Estimate Your Real College Cost with a Net Price Calculator

A college net price calculator is a federally mandated online tool that estimates a student's actual out-of-pocket expenses by subtracting anticipated grants and scholarships from a school's total cost of attendance. To generate an accurate estimate, families must use specific prior-prior year tax data, meticulously report assets according to newly updated federal rules, and carefully differentiate between guaranteed gift aid and misleading student loan projections. Because the underlying software and federal formulas vary wildly from campus to campus, these tools should be viewed as early planning benchmarks rather than binding financial promises.

The Gap Between Sticker Price and Net Price

The published cost of a college education - often referred to as the sticker price - is rarely the amount that families actually pay. The published cost of attendance encompasses tuition and fees, alongside housing, food, books, course materials, supplies, transportation, and estimated personal expenses 12. When families look at these comprehensive figures, the numbers can induce profound sticker shock. For the 2024 - 2025 academic year, the average published tuition and fees for a full-time undergraduate student at a private nonprofit four-year institution was $43,350, while public four-year out-of-state institutions averaged $30,780, and public four-year in-state institutions averaged $11,610 2.

However, looking solely at the published price is fundamentally misleading. The vast majority of undergraduate students do not pay the full sticker price because they receive institutional, state, or federal grant aid 2. General subsidies provided by state governments, local appropriations, private philanthropy, and institutional endowments allow colleges to charge students less than the actual cost of instruction, and direct grant aid further reduces the burden on individual families 3. The remaining balance that a student and their family must cover after all grant aid is subtracted is defined as the net price 13.

To bridge the information gap and help families understand actual affordability, the Higher Education Act of 1965 was amended to mandate transparency 4. Since October 2011, any postsecondary institution participating in Title IV federal student aid programs that enrolls full-time, first-time degree-seeking undergraduate students has been legally required to host a net price calculator on its website 467. The primary objective of these tools is to allow prospective students to input their specific demographic and financial information to discover what students in similar financial situations paid to attend that institution in previous academic years 485.

Despite this federal mandate, the landscape of net price calculators remains highly decentralized. The U.S. Department of Education does not formally approve institutional calculators; rather, colleges are responsible for self-regulating their compliance with the statute 4. Consequently, institutions have immense latitude in designing their calculators, deciding which data points to include, and determining how to present the final financial estimate 8. This flexibility has resulted in a fragmented system where some calculators provide highly precise, individualized estimates, while others offer vague averages that can severely mislead prospective students 810.

| Institution Type (2024-2025 Averages) | Average Published Tuition & Fees | Average Net Tuition & Fees Paid |

|---|---|---|

| Public Two-Year (In-District) | $4,050 | Varies (often fully covered by grants) |

| Public Four-Year (In-State) | $11,610 | $2,480 |

| Public Four-Year (Out-of-State) | $30,780 | Varies heavily by regional discounts |

| Private Nonprofit Four-Year | $43,350 | $16,510 |

Data reflects national averages for first-time, full-time undergraduate students, demonstrating that net tuition is historically a fraction of the published sticker price 2. Note that these figures isolate tuition and fees; total net cost of attendance (including housing and food) will be higher.

Step-by-Step: Preparing for the Net Price Calculator

Because a net price calculator functions by approximating the complex algorithms used by federal and institutional financial aid offices, the output is entirely dependent on the precision of the input 66. Families who attempt to guess their financial metrics often receive inaccurate net price estimates, leading to poor enrollment decisions. Before accessing any college's calculator, users must gather specific documentation and understand the chronological rules governing financial aid data.

Navigating the Prior-Prior Year Tax Rule

The most frequent error families make when using a net price calculator is referencing the wrong year's financial data. The Free Application for Federal Student Aid (FAFSA) - the gateway to all federal and most institutional need-based aid - operates on a "prior-prior year" rule 121314. This regulation dictates that financial aid eligibility is calculated using income data from the tax year two years prior to the start of the college academic year 1215.

