EGC status, compensation disclosure, and post-IPO governance

Legislative Context and the Expansion of Scaled Disclosure

The regulatory architecture governing initial public offerings (IPOs) and early-stage public companies in the United States underwent a profound structural transformation with the enactment of the Jumpstart Our Business Startups (JOBS) Act of 2012. The legislation was fundamentally designed to stimulate domestic capital formation and reverse a prolonged, systemic decline in public listings. Macroeconomic data indicates that the number of public companies listed on U.S. exchanges peaked at 7,522 in 1997, driven heavily by the technology bubble, before entering a sustained contraction that saw listings bottom out at 3,602 in 2017 1. To mitigate the regulatory deterrents that were purportedly suppressing public market entry, the JOBS Act established the "Emerging Growth Company" (EGC) classification.

An issuer qualifies for EGC status if it reports total annual gross revenues of less than $1.235 billion during its most recently completed fiscal year, provided it has not issued more than $1 billion in non-convertible debt over the prior three-year period 23. The classification affords newly public entities a transitional "on-ramp" of up to five fiscal years, during which they are exempt from several stringent reporting, governance, and compliance mandates that traditionally apply to standard public companies 2. The classification has been immensely popular; historical market analyses indicate that since the passage of the Act, roughly 90% of eligible IPOs have elected to utilize the EGC designation to minimize initial compliance friction 4.

The regulatory philosophy underpinning the EGC classification is currently undergoing a significant evolution. Recognizing the continuing necessity to incentivize companies to remain in the public markets, the Securities and Exchange Commission (SEC) introduced sweeping proposed reforms in May 2026. Proposed Release No. 33-11419, "Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies," seeks to consolidate the current five-tier filer status framework into primarily two categories: Large Accelerated Filers (LAFs) and Non-Accelerated Filers (NAFs) 4578.

Crucially, the 2026 SEC proposal would increase the public float threshold for LAF status from $700 million to $2 billion, while simultaneously introducing a rigorous 60-month "seasoning" requirement 467. Under this proposed framework, a company would not qualify as an LAF until it has been subject to Exchange Act reporting requirements for at least 60 consecutive calendar months (five years), regardless of its market capitalization reaching the threshold earlier 86. This effectively institutionalizes the five-year IPO on-ramp across approximately 80.8% of the public market, allowing a vast majority of issuers to benefit from scaled disclosures and delayed compliance mandates - such as the costly auditor attestation requirements over internal controls under Section 404(b) of the Sarbanes-Oxley (SOX) Act 467.

| Regulatory Parameter | Current Framework (Pre-2026 Reforms) | Proposed 2026 Framework (Release 33-11419) |

|---|---|---|

| Large Accelerated Filer (LAF) Threshold | $700 million public float | $2 billion public float |

| Seasoning Requirement for LAF Status | 12 calendar months of reporting | 60 consecutive calendar months of reporting |

| Primary Filer Classifications | Five tiers (LAF, Accelerated, Non-Accelerated, SRC, EGC) | Two primary tiers (LAF and NAF), plus Small NAF (SNF) |

| SOX 404(b) Attestation Exemption | Limited to EGCs (max 5 years) and SRCs | Extended to all NAFs (including those in the 60-month on-ramp) |

| Estimated Proportion of Market as LAFs | 35.4% | 19.2% |

Effects of Scaled Disclosure on Financial Reporting Quality

The de-burdening provisions of the EGC classification allow issuers to scale back financial accounting disclosures significantly. EGCs are required to provide only two years of audited financial statements in their IPO registration statements, down from the standard three years required for non-EGCs, and are permitted to adopt new or revised Generally Accepted Accounting Principles (GAAP) using delayed private company effective dates 38. Furthermore, the exemption from SOX 404(b) auditor attestations on internal controls over financial reporting introduces a substantial variable into the post-IPO information environment.

Empirical evidence suggests that these scaled disclosures correspond with a measurable deterioration in financial reporting quality. Analysis indicates that among active EGC filers providing a management report on internal controls, approximately 46% reported material weaknesses; even among exchange-listed EGCs, the rate of material weaknesses was 12%, which remains double the rate observed in non-EGC exchange-listed filers 12. This lack of external auditor attestation has prompted broader concerns regarding offering quality and the accuracy of forward-looking financial statements. Furthermore, academic literature demonstrates that EGCs exhibit lower value relevance of accounting information and generally lower financial performance relative to their non-EGC peers 13.

