How to File the 2026-2027 FAFSA and What SAI Means

The 2026-2027 Free Application for Federal Student Aid (FAFSA) introduces unprecedented structural shifts to American higher education financing, combining a highly streamlined application interface with strict new federal borrowing caps and reconfigured eligibility algorithms. For this cycle, the application utilizes 2024 tax data to calculate a family's Student Aid Index (SAI), a metric that determines access to federal, state, and institutional funds. Crucially, while the application process is now faster and exempts certain small businesses and farms from asset calculations, new legislative rules impose severe limits on Parent PLUS loans and Pell Grant eligibility.

A Historic Return to Stability After Systemic Disruption

For millions of prospective and current college students, the FAFSA serves as the indispensable gateway to higher education, unlocking access to federal Pell Grants, work-study allocations, subsidized student loans, and state-based financial aid. Over the preceding cycles, the deployment of the simplified FAFSA was fraught with severe technical and administrative disasters. The 2024-2025 cycle, in particular, was delayed by several months, plagued by critical system glitches, and resulted in a significant drop in application completions that forced higher education institutions across the country to push back their commitment deadlines and scramble to assemble financial aid packages 112. The Government Accountability Office (GAO) noted that the initial rollout blocked thousands of students from completing their forms, severely impacting enrollment patterns, particularly among low-income students 11.

By stark contrast, the 2026-2027 FAFSA cycle represents a determined return to operational stability and systemic efficiency. In direct response to the previous chaos, the federal government enacted the FAFSA Deadline Act, legally mandating an October 1 launch date for all future applications 13. Driven by this mandate, the U.S. Department of Education engaged in an extensive, multi-phase beta-testing period beginning in August 2025, partnering with school districts and community organizations to stress-test the application architecture 4.

Following this successful testing phase, the Department launched the 2026-2027 application on September 24, 2025, marking the earliest launch in the program's history 3567. Early operational data from the current cycle indicates a stabilizing system; officials report a 96% user satisfaction rate, with the vast majority of applicants completing the streamlined form in a fraction of the time required by legacy systems 7. For families preparing to finance a college education between July 1, 2026, and June 30, 2027, the interface is vastly improved, though the underlying financial aid formulas have undergone complex legislative adjustments that require careful strategic planning.

The Strategic Timeline for the 2026-2027 Cycle

The FAFSA operates on an extended 18-to-21-month application cycle, which is designed to ensure that any student who enrolls throughout a given academic year has an opportunity to secure federal aid 8. However, this extended timeline often lulls families into a false sense of security. Because financial aid is disbursed from multiple distinct pools of capital - federal, state, and institutional - each pool operates on its own strict timeline, and delaying submission is a severe strategic error.

The absolute final federal deadline to submit the 2026-2027 FAFSA is June 30, 2027, with a brief administrative grace period extending to September 12, 2027, solely for the purpose of processing necessary corrections 689. While the federal government will process applications until the end of the academic year, relying on the federal deadline will almost certainly result in lost funding. State governments and individual colleges utilize the FAFSA data to disburse their own limited grant endowments. Many of these local programs operate on a strict first-come, first-served basis, meaning the capital simply depletes as the year progresses 810.

To ensure maximum eligibility for all available pools of capital, financial aid professionals universally recommend filing the FAFSA in the autumn of the year prior to anticipated enrollment. If a college maintains an early priority deadline - which frequently falls between December and March - missing that institutional deadline could mean forfeiting thousands of dollars in need-based grants, regardless of a family's financial distress.

Priority Deadlines for State Financial Aid Programs

State higher education agencies impose their own deadlines for state-specific grants, which are often much earlier than the federal cutoff. Applicants are strongly advised to verify exact dates with their respective state agencies and intended colleges, as institutional deadlines frequently supersede state guidelines.

| State | 2026-2027 FAFSA Deadline or Priority Target | Allocation Methodology |

|---|---|---|

| California | March 2, 2026 (for priority Cal Grant consideration) | Hard priority deadline 810 |

| Texas | January 15, 2026 (for priority consideration) | Hard priority deadline 810 |

| New York | June 30, 2027 (TAP applications and other forms may apply) | Rolling / Final Deadline 810 |

| Florida | May 15, 2026 | Hard deadline 811 |

| Illinois | As soon as possible after application launch | First-come, first-served (funds deplete) 810 |

| Pennsylvania | May 1, 2026 (for the majority of state programs) | Hard deadline 11 |

| North Carolina | June 1, 2026 (UNC System), Aug 15, 2026 (Community Colleges) | Varies distinctly by institution type 810 |

| Michigan | July 1, 2026 | Hard deadline 8 |

Understanding the Prior-Prior Year Tax Rule

One of the most frequently misunderstood operational mechanics of the FAFSA is the specific tax year it utilizes to assess a family's financial strength. The 2026-2027 FAFSA does not request current income or anticipated future earnings. Instead, it relies on a statutory provision requiring tax information from the "prior-prior year," which, for the 2026-2027 academic cycle, corresponds strictly to the 2024 calendar tax year 121314.

