OpenAI Nonprofit-to-For-Profit Corporate Restructuring

The structural evolution of OpenAI from a 501(c)(3) tax-exempt organization into a Delaware Public Benefit Corporation (PBC) represents a watershed event in contemporary corporate governance. Finalized in October 2025, this restructuring was designed to reconcile the immense capital requirements of artificial general intelligence (AGI) infrastructure with an immutable mandate to ensure that AGI benefits humanity 123. By June 2026, OpenAI had completed a $122 billion private funding round at an $852 billion valuation and submitted a confidential S-1 draft registration statement to the U.S. Securities and Exchange Commission (SEC) 454.

This transition has precipitated profound legal and economic questions regarding the Charitable Trust Doctrine, the fiduciary boundaries of Delaware corporate law, and the tenability of asymmetric investor protections. The resulting corporate architecture - wherein a minority-stake nonprofit foundation wields absolute governance control over a publicly traded, commercial enterprise - establishes a novel precedent that tests the limits of mission-driven capitalism.

Historical Corporate Forms and Legal Transitions

To comprehend the legal and operational ramifications of the October 2025 recapitalization, it is necessary to trace the structural permutations OpenAI has undergone since its inception. The enterprise has repeatedly altered its legal form to accommodate the escalating financial costs of compute infrastructure while attempting to insulate its safety mission from pure profit motives 75.

Nonprofit Origins and Capped-Profit Subsidiary

OpenAI was incorporated in Delaware in 2015 as a 501(c)(3) nonprofit 2. By 2019, the organization recognized that philanthropic donations were vastly insufficient to fund the computational resources required for frontier model training; having raised only $130 million of an estimated $1 billion requirement, the board sought a mechanism to absorb private capital 67. Consequently, the nonprofit established OpenAI LP (later OpenAI Global, LLC), a "capped-profit" subsidiary.

Under the capped-profit model, private investors and employees could earn financial returns, but these returns were strictly capped. Initially set at 100 times the original investment, subsequent disclosures revealed internal rules allowing the profit cap to increase by 20% annually beginning in 2025 7. All value generated in excess of the cap was legally designated to flow back to the nonprofit parent 7. Crucially, the nonprofit board of directors retained absolute managerial control over the for-profit subsidiary, and investors - including Microsoft, which possessed a 40% profits interest - held economic exposure but no formal governance rights 378.

This structure fractured during a highly publicized governance crisis in November 2023, when the nonprofit board terminated Chief Executive Officer Sam Altman, citing a lack of candor 789. The subsequent investor and employee revolt, which forced Altman's rapid reinstatement, exposed a critical vulnerability in the capped-profit architecture: while the nonprofit board held absolute legal authority, it lacked the practical leverage to govern an enterprise completely dependent on external capital, compute providers, and highly specialized human talent 913.