In response to the increased information uncertainty generated by the JOBS Act, regulatory oversight mechanisms have naturally adjusted. The SEC conducts significantly more extensive reviews of EGC registration statements to afford adequate protection to retail and institutional investors. Studies demonstrate an increased risk of earnings management following the JOBS Act, prompting the SEC to heavily scrutinize broader accounting frameworks within S-1 filings, including non-core accounting data, to detect and mitigate potential misleading disclosures 9. Consequently, while EGCs save on direct external audit fees, they frequently face intensified regulatory friction during the SEC comment letter process.

Executive Compensation Transparency under Emerging Growth Company Status

The most acute informational asymmetry permitted by the EGC framework lies in the domain of executive compensation. The tension between limiting corporate compliance expenditures and satisfying investor demand for principal-agent alignment data is starkly resolved in favor of the issuer during the EGC transition period.

Reductions in Mandated Proxy Disclosures

Under the rigorous standard requirements of SEC Regulation S-K Item 402, mature public companies are legally obligated to provide exhaustive, granular disclosures detailing the compensation of their Named Executive Officers (NEOs). For a standard issuer, the NEO group comprises the Principal Executive Officer (PEO), the Principal Financial Officer (PFO), and the three next most highly compensated executive officers, totaling five individuals 41510. This disclosure must encompass three full fiscal years of compensation history to establish trendlines in pay practices.

Conversely, EGCs operate under a highly truncated reporting mandate. They are required to disclose compensation information for only three NEOs (the PEO and the two next most highly compensated executive officers, omitting the mandatory inclusion of the PFO) and are only obligated to provide two years of historical data 815. Furthermore, EGCs are entirely exempt from drafting a Compensation Discussion and Analysis (CD&A). For standard filers, the CD&A is the critical narrative centerpiece of the proxy statement, intended to explain the material elements of compensation, the underlying strategic objectives of the remuneration programs, the precise formulas and metrics used to determine performance-based payouts, and the justification for specific allocations between cash and equity vehicles 171119.

By omitting the CD&A, EGCs legally shield their internal compensation philosophies, peer-group benchmarking methodologies, and specific performance hurdle rates from public market scrutiny. While this exemption drastically reduces the legal, consulting, and administrative costs associated with producing complex annual proxy materials, it creates an environment of profound opacity. Institutional investors evaluating EGCs must rely exclusively on the limited quantitative data presented in the Summary Compensation Table (SCT). Without the qualitative context of the CD&A, it becomes exceedingly difficult for shareholders to ascertain whether equity grants and cash bonuses are genuinely tethered to rigorous performance milestones or merely function as guaranteed wealth transfers to founders and early executives.

| Disclosure Component | Emerging Growth Company (EGC) Requirement | Standard Public Company Requirement |

|---|---|---|

| Named Executive Officers (NEOs) Disclosed | 3 (including the PEO) | 5 (including PEO, PFO, and top 3 others) |

| Historical Data Window | 2 fiscal years | 3 fiscal years |

| Compensation Discussion & Analysis (CD&A) | Completely Exempt | Required comprehensive narrative |

| Pension Value Changes in Total Pay | Exempt | Required inclusion in Summary Compensation Table |

| CEO Pay Ratio | Exempt | Required (ratio of CEO pay to median employee) |

| Shareholder Advisory Votes (Say-on-Pay) | Exempt | Required (frequency voted by shareholders) |

| Pay-Versus-Performance (Item 402(v)) | Exempt | Required tabular and narrative alignment disclosure |

Exemption from the Pay-Versus-Performance Framework

The informational deficit surrounding EGC compensation widened considerably following the SEC's adoption of the Pay-Versus-Performance (PvP) rules, which took effect for fiscal years ending on or after December 16, 2022. Mandated originally by Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act, the creation of Item 402(v) of Regulation S-K forces registrants to clearly disclose the relationship between executive compensation actually paid and the definitive financial performance of the registrant over a five-year period 201213.

