Endowment Effect and the Valuation of Owned and Non-Owned Goods

The endowment effect remains one of the most rigorously debated phenomena in behavioral economics, cognitive psychology, and consumer theory. Initially conceptualized as a manifestation of loss aversion within the broader framework of prospect theory, the effect describes the systematic tendency of individuals to assign greater value to objects they own compared to identical objects they do not own 23. In empirical terms, this is observed as a persistent gap between an individual's willingness to accept (WTA) compensation to relinquish a good and their maximum willingness to pay (WTP) to acquire it 12. Standard neoclassical economic theory, formalized by Willig (1976), posits that absent substantial income effects or a lack of close market substitutes, the WTA and WTP for a given asset should theoretically converge 3. The persistent divergence of these metrics in laboratory and field settings fundamentally challenges the Hicksian model of consumer preferences and the assumption of rational, reference-independent valuation 45.

However, the consensus surrounding the endowment effect is far from absolute. Modern scholarship has subjected the phenomenon to intense methodological scrutiny, exploring whether the WTA-WTP gap represents a fundamental feature of human cognition or a mere artifact of experimental design 678. Recent neurobiological research utilizing eye-tracking and pupil dilation has sought to map the physiological roots of the bias, while meta-analyses have proposed alternative mechanisms based on adaptively rational market beliefs 19. Furthermore, the rapid virtualization of the global economy has introduced unprecedented complexities. As commerce shifts toward intangible assets, digital goods, and non-fungible tokens (NFTs), the traditional boundaries of "ownership" have been profoundly redefined 101112. Concurrently, cross-cultural studies and developmental economics have questioned the universality of the endowment effect, revealing striking variances across different geographic populations and socioeconomic strata, particularly among those living in extreme poverty 131415.

This exhaustive report provides a comprehensive analysis of the endowment effect, expanding upon classic paradigms to integrate contemporary critiques, boundary conditions, and digital applications. The analysis systematically delineates the endowment effect from related cognitive biases, rigorously dissects the methodological critiques of experimental artifacts, explores cultural and economic boundary conditions, and connects the underlying psychological mechanisms to modern digital asset valuations and consumer market strategies.

