4 Scenarios for the Future of Global Trade

The global trading system is fracturing away from frictionless commerce toward a landscape defined by regional alliances, digital services, and strategic security. Current macroeconomic data and international forecasts point to four overlapping futures: the "friendshoring" of critical supply chains, the rise of the Global South and BRICS+ networks, an unprecedented boom in cross-border digital trade, and the persistent threat of protectionist stagnation.

The Macroeconomic Baseline: Resilience Amid Divergence

Before examining the divergent scenarios shaping the future of global commerce, it is necessary to establish the macroeconomic baseline from which these shifts are occurring. Following a 1.2% decline in global merchandise trade volumes in 2023 - driven by the long-term consequences of high energy costs, inflationary pressures, and the unwinding of pandemic-era supply chain bottlenecks - the global economy entered 2024 demonstrating surprising resilience 12.

Initial forecasts from the World Trade Organization (WTO) and the International Monetary Fund (IMF) projected a stabilization period. Global gross domestic product (GDP) growth was expected to hold steady at 3.2% in 2024 and 3.3% in 2025, while merchandise trade volume was forecasted to rebound with growth of 2.6% and 3.3% across the same years 13. This baseline assumed that inflation would decline steadily, from 6.8% globally in 2023 to roughly 4.5% by 2025, allowing central banks to ease restrictive monetary policies and replenish diminished fiscal buffers 3.

However, this stabilization is fragile. By early 2025, the WTO revised its forecasts downward, warning that world merchandise trade could actually decline by 0.2% in 2025 - and potentially plunge by 1.5% in a worst-case scenario - if ongoing trade tensions and policy uncertainties escalate 45. This divergence between steady GDP growth and volatile trade volumes highlights a fundamental shift: economic growth is increasingly decoupling from traditional, frictionless globalization.

For decades, the global trading system operated on a singular principle of cost efficiency. Corporations optimized their supply chains to source the cheapest labor and the most efficient logistics regardless of national borders 57. Today, that era has definitively ended. The world's major economies have transitioned from a "market-first" to a "security-first" policy paradigm, unleashing massive state interventions, export controls, and unprecedented tariffs 86. The assertion that globalization is entirely dead misreads the data; rather, globalization has shattered into competing regional systems and shifted its momentum from physical goods to digital services 7711. The trajectory of international commerce is currently tracking along four primary scenarios.

Scenario 1: Gated Globalization and the Friendshoring Shift

The first dominant scenario shaping the future of global trade is the deliberate rewiring of supply chains toward allied nations - a phenomenon known as "friendshoring" or "gated globalization." Driven by intense geopolitical rivalry, recurrent trade wars, and national security concerns, companies and governments are systematically relocating manufacturing dependencies to countries with shared political and economic interests 12814.

The Geopolitics of Supply Chain Restructuring

The COVID-19 pandemic and subsequent geopolitical shocks exposed the severe vulnerabilities of just-in-time delivery systems and single-nation dependencies 1. In response, corporate strategy has shifted away from optimizing solely for cost. A comprehensive Capgemini survey conducted in 2025 indicated that 73% of large organizations plan to friendshore operations. More significantly, 82% of executives reported plans to reduce their supply chain reliance on China - a sharp increase from 58% in 2024 8. By 2028, friendshoring strategies are projected to account for 41% of global manufacturing capacity 8.

This shift is already highly visible in macroeconomic trade data. Mexico has epitomized friendshoring success, officially bypassing China to become the United States' largest trading partner. Driven by shared borders, synchronized time zones, and the United States-Mexico-Canada Agreement (USMCA), US imports from Mexico reached $475 billion, compared to $427 billion from China 8. Similarly, Vietnam and India have emerged as major beneficiaries as electronics manufacturers seek viable alternatives to Chinese assembly hubs 815.

The Fragility of Economic Interdependence

The transition toward gated globalization is largely a reaction to the weaponization of economic interdependence. The relationship between Germany and China illustrates this fragility. Throughout the late 2010s and early 2020s, China was Germany's most important trading partner. However, by 2025, Germany's bilateral trade deficit with China had surged to over €89 billion, up from roughly €67 billion in 2024 5. While Germany historically supplied China with high-end machinery, by 2025, it was purchasing more capital goods from China than it was exporting 5.