Transition to Public Benefit Corporation

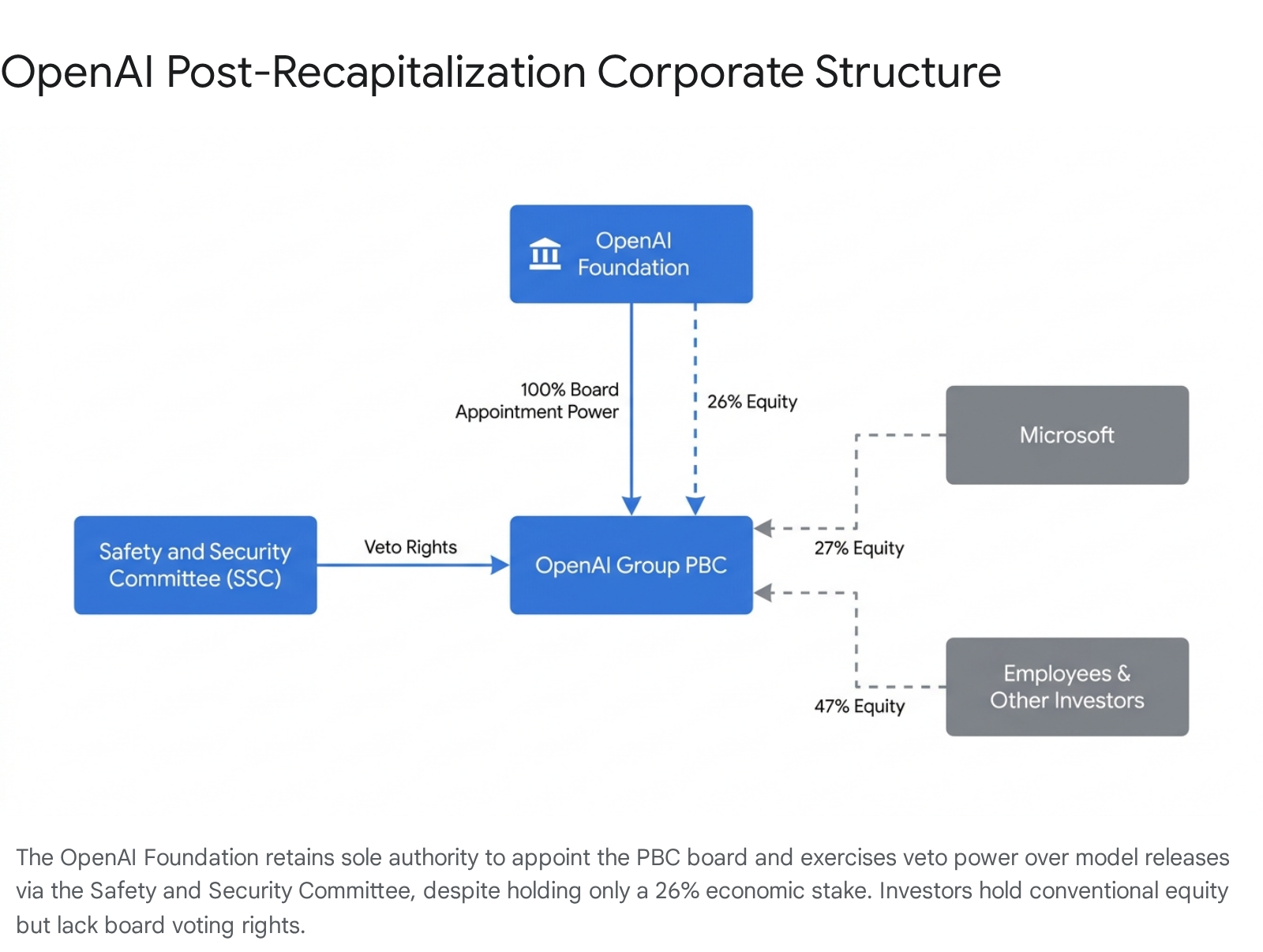

Recognizing that the capped-profit model was fundamentally incompatible with the scale of capital required to achieve AGI, OpenAI initiated a comprehensive recapitalization. The restructuring, formally approved by regulators in October 2025, dismantled the capped-profit LLC and converted the commercial enterprise into a Delaware Public Benefit Corporation known as OpenAI Group PBC 2610. Concurrently, the original nonprofit parent was rebranded as the OpenAI Foundation 23.

The transition to a PBC removed the 100x profit caps entirely, establishing a standard equity structure that allowed for unrestricted shareholder returns 713. This shift was a prerequisite for institutional investment at the magnitude of the $122 billion funding round closed in March 2026, enabling conventional venture capital and strategic partners to hold traditional equity 415.

Charitable Trust Doctrine and Asset Valuation

The transition from a tax-exempt entity to a for-profit PBC necessitated rigorous scrutiny by state regulators, particularly the Attorneys General of California and Delaware. At the core of this scrutiny was the Charitable Trust Doctrine, a foundational principle of nonprofit law dictating that assets held by a charitable corporation are irrevocably dedicated to the organization's specific charitable purpose 1112.

California Attorney General Intervention

Under California law, as established in precedents such as Lynch v. Spilman and Pacific Home v. Los Angeles County, a nonprofit cannot divert its assets for private profit, nor can it fundamentally alter its core mission to enrich private stakeholders 1112. When OpenAI announced its intention to restructure, a coalition of philanthropic and civic organizations - operating under the banner "Eyes on OpenAI" - filed formal petitions urging California Attorney General Rob Bonta to block the transition 121319.

