Dual-class share structures in 2026 technology IPOs

The 2026 Technology Initial Public Offering Environment

The global capital markets in 2026 are undergoing a profound structural transformation driven by a cohort of highly capitalized, privately held technology companies transitioning to the public equities market. These initial public offerings (IPOs), frequently classified as "mega-caps" due to valuations that exceed hundreds of billions or even reach trillions of dollars, introduce unprecedented governance complexities. The dominant feature of this new cohort is the pervasive utilization of dual-class and multi-class share structures, a mechanism allowing founders and insiders to retain absolute operational control while simultaneously raising massive tranches of public capital 1224.

The impetus for entering the public markets remains fundamentally economic. Data aggregated by the Securities and Exchange Commission's Office of the Advocate for Small Business Capital Formation (OASB) indicates that while private venture capital remains robust, it has become highly concentrated; in early 2025, 40% of all venture capital dollars were allocated to just ten companies, and the median age of a company raising a Series D or later round extended to 9.7 years 3. For entities developing frontier artificial intelligence or aerospace infrastructure, private funding pools are ultimately insufficient 4. The public markets offer superior liquidity, lower capital costs, and the ability to fund massive capital expenditures - four years post-IPO, public companies typically demonstrate a 40% increase in capital expenditures and a 50% increase in total assets compared to their private-market peers 3.

However, as these entities transition, their founders are systematically rejecting the traditional "one share, one vote" governance paradigm championed by institutional investors and pension funds 56. The dual-class share structure, which grants disproportionate voting rights to specific classes of stock, has evolved from a controversial exception to a standard feature of the technology sector 578. In 2021, 32% of all IPOs and 46% of technology IPOs featured multi-class structures 8. This high prevalence continued through the intermediate years, with prominent 2023 and 2024 tech IPOs such as ServiceTitan, Reddit, Ibotta, Rubrik, and Klaviyo all utilizing multi-class architectures 8.

In 2026, the scale of this phenomenon has escalated. Companies such as SpaceX, carrying an estimated valuation of $1.75 trillion, alongside leading artificial intelligence developers Anthropic and OpenAI, which command valuations in the hundreds of billions, are dictating terms to the public markets 12411. The sheer size of these offerings has forced a systemic capitulation among major index providers, altering the mechanical flow of passive capital and redefining long-run shareholder risk 910.

