GLP-1 and Weight-Loss Drug Statistics for 2026

BLUF: The landscape of obesity management has been irrevocably transformed by GLP-1 receptor agonists, with the global market projected to exceed $190 billion by 2035 as usage scales to tens of millions of patients. However, 2025 and 2026 real-world data definitively proves that these medications are chronic treatments rather than acute cures, with patients typically regaining 60% of their lost weight within a year of cessation. Navigating this new era requires balancing unprecedented clinical efficacy against high out-of-pocket costs, tightening insurance criteria, the closure of compounding loopholes, and emerging long-term considerations regarding bone density and muscle preservation.

For decades, the medical community and the general public viewed chronic weight management through a lens of behavioral economics and sheer willpower. Dieting was framed as a test of moral fortitude, and failure to maintain weight loss was routinely attributed to personal inadequacy. Today, that paradigm has collapsed. You should care about the rise of glucagon-like peptide-1 (GLP-1) receptor agonists because they have fundamentally reclassified obesity from a behavioral failing to a treatable, chronic metabolic dysfunction. Whether you are a patient navigating a complex insurance landscape, a healthcare provider managing longitudinal care, or an employer trying to balance ballooning healthcare premiums, the ripple effects of the GLP-1 revolution are inescapable. This report synthesizes 2024, 2025, and 2026 data to provide an exhaustive analysis of how these medications work, what they cost, how health systems worldwide are responding, and what the long-term outcomes truly look like.

How Exactly Do GLP-1 Medications Work to Drive Weight Loss?

To comprehend the profound clinical impact of GLP-1 medications, it is helpful to conceptualize the human body's metabolism as a highly sophisticated, yet stubbornly conservative, central heating thermostat. In an individual living with obesity, this biological thermostat has been effectively recalibrated to defend a higher "weight set point." When the individual attempts to lose weight through caloric restriction, the brain perceives this deficit not as a healthy choice, but as an acute starvation threat. In response, the body releases a cascade of hunger hormones, amplifies appetite, and deliberately slows down the basal metabolic rate to defend its higher weight 1.

GLP-1 medications function as advanced biological recalibration tools for this deeply entrenched thermostat. Glucagon-like peptide-1 is a naturally occurring incretin hormone produced in the gut in direct response to food intake. Physiologically, it serves multiple critical functions: it prompts the pancreas to release insulin to manage blood glucose, it drastically slows gastric emptying so that food remains in the stomach longer, and crucially, it crosses the blood-brain barrier to target receptors in the hypothalamus, the brain's primary appetite control center 1. By binding to these neural receptors, GLP-1 medications artificially and continuously signal profound satiety. Rather than relying on finite willpower to fight the body's innate starvation response, these medications alter the biochemical signaling pathways. They allow individuals to consume significantly fewer calories without experiencing the overwhelming, physiological drive to eat 1.

The pharmacological landscape has rapidly evolved beyond mimicking a single hormone. Newer iterations, most notably tirzepatide, are classified as "dual-agonists." They mimic both GLP-1 and a second incretin hormone called GIP (glucose-dependent insulinotropic polypeptide) 2. This dual-action mechanism not only amplifies the appetite-suppressing effects but also uniquely improves how the body metabolizes subcutaneous fat and regulates insulin sensitivity 11. Even more aggressive formulations currently in clinical trials, such as retatrutide, are "triple-agonists" that target GLP-1, GIP, and glucagon receptors simultaneously, pushing pharmacological interventions into efficacy thresholds that were previously the exclusive domain of bariatric surgery 2.

What Are the Real-World Outcomes When Comparing Semaglutide and Tirzepatide?

The clinical efficacy of these medications has created a tiered landscape of weight-loss outcomes, and robust data from 2025 and 2026 clearly delineates the performance advantages of newer multi-hormone formulations over their single-hormone predecessors.

