SEC Registered Offering Reform 2026

Introduction to the Regulatory Paradigm Shift

On May 19, 2026, the U.S. Securities and Exchange Commission (SEC) proposed a comprehensive package of rule and form amendments designed to modernize the registered securities offering framework under the Securities Act of 1933 123. Representing the most significant overhaul of public capital formation since the 2005 Securities Offering Reform, the proposal seeks to structurally reduce regulatory friction and incentivize private companies to enter and remain in the public equity markets 456. The core of the reform involves dismantling historical barriers to shelf registration - specifically, the one-year reporting history requirement and the $75 million public float threshold - thereby granting newly public and smaller reporting companies immediate access to highly efficient capital-raising mechanisms 347.

The U.S. capital markets have experienced a prolonged structural shift, characterized by a declining number of publicly listed operating companies and an increasing reliance on deep, mature private capital markets 8. Compounding regulatory requirements, strict disclosure scaling cutoffs, and the high fixed costs of public company status have driven many enterprises to defer initial public offerings (IPOs) or remain private indefinitely 589. The 2026 Registered Offering Reform, advanced as a foundational component of SEC Chairman Paul S. Atkins's agenda to revitalize the IPO landscape, represents a philosophical pivot regarding market access 4610.

Historically, the fundamental architecture of the U.S. registered offering process relied on a tiered system that correlated an issuer's market capitalization and tenure in the public markets with its access to streamlined capital-raising tools 711. When the SEC adopted the integrated disclosure system and the shelf registration rules in the 1980s, the presumption was that only companies with significant market following and a proven history of Exchange Act reporting had sufficiently disseminated public information to warrant abbreviated, continuous registration statements 12. This philosophy was expanded in 2005 with the introduction of the "Well-Known Seasoned Issuer" (WKSI) category, which granted the largest public companies unprecedented flexibility 710.

However, market dynamics and information technology have shifted profoundly. The ubiquity of broadband internet, cloud computing, structured data, and real-time electronic filing on the EDGAR system has rendered the historical 12-month seasoning period largely obsolete as a proxy for information dissemination 121314. Acknowledging this reality, the SEC's 2026 proposal transitions the regulatory gatekeeper for offering flexibility from an issuer's size and age to its strict compliance with ongoing disclosure obligations, exchange listing standards, and the absence of disqualifying bad actor status 41015.

In tandem with expanding Form S-3 eligibility, the SEC proposed replacing the domestic WKSI framework with a two-tiered system of "Eligible Listed Issuers" (ELIs) and "Seasoned Eligible Listed Issuers" (SELIs) 1016. Furthermore, the proposal expands incorporation by reference for Form S-1, preempts state-level registration requirements for all registered offerings, and aligns the treatment of former Special Purpose Acquisition Companies (SPACs) with traditional IPOs 11517. While the SEC expects these modernization efforts to yield significant cost savings and agility for issuers, the elimination of seasoning periods has necessitated new investor protection guardrails, including strict limitations on At-The-Market (ATM) offerings and the explicit barring of blank check and shell companies from utilizing the expanded benefits 1518.

Mechanics of the Pre-2026 Registration Framework

To fully contextualize the magnitude of the 2026 reforms, it is necessary to examine the mechanical disparities between the SEC's primary registration vehicles: Form S-1 and Form S-3. The Securities Act requires that every offer and sale of a security be registered with the SEC unless an exemption applies. The form on which an issuer registers these securities dictates the speed, cost, and flexibility of the capital-raising process 1920.

The Limitations of Form S-1

Form S-1 is the SEC's default, long-form registration statement. It is available to all issuers, including private companies executing an IPO and public companies that do not meet the stringent eligibility criteria for short-form registration 1920. Because it serves as the baseline disclosure document, Form S-1 requires exhaustive, standalone compliance with Regulation S-K and Regulation S-X, including comprehensive business descriptions, management discussions and analysis (MD&A), executive compensation details, and full audited financial statements 20.

