What an S-1 Filing Reveals About a Company Going Public

An SEC Form S-1 is the foundational registration document required by the U.S. Securities and Exchange Commission for domestic companies seeking to issue public securities, serving as a comprehensive disclosure of a company's financial health, business model, and material risks 123. By legally compelling exhaustive transparency, the S-1 filing allows institutional and retail investors to perform rigorous due diligence before purchasing shares in an Initial Public Offering (IPO) 34.

For anyone who has ever purchased a house, the process of taking a company public is remarkably similar; an S-1 is the corporate equivalent of a mandatory, comprehensive home inspection report that reveals the structural integrity beneath a fresh coat of paint 5. From the curb, a privately held startup might look immaculate, boasting soaring user growth, visionary press releases, and multi-billion-dollar private valuations 45. However, just as a home inspection looks past the staging furniture to evaluate the foundation, the electrical wiring, and the plumbing, the S-1 filing forces the company to open its doors to independent auditors and federal regulators 45. It reveals the true state of the business: whether the unit economics are sustainable, whether corporate governance is sound, and whether regulatory or competitive threats threaten to collapse the business model 345. If a company intends to attract public capital, it must legally disclose every material flaw, allowing prospective buyers to decide whether to invest, demand a lower valuation, or walk away entirely 4.

FAQ: What Exactly is an SEC Form S-1?

The Form S-1, formally known as the Registration Statement under the Securities Act of 1933, is the regulatory gateway through which a private enterprise must pass to become a publicly traded corporation in the United States 12. Enacted in the aftermath of the 1929 stock market crash, the Securities Act of 1933 was designed to ensure that buyers of securities receive complete and accurate information before they invest, fundamentally shifting the burden of transparency onto the issuer 123. The underlying philosophy of the SEC is not to judge the actual merit or financial viability of the investment, but rather to ensure that all material facts are fully disclosed so that the public can make an informed judgment 16.

The S-1 filing itself is a massive, highly structured document that is typically divided into two primary parts. Part I is the prospectus, the core document that will eventually be distributed to prospective investors 6. It contains the narrative business description, the management's discussion and analysis of financial condition (MD&A), the intended use of proceeds, exhaustive risk factors, and the fully audited financial statements 46. Part II contains supplemental information not strictly required in the prospectus but mandated by the SEC for the public record, such as indemnification arrangements for directors and officers, recent sales of unregistered securities, and itemized expenses related to the issuance 4.

The preparation of this document is a monumental organizational undertaking that requires coordination across multiple professional disciplines. The SEC outlines the formatting and disclosure requirements through various strict regulations: Regulation C governs the general preparation and filing procedures, Regulation S-K dictates the specific narrative and non-financial disclosure items, and Regulation S-X establishes the rigorous standards for the format and content of the financial statements 24. Furthermore, Regulation S-T requires that all of this information be filed electronically through the SEC's Electronic Data Gathering, Analysis, and Retrieval (EDGAR) system 4. The Office of Management and Budget (OMB) estimates that the average burden to prepare a single S-1 filing is approximately 972.32 hours of highly specialized legal, accounting, and executive labor 2. This immense time investment ensures that companies cannot selectively disclose flattering metrics while hiding existential threats, as any material omission or misstatement exposes the executive team, the board of directors, and the underwriting banks to severe litigation and securities fraud charges 16.