In May 2025, the New England Journal of Medicine published the results of the highly anticipated SURMOUNT-5 clinical trial. This represented the first head-to-head clinical trial comparing semaglutide (marketed for weight loss as Wegovy) and tirzepatide (marketed as Zepbound) in non-diabetic individuals diagnosed with obesity 15. The findings definitively established tirzepatide as the superior pharmacological agent for raw weight reduction. Over a 72-week treatment protocol, patients utilizing tirzepatide lost nearly 50% more weight on average than those administered semaglutide 5. The trial revealed that an impressive 32% of tirzepatide-treated patients lost 25% or more of their total body weight, compared to only 16% of patients in the semaglutide cohort achieving that same critical threshold 5. Furthermore, network meta-analyses confirmed that tirzepatide consistently yielded a mean difference of an additional 4.23 to 4.55 kilograms of absolute weight loss compared to semaglutide 13.

These controlled clinical trial results are heavily reinforced by real-world observational data. A massive 2024 cohort study published in JAMA Internal Medicine, which analyzed the electronic health records of over 41,000 adults, confirmed that patients receiving tirzepatide were significantly more likely to achieve clinically meaningful weight loss benchmarks across all timeframes 24. At the critical 12-month mark, 42.3% of tirzepatide users achieved at least a 15% reduction in total body weight, whereas only 18.1% of semaglutide users reached this milestone 2. The hazard ratios overwhelmingly favored tirzepatide, regardless of whether the patient had comorbid type 2 diabetes 24.

The following table synthesizes current 2026 data regarding the clinical efficacy, list pricing, and typical out-of-pocket costs for the major GLP-1 formulations available on the market.

| Medication | Formulation / Delivery | Mechanism of Action | Average Clinical Weight Loss | 2026 US Monthly List Price | Typical US Out-of-Pocket Cost (With Commercial Coverage) |

|---|---|---|---|---|---|

| Wegovy (Semaglutide) | Weekly Injection | GLP-1 Agonist | ~15% | ~$1,350 | $25 - $75 (Preferred Tier) 8 |

| Oral Wegovy (Semaglutide) | Daily Pill | GLP-1 Agonist | ~15% | ~$1,000+ | $25+ (Self-pay cash options from $149) 9 |

| Zepbound (Tirzepatide) | Weekly Injection | GLP-1 / GIP Dual Agonist | ~21% - 25% | ~$1,060 | $25 - $75 (Preferred Tier) 8 |

| Saxenda (Liraglutide) | Daily Injection | GLP-1 Agonist | ~5% - 8% | ~$1,349 | $25 - $100 810 |

Why Are GLP-1s Not a Quick Fix? The Reality of Weight Regain

One of the most pervasive and medically dangerous misconceptions surrounding GLP-1 medications is that they function as a temporary "quick fix" or a biological bridge to healthier habits, after which the medication can be safely discontinued without consequence. The reality, as illustrated by longitudinal data culminating in 2026, categorically debunks this myth. The data establishes that obesity is a chronic, relapsing condition, and pharmacological intervention requires a long-term, potentially lifelong, commitment 56.

When a patient ceases GLP-1 receptor agonist therapy, the biological suppression of appetite and the chemically delayed gastric emptying abruptly halt. Because these medications do not permanently rewrite the body's underlying biology, the organism's metabolic drive to return to its previous, higher set-point immediately reactivates 1. Appetite signals return with a vengeance, and metabolic adaptation slows calorie burn, creating a physiological environment heavily biased toward fat accumulation 1.

A landmark systematic review and non-linear meta-regression analysis published in eClinicalMedicine, involving 48 studies and over 3,200 participants, quantified the exact trajectory of this post-treatment rebound 7. The analysis revealed that patients regained an average of 60% of their total lost weight within just 52 weeks of discontinuing the medication 7. The statistical models demonstrated that weight regain eventually slows and plateaus at approximately 75.3% of the weight lost during treatment 7.

