5 Reshoring Scenarios for the Future of Manufacturing

The future of global manufacturing is shifting from a centralized, cost-chasing model to a diversified network that prioritizes supply chain resilience, automation, and geopolitical security. Driven by tariff policies, post-pandemic vulnerabilities, and advanced robotics, companies are abandoning single-source dependencies in favor of "China Plus One" expansions and high-tech domestic reshoring. While this transformation promises greater operational stability, it also ushers in a new era of structural inflation, complex logistics, and an intense global competition for technical talent.

The End of the "Factory of the World" Era

For decades, the global manufacturing paradigm was defined by a relentless pursuit of the lowest unit cost. This dynamic culminated in China's uncontested reign as the "factory of the world." However, the arithmetic that sustained this model has steadily fractured. Average manufacturing wages in China have tripled since 2010, eroding the original cost arbitrage that drove mass offshoring in the late 20th century 1. Compounded by a volatile tariff environment, geopolitical brittleness, and the lingering scars of pandemic-era supply chain collapses, the strategic calculus of multinational corporations has fundamentally changed.

In recent years, reshoring and foreign direct investment (FDI) initiatives have surged. In 2024 alone, such efforts brought approximately 244,000 manufacturing jobs back to the United States, pushing the cumulative total past two million since 2010 234. By 2026, the conversation has moved entirely from theoretical boardroom discussions to operational execution. Manufacturers are no longer asking whether to diversify their supply chains, but where to go, how fast they can scale, and at what cost 13.

Yet, the idea of a complete "decoupling" from Asian manufacturing remains a political myth rather than an economic reality. The industrial ecosystems established over the last forty years are too deeply integrated to be cleanly severed. Instead, the future of manufacturing is fracturing into a complex spectrum of strategies. By examining current macroeconomic data, corporate investment trends, and technological breakthroughs, we can identify five distinct scenarios defining the future of global supply chains.

| Scenario | Primary Catalyst | Key Geographies | Core Operational Challenge | Estimated Economic Impact |

|---|---|---|---|---|

| 1. The "China Plus One" Web | Geopolitical de-risking & rising Chinese labor costs | Vietnam, India, Malaysia, Mexico | Upstream dependency on Chinese components | Sustains Asian trade dominance but shifts final assembly locations. |

| 2. Regional Fortresses | Need for fast transit times & regional trade pacts | Mexico, Eastern Europe (Poland), North Africa | Policy uncertainty, infrastructure, and taxation | Massive regional FDI shifts, but constrained by local political volatility. |

| 3. Tech-Charged Reshoring | Smart manufacturing, AI, and government subsidies | United States, Western Europe | Severe shortage of skilled technicians and engineers | Reindustrialization of advanced economies; net positive for high-tech GDP. |

| 4. Decentralized Micro-Factories | 3D printing (Additive Manufacturing) & biotech advances | Highly localized (near specific consumer/patient hubs) | Regulatory standardization and initial capital expenditure | Disruption of mega-factories; enables hyper-customization and fast crisis response. |

| 5. Structural Inflation | Tariffs and higher domestic production costs | Global Consumer Markets | Passing increased "Total Cost of Ownership" to consumers | Persistent inflation pressure; potential reduction in global discretionary spending. |

Scenario 1: The "China Plus One" Supply Chain Web

For the vast majority of multinational corporations, fully abandoning Chinese manufacturing is neither practical nor mathematically viable. China accounts for nearly 30% of global manufacturing output - roughly $4.85 trillion in 2025 - and boasts tightly integrated industrial clusters that no other country has replicated at scale 5. Instead, the dominant strategy for 2026 and beyond is "China Plus One."

This strategy dictates that a company maintains its primary production base in China to serve both the massive Chinese domestic market and specific global routes, while simultaneously spinning up secondary, redundant capacity in a separate geopolitical jurisdiction 156. This dual-track approach provides a critical contingency plan that mitigates the risk of a single-point failure caused by port closures, evolving export controls, or sudden tariff hikes 667.

