What the 2026 Mega-IPO Window Means for Tech

The third quarter of 2026 is poised to host the largest concentration of mega-cap initial public offerings in financial history, led by the anticipated debuts of SpaceX, OpenAI, Anthropic, and Databricks. Together, these technology leaders represent roughly $4 trillion in private market value, testing whether global public markets possess the liquidity to absorb unprecedented capital demands. While their revenue growth curves are historically unparalleled, prospective investors must carefully weigh the staggering infrastructure costs of artificial intelligence and shifting global regulatory frameworks before participating in these landmark listings.

The Dawn of a Historic Liquidity Event

After a prolonged period of sluggish public listings, tight monetary policy, and macroeconomic uncertainty, the global initial public offering (IPO) market has roared back to life in 2026. In the first quarter of the year alone, global IPO proceeds surged 45% year-over-year to $42.6 billion, signaling a structural market shift toward fewer, but vastly larger, listings 1. This resurgence is not distributed evenly across the economy; it is highly concentrated in the artificial intelligence, data infrastructure, and space exploration sectors.

The upcoming wave is entirely unprecedented in its sheer scale. Driven by the rapid commercialization of generative AI and low Earth orbit satellite infrastructure, the potential combined value of the SpaceX, OpenAI, and Anthropic offerings alone could reach $4 trillion 2. To place this in historical perspective, this sum would comfortably exceed the cumulative valuation of the entire dot-com IPO wave from 1995 to 2000, and it would represent nearly half the value of all United States IPOs conducted since the end of the Second World War 2.

These are not traditional early-stage startups seeking growth capital to prove a business model. Thanks to incredibly deep pools of private equity, venture capital, and sovereign wealth, these entities have remained private far longer than their historical counterparts 2. They have reached massive global scale, developed complex multinational corporate structures, and achieved valuations that dwarf the gross domestic product of many sovereign nations before ever offering a single share to the public. The 2026 IPO window is therefore not a fundraising exercise in the traditional sense, but rather an enormous liquidity event designed to allow early investors to exit and to reprice the global technology sector.