The rate of this regain is startlingly fast, particularly for those discontinuing the most potent modern agents. For individuals stopping highly effective drugs like semaglutide or tirzepatide, weight returns to the initial baseline within an average of 18 months, with patients gaining back an average of 0.8 kilograms (approximately 1.7 pounds) per month 6. In the first year off the medication, patients who had successfully lost 15 kilograms typically gained back nearly 10 kilograms of that weight 6.

Crucially, this rapid physical weight regain is intrinsically tied to the total reversal of the cardiometabolic benefits the drugs provided. According to real-world 2026 data, as body weight returns to its baseline, so do vital health markers. Levels of fasting plasma glucose, systolic blood pressure, and circulating triglycerides routinely return to their dangerous pre-treatment baselines within one year of cessation 6. Metrics like glycated hemoglobin (HbA1c) and diastolic blood pressure follow closely behind, deteriorating completely within 1.4 years 6.

When researchers compared patients who discontinued behavioral weight-management programs to those who stopped pharmacological interventions, they found that the drug-cessation cohort regained weight at a significantly faster rate - gaining 0.3 kilograms more per month than the behavioral cohort 6. It typically takes nearly four years for weight to be fully regained following the end of a strictly behavioral intervention, whereas drug cessation triggers a violent metabolic snapback 6. This phenomenon underscores a critical clinical reality: GLP-1s suppress the pathology of obesity; they do not cure it. Initiating GLP-1 therapy must be viewed through the exact same long-term clinical lens as prescribing statins for hyperlipidemia or antihypertensives for severe high blood pressure.

What Does 2026 Data Reveal About Long-Term Safety and Side Effects?

As the usage of GLP-1 medications has scaled to tens of millions of global users, longitudinal safety data has brought both profound reassurance regarding psychiatric concerns and stark new warnings regarding musculoskeletal health.

Throughout 2023 and 2024, significant public and regulatory concern arose regarding a potential link between GLP-1 use and severe psychiatric side effects, specifically suicidal ideation. This panic was prompted by raw reports to the FDA's Adverse Event Reporting System (FAERS) 89. However, exhaustive reviews concluded in early 2026 have definitively cleared these medications of this association. The FDA conducted a massive retrospective cohort study using its Sentinel System - analyzing millions of health claims to compare the risk of intentional self-harm among new GLP-1 users against users of SGLT2 inhibitors 810. Concurrently, the agency executed a meta-analysis of 91 placebo-controlled trials involving over 107,000 patients 810. The European Medicines Agency (EMA) had reached similar conclusions following its own rigorous investigation in April 2024 8.

Both regulatory bodies concluded that there is no causal link between GLP-1 receptor agonists and increased risks of suicidal ideation, depression, or intentional self-harm 81011. Consequently, in a landmark decision in January 2026, the FDA formally mandated the removal of suicidal behavior and ideation warnings from the labels of semaglutide, tirzepatide, and liraglutide 81011. Paradoxically, emerging psychiatric literature in 2025 has even begun exploring the potential of GLP-1s for their neuroprotective, anti-inflammatory, and cognitive-enhancing properties in patients suffering from severe mental illnesses like schizophrenia and major depressive disorder 11.

While the psychiatric fears have been comprehensively assuaged, a much more insidious, long-term side effect profile has emerged regarding the musculoskeletal system: the profound loss of lean muscle mass and the subsequent degradation of bone mineral density (BMD).

Weight loss induced by GLP-1s does not exclusively target adipose (fat) tissue. Clinical trials indicate that a staggering 20% to 35% of the total weight lost on these medications consists of lean soft-tissue mass 2. For example, trials for orforglipron showed that 26.9% of the total weight loss was lean mass, while CagriSema resulted in a 14.4% reduction 2. For a patient losing 70 pounds on a highly aggressive future agent like retatrutide, up to 24.6 pounds of that loss may be vital, metabolically active muscle tissue 2.

