Gig Economy Workers, Pay, and Job Security Explained

The gig economy is a labor market characterized by short-term, task-based work mediated by digital platforms, encompassing everyone from app-based drivers to highly skilled freelance consultants. While data shows it offers unparalleled operational flexibility and acts as a vital income supplement for millions, workers often face severe pay volatility, high out-of-pocket expenses, and significant vulnerability due to the absence of traditional employment protections. Consequently, global regulators are increasingly challenging the independent contractor model to mandate algorithmic transparency and enforce basic financial security.

Defining the Modern Gig Economy

The traditional framework of employment - defined by standard hours, an employer-provided safety net, and a human managerial hierarchy - is being rapidly transformed by the rise of platform-mediated labor. In 2024, the global gig economy generated approximately $556.7 billion, a figure that industry analysts project will surpass $2.1 trillion by 2033, reflecting a compound annual growth rate (CAGR) of over 16% 12.

However, defining exactly what constitutes "gig work" remains a persistent challenge for labor economists. The term is often used as a catch-all that obscures vastly different work experiences. It includes hyper-local, app-based physical labor (such as ride-hailing and food delivery), global digital crowdwork (such as micro-tasking and online coding), and high-end freelance professional consulting. Because regulatory definitions vary wildly from country to country, estimates of labor force participation range significantly depending on whether analysts are measuring primary income earners, casual participants, or temporary agency workers 34.

Measuring the Unmeasurable Workforce

Attempting to pin down the exact number of gig workers yields a fragmented picture. Globally, the World Bank and the International Labour Organization (ILO) estimate that there are approximately 435 million gig workers, representing up to 12% of the global labor market 15.

In the United States, broader surveys that incorporate freelancers, temporary workers, and casual side-hustlers indicate that roughly 36% to 38% of the workforce (over 64 to 70 million people) earns some form of independent income 678. Yet, when isolating just those who work exclusively for digital labor platforms (like Uber, DoorDash, or TaskRabbit), participation drops to roughly 2% to 4% of the population, though this specific segment is growing at a rapid 5% to 8% annualized rate 910.

The discrepancy in measurement is largely due to outdated labor force surveys that fail to capture ad-hoc digital work. Traditional metrics, such as the U.S. Current Population Survey (CPS) and standard establishment surveys, rely on W-2 payroll data and traditional employment classifications. Recent research by the Federal Reserve utilizing the Survey of Informal Work Participation (SIWP) revealed that roughly 15% of people officially categorized as "unemployed" or "not in the labor force" actually perform some form of gig work to survive 910. If these hidden gig workers were formally integrated into household surveys, the U.S. employment-to-population ratio would likely sit closer to 65% rather than the officially reported 60% 910.

The Macroeconomic Reality in 2024 - 2025

The growth of the gig economy cannot be understood in a vacuum; it is deeply intertwined with broader macroeconomic headwinds. According to the ILO's World Employment and Social Outlook: Trends 2025 report, the global economy is entering a fragile period of "new normal" characterized by persistent geopolitical tensions, trade disruptions, and decelerating growth (revised down from 3.2% to 2.8% for 2025) 111213.

Against this backdrop, the global jobs gap - the number of people who want to work but cannot secure adequate employment - stands at a staggering 402 to 407 million people 1112. Furthermore, the global labor income share has continued its decade-long downward trajectory, falling from 53.0% in 2014 to 52.4% in 2024 1213. Had the labor income share remained stable, each worker globally would have earned an average of $290 more in 2024 12.

Faced with declining purchasing power, inflation, and stagnant real wages in traditional lower-tier jobs, workers are increasingly turning to the gig economy out of economic necessity. In 2025, real wages for low-wage workers in the U.S. actually declined by 0.3%, a stark departure from the strong gains seen over the previous five years, pushing many to seek supplementary income through flexible digital platforms 14.

Demographics: Who Works in the Gig Economy?

Public perception often relies on a narrow set of stereotypes - such as young urbanites delivering food by bicycle, or freelancers working from coffee shops. While these archetypes exist, large-scale payroll and survey data reveal a much more demographically diverse, and increasingly bifurcated, reality 3.

The Generational Divide

Age is one of the strongest predictors of gig economy participation, with younger workers driving the overwhelming majority of platform growth.