The petitioners argued that OpenAI's intellectual property, computational resources, and staff were developed under the aegis of a tax exemption and thus constituted charitable assets held in trust for the public. They contended that transferring control of these assets to a for-profit PBC violated the Charitable Trust Doctrine and demanded a full disgorgement of value to an independent foundation 1219. The coalition frequently cited the 1990s precedent of Blue Cross of California, which, upon converting to a for-profit entity, was compelled by regulators to endow independent health foundations with over $3 billion in equity 1314.

To resolve these legal vulnerabilities, OpenAI entered into a Memorandum of Understanding (MOU) with Attorney General Bonta in October 2025 1516. The MOU formalized a position of non-objection based on several critical financial and governance concessions. These concessions mandated annual public reporting, periodic meetings between OpenAI and the Attorney General's office, and a requirement to provide 21 days' advance notice before amending the PBC mission or altering the Foundation's voting rights 1617.

Endowment Creation and Equity Allocation

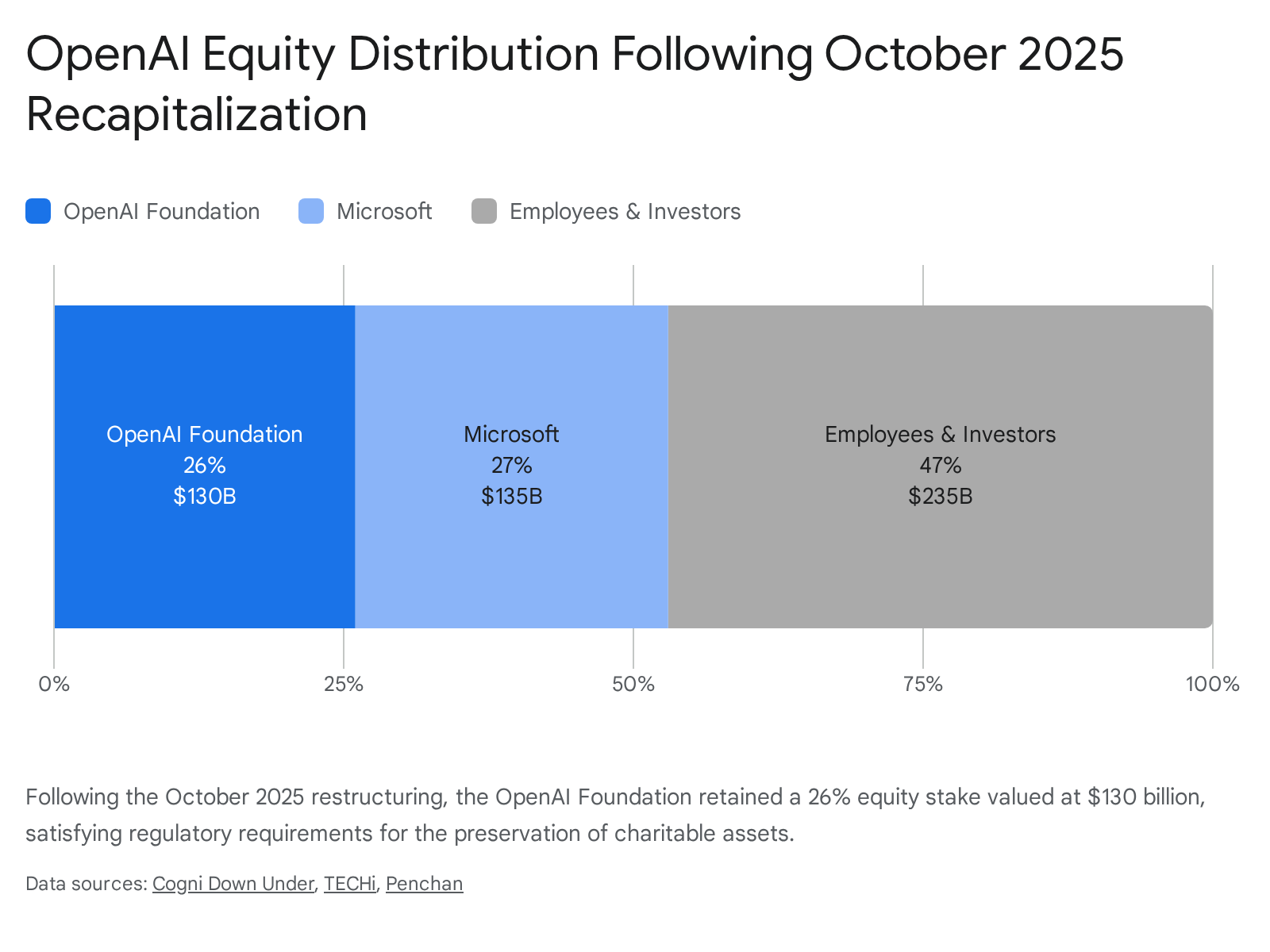

To satisfy the legal requirement that charitable assets be preserved at full fair market value, independent financial advisors assessed the value of the nonprofit's retained control and intellectual property rights 117. Under the recapitalization, the OpenAI Foundation was allocated 2.6 billion shares of convertible common stock, representing a 26% equity stake in the commercial PBC 2418.

At the time of the October 2025 conversion, the enterprise was valued at approximately $500 billion, placing the Foundation's stake at roughly $130 billion 319.

This capitalization instantly transformed the OpenAI Foundation into one of the most well-resourced philanthropic endowments in global history 1019. The Foundation immediately committed $25 billion to open-source health datasets, funding for scientists, and technical solutions for AI resilience, thereby satisfying regulatory demands that the public tangibly benefit from the commercialization of OpenAI's underlying technology 19.

Fiduciary Duties and Corporate Governance Mechanics

The deployment of a Public Benefit Corporation to house a frontier AI lab is not an entirely unique maneuver; competitors such as Anthropic and xAI also utilize the PBC structure to embed societal goals into their commercial operations 1027. However, OpenAI's specific implementation involves highly bespoke legal engineering mandated by the Delaware Attorney General, circumventing standard PBC frameworks to establish an absolute safety mandate 1720.