The rationale behind the two-year lookback is to allow families to complete their financial aid applications using tax returns that have already been filed and processed by the IRS, rather than waiting to file current-year taxes and delaying the college admissions timeline 1415. Therefore, a high school junior whose base income year has just ended must understand that their parents' financial decisions in that specific calendar year will dictate their college aid 13. Using current income estimates rather than the exact prior-prior year tax return will inherently corrupt the net price calculator's output.

| Student's Current Status | College Academic Year | Required Federal Tax Return Year |

|---|---|---|

| High School Senior (Class of 2025) | Fall 2025 - Spring 2026 | 2023 Tax Return 15 |

| High School Junior (Class of 2026) | Fall 2026 - Spring 2027 | 2024 Tax Return 1416 |

| High School Sophomore (Class of 2027) | Fall 2027 - Spring 2028 | 2025 Tax Return 13 |

If a family's financial situation has drastically changed since the prior-prior year - such as experiencing a sudden job loss, the death of a spouse, or overwhelming medical bills - the standard calculator estimate will not reflect their current reality 78. In these scenarios, the calculator relies strictly on the older, higher income. Families must eventually file a special circumstances appeal directly with the college's financial aid office to have their more recent, reduced income taken into consideration 8199.

Gathering Required Financial and Academic Documents

To generate a meaningful estimate, users should compile the same documents they would need to formally file the FAFSA and the CSS Profile. A comprehensive net price calculator will require detailed information from both the student and the parents 610.

First, families must locate their Adjusted Gross Income (AGI) from the corresponding prior-prior year federal tax return, as this is the foundational metric for determining need-based aid eligibility 6. Additionally, W-2 forms and records of untaxed income are necessary. Users frequently make the mistake of omitting untaxed income, such as voluntary contributions to tax-deferred retirement accounts, child support received, or worker's compensation, which many institutional formulas add back into the family's total resources 6911.

Second, the calculator will assess family assets. Parents must provide the current balances of all checking, savings, and cash accounts, alongside the net worth of investments, investment real estate, and sometimes the primary family home 2612. The federal methodology assesses parent assets at a maximum rate of 5.64% of their value (above a certain protection allowance), while student-owned assets are assessed much more harshly at 20% 24. Therefore, placing savings in the student's name rather than the parents' name will result in a higher expected contribution and a higher net price.

Finally, academic records are crucial. While the federal government only awards need-based aid, colleges themselves award billions of dollars in merit-based scholarships 813. A robust net price calculator will ask for the student's unweighted Grade Point Average (GPA), standardized test scores (SAT or ACT), and high school class rank 62413. If a student fails to input these academic metrics, the calculator cannot estimate potential merit scholarships, potentially making the college appear far more expensive than it will ultimately be.

Evaluating the Three Main Types of Calculators

Because the Department of Education affords colleges flexibility in how they build their required calculators, the user experience varies tremendously. Depending on the software an institution deploys, a family might spend less than a minute answering surface-level questions, or they might spend thirty minutes digging through tax schedules 1314. Generally, the simpler the calculator, the less accurate the net price estimate will be 14.

The Federal Template (The Baseline)

To assist colleges in meeting the 2011 transparency mandate, the federal government released a basic Net Price Calculator template 4. This template operates on a rudimentary lookup table populated by aggregate FAFSA data; it matches a family's estimated contribution against the median grant aid awarded to students in that same contribution bracket during a previous year 413.