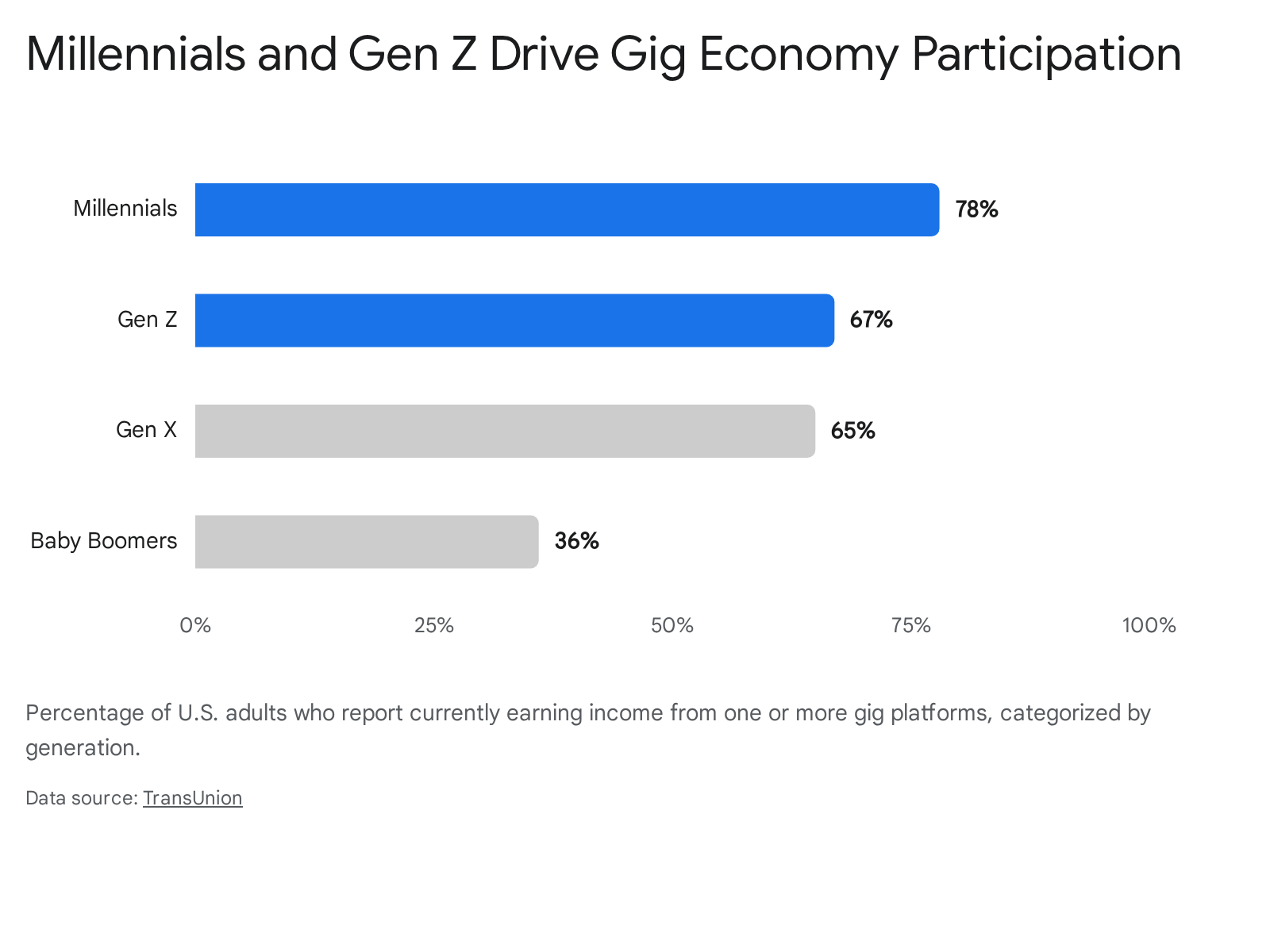

In the United States, an estimated 37% to 43% of Generation Z workers actively participate in the gig economy - more than any previous generation at the same life stage 57. For this cohort, gig work is rarely seen as a temporary stopgap. Research from 2025 indicates that over 28% of Gen Z gig workers consider freelance or platform work to be their primary source of income 7. For millennials, the figures are even higher in terms of sheer participation, with surveys indicating that 78% currently earn some form of income from one or more gig platforms 15.

