Why We Value Things More Once We Own Them

We inherently place a higher financial and emotional value on items simply because they belong to us, a cognitive bias known as the endowment effect. Originally attributed to a deep-seated human fear of losing what we already possess, a massive wave of recent behavioral research suggests this phenomenon is actually driven by strategic market behaviors, our desire to avoid a "bad deal," and cultural conditioning. Understanding this cognitive quirk can help you make more rational decisions, from decluttering your home to negotiating high-stakes purchases like real estate and vehicles.

The Discovery of the Endowment Effect

To fully grasp why we cling to our possessions, it is necessary to examine the foundational assumptions of classical economic theory. For centuries, mainstream economics was built on the model of Homo economicus - the idea that humans are perfectly rational, self-interested actors who consistently make decisions to maximize their personal utility. According to this traditional framework, the intrinsic value of a good should remain static regardless of who holds the property rights. If a standard coffee mug provides you with $3 worth of utility, you should be willing to pay exactly $3 to acquire it. Conversely, if someone offers you $3.01 for that same mug, you should be perfectly happy to sell it, as the cash offer exceeds your internal valuation. In classical terms, this assumes that a person's willingness to pay (WTP) for a good should always equal their willingness to accept (WTA) compensation to be deprived of it 1. This assumption underlies fundamental economic concepts like consumer theory, indifference curves, and the Coase theorem, which posits that the initial allocation of goods is irrelevant because rational actors will simply trade until they reach an efficient outcome 12.

However, as economists began to study actual human behavior in the late 1970s and 1980s, they noticed that real people rarely behave with such mathematical precision.

The term "endowment effect" was officially coined in 1980 by Richard Thaler, a pioneering behavioral economist who would eventually win the 2017 Nobel Prize in Economics for his contributions to the field 34. Thaler observed a distinct pattern of irrationality, which he famously illustrated through the anecdote of a "wine-loving economist." This hypothetical economist had purchased several bottles of high-quality Bordeaux wine years earlier at very low prices. Over time, the wines appreciated significantly in the market, to the point where a bottle that originally cost $10 would now fetch $200 at a wine auction 5. Thaler noted that the economist occasionally drank the wine with dinner, but he outright refused to sell his remaining bottles at the $200 auction price. Simultaneously, he refused to buy any new bottles at that $200 price point 56.

If the wine was truly worth $200 in utility to him, he should have been willing to buy more. If it was worth less than $200 to him, he should have been aggressively selling his cellar to capture the profit. Instead, the mere fact that the wine was already integrated into his "endowment" drastically altered its perceived value 57. He valued the wine highly because he owned it, demonstrating a profound asymmetry in human valuation.

The Classic Cornell Mug Experiment

Thaler's conceptualization of the endowment effect was a direct challenge to the standard economic theory of the time. To prove the phenomenon empirically, Thaler teamed up with renowned psychologists Daniel Kahneman and Jack Knetsch in 1990 to conduct what is now famously known in behavioral science as the "Mug Experiment" at Cornell University 468.

The experimental setup was elegantly simple, designed to eliminate transaction costs, wealth effects, and emotional sentimentality. The researchers recruited a group of undergraduate students and randomly divided them into two cohorts: buyers and sellers. The sellers were handed a standard, university-branded coffee mug, which was actively available for purchase at the campus bookstore for about $6. The buyers received nothing. After allowing the sellers to briefly examine their newly acquired mugs, the researchers opened a hypothetical laboratory market and asked both groups to state their desired transaction prices 468.

If classical economics held true, the random distribution of the mugs meant that the average selling price and the average buying price should have settled at roughly the same market clearing rate - somewhere near the $6 retail value, or perhaps slightly less depending on the students' budgets 68.

The actual results shattered standard economic expectations and created a cornerstone finding for behavioral economics. The students who were randomly endowed with the mugs demanded a median price of $5.25 to part with them. Meanwhile, the buyers in the other group were only willing to pay a median price of $2.25 to $2.75 to acquire one 688. The sellers valued the exact same ceramic object roughly twice as highly as the buyers, simply because they possessed it. No sentimental backstory, no sunk costs, and no extensive usage history were required; the psychological switch flipped in a matter of seconds, instantly rewiring the participants' valuation circuitry 16.