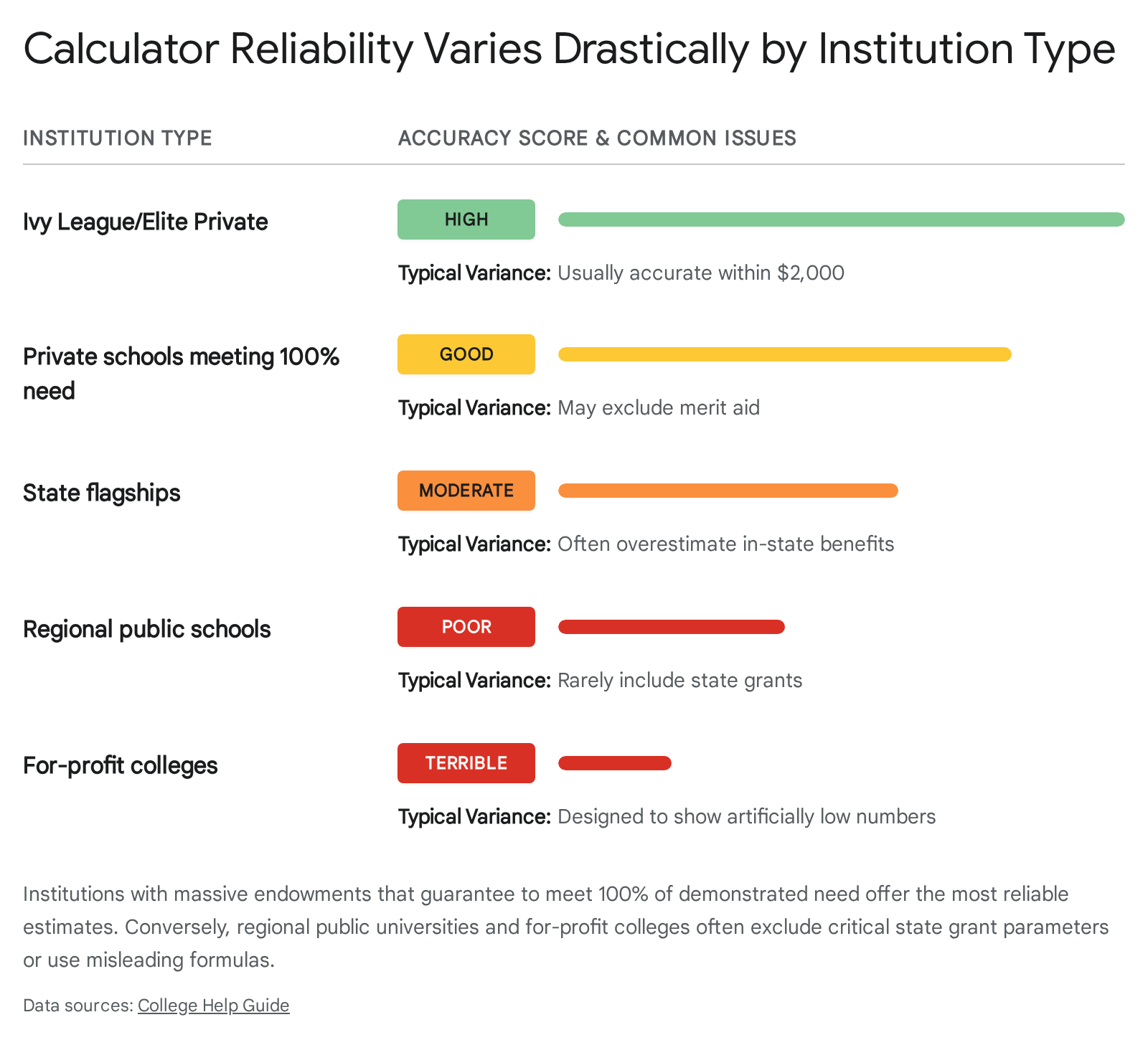

The greatest flaw of the federal template is its brevity. It requires the user to answer a maximum of eight basic questions regarding income and household size, entirely ignoring deep asset analysis and academic merit 1015. If an institution awards substantial merit scholarships, the federal template will completely fail to capture this, rendering it utterly useless for wealthier families who will not qualify for need-based aid but might qualify for academic awards 1316. Furthermore, because it ignores assets, the need-based estimates for middle-class families are often highly distorted 13.

Despite these glaring inaccuracies, the federal template is deeply entrenched in the higher education landscape. A comprehensive study by the Institute for College Access & Success (TICAS) evaluating colleges in Michigan found that 64% of all institutions relied on this minimal federal template, including 97% of public two-year colleges 15. State universities and institutions with limited financial aid resources often default to this template because it requires minimal administrative upkeep, even if it provides families with dubious cost estimates 1316.

Institutional and College Board Calculators (The Gold Standard)

Colleges that distribute robust institutional grant aid - particularly highly selective private universities - require a much more sophisticated tool to predict their unique financial aid algorithms. These institutions either build proprietary custom calculators or license comprehensive third-party software, most notably from the College Board 131417.