European efforts to apply "selective interdependence" - protecting only the highest-tier technologies while maintaining trade in older goods - have proven difficult. Retaliation targeting upstream inputs, critical raw materials, and mature-node components can effectively bypass these safeguards. The late-2025 supply disruption at Nexperia, a Dutch-rooted company under Chinese ownership, demonstrated that supply chain risks extend far beyond cutting-edge artificial intelligence chips 5.

The Semiconductor Supremacy Race

Nowhere is the friendshoring shift more apparent, or more capital-intensive, than in the semiconductor industry. Recognizing that advanced microchips are the foundation of the modern digital economy and a vital component of national security, global powers are engaged in an aggressive industrial subsidy race 8.

The United States enacted the CHIPS and Science Act, dedicating $52.7 billion to lift America's global production share from 12% to 20% by 2030 9. The European Union matched this ambition with a $47 billion Chips Act, targeting the same 20% global share 9. In response, China activated its Third State Semiconductor Fund, allocating $143 billion toward advanced lithography and memory manufacturing to achieve 70% self-sufficiency by 2025 9.

This massive capital influx has fundamentally altered the geography of technology manufacturing across the Asia-Pacific and Middle East: * India: Approved a $2.75 billion Micron Technology plant, marking the country's first major foray into advanced semiconductor packaging 9. * Southeast Asia: Malaysia, Vietnam, and Singapore are rapidly expanding their testing and packaging networks to absorb mid-tier demand. Malaysia alone aims to attract roughly $105 billion (RM 500 billion) in investment through its National Semiconductor Strategy, securing multi-billion-dollar commitments from Intel, Infineon, and Texas Instruments 159. * The Middle East: Diversifying away from energy exports, the United Arab Emirates and Saudi Arabia are investing over $5 billion into semiconductor industrial zones 9. * Japan: Partnering closely with the United States on joint research initiatives, Japan is restructuring its global supply chains to reduce dependency on any single country, acting as a core pillar of allied friendshoring strategies 12.

While friendshoring mitigates direct geopolitical risks, it entirely eliminates the cost advantages of frictionless trade. Duplicated fabrication capacity and logistical redundancies have already increased global semiconductor production costs by an estimated 10% to 15% 9. This signals a new normal of costlier, albeit more politically secure, supply chains.

Scenario 2: The Multipolar Pivot and the Global South

The second major scenario is the emergence of a multipolar global order spearheaded by the Global South and institutionalized by the expanded BRICS+ coalition. Comprising over 130 nations outside the direct economic orbits of Western advanced economies and China, the Global South is actively crafting its own economic path, utilizing "multi-aligned" strategies to maximize domestic growth while remaining unencumbered by the geopolitical agendas of legacy powers 10.

The Economic Gravity Shifts South

If treated as a unified bloc, the Global South is poised to drive the lion's share of future global growth. Their combined GDP is projected to grow by an average of 4.2% annually through 2029, vastly outpacing the 1.9% average growth projected for advanced economies 10. Furthermore, as a primary destination for foreign direct investment (FDI), the Global South has surpassed advanced economies, attracting $525 billion compared to the developed world's $464 billion in recent tracking periods 10.

A defining characteristic of this scenario is the explosive growth of "South-South" trade. Trade among developing nations is projected to expand by 3.8% annually through 2033, noticeably faster than the 2.2% growth projected for traditional North-North trade 10. Consequently, nations in the Global South are moving away from cost-driven models. Rather than merely exporting raw natural resources, countries are leveraging them to create broader domestic value chains. For example, Indonesia has restricted raw nickel exports to build domestic lithium-ion battery manufacturing, while Chile has established a national lithium policy to add value before export 10.

China has decisively pivoted its export strategy toward these emerging markets. Facing high tariffs in the United States and weakening demand in Europe, China's exports to the Global South have surged. By late 2025, China was exporting roughly $1.6 trillion to the Global South - more than 50% higher than its combined exports to the US and Western Europe 7. Certain countries, such as Vietnam, Thailand, and Mexico, have positioned themselves as highly lucrative "connector economies," mediating trade flows between China and the West to bypass direct bilateral restrictions 1018.