Governance Tradeoffs and Structural Mechanics

The Voting Power and Economic Interest Wedge

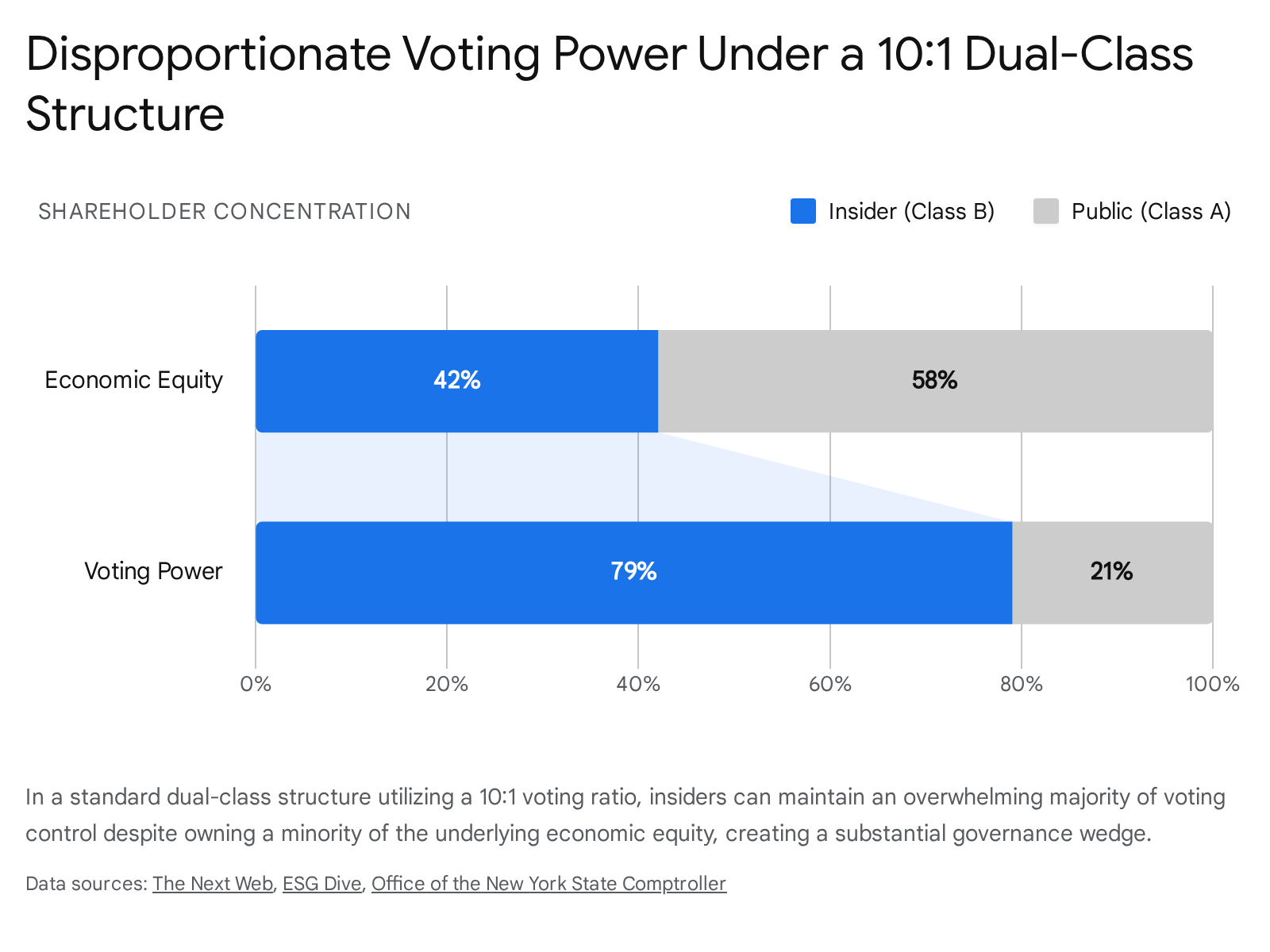

The fundamental mechanics of a dual-class share structure involve the separation of financial exposure from corporate control. In a conventional corporate structure, equity ownership and voting power are perfectly aligned on a 1:1 ratio. In a dual-class system, the public is typically offered Class A shares carrying one vote per share, while founders and key insiders retain Class B shares that carry multiple votes - most commonly ten votes per share 1611. This mathematical disparity creates a "wedge" between an insider's economic ownership and their voting dominance 11121314.

The SpaceX IPO scheduled for mid-2026 serves as the primary exemplar of this structure taken to its theoretical extreme. According to public filings and market analysis, SpaceX is targeting an IPO to raise approximately $75 billion by offering merely 4% to 5% of its total equity to the public at $135 per share 1224. The Class B shares retained by the CEO and insiders carry ten votes per share 1215. Consequently, while the CEO holds roughly 42% of the company's economic equity, the dual-class architecture guarantees approximately 79% to 85% of the total voting power 21516.

This extreme concentration of power yields specific agency costs. Under this structure, public shareholders acquire the majority of the economic exposure associated with the newly issued equity without a corresponding proportional voice in the governance of the company 16. Structural safeguards typically expected by institutional investors are nullified. For instance, reports indicate that the CEO cannot be removed from the board or from executive positions without a vote of the Class B shares - meaning removal mathematically requires the CEO's own consent 16. Furthermore, this insulation has historically allowed insiders to execute transactions without independent committee oversight, such as the reported all-stock acquisition of xAI in early 2026 and the issuance of performance-based super-voting grants tied to highly speculative milestones like planetary colonization 216. Proponents justify this structure by arguing it protects visionary leaders from short-term market pressures, allowing them to pursue capital-intensive, multi-decade innovations 4820. Conversely, governance advocates argue it entrenches management and removes the disciplining mechanisms necessary to correct strategic drift 617.