The College Board Net Price Calculator is widely utilized by elite institutions and represents a significant upgrade in accuracy. It typically requires users to answer between 30 and 43 detailed questions, delving into specific tax line items, home equity, non-custodial parent contributions, and precise academic metrics 15. By capturing a student's GPA and standardized test scores, these calculators can effectively estimate non-need-based merit scholarships alongside federal and institutional grants 813.

A major advantage of the College Board's cloud-based system is its portability. Students who create a free account can save their extensive financial inputs and automatically carry them over to other participating colleges' calculators 1417. This seamless data transfer significantly reduces the friction of comparing multiple institutions. For families applying to Ivy League schools or other elite private institutions that guarantee to meet 100% of demonstrated financial need, these detailed calculators are highly reliable and often estimate the final net price within a margin of $2,000 624.

MyinTuition (The Quick Estimator)

In an effort to overcome the intimidating complexity of traditional financial aid forms, several dozen selective colleges have adopted the MyinTuition Quick College Cost Estimator 3018. MyinTuition was engineered to rapidly dispel sticker shock by requiring only six fundamental questions: marital status, household income, cash savings, home value, mortgage balance, and retirement savings 1819.

While MyinTuition excels at encouraging low-income students to apply by quickly demonstrating that top-tier colleges are affordable, its methodology presents challenges for precise financial planning. Rather than providing a single, definitive net price, MyinTuition generates a broad spectrum of possibilities, categorized into a "Best," "Low," and "High" estimate 3320.

Furthermore, MyinTuition does not explicitly state the standard "net price" in its final output. To calculate the actual net price, families must manually add together the projected student contribution, parent contribution, expected student loans, and expected student employment 20. Because the tool inherently builds student loans into its projections, families often find that the initial MyinTuition estimate appears far more optimistic and cheaper than the detailed Net Price Calculator hosted by the exact same university 20. When attempting to build a strict household budget, admissions advisors consistently recommend relying on the rigorous College Board or custom NPC over the rapid MyinTuition estimator 20.

| Calculator Type | Average Number of Questions | Evaluates Academic Merit? | Overall Reliability for Budgeting |

|---|---|---|---|

| Federal Template | 6 to 8 15 | No 14 | Low. Relies on broad medians; ignores assets and merit aid 1316. |

| MyinTuition | 6 1819 | No | Moderate. Provides a wide range; optimistic presentation of loans 20. |

| College Board / Custom | 20 to 43+ 15 | Yes (institution dependent) 13 | High. Mimics complex institutional formulas and assesses home equity 2414. |

Why Calculator Estimates Often Miss the Mark

Even when a family utilizes a sophisticated, 40-question custom calculator and inputs their tax data flawlessly, the resulting estimate can still diverge dramatically from the official financial aid award letter they receive months later 1421. An extensive audit conducted by researchers at the University of Pennsylvania evaluated actual student profiles against college calculators and found alarming systemic inaccuracies 736.

The Illusion of Self-Help Aid: Loans and Work-Study

The most pervasive and deceptive practice found in college calculators is the manipulation of what constitutes "aid." By federal statutory definition, a net price should be calculated by taking the total cost of attendance and subtracting only grant and scholarship aid - money that never has to be repaid 245.

However, many institutions choose to artificially lower their displayed net price by subtracting "self-help" aid. An industry audit revealed that 27% of net price calculators included federal student loans in their net price reductions without clearly differentiating those loans from free grants 37. Similarly, calculators frequently subtract estimated earnings from Federal Work-Study programs, assuming the student will work 10 to 15 hours a week 2223.

When a calculator estimates a family's net price is $12,000, but achieves that number by assuming the student will take on $5,500 in subsidized loans and earn $2,500 working in the campus library, the actual billed amount the family must immediately finance is $20,000 3323. Furthermore, some calculators bundle loans under ambiguous names without using the word "loan," making it incredibly difficult for families to distinguish between gift aid and debt 23.

Outdated Institutional Data and FAFSA Delays

To maintain accuracy, institutions must continually update their calculators to reflect rising tuition costs and changing grant budgets. Although federal law requires annual updates, it only vaguely mandates the use of "recent" aid data, meaning colleges face no penalty for lagging behind 24.