A Comparative Snapshot of the 2026 Mega-Listings

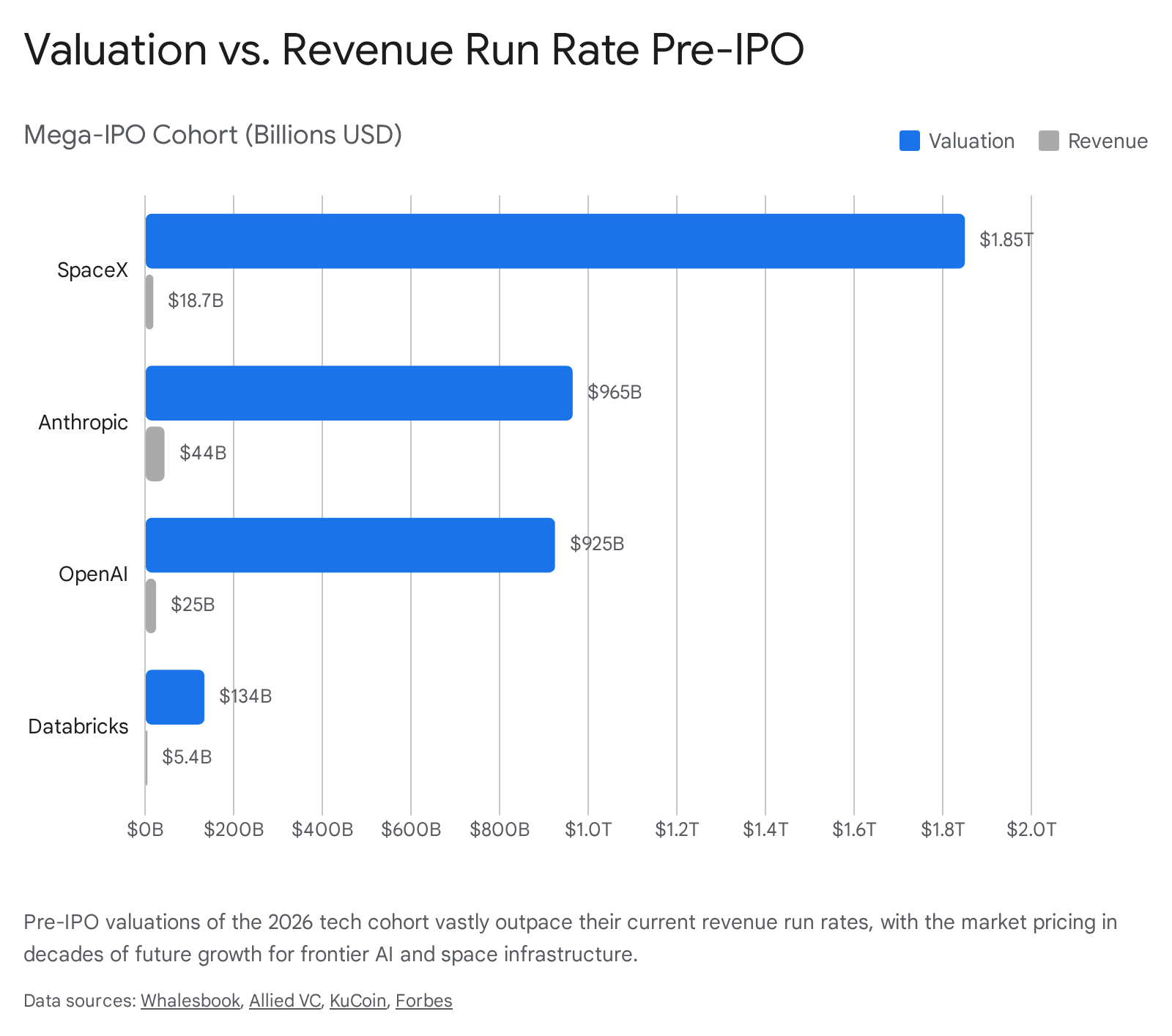

To understand the scale of the upcoming third and fourth-quarter window, it is helpful to look at the foundational financial metrics of the four most anticipated companies preparing to list. The data reveals a stark contrast between top-line revenue growth, which is universally strong, and bottom-line profitability, which remains deeply challenged for companies engaged in the capital-intensive pursuit of artificial general intelligence (AGI).

| Company | Estimated Valuation | Reported Revenue / ARR | Profitability Status | Target IPO Window |

|---|---|---|---|---|

| SpaceX | $1.75T - $2.0T | $18.7B (2025) | Net Loss ($4.94B in '25) | June/July 2026 |

| Anthropic | ~$965B | $30B+ - $44B ARR | Q2 2026 Operating Profit | October 2026 |

| OpenAI | $850B - $1.0T | $25B ARR (Early '26) | Heavy Net Loss | Q4 2026 / 2027 |

| Databricks | $134B | $5.4B ARR | Free Cash Flow Positive | H2 2026 |

The financial figures outlined above represent the most current data available through pre-IPO leaks, official S-1 filings, and verified executive conference statements as of mid-2026 33547.

Valuations are dynamic and subject to intense revision during the final institutional roadshows, particularly as global macroeconomic conditions fluctuate.

The Macroeconomic Backdrop: Liquidity, Rates, and Geopolitics

The success of these massive public offerings is entirely dependent on the willingness and ability of global investors to deploy capital in a shifting macroeconomic environment. The 2026 market is characterized by a multidimensional polarization: equity markets are split between AI and non-AI sectors, while the broader global economy balances robust corporate capital expenditures against sticky inflation and geopolitical instability 5.

At the heart of the IPO window's viability is the trajectory of global interest rates. Higher interest rates increase discount rates, which directly compress valuations, particularly for growth-oriented and long-duration tech assets that lack near-term profitability 9. At the beginning of 2026, market optimism was buoyed by expectations of multiple rate cuts from the United States Federal Reserve. However, a sharp rise in oil prices - driven by geopolitical tensions and conflicts in the Middle East - has acted as a supply-side inflation driver, increasing transportation and manufacturing costs 9. Consequently, the Fed is now widely expected to limit its easing cycle, bringing interest rates to a "neutral" level of around 3% and holding them there throughout the remainder of 2026 611.