This extreme, rapid reduction in muscle mass triggers a secondary crisis in the human skeletal system. According to Wolff's Law of bone adaptation, the skeletal system maintains its density based on the dynamic mechanical load it is forced to bear 18. As rapid weight loss drastically reduces this bodily load, and as muscle mass - which applies essential dynamic strain to the bones via tendons - diminishes, bone density begins to deteriorate 218. A 2025 review published in Nature Bone Research highlighted that rapid weight loss results in a 1% to 3% systemic loss in BMD for every 10% of total body weight lost 2.

Five-year follow-up data presented at the prestigious 2026 Annual Meeting of the American Academy of Orthopaedic Surgeons (AAOS) confirmed these theoretical fears. An analysis of over 73,000 matched patients revealed that long-term GLP-1 users faced a 22% higher relative risk of developing clinical osteoporosis compared to matched controls not utilizing the medication 21213. Specifically, incidence rates jumped to 4.1% among GLP-1 users compared to 3.2% in the control group 12. The relative risk for osteomalacia (severe bone softening) saw an even greater relative increase 12. Interestingly, the AAOS data also indicated that while GLP-1 users had lower surgical site infection rates for major joint replacements (TKA and THA), their revision rates for smaller procedures like carpal tunnel releases actually increased, presenting a complex picture of postoperative healing 12.

Beyond the musculoskeletal system, gastrointestinal distress remains the primary barrier to long-term therapeutic adherence. A novel 2026 study out of the University of Pennsylvania utilized artificial intelligence to analyze over 410,000 patient posts on social media platforms 14. The AI revealed that 43.5% of GLP-1 users experience reportable adverse effects 14. While nausea (36.9%), fatigue (16.7%), and vomiting (16.3%) dominated the reports, the analysis also uncovered underreported systemic side effects, including irregular menstrual cycles (reported by 4% of users) and severe thermal regulation issues, such as alternating chills and hot flashes 14.

How Rapidly Is the GLP-1 Market Expanding in 2026 and Beyond?

The adoption curve for GLP-1 medications represents one of the fastest and most aggressive escalations in global pharmaceutical history, transitioning the drugs from niche diabetic therapies to mass-market public health interventions.