The audit of national calculators demonstrated that 40% of institutions were using outdated data, with some relying on tuition and aid figures from three to four years prior 37. An additional 8% of calculators failed to disclose which academic year's data they were referencing, leaving families completely blind to the estimate's relevance 37. Using tuition data from 2021 to estimate a bill for 2026 guarantees a mathematically flawed outcome 37.

This systemic data lag was catastrophic during the rollout of the FAFSA Simplification Act in 2024 and 2025. Unprecedented technical failures at the U.S. Department of Education delayed the delivery of Institutional Student Information Records (ISIRs) to colleges by several months 24254226. Because financial aid administrators could not access the new federal data to model their institutional budgets, many colleges completely suspended updates to their net price calculators 44. As a result, students attempting to plan for the 2024 - 2025 and 2025 - 2026 academic years frequently encountered calculators prominently displaying warnings that they were still operating on prior-year costs and formulas 72728.

Hidden Indirect Costs and Living Expenses

Calculators can also distort the perceived affordability of an institution by manipulating the Cost of Attendance (COA) inputs. While direct costs like tuition and mandatory fees are rigid, indirect costs such as off-campus housing, food, transportation, and personal supplies are highly subjective estimates created by the college 221.

The UPenn study highlighted that some calculators utilize incomplete or highly misleading indirect cost estimates 7. For instance, a university in an expensive urban center might plug an unrealistically low figure for off-campus apartment rentals into their calculator to suppress the total COA 2. Other calculators completely omit transportation costs, which can add thousands of dollars for out-of-state students flying home for holidays 7. If the foundational COA is artificially depressed, the resulting net price estimate will be falsely optimistic.

Navigating Complex Family Financial Profiles

Net price calculators are generally programmed to handle standard financial scenarios: a married couple earning W-2 wages with standard cash savings. When a family's profile deviates from this baseline - due to divorce, business ownership, or independent student status - the rigid algorithms often produce highly unreliable estimates 242229.

Divorced and Separated Parents

Divorce dramatically alters the landscape of financial aid eligibility, and recent federal changes have upended decades of established protocol 1619. Prior to the 2024 - 2025 academic year, the FAFSA relied on a residency-based rule: the "custodial parent" responsible for filling out the FAFSA was the parent with whom the student lived for the majority of the previous 12 months 121930. Under that old system, a wealthy non-custodial parent's income was entirely ignored, allowing families to strategize custody to maximize need-based aid 1230.

This loophole has been permanently closed. Under the current rules governing the 2026 - 2027 FAFSA cycle, residency is irrelevant. The parent responsible for completing the FAFSA is solely the one who provides the greater portion of the student's financial support during the prior 12 months 1631. If both parents contribute exactly the same amount of financial support, the parent with the higher income and assets is legally obligated to file the form 1650. Furthermore, if this primary supporting parent has remarried, the new stepparent's income and assets must be reported in full, regardless of prenuptial agreements 1631.

This shift creates immense friction when using net price calculators. Because the FAFSA only assesses the primary supporting household, students applying to public universities only need to input that specific parent's data into the calculator 22. However, hundreds of highly selective private colleges require the CSS Profile in addition to the FAFSA. The CSS Profile universally demands the financial data of both the custodial and non-custodial biological parents, blending them together to determine institutional grant eligibility 192450.

Because many college net price calculators fail to clearly distinguish whether they are simulating the FAFSA methodology or the CSS Profile methodology, divorced families frequently receive inaccurate estimates 22. Financial aid consultants advise divorced parents to run private college calculators twice: once using only the primary supporting parent's income, and a second time combining the income and assets of all biological parents and stepparents 2422. The student's actual net price will almost always fall between these two figures, leaning heavily toward the higher, combined estimate at elite private institutions 24.

Independent Students and Age Criteria

The algorithms powering net price calculators also struggle with independent students. By default, the federal government assumes that all students under the age of 24 are dependents, meaning their parents' income must be factored into the expected contribution 32.

To qualify as an independent student - which bypasses the requirement for parent financial data entirely - the applicant must meet specific strict criteria. For the 2025 - 2026 and 2026 - 2027 cycles, a student is automatically considered independent if they are 24 years old, married, a veteran of the U.S. Armed Forces, an emancipated minor, currently in foster care, or have dependents of their own 1232.