This youth movement is reshaping the skill sets demanded by the freelance economy. The fastest-growing niches for Gen Z gig workers include AI prompt engineering (experiencing reported growth of ~180%), creator economy management, and short-form video specialization 7. Furthermore, younger gig workers are vastly outpacing traditional employees in technology adoption; 61% of Gen Z freelancers utilize generative AI tools in their daily workflows, compared to just 41% of their peers in full-time employment 713.

Primary Income vs. The "Side Hustle"

While younger generations view gig work as a primary career path, the aggregate global data shows that the majority of gig workers still participate to supplement their existing income. Approximately 60% of independent workers report using gig platforms specifically to offset inflation, supplement inadequate wages, or save for emergencies 515. In Malaysia, for instance, nearly 70% of platform workers operate on a part-time basis 16.

However, the cohort of "full-time independents" is surging. The number of Americans who work full-time as independent contractors more than doubled from 13.6 million in 2020 to 27.7 million by the end of 2024 6. These are not individuals picking up a few hours driving on the weekend; they are professionals building sustainable client bases outside the traditional W-2 employment structure. Consequently, the high-earning segment is expanding rapidly. Between 2020 and 2025, the number of independent workers earning over $100,000 annually grew by 87%, surging from 3 million to 5.6 million people 6.

The Hidden Tax Data Divide: 1099 vs. W-2

Demographic profiling becomes highly nuanced when analyzing how workers are legally classified. According to comprehensive payroll data analyzing 1.1 million U.S. employers, there is a stark divide between "independent contractors" (those filing 1099 tax forms) and "temporary employees" (those receiving short-term W-2 forms) 3.

Independent contractors tend to skew significantly older and are predominantly male (71% in 2024). Strikingly, 7.2% of 1099 contractors are over the age of 70, compared to just 3.8% of the broader workforce 3. This overrepresentation points to a lucrative sub-sector of semi-retired professionals, consultants, and advisors who leverage decades of industry experience to command high hourly rates while maintaining flexible schedules.

Conversely, temporary W-2 workers skew much younger, with 43% under the age of 30. These roles - often seasonal, on-call, or administrative - serve as entry points into the labor market for students or individuals seeking an income without long-term commitment. Unlike high-end consultants, these temp workers face significant job instability and lower wages, averaging just $15 per hour compared to the $25 per hour median for independent contractors 3.

Gender, Race, and Occupational Segregation

The gig economy is not immune to the systemic disparities found in traditional labor markets; in some cases, it exacerbates them. Globally, women make up roughly 42% of the online gig workforce, a rate higher than their 39.7% participation in the traditional labor market 6. The flexibility of platform work is highly attractive to workers balancing caregiving responsibilities.

However, the gender wage gap within the gig economy is notably severe. According to the World Economic Forum, the gender wage gap in platform work sits at nearly 30%, noticeably higher than the 20% gap observed in traditional employment markets 16. On average, women freelancers earn $22 per hour compared to $24 for men (roughly 92 cents on the dollar, though broader analyses indicate even wider disparities) 6. This gap is driven by occupational segregation (women disproportionately sorting into lower-paying micro-task or administrative gigs), differing project preferences, and systemic biases in algorithmic rate expectations 16.

Racial disparities are equally pronounced, particularly in the United States. Black and Latinx workers are disproportionately represented in the gig economy, particularly in the most precarious sectors. Black workers comprise 12.1% of the overall U.S. workforce but account for nearly 26% of temporary agency workers. Latinx workers make up 16.6% of the workforce but represent over 25% of the temporary workforce 17. These demographics are heavily concentrated in physical, location-based platform work - such as ride-hailing, warehouse fulfillment, and delivery - which typically offer lower wages, higher physical risks, and fewer legal protections than knowledge-based freelance work 17.

The Reality of Gig Pay: Gross Earnings vs. Net Take-Home

Evaluating the true earnings of a gig worker is arguably the most contested area of gig economy research. Platforms frequently highlight attractive gross hourly rates to recruit labor. However, independent academic studies, labor advocates, and tax analyses consistently reveal a massive gap between platform-reported gross pay and a worker's actual net take-home pay.