Delineating the Endowment Effect from Adjacent Cognitive Biases

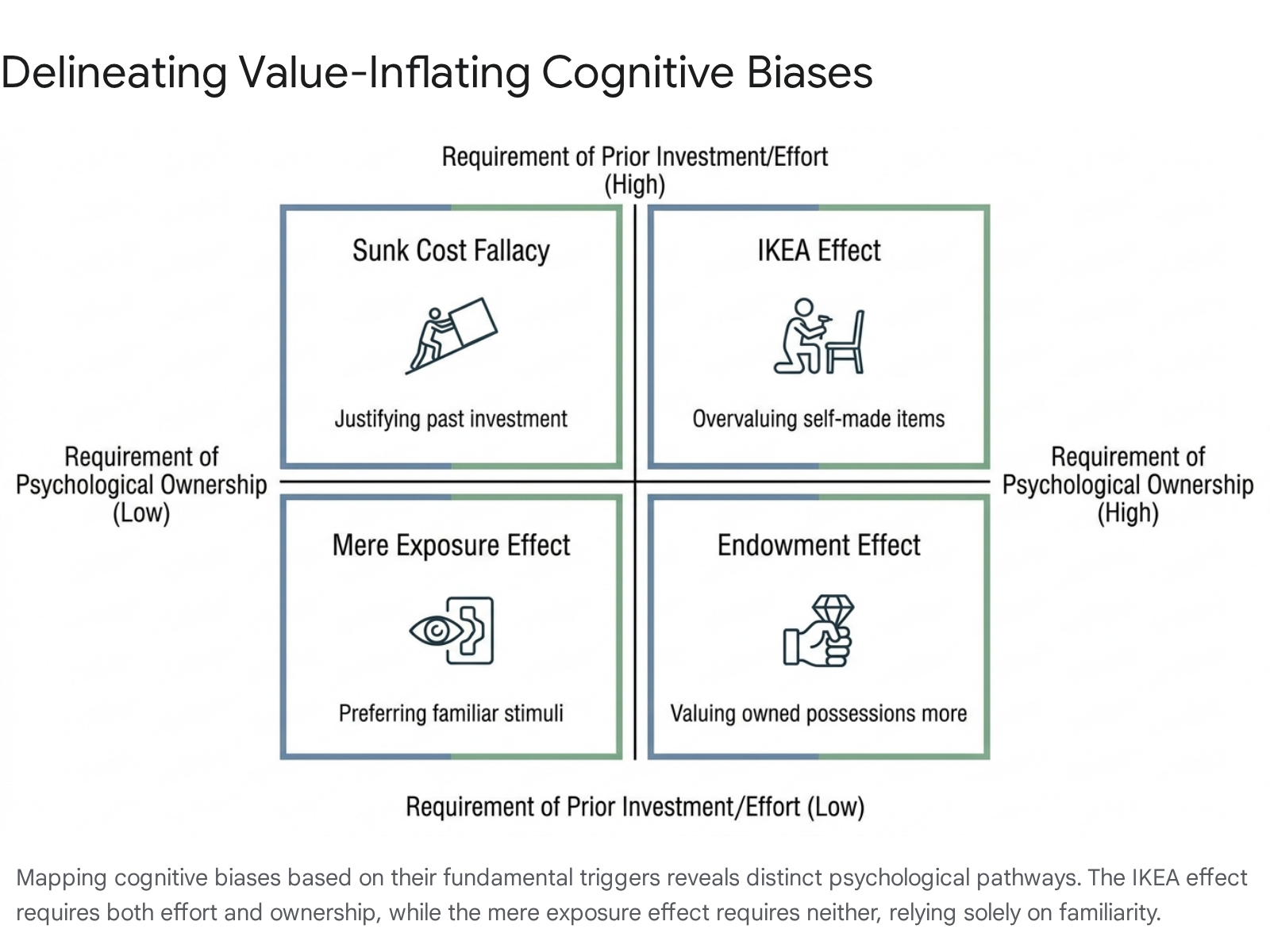

To accurately operationalize the endowment effect in economic modeling, it is imperative to explicitly delineate it from adjacent cognitive heuristics. While the endowment effect, the sunk cost fallacy, the mere exposure effect, and the IKEA effect all result in elevated valuations, cognitive rigidity, or commitments to the status quo, their underlying psychological triggers, required investments, and temporal orientations differ significantly 1621.

Failure to distinguish among these biases leads to conflated empirical results and misapplied market strategies.

The Endowment Effect vs. The Sunk Cost Fallacy

The endowment effect is triggered almost instantaneously upon the psychological or legal transfer of ownership. It requires no prior investment of time, physical labor, or financial capital. The elevated valuation stems purely from reference-dependent preferences and loss aversion; the prospect of giving up the item is encoded by the brain as a loss, which looms roughly twice as large as the equivalent gain of acquiring it 22217.

In stark contrast, the sunk cost fallacy - also referred to in the literature as the irrational escalation of commitment - is entirely dependent on historical, unrecoverable investments 18. An individual succumbing to the sunk cost fallacy continues a suboptimal endeavor or retains a depreciating asset specifically to justify prior expenditures of money, effort, or time, regardless of the asset's current objective utility 182519. The endowment effect is fundamentally a state-based bias rooted in the current condition of possession, whereas the sunk cost fallacy is a path-dependent bias rooted in past action and the psychological discomfort of admitting a wasted investment 2728. For example, in litigation negotiations, parties often overvalue their claims due to the endowment effect (psychological ownership of the claim), but they also refuse to settle due to the sunk cost fallacy, factoring in unrecoverable legal fees already spent 20.