Delaware Public Benefit Corporation Statutes

Under Section 141(a) of the Delaware General Corporation Law (DGCL), the business and affairs of a standard corporation must be managed by or under the direction of a board of directors tasked with maximizing shareholder value 2122. In a standard Delaware PBC, however, directors owe a tripartite fiduciary duty. They are statutorily required to balance: (1) the pecuniary interests of the stockholders, (2) the specific public benefit identified in the corporate charter, and (3) the best interests of those materially affected by the corporation's conduct 23322434.

Crucially, standard PBC law requires a balancing act; it does not inherently compel directors to prioritize the public mission over shareholder profit in every instance, leading to legal ambiguities regarding how courts will evaluate social-responsibility-washing 202425. To address widespread advocacy fears that OpenAI would simply abandon its commitment to safe AGI under immense commercial pressure, regulators conditioned their approval on a radical modification of this balancing standard 17.

Comparative Corporate Governance Structures

To illustrate the unprecedented nature of OpenAI's charter, the following table compares the fiduciary duties, mission durability, and structural mechanics of traditional corporations, standard PBCs, and the bespoke OpenAI Group PBC.

| Governance Feature | Traditional Delaware C-Corp | Standard Delaware PBC | OpenAI Group PBC (Post-2025) |

|---|---|---|---|

| Primary Fiduciary Duty | Maximize shareholder pecuniary value | Balance shareholder returns with stated public benefit | Balance returns generally, but exclusive duty to mission for safety matters |

| Mission Durability | Minimal; charter easily amended | Charter protection; requires shareholder majority to amend | Absolute protection; OpenAI Foundation holds unilateral veto over charter amendments |

| Safety Dispute Resolution | Board vote based on profit impact | Board vote balancing profit and public impact | Safety & Security Committee (Foundation) holds binding veto over commercial board |

| Board Composition | Elected by majority shareholders | Elected by majority shareholders | 100% appointed by the minority-stake OpenAI Foundation |

Section 141(a) Safety Mandate

The new Certificate of Incorporation for OpenAI Group PBC contains an explicit provision dictating that, in matters concerning the safety and security of the enterprise's technology, the board of directors may not consider the pecuniary interests of stockholders and must base decisions exclusively on the Foundation's mission 1017.

