Go-to-market motions for AI-native B2B products in 2026

Executive Summary

The transition from traditional Business-to-Business (B2B) Software-as-a-Service (SaaS) to AI-native enterprise architectures has catalyzed a fundamental restructuring of go-to-market (GTM) motions in 2026. After years of unchecked experimentation, the enterprise market has entered an era of rigid accountability. Buyers are no longer purchasing potential or conversational novelty; they are purchasing verifiable, automated business outcomes 12. This paradigm shift has rendered the foundational sales and marketing playbooks of the 2010s completely obsolete. Top-tier venture capital firms and enterprise analysts uniformly note that the next trillion-dollar organizations will operate as software companies masquerading as services firms, capturing massive labor budgets rather than remaining constrained by traditional IT budgets 34.

This exhaustive research report delivers a comprehensive analysis of the evolving AI-native B2B landscape. It delineates the diverging GTM requirements across horizontal, vertical, and infrastructure architectures, mapping them directly to Product-Led Growth (PLG), sales-assisted, and API-first motions. The analysis explores the terminal decline of per-seat pricing in favor of outcome-based and consumption-driven models, detailing the profound downstream effects on sales compensation, quota structures, and revenue operations. Furthermore, the report calls out and debunks pervasive misconceptions regarding the application of legacy SaaS financial benchmarks to AI unit economics, providing a recalibrated view of customer acquisition costs, payback periods, and gross margins. It meticulously deconstructs the enterprise sales lifecycle to address the persistent failure mode known as "pilot purgatory," offering a structured pathway from proof-of-concept to production. Finally, the research examines how international regulatory frameworks, spearheaded by the European Union's Artificial Intelligence Act and contrasted against fragmented United States and Asian frameworks, are forcing global vendors to localize their GTM strategies around trust, auditability, and compliance-by-design.

Architectural GTM Differentiation: Horizontal, Vertical, and API-First Plays

The monolithic approach to software distribution has permanently fractured. Enterprise AI adoption is no longer about deploying isolated tools; it is about deploying the correct architectural layer to solve specific business problems 1. Consequently, GTM strategies must be purpose-built for the specific nature of the artificial intelligence being sold. The distinction between horizontal AI, vertical AI, and API-first infrastructure dictates the target buyer, the sales velocity, the implementation methodology, and the underlying unit economics of the vendor. Modern sales organizations must align their motions - Product-Led Growth (PLG), Sales-Assisted, and API-first - to these distinct architectural realities.

Horizontal AI and the Product-Led Growth (PLG) Motion

Horizontal AI systems act as general-purpose agents designed to operate across multiple functions, teams, and industries 67. They serve as the connective tissue - or the "map" - of an organization, breaking down data silos and enabling enterprise-wide knowledge discovery, content generation, and routine task automation 17. Because horizontal AI is highly adaptable and requires minimal domain-specific fine-tuning initially, the optimal GTM strategy is overwhelmingly driven by Product-Led Growth (PLG) and bottom-up adoption.

The PLG motion relies on a high-velocity distribution model targeting the end-user or department head seeking immediate productivity gains 89. Time-to-value is exceptionally short, often measured in minutes or days, as foundational models require minimal bespoke configuration to begin generating outputs 78. Procurement friction at this stage is remarkably low, frequently bypassing heavy IT scrutiny via department-level credit card swipes or freemium adoption funnels. However, the strategic vulnerability of horizontal AI lies in its defensibility. Because horizontal platforms rely on generalized foundational models, they often lack the deep, proprietary industry nuance that creates structural business moats 67. The PLG GTM strategy must therefore focus on rapid land-and-expand motions. The objective is to embed the horizontal agent into as many cross-functional workflows as possible before enterprise procurement teams step in to consolidate shadow IT into a single vendor of record.

Vertical AI and the Sales-Assisted Enterprise Motion

In stark contrast, vertical AI systems are purpose-built for specific industries or highly specialized organizational functions. They act as the "engine," driving targeted insights, regulatory compliance, and deterministic automation in complex areas such as clinical diagnostics, legal contract adjudication, supply chain optimization, and financial risk assessment 168. Vertical AI integrates domain-specific knowledge, curated proprietary datasets, and human-in-the-loop (HITL) validations to secure high-stakes decisions 8.

The GTM strategy for vertical AI necessitates a top-down, Sales-Assisted enterprise motion. Selling a vertical AI solution is a deeply consultative process that engages C-suite executives, Chief Compliance Officers, and line-of-business leaders 211. Because vertical AI often redesigns entire workforce roles and ingests sensitive, high-value data, the procurement friction is intensely high 8. Time-to-value is elongated, typically ranging from six to twelve months, due to the necessity of complex systems integrations, algorithmic fine-tuning upon the client's proprietary data, and rigorous security and compliance evaluations 8.

Despite the slow sales velocity, the defensibility of vertical AI is unmatched. Once embedded, the proprietary data flywheels generated by specialized execution create an insurmountable competitive moat 8. This yields exceptional net revenue retention (NRR) and significant vendor lock-in. The Sales-Assisted motion relies heavily on forward-deployed engineers and solution architects who can map the AI's capabilities directly to the client's specific operational bottlenecks, effectively functioning as an extension of the client's own engineering and operations teams.