For standard filers, the PvP rule demands a highly structured tabular disclosure. The table must display the total compensation reported in the SCT alongside a newly calculated metric: "compensation actually paid." This adjusted figure recalculates equity award valuations based on year-end fair values and accounts for changes in pension benefits, providing a more accurate reflection of the executive's realized or realizable wealth during the fiscal year 1314. This compensation data must then be juxtaposed against Total Shareholder Return (TSR), peer group TSR, net income, and a specific, company-selected financial performance measure 131424. Registrants must also provide a clear narrative or graphical description of the relationships between these financial performance measures and the compensation actually paid 12. Because this data must be tagged in Inline XBRL, it allows quantitative analysts and institutional investors to systematically parse and correlate executive wealth accumulation with actual shareholder value creation across the broader market 12.

EGCs, however, are explicitly exempt from the entirety of the PvP disclosure requirements, just as they are exempt from reporting the CEO pay ratio 4201214. This exemption grants early-stage growth companies the latitude to issue highly aggressive, equity-heavy compensation packages - which are often highly dilutive to new public shareholders - without having to provide a standardized, multi-year mathematical reconciliation of how the value of those equity grants performs relative to the company's actual stock performance or net income.

The Transition Cliff: Exiting Emerging Growth Company Status

The strategic advantages of scaled disclosure are inherently temporary. An EGC loses its favored status on the last day of the fiscal year following the fifth anniversary of its IPO. The status may terminate even sooner if the company exceeds the $1.235 billion annual revenue threshold, issues more than $1 billion in non-convertible debt over a three-year span, or qualifies as a large accelerated filer under current rules 22515. For the unprecedented wave of companies that went public during the IPO boom of 2020 - a year that saw 480 IPOs, heavily populated by life sciences and technology firms - the EGC sunset date is firmly set for December 31, 2025 15.

Operational and Compliance Burdens at Transition

The transition from EGC to standard filer status creates a severe "disclosure cliff" that requires substantial advance planning, capital investment, and structural reorganization. Companies must rapidly scale their financial reporting infrastructure to complete the SOX 404(b) auditor attestation, a process that frequently uncovers control weaknesses that were previously unmonitored 15. Simultaneously, the proxy statement must be dramatically expanded to include the full CD&A, a five-person NEO roster covering three years of historical data, the CEO pay ratio, and the complex PvP tables 1515. Furthermore, former EGCs must hold their initial Say-on-Pay and Say-on-Frequency shareholder advisory votes no later than one year after losing their EGC status, thrusting their compensation practices into the public voting arena for the first time 1725.

Proxy Advisor Scrutiny Post-Transition

This sudden transition exposes the maturing company to rigorous, quantitative evaluation by major proxy advisory firms, most notably Institutional Shareholder Services (ISS) and Glass Lewis. These institutions wield immense influence over institutional voting blocks and utilize proprietary, algorithmic models to assess pay-for-performance alignment and overall governance health.

When a former EGC publishes its first full CD&A, proxy advisors evaluate the historical compensation practices that were previously obscured. Glass Lewis's 2024 and 2025 policy guidelines, for instance, emphasize a highly detailed, holistic analysis of executive compensation. The firm penalizes companies for opaque non-GAAP to GAAP reconciliations, warning that if significant adjustments materially impact incentive pay outcomes without transparent disclosure, it will negatively affect the company's Say-on-Pay recommendation 2728. Furthermore, Glass Lewis demands robust clawback provisions that provide the company with the ability to recoup incentive compensation in cases of material misconduct or operational failure, regardless of whether the executive was terminated with or without cause 2728.

Proxy advisors also closely monitor director bandwidth and overboarding. While historical investor skepticism surrounding directors serving on multiple public boards remains strong, recent data from the 2025 proxy season indicates a slight easing of resistance, with median support increasing marginally for non-executive directors serving on four or more public boards 2916. Nevertheless, the overarching trend is clear: companies that operated with relatively unchecked, founder-friendly compensation structures and insular board dynamics during their EGC phase frequently face severe backlash, low Say-on-Pay support, and negative director recommendations once their practices are subjected to standard market scrutiny 17.

Retention of Protective Post-IPO Governance Structures

The scaled disclosure environment afforded to EGCs does not exist in a regulatory vacuum; it operates as part of a broader ecosystem of post-IPO governance wherein early-stage public companies aggressively utilize structural mechanisms to insulate management and founders from the immediate pressures of public market accountability. While the JOBS Act relieves disclosure burdens, companies actively construct legal defenses to ensure operational control remains centralized.