The Three Paradigms of Endowment

Since the publication of the Cornell study, the endowment effect has become one of the most widely replicated phenomena in behavioral science, surviving intense methodological scrutiny. Researchers today typically elicit and measure the effect using three distinct experimental paradigms 1:

| Paradigm Type | Description of Methodology | Key Metric Measured | Typical Example Outcome |

|---|---|---|---|

| Valuation Paradigm | Participants are assigned as buyers or sellers and asked to state exact cash values for an item. | The resulting gap between Willingness to Pay (WTP) and Willingness to Accept (WTA). | Sellers demand $7 to part with a generic pen, while buyers only offer $3 to acquire it 1. |

| Exchange Paradigm | Participants are given an item and later offered the chance to trade it for a different item of equal market value. | The percentage of participants who irrationally refuse to trade. | 90% of participants given a mug refuse to trade it for a chocolate bar, and vice versa 19. |

| Mere Ownership Paradigm | Participants rate the attractiveness or quality of an item without financial incentives (no real money changes hands). | Subjective rating scores on a standardized Likert scale. | Randomly assigned "owners" rate a generic keychain much more favorably than "non-owners" 1. |

Across all three paradigms, the data reliably demonstrates that ownership - even trivial, momentary, or completely imagined ownership - fundamentally alters human preference and valuation 6.

The Traditional Explanation: Loss Aversion and Prospect Theory

For decades, the dominant psychological explanation for the endowment effect rested almost entirely on the concept of loss aversion, which serves as a core ingredient of Prospect Theory, introduced by Amos Tversky and Daniel Kahneman in 1979 4101112.

Prospect Theory maps out how humans make decisions under conditions of risk, uncertainty, and changing circumstances. Its most famous and heavily cited tenet is that the psychological pain of losing something is vastly more powerful than the psychological pleasure of gaining an equivalent item. Specifically, behavioral economists have calculated through extensive laboratory testing that humans are roughly 2 to 2.5 times more sensitive to losses than they are to gains of a similar size 811. Finding a $20 bill on the sidewalk brings a mild, fleeting burst of joy; losing a $20 bill from your wallet can trigger intense frustration that ruins an entire afternoon.

When applied to the endowment effect, loss aversion provides a seemingly perfect theoretical explanation. Because of our deep-seated evolutionary aversion to loss, any market transaction is framed differently depending on an individual's current reference point 3410. For a prospective buyer, the transaction is viewed as a potential gain (acquiring a new coffee mug). For the seller, however, the transaction is framed strictly as a loss (giving up their coffee mug). Because losses loom so much larger than gains in the human psyche, the seller naturally requires a much higher financial premium to offset the psychological pain of the loss. The stark difference between the pain of losing and the pleasure of gaining creates the massive WTA-WTP gap observed in the data 13.

The Role of Psychological Ownership

While actual, legal ownership clearly triggers loss aversion, researchers soon discovered that psychological ownership - the mere subjective feeling that something belongs to you - is equally potent. We are incredibly quick to forge a cognitive link between our possessions and our sense of self.

According to extensive research by Morewedge and Giblin, actual legal entitlement is not required for the endowment effect to kick in; a subjective sense of endowment is enough to shift our psychological reference point, causing us to view an item as ours to lose 341014.

This sense of psychological ownership can be triggered by incredibly subtle environmental and cognitive cues: * Touch and Physical Proximity: Merely picking up an item in a retail store, holding a piece of clothing, or even tapping a picture of a meal on an interactive iPad menu significantly increases our perceived ownership and our subsequent willingness to pay for it 415. * Imagination and Roleplay: Asking consumers to simply imagine themselves using a product (e.g., "picture yourself driving this car on your daily commute") activates the same cognitive biases as actual ownership. Studies show that auction participants who are instructed to imagine themselves as the current high bidder will bid far more aggressively to defend "their" item against competing bids 615. * Duration of Possession: The longer we hold onto an object, the more deeply it integrates into our self-concept. The endowment effect reliably grows stronger over time as psychological accustoming and adaptation set in 1015.