API-First Infrastructure and Developer-Led Motions

API-first companies and infrastructure providers supply the foundational compute, routing logic, and intelligence primitives upon which both horizontal and vertical applications are built 1. This category encompasses foundational large language model (LLM) providers, vector database vendors, embedding providers, and complex orchestration frameworks.

The GTM motion for API-first plays targets a highly technical buyer: developers, data scientists, and engineering leadership. The sales strategy centers on programmatic consumption, self-serve onboarding, and ecosystem building. Traditional marketing collateral is entirely replaced by comprehensive technical documentation, developer relations initiatives, and community advocacy. Revenue expansion in the API-first model is highly organic and frictionless; as the customer's downstream application scales in end-user adoption, their programmatic consumption of the underlying infrastructure API scales proportionally 1213. However, this model subjects the vendor to highly volatile compute-margin impacts, necessitating strict attention to infrastructure cost of goods sold (COGS) and dynamic rate-limiting to prevent unprofitable execution 214.

Architectural Motion Comparison

The distinct characteristics of these three AI paradigms require entirely different operational and financial frameworks. The following table synthesizes the core differences across GTM motions, target buyers, value realization timelines, procurement friction, and the ultimate impact on compute margins.

| GTM Motion | Architectural Alignment | Target Buyer Persona | Time-to-Value (TTV) | Procurement Friction | Compute-Margin Impact |

|---|---|---|---|---|---|

| Product-Led Growth (PLG) | Horizontal AI (Generalist) | End-users, Department Heads, RevOps, Marketing Leaders | Fast (Minutes to Days): Broad utility allows immediate deployment and self-serve onboarding. | Low: Often bypasses IT scrutiny initially via individual credit card adoption or freemium tiers. | Medium: Generalized inferences can be batched, but free-tier abuse requires aggressive cost capping. |

| Sales-Assisted | Vertical AI (Specialist) | C-Suite, Chief Compliance Officers, Specialized LOB Leaders | Slow (6-12 Months): Requires deep system integration, workflow redesign, and extensive compliance auditing. | High: Intense security reviews, data privacy auditing, and complex indemnification and liability negotiations. | High: Specialized fine-tuning, continuous retrieval-augmented generation (RAG), and custom retraining degrade baseline margins. |

| API-First | Infrastructure & Primitives | Developers, Data Scientists, CTOs, Engineering VPs | Variable: Immediate for sandbox prototyping; extensive for production-grade enterprise scaling. | Low (Entry) / High (Scale): Frictionless initial access; rigorous architecture review when scaling to enterprise usage. | Extreme: Margins are directly tied to raw compute/GPU costs and are highly sensitive to sudden usage spikes and token processing volumes. |