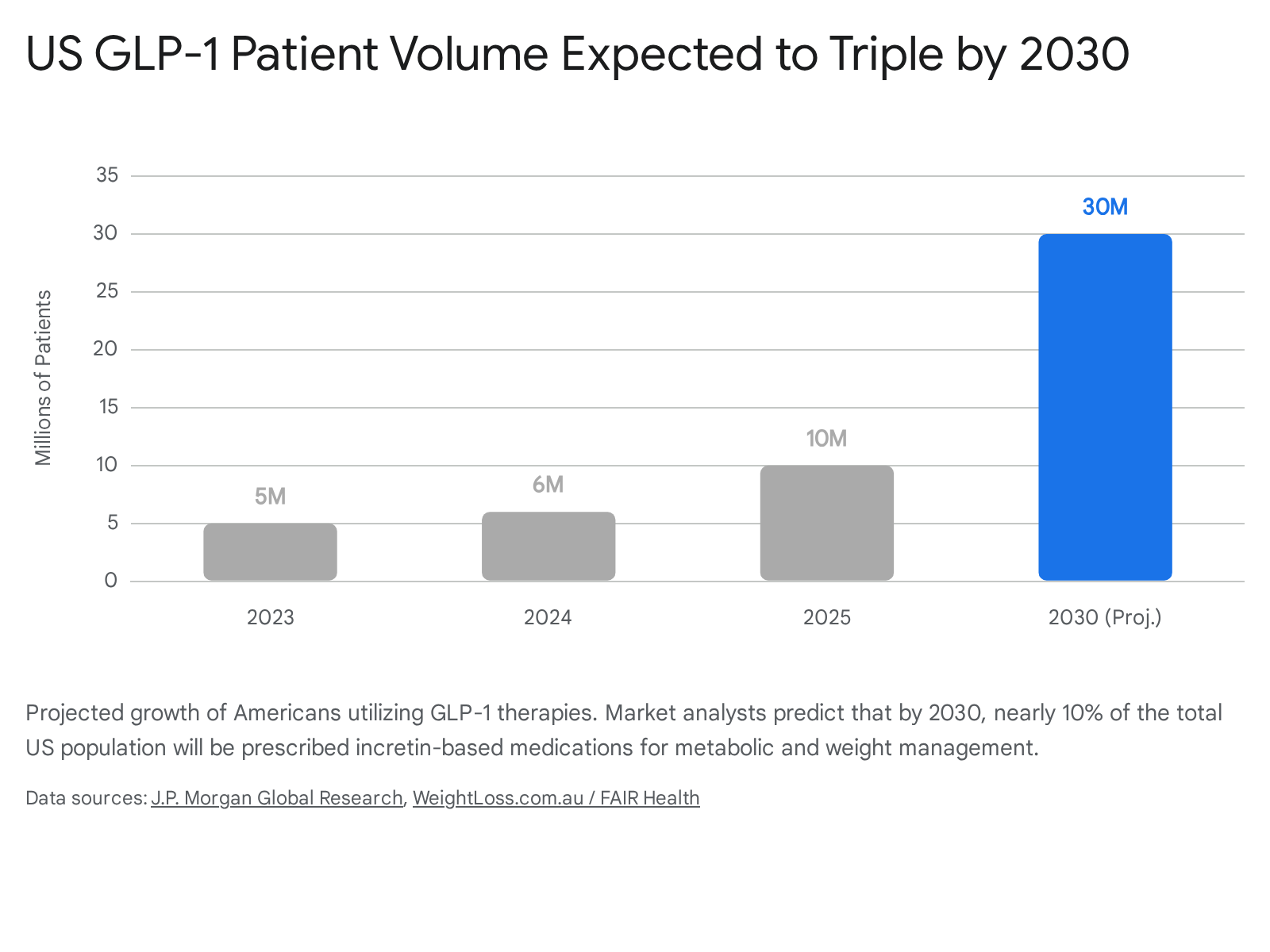

Between 2019 and 2024, non-diabetic prescriptions for GLP-1s targeting weight management exploded by 1,961% in the United States 22. By the end of 2024, data indicated that 11.2% of all patients diagnosed with overweight or obesity had been prescribed a GLP-1 drug, alongside 26.5% of all diabetic adults 22. Concurrently, the reliance on older interventions plummeted; bariatric surgery rates declined by a staggering 42% over the same period, and older weight-loss medications like Saxenda saw their market share drop from 79% in 2018 to just 9% by 2023 22.

By 2025, approximately 10 million Americans were actively taking a GLP-1 medication 2215. In 2026, the landscape shifted into an even higher gear, driven by the resolution of global supply chain shortages, the long-awaited FDA approval of oral GLP-1 formulations, and massively expanded Medicare access 15. Current macroeconomic models from institutions like J.P. Morgan and Morgan Stanley project that by 2030, between 25 million and 30 million Americans - representing nearly 10% of the entire U.S. population - will be on uninterrupted GLP-1 therapy 1516.

Globally, UBS forecasts that 40 million people will be utilizing these medications by 2029 22.

This exponential volume translates into staggering macroeconomic figures. The global GLP-1 market size, valued at roughly $53.5 billion in 2024, is projected to reach anywhere from $132 billion to $190 billion by the mid-2030s 221625. This financial explosion is driving massive corporate consolidation; in 2025, Pfizer won a fierce bidding war to acquire Metsera and its portfolio of incretin assets for $10 billion, marking one of the largest M&A deals of the year 1517.

First-time prescribing patterns in early 2026 heavily underscore this momentum. Data from millions of electronic health records indicates that while prescribing rates for anti-diabetic GLP-1s remain relatively stable, the prescribing rates for anti-obesity GLP-1s (AOMs) surged by over 17% in the first quarter of 2026 alone 18. First-time prescriptions for AOMs specifically jumped by 21.7% in March 2026 compared to late 2025 28. Tirzepatide, branded as Zepbound, has firmly overtaken semaglutide as the primary driver of this new growth, being prescribed at nearly twice the rate of its predecessor 18.