The Heavy Burden of Independence

In a traditional W-2 employment relationship, the employer absorbs a significant portion of operational friction. Employers pay half of the required payroll taxes (Social Security and Medicare), subsidize health insurance, provide paid time off, and cover direct operational expenses like equipment, fuel, and software licenses.

Gig workers, legally classified as independent contractors, bear all of these costs alone. From a tax perspective, U.S. independent contractors must pay the full 15.3% self-employment tax on their net earnings 1819. They must also make quarterly estimated tax payments, risking severe underpayment penalties if they fail to do so accurately 19.

The administrative burden of this independence is staggering. A 2024 study analyzing independent contractors in California found that navigating the tax filing system costs gig workers an average of $620 and 24 hours of labor annually. This makes tax compliance four times more expensive and three times more time-consuming for a gig worker than for a standard W-2 employee 21.

Furthermore, many gig workers suffer from acute gaps in tax literacy. The same study noted that two-thirds of platform workers receive no formal documentation (such as a 1099 form) of their earnings, and nearly half are completely unaware that they are legally allowed to deduct critical business expenses like gasoline, vehicle maintenance, and home office costs, leading to massive overpayment of taxes 21. This landscape is becoming even more complex; in 2024, the IRS reporting threshold for Form 1099-K was drastically lowered from $20,000 (and 200 transactions) to just $5,000, pulling millions of casual side-hustlers into a complex tax web for the first time 1820.

The Tax Incentive Illusion

The complexity of gig tax reporting has led to widespread misunderstandings about the actual growth of the platform economy. For years, economists observed a massive spike in individuals reporting self-employment income on their tax returns (Schedule SE) while standard labor force surveys showed no such rise 21. Many assumed this spike was purely driven by the explosion of Uber and DoorDash.

However, a landmark 2024 study published by the National Bureau of Economic Research (NBER) - conducted by researchers from Carnegie Mellon, Michigan State, and UChicago - debunked this assumption. By examining third-party IRS tax data, they found that while platform-mediated work has indeed grown since 2014, the actual amounts earned by most workers are incredibly small and mostly limited to occasional driving 2122.

The researchers concluded that the dramatic rise in self-employment tax reporting was not driven by the gig economy, but by tax incentives. Individuals in lower-income brackets became significantly more likely to self-report marginal gig earnings because doing so allowed them to qualify for lucrative refundable tax credits, such as the Earned Income Tax Credit (EITC) 2122. Once net earnings and deductible expenses (Schedule C) are calculated, many platform workers earn so little that they fall entirely below the filing threshold 22.

Case Study: Ride-Hailing and Delivery Earnings

The discrepancy between gross and net pay is most visible in the ride-hailing and food delivery sectors. While a platform like Uber has historically claimed that its active drivers earn upwards of $32 per hour, independent economic analyses paint a much starker picture 2324.

To understand true gig wages, analysts must deduct variable costs (fuel, battery charging, distance-based vehicle depreciation, and maintenance) and partially allocated fixed costs (commercial rideshare insurance, unlimited mobile data plans, and vehicle rental fees) 2425. Furthermore, true hourly wages must account for unpaid waiting time - the periods when a driver is logged into the app, burning fuel, but waiting for a dispatch.

The table below summarizes recent data comparing platform-reported metrics against independent academic and economic evaluations of net pay.

| Source & Scope | Reported Gross Pay | Estimated Net Pay (After Expenses) | Key Insight |

|---|---|---|---|

| HR&A Advisors (Chicago Study, 2024) 2425 |

$29.35 per hour (blended average) | $23.01 per hour | Driver expenses consume an average of $6.34 per hour (~21% of gross). Full-time drivers net slightly more ($23.54) due to economies of scale on fixed costs. |

| Gridwise Analytics (National App Data, 2025) 2328 |

Uber: $23.33 DoorDash: $16.61 TaskRabbit: $38.00 |

Not calculated (Gross data only) | Substantial variance exists between sectors. Physical labor/home repair (TaskRabbit) yields vastly higher gross hourly rates than food delivery. |

| Univ. of Oxford (UK Uber Drivers, 2016-2024) 2627 |

N/A | Hourly income fell from £22.20 to £19.06 (inflation adjusted, before operating costs) | The introduction of dynamic algorithmic pricing lowered driver earnings while increasing passenger fares. Unpaid wait times increased significantly. |

| Stanford/MIT Study (Historical Baseline) 31 |

N/A | $8.55 per hour (median profit) | Nearly half of drivers earned so little after vehicle depreciation and insurance that they qualified to report net losses on their tax returns. |

Algorithmic Pricing and Predatory "Take Rates"

A primary driver of declining net wages is the shifting "take rate" - the percentage of the total fare paid by the consumer that is kept by the platform rather than passed to the worker.