The Endowment Effect vs. The Mere Exposure Effect

The mere exposure effect, a foundational principle rooted in social psychology, dictates that individuals express an undue preference for things merely because they are familiar with them 162125. Familiarity breeds cognitive fluency, making the neural processing of the stimulus easier and subsequently generating a positive affective response.

Crucially, the mere exposure effect does not require ownership, nor does it typically generate the severe WTA-WTP asymmetries observed in economic exchanges 1825. An individual may exhibit a higher WTP for a familiar brand of coffee over an unfamiliar one simply due to repeated visual exposure. However, the endowment effect dictates that the individual's WTA to surrender a specific mug they were just handed will greatly exceed their WTP for it, even if both the owned mug and an alternative unowned mug are equally familiar to the subject 617. The mere exposure effect alters baseline preferences through repetition, while the endowment effect alters valuation metrics strictly through the lens of possession.

The Endowment Effect vs. The IKEA Effect

The IKEA effect represents a distinct cognitive bias wherein individuals assign a disproportionately high value to objects they have partially or fully assembled themselves, regardless of the objective quality of the final product 2119. While the endowment effect operates on the principle of mere possession, the IKEA effect operates on the principles of effort justification, self-efficacy, and the "effort heuristic" 183021.

Labor transforms a generic commodity into a personalized artifact, effectively infusing the creator's identity into the object 2233. Neuroimaging and behavioral studies demonstrate that the IKEA effect amplifies baseline endowment. Functional magnetic resonance imaging (fMRI) studies have shown significant activation in the right inferior frontal gyrus (R-IFG) when individuals evaluate self-assembled products, linking the labor experience directly to memory retrieval and subjective economic valuation 21. The labor converts the object into a self-extension, making the loss-aversion weighting exponentially stronger 2133.

Specific boundary conditions for the IKEA effect explicitly separate it from simple endowment: if a consumer builds a product but is then instructed to disassemble it, thereby nullifying the physical labor and destroying the creation, the IKEA effect vanishes, whereas standard endowment effects for the raw materials may persist 3022. Furthermore, if the assembly process is too difficult and the individual fails to complete the task, the value-enhancing effect is negated, proving that successful completion and the resulting sense of competence are prerequisite mechanisms 302122.

Methodological Critiques: The Plott and Zeiler Artifact Argument

Following Kahneman, Knetsch, and Thaler's seminal 1990 experiments demonstrating the undertrading of coffee mugs in laboratory settings, the endowment effect was largely accepted as empirical proof of loss aversion 417. However, a formidable wave of methodological critiques emerged in the early 2000s. The most consequential of these critiques was advanced by economists Charles R. Plott and Kathryn Zeiler (2005, 2007), who formulated the "experimental artifact" hypothesis. Their core argument posits that the widely observed WTP-WTA gaps do not reflect a fundamental feature of human preferences, but are instead symptomatic of subjects' profound misconceptions regarding the nature of the experimental valuation tasks 723.

Deconstructing the Valuation Paradigm

Endowment effect research typically utilizes two primary methodologies: the valuation paradigm and the exchange paradigm. In the valuation paradigm, subjects state their maximum WTP or minimum WTA for an item, usually elicited via the Becker-DeGroot-Marschak (BDM) mechanism, which is designed to be incentive-compatible 224.

Plott and Zeiler (2005) targeted the valuation paradigm, noting that the BDM mechanism is highly complex and unintuitive for lay participants. They hypothesized that subjects conflate the BDM mechanism with standard market bargaining, where the optimal strategy is to understate WTP and overstate WTA 25. To test this, Plott and Zeiler implemented a rigorous "revealed theory" methodology. Because no comprehensive theory of subject misconception existed, they combined the union of all experimental controls utilized in previous literature to create an environment where misunderstandings were theoretically eliminated 72326. These controls included: 1. Extensive Training: Providing detailed, explicit explanations of the BDM mechanism to ensure subjects understood that truth-telling (revealing their actual valuation) was the dominant strategy 78. 2. Paid Practice: Allowing subjects to participate in up to 14 paid practice rounds using induced-value tokens and small-stake lotteries before evaluating actual consumption goods like coffee mugs 823. 3. Anonymity: Ensuring decisions were entirely blind to mitigate social desirability bias, signaling, or the fear of appearing foolish in front of experimenters or peers 78.