Despite these inflationary pressures, the underlying economic engine remains healthy, fueled by unprecedented fiscal and monetary stimulus outside of a recessionary period 6. In the United States, consumer spending continues to be supported by a "K-shaped" economy, where middle- and higher-income households drive demand, bolstered by massive wealth effects from double-digit stock market and housing price gains, as well as anticipated federal tax rebates 6. Simultaneously, the European Union is undergoing a meaningful economic acceleration, driven by enormous fiscal stimulus packages in Germany focused on infrastructure and defense, combined with proactive rate cuts from the European Central Bank 67.

This combination of strong fiscal spending, robust corporate earnings, and a stabilization of consumer sentiment has created a highly constructive environment for risk assets, giving underwriters the confidence to push forward with the largest IPO pipeline seen in a generation 89.

The Sovereign Wealth Repositioning

A critical, often underappreciated factor in the 2026 IPO window is the strategic maneuvering of sovereign wealth funds (SWFs), particularly those in the Gulf region. Gulf SWFs currently control approximately $5 trillion in assets - a figure projected to balloon to nearly $18 trillion by 2050 - giving them the financial firepower to act as primary anchors or chief adversaries for any mega-cap public offering 10.

In 2026, a clear divergence in strategy has emerged among the major players. Saudi Arabia's Public Investment Fund (PIF) has dramatically altered its international allocation, announcing a new strategy to keep roughly 80% of its assets deployed domestically to support industrial transformation, tourism, and local manufacturing 1611. As part of this shift, the PIF aggressively trimmed its U.S. equity holdings to a five-year low of just $12 billion in the first quarter of 2026, holding positions in only four U.S.-listed companies 12. This withdrawal of Saudi capital from Western public markets raises the bar meaningfully for tech companies seeking immense liquidity upon listing 11.

Conversely, Abu Dhabi's Mubadala Investment Company has doubled down on global technology. Mubadala increased its U.S. stock holdings to $20.5 billion in Q1 2026, expanding its portfolio to include major semiconductor equipment makers, data intelligence firms, and AI infrastructure providers 12. Furthermore, sovereign entities like Singapore's GIC and the Qatar Investment Authority (QIA) have aggressively anchored late-stage private rounds for companies like Anthropic and Databricks, embedding sovereign capital deeply into the AI ecosystem immediately prior to their IPOs 1314. The presence, or absence, of these trillion-dollar sovereign anchors during the upcoming IPO roadshows will strongly dictate final pricing and secondary market stability.

SpaceX: Testing the Limits of Public Markets

Elon Musk's SpaceX is preparing to test the absolute limits of public market appetite. Having confidentially filed its S-1 prospectus with the U.S. Securities and Exchange Commission, the aerospace and communications giant is preparing for a Nasdaq debut under the ticker SPCX 31516. Originally anticipated for late 2026, the company has reportedly accelerated its timeline, targeting an IPO as early as mid-June 317.

SpaceX is aiming to raise between $75 billion and $80 billion in fresh capital, targeting a valuation floor of $1.75 trillion to $2 trillion 3181920. If the company achieves the upper end of this range, it will comfortably surpass the $1.7 trillion valuation record set by Saudi Aramco in 2019, making it the most valuable public debut in global financial history 21. A $2 trillion market capitalization would instantly place SpaceX in the same elite tier as Apple, Microsoft, and Nvidia, a staggering achievement for a company historically associated with heavy industrial rocket manufacturing 22.

The Financial Dichotomy: Starlink's Profitability vs. xAI's Cash Burn

The financial narrative revealed within the SpaceX S-1 prospectus presents a sharp dichotomy between a highly profitable utility business and a massive, cash-burning technology bet.

On one side of the ledger is Starlink, the company's satellite internet subsidiary. Starlink has quietly evolved into one of the most profitable and rapidly growing subscription businesses on the planet. By the end of 2025, Starlink generated $11.39 billion in revenue - representing 61% of SpaceX's total consolidated revenue of $18.7 billion - and produced an impressive $4.4 billion in operating income 320. The service boasts over 10 million active subscribers across 80 countries, with a year-over-year revenue growth rate exceeding 40% 122.