This rule was implemented by the Department of Education to align the financial aid application sequence with the traditional college admissions timeline. By utilizing two-year-old tax data, families do not have to wait to file their current year's taxes before applying for educational aid; the 2024 tax returns have already been finalized and processed by the Internal Revenue Service 13. For the parents of high school juniors - the high school Class of 2027 - the "base income year" that will dictate their child's freshman year financial aid eligibility has already concluded 12.

Every dollar earned in wages, every capital gain realized from an investment, and every taxable retirement withdrawal taken during the 2024 calendar year will directly inform the 2026-2027 Student Aid Index calculation. Conversely, strategic pre-tax contributions to employer-sponsored retirement accounts, such as a 401(k) or the Thrift Savings Plan (TSP), made during 2024 served to lower a family's Adjusted Gross Income (AGI), which generally improves aid eligibility under the current formula 17. However, a massive one-time bonus, the liquidation of a stock portfolio, or the profitable sale of real estate in 2024 could artificially inflate a family's perceived wealth for the 2026-2027 school year, severely suppressing their eligibility for need-based grants 1718.

Crucially, applicants cannot simply substitute 2025 or 2026 income data onto the application merely because they feel it reflects a more accurate picture of their current financial reality 13. The federal formula is rigid on the initial application. If a family's financial situation has drastically deteriorated since 2024 - perhaps due to sudden unemployment, a severe reduction in pay, exorbitant out-of-pocket medical expenses, or a recent divorce - they must still initially file the FAFSA using the mandated 2024 data. Following submission, the family must contact the financial aid administrator at the student's intended college to formally request a "professional judgment review," commonly known as a financial aid appeal 1315. Financial aid administrators possess the statutory authority to manually adjust the underlying FAFSA data elements using current income estimates, provided the family supplies adequate, verifiable documentation of the special circumstance 1315.

Modernized Application Mechanics and System Improvements

The user experience of completing the 2026-2027 FAFSA has been dramatically overhauled through a series of backend technological integrations designed to eliminate the systemic friction points that caused widespread application abandonment in previous years.

Real-Time Identity Verification

Historically, when a student or a parent created a new StudentAid.gov account to obtain their Federal Student Aid (FSA) ID - the secure digital signature required to authenticate and complete the form - they were forced to endure a waiting period of one to three days while the Social Security Administration manually verified their identity parameters against federal databases 162117. This delay frequently disrupted the application process, requiring families to return to the system multiple times.

For the 2026-2027 cycle, the Department of Education implemented a robust real-time identity verification protocol. Applicants and contributors who possess a valid Social Security Number are now verified instantaneously upon the creation of their account 9211723. This immediate validation allows families to establish an account, seamlessly provide legal consent to the IRS Direct Data Exchange (DDX), automatically import their verified tax data, and complete the entirety of the FAFSA within a single session 1723.