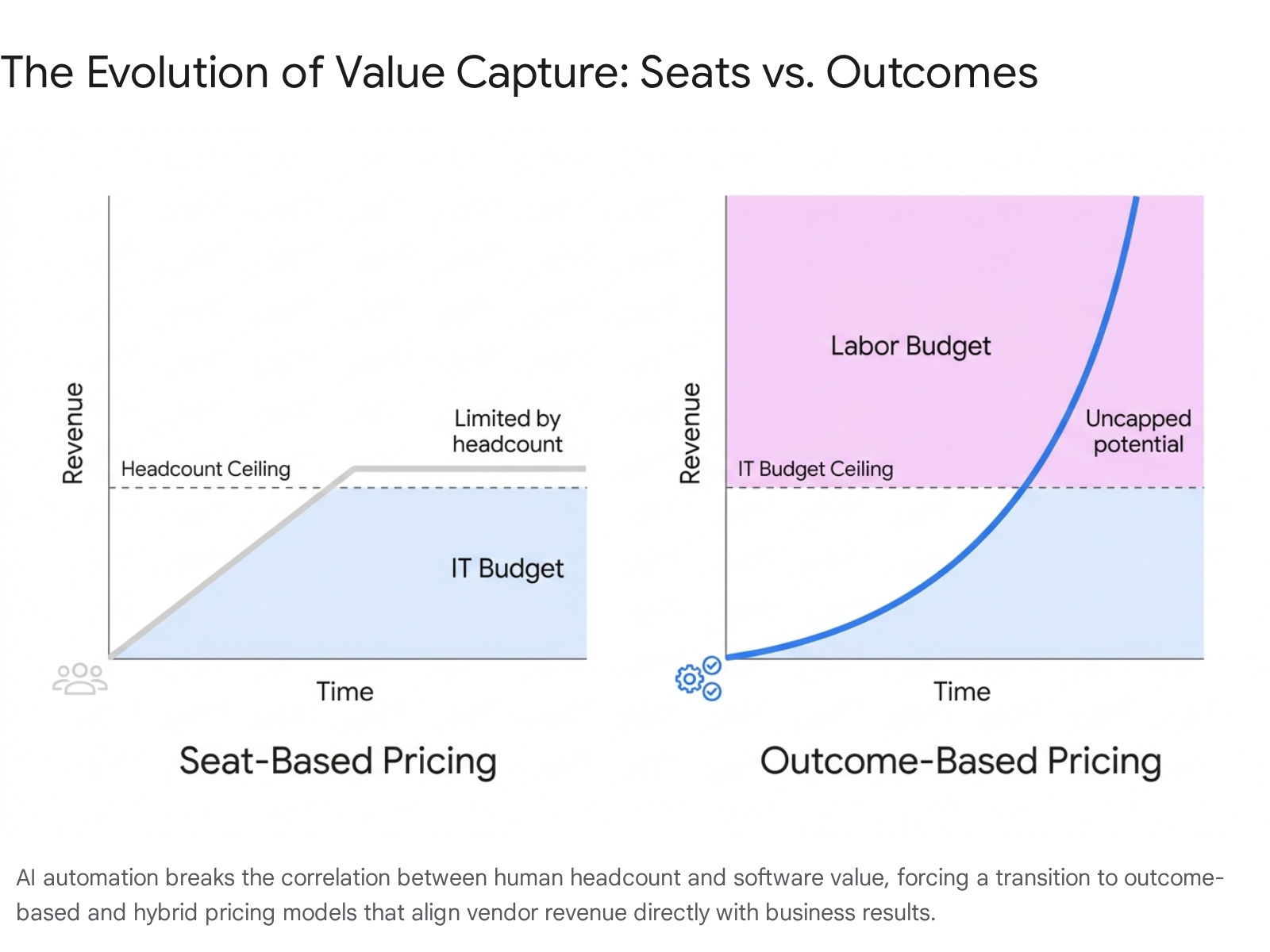

The Monetization Paradigm Shift: From Seats to Outcomes

For over two decades, the B2B software industry operated on a simple, predictable mathematical premise: organizational growth equals headcount growth, which naturally equals more software seats, thereby driving compounding vendor revenue 15. Artificial intelligence has permanently decoupled software value from human headcount. When a single autonomous agent can execute the workload of ten human analysts, charging a fixed licensing fee per human user fundamentally undervalues the software and catastrophically misaligns the vendor's economic incentives 1516.

As a result, the enterprise landscape of 2026 is witnessing the aggressive and terminal decline of traditional seat-based pricing among AI-native organizations. Leading venture capital firms, including Sequoia and Bessemer Venture Partners, note that the most successful AI startups are rapidly abandoning access-based monetization in favor of models that scale proportionally with verified value creation and underlying infrastructure consumption 1214. This transition is manifesting in three primary forms: usage-based consumption models, outcome-based pricing models, and sophisticated hybrid monetization bridges.

Usage-Based and Token Consumption Models

Usage-based pricing charges customers strictly for the raw utility they consume, typically measured in tokens processed, API calls executed, or raw compute hours logged 21214. This model inherently protects the vendor's gross margins because top-line revenue scales perfectly in tandem with the expensive computational workloads required by deep learning models 14. The cost of goods sold (COGS) in AI is non-trivial; unlike traditional SaaS where an additional user costs virtually nothing to host, every single AI inference incurs a real-time expense on the backend 2. Token costs have fluctuated, with analyses noting massive declines from early 2023 to 2026, yet the aggregate volume of consumption demands strict metered billing 17.

While highly favored by API infrastructure providers and technical buyers who intrinsically understand the correlation between data tokens and programmatic value, pure consumption pricing introduces severe friction for standard enterprise buyers 218. Chief Financial Officers demand budget predictability above all else 2. A pricing model that fluctuates wildly based on unpredictable end-user querying creates a massive risk of "bill shock" and can perversely disincentivize platform adoption, as organizations fear runaway costs 218. Consequently, while token-based pricing remains the undisputed standard for the API-first infrastructure layer, application-layer vendors are evolving toward much more sophisticated, business-aligned metrics.

Outcome-Based Pricing: Capturing the Corporate Labor Budget

The most profound monetization shift in 2026 is the rapid maturation and adoption of outcome-based pricing. Under this paradigm, enterprise customers do not pay for software access, nor do they pay for the computational attempt to complete a task; they pay exclusively when the software delivers a verified, measurable business result 17320.

Vendors are successfully redefining their fundamental unit of value from "software access" to "completed work" 13. This is central to Sequoia Capital's "Services: The New Software" thesis, which argues that AI has crossed the threshold for handling deterministic intelligence work, shifting the winning enterprise model from selling tools (copilots) to selling completed work (autopilots) 34. Customer support platforms, such as Intercom's Fin AI, are charging approximately $0.99 per successfully resolved ticket, completely assuming the performance risk 2153. Sierra, an AI customer service company, reportedly achieved $100 million in annual recurring revenue in less than two years leveraging a strict outcome-based pricing approach 15. Sales development platforms are charging per qualified meeting booked, while fintech vendors are entering revenue-sharing agreements based on AI-driven product recommendations 17.