Starlink's value is underpinned by an insurmountable infrastructure moat. SpaceX has launched over 6,500 low Earth orbit satellites, and analysts estimate that competitors like Amazon's Project Kuiper are at least five years behind in matching the constellation's capacity 22. By manufacturing its own consumer terminals and controlling launch costs through its reusable Falcon 9 rockets, SpaceX has driven customer acquisition costs down to levels that make Starlink wildly cash-flow positive in most global markets 22.

However, the company's broader profitability has been severely eroded by Musk's aggressive capital allocation into artificial intelligence. Following an all-stock merger with Musk's AI startup xAI in February 2026, SpaceX redirected tens of billions of dollars into AI computing infrastructure and orbital data centers 13. In 2025 alone, SpaceX's capital expenditures surged to over $20 billion, driven largely by a $12.7 billion allocation specifically earmarked for AI infrastructure 2129.

Consequently, despite Starlink's operational success and an adjusted EBITDA profit of $6.6 billion, SpaceX reported a consolidated GAAP net loss of $4.94 billion in 2025 320. This cash burn accelerated into the current year, with the company posting a massive $4.28 billion net loss in the first quarter of 2026 alone 2021. The company's accumulated deficit now sits at a staggering $41.3 billion 20. Public market investors are essentially being asked to underwrite a highly profitable satellite internet monopoly that is actively funneling its cash flow into a highly speculative, capital-intensive AI arms race.

A Unique Corporate Governance and Retail Structure

SpaceX's offering is highly unusual in its structural approach to investors. The company is actively courting retail participation, explicitly naming consumer brokerage platforms like Charles Schwab, Fidelity, Robinhood, SoFi, and E-Trade as official allocation channels in its S-1 filing 1929.

Historically, highly anticipated mega-IPOs lock retail investors out of the primary offering, allocating roughly 95% of the float to institutional clients and leaving everyday traders to buy shares on the open market at a significant premium 1629. SpaceX, however, has reportedly earmarked an unprecedented 30% of its offering for retail buyers 1620. At a $75 billion raise, this means retail investors could see up to $22.5 billion in shares allocated directly to them 20. Crucially, these retail shares will be offered at the exact same IPO price as institutional allocations, bypassing the typical "first-day pop" markup that often penalizes ordinary investors 30.

While this retail-friendly distribution has been praised for democratizing access to generational wealth, critical analysts view it as a mechanism to generate immediate demand-driven momentum to validate an exorbitant $2 trillion valuation on day one 20. Furthermore, the inclusive retail offering masks a deeply restrictive internal governance model. Musk will retain absolute majority voting control through a superclass of Class B shares that grant him ten votes per share, effectively rendering public shareholders powerless in corporate decision-making regardless of the public float size 32029.

The mechanics of the listing also heavily favor the company over passive investors. Following a recent rule change by the Nasdaq exchange - effective just weeks before SpaceX's filing - mega-cap companies can now be included in the prestigious Nasdaq-100 index within three weeks of listing, even with a low public float of 8% to 18% 16. Because over $600 billion in passive index funds track the Nasdaq-100, these funds will be forced to buy SpaceX shares blindly at whatever the market price dictates simply to match their benchmark weighting, creating an artificial floor for the stock price regardless of the company's underlying financial fundamentals 1631.

The Generative AI Race: OpenAI vs. Anthropic

As SpaceX paves the way, the two dominant forces in generative artificial intelligence - OpenAI and Anthropic - are locked in a fierce, high-stakes race to the public markets. Both companies are engaged in the pursuit of Artificial General Intelligence (AGI), but they present vastly different financial profiles, risk paradigms, and go-to-market strategies for prospective public shareholders.

OpenAI: The Consumer Giant Facing a "Cash Bonfire"

OpenAI, the creator of ChatGPT, is navigating one of the most complex corporate transitions in modern tech history. Originally founded in 2015 as a non-profit research lab dedicated to ensuring AI benefits humanity, the organization has ballooned into a $500 billion-plus commercial behemoth 2324. To facilitate an IPO and accommodate massive capital infusions from partners like Microsoft and Nvidia, OpenAI recently completed a multi-year restructuring process, abandoning its convoluted "capped-profit" hybrid model to become a traditional for-profit Public Benefit Corporation (PBC) 24343525.