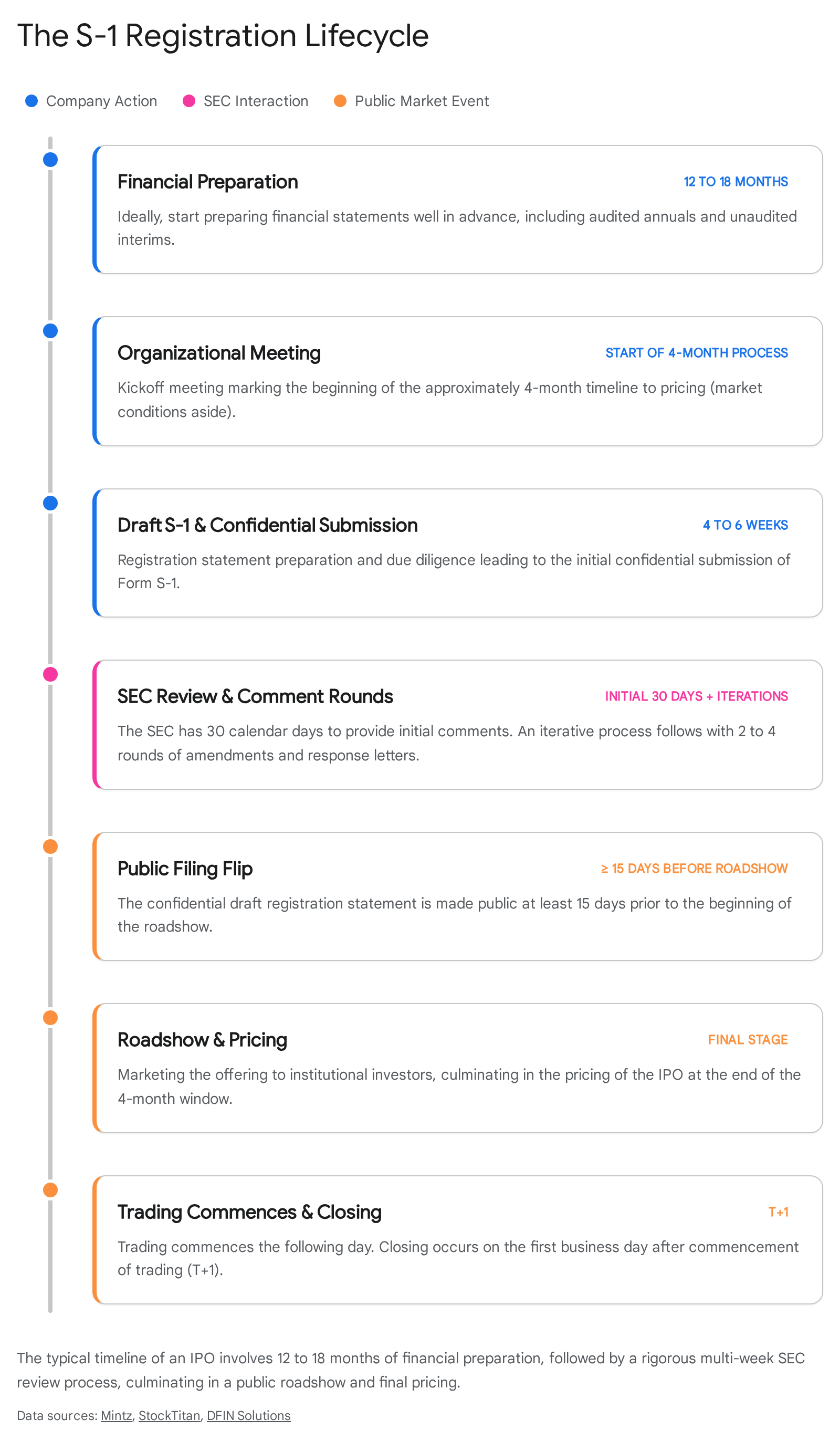

FAQ: How Does the S-1 Filing Process Work?

Filing an S-1 is not a singular event but rather the commencement of a grueling, iterative dialogue with federal regulators. The timeline generally begins 12 to 18 months before the anticipated offering, as the company must transition its accounting practices from private standards to the rigorous public company standards dictated by the Public Company Accounting Oversight Board (PCAOB) 78. This process often requires restating multiple years of financials to ensure absolute compliance and accuracy, a task that demands significant resources from external auditing firms 78.

Following an organizational meeting with underwriters, legal counsel, and auditors, the company spends four to six weeks drafting the initial registration statement 7. Once submitted to the SEC via the EDGAR system, the staff at the SEC's Division of Corporation Finance undertakes a comprehensive review of the document 14. The SEC has 30 calendar days to issue its first round of comments 710. These comment letters act as rigorous interrogations of the company's disclosures. Regulators frequently dissect the filing to question revenue recognition policies, demand clearer risk disclosures, or challenge the definitions of custom, non-GAAP (Generally Accepted Accounting Principles) metrics that management might be using to paint a rosier financial picture 7811.

The company must then respond to these comments and file an amended registration statement, known sequentially as an S-1/A 12. This back-and-forth process typically spans two to four rounds of amendments, stretching over several weeks or months, depending on the complexity of the business, the responsiveness of the corporate team, and the regulatory environment 47. The entire review process can easily take 6 to 12 months from the initial drafting stage 8. Furthermore, if too much time passes since the end of the period covered by the financial statements (typically 135 days), the financial data is considered "stale," and the company must halt the process to update the S-1 with the most recent quarterly numbers, adding further delays and costs 8. Only when the SEC is completely satisfied that all material disclosures meet the stringent requirements of the Securities Act will the registration statement be declared "effective," allowing the underwriting investment banks to finalize the share price and allocate shares to institutional and retail investors 479.