Strategic Drivers and Key Beneficiaries

In 2026, the primary beneficiaries of this strategy are aggressively competing for foreign capital, each offering a radically different value proposition for enterprises racing to de-risk their operations:

- Vietnam: Acting as the primary release valve for Chinese manufacturing, Vietnam has absorbed tens of billions in foreign direct investment, attracting over $36 billion in 2025 alone 1. Its proximity to China means that sub-components can be trucked across the border with minimal disruption, allowing finished goods to be shipped to Western markets without triggering tariffs applied to Chinese-origin goods 1. The Hanoi - Ho Chi Minh City manufacturing corridor now rivals traditional Chinese hubs in density for electronics, semiconductors, and footwear.

- India: Viewed as the "long game" for supply chain diversification, India is leveraging its 1.4 billion population and aggressive government subsidies, such as the Production-Linked Incentive (PLI) scheme, to attract mega-factories 1. With labor costs roughly 30% to 40% cheaper than Vietnam for equivalent skill levels, India is positioning itself as a powerhouse in pharmaceuticals, chemicals, and consumer electronics 1.

- Malaysia: While India and Vietnam are rapidly developing their capabilities, Malaysia captures high-end investments due to its mature industry, boasting over five decades of semiconductor manufacturing experience and a stance of strategic non-alignment 6.

The Upstream Dependency Paradox

Despite the massive capital flight to these alternative nations, a critical vulnerability remains: an indirect, deeply entrenched dependency on China. While United States import shares from Vietnam and Mexico have surged, those countries' own imports from China have increased at an even faster rate 58. Between 2017 and 2022, Vietnam's import share from China grew from 28% to 33%, and Mexico's grew from 18% to 20% 8.

In industries like textiles and electronics, a Vietnamese factory might handle the final assembly, but the raw materials, complex tooling, and critical internal components are overwhelmingly sourced from Chinese suppliers 57. Because China produces the materials that Southeast Asian factories still import, the global supply chain is not necessarily decoupling; it is merely adding a geographic buffer zone, elongating the chain rather than replacing it 59.

Chinese Firms Expanding Abroad

Adding to the complexity, Chinese firms are actively participating in the supply chain migration. Facing steep tariffs and export controls in advanced economies, Chinese manufacturers are aggressively investing in Mexico and Southeast Asia to bypass trade barriers 91011.

For example, industrial parks in Mexico are seeing a growing presence of Chinese automotive suppliers, furniture manufacturers, and battery makers attempting to utilize free trade agreements to enter the United States duty-free 1013. This reality means that even as Western companies attempt to reshore or nearshore, they often find themselves operating alongside - or purchasing components from - the very Chinese firms they sought to diversify away from.

Scenario 2: Regional Fortresses and Nearshoring

While the China Plus One strategy focuses on Southeast Asia, a parallel movement is creating highly integrated, regionalized trade fortresses. Driven by the need to drastically cut transit times from weeks to days, companies are establishing "nearshore" operations on the immediate borders of the world's largest consumer markets.

Mexico and the North American Ecosystem

For the United States, Mexico is the undisputed center of gravity for nearshoring. Overland shipping between Mexico and the U.S. takes just two to five days, making agile, just-in-time inventory strategies viable again 112. Propelled by the United States-Mexico-Canada Agreement (USMCA), Mexico surpassed China in recent years to become the top U.S. trading partner, reaching nearly $930 billion in total trade in 2024 131415. Foreign direct investment into Mexican manufacturing also hit a record $36.1 billion in 2024, largely driven by the automotive, aerospace, and medical device sectors 1.

However, Mexico's nearshoring boom is currently colliding with severe institutional and political headwinds. As the scheduled 2026 review of the USMCA approaches, extreme uncertainty has gripped the market. Companies are highly sensitive to unpredictability regarding fiscal governance, potential retaliatory tariffs, and ongoing disputes over double taxation 131416.

Despite the geographic advantages, Mexican economic growth projections for 2026 sit sluggishly between 0.6% and 1.5% 13. The paradox of nearshoring in Mexico is illustrated by domestic investment figures: between mid-2024 and late 2025, public investment in Mexican infrastructure dropped by a staggering 64% 16. This exposes the reality of a country perfectly positioned geographically, but struggling to provide the predictable regulatory and infrastructural environment required to sustain long-term mega-projects.

The European Pivot to the Periphery

A similar nearshoring dynamic is fundamentally reshaping Europe. Sluggish economic growth - projected at just 1.1% to 1.3% for the Euro area in 2026 - combined with the threat of geopolitical instability and demographic constraints, has forced European manufacturers to redesign their logistics networks 1718.