This restructuring resolved significant legal overhangs - including a federal lawsuit brought by Elon Musk that was ultimately dismissed by a jury due to statute of limitations constraints - and cleared the runway for a public listing 26. Reports from early 2026 indicate that OpenAI is accelerating its path to the public markets, aiming for an IPO in the fourth quarter of 2026 or early 2027 to capture investor appetite before its rivals 134.

OpenAI boasts unrivaled consumer dominance. The platform commands 67% of global AI app downloads and reports a staggering 900 million weekly active users, driving roughly 70% of its massive subscription revenue base 154. The company generated $13.1 billion in revenue in 2025 and entered 2026 with an annualized revenue run rate (ARR) of $25 billion 4.

However, operating at the frontier of AI requires astronomical computing power. Training foundational models and running ChatGPT daily has resulted in a severe cash burn. Microsoft recently took a $3.1 billion charge to account for its 27% share of OpenAI's losses, implying total company losses approaching $11 billion 35. Officially, OpenAI recorded an $8 billion net loss in 2025, and internal projections reviewed by early investors suggest cumulative corporate losses could reach an astonishing $115 billion by 2029 4. The company does not expect to achieve true profitability before the early 2030s, with projected annual cash burns of $17 billion in 2026, $35 billion in 2027, and $47 billion in 2028 438.

Despite this lack of profitability, secondary markets and recent funding rounds have valued the company at roughly $852 billion, with the firm reportedly targeting a $1 trillion valuation for its IPO 13439. The central question for public investors will be whether they are willing to underwrite tens of billions in annual losses in exchange for a stake in the world's most recognizable consumer AI brand.

Anthropic: The Enterprise Contender Nearing Profitability

Anthropic, the developer behind the Claude LLM family, has emerged as the most formidable counter-narrative to OpenAI. Founded by former OpenAI executives, Anthropic has positioned itself as the safer, more reliable, and ultimately more financially disciplined alternative 2741.

In late May 2026, Anthropic closed a historic Series H funding round. Led by top-tier venture firms including Altimeter Capital, Dragoneer, Greenoaks, and Sequoia Capital - alongside massive strategic investments from Google and Amazon - the company raised $65 billion overnight 527. This unprecedented capital injection skyrocketed Anthropic's post-money valuation to $965 billion, allowing it to officially surpass OpenAI's last pre-money valuation mark and claim the title of the world's most valuable private AI company 52742.

What separates Anthropic from OpenAI is its operational efficiency and client composition. While OpenAI dominates the consumer space, approximately 80% of Anthropic's revenue is derived directly from lucrative enterprise customers 14. Major corporations, banks, and legal firms prefer Anthropic's Claude models for complex coding, cybersecurity, and automated workflows 2728. According to Counterpoint Research, Anthropic officially overtook OpenAI in global LLM enterprise revenue share in the first quarter of 2026, capturing 31.4% of the market compared to OpenAI's 29% 1. By mid-2026, CEO Dario Amodei reported that Anthropic's annualized revenue run rate had accelerated past $30 billion, with some internal statements suggesting it reached $44 billion representing 80x year-over-year growth 17.

Crucially, internal financial projections reviewed by the Wall Street Journal indicate that Anthropic expects to post a $559 million operating profit in the second quarter of 2026, marking a historic turning point for foundation model developers 2844. The company is achieving this by driving down computing costs from 71 cents to 56 cents for every dollar of revenue 28.

Both OpenAI and Anthropic are legally structured as Public Benefit Corporations (PBCs). Under Delaware corporate law, a PBC board must balance financial returns with a stated mission of public benefit - such as Anthropic's goal of the "responsible development" of AI 26. While legal scholars note that these broad missions give corporate boards enormous deference under the business judgment rule, public market investors generally view the PBC structure with suspicion, fearing that executives might prioritize societal goals over shareholder returns 26. However, Anthropic's rapid path to actual operating profit mitigates this structural concern, making its rumored October 2026 IPO a highly attractive proposition for institutional buyers seeking stability in the AI sector 22845.

Databricks Offers a Stable Enterprise Software Play

While the financial media obsesses over the multi-trillion-dollar valuations and cash-burning arms races of frontier AI labs and space exploration, Databricks represents a more traditional, fundamentally sound enterprise software IPO.