FAQ: What is the Difference Between a Confidential and a Public S-1?

Historically, all S-1 filings were immediately public the moment they were submitted. This meant a company's most sensitive financial data, strategic roadmap, and operational weaknesses were instantly available to competitors, the media, and the broader market the moment the document was transmitted to the SEC 1011. This dynamic created significant risk for private companies, as a failed or delayed IPO attempt would leave their proprietary information exposed without the benefit of public capital. This paradigm shifted fundamentally with the passage of the Jumpstart Our Business Startups (JOBS) Act of 2012, which introduced the confidential filing process for "Emerging Growth Companies" (EGCs) - enterprises with less than $1 billion in annual revenue 1015. Recognizing the value of this process in encouraging capital formation, the SEC expanded this accommodation in July 2017, allowing all companies, regardless of revenue size or EGC status, to submit their draft registration statements (DRS) confidentially 101512.

Filing confidentially allows a company to undergo the rigorous SEC review process - and address the associated, often highly critical, comment letters - entirely out of the public eye 1117. This provides immense strategic flexibility. If the SEC demands major restatements of financials, or if macroeconomic conditions deteriorate, the company can abandon its IPO plans without having aired its internal vulnerabilities to competitors 1011. It essentially allows management to "test the waters" and refine their disclosures without public scrutiny or market speculation 810.

This confidential pathway has also become increasingly vital for companies entering the public markets via Special Purpose Acquisition Companies (SPACs). In de-SPAC transactions, where parties often work against a strict timeline before the SPAC's redemption deadline, submitting a confidential draft allows the SEC to begin reviewing the narrative sections of the prospectus even before the final audit updates are completed, saving valuable time 15. However, the SEC mandates that the veil of secrecy must eventually be lifted; a confidential S-1 must be filed publicly on the EDGAR database no later than 15 days before the company begins its investor roadshow, giving the market adequate time to digest the finalized disclosures before trading begins 111517.

| Feature | Confidential Draft Registration Statement (DRS) | Public Form S-1 |

|---|---|---|

| Visibility | Hidden from the public, media, and competitors during the initial review. | Immediately available to all investors and competitors via the SEC EDGAR database. |

| SEC Review Process | The SEC issues comment letters privately; the company responds and amends the draft privately. | The SEC comment letters and amendments (S-1/A) become part of the public record, tracking the regulatory dialogue. |

| Strategic Flexibility | High. The company can withdraw from the IPO process entirely without public knowledge, avoiding reputational damage. | Low. Withdrawing a public S-1 signals failure or severe market/financial issues, often severely damaging the company's private valuation. |

| Competitor Insight | Competitors remain entirely blind to the company's profit margins, customer concentration, and strategic risks. | Competitors can immediately mine the document for proprietary business strategies, financial weaknesses, and market opportunities. |

| Timing of Disclosure | Must be "flipped" to a public filing at least 15 days prior to the commencement of the IPO roadshow or requested effective date. | Public from day one; investors can track the company's progress and changing metrics through multiple public amendments over several months. |

FAQ: What Are the Common Misconceptions About S-1 Filings?

Because the S-1 is the primary vehicle for entering the public markets, it generates significant media attention. However, it is frequently misunderstood by retail investors and casual market observers. Several pervasive misconceptions can lead to dangerous misinterpretations of a company's timeline, valuation, and immediate market actions.

Misconception 1: Filing an S-1 means the IPO is immediate. Many novice investors assume that once a company files an S-1, shares will be trading on a public exchange within a matter of days. In reality, the public filing merely initiates the visible phase of the SEC review process 49. Even after a public filing, a company may go through several months of S-1/A amendments before the SEC declares the statement effective 4. Furthermore, an S-1 filing does not legally obligate the company to go public; sudden market volatility, macroeconomic shocks, or poor feedback from institutional investors during the roadshow can prompt a company to delay or cancel the offering indefinitely 910.