A massive catalyst for the 2026 market expansion was the introduction of oral GLP-1 formulations. The once-daily Wegovy pill, launched in the US in January 2026, captured approximately one-third of all new-to-brand prescriptions within its first eight weeks on the market 1719. Crucially, IQVIA analytics suggest that the oral pill is expanding the total addressable market rather than simply cannibalizing injectable sales; roughly two-thirds of the volume for the Wegovy pill comes from patients who have never used any GLP-1 therapy before, indicating that needle phobia was a major prior barrier to adoption 1719. With Eli Lilly's small-molecule oral GLP-1, orforglipron, launching in mid-2026, the oral market is poised for a fierce duopoly 221719.

Why Are Costs and Insurance Coverage So Variable in the United States?

The staggering clinical efficacy of GLP-1 medications has collided violently with the stark realities of healthcare economics. Because obesity impacts over 40% of the adult population in the United States, the financial implications of universally funding medications that cost upward of $10,000 to $15,000 annually per patient are potentially system-breaking 2021. Consequently, access and out-of-pocket costs differ radically depending on the intricate mechanics of local health systems, Pharmacy Benefit Managers (PBMs), and state borders.

In the United States, the list price for branded semaglutide or tirzepatide generally exceeds $1,000 to $1,350 per month 83233. However, this "sticker price" is largely a theatrical starting point for secretive negotiations between pharmaceutical manufacturers, insurers, and PBMs. Counterintuitively, a high list price allows drug makers to offer larger, opaque rebates to PBMs in exchange for securing favorable tier placement on insurance formularies 8. The savings from these proprietary rebates are rarely passed directly to the patient at the pharmacy counter 8.

For patients with robust commercial insurance whose employer plans actually cover anti-obesity medications, final out-of-pocket costs are dictated by their deductible status and formulary tier. A 2024 analysis showed that if a drug is on a preferred tier (Tier 2), copays hover between $45 and $75 a month 8. If relegated to a non-preferred brand tier (Tier 3), costs frequently exceed $200 to $350 a month 8. Even with manufacturer copay cards - which can temporarily reduce copays to $25 - the annual maximum benefit caps quickly run out, leaving patients exposed to full costs 8.

Crucially, coverage is far from guaranteed. Fearing premium destabilization, most employer and ACA Marketplace plans categorically exclude GLP-1s prescribed solely for weight loss 2134. Even when coverage theoretically exists, prior authorization (PA) requirements serve as a universal, aggressively managed gatekeeper 34. Insurers routinely mandate a BMI of 30 or higher (or 27 with an associated comorbidity like hypertension or sleep apnea), documented proof of a 3-to-6-month supervised clinical diet program, and step-therapy protocols requiring the patient to clinically "fail" cheaper, older weight-loss drugs (like Contrave or Qsymia) before approving Zepbound or Wegovy 343536. Because of these stringent hurdles, initial prior authorization requests are denied in roughly 30% to 40% of cases 3437. For the uninsured or those with exclusionary plans, self-pay prices remain punishing. Even after massive manufacturer price cuts in 2025 and 2026, states with the highest obesity rates - such as Mississippi, West Virginia, and Louisiana - face severe double-digit income burdens, with annual out-of-pocket costs exceeding $3,000 20.

A truly seismic shift in U.S. coverage dynamics occurred in 2026 with Medicare. Historically prohibited by federal law from covering weight-loss drugs, Medicare leveraged its immense negotiating power to initiate the GLP-1 Bridge program in July 2026 2138. The government negotiated an astonishing 82% price drop, securing a net price of $245 per 30-day supply from manufacturers Novo Nordisk and Eli Lilly 38. For eligible seniors meeting strict clinical criteria, this Bridge program caps their monthly copay at a flat $50, vastly expanding access and potentially saving the system $3.4 billion by 2034 through reduced cardiovascular and diabetic complications 2138. This temporary Bridge program paves the way for the permanent BALANCE (Better Approaches to Lifestyle and Nutrition for Comprehensive hEalth) coverage model, which will expand to include drugs like Mounjaro and Ozempic in January 2027 3822.