Durability of Classified Boards and Supermajority Voting

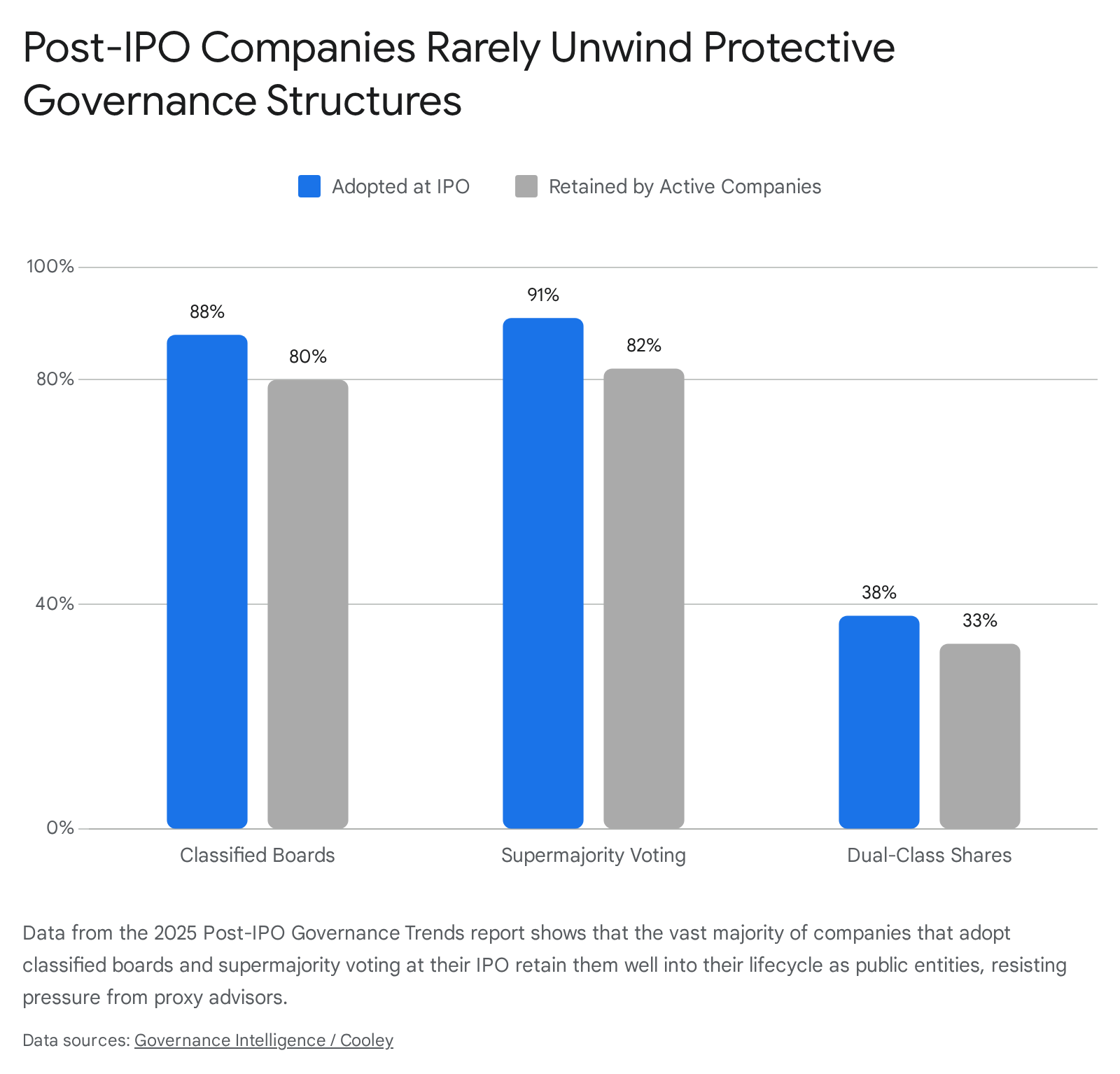

Empirical research analyzing post-IPO governance trends reveals a striking persistence of protective board structures that intentionally limit shareholder influence. According to Cooley's 2025 Post-IPO Governance Trends report, an overwhelming 88% of companies adopt classified (staggered) boards immediately following their IPO, and crucially, 80% of those that remain publicly listed hold onto this structure well into their maturation phase 17. Similarly, 91% of surveyed companies adopt supermajority voting requirements at the time of their IPO, with 82% retaining them as active public companies 17.

