Go-to-market strategies for AI startups in 2026

Macroeconomic and Market Context

The artificial intelligence landscape in 2026 has transitioned from an era of unchecked experimentation and soaring infrastructure investment into a period characterized by rigorous financial discipline, enterprise consolidation, and a fundamental restructuring of software economics. Venture capital funding remains highly concentrated, with artificial intelligence startups capturing roughly 80% of venture dollars globally, translating to over $242 billion in 2025 alone 12. However, this aggregate funding obscures a polarized funding environment. Outsized mega-rounds for foundation model developers and compute infrastructure providers account for the vast majority of deployed capital, leaving early-stage application layer startups to navigate a highly competitive environment with elevated valuation thresholds and intense scrutiny on unit economics 234.

Simultaneously, the broader software-as-a-service (SaaS) market has experienced a severe deceleration. While companies projected growth rates of 35% in 2024, median private SaaS growth settled at 26%, with top-quartile growth declining from 60% in 2023 to roughly 50% 5. In early 2026, the software market saw a $1 trillion contraction as investors recognized that autonomous AI agents effectively eliminate the need for expanding human headcount, severely threatening the traditional per-seat licensing model upon which legacy SaaS was built 6. This structural shift has created a unique opening for agile, bootstrapped, and AI-native startups that can adapt to outcome-based pricing frameworks.

Despite the availability of venture capital for top-tier firms, the failure rate for AI startups remains severe. Data from 2026 indicates that approximately 40% of AI startups launched in 2024 have already ceased operations, representing a faster mortality rate than the historical software average 7. Across an analysis of 431 failed venture-backed companies, 43% cite poor product-market fit as the primary cause of failure, indicating that many founders build advanced capabilities without validating a specific, monetizable market need 6910. Consequently, the most effective go-to-market (GTM) strategies in 2026 are not predicated on horizontal model supremacy, but rather on vertical specialization, proprietary data integration, and demonstrable return on investment (ROI) that directly addresses hard business outcomes.