By tying revenue directly to verifiable return on investment (ROI), outcome-based pricing allows software companies to bypass constrained IT budgets and tap directly into massive corporate payroll and operational budgets, a transition Bain & Company estimates represents a largely untapped $100 billion opportunity 3174.

However, executing outcome-based pricing requires immense operational discipline. The vendor must develop airtight contractual definitions of what constitutes a "successful outcome," build robust, tamper-proof telemetry to measure it, and absorb the raw compute costs of all failed attempts 220.

The Hybrid Compromise

Due to the margin volatility inherent in pure outcome models and the budget unpredictability of pure usage models, the prevailing standard for enterprise AI applications in 2026 is the hybrid pricing model 2163. Hybrid architectures blend a predictable base subscription - which guarantees baseline revenue for the vendor and access predictability for the buyer - with variable consumption or outcome tiers that capture the upside as the customer scales their automation workflows 216. For instance, a vendor might charge a $12,000 annual platform fee to cover fixed infrastructure and baseline support, bundled with an allotment of 1,000 successful task resolutions per month, with subsequent resolutions billed dynamically 16. This ensures vendors can cover their fixed infrastructure overhead while retaining the uncapped revenue expansion potential that defines elite net revenue retention 13.

Revolutionizing Sales Compensation for AI-Native GTM

The sudden obsolescence of static subscription pricing has triggered a cascading failure in legacy sales compensation and incentive structures across the technology sector. Historically, Account Executives (AEs) were compensated based on a flat percentage of the total Annual Contract Value (ACV) secured at the exact moment of closing 2324. When ACV was a fixed, predictable sum derived from the multiplication of licensed seats by a set duration, the commission calculation was a straightforward administrative task 23.

In a world dominated by post-closing usage models, token consumption, and variable autonomous outcomes, this legacy paradigm breaks down entirely. Sales professionals now secure enterprise commitments where the true financial value of the contract is entirely dependent on how heavily the client utilizes the AI over the subsequent twelve months 1323. This structural reality creates a severe misalignment: AEs invest extensive resources into complex, multi-threaded enterprise sales cycles, only to have their earnings delayed and tethered to post-sale adoption metrics that are outside their direct control 1323.

The Move to Margin-Based and Trailing Commissions

To adapt to this friction, forward-thinking revenue organizations are aggressively restructuring their incentive plans. One emerging, highly disruptive strategy is the shift from revenue-based commissions to margin-based compensation 25. Because AI compute costs are highly variable depending on the intensity of the specific workflow, raw top-line revenue does not accurately reflect the true profitability of a deal. Margin-based compensation aligns the sales representative intimately with the company's unit economics, incentivizing them to target highly profitable automation use cases, defend premium outcome pricing, and avoid aggressive discounting that would otherwise erode the already-thin gross margins of AI operations 25.

Furthermore, commission payouts are increasingly tied to trailing outcome delivery rather than upfront contract signatures 20. Organizations are blending fixed base salaries with phased variable payouts linked to specific customer consumption milestones, implementation success, and actual realized return on investment 172026. This compensation evolution has forced a tighter, systemic integration between the Sales and Customer Success functions, as revenue realization is now viewed as a continuous, shared operational responsibility rather than a discrete, isolated transaction 27.

Recalibrating OTE and Quota Ratios

The structural disruption in AI pricing has also forced a massive recalculation of On-Target Earnings (OTE) and quota expectations. Industry benchmarks indicate that the standard quota-to-OTE ratio remains anchored around a 5:1 multiple (meaning a rep with a $200,000 OTE is expected to retire $1,000,000 in annual quota) 2829. The typical compensation mix retains a 50/50 split between base salary and variable commission for mid-market and enterprise AEs, though some product-led growth companies operate closer to a 60/40 mix to reflect the self-serve nature of their funnels 2830.

However, beneath these top-line structural averages, a severe crisis of execution is evident across the industry. In recent benchmark periods spanning late 2024 through 2026, only 51% of Account Executives successfully achieved their quotas, a sharp decline from historical SaaS norms 2431. The difficulty of forecasting consumption, coupled with longer scrutiny cycles from buyers demanding verifiable ROI, means that the stated OTE is frequently an aspirational recruiting target rather than a realized median 24.

To mitigate corporate risk amid this uncertainty, a significant percentage of firms - between 45% and 50% - have reintroduced stringent clawback provisions into their compensation agreements, ensuring that unfulfilled consumption projections do not result in unrecoverable commission payouts 9. The complexity of managing these fluid, multi-tiered variables has driven rapid adoption of specialized, AI-native compensation software platforms that offer real-time payout transparency, anomaly detection, and human-readable explanations to maintain seller trust 243233.

Debunking the Legacy B2B SaaS Benchmark Myth

The financial frameworks, multiples, and key performance indicators (KPIs) used to value and evaluate B2B software companies for the past decade are fundamentally flawed when applied to AI-native businesses. The most pervasive misconception among executives and private market investors is the assumption that AI software economics seamlessly mirror traditional cloud software economics. They do not, and managing an AI firm against legacy SaaS benchmarks is a fast track to insolvency.