Cognitive Biases and Status Quo Inertia

Another layer of the traditional explanation involves "status quo bias" and the concept of psychological inertia. Humans require a significant amount of mental effort and energy to change their current state. When faced with a transaction, there is often a range of prices that leaves both buyers and sellers feeling ambivalent. Because changing the status quo requires accumulating mental evidence and overcoming cognitive friction, both parties tend to default to doing nothing out of sheer inertia, creating market stagnation 1816.

Memory also plays a vital role in reinforcing the endowment effect. We generally have a much more robust and accessible memory for goods we own than for goods we do not. Because most objects have more positive features than negative ones, this accessibility bias means owners seamlessly recall more positive attributes about their possessions during a negotiation, resulting in a naturally higher evaluation compared to a buyer who lacks that self-referential memory 1.

The Modern Pushback: Is It Really About Loss?

For decades, the inextricable link between the endowment effect and loss aversion was treated as scientific gospel. It became a somewhat circular pillar of behavioral economics: loss aversion was routinely used to explain the endowment effect, and the endowment effect was simultaneously cited as the primary empirical proof of loss aversion 17.

However, as behavioral science has advanced - and weathered the intense methodological scrutiny of the ongoing "replication crisis" in psychology - researchers have begun to pull these two concepts apart. To contextualize this shift, it is important to note the scale of the replication crisis. Recent large-scale efforts, such as the SCORE project published in 2026, found that only about 55% of published social science findings hold up when subjected to careful replication attempts 1820. Furthermore, a 2021 study from UC San Diego revealed a troubling dynamic: papers in leading psychology and science journals that fail to replicate are actually cited at a significantly higher rate - often 153 times more frequently - than those that successfully replicate, simply because their counterintuitive claims make for better narratives 19.

Against this backdrop of intense skepticism, the endowment effect has actually fared quite well. Modern replication studies consistently confirm that the behavioral outcome of the endowment effect (the WTA-WTP gap) is incredibly robust and real across diverse settings 220. However, the psychological mechanism driving it is now highly contested.

Several prominent researchers argue that the endowment effect is not driven by an irrational fear of loss, but rather by rational market strategies, cognitive attention mechanics, and a deep-seated human aversion to getting ripped off.

Reference Price Theory and "Bad Deal Aversion"

One of the most compelling challenges to the loss aversion narrative comes from "Reference Price Theory," frequently referred to as bad deal aversion. In a seminal 2012 paper, researchers Ray Weaver and Shane Frederick argued that the endowment effect occurs simply because buyers and sellers rely on entirely different reference points when evaluating a trade 314.

When you approach a transaction, you do not evaluate the item in a cognitive vacuum; you evaluate it against your understanding of the broader market. A seller looks at an item and thinks, "What is the maximum I can get for this without looking foolish?" A buyer looks at the item and thinks, "What is the absolute minimum I can pay for this to secure a bargain?" 14.

If you are handed a promotional mug that you know retails for $5, its market value is firmly anchored in your mind at $5. If someone offers you $2.50 for it, you will reject the offer - not because you are emotionally attached to the mug, and not because you are paralyzed by the profound pain of losing it, but simply because selling a known $5 item for $2.50 is an objectively bad deal 3. Conversely, a buyer is fully aware they do not strictly need the mug, so they will only open their wallet if the price represents a significant discount.

In this light, a meta-analysis from 2021 argues that the endowment effect reflects "adaptively rational" behavior. Both parties are acting logically based on their differing market goals: sellers are attempting to match the objective market rate based on the item's perceived quality, while buyers are aggressively hunting for a discount 14.

The "Pay-To-Keep" Discrepancy

Further cracks in the traditional loss aversion theory were exposed by a clever 2021 study conducted by Smitizsky, Liu, and Gneezy. They designed an experiment to isolate exactly why sellers systematically set high prices, seeking to separate loss aversion from mere market posturing 72122.

The researchers introduced a critical third metric to the classic experimental design: Pay-to-Keep (PTK). Participants were divided into three conditions: 1. Buyers (WTP): Participants were asked, "How much will you pay to acquire this pen?" 2. Sellers (WTA): Participants were given the pen and asked, "How much will you accept to sell this pen?" 3. Keepers (PTK): Participants were given the pen, told they were about to lose it, and asked, "How much will you pay out of pocket to keep this pen?"