Misconception 2: The S-1 contains the final share price and valuation. The initial S-1 almost never contains the actual price at which the shares will be sold to the public 813. The "Proposed Maximum Aggregate Offering Price" listed on the cover page of an early draft is usually a placeholder figure - often an arbitrary, nominal amount like $100 million - used solely by the SEC to calculate the required filing fee 14. The actual estimated price range is typically left entirely blank in the initial public filing and is only filled in via an S-1/A amendment shortly before the roadshow begins 1320. The final, exact pricing is determined the night before the stock begins trading, based on institutional order book demand and negotiations between the company and its underwriters 37.

Misconception 3: Reserving a ticker symbol guarantees a specific exchange listing. An S-1 will often state that the company intends to list on the New York Stock Exchange (NYSE) or the Nasdaq under a specific, catchy ticker symbol 1516. However, this is merely a statement of intent, not a guarantee of acceptance. The company must separately apply to the exchange and meet their stringent quantitative and qualitative listing standards, which operate independently of the SEC's registration process 1716.

Misconception 4: Executives can heavily promote the stock once the S-1 is filed. Once the S-1 is filed, the company enters a legally mandated "quiet period" 9. During this time, federal securities laws strictly limit what information the company, its executives, and its related parties can release to the public 9. This prevents management from hyping the stock or making forward-looking statements outside the boundaries of the audited S-1, ensuring that all investors are making decisions based solely on the regulated disclosures 9. Violating the quiet period can result in the SEC delaying the IPO or levying severe penalties.

FAQ: How Should an Investor Scan an S-1 Filing?

An S-1 filing can easily exceed 200 pages of dense legal and financial prose. For analysts and investors, attempting to read the document cover-to-cover like a novel is highly inefficient. Analyzing an S-1 requires a systematic approach to extract the signal from the regulatory noise, focusing on specific sections that reveal the true health of the enterprise 417.

The Prospectus Summary

The filing opens with the Prospectus Summary, which serves as management's carefully crafted "elevator pitch." It distills the company's overarching mission, total addressable market opportunity, competitive strengths, and high-level financial metrics into a few readable pages 4. While this section is heavily curated by the company's marketing and legal teams to present the most optimistic view of the business, it provides crucial baseline context. It establishes the scale of the operation, the primary revenue drivers, and the headline growth rates (such as year-over-year revenue growth or active user counts) that management desperately wants the market to focus on 41314.

Risk Factors

Legally mandated under Regulation S-K, the "Risk Factors" section is arguably the most illuminating part of the entire document 46. To shield themselves from future shareholder lawsuits and SEC enforcement actions, companies must exhaustively detail every conceivable threat that could materially harm their business, operations, or financial condition 46.

While many risks are standard boilerplate language required of any public entity (e.g., "we operate in a highly competitive industry" or "macroeconomic downturns may affect consumer spending"), astute investors scan for highly specific, idiosyncratic risks 41317. If a company discloses that a massive percentage of its revenue is derived from a single client whose contract is up for renewal, or that its entire software stack relies on a third-party vendor with whom they are currently in litigation, these are massive red flags 4. Furthermore, analyzing the order of the risks can be telling, as companies often place the most material, probable, or unique threats near the beginning of the section 4.

Management's Discussion and Analysis (MD&A)

The MD&A is where the raw data of the financial statements is given a narrative voice 617. Here, the executive team must explain the "why" behind the numbers: why revenue grew or shrank, why profit margins contracted, and how capital is currently being allocated 4914. This section is vital for understanding operating leverage and unit economics. Investors should look for disclosures regarding Customer Acquisition Cost (CAC), Lifetime Value (LTV), churn rates, and the company's reliance on specific marketing channels 424. If top-line revenue is growing at 30%, but sales and marketing expenses are growing at 60%, the MD&A will reveal whether that spending is an intentional, temporary land-grab strategy or a sign of deteriorating marketing efficiency and an unsustainable business model.

Financial Statements, Notes, and the Auditor's Report

Located toward the back of Part I, the audited financial statements provide the unvarnished truth about the company's past performance, typically covering two to three prior fiscal years 49. Crucially, investors must check the independent auditor's report that precedes the financials 4. If the auditor includes an explanatory paragraph expressing "substantial doubt" about the company's ability to continue as a "going concern," it indicates a dire situation; the auditors are essentially warning that the company is burning through cash so rapidly that it may face insolvency if the IPO is not successful in raising immediate capital 4.

Furthermore, the footnotes to the financial statements are essential reading. They explain complex revenue recognition methodologies, the assumptions used in valuing stock-based compensation, and the critical details of off-balance-sheet arrangements or looming debt maturities 418.