This uncompromised safety mandate effectively insulates the board from shareholder derivative suits that might demand profit maximization in safety-critical scenarios. Conversely, it empowers motivated minority shareholders - provided they meet the 2% equity threshold required for PBC standing - to sue the PBC board if it fails to prioritize the charitable mission over profit, creating a novel litigation risk mechanism designed to enforce alignment through the courts 20.

Safety and Security Committee Authority

To operationalize this safety mandate, the restructuring formalized the ultimate authority of the Safety and Security Committee (SSC). Notably, the SSC is housed strictly within the nonprofit Foundation, not the for-profit PBC 317. Chaired by independent director Zico Kolter - who sits on the Foundation board but serves only as an observer on the PBC board - the SSC holds a contractual "effective approval right" over PBC actions 17.

The SSC possesses the unilateral authority to mandate mitigation measures, up to and including halting the deployment of new AI models, even if the commercial PBC board, external investors, or cloud partners advocate for immediate release 101726. By severing the SSC from the PBC's fiduciary structure and housing it within the tax-exempt entity, OpenAI established a structural brake on rapid, unsafe commercialization, ensuring that safety assessments are entirely insulated from the financial incentives of the underlying business 326.

Legal Precedents and Litigation Risks

The legality of OpenAI's governance structure - where a 26% minority shareholder exercises 100% control over board appointments - relies heavily on evolving Delaware case law regarding DGCL Section 141(a) and ongoing judicial scrutiny surrounding founder duties.

The Moelis Decision and Board Authority

The delegation of absolute governance rights to the OpenAI Foundation was fundamentally tested by recent corporate law developments. In early 2024, the Delaware Court of Chancery issued a landmark ruling in Moelis & Company v. West Palm Beach Firefighters' Pension Fund. The Chancery invalidated several stockholder agreements that granted founders disproportionate veto and appointment powers, ruling that such contracts unlawfully stripped the board of its statutory managerial authority under DGCL Section 141(a) and were therefore void 212728.

Had the Moelis Chancery ruling stood, OpenAI's mechanism of granting the Foundation absolute authority over the PBC board might have been subject to successful facial challenges by public investors. However, the Delaware corporate landscape shifted dramatically to protect bespoke governance agreements. First, in July 2024, the Delaware General Assembly passed Senate Bill 21 (adding DGCL Section 122(18)), explicitly creating a statutory safe harbor for these types of stockholder agreements and conflict-of-interest transactions 272829.

Subsequently, in January 2026, the Delaware Supreme Court reversed the original Moelis Chancery decision. The Supreme Court ruled that corporate acts contravening Section 141(a) are voidable rather than intrinsically void, and are therefore subject to equitable defenses such as laches 212830. The combination of the Supreme Court's reversal and the legislative amendments solidifies the legal foundation of OpenAI's structure. It ensures that the Foundation's asymmetric control rights - particularly its sole power to appoint directors - cannot be easily unraveled by activist investors post-IPO 28.

Elon Musk Litigation and Fiduciary Breach Claims

Alongside structural corporate challenges, OpenAI faced intense litigation regarding its historical transition. In 2024, Elon Musk - an original co-founder of the organization - filed state and federal lawsuits claiming that OpenAI and Sam Altman abandoned their founding charitable purpose to develop open-source AGI for humanity 82731. Musk alleged violations of the Racketeer Influenced and Corrupt Organizations (RICO) Act, breach of contract, false advertising, and breach of fiduciary duty, demanding $150 billion in damages and accusing Microsoft of aiding and abetting a breach of charitable trust 831.