If loss aversion were the true underlying driver of the endowment effect, the "Keepers" should have been willing to pay a distinctly high price to avoid the painful psychological loss of their newly endowed pen. However, the empirical results showed that the Pay-to-Keep valuations were almost identical to the normal Willingness to Pay valuations. The participants did not actually care about losing the pen 72122.

The famous WTP-WTA gap only appeared when participants were put in a strict selling posture. The researchers concluded that the endowment effect is primarily a "buy-sell discrepancy" - an automatic overgeneralization of high-pricing strategies that make strategic sense for sellers in real-world markets, but which manifest as apparent bias in a controlled laboratory setting 72122. We do not overprice our used items because we cry at the thought of losing them; we overprice them because we have been culturally and economically trained to ask for high prices when negotiating.

Cognitive Attention and Eye Tracking

In 2023, research utilizing advanced neuroeconomics and eye-tracking technology added a physiological layer to the debate. A collaborative study led by Michael Platt at the University of Pennsylvania tracked the pupil dilation and precise gaze allocation of buyers and sellers during active negotiations 1623.

Platt's team found that human deal-making relies on a dynamic evidence-accumulation framework in the brain. The endowment effect manifests physically as an asymmetrical allocation of visual and cognitive attention. In trading situations, human vigilance systems naturally evolved to scan for threats, meaning sellers tend to fixate on the item they might lose. However, Platt found that a deal is successfully struck only when both the buyer and the seller shift their gaze to focus on potential gains, accompanied by synchronized pupil dilation (a recognized physiological marker of arousal, mental effort, and the release of norepinephrine/adrenaline) 1623.

This physiological data suggests that the endowment effect is not an unchangeable emotional state or a permanent cognitive flaw, but rather a momentary cognitive bottleneck that can be overcome by forcefully redirecting a person's attention away from market threats and toward mutual gains.

Summary of Competing Theories

To understand the current state of behavioral economics, it is helpful to compare how different camps interpret the exact same phenomenon.

| Theoretical Model | Core Argument | Key Proponents & Evidence Base |

|---|---|---|

| Loss Aversion | The psychological pain of losing an object heavily outweighs the joy of acquiring it. Sellers naturally demand a premium to offset this emotional pain. | Kahneman, Tversky, Thaler (Classic Prospect Theory formulations) 11012. |

| Psychological Ownership | The mere cognitive association between an item and a person's "self-concept" instantly raises its perceived value, regardless of market conditions. | Morewedge, Giblin, Dommer (Evidence from the Mere Ownership Paradigm) 341014. |

| Reference Price / Bad Deal Aversion | Sellers anchor to retail market prices; buyers hunt for deep discounts. The resulting price gap reflects rational market posturing, not emotional bias. | Weaver, Frederick, Isoni (2011, 2012 retail price anchoring studies) 314. |

| Buy-Sell Strategy Discrepancy | Humans blindly apply aggressive negotiation strategies when placed in the role of a "seller," regardless of the item's true utility or their attachment to it. | Smitizsky, Liu, Gneezy (2021 Pay-to-Keep experimental data) 72122. |

Is the Endowment Effect Universal? Cross-Cultural and Evolutionary Evidence

For a long time, the endowment effect was assumed to be an innate, hardwired human trait - perhaps an evolutionary hangover from our deep ancestral past. Evolutionary psychologists posited that in primitive environments where resources were scarce, natural selection favored individuals who jealously guarded their possessions, leading to a biological instinct to overvalue what is already ours 424.

However, this assumption suffered from a common, critical flaw in psychological research: almost all of the early experiments were conducted on "WEIRD" populations - people from Western, Educated, Industrialized, Rich, and Democratic societies (mostly American college students) 925. When researchers finally stepped out of the laboratory and began testing the endowment effect across fundamentally different cultures and economic systems, the theory of biological universality quickly fell apart.