Use of Proceeds and Capital Structure

The "Use of Proceeds" section dictates exactly how the company intends to spend the incoming public capital 3413. A healthy, ambitious growth company will allocate proceeds to research and development, sales team expansion, or strategic acquisitions 4. Conversely, if the majority of the funds are earmarked to pay down existing high-interest debt or to buy out early private equity backers, the IPO is serving as a balance sheet bailout or a liquidity exit for insiders rather than a growth catalyst for the underlying business 4.

Additionally, the capitalization table and ownership disclosures reveal whether the company utilizes a dual-class or multi-class share structure 414. These structures often grant founders or early insiders "super-voting" shares (e.g., 10 or 20 votes per share compared to the 1 vote per share offered to the public), effectively stripping public market investors of any real influence over corporate governance and ensuring that management remains entrenched regardless of performance 41426.

FAQ: What Do Real-World S-1 Filings Reveal? (Case Studies)

To understand the immense power of the S-1, one must look at how historical and anticipated filings have reshaped market perceptions. The transition from private market hype to public market reality often exposes deep structural challenges or, conversely, validates extraordinary growth engines. Data extracted from these filings strips away the marketing veneer, forcing companies to disclose audited revenue, operating losses, and highly specific concentration or regulatory risks prior to listing.

| Company | Filing Year | Pre-IPO Valuation / Target | Annual Revenue | Profitability Status | Primary Disclosed Risk |

|---|---|---|---|---|---|

| Uber | 2019 | ~$120 Billion (Target) | Flatlining Core Revenue | $3.03 Billion Net Loss | Toxic corporate culture & massive 5-city concentration |

| Arm Holdings | 2023 | ~$60 Billion | $2.68 Billion | Profitable | Heavy China exposure & open-source RISC-V competition |

| 2024 | ~$6.4 Billion | $804 Million | $90.8 Million Net Loss | Unsustainable R&D burn rate & FTC data inquiry | |

| Anthropic | 2026 (Draft) | $965 Billion | $30B+ Run-Rate | Nearing Profitability | Margin compression & massive hyperscale GPU costs |

| OpenAI | 2026 (Draft) | $852 Billion | $25B Run-Rate | Heavy Losses | Unprecedented capital structure & AGI safety tensions |

Uber (2019): Growth at All Costs and the Reality of Unit Economics

When Uber Technologies filed its S-1 in April 2019, it was one of the most highly anticipated IPOs in history, heavily backed by private venture capital and sovereign wealth funds 1920. However, the S-1 revealed the staggering financial toll of its global expansion. The filing disclosed that Uber suffered a massive operating loss of $3.03 billion in 2018 alone 20. More concerning to fundamental analysts, the MD&A revealed that overall net revenue had actually flatlined in late 2018, driven by massive driver incentives and a broad consumer shift toward lower-margin services like UberPool, which cannibalized their premium offerings 29.

The Risk Factors section was equally revealing. A machine-learning analysis of Uber's 35,000-word risk section found it highly distinctive compared to other public companies in the S&P 500 19. Uber was forced to explicitly outline the financial dangers of its toxic corporate culture, noting that public scandals, campaigns like #DeleteUber, and relentless regulatory scrutiny had actively harmed its brand and ongoing operations 19. Furthermore, the S-1 highlighted severe concentration risk: roughly 24% of its global ride-sharing gross bookings came from just five metropolitan areas (Los Angeles, San Francisco, New York, London, and São Paulo) 20. The S-1 effectively forced the market to confront whether a company built on massive subsidies and perpetual regulatory battles could ever transition to sustainable profitability.

Arm Holdings (2023): Intellectual Property and Concentration Risk

When the British semiconductor design giant Arm Holdings filed its F-1 (the foreign equivalent of an S-1) in August 2023, the market was eager to capitalize on the artificial intelligence hardware boom 2132. While the filing confirmed Arm's absolute dominance in mobile CPU architectures, showing steady revenue growth to $2.68 billion, it exposed significant vulnerabilities 2132.

The financial disclosures revealed acute customer concentration: Arm's top five customers accounted for approximately 57% of total revenue for the fiscal year ending March 2023 32. The most glaring risk was geopolitical; Arm China, an entity over which Arm Holdings had limited direct control due to complex regional corporate structures and ongoing disputes, accounted for a massive 24% of total revenue 32. Additionally, the risk factors heavily emphasized the rising threat of RISC-V, an open-source instruction set architecture that poses a direct, free alternative to Arm's proprietary, royalty-bearing designs 32. By laying bare these risks, the S-1 tempered expectations, forcing investors to weigh the company's aggressive 80x earnings multiple against its heavy reliance on the volatile Chinese market and aging legacy IP 32.