Instead of relying on fragile, single-source long-haul routes from East Asia, European supply chains are adopting "bend, don't break" architectures 19. This involves shifting origin points to Eastern Europe (such as Poland and Romania) and North Africa (Morocco and Egypt), alongside an increased reliance on Turkey 19.

By creating more intra-European flows and regional hubs, European retailers and manufacturers aim to flex delivery routes and stock positions instantly when disruption hits 19. Companies that treat resilience as a core design requirement are successfully navigating climate events and labor actions, while those holding onto optimized, single-source Asian models continue to suffer margin-erasing stockouts 19.

Scenario 3: Tech-Charged Reshoring and Automation

The most politically celebrated scenario is pure "reshoring" - bringing manufacturing back to the domestic soil of the United States and Western Europe. However, there is a pervasive public misconception regarding what modern reshoring actually entails.

The Myth of Returning 1970s Manual Labor

The widespread belief that reshoring will restore the massive, manual-labor assembly line jobs of the 1970s is a profound myth 202122. At its peak in 1979, U.S. manufacturing employed almost 20 million people 23. Today, despite a massive surge in factory construction fueled by federal incentives like the CHIPS and Science Act, factory headcount is actually shrinking in some legacy sectors 2324.

The primary bottleneck preventing a massive influx of traditional manufacturing jobs is the severe demographic and skills cliff. Roughly 26% of the U.S. manufacturing workforce is currently eligible for retirement, creating a capability transfer problem on a generational scale 24. Even without a surge in reshoring, 2.1 million manufacturing jobs are forecast to go unfilled by 2030 25. Furthermore, the manufacturing "wage premium" - which saw factory workers earn 40% more than other sectors in the 1960s and 1970s - has collapsed to roughly 2% nationally 24. Today, an entry-level worker can often earn a comparable starting wage in a climate-controlled fulfillment center or the gig economy as they can performing manual labor on a factory floor 2426.