These structural mechanisms are primarily designed to defend against hostile takeovers and activist shareholder interventions. A classified board, wherein only a fraction of directors (typically one-third) are up for election in any given year, ensures that an insurgent or activist investor cannot gain control of the board in a single proxy season, thereby entrenching incumbent management 18. Proxy advisory firms and institutional investors generally oppose these mechanisms; empirical studies frequently link staggered boards to reductions in firm valuation and diminished accountability to shareholder interests 291833. EGC status acts as an initial shield against this investor pressure, but as the company matures, the stubborn retention of classified boards frequently results in substantial shareholder dissent. Recent data indicates that 40% of active IPO companies have received at least one director vote below 80% support, and almost all active IPO companies have received at least one negative ISS recommendation for director nominees due to these persistent protective structures 17.

Dual-Class Share Structures and the Unicorn Market

The proliferation of dual-class share structures represents perhaps the most contentious governance trend among late-stage EGCs. In a standard dual-class system, founders and early insiders hold a specific class of stock endowed with superior voting rights - often a 10:1 ratio compared to common public shares. This structural disparity allows founders to retain absolute voting control over the corporation despite holding a minority of the actual economic equity 1734. In recent years, data indicates that 38% of active IPO companies maintained multi-class structures, a figure that drastically eclipses the 8% prevalence observed in the broader, mature Russell 3000 index 17.

The widespread adoption of dual-class structures is inextricably linked to the rise of "unicorns" - privately held startup companies valued at over $1 billion. During periods of abundant private venture capital, founders gained unprecedented leverage. If stock exchanges or regulatory bodies strictly prohibited dual-class structures in public markets, founders holding the leverage of massive private valuations could simply opt to remain private indefinitely 3536. However, the private market inherently lacks the mandatory disclosure, SEC scrutiny, and rigorous financial analysis that defines the IPO process. From a macroeconomic governance perspective, prolonged private status for heavily capitalized unicorns can lead to catastrophic failures of internal oversight, a risk vividly exemplified by the highly publicized, multi-billion-dollar collapses of dominant-founder private firms such as WeWork, Theranos, and FTX 36.

Consequently, both venture capitalists and public market institutional investors have increasingly, albeit begrudgingly, acquiesced to dual-class IPOs. By conceding superior voting rights to the founder, venture capitalists incentivize the startup to enter the public market at an earlier stage in its lifecycle. The mandatory disclosure requirements inherent in the IPO process - even when scaled back under the EGC framework - serve to effectively filter out startups that lack viable, sustainable business models 3536. In this nuanced context, dual-class stock, while heavily criticized by proxy advisors like ISS as an agency cost that perpetually entrenches management, actually serves as a pragmatic, real-world solution to the "unicorn governance failure" problem. The market effectively trades post-IPO voting equality for the pre-IPO financial transparency and regulatory discipline required to prevent catastrophic, opaque private market collapses.

Implications for Cost of Equity, Underpricing, and Market Liquidity

The core legislative intent of the JOBS Act was to unequivocally lower the cost of capital for emerging companies. However, reducing mandatory financial and compensation disclosure theoretically increases information asymmetry between the issuing corporation and potential public investors. In efficient financial markets, increased valuation uncertainty generally leads investors to demand a higher risk premium, which manifests during an IPO as underpricing - the positive percentage difference between the initial public offer price set by underwriters and the closing price on the first day of open market trading.

The Underpricing Debate and Information Asymmetry

Initial empirical evaluations of the JOBS Act identified a highly concerning trend that directly contradicted the legislation's goals: EGCs appeared to suffer from significantly higher underpricing compared to non-EGCs, suggesting that the reduction in transparency actually increased their cost of equity capital. Studies by Barth et al. (2017) and Chaplinsky et al. (2017) observed a larger jump in the aftermarket price relative to the offer price specifically for EGC issuers 371939. Chaplinsky et al. concluded that EGCs opting for scaled disclosures experienced significantly higher indirect costs of issuance, and that this greater underpricing penalty was heavily concentrated among larger firms that were newly eligible for scaled disclosure under the Act 3920. Furthermore, concurrent research indicated that EGCs experienced higher post-IPO total and idiosyncratic volatility extending up to 30 days post-listing, corroborating the classical financial theory that reduced disclosure elevates ex ante uncertainty and aftermarket trading friction 821.