Prior to the 2026 proposals, Form S-1 presented severe logistical challenges for continuous capital raising. The form did not permit "forward incorporation by reference" for the vast majority of issuers 1921. Consequently, whenever a material event occurred or new quarterly financial data was filed on Form 10-Q, the Form S-1 registration statement became instantly stale. To update the prospectus and resume selling securities, the issuer was required to file a post-effective amendment 21. These amendments were subject to mandatory SEC staff review, introducing unpredictable delays that frequently caused issuers to miss brief windows of favorable market volatility 317. Furthermore, Form S-1 could not be used to conduct delayed primary shelf offerings or continuous At-The-Market programs, forcing ineligible issuers to raise capital through rigid, fully marketed follow-on offerings or highly dilutive private placements 3.

The Strategic Advantages of Form S-3

Form S-3 is the SEC's short-form registration statement, historically reserved for seasoned, heavily capitalized reporting issuers 12022. Form S-3 relies heavily on the concept of integrated disclosure. Rather than repeating exhaustive corporate information in the prospectus, the form allows the issuer to satisfy disclosure requirements by "incorporating by reference" its previously filed Exchange Act reports 202122.

More critically, Form S-3 permits forward incorporation by reference 192123. This "evergreen" feature dictates that any future Form 10-K, Form 10-Q, or Form 8-K filed by the issuer is automatically deemed to be incorporated into the active Form S-3 registration statement 121. This eliminates the need to file post-effective amendments to update financial information 21.

This evergreen capability is what enables "shelf registration" under Rule 415. A Form S-3 eligible issuer can file a single base prospectus registering a large, unspecified dollar amount of securities for future issuance 1923. Once the SEC declares this base registration statement effective, the securities sit "on the shelf" for up to three years 2324. When the issuer's management identifies favorable market pricing, they can execute a "takedown" overnight by simply filing a brief prospectus supplement detailing the specific terms of the trade (e.g., share price and volume), bypassing SEC review entirely 1623.

| Feature | Form S-1 (Long-Form Registration) | Form S-3 (Short-Form Registration) |

|---|---|---|

| Eligibility | All issuers, including private companies | Historically limited by public float and seasoning |

| Disclosure Format | Full standalone prospectus required | Highly streamlined; incorporates Exchange Act filings |

| Forward Incorporation | Prohibited for most issuers pre-2026 | Automatic incorporation of future 10-Ks, 10-Qs, 8-Ks |

| Updates to Financials | Requires SEC-reviewed post-effective amendments | Evergreen; updates automatically via ongoing filings |

| Delayed Shelf Offerings | Prohibited | Permitted (valid for up to three years) |

| At-The-Market Programs | Prohibited | Permitted |

| Preparation Burden | Extremely high cost and time commitment | Low friction, highly cost-effective for takedowns |

Elimination of the Seasoning and Float Constraints

Despite its profound advantages, Form S-3 access was heavily restricted prior to the 2026 reform. To file a primary shelf registration statement, an issuer had to satisfy strict registrant and transaction requirements. The 2026 SEC proposal systematically dismantles these historical gatekeepers, shifting the regulatory focus from corporate maturity to reporting discipline 4715.