The Hadza Hunter-Gatherer Study

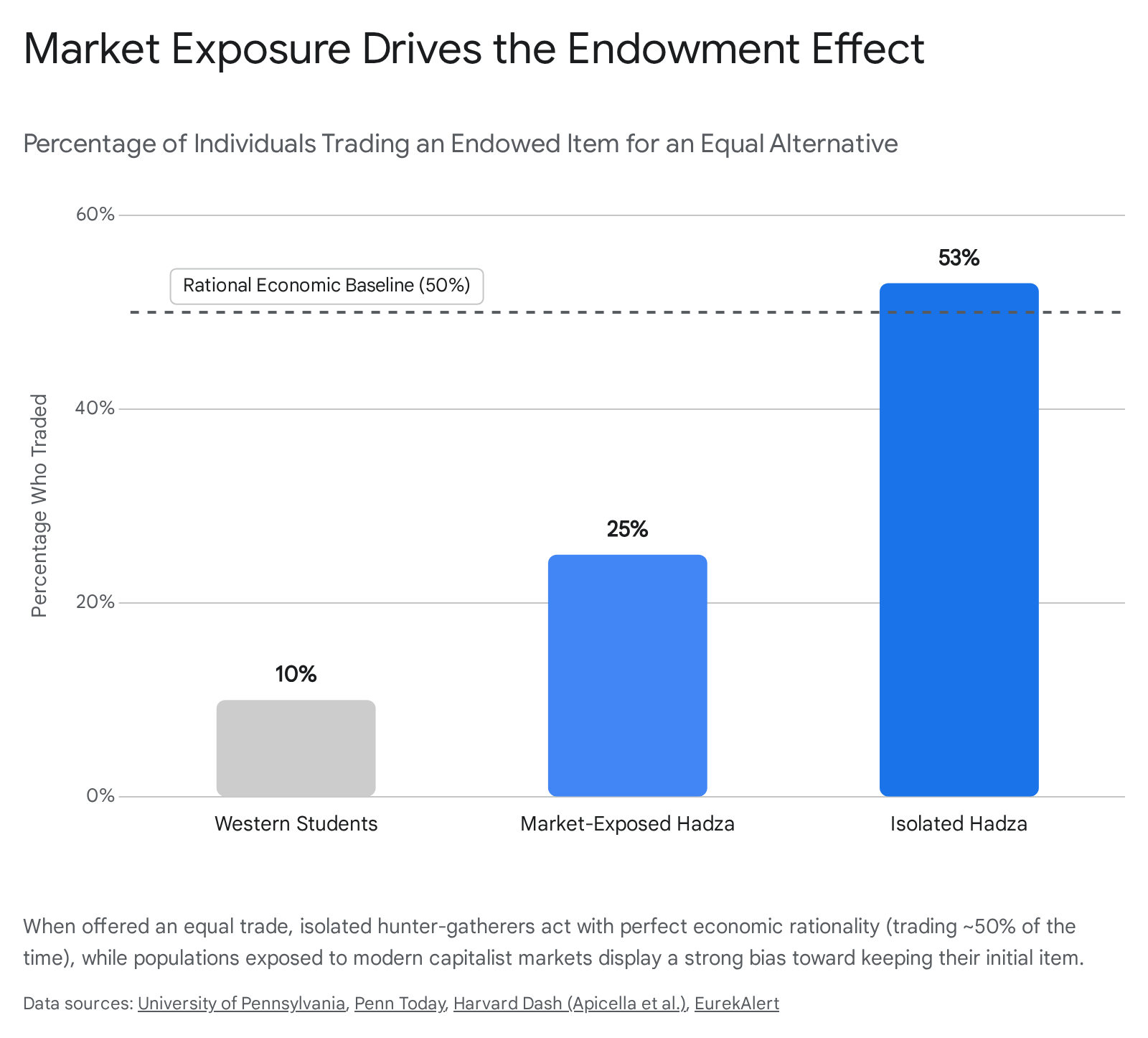

One of the most consequential studies on the endowment effect was published in 2014 by Coren Apicella, Eduardo Azevedo, Nicholas Christakis, and James Fowler. To explicitly test the evolutionary argument, they traveled to Northern Tanzania to study the Hadza Bushmen, one of the last remaining hunter-gatherer societies on Earth 9252627.