Mission-Driven Governance and Public Benefit Corporations

While traditional dual-class structures are utilized to preserve founder authority, alternative legal architectures have emerged among artificial intelligence developers in the 2026 IPO pipeline. These alternative structures are engineered not for individual entrenchment, but to ensure "mission-driven" governance, specifically balancing the extreme capital requirements of frontier AI training with rigorous safety mandates 41118.

Anthropic, which operates with a revenue run-rate approaching $9 billion and a valuation exceeding $180 billion, is navigating its IPO preparation through a Public Benefit Corporation (PBC) model 423. A PBC legally requires corporate directors to balance shareholder financial returns with a stated public benefit - in Anthropic's case, the safe deployment of artificial intelligence 2324. To enforce this, Anthropic utilizes a Long-Term Benefit Trust (LTBT), an independent body holding a special class of shares (Class T) equipped with escalating board-election rights 424. Over time, the LTBT is designed to elect a majority of independent directors, providing technical and safety experts with ultimate oversight of strategic decisions 4. This architecture effectively inverts the standard dual-class model: rather than founders utilizing super-voting shares to entrench themselves against public markets, the founders cede ultimate, long-term authority to an independent mission guardian 4. The proposed offering structure involves a single class of common stock for public buyers, simplifying the capitalization table while introducing an unprecedented center of gravity in corporate control that prevents any single investor or tech conglomerate from steering the research agenda solely for commercial gain 424.

OpenAI has undertaken a similar structural evolution. Transitioning away from its complex capped-profit structure, the organization announced in late 2025 a recapitalization into OpenAI Group PBC, a standard for-profit entity governed and controlled by the nonprofit OpenAI Foundation 1819. Under this model, all equity holders own traditional stock that participates proportionally in value creation 1819. However, the nonprofit Foundation maintains special voting and governance rights, allowing it to appoint all members of the PBC's board of directors and replace them at any time 19.

| Governance Architecture | Primary Control Mechanism | Stated Purpose | Example Entity |

|---|---|---|---|

| Traditional Dual-Class | 10:1 super-voting Class B shares held by insiders. | Insulate management; prevent hostile takeovers; enable long-term strategic execution. | SpaceX, Meta 1216 |

| Public Benefit Trust | Independent trust holds special voting shares to elect the board majority. | Lock in mission alignment; prevent commercial prioritization over safety protocols. | Anthropic 424 |

| Nonprofit Control | Nonprofit foundation holds special voting rights to appoint the entire corporate board. | Ensure technological development benefits humanity; override profit maximization if necessary. | OpenAI 1819 |

These distinct models indicate that technology governance in 2026 is fracturing into specific typologies. While they differ in execution, they share a fundamental premise: public equity investors are expected to provide capital while systematically waiving the governance rights traditionally associated with public ownership 2416.

Post-IPO Performance and the Valuation Lifecycle

The Initial Valuation Premium

The proliferation of dual-class shares is frequently justified by the assertion that insulated management teams generate superior long-term financial performance. Empirical studies analyzing initial public offerings over extended time horizons present a nuanced reality governed by a distinct corporate life cycle 142027.

Comprehensive research assessing matched samples of U.S. dual-class and single-class firms demonstrates that dual-class companies exhibit a distinct valuation premium at the time of their IPO 1420. Measured by Tobin's Q - a financial ratio dividing a firm's market value by the replacement cost of its assets - dual-class firms average a 13% higher valuation than comparable single-class firms at the end of their IPO year 14. Furthermore, dual-class issues experience less underpricing at the time of the offering (by approximately three percentage points) and achieve slightly higher post-IPO institutional ownership 21. This initial premium indicates that market participants attribute positive value to the founder's distinct vision during the high-growth, early-stage phase of a technology company's life cycle 111720. A strong bargaining position, fueled by the vast availability of private capital, allows founders to raise financing without losing control, and the market initially rewards this continuity of leadership 1213.