Abolishing the One-Year Seasoning Requirement

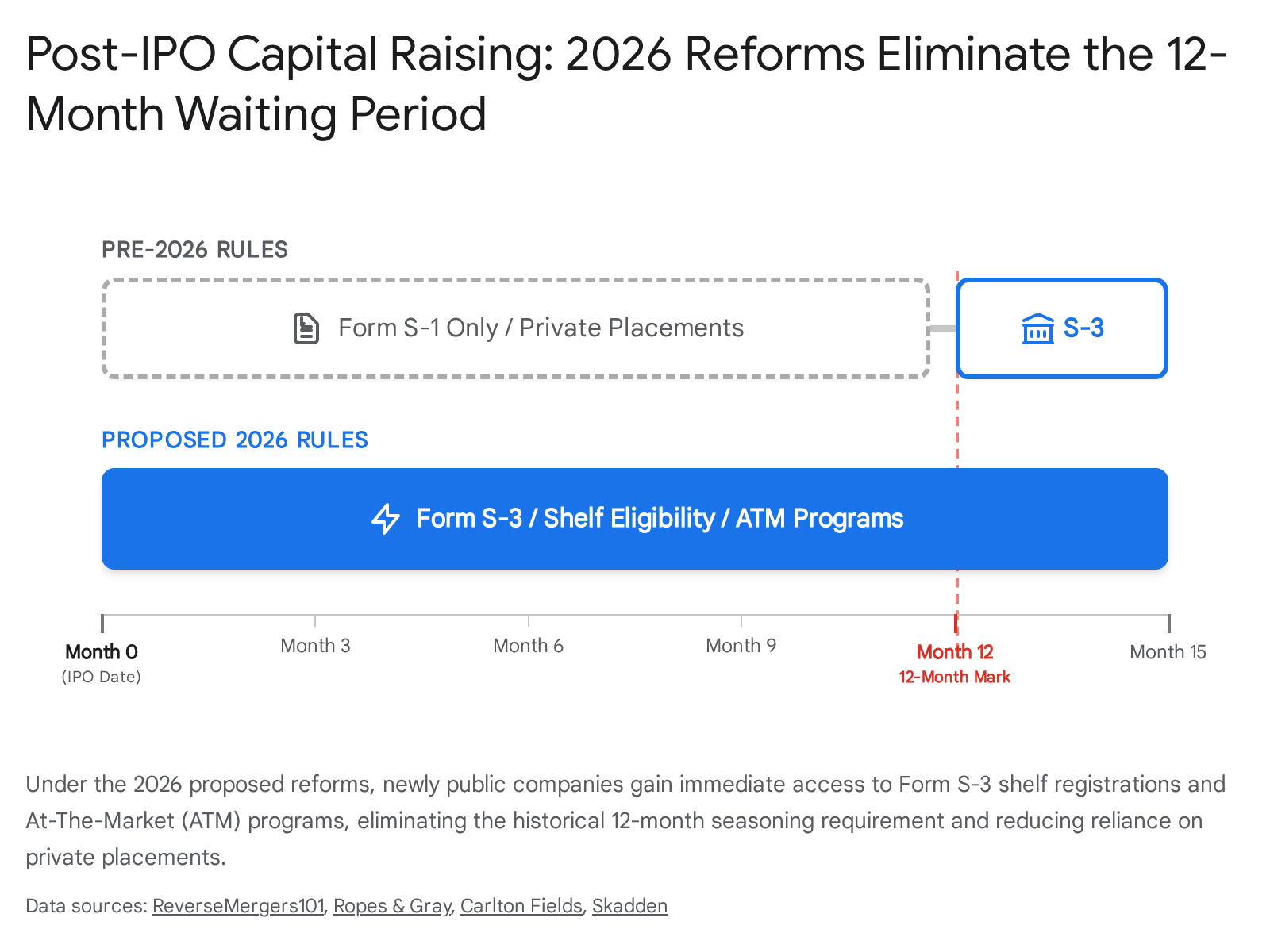

The most significant temporal barrier to Form S-3 eligibility was the one-year seasoning requirement. Under legacy rules, an issuer must have been subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act for at least 12 calendar months immediately preceding the filing of the registration statement 152025.

The 2026 proposal eliminates this 12-month seasoning requirement entirely 31525. Under the revised framework, an issuer becomes eligible to use Form S-3 immediately upon registering a class of securities under Section 12(b) or 12(g) of the Exchange Act, or upon becoming subject to Section 15(d) 1518. The SEC determined that in modern capital markets, the initial registration statement (such as an IPO prospectus) provides sufficient baseline information to investors, which is subsequently updated by current reports, rendering an arbitrary one-year waiting period unnecessary 512.