The litigation probed the core vulnerabilities of OpenAI's mission drift, arguing that the transfer of intellectual property into the for-profit vehicle fundamentally enriched private executives and corporate partners at the public's expense 1931. However, in May 2026, a federal jury cleared OpenAI of liability. The verdict did not explicitly validate OpenAI's restructuring on its ethical or substantive merits; rather, the judge instructed the jury to evaluate the statute of limitations for California charitable trust claims (typically three to four years), and the jury concluded that Musk had filed his lawsuit too late, given his departure from the organization in 2018 and his final financial contributions in 2020 31. While OpenAI survived the litigation, the trial publicly underscored the friction between the enterprise's philanthropic origins and its current commercial realities 19.

Antitrust Scrutiny and Global Regulatory Frameworks

As OpenAI restructured its internal governance, its deep entanglements with Big Tech - specifically its exclusive cloud partnerships and massive infrastructure contracts - drew intense antitrust scrutiny across multiple international jurisdictions. The regulatory focus expanded from examining OpenAI's corporate form to interrogating its market power and infrastructural dependencies.

United Kingdom Competition and Markets Authority

The United Kingdom's Competition and Markets Authority (CMA) launched a complex 15-month merger inquiry into the partnership between Microsoft and OpenAI, probing whether Microsoft's $13 billion initial investment and compute provisions constituted a de facto merger 323334. The CMA expressed deep concerns that Microsoft could leverage its control over OpenAI to restrict rivals' access to foundational models, particularly within the cloud compute and productivity software markets 323335.

In March 2025, the CMA concluded its investigation without imposing sanctions, determining that while Microsoft held "material influence" over OpenAI's commercial policy, it did not possess "de facto control" under the Enterprise Act 2002 333446. This favorable ruling was catalyzed by strategic adjustments to the partnership. Evidence reviewed by the CMA highlighted a reduction in OpenAI's reliance on Microsoft for compute power 3447. These adjustments were formalized in April 2026, when OpenAI and Microsoft amended their agreement to explicitly end Azure's exclusivity, allowing OpenAI to serve its products on competing infrastructure like Amazon Web Services (AWS) 4636. Furthermore, the amendment capped OpenAI's revenue-share payments to Microsoft through 2030 and rendered Microsoft's intellectual property licenses non-exclusive through 2032 3637. This deliberate dilution of absolute exclusivity was vital in neutralizing the CMA's antitrust concerns.

European Union Artificial Intelligence Act and Antitrust Measures

Concurrently, the European Commission pursued aggressive regulatory actions under the Digital Markets Act (DMA) and finalized the implementation framework for the EU AI Act. While the Commission concluded in mid-2024 that the Microsoft-OpenAI partnership did not violate EU merger regulations - pivoting instead to investigate potential anti-competitive exclusivity clauses and "acqui-hires" - the broader regulatory environment remained highly restrictive 5038.

In May 2026, the European Commission published its draft guidelines on High-Risk AI Systems (HRAIs) under the newly revised AI Act 52. Although intense lobbying succeeded in pushing the implementation deadlines for high-risk system classifications to 2027 and 2028, the stringent transparency and risk-management rules covering general-purpose AI models (such as OpenAI's GPT-4 and Anthropic's Claude) remained on their original enforcement schedule 3940.

Furthermore, the Commission demonstrated an unprecedented willingness to intervene directly in AI market dynamics. In June 2026, the EU imposed emergency interim antitrust measures against Meta, ordering the company to restore third-party AI assistants' free access to WhatsApp to prevent irreparable harm to competition in the general-purpose AI assistant market 4156. This aggressive enforcement action signals that while OpenAI survived merger control reviews, its commercial expansion and distribution tactics remain tightly constrained by behavioral antitrust mandates in the European Economic Area.

United States Federal Trade Commission Investigations

In the United States, the regulatory environment similarly intensified under the second Trump administration. By 2025, the Federal Trade Commission (FTC), led by Assistant Attorney General for Antitrust Gail Slater, initiated expansive investigations into Microsoft's cloud infrastructure and AI operations 57. The probe scrutinized AI training costs, data acquisition strategies, and alleged anti-competitive licensing practices that penalized customers running Microsoft software on rival platforms 57. The continued regulatory pressure forced OpenAI to maintain rigorous documentation separating its operational independence from Microsoft's broader cloud ecosystem.