Historically, ride-hailing platforms operated on a fixed commission model, typically taking 20% to 25% of the fare. However, around 2022, major platforms fundamentally overhauled their pricing structures, implementing "upfront pricing." This system officially decoupled passenger fares from driver pay, utilizing opaque algorithms to determine the two figures entirely independently 2632.

The results of this shift have been heavily criticized by labor advocates. According to comprehensive analyses by the National Employment Law Project (NELP) and Columbia Business School, Uber's average take rate increased from roughly 32% to 42% by the end of 2024 3233. In the UK, the Oxford study noted a similar steady climb toward a 30% average 26.

However, averages obscure the reality of algorithmic variance. Driver-submitted "pay stubs" and independent tracking reveal that on individual, high-value rides, platforms sometimes extract 65% to 70% of the total fare 263233. The Oxford study specifically found that platforms concentrate their highest commissions on higher-fare trips. Consequently, the more a customer pays for a surge-priced ride, the smaller the percentage the driver actually receives 2627.

This algorithmic decoupling also impacts service quality. A 2025 study highlighted the practice of "forward-dispatching" - assigning a driver a new trip before they have completed their current drop-off. While platforms claim this reduces wait times, the data showed that forward-dispatched riders waited up to 60% longer (averaging over 11 minutes compared to 7 minutes) and paid up to 11% more per mile. Crucially, the drivers saw no increase in compensation for these premium-priced, forward-dispatched rides, allowing the platform to absorb the entire surplus profit 28.