The BRICS+ Expansion and Institutional De-Dollarization

The institutional anchor for this multipolar shift is the BRICS+ alliance. Expanding from its original five members (Brazil, Russia, India, China, South Africa) to officially include Egypt, Ethiopia, Iran, and the United Arab Emirates, the bloc now represents 54% of the global population and 42.5% of global GDP based on Purchasing Power Parity (PPP) 1112.

A central objective of the expanded BRICS+ group is to challenge the hegemony of the US dollar in international trade. The bloc is actively advancing the "BRICS Pay" initiative, a cross-border payment system designed to bypass the Western-dominated SWIFT network and facilitate trade settlements in local currencies 1112. By reducing dependence on the dollar, these nations seek to insulate their economies from Western sanctions and the ripple effects of US monetary policy 13.

While a unified, single BRICS currency remains largely theoretical, the institutional push toward bilateral currency swaps and decentralized digital platforms - such as China's Cross-Border Interbank Payment System (CIPS) - is establishing a parallel trade ecosystem 14. The bloc's New Development Bank (NDB) is also expanding its lending footprint, offering infrastructure and logistics financing as an alternative to the International Monetary Fund and the World Bank 1114. This architecture allows emerging economies to trade on what they perceive as more equitable terms, though it deeply accelerates the broader fragmentation of the global economy 1214.

Scenario 3: The Unprecedented Boom in Digital Trade

While physical merchandise trade faces steep tariffs and logistical bottlenecks, digital trade is expanding at an unprecedented rate, forming the third distinct future scenario. The trade of digitally enabled services - ranging from cloud computing and financial services to software licensing, telemedicine, and consulting - is rapidly becoming the most critical engine of global commerce 71115.