How Does US Access Compare to the UK, Europe, and Canada?

Outside the United States, single-payer healthcare systems and national health authorities hold immense leverage over pharmaceutical pricing. However, to protect finite public health budgets, they employ aggressive clinical rationing and outright coverage bans, leading to vastly different patient experiences.

In the United Kingdom, the National Health Service (NHS) secures deeply discounted prices but strictly limits who can receive the drugs. The National Institute for Health and Care Excellence (NICE) officially approved both Wegovy and Mounjaro for obesity management. However, the NHS recognized that offering these injections to all eligible adults immediately would bankrupt local Integrated Care Boards and consume an unsustainable 20% of all primary care GP appointments 40. Consequently, the UK is currently executing a highly restrictive, 12-year phased rollout 40.

In 2026, NHS access to drugs like tirzepatide is generally restricted to an elite clinical tier: patients with a BMI over 40 (adjusted to 37.5 for individuals of South Asian, Chinese, Black African, or African-Caribbean descent due to higher metabolic risks at lower weights) who also suffer from at least four severe weight-related long-term conditions (such as cardiovascular disease and sleep apnea) 40232443. By June 2026, these criteria are expected to marginally broaden to include a BMI of 35 with four conditions 40. Those who fail to meet these extreme public criteria must seek private prescriptions. The UK private market is booming as a result, with patients paying between £150 and £300 out-of-pocket per month 3244.

In Germany, Europe's largest pharmaceutical market, the system has taken a draconian stance against reimbursement. The Federal Joint Committee (G-BA) has strictly classified weight-loss GLP-1s like Wegovy as "lifestyle medications" (Lifestyle-Medikament) under Section 34 of the Fifth Book of the German Social Code (SGB V) 334525. Because statutory health insurance (GKV) - which covers 90% of the population - is legally banned from covering lifestyle products, patients must pay entirely out-of-pocket. Regional social courts have repeatedly upheld this ban, declaring that public insurers are not obligated to fund weight reduction unless it addresses approved non-obesity indications 4526. Consequently, German patients typically pay between €180 to €250 per month for off-label Ozempic, and €290 to €380 per month for Wegovy, unless they possess exceptionally rare private insurance (PKV) policies 3344. Similar restrictive public coverage models dominate France and Italy, driving massive private-pay demand 44.

In Canada, coverage is highly fragmented across provincial lines. Without private supplemental coverage, Canadian patients face steep monthly costs of roughly $350 to $500 CAD for Ozempic, and $500 to $700 CAD for Wegovy 33.

Are the GLP-1 Drug Shortages Finally Over in 2026?

The severe supply chain crises that defined the global GLP-1 market from 2022 to 2024 have largely been resolved as of 2026, creating a double-edged sword for millions of patients.

Pharmaceutical giants Novo Nordisk and Eli Lilly invested billions of dollars into aggressively expanding their global manufacturing and fill-finish capacities 48. The introduction of single-dose, 7.2mg maximum-strength Wegovy pens by the UK's MHRA in April 2026 also helped streamline manufacturing efficiency, moving away from requiring patients to take multiple smaller doses simultaneously 27. Consequently, the U.S. Food and Drug Administration (FDA) officially declared the systemic shortage of tirzepatide resolved in October 2024, followed by the formal resolution of the semaglutide shortage in February 2025 2829. While localized pharmacy bottlenecks and highly intermittent delays for specific introductory dosage strengths occasionally occur, the days of systemic, nationwide unavailability are over 4829.