Go-to-Market Economics and Customer Acquisition

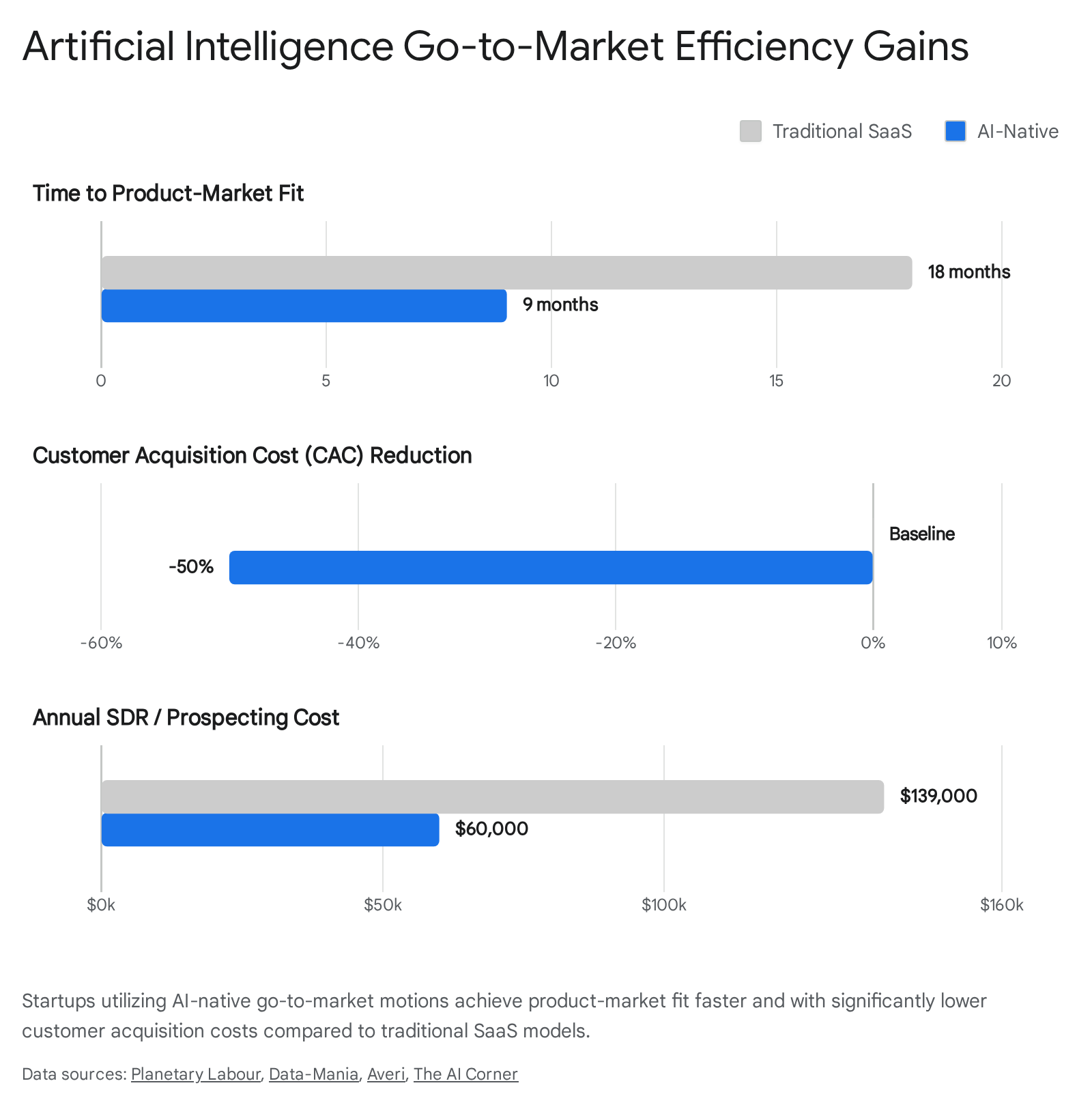

The mechanics of customer acquisition and pipeline generation have been completely re-architected by the integration of AI into the GTM motion itself. Traditional startup playbooks dictated hiring large teams of sales development representatives (SDRs), enduring 12-to-18-month timelines to reach product-market fit, and deploying $2 million or more in annual GTM budgets 11. In 2026, AI-native startups are achieving product-market fit within six to nine months, utilizing highly efficient GTM budgets ranging from $800,000 to $1.2 million, and operating with teams half the size of their historical counterparts 11.

Customer Acquisition Cost Benchmarks

Customer Acquisition Cost (CAC) benchmarks have evolved significantly, rising 40% to 60% since 2023 for companies relying on traditional paid channels 12. The average CAC for B2B SaaS ranges between $536 and $702, climbing to over $800 for enterprise segments and $1,450 for complex fintech sectors 12. In contrast, AI-powered GTM strategies are actively compressing these figures. Startups employing systematic AI marketing automation report CAC reductions of 25% to 50% 1113.

This reduction is driven by hyper-personalized outreach, predictive intent scoring, and the replacement of manual prospecting with autonomous systems. For example, the cost per lead utilizing an AI SDR platform has dropped to approximately $39, an 85% reduction from the $262 average associated with human-led outbound efforts 14. At scale, VC-backed companies spend roughly 47% of revenue on sales and marketing, making the efficiency gains from AI automation critical for reaching profitability 5.

Sales Pipeline Velocity

The integration of artificial intelligence accelerates pipeline velocity by automating top-of-funnel and middle-of-funnel friction points. Traditional B2B sales cycles typically span 70 to 162 days, with an average of 134 days for complex software 1115. By leveraging AI agents to conduct instantaneous account research, generate hyper-personalized outreach, and automate meeting scheduling, startups are shrinking average sales cycles to under 90 days 11.

Furthermore, AI systems equipped with predictive analytics can identify the optimal channels and messaging required for conversion. Organizations report a 35% higher win rate for teams utilizing fully integrated AI GTM workflows, with AI-personalized emails seeing reply rates jump from 9% to 21% 131416.

| Go-to-Market Metric | Traditional SaaS (Pre-2024) | AI-Native SaaS (2026) |

|---|---|---|

| Time to Product-Market Fit | 12 to 18 months 11 | 6 to 9 months 11 |

| Annual GTM Budget | $2.0M+ 11 | $800K to $1.2M 11 |

| Average Sales Cycle | 134 to 162 days 1115 | Under 90 days 11 |

| SDR Cost (Annual) | ~$139,000 (Human) 14 | $12,000 to $60,000 (Agent) 14 |

| Average Cost Per Lead | $262 14 | $39 14 |

| Visitor to Lead Conversion | 0.7% to 1.4% 15 | Up to 7x higher 11 |

Product Archetypes and Strategic Positioning

The success of an AI startup's GTM strategy in 2026 is heavily dependent on its product archetype and the structural defensibility of its offering. The market has definitively segmented into three primary pathways: vertical applications, developer-led open-weight infrastructure, and horizontal platforms.