Eradication of the Public Float Threshold and Baby Shelf Limits

Historically, even if a company had been public for a year, unlimited access to primary shelf offerings required the issuer to maintain an aggregate worldwide market value of voting and non-voting common equity held by non-affiliates (public float) of $75 million or more 41525.

Companies falling below this $75 million threshold were subjected to the restrictive "baby shelf" rules dictated by General Instruction I.B.6 of Form S-3 1524. Under the baby shelf framework, smaller reporting companies were strictly capped in the amount of primary capital they could raise: they could only sell securities equivalent to one-third of their public float during any trailing 12-month period 1526. For a micro-cap company with a $30 million float, this meant a maximum annual shelf access of just $10 million, effectively choking off public capital formation for the very growth-stage enterprises that needed it most 2627.

The 2026 proposal entirely eliminates the $75 million public float threshold and subsequently deletes the baby shelf limitation 31826. Consequently, any reporting issuer that satisfies the baseline registrant requirements can conduct primary shelf offerings of an unlimited size, regardless of its market capitalization or public float 32427. The SEC estimates that removing this arbitrary financial threshold will result in an increase of more than 60 percent in the number of issuers eligible to offer an unlimited amount of securities via shelf registration 102728.

Current and Timely Reporting as the Sole Gatekeeper

With the removal of seasoning and size requirements, the SEC has elevated compliance with Exchange Act reporting as the absolute central pillar of Form S-3 eligibility. To utilize the form under the 2026 framework, an issuer must be strictly current and timely with respect to all material required to be filed pursuant to Sections 13(a), 14(a), 14(c), and 15(d) of the Exchange Act 725. For newly public companies, this means being current and timely for the precise duration they have been a reporting company, rather than a mandatory trailing 12 months 13.

Recognizing that strict adherence can lead to draconian outcomes for minor administrative errors, the SEC integrated a vital grace period into the proposal. Under the new rules, an issuer will not lose its Form S-3 eligibility due to a single untimely filing during the applicable lookback period, provided the late filing was successfully submitted within seven calendar days of its original statutory due date 71115. This late-filing relief is strictly capped at one administrative error per lookback period and expressly does not apply to the failure to file Part III information for an annual report on Form 10-K within the required 120-day timeline 729. The SEC also proposed eliminating historical qualitative disqualifications tied to certain minor electronic EDGAR filing mechanics, Interactive Data File (XBRL) compliance, and immaterial payment defaults, further streamlining the eligibility analysis 715.

Establishment of the Eligible Listed Issuer Hierarchy

The 2005 Securities Offering Reform fundamentally altered the regulatory landscape by creating the "Well-Known Seasoned Issuer" (WKSI) category. WKSIs - defined generally as issuers with at least $700 million in public float or those that had issued $1 billion in non-convertible registered debt - were granted the highest degree of registration and communication flexibility 101630. This created a heavily bifurcated market where massive corporations could raise capital instantaneously, while mid-cap and small-cap companies faced significant procedural friction.

The 2026 SEC proposal retires the WKSI framework entirely for domestic operating companies, determining that raw market capitalization is an inadequate proxy for market efficiency 101630. In its place, the SEC introduces a new two-tiered hierarchy based on exchange listing and reporting compliance: the "Eligible Listed Issuer" (ELI) and the "Seasoned Eligible Listed Issuer" (SELI) 103031.

The Eligible Listed Issuer (ELI)

An Eligible Listed Issuer is defined as any entity that meets the newly simplified Form S-3 registrant requirements and has at least one class of common equity securities listed on a national securities exchange 71029. Because public float has been decoupled from the definition, thousands of sub-$700 million companies will instantly qualify for ELI status, democratizing access to benefits previously reserved for the corporate elite 161732.

