralyzed financial aid offices, forcing many institutions to push back their traditional May 1 National Candidates Reply Date, leaving millions of families in limbo, forced to make high-stakes enrollment decisions with compressed timelines and severely delayed award letters 2526.

Beyond the operational failure of the rollout, the FAFSA Simplification Act introduced permanent mechanical changes to how aid is calculated:

- From EFC to SAI: The familiar Expected Family Contribution (EFC) metric has been permanently retired and replaced by the Student Aid Index (SAI) 2327. Unlike the EFC, which bottomed out at $0, the SAI can drop to a negative -1,500 2428. This negative index allows financial aid administrators to more accurately segment and identify students with the most extreme, profound financial need 2829.

- Removal of the Sibling Discount: Controversially, the new SAI formula no longer provides a division of parent contribution for families with multiple children enrolled in college simultaneously 2329. This shift has significantly altered the net price expectations for middle-income families with overlapping college-aged children, who previously relied on this discount 2426.

- Pell Grant Expansion: The legislation expanded Federal Pell Grant eligibility by linking it directly to family size and federal poverty guidelines, rather than just the complex need-analysis formula 2829. This structural change automatically guarantees maximum Pell Grants for some low-income students and is expected to expand access to hundreds of thousands of previously ineligible applicants 2438.

The 2026 "One Big Beautiful Bill Act" (OBBBA) Paradigm Shift

Looking forward, the financial aid environment will experience another seismic shift on July 1, 2026, when the sweeping provisions of the newly enacted "One Big Beautiful Bill Act" (OBBBA) take effect 443046. Signed into law on July 4, 2025, this legislation radically alters federal borrowing limits and repayment paradigms 4430. Consequently, award letters issued for the Fall 2026 semester and beyond will look structurally different, heavily restricting access to federal liquidity.

| OBBBA Provision | Legacy Policy (Pre-July 2026) | New Policy (Effective July 1, 2026) | Impact on Borrowers |

|---|---|---|---|

| Parent PLUS Loan Limits | Parents could borrow up to the total Cost of Attendance (minus other aid) with no absolute dollar cap 4631. | Strictly capped at $20,000 per academic year per dependent student, with a hard $65,000 lifetime aggregate maximum 4632. | Families relying on massive Parent PLUS loans to bridge the gap at expensive private institutions will face severe cash shortfalls 4633. |

| Graduate PLUS Loans | Graduate students could borrow up to the full Cost of Attendance via Grad PLUS loans 4446. | Eliminated entirely for new borrowers. Graduate students are restricted to Unsubsidized Stafford loans 3046. | New annual limits of $20,500 for general graduate degrees and $50,000 for specific professional degrees, imposing strict borrowing ceilings 4446. |

| Part-Time Loan Proration | Students could often access full annual loan limits regardless of specific credit load 3334. | Federal loans are treated as annual loans based on a 24-credit year. Loan amounts must be reduced proportionally for less-than-full-time enrollment 3334. | Part-time students will have significantly less access to federal loan liquidity per semester 3335. |

| Repayment Plans | A complex maze of Income-Driven Repayment (IDR) plans (SAVE, PAYE, ICR, IBR) 4652. | New borrowers are restricted to a Tiered Standard Plan or the new Repayment Assistance Plan (RAP) 4653. | RAP caps monthly payments at 1% to 10% of AGI, eliminates negative amortization, but extends the timeline to 30 years for forgiveness 5336. |

The implementation of OBBBA represents a fundamental philosophical shift by the federal government to curb runaway student and parent debt by choking off unlimited borrowing. For parents, the $20,000 annual cap means that an award letter featuring a $40,000 gap can no longer be solved simply by signing a master promissory note 3237. Families must pivot their strategies toward more affordable state schools, community colleges, or institutions with massive endowments capable of meeting full demonstrated need without loans 4656.