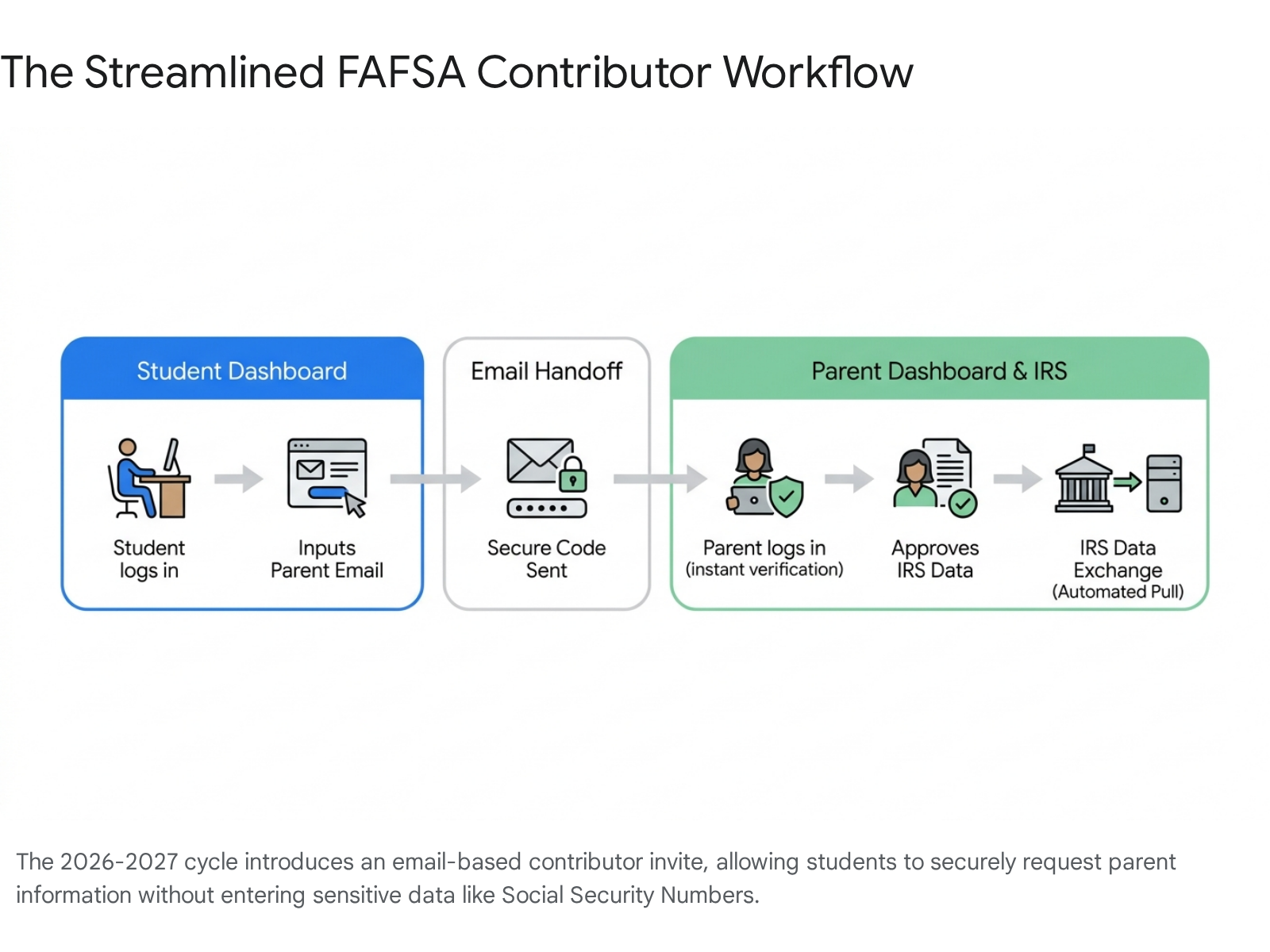

Streamlined Contributor Invitations

The architecture of the simplified FAFSA relies on independent inputs from various "contributors" - typically the student and one or both parents, or, in the case of married independent applicants, the student's spouse. In preceding versions of the application, students were required to input highly sensitive personal identifiable information (PII), including a parent's exact legal name, precise date of birth, and Social Security Number, simply to dispatch an electronic invitation requesting the parent to complete their mandatory section 211723. Minor typographical errors in this PII caused accounts to mismatch, locking frustrated families out of the system entirely.

The 2026-2027 application interface entirely eliminates this hurdle. Students now only need to provide the contributor's active email address. The system automatically dispatches a secure, non-case-sensitive code to that email inbox, which the parent or spouse then utilizes to link their independent StudentAid.gov account directly to the student's active FAFSA application 5921172324.

This architectural update has dramatically reduced user error rates, improved completion velocities, and significantly reduced the burden on federal call centers 523.

Pathways for Contributors Without a Social Security Number

For decades, students who were legally eligible U.S. citizens but whose parents were undocumented or otherwise lacked a Social Security Number faced immense, often insurmountable technical barriers when attempting to submit the FAFSA. While recent programmatic patches attempted to allow non-SSN contributors to participate, those fixes relied on a laborious manual identity validation process involving a dedicated federal email address, which resulted in massive administrative backlogs and jeopardized student aid 25.

The 2026-2027 cycle integrates a far smoother and more equitable pathway. The flawed manual validation email process has been officially paused and the old routing addresses deactivated 25. Instead, contributors without an SSN are now required to complete a separate, embedded attestation certifying their lack of an SSN directly within the online account creation workflow 25. As part of this process, these individuals are presented with a series of knowledge-based verification questions drawn securely from credit bureaus (where applicable) to confirm their identity digitally 18. Once this integrated identity step is cleared, non-SSN contributors can proceed directly to the FAFSA form without waiting for manual intervention by federal staff, ensuring that the student's financial aid timeline is preserved 25.