The Gross Margin Reality Check

Legacy SaaS operations were built on the profound economic principle of near-zero marginal costs. Once the core software codebase was written and deployed to the cloud, the cost to provision an additional human user was negligible, resulting in software gross margins that frequently exceeded 80% to 90% 2.

AI-native applications possess a fundamentally different, compute-heavy cost structure. Every user interaction, every query, and every automated workflow requires active, expensive computational power. Generative AI involves continuous token processing, retrieval-augmented generation (RAG) lookups against massive vector databases, and often human-in-the-loop (HITL) oversight for strict quality assurance 82. These highly variable costs drag typical AI gross margins down to the 50% to 60% range 2. If a vendor prices their software based on legacy SaaS margin expectations, their unit economics will collapse as customer usage scales. The foundational axiom that "delivering AI isn't free" requires companies to obsessively track compute costs from inception, proving profitability at the individual transaction and outcome level before scaling 2.

Re-evaluating Customer Acquisition Cost (CAC) and Payback Periods

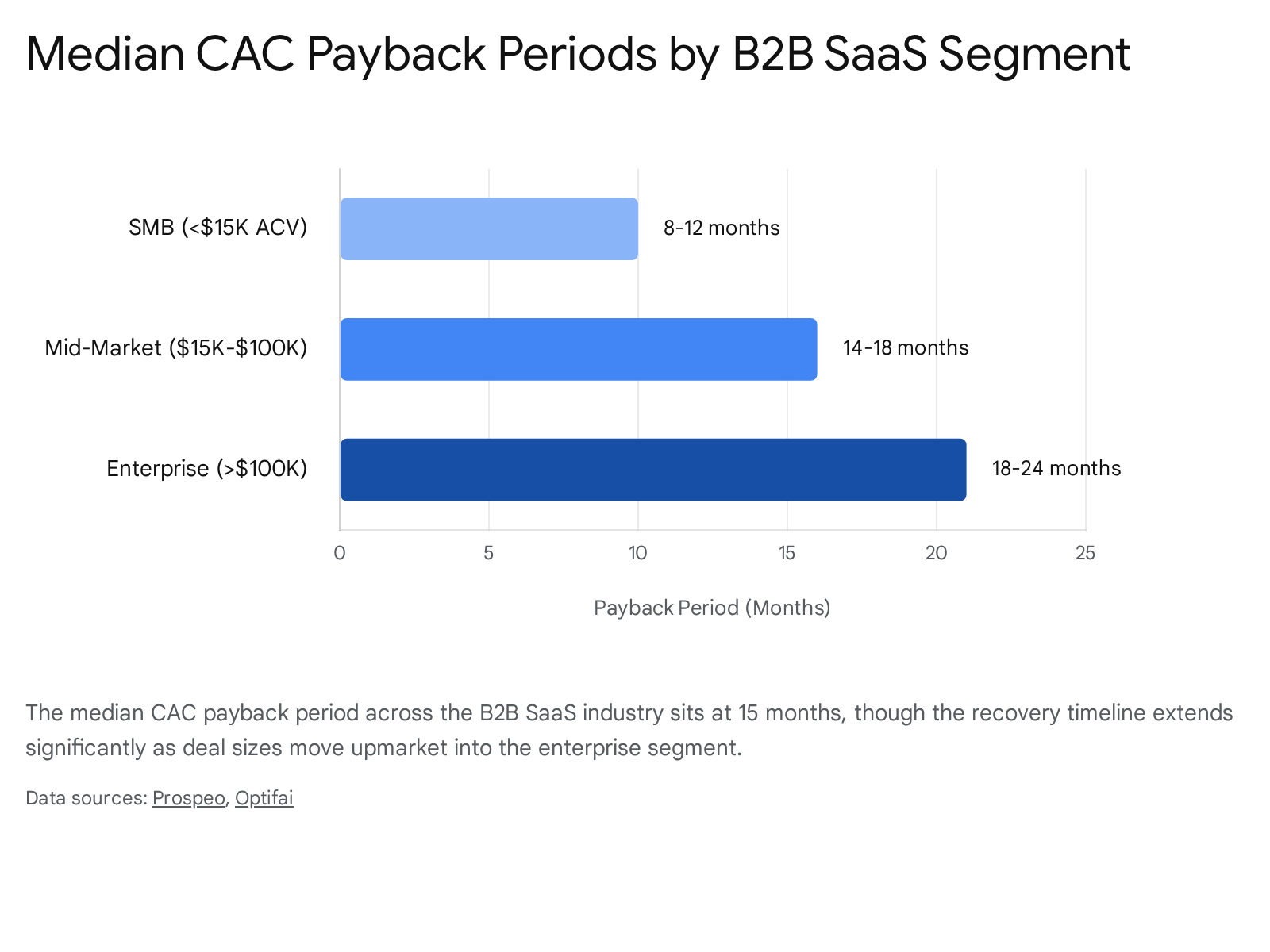

A secondary, highly dangerous misconception surrounds the cost of growth and the required speed of capital recovery. During the era of zero-interest-rate policy (ZIRP), SaaS operators tolerated extended Customer Acquisition Cost (CAC) payback periods, frequently accepting 18 to 24 months to break even on a new logo 3435. In the scrutinized 2026 funding environment, capital efficiency expectations have tightened severely. Investors now dictate a strict target payback period of under 12 months for best-in-class organizations, with the industry median hovering at 15 months 343536.