If a student does not meet these rigid federal definitions but is estranged from their parents due to abuse, abandonment, or incarceration, they can no longer accurately use a standard net price calculator. The FAFSA Simplification Act introduced a "provisional independent status," allowing students with unusual circumstances to submit the FAFSA without parental data 1133. However, this status is not guaranteed; it generates an estimated aid index, but the final determination requires a manual dependency override by the college's financial aid administrator 11. Standard net price calculators cannot simulate this nuanced, human-driven override process, making their estimates highly unreliable for estranged youth.

Recent Legislative Overhauls: FAFSA Simplification and OBBBA

The accuracy of historical net price calculators has been severely compromised by two massive pieces of federal legislation that fundamentally rewrote the algorithms determining who can pay for college. Institutions that have failed to update their calculators to reflect both the 2024 FAFSA Simplification Act and the 2025 One Big Beautiful Bill Act (OBBBA) are providing families with mathematically obsolete estimates 343536.

The Shift from EFC to the Student Aid Index (SAI)

The most visible change implemented by the FAFSA Simplification Act was the elimination of the Expected Family Contribution (EFC) terminology, replacing it with the Student Aid Index (SAI) 333738. While the EFC could never drop below zero, the new SAI formula allows for a negative index, dropping as low as -$1,500 323337. This negative threshold allows financial aid administrators to distinctly identify and allocate additional state and institutional funds to the most profoundly low-income students 3337. Independent students who are not required to file a federal tax return automatically qualify for this -$1,500 SAI and the maximum Pell Grant 32.

Conversely, the SAI formula aggressively penalized middle- and high-income families with multiple children. Under the old EFC rules, if a family had two children in college simultaneously, their expected contribution was essentially cut in half, recognizing the divided financial strain 3439. The FAFSA Simplification Act completely abolished this "sibling discount." The new SAI algorithm does not divide the parent contribution by the number of children enrolled in higher education 333739. Therefore, a family that anticipated a substantial aid package based on older sibling experiences will find that updated net price calculators project a vastly higher out-of-pocket cost 3439.

The 2026 Reversal on Small Businesses and Family Farms

For rural families and entrepreneurs, the net price calculator experience has been chaotic. Initially, the FAFSA Simplification Act mandated that the net worth of all family-owned businesses and farms be reported as liquid assets, brutally inflating the SAI for families whose wealth was tied up in illiquid tractors, land, or restaurant equipment 363740.

Following massive pushback, Congress passed the One Big Beautiful Bill Act (OBBBA) on July 4, 2025 604142. A crucial component of this legislation completely reversed the small business mandate. Beginning with the 2026 - 2027 FAFSA, applicants are no longer required to report the asset value of family-owned businesses with 100 or fewer full-time (or full-time equivalent) employees, family farms on which the family resides, or family-owned commercial fishing operations 3660424364.

This exemption allows rural families and small business owners to qualify for significantly more need-based aid 3664. However, because this is a brand-new legislative reversal, many institutional net price calculators have not yet patched their software to reflect the OBBBA update 36. If an entrepreneur uses an outdated calculator, the tool will mistakenly assess their business net worth and project a devastatingly high net price. Families must manually exclude these assets when using older calculators to generate an accurate 2026 - 2027 estimate 3664. It is important to note that while the physical asset is exempt, the adjusted gross income generated by the farm or business and reported on the prior-prior year tax return remains a primary factor in the SAI calculation 3660.

Hard Cutoffs for Pell Grants and Foreign Income

The OBBBA also introduced rigid new barriers to Federal Pell Grant eligibility starting in the 2026 - 2027 academic year. Previously, Pell Grant eligibility scaled along a gradient. Now, there is a hard, mathematical cutoff: if an applicant's Student Aid Index (SAI) is equal to or greater than twice the maximum Pell Grant award for that specific year, the student is entirely ineligible for a Pell Grant 60434445. For the 2026 - 2027 cycle, the maximum Pell Grant is $7,395; therefore, any student with an SAI of $14,790 or higher is automatically disqualified, barring specific exceptions for dependents of deceased service members 36604243.