Anti-Fraud Bot Screening and Real-Time Identification Checks

In response to a documented rise in fraudulent federal applications and the deployment of synthetic identities designed to siphon taxpayer funds, the Department of Education introduced sophisticated real-time bot screening and enhanced security measures starting in the spring of 2026 1928. The explicit goal of these measures is to crack down on identity assumption without penalizing legitimate applicants.

While the vast majority of standard applicants will navigate the form without ever noticing this background screening, a subset of users flagged by the system's algorithms may be suddenly prompted to submit to a live identity verification check while actively filling out the application 28. If triggered, a student completing the form on a desktop or laptop computer will be presented with a dynamic QR code. By scanning this code with a smartphone, the student is prompted to take a live, high-resolution photograph of a government-issued photo ID 28. The captured image is analyzed and processed in real time by federal systems; upon successful validation, the student is automatically returned to the FAFSA interface to apply their digital signature and submit the document 28.

This security mechanism has a very short completion window and cannot be saved for later completion. If an applicant lacks a valid photo ID, or if a vulnerable student experiencing homelessness is unable to complete the prompt, the system will not block the submission entirely. The student can still technically submit the FAFSA, but a severe administrative hold will be placed on their account 28. Consequently, the student's intended college financial aid office will be required to physically verify the student's identity in person before any federal or institutional aid can be released 28.

Demystifying the Student Aid Index (SAI)

Beginning with the 2024-2025 academic year, the Department of Education officially retired the long-standing Expected Family Contribution (EFC) metric, replacing it with the newly calibrated Student Aid Index (SAI) 142021. While both figures serve the exact same overarching purpose - providing college financial aid offices with a single, unified number to plug into their institutional aid algorithms - the mathematics and policy goals underpinning the SAI have been continually refined, with major regulatory updates taking effect for the 2026-2027 award year.

The transition away from the EFC was driven largely by optics and consumer confusion; families historically assumed that the Expected Family Contribution represented the exact, definitive dollar amount they would be billed for a year of college tuition 20. The SAI is more accurately labeled as an index number - a gauge of financial strength that helps administrators measure comparative need. The foundational equation utilized by colleges to calculate financial need remains straightforward: Cost of Attendance (COA) - Student Aid Index (SAI) = Financial Need 3122.

Interpreting the Range of SAI Scores

The Student Aid Index utilizes a significantly wider numerical range than the legacy EFC, stretching from a minimum baseline of -1,500 up to a theoretical maximum of 999,999 2031.

A highly favorable SAI for an applicant generally falls within the negative to zero range (-1,500 to 0). An SAI that drops to zero or below serves as an immediate, clear indicator of severe financial distress 3123. Achieving this low index generally guarantees that the student will qualify for the maximum allowable Federal Pell Grant, alongside priority access to subsidized federal student loans and the maximum allocation of college-funded institutional grants 3123. Under the old system, the EFC bottomed out at $0; the implementation of the new negative range allows educational institutions to differentiate clearly between families who merely lack expected disposable income and those who are facing deep, systemic poverty 2031.

As an applicant's SAI climbs into the low-to-moderate tier (ranging from 1 to roughly 14,000), they will likely still qualify for partial, prorated Pell Grants, subsidized loans, and varying levels of state and institutional support, heavily dependent on the total cost of the specific college they attend 23. However, as the SAI scales higher into the 15,000+ range, eligibility for need-based federal "free money" evaporates rapidly. Students presenting with high SAIs are expected by the federal government to finance their education out of pocket, through unsubsidized student loans, Parent PLUS loans, or by aggressively pursuing non-need-based merit scholarships awarded directly by the university 3123.

The SAI Calculation vs. The Legacy EFC

The shift from the EFC to the SAI was not merely a cosmetic rebranding exercise; it fundamentally altered the underlying mathematics of federal aid, creating distinct cohorts of winners and losers based on household composition and asset distribution 20.

| Feature Metric | The Legacy Expected Family Contribution (EFC) | The Calibrated Student Aid Index (SAI) | Practical Impact on Applying Families |

|---|---|---|---|

| Minimum Index Score | Bottomed out completely at $0 20. | Can drop to a floor of -$1,500 2031. | Enables the lowest-income applicants to signal deeper financial need to college administrators 20. |

| The Sibling Discount | Beneficially divided the total EFC by the number of children enrolled in college simultaneously 20. | Explicitly removes any adjustment for having multiple children enrolled in college 14202122. | Represents a major financial loss for middle-class households supporting overlapping college students 2021. |

| Untaxed Financial Support | Included cash support from relatives, as well as housing allowances for military and clergy members 14. | Eliminates the reporting requirement for many forms of untaxed income, including 529 plan distributions from grandparents 1418. | Allows extended family to financially support students without inadvertently penalizing the student's federal aid eligibility 1418. |