When these rigorous controls were applied simultaneously, the WTA-WTP gap for standard physical goods completely vanished, with markets clearing at expected neoclassical rates. Plott and Zeiler concluded that the gap could be "turned on and off" by manipulating laboratory procedures, casting severe doubt on the interpretation of observed gaps as evidence of loss aversion 7826.

Deconstructing the Exchange Paradigm

In a subsequent 2007 paper, Plott and Zeiler applied similar scrutiny to the exchange paradigm, where subjects are endowed with a good and subsequently offered the opportunity to trade it for an alternative good of roughly equal value 26. Knetsch (1989) famously showed that individuals dramatically under-trade in these scenarios 142527.

Plott and Zeiler argued that standard exchange experiments feature subtle procedural cues that artificially alter behavior. For instance, an experimenter physically handing an item to a subject and stating "this is yours" may implicitly signal value or establish a social norm against rejecting a "gift" 62728. By removing these signaling mechanisms, altering how the endowment was framed, and placing items in unmarked bags, they demonstrated that trade volumes increased to the theoretically predicted 50%, effectively eliminating the exchange asymmetry 628. Follow-up studies demonstrated that allowing participants to physically taste or sample goods (like chocolate) before trading also fully dissipated exchange asymmetries by resolving object uncertainty 6.

Rebuttals, Lotteries, and Market Beliefs

The Plott and Zeiler findings initiated fierce academic debate. Critics, notably Isoni, Loomes, and Sugden (2011), replicated the Plott and Zeiler procedures and confirmed that while the gap for simple consumption goods like mugs disappeared, significant WTA-WTP disparities persisted when the assets were lotteries or risky prospects 82930. Plott and Zeiler responded by asserting that lotteries generate unstable attitudes toward uncertainty, and that anomalies involving risk should not be conflated with the pure endowment effect for certain goods 2330.

As the debate progressed, researchers proposed alternative psychological frameworks that do not rely on standard loss aversion. Weaver and Frederick (2012) proposed that the WTA-WTP gap reflects "adaptively rational" behavior based on market beliefs. In their meta-analysis, they found that buyers and sellers anchor heavily on reference prices (market retail prices). Buyers will only offer a WTP that represents a "good deal" (substantially below retail), while sellers demand a WTA close to what they believe the product is worth in the broader market. Thus, the gap may not represent an ownership-induced change in intrinsic preferences, but rather an aversion to conducting a "bad trade" relative to perceived market norms 12.

Further biological research supports the complexity of this transaction process. A 2023 study mapping the physiological mechanisms of trading found that gaze duration and pupil dilation predict the likelihood of a transaction. Sellers' pupils dilate when they focus on their goods, suggesting loss aversion is deeply tied to the biological yoking of visual attention and vigilance systems 9. If attention is manipulated away from the endowed object, the effect diminishes, suggesting that the endowment effect is a complex interplay of visual attention, market-belief anchoring, and procedural context 914.

Boundary Conditions I: Socio-Cultural Conditioning and Evolutionary Context

The classical assumption that the endowment effect is a universal, hardwired human trait has been profoundly challenged by cross-cultural psychology and evolutionary anthropology. Evidence suggests that the manifestation of the bias is heavily contingent upon cultural self-construal and historical exposure to market economies 1315.

Cultural Conditioning and Self-Construal

If the endowment effect is fundamentally tied to identity - the psychological extension of the self into owned objects - then cultural frameworks governing the definition of the "self" should modulate the effect. Maddux et al. (2010) demonstrated precisely this by conducting comparative studies between Western and East Asian populations.