The disparity in acquisition costs across different GTM motions is striking and highlights the inefficiency of generalized benchmarks. In 2026, the median CAC for a self-serve, product-led SaaS motion is approximately $702, whereas enterprise sales-led CAC has surged past $11,400 34. This massive 16x gap is driven by elongated sales cycles, buying committees demanding extensive security proofs, and the rising compensation expectations of enterprise sales talent 34. Furthermore, the introduction of AI-powered buyer bots means prospects are pre-screening vendors autonomously, forcing marketing teams to invest heavily in expensive signal-based targeting and dynamic data enrichment just to get a human meeting 3738.

To survive, organizations must acknowledge that blended CAC metrics obscure the dangerous reality of their paid acquisition channels. The focus must pivot to optimizing the LTV:CAC (Lifetime Value to Customer Acquisition Cost) ratio, maintaining a strict floor of 3:1, while leveraging AI automation internally to drive down the cost of pipeline generation and outbound prospecting 343639.

Beyond the Rule of 40 to the Rule of X

The classical "Rule of 40" - whereby a healthy software company's growth rate plus its profit margin should equal or exceed 40% - is actively being challenged by top-tier analysts 2540. Investors are pivoting toward the "Rule of X," which applies a higher multiplier (often 2x to 3x) to the growth rate component, reflecting the massive premium placed on rapid scale in a winner-takes-most AI landscape 40. For context, the Bessemer Venture Partners Cloud Index notes a Rule of X benchmark of 80% for the top decile of cloud investments 40. While AI natively increases variable COGS, it simultaneously promises to drastically reduce the fixed operational costs of Research & Development and internal Sales & Marketing 9. As autonomous agents compress internal corporate labor costs, AI-native companies have the potential to achieve massive EBITDA expansion, fundamentally altering the trajectory of software profitability and rewarding organizations that prioritize exponential growth 9.