The complete removal of the multiple-in-college sibling discount remains the most painfully felt mathematical adjustment for middle-income families 20. Under the obsolete EFC formula, a family calculated to have an expected contribution of $30,000 would see that expectation generously split to $15,000 per child if two siblings were attending university simultaneously. Under the strict new SAI formula, the federal algorithm does not divide the burden; that family is assigned a $30,000 index score for each child, drastically reducing their calculated financial need and effectively requiring them to finance a much larger portion of the combined educational costs 20.

The Analytical Mechanics of the SAI Formulas

To accurately determine a student's precise standing on the index, the FAFSA Processing System (FPS) relies on three distinct legal algorithms - Formula A, Formula B, and Formula C - which cater to different applicant demographics and assess income and assets at steeply progressive rates 24.

For dependent students, the system deploys Formula A. This calculation is an aggregation of three distinct elements: the parents' contribution from income and assets, the student's contribution from available income, and the student's contribution from assets 24. The system first determines the parents' adjusted available income by deducting specific living allowances and taxes from their total income, and then adds an asset contribution derived by multiplying their discretionary net worth by a 12% conversion rate 24. This combined parental pool is then assessed at progressive tax-like rates ranging from 22% up to 47% 24. Meanwhile, the student's personal income is heavily protected; for the 2026-2027 cycle, students receive an income protection allowance of $11,770, meaning they are not expected to contribute from their earnings unless they surpass that threshold 1822. Any student income above $11,770 is assessed at a steep 50% rate, and any personal assets held by the student (such as savings accounts or personal brokerage accounts) are assessed aggressively at a 20% conversion rate 2224.

For independent students without dependents other than a spouse, the system utilizes Formula B. This simpler algorithm calculates an index based solely on the student's (and spouse's) available income, which is assessed at a flat 50% rate after standard allowances, combined with their net worth, which is multiplied by a 20% conversion rate 24.

Finally, for independent students who support dependents of their own, the system applies Formula C. This formula combines the student's available income and asset contributions to determine an adjusted available income pool. Recognizing the financial burden of supporting a family, this pool is then assessed using a sliding scale that increases from 22% to 47% as the applicant's income rises, mirroring the parental assessment mechanism found in Formula A 24.

The Return of the Small Business and Family Farm Exemptions

When the simplified FAFSA was originally rolled out, one of the most fiercely debated and controversial changes was the sudden regulatory requirement that families explicitly report the net worth of small businesses and family farms as available assets on the application 23202536. For multi-generational farm families who are frequently described as "asset rich but cash poor" - meaning they may hold millions of dollars in illiquid agricultural land and heavy equipment while generating only a modest annual operational income - this regulatory shift artificially inflated their SAI and immediately disqualified their children from vital federal and state aid 202536.

Following massive public outcry from rural constituencies and intense legislative lobbying, Congress passed the One Big Beautiful Bill Act (OBBBA), which definitively reversed this deeply unpopular requirement beginning with the 2026-2027 award year 14232526. Federal law now dictates that the following assets are strictly exempt from the financial aid calculator and should not be reported on the 2026-2027 FAFSA under any circumstances: * The net worth of any family-owned business that employs 100 or fewer full-time (or full-time equivalent) employees 91421232526. * The net worth of an operating family farm on which the applicant's family actively resides 1421232526. * The net worth of a commercial fishing business and its related operational expenses, provided it is owned and controlled by the family 1421232526.

This statutory exemption represents a massive financial victory for rural students, agricultural communities, and local entrepreneurs, returning the assessment formula to the equitable standards that operated prior to 2024 and shielding their primary livelihood assets from the scrutiny of the financial aid calculator 14232536.

Pell Grant Eligibility and the One Big Beautiful Bill Act

The Federal Pell Grant serves as the foundational cornerstone of need-based aid offered by the United States Department of Education. Unlike federal student loans, Pell Grants are direct subsidies that do not have to be repaid, making them the most highly sought-after form of undergraduate financial assistance 38.

For the 2026-2027 academic year, the maximum scheduled Federal Pell Grant award remains flat at $7,395, and the minimum possible award sits at $740, representing 10% of the maximum 272841. However, the federal budget is subject to constant legislative revision, and credible higher education analysts have warned of potential future legislative threats that could seek to drastically reduce the maximum award to offset national deficits 2742.