Databricks sits at the highly lucrative intersection of enterprise data warehousing and AI monetization 46. Rather than burning billions to build foundational LLMs from scratch, Databricks provides the vital picks-and-shovels infrastructure that allows Fortune 500 companies to securely apply external AI models to their own proprietary internal data 29.

The company's financial metrics reflect the gold standard of mature SaaS businesses. In early 2026, Databricks crossed a $5.4 billion annualized revenue run rate, growing at an impressive 65% year-over-year 31430. Importantly, its dedicated AI products - including its Genie conversational assistant and its new Lakebase operational database built for AI agents - recently crossed a $1.4 billion revenue run rate on their own 31431. The company serves over 20,000 customers, including 60% of the Fortune 500, with more than 800 clients consuming over $1 million annually 142930.

Following a massive $5 billion equity financing round in early 2026, Databricks is currently valued at $134 billion 31430. Unlike the AGI labs, Databricks has achieved positive free cash flow over the trailing 12 months and maintains a world-class net revenue retention rate exceeding 140% 1430.

While the exact IPO timeline remains unconfirmed, CEO Ali Ghodsi has stated the company is fully "IPO-ready," with market chatter pointing heavily toward a listing in the second half of 2026 when market conditions optimize 346. For public investors wary of the massive capital expenditures required by OpenAI and SpaceX's xAI division, a Databricks IPO offers direct exposure to the AI boom wrapped in the familiar, cash-generative safety of premium enterprise software 9.

Macroeconomic Catalysts and the "Dot-AI" Bubble Debate

The sheer scale of these upcoming offerings has reignited a fierce debate regarding market health and systemic fragility. With the top five technology companies already comprising roughly 30% of the S&P 500 - the highest market concentration in half a century - can the public markets absorb hundreds of billions in new tech equity without buckling under the weight? 3850

Is 2026 a Repeat of the 1999 Dot-Com Crash?

Skeptics, including the chief economist of the International Monetary Fund, frequently compare the 2026 AI boom to the 1999 dot-com bubble 32. The rhetorical language is strikingly similar, and the metrics are alarming: the Shiller CAPE (cyclically-adjusted 10-year price-to-earnings ratio) is higher today than it was on the eve of the 1929 stock market crash, trailing only the absolute peak of the dot-com era 50. Furthermore, U.S. retail investors have poured over $700 billion into equities since January 2026, a retail mania roughly five times faster than the volume seen during the 2000 bubble 32.

However, forensic financial analysis reveals critical structural differences between the two eras. During the dot-com bubble (1995-1999), 314% of the tech sector's total return was driven purely by multiple expansion - meaning investors were simply paying higher and higher premiums for companies that produced no actual profits 33. By contrast, in the current 2021-2026 cycle, 78% of the tech sector's stock return has been driven by actual, verified earnings growth 33. The "Magnificent Seven" tech giants, unlike the startups of 1999, are enormously net cash positive. They carry a return on equity of 46%, generate net income margins of 29%, and fund their operations predominantly through free cash flow rather than toxic debt 50.