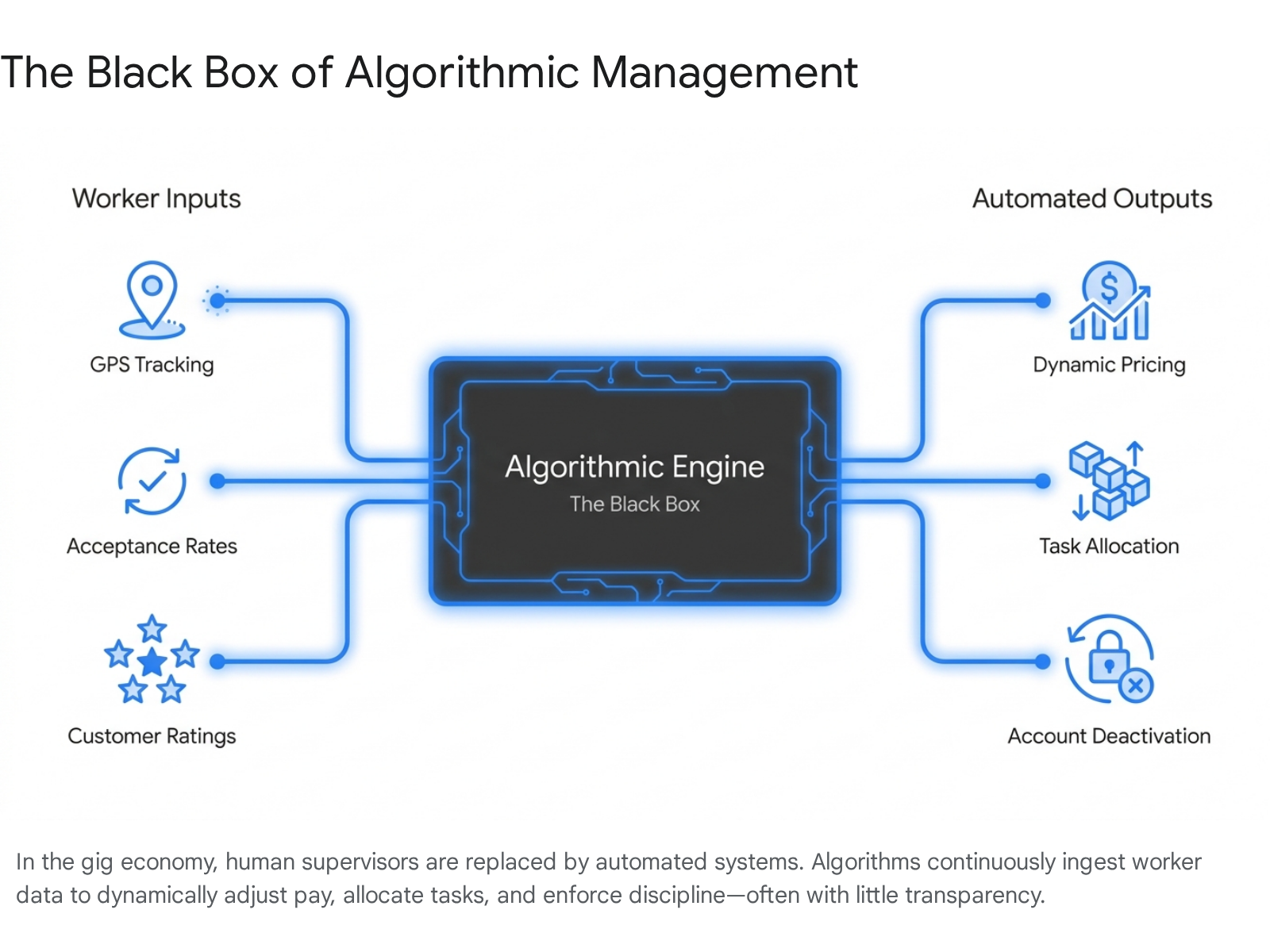

Algorithmic Management: The New "Boss"

The defining narrative of the gig economy is the promise of entrepreneurial freedom. Marketing materials routinely emphasize that platform workers can "log in when they want, log out when they want, and be their own boss" 293031.

However, labor sociologists and employment law experts argue that this autonomy is largely a mirage. In the platform economy, the traditional human manager has not been eliminated; they have simply been replaced by code. This phenomenon is known as "Algorithmic Management" (AM).

The Mechanisms of Digital Control

In conventional employment, a supervisor assigns tasks, monitors attendance, evaluates performance, and provides qualitative feedback. Under Algorithmic Management, these functions are entirely automated. Algorithms determine who receives a task, exactly how much they will be paid for it, the optimal route they must take, and whether their future earning potential will be restricted based on their current acceptance rate 2932.

The defining characteristic of AM is its profound opacity. These systems function as a "black box" 262931.

A driver does not know why the algorithm assigned them a specific ride, why their pay rate suddenly dropped, or why their account was abruptly suspended. Unlike a human manager who must justify a disciplinary action verbally or legally, an algorithm presents its decisions as unarguable faits accomplis on a smartphone screen 2933.

Furthermore, customer ratings - often presented by platforms as neutral feedback mechanisms - function as punitive tools of governance. A worker's ability to remain on a platform is entirely conditional on maintaining a specific algorithmic threshold. Because workers cannot bargain with or question the algorithm, they are forced into a state of hyper-compliance 293233.

The Psychological Toll: From Autonomy to Exhaustion

The impact of AM on worker well-being is complex and heavily researched. Applying the Job Demands-Resources (JD-R) theory, organizational psychologists view algorithmic systems as both a resource and a severe demand 3435.

When algorithms are transparent and provide real-time, objective feedback, they can actually enhance worker motivation through a "gameful experience." Clear goals, rapid payouts, and gamified milestones can trigger promotion-focused "job crafting," where workers actively try to optimize their performance to beat the system and increase their resources 4236.

However, for the vast majority of platform workers, AM operates as a relentless "techno-stressor." Continuous GPS surveillance, biometric monitoring, and the threat of automated deactivation deplete a worker's personal psychological resources 3435. This dynamic creates "illusory freedom." A gig worker might have the autonomy to choose when to log on, but once active, they must passively comply with strict constraints to access essential income 35. Empirical evidence underscores that this combination of intense surveillance and limited actual task autonomy leads to severe anxiety, emotional exhaustion, and high burnout rates 343544. Workers find themselves trapped in the "datafication" of work, forced to accept low-paying tasks simply to satisfy the algorithm and ensure future dispatch opportunities 2735.