While the maximum dollar amount has not changed for the upcoming cycle, the One Big Beautiful Bill Act (OBBBA) significantly altered the strict statutory criteria governing who is actually allowed to receive these funds.

The New Hard Cutoff: The 2x Maximum Rule

The 2026-2027 cycle introduces a rigid new statutory ceiling on Pell Grant eligibility that prevents moderate-income families from accessing the program. Federal law now explicitly bars an applicant from receiving any Pell Grant funding if their calculated Student Aid Index is equal to or greater than exactly twice the maximum Pell Grant award amount for that specific award year 1423362628.

Because the maximum award for the current cycle is locked at $7,395, the strict SAI threshold for the 2026-2027 year is explicitly defined as $14,790 1436262829.

If a student's calculated SAI lands at $14,789, they may still technically qualify for the minimum Pell Grant allocation. However, the moment their SAI hits $14,790 or climbs higher, federal Pell funding is categorically eliminated for that academic year 3630. The legislation allows only one extremely narrow exception to this strict cutoff: the threshold does not apply to applicants who qualify for a Pell Grant under the Special Rule, which is reserved exclusively for the dependents of certain deceased military service members and fallen Public Safety Officers 14232628.

Closing the Foreign Income Loophole

Another subtle but highly impactful calculation change mandated by the OBBBA involves the strict treatment of foreign-earned income. In prior academic years, income that was legally excluded from federal taxation due to the IRS Foreign Earned Income Exclusion was loosely categorized as untaxed income on the FAFSA, but it was not systematically integrated back into the Adjusted Gross Income (AGI) when the algorithms determined a student's basic eligibility for maximum or minimum Pell Grants 24.

Beginning with the 2026-2027 award year, the foreign-earned income exclusion amount reported on the FAFSA is automatically and mandatorily added back into the applicant's AGI during the core Pell eligibility determination phase 142324262931. Families who live and work internationally but maintain U.S. citizenship will now see their previously sheltered foreign income fully weaponized in the calculation, which will inevitably push their SAI higher and likely disqualify a significant cohort of international expatriates from federal grant programs 2131.

The "Full Ride" Exclusion Policy

Historically, a deeply impoverished student who managed to earn a massive, prestigious private scholarship - such as a foundation grant covering their full tuition, room, and board - might still receive a federal Pell Grant. Because their SAI was inherently low, the government disbursed the Pell funds, which the student could then utilize for indirect educational expenses, travel, or living stipends.

Effective immediately for the 2026-2027 aid year, students who receive grants or scholarships from non-federal sources (such as private nonprofits, institutional endowments, or community foundations) that fully meet or exceed their calculated Cost of Attendance (COA) are entirely ineligible to receive a Pell Grant, even if their verified household income would otherwise easily qualify them for the maximum program award 233641293031. The government has reclassified the Pell Grant strictly as a gap-filling mechanism; if external philanthropic money successfully fills the student's financial gap, the federal government will systematically withhold the Pell funds 36.

Sweeping Changes to Federal Student Loan Limits

While need-based grants represent the ideal form of educational funding, the stark reality is that the vast majority of American families rely heavily on the federal student loan system to bridge the widening gap between their financial aid packages and the actual, escalating cost of college attendance.

Starting July 1, 2026, the federal student loan apparatus is undergoing its most radical and restrictive transformation in decades. Driven by the mandates of the OBBBA legislation, the federal government is placing aggressive new caps on how much students and parents are legally permitted to borrow, effectively ending the long-standing era of unlimited federal educational debt 264130.