The Transition to Valuation Discount

However, empirical data demonstrates that this valuation premium is impermanent. As the firm matures, the advantages of the dual-class structure recede, and the inherent agency costs compound 111427. Longitudinal analysis of Tobin's Q differentials reveals a systematic decay. In the first three years following an IPO, dual-class firms maintain an average premium in Tobin's Q of 0.22 to 0.24 over single-class firms 14. By years four and five, this premium dissipates entirely, becoming statistically insignificant 14. Critically, by years six to nine (and beyond), the dual-class structure becomes a liability; dual-class firms trade at a significant valuation discount, demonstrating a Tobin's Q that is on average 10% lower (a differential of -0.17 to -0.22) than equivalent single-class firms 14.

This predictable degradation is driven by the mechanical widening of the "wedge" between economic ownership and voting power. At the time of the IPO, controlling shareholders in dual-class firms typically hold significant economic equity. However, as the company ages, founders frequently liquidate shares, issue new equity for employee compensation, or raise secondary capital to fund expansion 14. Research indicates that the mean controlling shareholders' equity stake decreases from 53.24% in the first year post-IPO to 38.11% by the fifth year 14. Simultaneously, because their high-vote shares are retained, their voting power remains artificially rigid. Consequently, the mean governance wedge increases from 19.33% to 22.53% over the same five-year period 14. As founders assume less financial risk while maintaining absolute control, the misalignment of incentives grows, triggering the valuation discount observed in mature dual-class entities 1114.

| Post-IPO Phase | Average Tobin's Q Differential (Dual vs. Single) | Driving Factors |

|---|---|---|

| Years 1 - 3 | +0.22 to +0.24 (Premium) 14 | Market rewards founder vision; strong revenue growth; high initial insider economic alignment. |

| Years 4 - 5 | Minimal / Insignificant 14 | Growth stabilizes; insiders begin equity dilution; initial premium dissipates. |

| Years 6 - 9+ | -0.17 to -0.22 (Discount) 14 | Governance wedge expands significantly; agency costs outpace strategic benefits; potential entrenchment. |

Implementation of Sunset Provisions

The documented degradation of value has catalyzed robust advocacy for "sunset clauses" - mechanisms written into the corporate charter that dictate the automatic conversion of high-vote shares into standard single-vote shares.

Sunset provisions generally fall into three categories 2223: 1. Time-Based Sunsets: Automatic conversion occurs after a predetermined period (e.g., five or seven years) regardless of external events 623. 2. Dilution-Based Sunsets: Conversion is triggered when the high-vote class is diluted below a prescribed threshold of total outstanding common stock (e.g., falling below 10% of total shares) 23. 3. Event-Driven Sunsets: Conversion is tied to the founder's departure, disability, death, or the transfer of shares to third parties 2223.

Institutional advocates, most notably the Council of Institutional Investors (CII), strongly promote mandatory time-based sunsets, arguing that unequal voting rights should persist no longer than seven years post-IPO 62223. This seven-year benchmark is informed directly by the empirical life-cycle data indicating that valuation premiums evaporate within that window 614. Quantitative studies reveal that organizations adopting sunset provisions exhibit significantly higher valuations in their third year of public trading compared to businesses utilizing permanent, perpetual dual-class structures 27.

Despite these performance indicators, the private ordering of markets demonstrates a varied landscape. While many institutional investors demand seven-year limits, founders with immense bargaining power continue to resist. Data covering the 2023 and 2024 tech IPO cohorts highlights a nearly even division, with roughly half of the dual-class entities adopting sunsets and the remaining half eschewing them entirely in favor of perpetual control 8. Even among those adopting time-based sunsets, the horizons vary drastically: companies like Ibotta and Klaviyo adopted seven-year sunsets, whereas Rubrik opted for ten years, ServiceTitan for fifteen years, and Tempus AI for twenty years 8.