Achieving ELI status unlocks a profound suite of registration and communication flexibilities. Under the proposed framework, ELIs gain the ability to pay SEC registration fees on a "pay-as-you-go" basis at the exact time of the shelf takedown, rather than tying up vital working capital by pre-paying fees when the base Form S-3 is filed (Rules 456(b) and 457(r)) 41630. ELIs are also permitted to register additional securities or entirely new classes of securities (including securities of majority-owned subsidiaries) simply by filing a post-effective amendment to a non-automatic shelf registration, bypassing the need to draft a new base prospectus (Rule 413(b)) 41630.

Furthermore, the ELI designation drastically relaxes communication restrictions. ELIs may omit substantial information from their base prospectus, such as the plan of distribution or the specific distinction of whether the offering is primary or secondary, deferring those details to the prospectus supplement (Rule 430B(a)) 4716. In terms of marketing a transaction, ELIs are granted enhanced pre-filing and post-filing communications flexibility, allowing management to issue free writing prospectuses (FWPs) and gauge institutional interest without triggering severe "gun-jumping" violations under Section 5 of the Securities Act (Rules 163, 163A, and 164) 41630.

The Seasoned Eligible Listed Issuer (SELI)

The highest echelon of the new framework is the Seasoned Eligible Listed Issuer. A SELI is defined as an ELI that has additionally been subject to Exchange Act reporting requirements for at least 12 consecutive calendar months 71033.

The SELI tier retains a one-year seasoning requirement because it governs access to the single most powerful tool in the registered offering framework: the automatic shelf registration statement 732. Authorized under Rule 462, an automatic shelf registration statement becomes effective immediately upon filing with the SEC 71516. It is not subject to preliminary SEC staff review, it cannot be delayed by regulatory comment letters, and it allows the issuer to dictate the precise timing of their market entry down to the minute 172334. The SEC concluded that granting automatic effectiveness necessitates at least a one-year track record of public reporting to ensure the market has sufficiently digested the issuer's baseline operational data 732.

The SEC estimates that transitioning from the WKSI system to the ELI/SELI framework will dramatically expand market agility. While only 36 percent of reporting issuers qualified for WKSI benefits under the legacy rules, approximately 74 percent of all reporting issuers will qualify for SELI status and automatic shelf registration under the 2026 proposals 316.

Reallocation of Universal Form S-3 Benefits

Beyond the specific ELI and SELI tiers, the proposal also democratizes several communication safe harbors, extending them to all issuers eligible to use Form S-3, regardless of exchange listing 732.

Under the revised framework, the Rule 139 safe harbor is universally expanded 163032. This rule permits broker-dealers participating in a syndicate to publish and distribute ongoing research reports regarding the issuer without those reports being legally classified as an "offer" of securities 43032. Previously restricted by float requirements, this expansion ensures that newly public and smaller companies can maintain vital analyst coverage during capital-raising windows, bolstering market liquidity and price discovery 4817. Similarly, all Form S-3 eligible issuers gain the ability to utilize Rule 433 free writing prospectuses without requiring the prior delivery of a statutory prospectus, and may utilize Rule 430B(b) mechanics to omit the specific identities and allocation amounts of selling securityholders from resale prospectuses until the actual time of sale 71632.

| Registration / Communication Benefit | Legacy Framework (Pre-2026) | Proposed 2026 Framework |

|---|---|---|

| Unlimited Primary Shelf Registration | 12 months reporting + $75M public float | Form S-3 Eligible (Current & Timely reporting only) |

| Broker-Dealer Research Safe Harbor (Rule 139) | Form S-3 Eligible ($75M float) | All Form S-3 Eligible Issuers |

| Omission of Selling Securityholders (Rule 430B(b)) | WKSI or Form S-3 Eligible | All Form S-3 Eligible Issuers |

| Free Writing Prospectus (Rule 433) w/o delivery | WKSI or Form S-3 Eligible | All Form S-3 Eligible Issuers |

| Pre-Filing Communications Flexibility (Rule 163) | WKSI Only ($700M float) | ELI and SELI |

| Pay-As-You-Go Registration Fees | WKSI Only | ELI and SELI |

| Add Securities via Post-Effective Amendment | WKSI Only | ELI and SELI |

| Automatic Shelf Registration (Rule 462) | WKSI Only | SELI Only (ELI + 12 months reporting) |