However, the regulatory resolution of these shortages triggered a severe financial consequence for cash-paying patients. During the height of the shortage years, federal law permitted 503A compounding pharmacies and massive 503B outsourcing facilities to legally manufacture, compound, and sell unbranded "copies" of semaglutide and tirzepatide 28. These compounded alternatives typically cost patients between $129 and $300 a month, serving as a vital, affordable loophole for millions who were routinely denied commercial insurance coverage 102830.

Once the FDA officially removed the branded drugs from the national shortage list, the legal justification for this massive compounding industry evaporated. The agency mandated strict enforcement deadlines requiring compounders to wind down operations by April and May of 2025 2830. As of mid-2025 and moving into 2026, the FDA explicitly proposed stringent rules permanently prohibiting 503B bulk compounding of these agents, regardless of any future market conditions 2830. The permanent closure of this compounding loophole means that patients who successfully relied on $200 compounded alternatives for years are now forced back into a rigid system where they must either fight for highly restrictive insurance approvals or pay $1,000 or more per month for the branded commercial products 30.

What Are the Practical Takeaways for Navigating Treatment in 2026?

Given the immense complexities of out-of-pocket costs, hostile insurance algorithms, and unavoidable physiological outcomes, patients and their healthcare providers must approach GLP-1 therapy as a strategic, multi-year clinical campaign.

- Mastering the Prior Authorization (PA) Process: Insurers utilize automated systems to aggressively reject incomplete requests 37. Ensure that the prescribing physician meticulously documents a history of failed behavioral weight-loss attempts (spanning 3 to 6 months), exact BMI measurements, and any associated comorbidities (like hypertension or dyslipidemia) prior to submitting the claim 3437. In 2026, utilizing specialized third-party PA coordination software is becoming standard practice to fight denial rates 37.

- Leveraging Alternative Medical Diagnoses: Commercial plans that categorically exclude "anti-obesity medications" as a matter of policy may still cover the exact same drug if it is prescribed for a different, fully covered FDA-approved indication. For example, Zepbound received specific FDA approval in late 2024 for the treatment of moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity 35. Filing the PA under an OSA diagnosis pathway (requiring sleep study documentation) often successfully bypasses standard weight-loss exclusions 35. Similarly, Medicare Part D now covers Wegovy specifically for cardiovascular risk reduction in patients with established heart disease, even if they refuse to cover it for pure weight loss 3336.

- Mandatory Muscle and Bone Preservation: The loss of bone mineral density and vital lean muscle mass is not a theoretical risk; it is a guaranteed physiological consequence of rapid weight reduction 21812. Treatment protocols must not rely on the medication alone; they must be aggressively paired with high protein intake and mandatory resistance training. Exercise is no longer just about burning calories while on a GLP-1; it is a critical, preventive medical necessity to safeguard the skeletal system against crippling osteoporosis and osteomalacia 18.

- Prepare an Exit Strategy or Budget for the Long Haul: Because statistical models prove that 60% of lost weight is rapidly regained within a single year of stopping the medication 7, patients must completely abandon the idea of using the drug for a quick, six-month cosmetic fix. Before taking the first injection, patients should honestly evaluate if they have the financial resources, or the insurance stability, to maintain the prescription indefinitely, or risk severe, rapid metabolic rebound and the reversal of all cardiometabolic gains 6.

Bottom Line

The exhaustive data compiled through 2026 definitively proves that GLP-1 receptor agonists are highly effective, generational advancements in the treatment of obesity and severe metabolic disease. However, they demand a radical paradigm shift in how patients, providers, and healthcare systems approach long-term weight management. These medications are not acute, cosmetic fixes; they are lifelong pharmacological interventions akin to daily blood pressure medications, requiring continuous adherence to prevent rapid weight regain and the violent reversal of cardiometabolic benefits. As supply shortages end and the era of cheap, compounded alternatives permanently closes, patients must navigate increasingly complex insurance hurdles while proactively managing long-term, systemic side effects like muscle wasting and bone density loss to ensure true, lasting health improvements.