The Scale and Velocity of the Digital Economy

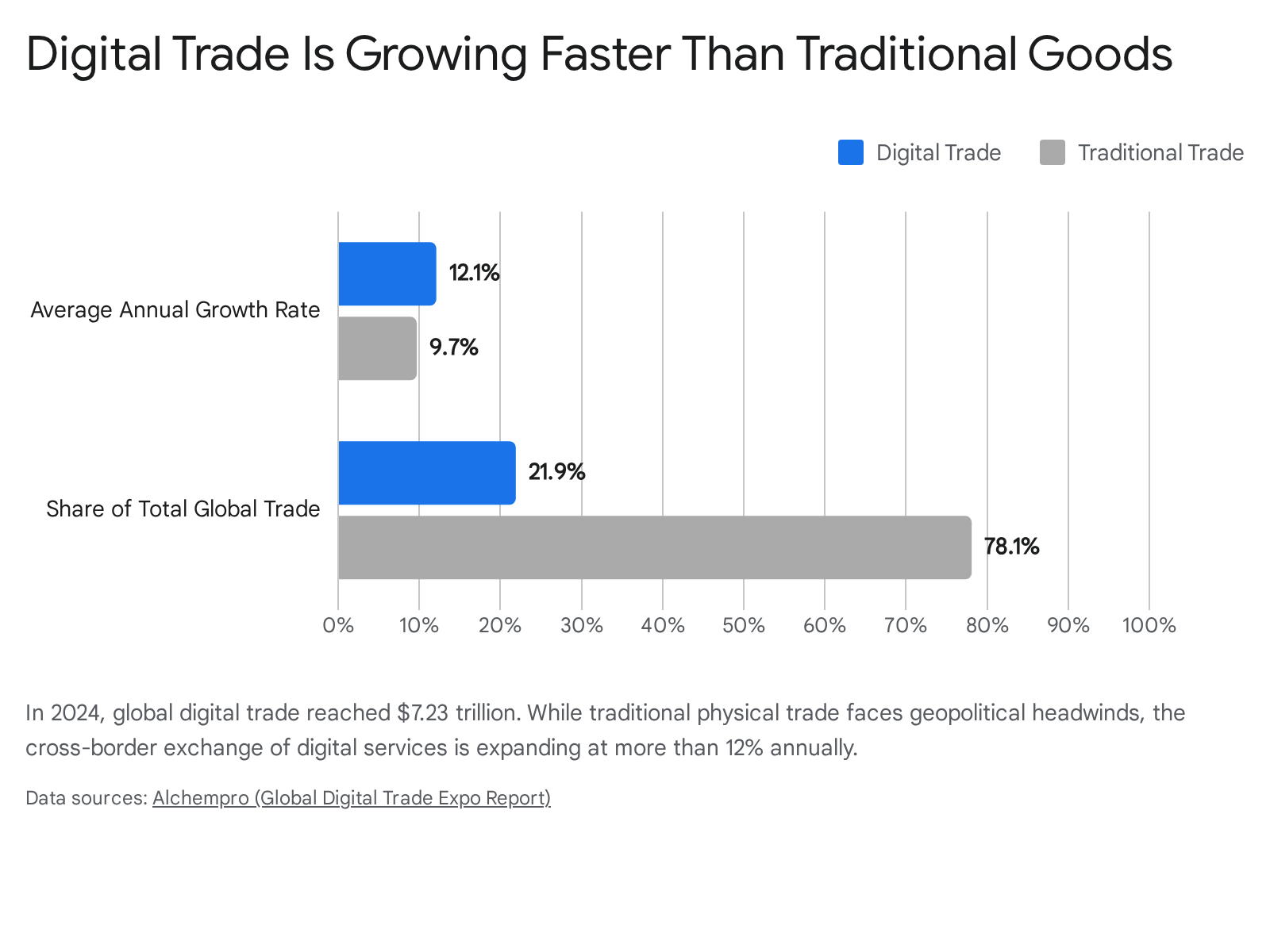

Data has evolved from mere business information into a highly valuable strategic commodity 7. Global digital trade reached $7.23 trillion in 2024, expanding at an average annual rate of 12.1% - a pace significantly faster than overall global trade growth, which stood at roughly 9.7% 1116. Digital transactions now account for approximately 22% of all international commerce 1116.

Digitally deliverable services specifically accounted for $5.4 trillion in global exports by 2025. While developed economies currently dominate this sector - originating roughly three-quarters of these exports (valued at $4.1 trillion) - developing economies are catching up rapidly 11. Digital service exports from developing nations grew at 12%, noticeably faster than the 9% growth recorded in advanced economies 11. This global reach means that geographical distance is far less of a barrier for digital services than it is for physical goods, offering small, geographically isolated economies unparalleled access to international markets 1517.

Regulatory Uncertainty and the African Digital Paradox

Despite its rapid growth, the digital trade landscape is entering a period of severe regulatory uncertainty. Since 1998, the WTO has upheld a moratorium on imposing customs duties on electronic transmissions. However, led by intense opposition from nations like Indonesia, India, and South Africa, this moratorium expired in March 2026 711. The end of the moratorium paves the way for the implementation of digital tariffs, as developing nations increasingly view domestic data generation as a key strategic resource that must be protected and monetized locally 7.

This regulatory shift presents a double-edged sword for emerging markets, particularly in Africa. Currently, the African continent holds only a 1% share of globally delivered digital services 18. To bridge this gap, initiatives like the WTO-World Bank "Digital Trade for Africa" project aim to develop connectivity infrastructure and digital skills across nations like Kenya, Rwanda, and Ghana 1819.

However, current trade policies undermine these efforts. African countries impose tariffs on imported digital goods (such as computers, networking equipment, and software) that are roughly three times higher than the rest of the world 20. While these high tariffs are intended to protect nascent local tech industries, they significantly stifle broadband penetration and digital literacy by making foundational technology unaffordable. World Bank research suggests that if African nations were to unilaterally eliminate tariffs on digital goods, their digital imports would soar by 8%, vastly improving the infrastructure necessary to participate in the global digital services boom 20.

Scenario 4: Protectionist Stagnation and Inflationary Drag

The fourth scenario represents the severe downside risk of aggressive geoeconomic fragmentation. As the United States, the European Union, and China engage in spiraling reciprocal tariff wars, global trade threatens to revert to protectionist levels not seen since the Great Depression, dragging down overall output and fueling persistent inflation 521.