Re-evaluating Valuation Multiples and Macroeconomic Conditions

However, subsequent methodological advancements in financial econometrics have robustly challenged this prevailing narrative. Later research, notably the 2022 difference-in-differences (DID) analysis conducted by Even-Tov et al., argues compellingly that the observed increase in IPO underpricing among EGCs is a spurious correlation driven by contemporaneous macroeconomic shifts in overall IPO market conditions, rather than a punitive market reaction to the JOBS Act's disclosure relief itself 3719. By meticulously controlling for intertemporal changes using a control group of large issuers (those with pre-IPO revenues exceeding $1 billion), the DID analysis demonstrated that EGCs actually successfully raise capital at significantly higher pre-IPO valuation multiples 3719.

This empirical finding introduces a critical paradigm shift: institutional underwriters and early-stage investors are not aggressively discounting EGCs due to their scaled disclosures. On the contrary, EGCs that aggressively take advantage of accounting and compensation relief manage to raise capital at higher valuation multiples, despite objectively possessing more speculative financial profiles and being empirically more likely to destroy long-term shareholder value in the aftermarket. Data tracking long-term outcomes reveals that reduced-accounting EGCs are nearly 1.4 times more likely to underperform the broader market index over the three years following their IPO relative to non-reduced accounting EGCs 37.

The synthesized data suggests a complex transfer of risk: while EGCs undeniably benefit from higher initial valuations, lower immediate compliance burdens, and shielded executive compensation packages, the ultimate financial cost is heavily borne by long-term aftermarket retail and institutional investors. These subsequent investors suffer from the delayed realization of weak fundamental performance that was previously legally obscured by the scaled disclosure framework during the crucial pricing phase of the IPO.

International Divergence in Executive Remuneration Governance

The leniency of the U.S. EGC framework and the proposed 2026 expansion of NAF accommodations contrast sharply with the tightening regulatory regimes in other major global financial hubs. The profound divergence in executive compensation disclosure, transparency, and shareholder voting rights has evolved into a primary macroeconomic factor influencing cross-border capital flows, executive talent retention, and IPO venue selection.

The United Kingdom Framework and Capital Flight

In the United Kingdom, executive compensation - referred to as "remuneration" - is subject to perceptibly stronger shareholder rights and exhaustive disclosure requirements. Unlike the U.S. framework, where Say-on-Pay votes are strictly advisory and corporate boards face no legal compulsion to alter compensation practices following a negative shareholder vote, the U.K. employs a rigorous bifurcated voting system. Shareholders possess an advisory vote on the backward-looking implementation of pay (the annual remuneration report) and a highly potent, binding, forward-looking vote on the remuneration policy itself 2243. If the forward-looking policy is voted down by shareholders, the company is legally prohibited from implementing it.

This stringent regulatory environment, coupled with pervasive cultural norms that exhibit significantly greater public opprobrium toward high executive pay and stronger regional economic headwinds, has resulted in U.K. executives being compensated at levels vastly below their U.S. peers. A comparative analysis of the top ten U.K.-listed companies versus the top ten U.S.-listed companies in 2022 revealed a staggering disparity: the average U.K. CEO earned approximately $10.1 million, while the average U.S. CEO earned $106.6 million 44. While differing aggregate market capitalizations account for a portion of this variance, the combination of binding shareholder vetoes, cultural restraint, and rigid institutional investor guidelines (such as the U.K. Investment Association specifically advising companies to show "additional restraint" in base salary increases) fundamentally suppresses U.K. pay ceilings 4445.

Consequently, the U.K. has experienced a highly publicized wave of capital flight and listing venue shifts, with prominent London-listed companies increasingly exploring primary or dual listings in the United States. The U.S. public market, particularly bolstered by the EGC framework that explicitly shields newly public companies from immediate Say-on-Pay votes, CD&A disclosures, and PvP alignment scrutiny, presents an immensely attractive environment for executives seeking higher, equity-driven compensation without the friction of binding shareholder mandates 4344.