Western cultures predominantly foster an independent self-construal, which prioritizes self-enhancement, autonomy, and individual distinctiveness. Consequently, Westerners exhibit a robust endowment effect; owning an object automatically elevates its value as a psychological extension of the enhanced individual self 313233. Conversely, East Asian cultures emphasize an interdependent self-construal, characterized by social harmony, relationship orientation, and self-criticism. In these populations, the object-to-self association does not trigger the same automatic value inflation, resulting in a significantly smaller, or entirely absent, endowment effect 313233. When researchers experimentally primed individuals with independent versus interdependent self-construals, the magnitude of the endowment effect shifted accordingly, proving that the bias is highly malleable and culturally sensitive 3133.

Evolutionary Origins and Hunter-Gatherer Evidence

Evolutionary psychologists have long sought to determine if the endowment effect is an ancestral human trait or a modern byproduct of capitalism. While some studies have found mixed evidence of the bias in non-human primates like capuchin monkeys and chimpanzees, the most definitive human evidence comes from isolated populations 1333.

Apicella et al. (2014) conducted groundbreaking behavioral experiments with the Hadza hunter-gatherers of Northern Tanzania, one of the last remaining populations living in an ancestral environment 131534. The Hadza living in remote, isolated camps characterized by highly egalitarian, communal sharing norms exhibited virtually zero endowment effect; they traded randomly assigned goods freely, operating closer to the rational neoclassical benchmark than Western college students 131535. However, Hadza individuals living in geographic regions with frequent exposure to ethno-tourists, modern market economies, and the concepts of formalized property rights displayed a pronounced endowment effect 133435. This strongly suggests that the psychological aversion to relinquishing property is not a human universal, but rather a learned heuristic that is culturally conditioned by exposure to capitalistic societies and modern economic exchange 131534.

Boundary Conditions II: Extreme Poverty, Scarcity, and Rational Inattention

Behavioral development economics provides another critical boundary condition for the endowment effect: extreme poverty. Theoretical models propose a "scarcity mindset," wherein the constant psychological burden of poverty consumes cognitive bandwidth, causing mental taxation, stress, and poor nutrition 343649. This chronic scarcity is theorized to exacerbate cognitive biases, particularly present-bias and loss aversion 364937. Under this framework, it is hypothesized that the poor, possessing highly constrained budgets, should exhibit extreme loss aversion and a magnified endowment effect, clinging tightly to whatever few assets they own.

Empirical Field Evidence from Zambian Farmers

However, empirical evidence from large-scale field studies reveals a much more nuanced reality regarding acute scarcity. Fehr et al. conducted a massive series of decision experiments involving 3,059 small-scale farmers in rural Zambia, capturing 5,842 trading decisions over multiple agricultural seasons 142728.

While the baseline exchange asymmetry among these farmers was remarkably robust (on average, only 34% of subjects traded their endowed items), the effect size fluctuated wildly based on the immediate severity of resource constraints 2728. During the "hungry season" - the period of extreme acute scarcity just prior to the harvest when financial and caloric resources are depleted - the likelihood of trading the endowed item increased by roughly 10 percentage points 2728. This increase in trade effectively reduced the exchange asymmetry by more than 50% 2728. Furthermore, when these farmers were provided access to short-term liquidity, mitigating their immediate scarcity, their exchange asymmetries actually widened, indicating a return to standard endowment behavior 28.

Rational Inattention Theory

This counterintuitive finding - that acute poverty diminishes the endowment effect - aligns with the economic theory of rational inattention 14. According to this theory, decision-makers choose how much cognitive attention to allocate to a problem based on its relative importance 14. During times of relative abundance, low-value household items do not warrant the cognitive effort required to calculate optimal utility trades, allowing the default status quo bias (the endowment effect) to dominate decision-making 14.