It is vital to note that OBBBA includes specific legacy provisions. If a parent or graduate student borrowed a federal loan prior to July 1, 2026, for a specific program of study, they are generally grandfathered into the old rules. They may continue borrowing under the previous limits for up to three additional academic years, or until they complete their expected credential, whichever is less 4632.

Can I negotiate or appeal my financial aid offer?

Many families mistakenly view a financial aid award letter as a final, non-negotiable contract akin to a retail price tag. In reality, the Higher Education Act of 1965 grants financial aid administrators the statutory authority to adjust the underlying data elements on a student's FAFSA to accurately reflect changes in a family's financial reality 5738. This formal administrative process is known as a "Professional Judgment" (PJ) or special circumstances review 5739.

The necessity of Professional Judgment stems from the inherent lag in FAFSA data collection. The FAFSA relies on "prior-prior year" tax data 2857. For a student entering college in the Fall of 2024, the FAFSA utilized tax returns filed for the 2022 calendar year 28. If a family experienced significant financial turbulence in the intervening two years - such as a pandemic-related layoff or a severe medical crisis - the Student Aid Index (SAI) generated by the FAFSA will drastically overstate their current ability to pay 57.

A financial aid appeal should never be approached as a negotiation or haggling session; one cannot ask for a discount simply because another college offered a better package or because the family feels they "deserve" more aid 3960. Instead, it is a formal, evidence-based request for a recalculation based on documented special or unusual circumstances 3839.

Valid grounds for a Professional Judgment appeal include: * Recent, involuntary job loss, significant reduction in income, or termination of employment 5760. * The death, divorce, or legal separation of the student's parents after the FAFSA was formally filed 60. * Excessive, unreimbursed medical or dental expenses that consume a disproportionately large percentage of the family's Adjusted Gross Income (often needing to exceed 11% of AGI to trigger a review) 5740. * The sudden end of child support, Social Security benefits, or alimony payments 60. * Unusual circumstances warranting a "dependency override." This applies to severe situations involving an abusive family environment, parental abandonment, or parental incarceration, which allows a student to bypass the requirement for parental financial data and file independently 3839. Crucially, a dependency override cannot be granted simply because parents refuse to contribute to college costs or refuse to fill out the FAFSA 38.

Executing a Successful Appeal: To initiate an appeal, the student must bypass the standard admissions office and contact the college's financial aid office directly as soon as the financial hardship is identified 5760. The process generally requires submitting a formal, concisely written financial aid appeal letter that explains the timeline of events, emphasizing that the financial shock is completely outside of the family's control 6040.

The paramount requirement for a successful appeal is rigorous, irrefutable third-party documentation 3860. A financial aid officer, operating under strict federal audit guidelines, cannot act on a narrative alone. Families must provide termination letters, unemployment benefits statements, finalized divorce decrees, death certificates, or detailed medical billing receipts 5760. For dependency overrides, letters from third parties with direct knowledge of the situation - such as social workers, high school guidance counselors, clergy, or law enforcement - are strictly required 3860. While initiating an appeal does not guarantee the disbursement of additional grant money, financial aid officers are bound by their professional mission to support college access, and a meticulously documented Professional Judgment can yield thousands of dollars in previously inaccessible aid 357.

Bottom line

A financial aid award letter is a complex, high-stakes financial document that requires active, highly critical decoding. By stripping away disguised student loans and unearned work-study promises, analysts and families can calculate the true Net Price (Total Cost of Attendance minus Gift Aid) to ensure they are comparing institutional affordability on an equal, mathematical footing. Families must remain vigilant against pervasive deceptive practices, such as the packaging of Parent PLUS loans as awards or the algorithmic front-loading of grants. Furthermore, families must factor in sweeping legislative changes like the OBBBA borrowing caps, which permanently alter the availability of federal liquidity. When armed with these analytical tools, an understanding of the true cost of attendance, and knowledge of the Professional Judgment appeals process, students and their families can successfully navigate the opaque higher education pricing structure and avoid the devastating trap of unmanageable, long-term debt.