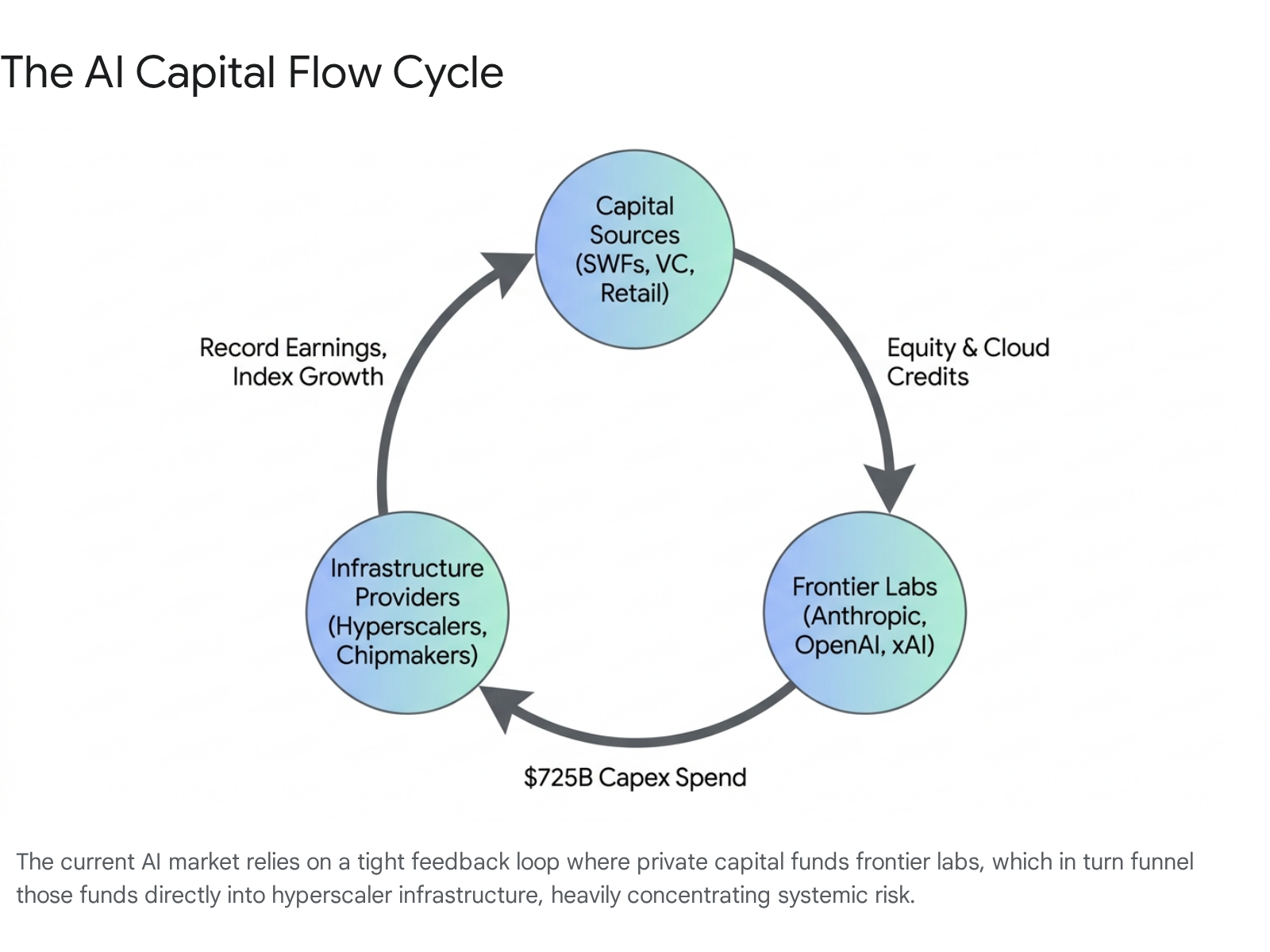

The True Systemic Risk: The Infrastructure Capex Loop

If the software layer is fundamentally sound, where does the risk lie? The true systemic vulnerability in the 2026 market is concentrated in infrastructure capital expenditures (capex).

In order to train and run next-generation AI models, Big Tech hyperscalers (Amazon, Google, Microsoft, Meta) are projected to spend between $650 billion and $725 billion on AI data centers and Nvidia chips in 2026 alone 3853.

This creates a highly fragile "circular financing loop."

Venture capital and sovereign wealth flow into frontier labs like Anthropic and OpenAI. These labs immediately hand that cash directly to the hyperscalers and chipmakers to lease compute power. The hyperscalers then report record corporate earnings to Wall Street, which drives up the S&P 500 and attracts more retail capital, starting the cycle anew 53.

The depreciation math on this hardware is unforgiving. To justify a three-to-five-year lifespan on a $725 billion server investment, the tech industry requires an annual downstream software revenue growth of $360 billion to $600 billion 53. Current enterprise software revenue falls massively short of that threshold. While large tech companies have the free cash flow to absorb impending asset impairments, the massive web of privately valued startups caught in this capital cycle could face a brutal repricing if enterprise ROI on AI tools begins to stall 53.

Global Regulatory Hurdles: The EU AI Act

As OpenAI, Anthropic, and Databricks prepare to enter the public sphere, they face an imminent regulatory cliff that could severely impact their global margins: the European Union Artificial Intelligence Act (EU AI Act).