Index Inclusion Policies and Passive Capital Dynamics

The Reversal of the 2017 Exclusions

The rapid expansion of the passive investment industry means that inclusion in broad-market indexes fundamentally determines the liquidity, cost of capital, and shareholder base of newly public companies. Following the 2017 initial public offering of Snap Inc., which issued non-voting shares entirely to the public, institutional outrage prompted the major index providers to enact stringent eligibility rules 5731. S&P Dow Jones Indices banned all new dual-class share offerings from the S&P Composite 1500 (including the S&P 500), and FTSE Russell implemented a rule barring companies unless greater than 5% of voting rights were held by public shareholders 57924.

However, the sheer market capitalization and economic footprint of multi-class technology firms forced a pragmatic retreat by 2023 and 2026. Asset managers, including Vanguard, State Street, and BlackRock, publicly contested the exclusions, noting that barring massive tech entities from broad market indices deprived index-fund clients of access to the investable universe and distorted the indices' representation of the actual economy 57. As the $3.6 trillion wave of IPOs approached, the index providers capitulated 1133. In April 2023, S&P Dow Jones reversed its 2017 policy, allowing companies with multiple share classes to once again be eligible for the S&P Composite 1500 and its component indices 8931.

Fast-Entry Mechanisms and Minimum Free Float Waivers

To accommodate the unprecedented scale of the 2026 mega-cap IPOs, index providers undertook significant methodology adjustments focused on "fast entry" mechanisms 103325. These rules ensure massive IPOs are rapidly integrated into index benchmarks, preventing severe tracking errors for passive funds.

FTSE Russell conducted a market consultation in early 2026 specifically citing the impending IPOs of SpaceX, OpenAI, and Anthropic 1033. Effective May 2026, FTSE Russell updated its rules to allow companies that rank in the Russell Top 500 to be added to the index after the close of trading on the fifth day following initial listing 91025. Crucially, FTSE Russell addressed the restrictive 5% voting rights and 5% free-float rules. A security with 5% or less free float may now qualify for fast entry if the company's investable market capitalization exceeds ten times the regional inclusion threshold, entirely waiving the requirement to satisfy the minimum percentage float 3335. For developed market companies failing the 5% public voting rights threshold at the time of IPO, they remain eligible if lock-up expirations are mathematically expected to push public voting rights above the 5% threshold within 12 months 2535.

Other index providers exhibit similar accommodations for absolute scale: * MSCI: MSCI's Global Investable Market Indexes have maintained fast-track rules since 2007, bypassing traditional length-of-trading and liquidity screens. A large IPO is eligible for early inclusion after 10 trading days if its full market capitalization exceeds 1.8 times the interim size-segment cutoff (approximately $26 billion for the U.S. in May 2026) and its free-float market cap exceeds half that threshold 92637. MSCI waives standard percentage-based free-float requirements (typically 15%) for mega-IPOs that meet these absolute dollar-value thresholds 263738. * CRSP (Center for Research in Security Prices): CRSP adjusted its fast-track screen to admit low-float companies if their float-adjusted market capitalization is at least 0.005% of the index-eligible universe (roughly $3.3 billion as of early 2026), moving away from strict percentage-float requirements 937.

| Index Provider | Fast-Entry Timing | Free Float Exception for Mega-IPOs | Voting Rights Requirement for IPOs |

|---|---|---|---|

| S&P Dow Jones | Varies by index. | Subject to committee review. | Eliminated completely in 2023. 931 |

| FTSE Russell | Day 5 post-listing. | Waived if market cap > 10x regional threshold. 332535 | Permitted < 5% at IPO if lock-up expiry pushes > 5% within 12 months. 2535 |

| MSCI | Day 10 post-listing. | Dollar-value thresholds override 15% minimum. 263738 | No restrictive minimum voting rights rule applied. 2637 |

| CRSP | Day 5 post-listing. | Allowed if float-adjusted market cap > ~$3.3B. 937 | No specific voting rights barrier. 9 |

Passive Fund Rebalancing and Volatility Risks

The intersection of fast-entry index rules and highly constrained dual-class IPO structures creates acute mechanical pressures in the equity markets. When an entity lists with a trillion-dollar valuation but offers only a minuscule percentage of its equity to the public (e.g., a 4% public float), it presents severe liquidity constraints 243727.