The European Union Pay Transparency Directive

The regulatory divergence is set to widen further as the European Union implements its sweeping Pay Transparency Directive, which mandates transcription into national legislation by all member states by June 7, 2026 2347. While the directive is primarily championed as a mechanism to eradicate gender pay gaps, its enforcement protocols have profound implications for executive compensation transparency across EU-domiciled growth companies.

The EU directive mandates that companies establish objective, strictly gender-neutral criteria for setting pay and career progression across all levels of the corporate hierarchy, from entry-level to the C-suite. Furthermore, it aggressively shifts the burden of proof to employers in equal pay disputes and requires companies exhibiting a gender pay gap above 5% to conduct mandatory joint pay assessments in conjunction with employee representatives 47. Unlike the U.S., where pay transparency has evolved organically through a fragmented patchwork of state and local laws, the EU directive imposes a unified, highly centralized, and strictly enforced regulatory framework 23.

For EU-based SMEs and emerging growth companies, this regulatory shift dictates that executive compensation differentials will become highly visible and contestable not just by institutional shareholders, but by the entire internal workforce. The strategic opacity permitted by the U.S. EGC classification is entirely antithetical to the EU's legislative trajectory, further cementing the U.S. capital markets' distinct positioning as a deregulatory haven for corporate issuers and executives prioritizing flexible governance and shielded compensation practices 47.

| Regulatory Jurisdiction | Post-IPO Executive Pay Transparency | Shareholder Voting Power on Compensation | Systemic Focus |

|---|---|---|---|

| United States (Non-EGC) | High (PvP, CD&A, CEO Pay Ratio required) | Advisory Only (Say-on-Pay) | Disclosure-based alignment |

| United States (EGC / NAF) | Low (Exempt from PvP, CD&A, Pay Ratio) | Exempt from mandatory voting during transition | Capital formation & burden reduction |

| United Kingdom | High (Detailed remuneration reporting) | Binding (Forward-looking policy vote) | Strict shareholder control & restraint |

| European Union (2026) | High (Mandatory criteria, joint assessments) | Advisory/Binding (varies by member state) | Internal parity & workforce visibility |

Conclusion

The Emerging Growth Company classification has profoundly and permanently reshaped the trajectory of early-stage public companies in the United States. By permitting heavily scaled financial reporting and significantly truncating executive compensation transparency, the EGC framework has successfully lowered the immediate administrative barriers to entry for accessing public capital. While initial academic consensus theorized that these opaque conditions artificially increased the cost of equity via severe IPO underpricing, recent robust econometric models indicate that EGCs are, in reality, highly successful at securing aggressive pre-IPO valuation multiples despite their lack of financial transparency.

However, the deliberate deferral of transparency inherently results in a systemic shift of risk. The scaled disclosure of executive compensation - specifically the legal omission of the CD&A, the exemption from Pay-Versus-Performance metrics, and the limitation of NEO visibility - allows for the rapid, unchecked accumulation of executive equity wealth without requiring an immediate, publicly auditable correlation to long-term shareholder value creation. When the protective EGC transitional period inevitably sunsets, companies face a severe disclosure cliff that triggers intense scrutiny from proxy advisory firms and institutional investors. This delayed exposure frequently results in highly contentious proxy battles regarding Say-on-Pay approvals and the stubborn retention of protective, management-entrenching governance structures like staggered boards and dual-class shares.

As global jurisdictions such as the European Union and the United Kingdom move aggressively toward binding shareholder votes, stringent internal pay parity assessments, and mandated pay transparency across all corporate levels, the U.S. capital markets are actively diverging. The SEC's 2026 proposed regulatory reforms seek to permanently embed EGC-like scaled disclosures for up to 80% of the public market via the expanded Non-Accelerated Filer status. This trajectory underscores a definitive, macroeconomic policy choice: the U.S. regulatory apparatus is prioritizing unfettered market access, maximum issuer flexibility, and the stimulation of IPO volume over granular, immediate governance transparency. For institutional and retail investors operating within this framework, this environment necessitates the development of significantly more sophisticated, independent due diligence mechanisms, as reliance on mandated regulatory disclosures in the formative years of a company's public life will intentionally yield an incomplete picture of corporate health and executive alignment.