The Hadza live in small, nomadic camps and practice high degrees of egalitarianism, communally sharing almost all food and possessions. Crucially, a large geographical feature - a lake - separates different Hadza camps, creating a perfect natural experiment. The camps on the near side of the lake have frequent interactions with modern tourists and capitalistic markets. The camps on the far side of the lake remain highly isolated from modern commerce and property norms 9252728.

The researchers conducted classic exchange paradigm experiments, giving participants either a package of cookies or a lighter, and then offering them the chance to trade for a different flavor or color. Because the initial items were randomized, standard rational choice dictates that participants should prefer the alternative item about 50% of the time. In Western societies, due to the heavy influence of the endowment effect, people generally only trade about 10% of the time 92529.

The results among the Hadza were revelatory: * The Market-Exposed Hadza: Traded roughly 25% of the time. They exhibited a clear, if slightly muted, endowment effect. * The Isolated Hadza: Traded 53% of the time. They exhibited zero endowment effect, behaving with perfect economic rationality 9262730.

The Hadza study strongly implies that the endowment effect is not hardwired biology, but rather a learned behavior.

It appears to be an artifact of interacting within capitalistic, market-based societies where individual property rights and aggressive trading strategies are necessary for survival 930.

East vs. West: The Role of the Self-Concept

Cultural differences in the endowment effect are not just found in remote hunter-gatherer populations; they exist profoundly among modernized, industrialized nations. A wealth of research compares Western, individualistic cultures (such as the United States and the United Kingdom) with East Asian, collectivistic cultures (such as Japan and Taiwan) 38303132.

In highly individualistic societies, people are socially conditioned from a young age toward "self-enhancement" - the practice of associating themselves with objects, brands, and property to boost their self-esteem, broadcast their identity, and signal status. When a Westerner acquires an object, that object quickly becomes an extension of their ego, triggering a strong, immediate endowment effect 383032.

In collectivistic cultures, which place a much higher emphasis on interdependence, social harmony, and self-criticism over self-enhancement, the psychological link between personal possessions and self-worth is significantly weaker. Consequently, multiple cross-cultural studies have found that East Asian participants exhibit a much smaller - and sometimes entirely absent - endowment effect compared to their Western counterparts 30313233. Furthermore, cognitive studies tracking "self-referential memory processing" show that Westerners remember items they own far better than items they do not, whereas East Asian participants do not display this memory bias, reinforcing the cultural divide in how ownership is internalized 31.

The Kanak Gift Economy

Perhaps the most radical departure from the Western endowment effect is found among the Kanak, an Indigenous Melanesian population located primarily in New Caledonia. When behavioral researchers attempted to run the standard Exchange Paradigm with Kanak participants, they discovered that the very conceptual framework of the experiment violated local social norms 34.

In standard Western experiments, participants view the endowed item (such as the coffee mug) as a finalized gift from the experimenter. In Western politeness norms, to immediately turn around and trade away a newly received gift is considered socially rude, which artificially inflates the refusal to trade. However, in Kanak culture, a gift is viewed entirely differently: it is the initiation of an ongoing social exchange based on strict reciprocity (the continuous cycle of gift and counter-gift). When the experiment is conducted entirely within the Kanak vernacular and customary context, honoring their social structures, the endowment effect vanishes completely, and participants trade freely, viewing the exchange not as a loss, but as the natural continuation of a social relationship 34.

How Marketers Weaponize the Endowment Effect

While academic economists debate the precise neurological and cultural underpinnings of the endowment effect, the global business world has long recognized its immense behavioral power. Marketers, salespeople, and tech designers routinely exploit this bias to increase sales conversions, reduce churn, and justify higher price points 153735.

By artificially engineering a sense of psychological ownership before a transaction is finalized, companies can effortlessly shift a consumer's mindset from the objective question of "Should I buy this?" to the highly emotional question of "Am I willing to lose this?"

30-Day Free Trials and the "Puppy Dog Close"

The most ubiquitous and profitable application of the endowment effect in the modern digital age is the free trial. Companies spanning from massive streaming services like Netflix and Spotify to enterprise software providers like Adobe and Salesforce offer 30-day, risk-free access to their premium platforms 415373637.