However, during periods of extreme poverty, the marginal utility of every physical asset skyrockets. The stakes of the decision are significantly higher relative to the household's total income 14. This acute scarcity forces individuals to overcome heuristic inertia, allocate cognitive bandwidth to the problem, and engage in highly rational, utility-maximizing trade 14. Thus, while chronic, generational poverty may induce systemic psychological traps, the pressure of acute, immediate scarcity over tradable goods actually suppresses the endowment effect, pushing behavior much closer to standard neoclassical predictions than is seen in affluent populations 1449.

The Digital Frontier: Intangibility, Psychological Ownership, and 2023+ Asset Classes

As global consumption paradigms shift from physical environments to digital ecosystems, the parameters of the endowment effect are being fundamentally rewritten. Traditional economic definitions of the bias rely heavily on physical possession and tactile interaction 310. Digital goods - ranging from streaming media and software to video game cosmetics and Non-Fungible Tokens (NFTs) - are inherently intangible, infinitely replicable, and often reside on corporate servers rather than in a consumer's physical hands 310.

Psychological Ownership Without Physical Possession

Extensive research from 2023 onward confirms that the endowment effect persists in digital environments, but its magnitude is entirely mediated by the concept of psychological ownership 383940. Psychological ownership is defined as the cognitive state in which an individual perceives an object, whether tangible or intangible, as "theirs" 4142.

Pierce et al. (2001) argued that psychological ownership arises from three fundamental motives: efficacy, self-identity, and belongingness, which are fulfilled through three pathways: investing the self into the target, having control over the target, and intimately knowing the target 404142. Because digital goods lack physicality, they inherently struggle to trigger these pathways. In a foundational study, Atasoy and Morewedge (2018) demonstrated that consumers generally value digital goods less than their exact physical counterparts (e.g., digital movies vs. DVDs, e-books vs. paperbacks) precisely because intangibility inhibits the formation of robust psychological ownership 104344. When evaluated using "Pay-What-You-Want" (PWYW) or standard WTP metrics, consumers consistently offer less for digital formats 1044.

However, modern digital environments can artificially induce profound psychological ownership to overcome this tangibility deficit 4041. In online gaming environments (e.g., Counter-Strike: Global Offensive or World of Warcraft), players develop intense psychological ownership over virtual avatars and cosmetic "skins" 414546. When a player identifies heavily with an avatar, the in-game items become extensions of the digital self, satisfying the self-investment and control pathways of ownership 41. Consequently, players exhibit severe loss aversion regarding these virtual assets, leading to highly inflated WTA metrics in secondary gaming markets that rival or exceed physical goods 334161.

Non-Fungible Tokens (NFTs) and Extreme Valuation Disparities

The advent of blockchain technology and Non-Fungible Tokens (NFTs) introduced verifiable digital scarcity, fusing the intangibility of digital assets with the exclusivity of physical collectibles 474849. Empirical analyses of major NFT collections (e.g., CryptoPunks, Bored Ape Yacht Club, Pudgy Penguins) reveal highly irregular, asymmetric endowment effects that break traditional models 1250.

Unlike traditional physical goods where the WTA/WTP ratio generally hovers around 2:1, NFT markets exhibit massive disparities driven by asset rarity, social signaling, and on-chain herding 1250. A comprehensive 4-layer valuation framework - comprising the Asset, Market, Technology, and Ecosystem layers - highlights how NFTs decouple from standard utility 50. Sellers of NFTs index their WTA heavily on the token's within-collection rarity and specific aesthetic traits, often refusing to lower prices even during severe macroeconomic downturns 1250. Buyers, however, are more heavily influenced by overall market trends and crypto-volatility, leading to fragmented liquidity and persistent pricing disparities 124850.