Drastic Reductions for Undergraduate Borrowers and Parents

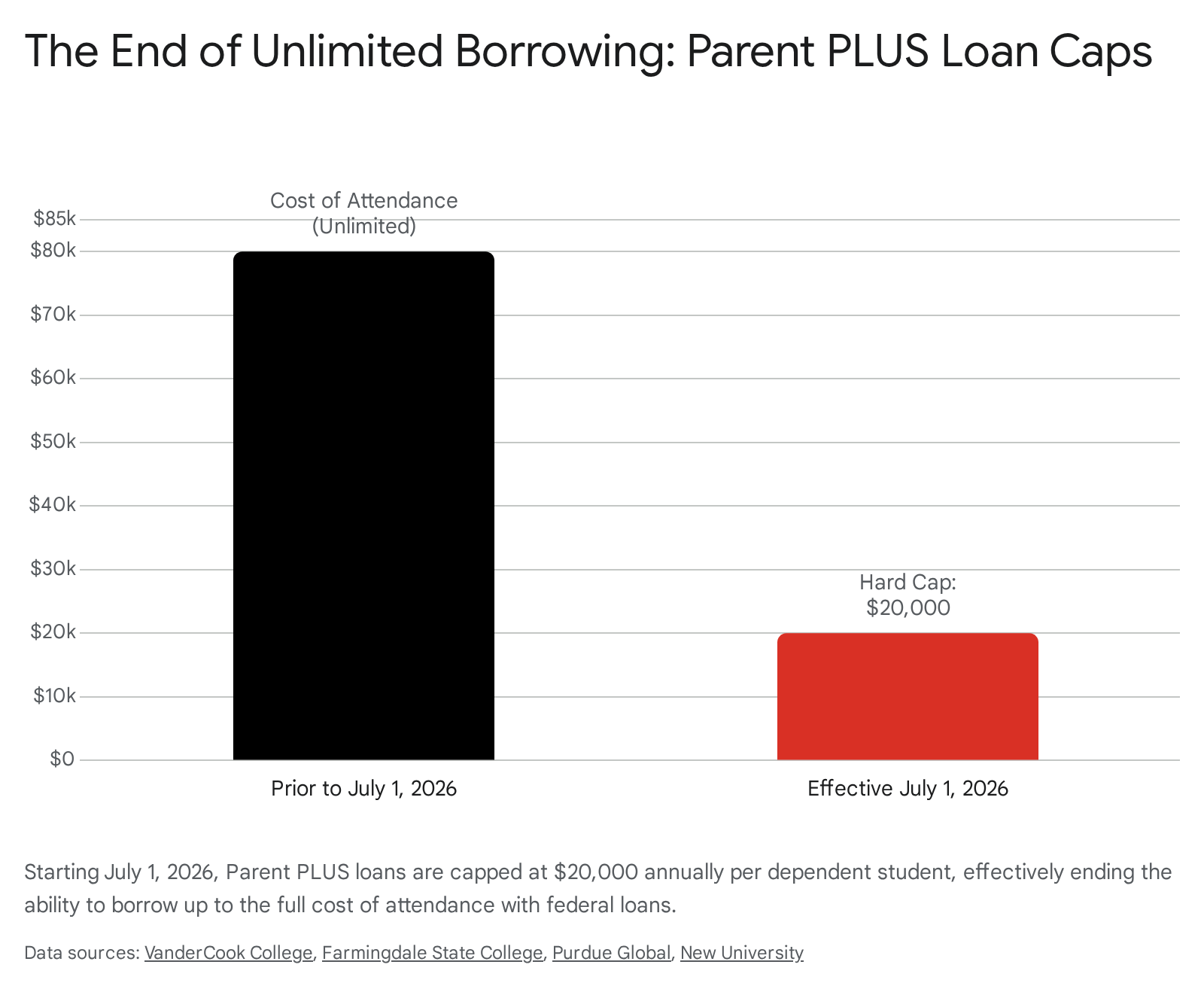

For decades, the Parent PLUS loan program served as the ultimate financial safety valve for middle-class families. The program generously allowed the parents of dependent undergraduate students to borrow up to the total Cost of Attendance of a university, minus any other financial aid the student had received. For example, if an elite private university cost $75,000 a year and a student received a $15,000 aid package, the parents were legally permitted to borrow the remaining $60,000 a year directly from the federal government.

This open-ended borrowing practice has been terminated. For all new federal loans originated on or after July 1, 2026, Parent PLUS borrowing is strictly capped at $20,000 per year, per dependent student 26412930.

Furthermore, the legislation establishes a strict aggregate lifetime limit of $65,000 per dependent student for Parent PLUS loans, without regard to amounts that may have been previously forgiven, repaid, or discharged 264129.

The implications of this cap are profound. If a student faces a financial gap that exceeds $20,000 per year, families can no longer rely on the federal government to float the difference. They will be forced to either liquidate personal assets, seek out private student loans from commercial banks - which require stringent credit checks, often demand co-signers, and lack the generous repayment protections inherent to federal loans - or abandon their first-choice university in favor of a more affordable public institution.

Additionally, undergraduate students who choose to enroll on a less-than-full-time basis will now face strict proration of their loan eligibility. Under the old rules, part-time students could often access maximum loan limits; effective July 1, 2026, if a student drops a class mid-semester and falls to half-time status, their eligible loan amounts for that specific term, and potentially subsequent terms, will be reduced proportionally 3031.

The Elimination of Graduate PLUS and New Professional Limits

Graduate and professional students are facing similarly severe curtailments to their borrowing power. Beginning July 1, 2026, the Graduate PLUS loan program - which operated on the same open-ended "up to the cost of attendance" premise as the Parent PLUS program - will be discontinued entirely for all new borrowers 264129.