Strategic Implications for Newly Public Companies

The removal of the seasoning requirement and the implementation of the ELI framework fundamentally rewrite the post-IPO playbook for operating companies. Under the legacy rules, a newly public company faced a perilous 12-month "dead zone."

If the company required secondary capital, or if early venture capital investors wished to monetize their stakes following the expiration of the standard 180-day IPO lock-up, the company was constrained to highly rigid, high-friction methodologies 35.

Accelerated Transition to Shelf Registration

Previously, an issuer seeking to facilitate resales or conduct a follow-on offering within its first year was forced to file a Form S-1 registration statement 321. Because Form S-1 lacked forward incorporation by reference for unseasoned issuers, maintaining its legal validity required the constant drafting and filing of post-effective amendments corresponding to every new quarterly financial statement or material 8-K event 321. This process incurred massive legal and accounting fees and subjected the issuer to rolling windows of SEC staff review, during which no securities could be sold.

Under the 2026 proposal, a newly public company can file a comprehensive primary and resale shelf registration on Form S-3 immediately 91735. The Form S-3's evergreen forward incorporation by reference automatically pulls in subsequently filed Exchange Act reports, keeping the base prospectus legally current in perpetuity without manual intervention 2123. This fundamentally alters the corporate finance timeline, allowing companies to seamlessly transition from an IPO directly into a continuous shelf-based capital-raising model, executing rapid "takedowns" overnight when market pricing hits target valuations 92635.

The Democratization of At-The-Market Offerings

At-The-Market (ATM) offerings represent one of the most cost-effective capital formation strategies available to public companies. Rather than pricing a massive block of shares at a steep discount to secure an underwritten follow-on offering, an ATM program allows an issuer to sell newly issued shares directly into the secondary trading market incrementally, at prevailing market prices, utilizing a broker-dealer acting as an agent 14.

Under Rule 415(a)(4), ATM programs generally require the issuer to be explicitly eligible to use Form S-3 for primary offerings 1824. By eliminating the $75 million public float requirement and the 12-month seasoning period, the 2026 reform opens ATM access to a vast new population of micro-cap, small-cap, and newly public issuers 1527. A newly listed company could theoretically establish a comprehensive ATM program immediately following its IPO, allowing corporate treasurers to drip shares into the market to capture post-IPO volatility, thereby raising incremental capital without the severe dilution or negative signaling effects associated with traditional secondary offerings 11727.

Decreased Reliance on Dilutive Private Placements

The historical friction and delay associated with filing a Form S-1 frequently drove newly public or sub-$75 million float companies entirely out of the registered public markets. To secure capital swiftly to fund operations or acquisitions, these issuers relied heavily on Private Investments in Public Equity (PIPEs) or registered direct offerings structured around private placement exemptions like Rule 506 32136.

PIPE transactions inherently require issuers to sell equity at a steep discount to the current market price to compensate institutional investors for assuming illiquidity risk. Furthermore, PIPEs frequently involve the issuance of highly dilutive warrant coverage and require the company to commit to filing a resale Form S-1 post-closing anyway 336. By democratizing access to Form S-3 and the ELI framework, the SEC intends to make the registered public markets the path of least resistance. Affording smaller issuers the ability to raise capital instantly via shelf takedowns and ATMs reduces their cost of capital, tightens offering spreads, and protects retail shareholders from predatory private dilution 311.