Deconstructing the POC-to-Production Sales Lifecycle

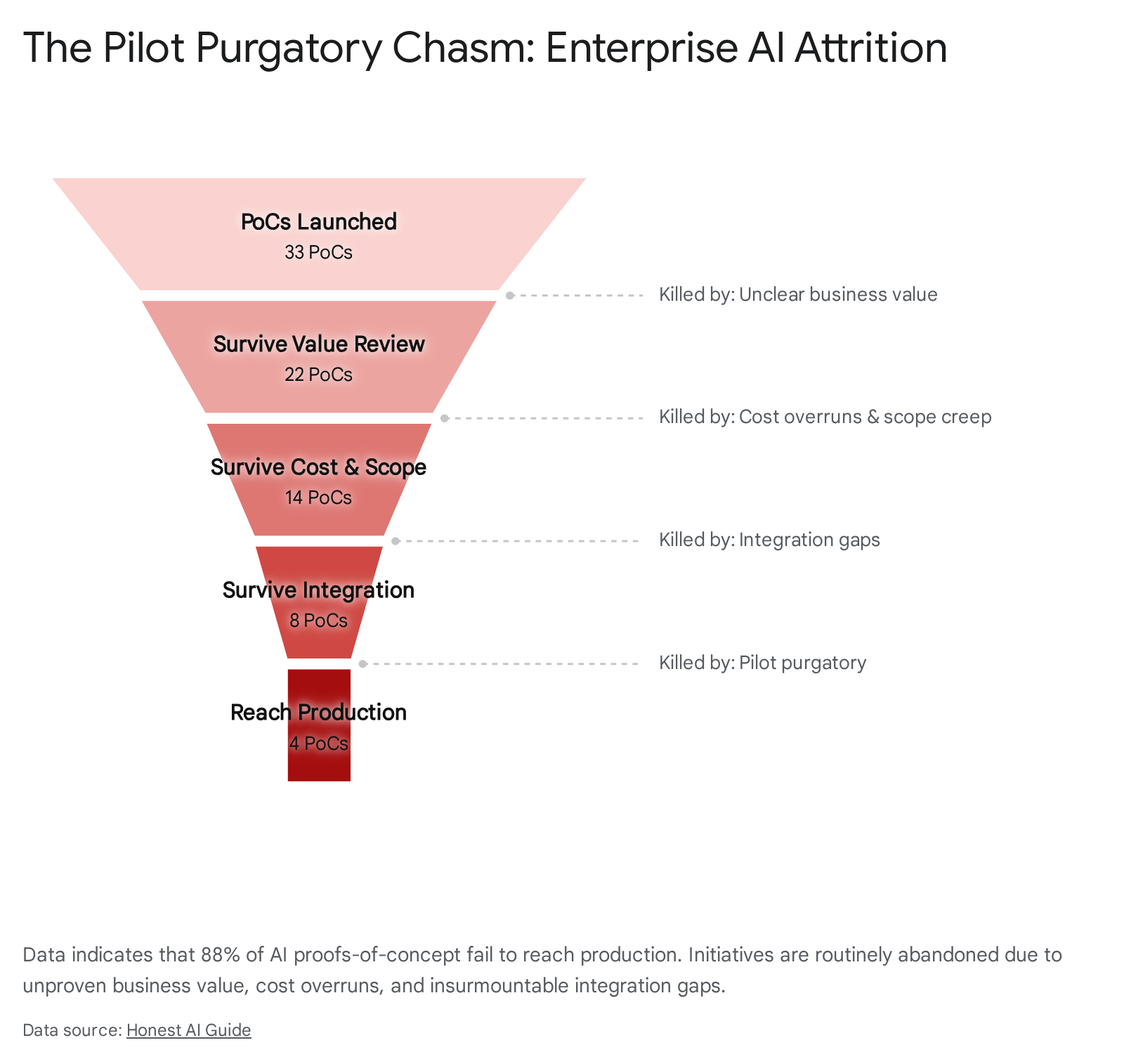

The most significant bottleneck in enterprise AI adoption is not technological capability or model intelligence; it is organizational execution. Current industry data reveals a staggering failure rate: between 87% and 88% of all enterprise AI initiatives fail to progress beyond the testing phase into live production 4142. An analysis by IDC highlighted that for every 33 AI proofs-of-concept (PoCs) a company launches, only 4 actually graduate to production 42.

This phenomenon has birthed a vast, expensive graveyard of well-funded, well-intentioned initiatives known universally across the industry as "pilot purgatory" 11424344.

The Crisis of Pilot Purgatory

Pilot purgatory is characterized by a state of indefinite corporate experimentation. An organization runs multiple localized PoCs that consume immense budget, leadership attention, and technical resources, yet never graduate to operational deployment because they cannot prove scalable ROI 4345.

The failure modes leading to this purgatory are highly predictable and rarely stem from model failure. They are rooted in complexity overload, capability gaps, resource constraints, and systemic change resistance 43. Fundamentally, they stem from a confusion between a scientific experiment designed to answer "Is this theoretically possible?" and a robust software engineering project designed to answer "Is this reliable, secure, scalable, and compliant?" 46. Pilots frequently succeed in sterile, isolated sandbox environments with perfectly sanitized datasets, only to shatter immediately when exposed to the chaotic data quality, stringent latency requirements, and unyielding security policies of the live enterprise architecture 41425.

The Structured Six-Stage Deployment Framework

To successfully bridge the pilot-to-production chasm, enterprise GTM strategies must entirely abandon the traditional "demo-and-sell" motion. Selling enterprise AI requires a highly structured, rigorous deployment lifecycle. Best-in-class vendors execute a disciplined, six-stage framework to ensure survivability and enterprise scale 2.

The initiative must begin with comprehensive Discovery and Value Alignment. Vendors must identify a specific, high-friction workflow where AI can drive measurable financial impact. Success metrics and explicit "kill criteria" - inflection thresholds below which the project will be immediately aborted - must be established and agreed upon by executive sponsors before a single line of code is written 48.

Following discovery, vendors must conduct a rigorous Architectural Readiness Check to audit the client's existing data infrastructure. A pilot's performance is strictly bounded by the quality of the underlying enterprise knowledge layer; poor data lineage will instantly kill an AI deployment 49. This phase must also proactively address integration complexity and MLOps prerequisites to ensure the client can actually support the tool 416.

Once readiness is confirmed, the engagement moves to Secure-by-Design Prototyping. The PoC cannot be treated as a disposable toy or a lightweight lunch-menu bot. It must be built using production-grade security principles, integrating identity access management, role-based permissions, and data privacy controls from day one. Treating security as a "Day 2" problem is a primary, fatal cause of stalled deployments 51.

With a secure prototype, vendors execute a Shadow Pilot. Rather than deploying immediately to end-users, the AI agent is run silently in parallel with existing human-driven processes. This gathers vital baseline performance metrics, exposes unpredicted edge cases, and allows for the refinement of context engineering without risking live business operations or customer satisfaction 2.

The outputs of the shadow pilot are then subjected to a rigorous Measurement and Governance Review. The data is evaluated strictly against the predefined kill criteria established in step one. This includes an uncompromising review of model accuracy, the variable cost-per-transaction, and adherence to all compliance protocols 4852. Only upon mathematically satisfying these metrics does the project proceed.

The final stage requires Enterprise Integration and Scaling, embedding the AI directly into the live workflow ecosystem. This demands continuous observability, anomaly detection dashboards, automated fallback procedures, and robust organizational change management to ensure human operators trust, adopt, and collaborate with the new autonomous system 4248. Vendors who master this lifecycle transition from selling software tools to selling verified business impact, successfully escaping purgatory.