In traditional sales parlance, this tactic is known as the "puppy dog close" - if a pet store lets you take a puppy home for the weekend, you will almost never bring it back. The exact same psychological principle applies to software. When a consumer uses a digital product for 30 days, they integrate it into their daily routine. They upload their personal data, customize their dashboard settings, and develop a profound sense of digital ownership. When the trial ultimately expires, the prospect of downgrading to a free tier or losing access entirely is no longer framed as saving a monthly fee; it is framed in the brain as a painful loss of their optimized workflow 415373738.

This strategy is highly effective because recent behavioral research demonstrates that the endowment effect actively amplifies over time. A 2023 study published by Cambridge University Press found that as transactions are delayed into the future and users spend more time with an item, their baseline willingness to pay actually decreases, but their willingness to accept (their selling price) remains stubbornly flat or increases, causing the endowment gap to widen and locking them further into the ecosystem 13.

SaaS (Software as a Service) companies amplify this effect by utilizing targeted "loss framing" in their communication. Instead of sending an optimistic email that says, "Upgrade now to get premium features," an optimized, psychologically weaponized marketing campaign will say, "Don't lose your custom analytics dashboard - upgrade to keep your data safe" 38.

Money-Back Guarantees and Experiential Retail

Retailers use the exact same psychological levers in the physical world to drive conversions and limit returns. * The Test Drive and Tactile Engagement: Allowing a customer to test-drive a vehicle, or Apple's famous store policy of encouraging customers to linger and physically play with devices, fosters a rapid sense of psychological ownership. Studies confirm that simply touching an item significantly increases the probability of a purchase 153736. * Money-Back Guarantees: Offering a 100% money-back guarantee serves two distinct purposes. First, it lowers the initial barrier to entry by removing financial risk. Second, it relies heavily on the endowment effect: once the product is physically in the customer's home, they will begin to value it more than the money they paid for it, making them highly unlikely to go through the effort of returning it 611. * Home Try-On Programs: Disruptive brands like Warby Parker ship multiple pairs of glasses directly to a consumer's home for free. Having the physical items in your personal possession drastically increases the likelihood of a purchase compared to simply browsing identical frames in a traditional retail store 1536.

The Valuation of Useless Information

Interestingly, the endowment effect is not strictly limited to physical commodities, financial instruments, or useful software; it also applies to entirely abstract information. A robust 2022 study by Litovsky and Loewenstein (successfully replicated in 2024 by Clearer Thinking) found that people exhibit the endowment effect even for noninstrumental information - trivial facts that serve absolutely no practical purpose or utility 124239.

When experiment participants were randomly "endowed" with a bundle of useless facts, they placed a significantly higher value on keeping those specific facts than they did on acquiring a different set of alternative facts. This phenomenon highlights exactly why people often fiercely resist letting go of their established beliefs or hoarding old, irrelevant data in the digital age, even when that information is demonstrably no longer serving them 124239.

The Endowment Effect in High-Stakes Markets

While hoarding cheap coffee mugs, accumulating useless trivia, or holding onto a forgotten Spotify subscription are relatively minor financial leaks, the endowment effect can cause massive friction, delayed transactions, and severe economic inefficiency in high-stakes markets.

The Housing Market: The Seller's Trap

The residential real estate market is a textbook environment for the endowment effect to wreak havoc. Homeowners spend years pouring time, money, and intense emotional energy into their properties. They paint walls, upgrade patios, and build personal memories. When it comes time to sell, the owners view the house primarily through the lens of psychological ownership and loss aversion, leading them to severely inflate the asking price well beyond what the objective data supports 44440.

Buyers, however, do not care about the seller's memories or the weekend they spent installing a custom backsplash. They evaluate the house coldly, comparing it strictly against alternative properties currently on the market 40. This resulting WTA-WTP gap causes immense market friction, resulting in homes sitting unsold for months until the seller is finally forced to accept humiliating price cuts that destroy their initial negotiating leverage 40.

Interestingly, researchers have found that structured behavioral interventions can successfully mitigate this bias. A 2024 lab-in-the-field experiment simulating the Polish housing market measured the initial WTA-WTP gap at a staggering 7.01%. Researchers then introduced an intervention: forcing sellers to engage with highlighted, graphically visualized data about objective market prices for comparable properties in their area. Following this data visualization, the endowment gap shrank significantly to just 2.48%, proving that confronting owners with hard data can break the spell of psychological ownership 4142.