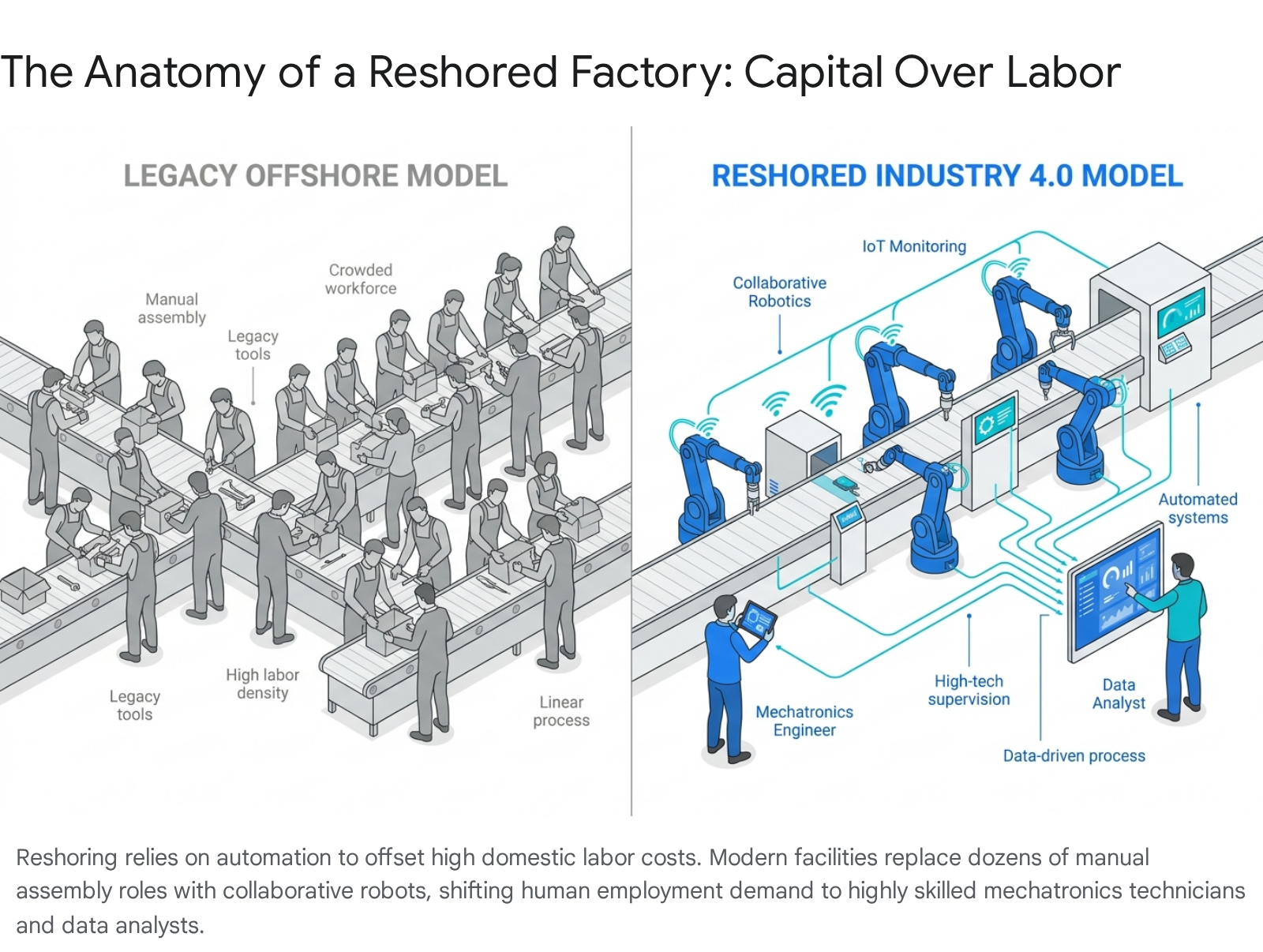

Capital Over Labor: The Automation Imperative

To offset domestic labor costs that can be dramatically higher than in Asia, reshored facilities must be hyper-efficient. Automation is not merely a feature of reshoring; it is the fundamental prerequisite that makes domestic production economically viable.

A staggering 95% of U.S. industrial organizations plan to introduce new automation over the next three years to support reshoring efforts and combat labor shortages 27. A highly automated plant running collaborative robots, machine vision inspection, and Internet of Things (IoT) monitoring can match the unit economics of a labor-intensive overseas facility 4.

Manufacturers implementing these Industry 4.0 technologies are reaping massive benefits, including 15% to 30% improvements in labor productivity and up to 50% reductions in machine downtime 3.

The Rise of Mechatronics and High-Tech Manufacturing

Because automation handles the repetitive tasks, the types of jobs being created are changing radically. In 2024, 88% of reshoring job announcements were for high-tech or medium-high-tech products, heavily concentrated in electrical equipment, electric vehicle batteries, and semiconductors 427. By 2025, that metric rose to 90% 27.

The industry does not need traditional line assemblers; it desperately needs mechatronics engineers, robotics technicians, and software developers to keep the automated systems running. As automation scales, manual roles like patternmakers and basic machine operators face an estimated 97% to 99% risk of total displacement 2128. The companies that win the reshoring race will not simply be the ones that purchase the most robots, but the ones capable of upskilling a modern workforce to manage complex, data-driven factory floors 24.

Scenario 4: Decentralized Micro-Factories

Looking beyond immediate supply chain reshuffling, a more radical scenario is taking shape: the shift from massive, centralized "mega-factories" to a network of decentralized micro-factories. Propelled by the principles of Industry 4.0, this scenario envisions production moving directly to the point of consumption.

Additive Manufacturing and 3D Printing

Traditional manufacturing relies on subtractive processes and massive economies of scale, requiring goods to be produced in millions of units in concentrated hubs and shipped globally. Additive Manufacturing (AM), commonly known as 3D printing, disrupts this paradigm entirely. By producing components directly from digital design files layer-by-layer, AM allows for rapid, customized manufacturing with minimal tooling and near-zero supply chain lag 2930.

This is already making waves in heavy industries like construction and aerospace. With large-scale robotic arms pumping specialized concrete or printing metal alloys, components can be printed autonomously on-site or in regional hubs 2931. This drastically reduces the required labor, physical footprint, capital investment, and complex international logistics typically associated with heavy industry 29.