Furthermore, these decentralized digital markets are not immune to real-world sociological biases. Empirical studies of avatars in the metaverse show that CryptoPunk NFTs representing female identities trade at a 37% lower price than their male counterparts, and Black avatars trade at a 31% discount compared to White counterparts, holding other image attributes equal 51. Interestingly, equipping these avatars with tech-oriented attributes (e.g., 3D virtual reality headsets or "nerd glasses") neutralizes these racial and gender price disparities, indicating that the WTA-WTP gap in the metaverse is deeply intertwined with complex real-world prejudice and technological signaling 51.

Data Privacy as an Endowed Asset

The digital economy has also commodified personal data, transforming privacy into a virtual asset subject to severe endowment effects. In emerging digital economies, such as India, consumers demonstrate an "extraordinary superendowment effect" regarding their personal information 67.

Recent empirical studies reveal that while Indian consumers display a very low WTP to protect their general data (e.g., paying approximately ₹300 per month for ad-free, secure services), they demand exorbitant compensation (a WTA of ₹3,800 per month) to voluntarily surrender it 67. This creates a staggering WTA:WTP ratio of 14:1. This massive disparity suggests that digital privacy is often treated not as a fungible commodity, but as a deeply symbolic asset tied to dignity, national identity, and personal sovereignty 67. High WTA figures in this context reflect "moral outrage" and a symbolic stand that dignity is not for sale, rendering traditional utility-based cost-benefit models wholly inadequate for data valuation 67.

The Impact of Payment Methods on Valuation

The medium of exchange itself also modulates the endowment effect. Research into mental accounting demonstrates that consumers' psychological ownership of their chosen payment method directly influences their valuation of goods 4452. Consumers generally hold stronger psychological ownership over physical cash compared to Mobile Payments (MP) 44. Because cash is physically held and visually depleted when spent, the pain of paying (loss aversion) is acute 3. Consequently, when paying with cash, WTP is generally suppressed. Conversely, when paying with mobile wallets, the psychological distance dampens the loss aversion, resulting in a higher WTP for identical goods 4452. In remittance and receiving scenarios, if a consumer receives payment via a highly owned method (cash), their subsequent WTA for acquired goods is lower, showcasing that the psychology of the transaction medium bleeds into the valuation of the object itself 52.

Comparative Valuations: Physical vs. Digital Assets

The following table synthesizes the varying magnitudes of the WTA/WTP ratio across classic physical goods and contemporary digital assets, highlighting the profound impact of intangibility, rarity, and psychological ownership.

| Asset Category | Specific Good / Asset Type | Estimated WTA/WTP Ratio | Primary Valuation Driver | Source Literature |

|---|---|---|---|---|

| Classic Physical | Coffee Mugs, Pens | ~ 2.0 : 1 | Mere possession, tactile control | Kahneman et al. (1990) 417 |

| Classic Physical | Lottery Tickets (Small Stakes) | ~ 1.5 - 2.0 : 1 | Risk aversion, uncertainty | Knetsch & Sinden (1984) 2969 |

| Public/Environmental | Clean Air, Safety | ~ 5.0 - 6.0 : 1 | Lack of substitutes, moral outrage | Tunçel & Hammitt (2014) 6753 |

| General Digital | Standard Digital Media (E-books, MP3s) | < 2.0 : 1 (Often lower than physical counterparts) | Deficient psychological ownership, infinite replicability | Atasoy & Morewedge (2018) 1043 |

| Virtual Economies | Digital Cosmetics (Game Skins) | Variable (~ 2.0 - 3.0 : 1) | Avatar identification, perceived control, platform lock-in | Lehdonvirta (2009), An & Lv (2025) 414661 |

| Blockchain/Web3 | Non-Fungible Tokens (NFTs) | Highly elevated (Extreme variance) | Provable digital scarcity, within-collection rarity, social signaling | Vomberg et al. (2025), Horky et al. (2022) 1250 |

| Digital Identity | Personal Data Privacy (India context) | 14.0 : 1 | Symbolic value, moral outrage, superendowment | Asia Research (2025) 67 |

Applied Behavioral Economics: Consumer Strategies and Market Engineering

The theoretical mechanisms underpinning the endowment effect - specifically psychological ownership, effort justification, and loss aversion - have been heavily weaponized in modern consumer marketing and software distribution. Corporations actively circumvent traditional price resistance (WTP) by allowing consumers to acquire temporary or partial ownership of a product at zero initial cost, relying on the endowment effect to drive eventual conversion.