The Used Car Bubble and Negative Equity

The global used car market in the mid-2020s has been uniquely and severely distorted by the endowment effect. During the acute supply chain shortages of 2021 and 2022, used car prices skyrocketed by roughly 40%, with many standard vehicles actually appreciating in value - a historical anomaly 48.

By 2025 and 2026, the auto market normalized, but consumer psychology severely lagged behind. Sellers and trade-in customers remained stubbornly anchored to the inflated prices of the pandemic era. Because they feel they "own" an asset that was recently worth a premium, they suffer from acute bad-deal aversion and refuse to accept current, significantly lower market valuations for their trade-ins 434445.

This psychological stubbornness, combined with record-long auto loan terms (which now average between 68 and 72 months), has trapped millions of consumers in a cycle of negative equity 484546. Buyers owe more on their cars than the vehicles are currently worth in the market, yet the endowment effect blinds them to the sunk costs, preventing them from downsizing or making rational financial transitions to more affordable transportation 4845. Delinquency rates on auto loans have subsequently reached their highest levels in over a decade as a direct result of this market-wide psychological friction 45.

Practical Strategies to Overcome the Endowment Effect

Because the endowment effect operates largely below our conscious awareness, overcoming it requires deliberate, structured interventions. Whether you are trying to declutter your home, sell a high-value asset, or avoid falling into a digital marketing trap, you can employ several proven strategies to neutralize the bias 354440.

1. Rely on Objective, Third-Party Valuation When pricing a house, a car, or an antique, do not rely on your gut feeling. The human brain is simply incapable of separating sentimental value from objective market value. Seek out a professional third-party appraisal, strictly review comparable market data (comps), or ask a neutral friend to price the item. Relying on hard data shifts your cognitive attention away from "what I am losing" and anchors it firmly to realistic market conditions 33540.

2. Use an Agent to Buffer the Transaction Economic research shows that the endowment effect nearly disappears when transactions are handled by a proxy or an agent 44. Because a real estate agent or a financial broker has absolutely no psychological ownership over your property, they do not suffer from loss aversion. Allowing an agent to handle the pricing strategy and negotiations removes your ego from the equation, leading to faster, more efficient market clearing.

3. Depersonalize and Neutralize the Asset If you are selling a home, you must purposefully transition it from a "personal environment" to a "market-ready product." Bold paint choices, custom collections, and family photos immediately trigger your own endowment effect and simultaneously distract potential buyers. Neutralizing and staging the space forces your brain to detach from the property, making it significantly easier to accept fair market offers without feeling a sense of personal rejection 40.

4. Reframe the Transaction (Focus on Opportunity Costs) If you are struggling to declutter your home or cancel a persistent software subscription, change your psychological reference point. Instead of focusing on what you are giving up (e.g., "I am losing my extensive figurine collection"), force yourself to focus explicitly on the opportunity cost (e.g., "If I sell this, I gain physical space, save hours of time dusting, and have $500 cash to spend on a vacation") 335. By shifting your visual and cognitive attention to the gains, you fulfill the exact physiological requirement for deal-making identified in modern eye-tracking studies 1623.

5. Apply the "Repurchase Test" When agonizing over whether to keep or sell an item, ask yourself a simple, clarifying question: "If I didn't already own this item, how much would I be willing to pay out of my own pocket to buy it today?" If the cash amount you would pay to acquire the item is significantly less than the amount you are currently demanding to sell it, you are actively under the influence of the endowment effect. Sell the item 3.

Bottom line

The endowment effect is a pervasive cognitive bias that compels us to systematically overvalue the things we own simply because we own them. While classical behavioral economics attributed this phenomenon entirely to an irrational, hardwired fear of loss, modern cross-cultural research and replication studies reveal a much more complex reality: the effect is heavily influenced by cultural conditioning, strategic negotiation habits, and our intense aversion to feeling like we have been given a bad deal in a capitalist market. By recognizing that this bias is largely a learned market reflex rather than an unchangeable human instinct, we can use objective data, third-party agents, and deliberate perspective shifts to detach our emotions from our possessions and make significantly smarter financial decisions.