Capital Formation and Initial Public Offering Preparations

The culmination of OpenAI's restructuring was the decision to pursue liquidity and permanent capitalization in the public markets. On June 8, 2026, OpenAI submitted a confidential draft S-1 registration statement to the SEC, initiating the Initial Public Offering (IPO) process 245. This submission followed a historic private financing round that fundamentally altered the cap table.

March 2026 Private Funding Round

In March 2026, OpenAI closed a $122 billion funding round, anchoring the company at an $852 billion post-money valuation 442. While the headline figure represented the largest private financing in Silicon Valley history, the architecture of the capital injection relied heavily on contingent commitments and vendor financing 5960.

Of the $122 billion raised, $110 billion was supplied by three strategic anchors: Amazon ($50 billion), Nvidia ($30 billion), and SoftBank ($30 billion) 41561. However, Amazon's contribution included $35 billion entirely contingent on OpenAI achieving an IPO or officially reaching AGI, bundled alongside a requirement for OpenAI to spend $100 billion on AWS infrastructure over eight years 15. Similarly, Nvidia's $30 billion commitment was primarily structured as dedicated compute capacity and training infrastructure on its Vera Rubin systems, rather than liquid cash 15. Only the remaining $12 billion - sourced from traditional venture capital firms, sovereign wealth funds, and a retail banking tranche - functioned as standard financial equity 415.

Capital Allocation of March 2026 Funding Round

| Investor Category | Committed Value | Structural Nature of Commitment |

|---|---|---|

| Amazon | $50 Billion | $15B initial; $35B conditional on AGI/IPO. Tied to $100B AWS spend. |

| Nvidia | $30 Billion | Primarily in-kind provision of compute capacity and Vera Rubin systems. |

| SoftBank | $30 Billion | Direct equity investment and syndicated co-investments. |

| Institutional & Retail VC | $12 Billion | Clean, unrestricted capital from firms like a16z, MGX, and retail banks. |

Financial Projections and Margin Pressures

OpenAI's S-1 filing tests the public market's appetite for frontier AI economics, forcing a collision between unprecedented top-line growth and astronomical infrastructure burn 62. By early 2026, OpenAI reported an annualized revenue run rate of approximately $24 to $25 billion - generating nearly $2 billion per month - driven by rapid enterprise adoption and paid consumer subscriptions 4263. This growth trajectory drastically outpaces the historical scaling of legacy platforms like Alphabet and Meta 459.

However, the foundational models require staggering capital expenditures. S-1 disclosures and internal projections indicate that OpenAI is on course to record net losses of roughly $14 billion in 2026 alone, with cumulative losses potentially reaching $44 billion before the company projects profitability in 2029 156364. The company's gross margins hover at an estimated 33%, a figure that resembles hardware semiconductor or heavy cloud infrastructure providers rather than high-margin software-as-a-service (SaaS) platforms 63. With over $600 billion in committed server spending projected through the end of the decade, the financial viability of the enterprise rests entirely on achieving massive inference optimization and sustained pricing power 6063.

Securities and Exchange Commission Registration

The confidential S-1 submission formalizes a profound structural anomaly for prospective public investors: purchasing equity in OpenAI provides economic exposure to the AI revolution but absolutely no governance control over the company's strategic direction 42463.

Because the OpenAI Foundation explicitly retains the sole authority to appoint and remove all PBC directors, public shareholders will have no mechanism to enact leadership changes, block acquisitions, or demand cost-cutting measures 244366. Furthermore, if the Safety and Security Committee exercises its veto power to halt a highly profitable product release due to alignment risks, public shareholders have virtually no legal recourse under the tailored Section 141(a) safety-first charter 317.

This dynamic establishes a new paradigm in public equities: a near-trillion-dollar commercial vehicle governed entirely by an autonomous, tax-exempt entity holding only 26% of the economic value 2418. While super-voting shares and dual-class structures have long insulated tech founders, OpenAI's structure divorces governance from equity wholesale. Public investors must underwrite the financial risk of AGI development while accepting that the fiduciary priority of the board is a philanthropic mission, not shareholder value maximization. The success of the forthcoming IPO will dictate whether global capital markets are willing to subsidize this unprecedented experiment in mission-driven capitalism.