Reddit (2024): The Cost of Community and AI Licensing

Reddit's long-awaited S-1 filing in early 2024 provided a fascinating look under the hood of a cornerstone of internet culture 2622. The filing revealed robust top-line growth, with 2023 revenue hitting $804 million (up 21% year-over-year) and gross margins expanding to an impressive 86% 182634. However, the S-1 exposed the immense operational costs required to maintain and grow the platform. Reddit was spending $438 million - a staggering 54% of its total revenue - on Research & Development, an unusually high ratio even for high-growth software companies, which heavily contributed to its $90.8 million net loss for the year 2434.

The S-1 also illuminated the company's strategic pivot toward the AI economy. Reddit highlighted its opportunity to license its massive repository of user-generated conversational data to train Large Language Models (LLMs), a strategy validated by a $60 million annual deal with Google 24. Yet, the rigorous disclosure requirements of the S-1 process forced Reddit to file an amendment (S-1/A) in March 2024, revealing that it had received a letter from the Federal Trade Commission (FTC) 23. The FTC was conducting a non-public inquiry into Reddit's sale and licensing of user data for AI training 23. This late-stage disclosure underscored the S-1's role in ensuring that investors are alerted to emerging regulatory threats before pricing the IPO. Furthermore, the filing detailed a dual-class share structure where Class B shares held 10 votes per share, cementing insider control and raising concerns about long-term corporate governance 26.

The 2026 AI Reckoning: Anthropic and OpenAI

The rumored and confirmed IPO activity of June 2026 represents a watershed moment for the global technology sector, as the two most prominent frontier artificial intelligence laboratories - Anthropic and OpenAI - move aggressively toward public markets 36. In a span of a single week, Anthropic (June 1, 2026) and OpenAI (June 8, 2026) submitted confidential draft Form S-1s to the SEC, initiating a race that analysts believe will redefine public market valuations 36243839.

The transition of these entities from the private sphere to the public domain will drastically alter the AI landscape. In the private markets, both companies achieved staggering, historically unprecedented valuations based on immense capital raises: OpenAI closed a round at an $852 billion valuation with $25 billion in annualized revenue, while Anthropic secured a $965 billion valuation on the back of an astonishing $30 billion to $47 billion annualized revenue run-rate 36243940. In the opaque private ecosystem, rapid growth and model capability are paramount, and exact profit margins can be easily obfuscated from the broader public 4142.

However, the impending public S-1 filings will force a historic recalibration. For the first time, these frontier labs will be required to publish audited financial statements revealing their true gross margins and the exact capital expenditures of their massive hyperscale GPU compute buildouts 2442. The S-1s will expose whether the underlying unit economics of generative AI are sustainable at scale, or if the companies are losing massive amounts of money on every API call to subsidize user growth (OpenAI, for instance, is projected to lose $14 billion in 2026) 404243. If Anthropic's disclosed margins fall below investor expectations, it could trigger a massive compression of AI multiples across the entire venture capital ecosystem, resetting valuations for thousands of smaller startups 42. Furthermore, the SEC mandates will force these companies to articulate the severe tension between their original "safety-first" non-profit ethos and the fiduciary duty to generate quarterly profit growth for public shareholders 36. The S-1 filings will fundamentally transform the AI narrative from speculative potential to audited financial reality 2441.

Bottom Line

The SEC Form S-1 is much more than a bureaucratic hurdle or a mere administrative form; it is the great equalizer in the financial markets. It forces private companies, regardless of their media hype or multi-billion-dollar venture capital valuations, to translate their grand visions into the cold, standardized realities of audited accounting, legal liability, and comprehensive risk disclosure. By carefully scanning the MD&A for unit economics, dissecting the Risk Factors for hidden vulnerabilities, and scrutinizing the Use of Proceeds and capital structure, astute investors can bypass the marketing spin of an IPO roadshow. Whether evaluating a ride-hailing giant bleeding cash, a semiconductor monopoly heavily exposed to geopolitical tensions, or the next frontier of artificial intelligence, mastering the S-1 filing is essential for conducting rigorous, evidence-based fundamental analysis.