Regional Privacy Regulations and Localized GTM Strategies

As AI capabilities have rapidly advanced, global regulatory scrutiny has intensified proportionately, fundamentally altering how enterprise software is bought, sold, and deployed. The vanguard of this regulatory shift is the European Union's Artificial Intelligence Act (AI Act), which officially entered into force in August 2024, with full enforcement of its high-risk provisions taking effect in August 2026 5354.

The AI Act is not merely a regional policy exercise; it is a strict, comprehensive liability framework that enforces the "Brussels Effect." It exerts broad extraterritorial reach over any organization that places an AI system on the EU market or utilizes the output of an AI system within the EU, entirely regardless of where the vendor's geographic headquarters are located 54756.

Categorization and Compliance Burdens in the EU

The EU legislation establishes a rigid four-tier, risk-based classification system that directly dictates a vendor's GTM requirements and potential legal liabilities. Systems posing an "unacceptable risk," such as social scoring or subliminal manipulation, are outright prohibited 5356. "Minimal" and "limited" risk systems face lighter, yet mandatory, transparency requirements, such as explicitly notifying users when they are interacting with an AI chatbot or viewing AI-generated content (enforced via Article 50 starting in August 2026) 5357.

The profound impact on B2B sales lies within the "high-risk" classification. High-risk systems encompass AI utilized in critical, consequential areas such as employment screening, healthcare access, educational grading, and biometric categorization 5658. Providers and deployers of high-risk AI are legally mandated to implement exhaustive risk management protocols, maintain rigorous data quality standards, generate highly detailed technical documentation, ensure continuous human oversight, and register their systems in an EU database prior to deployment 53759. Non-compliance carries devastating financial penalties of up to €35 million or 7% of a company's global annual turnover, making it a board-level risk 53.

Fragmented Frameworks in the US and Asia

The monolithic, centralized approach of the European Union contrasts sharply with the regulatory frameworks emerging in the United States and Asian markets. In the US, AI regulation remains highly fragmented, driven by a patchwork of state-level legislation (such as the Colorado Artificial Intelligence Act) and hyper-localized ordinances (such as the New York City AI Bias Law) 7. Furthermore, US regulation relies heavily on sector-specific guidance rather than a universal standard; for example, the FDA heavily regulates AI in medical devices, while the Federal Reserve enforces SR 11-7 model risk management guidelines for financial institutions 18.

This divergence forces global vendors to localize their GTM strategies drastically. A uniform, global sales narrative is no longer viable. In the US market, GTM teams must adopt an agile, verticalized approach, demonstrating compliance with specific sectoral frameworks. In the EU, however, trust must be built through demonstrable architectural compliance across the board, utilizing secure enclaves, exhaustive algorithmic explainability, and comprehensive control catalogs 60.

Transforming Enterprise Procurement into a Strategic Moat

This bifurcated regulatory environment has effectively weaponized the enterprise procurement process. By 2026, compliance is no longer an afterthought negotiated post-sale by legal teams; it is an absolute prerequisite for market entry 61. EU-based enterprise buyers are systematically embedding stringent transparency, auditability, and traceability obligations into their standard vendor contracts, demanding AI Act compliance documentation within tight procurement windows 5861.

For global AI vendors, this necessitates a localized, highly defensive GTM strategy. Sales cycles are increasingly stalled by procurement teams demanding proof of training data provenance and risk assessments 5860. Vendors who fail to proactively prepare these "control catalogs" find themselves entirely locked out of the European market, or subjected to emergency consulting fees that obliterate deal margins 58. Furthermore, because there is no formal "EU AI Act certification," enterprise buyers have begun relying on secondary trust signals, such as the ISO 42001 certification for AI management systems, as a proxy for comprehensive governance 57. GTM teams must now position their technical documentation and governance frameworks as core product features, utilizing them as competitive differentiators against less mature vendors who simply cannot survive regulatory scrutiny.

Conclusion

The go-to-market landscape for B2B software in 2026 bears little resemblance to the playbooks of the previous decade. The integration of artificial intelligence has decisively moved past the realm of speculative technological hype and entered a demanding phase of ruthless operational execution. To survive and scale, organizations must recognize that AI alters the foundational mechanics of software economics, enterprise sales, and technical implementation.

Success requires abandoning antiquated, access-based per-seat pricing models and fully embracing the operational complexity of outcome-based and consumption-based monetization, which perfectly aligns vendor success directly with verified customer value. Revenue leaders must urgently restructure compensation plans to reward margin preservation and trailing outcomes rather than upfront bookings, ensuring that sales teams are economically incentivized to drive sustainable adoption and avoid the dreaded 2026 renewal cliff. Furthermore, GTM strategies must be meticulously tailored to the distinct deployment realities of horizontal, vertical, and API-first architectures.

Above all, escaping the pervasive trap of "pilot purgatory" demands the application of strict, uncompromising software engineering discipline to AI initiatives. Vendors must transition from selling exploratory experiments to delivering hardened, secure-by-design integrations that guarantee measurable business outcomes. In a global market increasingly governed by stringent, divergent regulatory frameworks like the EU AI Act, the ultimate competitive advantage lies not in building the most intelligent model, but in building the most trustworthy, accountable, and flawlessly executed go-to-market engine.