Freemium Models and Digital Free Trials

The "freemium" SaaS (Software as a Service) model relies fundamentally on the rapid establishment of psychological ownership. By providing users with free, immediate access to a platform (e.g., Spotify, Zoom, Adobe), the provider shifts the consumer's decision-making frame 227172. At the end of a 30-day trial, the user is no longer evaluating the abstract utility of gaining a premium service (which triggers WTP friction and standard budget constraints); instead, they are evaluating the immediate pain of losing ad-free listening, customized dashboards, or essential enterprise features 2272.

Because the pain of loss is weighted roughly twice as heavily as the pleasure of an equivalent gain, conversion rates soar. Interestingly, empirical research sharply differentiates between "Time-Limited" and "Feature-Limited" freemium models. Time-limited trials are generally more profitable because they allow the user to fully integrate the software into their daily routine, maximizing psychological ownership and generating high "time-to-value" metrics 717273. When the trial expires, the loss aversion is acute. Conversely, feature-limited freemium models (where a basic tier is free forever, but premium features are locked) often fail to trigger the endowment effect for the premium tier, as the user never experiences psychological ownership of the locked features 7173.

Customization and Artificial Lock-In

Digital product managers intentionally foster the endowment effect through guided user onboarding. When users invest time configuring a SaaS dashboard, customizing an avatar, or uploading proprietary data, they create an association between the self and the platform 272. This effectively merges the endowment effect with the effort-justification mechanisms of the IKEA effect 72. The more data and customized content a user inputs, the higher the psychological switching costs. Some platforms implement "artificial lock-in mechanisms," intentionally designing data export or migration to be cumbersome, thereby weaponizing loss aversion to maintain high customer retention rates 7172.

Money-Back Guarantees

In physical retail and e-commerce, the "100% money-back guarantee" serves as an elegant heuristic hack. For a prospective buyer, the guarantee essentially lowers the perceived risk and standard WTP barrier to zero, framed safely as a risk-free trial 2273. However, marketers understand that once the product is in the consumer's home, the endowment effect activates. The consumer takes physical possession, begins to view the item as "theirs," and potentially invests effort in setting it up 7273. When the 30-day return window inevitably closes, the cognitive cost of relinquishing the item - combined with the physical friction of packaging and shipping it - far outweighs the utility of recovering the initial funds. As a direct result of this engineered loss aversion, return rates remain highly suppressed, making the guarantee highly profitable for the retailer 2273.

Conclusion

The endowment effect has evolved from a simple anomaly of laboratory economics into a highly complex, multi-dimensional construct mediated by methodology, culture, and technology. The rigorous critiques posed by Plott and Zeiler successfully demonstrate that experimental artifacts and subject misunderstandings can artificially inflate the WTA-WTP gap, demanding strict incentive-compatible controls in all future valuation research. However, the persistence of the bias in field data, complex financial assets, and cross-cultural evaluations confirms that reference-dependent valuation is a deeply ingrained cognitive feature, albeit one that is adaptively rational and culturally conditioned rather than biologically absolute.

As global economies transition toward intangible, digital assets, the locus of the endowment effect is rapidly shifting from physical possession to psychological ownership. While standard digital goods initially suffer from lower valuations due to a lack of tactile engagement, modern digital platforms aggressively circumvent this by leveraging customization, avatar identification, and cryptographic scarcity to engineer profound loss aversion. Ultimately, understanding the boundary conditions of the endowment effect - from the acute rationality induced by extreme poverty to the massive superendowment of digital privacy - is essential for both macroeconomic policy modeling and the ethical design of digital consumer architecture.