Vertical Artificial Intelligence

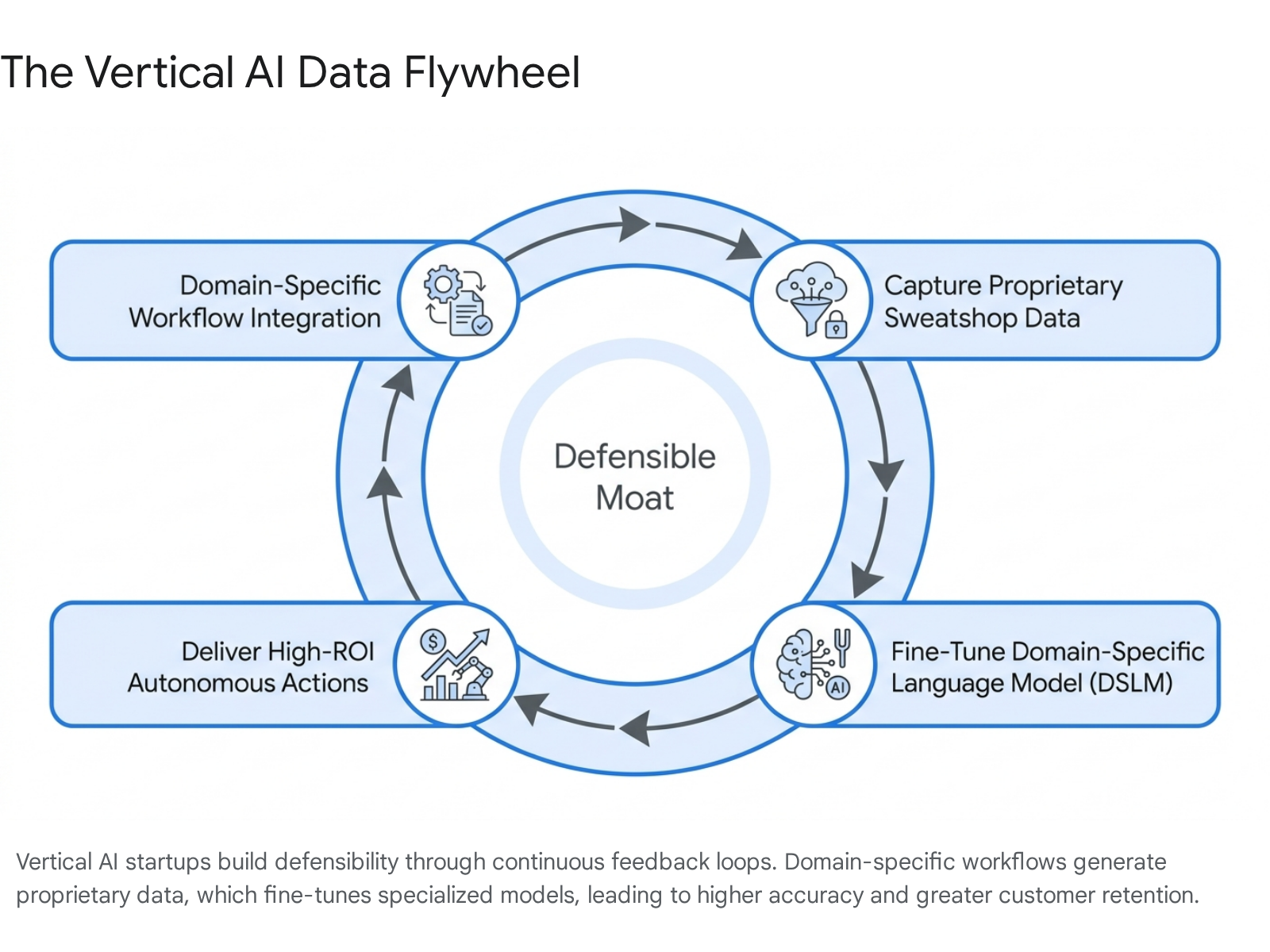

The most successful and capital-efficient go-to-market motion in 2026 is the vertical AI application. According to benchmarking data, vertical SaaS companies featuring AI-enabled products are growing up to three times faster than their horizontal competitors, charging significantly higher premiums, and exhibiting retention metrics that far outpace the broader software market 17187. During 2025, vertical startups captured 53% of venture deal volume across 4,395 financings, with sectors like Manufacturing, Legal, and Healthcare leading adoption 8.