Upon the execution of the fast-entry rules (such as day 5 for Russell or day 10 for MSCI), trillions of dollars in passive index-tracking funds are mathematically required to purchase the stock simultaneously to align their portfolios with the updated index weightings 373828. Because the public float is exceedingly thin, this mechanical, price-insensitive demand can trigger severe short-term volatility and dramatic price inflation. Institutional critics argue this dynamic disproportionately benefits early retail and active institutional allocators who engage in "front-running," while embedding an artificially inflated cost-basis into the retirement accounts of passive investors 43727. Furthermore, as insider lock-up periods expire over the subsequent 180 to 366 days post-IPO, the float-adjusted market capitalization expands, forcing passive funds to execute subsequent waves of buying, further cementing the dual-class entity into the core of the U.S. equities market 9.

Global Regulatory Convergence and Listing Frameworks

The concentration of technology mega-IPOs in U.S. markets has forced competing global exchanges to revise their regulatory frameworks to accommodate weighted voting rights (WVR) and dual-class structures. Rather than enforcing strict corporate governance mandates, international bourses are optimizing their rules to compete for the liquidity and prestige of high-growth innovators.

Hong Kong Exchanges and Clearing Reforms

The Stock Exchange of Hong Kong (HKEX) initiated substantial reforms in early 2026 to optimize its WVR listing requirements and enhance market competitiveness 29303132. To capture a broader range of innovative companies, HKEX proposed halving the financial eligibility thresholds for dual-class listings, bringing the minimum market capitalization requirement down to HK$20 billion, or an alternative threshold of a HK$6 billion market cap combined with HK$600 million in revenue 303132.

Furthermore, to remain competitive with the aggressive governance accommodations available in the United States, HKEX proposed relaxing the cap on weighted voting ratios. Historically capped at 10 votes per share, the exchange now allows a higher weighted voting ratio cap of up to 20 votes per WVR share if the applicant possesses a market capitalization of at least HK$40 billion at the time of listing 293133. HKEX also reduced the minimum economic interest that WVR beneficiaries must hold from 10% to 5%, provided the value of the underlying interest represents at least HK$4 billion at listing 293133. These structural concessions explicitly prioritize the attraction of top-tier technology firms over the preservation of equal shareholder enfranchisement 33.

Singapore Exchange Global Listing Board

Concurrently, the Monetary Authority of Singapore (MAS) and Singapore Exchange Regulation (SGX RegCo) implemented amendments to the Securities and Futures Act in May 2026 to establish the Global Listing Board (GLB) 343548. Developed in collaboration with Nasdaq, the GLB provides an innovative, direct pathway for dual listings across both SGX and Nasdaq utilizing a single prospectus and a harmonized set of listing rules 3435.

While SGX adopted dual-class share structures in 2018 (capping multiple-vote shares at 10 votes per share and embedding safeguards like a 12-month IPO moratorium on WVR share transfers), the 2026 GLB framework represents a comprehensive effort to minimize friction for mega-cap issuers 343637. By harmonizing the timeline, creating safe harbors for forward-looking statements, and enabling pre-marketing outreach to institutional investors in Singapore prior to prospectus lodgment, the GLB framework lowers the operational barriers for U.S.-bound tech IPOs to simultaneously access Asian capital 343548. This global race to efficiency solidifies the dual-class structure as an unavoidable fixture of modern international corporate finance.

| Exchange / Framework | Minimum Financial Threshold for WVR | Max Voting Ratio | Key 2026 Reform Feature |

|---|---|---|---|

| HKEX (Hong Kong) | HK$20B Market Cap (or HK$6B + HK$600M Rev) 31 | Up to 20:1 (if Market Cap > HK$40B) 2933 | Lowered financial eligibility; doubled voting ratio cap for mega-caps. 3133 |

| SGX GLB (Singapore) | S$2B Market Cap 48 | 10:1 36 | Single prospectus dual-listing with Nasdaq; safe harbors for pre-marketing. 343548 |

Institutional Proxy Voting Policies

As the equity markets absorb these structural changes, institutional proxy advisory firms serve as the primary counterweight to absolute insider control. The 2026 proxy voting policy updates from Institutional Shareholder Services (ISS) and Glass Lewis demonstrate an intensified focus on capital structure discipline, executive compensation, and post-IPO shareholder rights 3839404142.