Biotech and Modular Cleanrooms

The decentralized model is particularly critical in the biopharmaceutical sector. Historically, producing medicine required massive, centralized facilities. Today, companies are treating the manufacturing facility itself as "equipment" via modular and mobile cleanrooms 34.

This approach allows pharmaceutical companies to rapidly deploy vaccine production or personalized gene therapies directly to regional hospitals or pandemic hotspots, bypassing global supply chain bottlenecks entirely 34. By shrinking the footprint of production, treatments can be hyper-localized, reducing lead times and improving patient outcomes.

Human-in-the-Loop Cyber-Physical Systems

Academic foresight models describe these decentralized setups as highly complex cyber-physical systems 32. Despite their high levels of automation, these micro-factories will not be completely "lights out." They will require a "human-in-the-loop" to provide fine-grain oversight, mediate complex problem-solving, and manage exceptions via advanced software interfaces 32. This scenario envisions a global manufacturing network where the physical product is made locally, but the engineering, digital design, and quality control are managed globally through the cloud.

Scenario 5: The Structural Inflation Trade-Off

The ultimate consequence of moving away from hyper-optimized, low-cost Asian mega-factories is that global goods will simply cost more to produce. Whether a company adopts a China Plus One strategy, nearshores to Mexico, or heavily automates a new facility in the American Midwest, the transition requires massive capital expenditure. Energy costs, labor wages, and environmental compliance are all significantly higher in Western and nearshore markets compared to legacy offshore hubs 3334.

From Ex-Works to Total Cost of Ownership (TCO)

To justify these moves, procurement executives are changing how they calculate value. They are moving away from traditional "Ex-Works" pricing - the raw cost of the product sitting at the factory door in China - to a "Total Cost of Ownership" (TCO) model 2535.

TCO accounts for the hidden costs of offshoring that were previously ignored: the carrying cost of a six-week ocean freight lead time, the risk of geopolitical disruptions, intellectual property theft, and incoming carbon taxes. By factoring in a 30% to 50% reduction in supply chain disruption costs, domestic manufacturing suddenly looks highly profitable over a long time horizon 335. However, while the business risk is mitigated, the absolute baseline production price of the physical item still rises.

The 2026 Macroeconomic Clash

Because businesses generally pass these increased costs directly to the consumer, the reshoring megatrend is recognized by economists as a powerful driver of structural inflation. As we move through 2026, a fierce debate is occurring among leading financial institutions regarding exactly how high this structural inflation will go:

- The High-Inflation Warning: Analysts at the Peterson Institute for International Economics (PIIE) argue that consensus forecasts are overly optimistic. Driven by the delayed pass-through effects of global tariffs, structurally tighter labor markets, and the massive upfront costs of supply chain restructuring, PIIE warns that U.S. inflation could surprise to the upside, potentially exceeding 4% by the end of 2026 3436.

- The Controlled-Descent View: Conversely, institutions like Goldman Sachs argue that while energy shocks pose risks, core inflation is successfully decelerating. As the initial shock of tariff pass-throughs runs its course and automated productivity kicks in, they project core inflation will settle down toward a much more manageable 2.1% to 2.2% by the end of 2026 4037.

Passing Costs to the Consumer

Regardless of which macroeconomic forecast proves accurate, the microeconomic reality for businesses is settled. Surveys indicate that a staggering 86% of manufacturers plan to pass on at least some of their tariff and reshoring-related cost increases directly to consumers 4243.

Consumers are already highly sensitive to these shifts. As of early 2026, nearly 78% of consumers state that inflation has impacted them somewhat to overwhelmingly over the past three years 43. In this scenario, the future of global manufacturing achieves the desired resilience and geopolitical security that governments are demanding, but it is paid for by a permanent reduction in consumer purchasing power and discretionary spending.

Bottom line

The future of manufacturing is not a simple reversal of globalization, but rather a complex fracturing of it. While the "China Plus One" strategy and nearshoring to regions like Mexico and Eastern Europe will dominate the medium term, the ultimate success of Western reshoring relies entirely on massive capital investments in automation and robotics to overcome severe skilled labor shortages. Ultimately, consumers, executives, and policymakers must accept the fundamental trade-off of this new era: achieving highly resilient, localized, and technologically advanced supply chains will inevitably come at the permanent cost of higher structural inflation.