Furthermore, the OBBBA closed a loophole regarding international earnings. When calculating Pell Grant eligibility, the Department of Education will now add any foreign earned income exclusion amount reported on the FAFSA directly back into the family's Adjusted Gross Income (AGI) 424344. Expatriate families or those working abroad who previously appeared to have zero domestic income will now see their true global earnings reflected in their net price calculator estimates, drastically reducing their grant eligibility 4264.

How New Borrowing Caps Redefine College Affordability

Historically, if a net price calculator generated a massive, unaffordable figure, a family's final fail-safe was the federal loan system. Parents could utilize the Federal Direct PLUS Loan program to borrow up to the entire total cost of attendance minus any received aid, with virtually no annual ceiling 36. This allowed families to bridge the gap between their actual cash flow and the college's calculated net price, albeit by taking on crippling debt.

The passage of the OBBBA fundamentally dismantled this safety net, redefining how families must interact with their net price estimates. Effective July 1, 2026, the federal government imposed strict, absolute caps on student and parent borrowing 4167.

| Federal Loan Type (Post July 1, 2026) | New Annual Limit | New Lifetime Aggregate Limit |

|---|---|---|

| Parent PLUS (Per Dependent Student) | $20,000 4167 | $65,000 3567 |

| Graduate Students (Direct Loans) | $20,500 6746 | $100,000 6746 |

| Medical / Professional Students | $50,000 6746 | $200,000 6746 |

| Universal Lifetime Cap (All Direct Loans) | N/A | $257,500 436467 |

Note: The Graduate PLUS loan program has been entirely eliminated for new borrowers starting July 1, 2026 416746.

The imposition of a $20,000 annual cap on Parent PLUS loans drastically changes the utility of a net price estimate 366746. If a calculator accurately projects a family's net price to be $40,000 a year, the parents can no longer rely on federal loans to sweep the problem under the rug. They will be strictly limited to borrowing $20,000 in federal funds, leaving a massive $20,000 "funding gap" every single year that must be covered by immediate out-of-pocket cash, private high-interest loans, or intense student employment 3646.

There is a narrow "legacy provision" built into the OBBBA. If a parent or graduate student received a Federal Direct Loan disbursement for a specific academic program before July 1, 2026, they are permitted to continue borrowing under the old, limitless rules for a maximum of three additional academic years, provided they remain continuously enrolled in the exact same program at the same institution 41434546. For all new incoming students analyzing their net price calculator results, the new strict limits apply, meaning the calculated net price is a hard cash reality rather than a mere borrowing suggestion.

Transitioning from Estimates to Actual Aid Offers

Because of systemic delays, differing software platforms, and sweeping legislative changes, a net price calculator is merely a starting hypothesis. The true cost of college is not cemented until the student applies, is accepted, and receives an official financial aid award letter from the institution 21.

If a family utilizes a robust, 40-question net price calculator, inputs their exact prior-prior year tax data, and receives an estimate of $15,000, they should expect the official award letter to closely mirror that figure 614. However, if the official award letter demands a net price of $30,000, the family possesses strong grounds for an appeal. Financial aid advisors strongly recommend saving the output document from the net price calculator 1017. If the final award is significantly less generous than the calculator's estimate, the family can present the saved calculation to the financial aid office and formally request that the award be reassessed 810. While the calculator is explicitly not a binding contract 18, presenting the institution's own algorithm back to them often forces the financial aid office to either explain a specific data discrepancy or increase the grant award to match the initial promise 1629.

Bottom line

A college net price calculator is an indispensable tool for anticipating the true out-of-pocket costs of higher education, but its accuracy is heavily dependent on the quality of the institution's software and the precision of the family's inputs. Calculators at well-endowed private institutions that utilize detailed tax metrics and academic profiles are highly reliable, whereas regional universities relying on bare-minimum federal templates often produce misleadingly optimistic estimates. Families must remain hyper-vigilant regarding recent legislative shocks - such as the 2026 OBBBA restoration of the small business asset exemption and the new, strict $20,000 annual caps on Parent PLUS loans - as many college websites lag severely behind federal law. Ultimately, while an NPC provides a critical baseline for budget planning and financial aid appeals, the final cost is never truly settled until the official award letter arrives.