Security, Vulnerability, and the Financial Safety Net

The classification of gig workers as independent contractors inherently strips them of the traditional social safety net. By avoiding an employer-employee relationship, platforms bypass obligations to provide minimum wage guarantees, overtime pay, workers' compensation for injuries, unemployment insurance, and paid sick leave 173345.

The Benefit Gap and Public Subsidization

The lack of benefits leaves the gig workforce highly vulnerable to macroeconomic shocks and personal emergencies. Recent surveys indicate that over 54% of gig workers have absolutely no access to employer-based benefits, leaving them exposed to the financial devastation of illness or disability 17. Approximately 45% of gig workers report that they could not handle a $400 emergency expense without resorting to borrowing 17.

Because platforms do not contribute to social security or unemployment funds, the financial risk is effectively externalized onto the public taxpayer. When gig workers face downturns, they must rely on non-contributory public programs like food stamps (SNAP) or Medicaid. According to the Economic Policy Institute and Human Rights Watch, roughly 15% of gig workers - including 13% of food delivery drivers - rely on food stamps 17. A tax analysis estimated that between 2020 and 2022, the state of Texas alone missed out on over $111 million in unemployment insurance contributions that platforms would have paid had their workers been classified as standard employees 33.

Spending Behavior and Financial Precarity

The precarious nature of gig income fundamentally alters how these workers participate in the broader economy. A comprehensive study by Harvard Business School researchers, analyzing the banking data of over 90,000 individuals, found striking differences in the spending habits of people holding multiple jobs (a proxy heavily populated by gig workers) compared to those with equivalent income from a single, stable full-time job 37.

The data revealed that gig workers are forced to practice severe financial austerity. Equivalent-income gig workers spend 17 percentage points less of their total take-home pay than standard employees. Specifically, they spend 16% less on core necessities (housing, utilities, healthcare), including a 19% reduction in doctor visits 37. They also spend significantly less on well-being "indulgences," cutting entertainment by 26%, travel by 17%, and dining out by 18%. Furthermore, gig workers are 29% less likely to allocate funds toward a mortgage, highlighting how income volatility directly impedes long-term wealth building and economic mobility 37.

Global Regulatory Shifts: The Fight for Classification

As the data surrounding low net pay, algorithmic exploitation, and taxpayer subsidization becomes undeniable, governments worldwide are moving aggressively to regulate the gig economy. The defining legal battle centers entirely on classification: should platform workers remain independent contractors, or should they be reclassified as employees?

The European Union Platform Work Directive

The most consequential and sweeping regulatory shift is occurring in the European Union. In October 2024, the EU officially adopted the Platform Work Directive, which entered into force in December 2024. All 27 EU member states have a strict deadline of December 2, 2026, to integrate the directive into their national laws 384839.

The Directive fundamentally alters the balance of power for Europe's estimated 43 million platform workers through two main pillars:

- The Presumption of Employment: The directive creates a legal presumption that platform workers are employees rather than self-employed contractors 383950. If a platform meets certain criteria of control - such as setting upper limits on pay, electronically monitoring performance, restricting task allocation, or enforcing conduct rules - the worker is automatically deemed an employee. Crucially, the directive reverses the burden of proof. It is no longer the worker's responsibility to sue for recognition; instead, the digital platform must prove in court that the worker is genuinely an independent business 4850.

- Algorithmic Transparency and Data Protection: The directive imposes unprecedented regulations on Algorithmic Management, surpassing even the requirements of the broader EU AI Act 38. Platforms are now explicitly banned from processing biometric data, psychological states, or private conversations. Most importantly, any decision to restrict, suspend, or terminate a worker's account can no longer be executed solely by an algorithm - human oversight is legally mandatory 485051.

By establishing these rules, the EU is intentionally increasing the cost of relying on casual gig labor, betting that the societal benefits of formal employment and tax revenue outweigh the frictionless business models of the tech platforms 51.

Patchwork Reforms: The US, UK, and Australia

Outside of the EU, regulatory approaches are heavily fragmented.