The GTM strategy for vertical AI relies on "sweatshop data" - deep, proprietary, domain-specific data accumulated through highly specialized daily workflows that general foundation models cannot easily access or replicate 721.

By focusing on a single industry and solving acute, high-cost problems, vertical AI startups benefit from extremely short sales cycles. Because their ideal customer profile (ICP) is highly constrained, GTM messaging can be highly targeted, circumventing the noise of broad enterprise software marketing 1718.

Outcome-Based Pricing in Vertical Sectors

A defining characteristic of successful vertical AI is the shift from per-seat SaaS pricing to outcome-based pricing, or "Results-as-a-Service" (RaaS) 69. Because AI agents replace human labor in workflows where errors carry real consequences, pricing models are aligning revenue with delivered value.

For instance, the healthcare sector consistently generates the highest ROI for vertical AI due to massive administrative burdens. Startups automating prior authorization workflows are achieving ROI for health systems within 12 months 1024. A physical therapy authorization agent can reduce a 45-minute manual task to 90 seconds. Instead of charging a flat monthly software fee, the startup charges an outcome-based fee - such as $5 per successful authorization - directly aligning the software cost with the $30 to $50 in labor savings generated 18. Similarly, ambient clinical documentation tools are saving clinicians 60 to 90 minutes per day, producing up to $75,000 of recovered time per clinician annually 24.

| Vertical AI Use Case | Primary Industry | Operational Impact | Economic ROI |

|---|---|---|---|

| Ambient Clinical Scribes | Healthcare | 30% to 60% reduction in documentation time 24. | $50k to $75k recovered clinician time annually 24. |

| Prior Authorization Agents | Healthcare | Reduces 45-minute tasks to 90 seconds 1824. | $1.5M+ annual recovered staff time for mid-sized hospitals 24. |

| Contract Review Automation | Legal | Eliminates manual document scanning and redlining 18. | Replaces billable associate hours; highly defensible pricing 188. |

| Logistics Routing | Manufacturing | Optimizes last-mile costs and load efficiencies 11. | Margin improvement in highly saturated markets 811. |

Developer-Led Growth and Open-Weight Commercialization

For startups operating at the infrastructure or foundational tooling layer, developer-led growth fueled by open-weight models has emerged as the dominant GTM strategy. As enterprise organizations face growing concerns regarding data privacy, vendor lock-in, and the soaring costs of closed-API foundation models, a massive shift toward locally hosted, open-weight AI has occurred 262712.

Mistral AI represents the premier case study of this GTM approach. While competitors prioritized horizontal consumer dominance and closed APIs, Mistral built its $14 billion valuation by executing a deliberate commercial strategy tailored to enterprise data sovereignty 2713. Mistral releases highly capable open-weight models under permissive licenses (e.g., Apache 2.0), allowing developers to test and adopt the models for free 12. Its models, such as Mistral Large 3 (utilizing 675 billion parameters with only 41 billion active in a sparse Mixture-of-Experts architecture), offer frontier-level performance at a fraction of the computational cost 1214. Once integrated, Mistral monetizes through its "Forge" platform, providing enterprise tools for proprietary data fine-tuning and secure, air-gapped deployment 271215.

Similarly, in the vector database sector, the GTM dynamics between Pinecone and Qdrant illustrate the appeal of open-source optionality. While Pinecone historically dominated as a managed service, Qdrant captured significant market share by offering an open-source, Rust-based database that can be self-hosted. As enterprises scale their AI workloads past 10 million vectors, the infrastructure costs of managed cloud services compound rapidly, making open-source, self-hosted options highly attractive for lowering unit economics 1617. Redis has also entered this space by offering sub-millisecond vector search combined with semantic caching, explicitly marketing the ability to reduce large language model (LLM) costs by up to 70% 17. Startups building infrastructure tools in 2026 must offer tangible pathways for enterprises to control their data and manage inference costs.

Horizontal Platforms and the Wrapper Extinction Event

Conversely, startups building horizontal AI applications - those attempting to serve a broad range of functions across multiple industries without proprietary data - face an "extinction event" 721. Horizontal tools built as thin wrappers around general LLMs suffer from a complete lack of defensibility. Feature parity is reached in weeks, and incumbent enterprise software giants are rapidly embedding similar generative AI capabilities directly into their existing suites 718.

The failure of horizontal applications stems from broken unit economics. If a startup charges a flat monthly subscription for unlimited AI usage, scaling the customer base exponentially increases API inference costs, leading to negative gross margins 7. Furthermore, horizontal platforms lack the deep contextual awareness required to drive complex, multi-step agentic workflows 19. Therefore, research consensus in 2026 strongly advises against a horizontal GTM motion unless a startup possesses a fundamentally unique algorithmic breakthrough.