Unlike prior "soft law" ethical guidelines, the EU AI Act is a comprehensive, legally binding, risk-based framework backed by severe financial penalties. Crucially, the law features an extraterritorial scope; any U.S. company whose AI system or output touches a user within the European Union is fully subject to its rules, regardless of whether the company maintains a physical office or servers in Europe 5434. Non-compliance can result in devastating fines of up to €35 million or 7% of a company's global annual turnover 5434.

While some basic AI literacy obligations went into effect in 2025, the sweeping enforcement deadlines that will directly impact IPO valuations occur in 2026. Full enforcement for "High-Risk" AI systems takes effect in August 2026 - precisely when these companies are pitching their long-term operational viability to Wall Street 5435. Additionally, a new digital omnibus provision mandates that AI watermarking obligations and strict prohibitions on systems that generate non-consensual deepfakes must be active by December 2, 2026 3436.

For public investors, this regulatory landscape fundamentally alters the investment thesis. AI companies can no longer be valued purely on theoretical technological capabilities or user growth metrics. Their valuations must now heavily discount the massive legal and engineering compliance architectures required to operate globally, effectively acting as a "regulatory fragmentation tax" on their future operating margins 37.

Debunking IPO Myths for the Retail Investor

The intense media hype surrounding SpaceX and the AI revolution has flooded retail trading platforms with anticipation. However, retail investors historically face structural disadvantages and informational asymmetries during mega-cap IPOs. It is crucial to separate fact from fiction before committing capital.

Myth 1: Retail Investors Are Completely Locked Out of Good IPOs. Reality: While traditionally true, SpaceX is rewriting the institutional playbook. By allocating 30% of its massive offering directly to retail platforms like SoFi, Robinhood, E-Trade, Fidelity, and Charles Schwab, everyday investors can participate in the primary market 162959. Investors can submit Conditional Offers to Buy (COB) or Indications of Interest (IOI) through these apps prior to listing 2959.

Myth 2: Retail Investors Pay a Huge Premium. Reality: If allocated shares through the official brokerage programs, retail investors will purchase shares at the exact same price as institutional funds and hedge funds. This structure bypasses the punishing secondary market markups that occur when retail traders are forced to buy on the open market after the stock has already begun trading 2930. Note that brokerages enforce strict eligibility criteria; for example, Charles Schwab and Fidelity generally require a minimum account balance of $100,000 to participate in the IPO, whereas SoFi and Robinhood currently require no minimum balance, provided the user has sufficient funds to cover their specific requested share amount 2959.

Myth 3: You Must Buy on Day One to Secure Returns. Reality: The "first-day pop" is often a manufactured illusion driven by artificially tight share supply. Historical quantitative analysis demonstrates that investors who buy during the frenzied first days of high-valuation mega-IPOs generally underperform the broader S&P 500 market over a three-year horizon 60. Renaissance Capital, an IPO research firm, notes that the most favorable buying opportunities often emerge one to three months after the IPO, when initial hype fades, retail traders take profits, or shortly after the standard 180-day insider lock-up period expires, flooding the market with new supply 38.

Myth 4: Mega-Valuations Guarantee Safety and Success. Reality: Valuation at IPO is an exercise in marketing as much as it is in financial mathematics. Buying into SpaceX at a $1.75 trillion valuation means paying over 93 times its 2025 revenue 16. Market history is unforgiving to such premiums: between 1980 and 2023, of the 45 companies that went public with valuations above 40 times their annual sales, only seven traded at a higher price three years later 16. Retail investors buying into the 2026 IPO cohort are inherently buying into high-growth, high-loss profiles, where years of flawless future execution are already completely priced into the initial stock offering.

Bottom line

The third-quarter 2026 IPO window represents a generational stress test for global capital markets. SpaceX, OpenAI, Anthropic, and Databricks are offering investors a direct stake in the infrastructure of the next decade, but at unprecedented valuations that demand flawless commercial execution and sustained, massive capital expenditure. While structural innovations like SpaceX's 30% retail allocation democratize access to these offerings, astute investors must look past the media frenzy to weigh the harsh realities of multi-billion dollar operating losses, impending European regulations, and the finite limits of global liquidity.