In its place, graduate students are now subject to strict new annual and aggregate caps on standard federal unsubsidized direct loans, determined by their specific level of post-baccalaureate study: * Standard Graduate Students (Non-Professional Degrees): Borrowing is rigidly capped at $20,500 annually, with a new lifetime aggregate limit of $100,000 for graduate studies 264129. * Professional Students (e.g., Medical, Dental, and Law Degrees): Acknowledging the exorbitant costs of specialized professional training, these students are afforded higher limits, capped at $50,000 annually, with a hard aggregate limit of $200,000 412931.

To reinforce these new austerity measures, the federal government has also instituted a sweeping, overarching lifetime limit across all programs: $257,500 for all federal loans combined (excluding any amounts borrowed via Parent PLUS) across a borrower's entire lifetime of academic study 264129.

(Note: Recognizing the disruption these sudden changes would cause, lawmakers included a "legacy provision" for students who are currently enrolled in continuous academic programs using federal loans disbursed prior to July 1, 2026. These specific grandfathered borrowers are permitted to continue borrowing under the old, pre-2026 limits for up to three academic years or until they finish their expected credential, provided they maintain continuous enrollment and do not change their program of study or withdraw 263031.)

The FAFSA Submission Summary and Post-Filing Verification

The financial aid application process does not magically conclude the moment the "Submit" button is clicked. Within one to three business days, the Department of Education processes the submitted data and generates an essential document known as the FAFSA Submission Summary 3233.

This critical summary document - which replaced the antiquated Student Aid Report (SAR) in 2024 - is securely accessible exclusively on the student's personal dashboard; invited contributors, including parents, are legally restricted from viewing the student's finalized summary 33. The summary serves as the official blueprint of the family's financial aid profile. It clearly displays the legally calculated Student Aid Index (SAI), provides a preliminary estimate of the student's Federal Pell Grant eligibility, and flags any glaring data errors or missing signatures that require immediate correction before the form can be transmitted to colleges 42323334.

The Modernized Verification Process

Universities are required by federal regulations to systematically "verify" the accuracy of a specific percentage of FAFSA applications to prevent fraud and ensure equitable distribution of funds. If a student's summary clearly states that their application has been selected for verification, it is not an accusation of wrongdoing or fraud; it simply indicates that the college's financial aid office requires additional, verifiable documentation before they are legally permitted to disburse any federal or institutional money 3334.

Historically, the verification process was a grueling audit of a family's tax returns. However, because the vast majority of financial data is now imported directly from the IRS via the DDX mechanism, that income is legally considered "pre-verified" by the federal government, meaning schools generally no longer need to demand cumbersome tax transcripts or manual W-2s from families 3550. Today, the verification process focuses heavily on confirming the student's physical identity.

For the 2026-2027 cycle, the identity verification process has been highly modernized to reduce the administrative burden on students, particularly those who are studying remotely or lack easy access to transportation. The Department of Education officially eliminated the outdated requirement for students to provide a physical, paper "Statement of Educational Purpose" 355036. Furthermore, if a student cannot appear in person at the college's financial aid office to verify their identity, universities are now authorized to utilize two advanced digital alternatives: 1. A live, real-time video call between the student and an authorized financial aid administrator, effectively replacing the burdensome historical requirement to find a notary public and mail physical, notarized documents 5036. 2. The deployment of a secure third-party identity verification software service that strictly meets the rigorous National Institute of Standards and Technology (NIST) Identity Assurance Level 2 (IAL2) standard 5036.

Any identity flags or data discrepancies highlighted on the FAFSA Submission Summary must be resolved with the university immediately. The official financial aid offer letters that colleges dispatch to students in the spring are based entirely on the finalized, verified data established during this critical post-submission phase.

Bottom line

The 2026-2027 FAFSA is structurally easier to navigate than its predecessors, boasting instant identity verification and a streamlined, email-based contributor system that resolves the massive technical bottlenecks of the past. However, the financial landscape that this simplified form unlocks is vastly more restrictive. While the return of the family farm and small business asset exemptions will legally shield the livelihoods of rural and entrepreneurial families, the imposition of a $20,000 annual hard cap on Parent PLUS loans, the elimination of the Grad PLUS program, and the new 2x maximum rule for Pell Grants mean that middle- and lower-income families must aggressively rethink how they finance severe funding gaps. Students should file the FAFSA as early as possible using their finalized 2024 tax data to secure their rightful place in line for limited state and institutional grants before the money inevitably runs out.