ISS updated its 2026 Benchmark Proxy Voting Policies to explicitly target what it defines as "problematic" capital structures. ISS will generally recommend voting against directors at companies possessing multi-class capital structures featuring unequal voting rights 38. Crucially, exceptions are made only for newly listed companies that implement limited-duration enhanced voting rights (time-based sunset provisions), reinforcing the seven-year timeline advocated by institutional shareholder groups 38. Furthermore, proposals seeking to create new classes of common or preferred stock with superior voting rights will face presumptive opposition from ISS unless specific, stringent conditions are met 3839. ISS also extended its pay-for-performance testing horizon from three years to five years, placing a heavier emphasis on sustained, long-term alignment between executive compensation and shareholder returns 4041.

Glass Lewis has similarly refined its 2026 benchmark guidelines to enhance shareholder protections against unilateral actions by entrenched boards. The firm has intensified its scrutiny of unilateral governance changes adopted post-IPO without shareholder approval. Under the 2026 rules, Glass Lewis will recommend voting against governance committee chairs if a company adopts mandatory arbitration provisions or implements bylaw amendments that reduce shareholder rights (such as limits on shareholder proposal submission or the instatement of supermajority vote requirements) shortly after an IPO, spinoff, or direct listing 384042. Additionally, Glass Lewis implemented a comprehensive, scorecard-based methodology for evaluating executive pay-for-performance alignment, aggregating up to six quantitative tests to penalize firms that enrich management without delivering sustained value 3841.

While proxy advisors wield significant influence over the vast pool of institutional capital that votes at annual meetings, their practical leverage is inherently limited in companies operating with massive voting wedges. Even if ISS and Glass Lewis recommend wholesale voting against a board of directors, a founder controlling 75% to 85% of the voting power can unilaterally ratify all governance and compensation decisions, rendering the advisory recommendations largely symbolic 1516. Consequently, the proxy advisors' policies increasingly serve as punitive signaling mechanisms for secondary market investors rather than direct levers of corporate control in dual-class mega-caps.

Conclusion

The 2026 landscape for technology initial public offerings solidifies the dual-class share structure as the dominant operational vehicle for premier, highly valued enterprises. The sheer scale of entities such as SpaceX, Anthropic, and OpenAI provides their leadership teams with unparalleled bargaining power, enabling them to dictate terms to public markets that prioritize visionary autonomy and mission-driven mandates over democratic corporate governance.

Empirical research confirms a distinct life cycle for these structures: while public markets assign a tangible valuation premium to founder-controlled firms in the immediate years following an IPO, this premium systematically decays. It transitions into a structural valuation discount as the wedge between economic ownership and voting power grows, amplifying agency costs and misaligning incentives over the long term. Despite these documented long-run risks, the systemic barriers to dual-class inclusion have collapsed. Recognizing the existential threat of tracking error and the absolute necessity of reflecting the true macroeconomic landscape, major index providers - including S&P, FTSE Russell, and MSCI - have definitively unwound the exclusions of 2017. They have constructed aggressive fast-entry pathways that mechanically force trillions in passive capital into these low-float equities.

Simultaneously, global exchanges from Hong Kong to Singapore have aggressively liberalized their listing standards to compete for these assets, authorizing higher voting ratio caps and streamlined dual-listing channels. While proxy advisors continue to penalize perpetual multi-class structures and demand rigid, time-based sunset provisions, the confluence of index inclusion mandates, international regulatory competition, and the concentration of public capital virtually guarantees that public market participants in 2026 and beyond must accept significant, structural governance tradeoffs to participate in the highest echelons of technological growth.