The Escalation of the Average Effective Tariff Rate

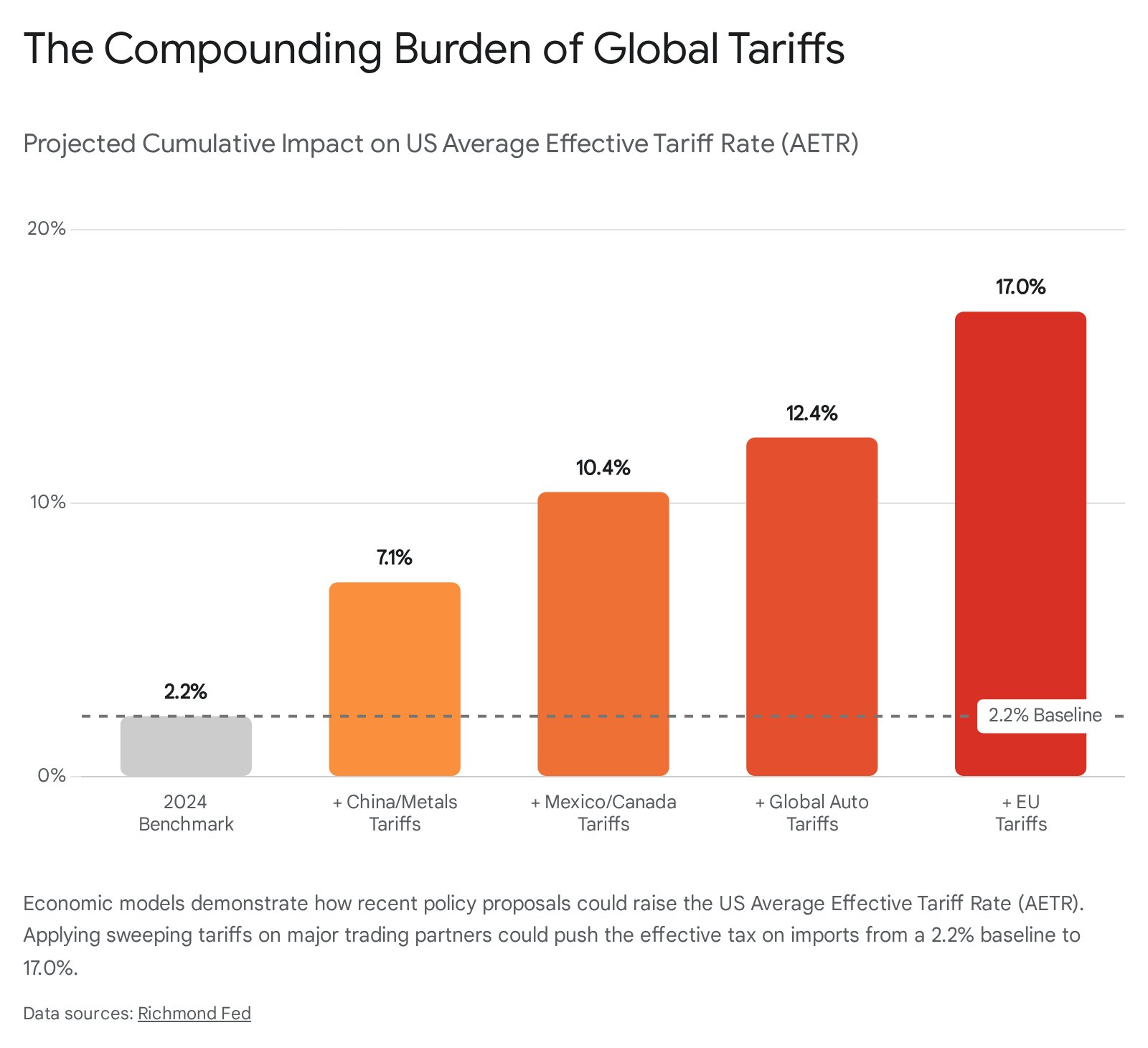

Trade policy has increasingly been weaponized to force geopolitical concessions and protect domestic industries, bypassing multilateral WTO frameworks in favor of bilateral coercion 5. The economic impact of these policies can be measured through the Average Effective Tariff Rate (AETR) - the average tariff paid across all imported goods.