Re-Architecting the Go-to-Market Technology Stack

The operational mechanics of startup growth teams have fundamentally shifted. GTM strategy is no longer solely the domain of marketing and sales personnel; it requires the integration of product engineering, revenue operations, and AI workflow orchestration 2037.

Autonomous Sales Agents and Workflow Orchestration

The most pronounced technological shift within GTM organizations is the rapid deployment of AI Sales Development Representatives (SDRs). The market for AI SDR platforms is projected to grow from $4.1 billion in 2025 to $15 billion by 2030, driven by compelling unit economics and the inability of human SDRs to process thousands of signals simultaneously 1114. Platforms such as 11x, Artisan, and Apollo are enabling startups to orchestrate complex, multi-step prospecting workflows autonomously 14.

However, the underlying infrastructure for these agents is moving away from simple prompt engineering toward sophisticated runtime architectures. Frameworks like LangChain and LangGraph are essential for building robust GTM agents that connect LLMs to CRM data, internet search, and internal company context 382140. A case study from LangChain's own internal implementation demonstrates that deploying a GTM agent to autonomously check Salesforce leads, gather context from Gong and LinkedIn, and draft personalized slack messages for sales representatives increased lead-to-qualified-opportunity conversion rates by 250% over three months, saving reps 40 hours per month 21.

The critical success factor for these agentic deployments is an engineering shift from "prompting" to "debugging" 22. As agents begin executing real-world actions, system reliability depends on explicit state management, human-in-the-loop approvals, and rigorous trace analysis to prevent hallucination-driven outreach errors 2122.

Generative Engine Optimization

Traditional search engine optimization (SEO) is being actively replaced by Answer Engine Optimization (AEO) and Generative Engine Optimization (GEO). As B2B buyers increasingly rely on AI tools like ChatGPT, Perplexity, and Claude for vendor discovery, startups must ensure their products are legible to these AI systems 923. Currently, 47% of high-growth companies are experimenting with AEO, structuring their website content and digital footprint to serve as verifiable "trust hubs" for AI web crawlers 923. A modern GTM strategy mandates building visibility within large language model responses rather than relying exclusively on traditional search engine rankings.

Regulatory Frameworks and Geographic Expansion

Geographic market entry in 2026 requires navigating a fragmented and complex web of regulations, infrastructure availability, and sovereign technology strategies. Regulatory compliance is no longer a late-stage corporate chore; it is a fundamental pillar of early-stage GTM strategy that determines market access and investor fundability 2425.

The European Union Artificial Intelligence Act

The European Union AI Act represents the most significant regulatory hurdle for global AI startups. Entering full enforceability in August 2026, the Act categorizes AI systems based on risk and imposes stringent technical, operational, and governance obligations 2646. The regulation possesses profound extraterritorial reach. A startup need not have an office or employees in Europe; if a non-EU company sells, licenses, or operates a system whose outputs impact EU residents, it falls under the Act's jurisdiction 2748.

Providers of high-risk systems must complete conformity assessments, register in public databases, establish rigorous data governance to reduce bias, and maintain extensive technical documentation 2748. Penalties for non-compliance are severe, reaching up to €35 million or 7% of a company's global annual turnover 2648. Startups targeting the European market must integrate these compliance costs into their GTM financial models and utilize their regulatory readiness as a competitive differentiator to build trust with enterprise buyers 1424.

The Chinese Market and Local-First Mandates

The AI landscape in China operates under fundamentally different mechanics, characterized by strict regulatory controls and a "local-first" deployment mandate 28. Although China lacks a single comprehensive AI statute, its fragmented framework requires exhaustive security assessments, algorithm filings, and strict data localization 28. Algorithm filings must be executed by China-based entities, creating significant barriers to entry for foreign startups 28.

For domestic Chinese startups, a brutal price war triggered by highly capable, low-cost models like DeepSeek V4 has compressed margins at the application layer, causing stock slumps for prominent AI firms like MiniMax and Zhipu 29. Survival in the Chinese market requires deep vertical integration into enterprise workflows - such as e-commerce, logistics, and healthcare - where exclusive data assets provide a moat against the commoditization of foundational models 1129. Concurrently, tightening US export controls have driven a surge of Chinese AI unicorns to seek capital through the Hong Kong stock exchange, utilizing the city as a gateway to expand into Southeast Asian markets 30.