In the United States, the regulatory landscape is a volatile state-by-state battleground. In early 2024, the Biden administration issued new federal labor rules narrowing the definition of an independent contractor, intending to make it easier to classify gig workers as employees under the Fair Labor Standards Act 2. However, enforcement relies heavily on local jurisdictions. In states like California (under AB5), platforms have spent hundreds of millions of dollars on ballot initiatives to maintain the contractor classification while offering marginal, customized benefit concessions 2140.

Australia has opted for a middle-ground approach. Recognizing the "thin line" between contractor and employee, Australia introduced a hybrid "employee-like worker" category. This allows the Fair Work Commission to set minimum standards for pay, workplace health, safety, and unfair deactivation specifically for digital platform workers, without forcing them into full traditional employment 41.

South Africa is following a similar path. The proposed Employment Laws Amendment Bill 2025 aims to expand the definitions of "employer" and "employee" specifically to cover digital platform workers. If enacted, it would extend minimum wage coverage, paid leave, social security, and collective bargaining rights to gig workers who have historically operated in legal gray areas 4243. Similar baseline protections and gig-specific legislation have recently been introduced in Malaysia, Brazil, and Mexico 241.

The Global South: A Pathway to Formalization?

While policymakers in North America and Europe generally view the gig economy as a degradation of standard, secure employment, the narrative in the Global South is profoundly different.

In developing economies across sub-Saharan Africa, South Asia, and Latin America, the "traditional" 9-to-5 job with full benefits is a luxury. Informality is the norm. According to the ILO and the World Economic Forum, over 61% of the global workforce - roughly 2 billion people - is employed in the informal economy 4445. These individuals work as uncontracted street vendors, domestic care workers, unregistered masons, and independent motorcycle taxis. They operate entirely outside the purview of state taxation, labor law, and social protection 4445.

In these highly informal markets, the arrival of digital gig platforms is not dismantling the formal labor market; it is actively creating one.

Mechanisms of Institutional Change

Research into dominant regional platforms - such as Gojek in Indonesia and Rappi in Latin America - demonstrates that digital platforms serve as vital "on-ramps" to economic formalization 465947. When a platform enters an informal sector (like street-hailing motorcycle taxis), it aggregates disconnected, invisible workers into a structured ecosystem.

This formalization occurs through three specific institutional mechanisms 59: 1. Codifying Market Interactions: In the informal economy, transactions are cash-based and untraceable. Platforms force the adoption of digital payments. This provides unbanked workers with a verifiable financial history, which is essential for accessing future credit or micro-loans 4659. 2. Standardizing Work Practices: Platforms enforce strict safety standards, transparent geographic pricing, and service quality metrics. While this represents a loss of absolute freedom for the informal worker, it drastically reduces market uncertainty and protects consumers 5948. 3. Controlling Ecosystem Boundaries: By utilizing digital identities and customer ratings, platforms allow informal workers to build a portable, verifiable "CV" of their reliability. In areas where traditional educational credentials are rare, a digital reputation becomes a worker's most valuable asset 4459.

The Policy Opportunity for Developing Nations

For governments in the Global South, the platformization of informal work presents a once-in-a-generation policy opportunity. Rather than attempting to force top-down bureaucratic formalization (which historically fails due to high costs and red tape), states can leverage the platforms' existing infrastructure 464950.

Because platforms centralize remuneration through bank accounts rather than cash, governments finally have an access point to monitor labor data and collect tax revenue 46. In exchange, governments can implement "co-regulation" strategies. By partnering with platforms, states can seamlessly deliver universal social protections - such as micro-insurance, occupational safety nets, and healthcare - directly to gig workers who would otherwise remain completely marginalized 4650. As noted by development economists, AI and digital platforms, if governed equitably, possess the potential to act as the connective tissue that binds previously invisible informal labor to state-sponsored opportunity and agency 44.

Bottom line

The gig economy has undeniably matured from a fringe, supplementary side-hustle into a permanent, structural pillar of the global labor market. However, the foundational promise of unparalleled entrepreneurial freedom is increasingly compromised by opaque algorithmic management, predatory platform take-rates, and the severe financial precarity that comes from shouldering all operational costs and tax burdens independently. Moving forward, the defining economic battle will be regulatory: determining whether ambitious legal frameworks, like the EU's Platform Work Directive, can successfully force platforms to provide fair compensation and baseline security without destroying the frictionless flexibility that makes the model viable in the first place.