Economic modeling by the Richmond Federal Reserve outlines a staggering potential escalation in trade barriers based on recent US administration proposals:

| Tariff Scenario | Applied Tariffs | Estimated US AETR | Core Impact |

|---|---|---|---|

| Baseline (2024) | Standard WTO MFN rates and existing 2018-2019 measures. | 2.2% | Represents the relatively low-friction baseline before the 2025 escalations 22. |

| China & Metals | +20% on all Chinese imports; +25% global aluminum and steel. | 7.1% | Spikes the specific effective rate on Chinese goods past 30%, forcing immediate supply chain diversion 22. |

| USMCA Disruption | +25% on non-USMCA compliant goods from Mexico and Canada. | 10.4% | Profoundly disrupts highly integrated North American manufacturing supply chains 22. |

| Global Auto Levies | +25% tariff on all motor vehicle imports regardless of origin. | 12.4% | Severe burden on transportation equipment sectors globally 22. |

| EU Retaliation | +25% tariff applied universally on all European Union imports. | 17.0% | Pushes effective rates for EU imports to nearly 30%, representing extreme protectionism 22. |

The Inflationary Pass-Through and Global Ripple Effects

The primary macroeconomic consequence of this protectionist stagnation is severe consumer inflation. Empirical research demonstrates that the "pass-through" rate of tariffs is often near 100%, meaning the cost burden is not absorbed by the foreign exporter, but rather falls almost entirely on domestic importing firms and everyday consumers 22.

In the United States, categories heavily exposed to international trade, such as durable goods (furniture, electronics, and vehicle parts), have seen sharp price increases directly correlated with tariff implementation timelines . By mid-2025, model-based estimates by the Federal Reserve indicated that tariffs were responsible for a 0.5 percentage point increase in annualized headline Personal Consumption Expenditures (PCE) inflation, and a 0.4 percentage point rise in core PCE, actively complicating central bank efforts to achieve price stability 3.

The damage extends rapidly across the global system. In Europe, the European Central Bank (ECB) was forced to repeatedly cut its benchmark interest rate - reaching 2.00% by June 2025 - to cushion the economic fallout of these trade tensions 23. The EU faces a distinct vulnerability known as the "second China shock." As Chinese manufacturing is blocked from the US market by prohibitive 60% to 100% tariffs, Beijing redirects its excess industrial capacity into European and Global South markets. This diversion floods regional economies with subsidized goods, intensifying competition and threatening domestic steel, electronics, and machinery producers 2324. Ultimately, long-term models suggest that the combination of severe global trade fragmentation and technological decoupling could result in staggering economic losses, wiping out up to 7% of total global output 6.

Synthesizing the Future of Commerce

The four scenarios outlined above are not mutually exclusive; rather, they are distinct, interacting forces acting simultaneously on different sectors and regions of the global economy.

| Scenario | Core Driver | Primary Geographic Focus | Main Economic Impact |

|---|---|---|---|

| 1. Gated Globalization | National security, supply chain resilience, and geopolitical alignment. | US, EU, Japan, Mexico, India, Vietnam. | Increased manufacturing costs, massive state subsidies, and duplication of capital infrastructure (e.g., semiconductors). |

| 2. Rise of the Global South | Multipolar diplomacy, resource nationalism, and unaligned pragmatism. | BRICS+ nations, ASEAN, Latin America, Africa. | De-dollarization initiatives (BRICS Pay), surging South-South trade, and bypassing Western financial institutions. |

| 3. Digital Trade Boom | Cloud computing, cross-border data flows, and remote services. | Advanced economies (currently), with high growth potential in emerging markets. | Services trade rapidly outpaces physical goods; new regulatory battlegrounds emerge over data sovereignty and digital tariffs. |

| 4. Protectionist Stagnation | Reciprocal tariffs, economic nationalism, and bilateral coercion. | Global, but heavily impacting the US, China, and EU trade triangles. | Rising consumer inflation, depressed global GDP output, and severe disruptions to long-standing supply chains. |

Bottom line

The assertion that globalization is dead is fundamentally inaccurate; the global economy is merely undergoing a profound and often painful rewiring. International trade is aggressively shifting from a paradigm of frictionless cost-efficiency to one defined by political security, regional alliances, and digital services. While the boom in cross-border data flows and the rise of autonomous Global South economies offer massive, decentralized opportunities for future growth, the looming threat of retaliatory tariffs and geoeconomic fragmentation threatens to burden consumers with persistent inflation and heavily drag down overall global GDP.