Middle East Compute Infrastructure and the GCC

The Gulf Cooperation Council (GCC), led by the United Arab Emirates (UAE) and Saudi Arabia, has emerged as a premier global hub for AI investment and infrastructure. Driven by sovereign wealth funds managing trillions in assets and a strategic imperative to transition away from hydrocarbon dependence, the GCC is deploying massive capital into foundational compute 3132. The UAE's "Stargate" project, a 5-gigawatt AI data center complex in Abu Dhabi developed in collaboration with global tech giants, exemplifies this infrastructure-first approach 3132.

For AI startups, the GCC offers a highly attractive GTM environment. However, the region is transitioning from early-stage experimentation to structured, commercial execution. Success requires aligning with national digitization strategies (such as Saudi Vision 2030) and targeting specific verticals like public administration, hospital systems, and Islamic fintech 313334. Due to increasing global energy constraints, the GCC's combination of affordable energy, proactive state-backed investment, and clear regulatory frameworks provides a stable platform for startups requiring significant computing power 3234.

Indian Market Dynamics and Localization

In India, GTM strategies are shifting from generalized user acquisition to specialized systems built for "Bharat" - focusing on local languages, varied literacy levels, and non-linear user journeys 56. Startups in the banking, financial services, and insurance (BFSI) sectors are moving beyond basic chatbot interfaces to integrate AI deeply into underwriting, claims processing, and personalized credit distribution 56. According to NASSCOM, Indian startups that systematically integrate AI into their marketing operations see a 35% to 60% reduction in customer acquisition costs within 12 months 35. Despite this domestic growth, venture capital firms are increasingly pressuring Indian AI founders building for North American audiences to relocate to Silicon Valley early in their lifecycle to stay closer to capital, talent, and monetization signals 36.

| Region | Regulatory Posture & Market Dynamic | Strategic GTM Implication for Startups |

|---|---|---|

| United States | Fragmented oversight (FTC, state-level laws). High VC concentration but saturated markets 2436. | Requires aggressive vertical specialization and demonstrable hard ROI to secure funding 721. |

| European Union | Stringent classification under the EU AI Act (enforceable Aug 2026). Extraterritorial reach 4627. | Compliance must be embedded early. Data governance and transparency are core GTM messaging components 2448. |

| China | "Local-first" mandate. Strict data localization and algorithm filing requirements 28. | Foreign entry is highly constrained. Domestic survival depends on exclusive enterprise data integration 1129. |

| Middle East (GCC) | State-sponsored, infrastructure-led growth. Massive sovereign wealth investment in compute 3132. | GTM must align with national visions (e.g., healthcare, public administration). Lucrative for domain-specific AI 34. |

| India | Focus on localized languages and the "Bharat" demographic. AI moving to the middle-office in BFSI 56. | High ROI from AI marketing automation. Global-facing startups pushed to relocate to the US for market proximity 3536. |

Analyst Forecasts and Return on Investment Validation

The transition from AI hype to a demand for measurable business outcomes defines the 2026 strategic landscape. Major industry analysts, including Gartner, Forrester, and IDC, have converged on a unified consensus: enterprise buyers are actively rejecting experimental AI projects in favor of hard financial ROI 193738.

Forrester predicts that 25% of planned AI spend will be delayed into 2027 as Chief Financial Officers halt initiatives that cannot draw a direct line between AI implementation and profit margin improvement 38. The era of "checked-box AI" is over; startups must explicitly prove how their product reduces specific operational costs or drives revenue velocity 21. Furthermore, Forrester warns of a "shadow AI" crisis, predicting that the ungoverned use of generative AI tools could result in data leaks and compliance breaches costing enterprises over $10 billion in value 3839. Consequently, startups that build integrated security, decentralized governance controls, and transparency into their GTM narratives will secure significantly higher close rates.

Gartner's Top Strategic Technology Trends for 2026 reinforce the necessity of targeted architecture. Technologies such as AI Supercomputing Platforms, Multiagent Systems, and Domain-Specific Language Models (DSLMs) are highlighted as critical growth catalysts 4041. DSLMs, in particular, provide the accuracy and compliance required for industry-specific use cases, perfectly aligning with the vertical AI GTM motion 4142. Similarly, research from MIT Sloan highlights four core tensions organizations face with agentic AI: scalability versus adaptability, experience versus expediency, supervision versus autonomy, and retrofitting versus reengineering 43. Startups that can help enterprises navigate these tensions safely - particularly by balancing autonomy with necessary human supervision - will dominate vendor selection processes.