Regulatory Parity for Former SPACs

Special Purpose Acquisition Companies (SPACs) have faced intense regulatory scrutiny and unique stigmas under federal securities laws. Historically, operating companies that bypassed a traditional IPO by merging with a SPAC (the "de-SPAC" process) were classified generically as "former shell companies" 1516. Under legacy rules, this classification triggered a draconian three-year lookback period. During this time, the post-de-SPAC operating company was branded an "ineligible issuer" and was broadly barred from utilizing Form S-3, achieving WKSI status, or accessing critical communication safe harbors 151637.

The 2026 Registered Offering Reform deliberately rectifies this disparity, treating former SPACs with parity to traditional IPOs 11537. The proposal explicitly states that provided the post-merger entity is no longer a shell company at the exact time it files the Form S-3, it will not be deemed a shell company solely because its predecessor was a SPAC 1315. This specific carve-out removes the three-year penalty box, allowing de-SPACed entities to file Form S-3 shelf registrations, initiate ATM programs, and qualify for ELI and SELI benefits on the exact same accelerated timeline as a conventional newly public enterprise 1516.

Modernization of Form S-1 and Federal Preemption

While the expansion of Form S-3 covers the vast majority of reporting issuers, the SEC also proposed highly technical modernizations to Form S-1. These changes assist companies that remain ineligible for short-form registration - such as those that failed to maintain timely reporting, missed the 7-day grace period, or fell into specific excluded categories 11728.

Expanding Incorporation by Reference in Form S-1

Prior to the 2026 proposal, the ability to utilize forward incorporation by reference in a Form S-1 was strictly limited to "smaller reporting companies" (SRCs) 2021. Furthermore, the ability to use backward incorporation by reference (pulling in historical filings to satisfy current disclosure) was strictly limited to issuers that had already filed at least one annual report on Form 10-K for their most recently completed fiscal year 11129.

The 2026 proposal drastically liberalizes these mechanics. It eliminates the requirement that an issuer must have filed an annual report to utilize backward incorporation 11129. Most impactfully, the SEC extends the privilege of forward incorporation by reference to all domestic issuers eligible to use Form S-1, provided they are not classified as blank check, shell, or penny stock issuers 1329.

This operational tweak effectively transforms Form S-1 into a continuous, automatically updating registration statement for standard offerings, heavily reducing repetitive drafting costs, legal fees, and the risk of inconsistencies between the prospectus and subsequent EDGAR filings 34. However, it is vital to emphasize a strict legal boundary: even with forward incorporation enabled, Form S-1 still cannot be used to conduct delayed primary shelf offerings under Rule 415(a)(1)(x), nor can it be used to host an At-The-Market program 3435. Those highly flexible mechanisms remain strictly the domain of Form S-3 635.

Universal Preemption of State Blue Sky Laws

One of the most universally praised logistical changes in the 2026 reform package is the proposal to fully preempt state-level securities registration and qualification laws - commonly known as "blue sky" laws - for all SEC-registered offerings 233.

Under Section 18(b) of the Securities Act, as amended by the National Securities Markets Improvement Act of 1996 (NSMIA), states are preempted from regulating "covered securities" 1538. Historically, covered securities were largely defined by exchange listing; preemption applied almost exclusively to securities listed, or approved for listing, on a national securities exchange 153338. Issuers of unlisted registered securities were forced to navigate a labyrinthine regulatory environment, undergoing expensive, fragmented, and time-consuming substantive merit reviews in up to 50 individual state jurisdictions 17.

To eliminate this friction, the SEC proposed leveraging its statutory authority under Section 18(b)(3) to redefine the term "qualified purchaser." Under the proposed definition, a qualified purchaser includes any person to whom securities are offered or sold in a federally registered offering 111533. This administrative action automatically grants covered-security status to all registered offerings, fully and immediately preempting state blue sky registration requirements nationwide 41538.

This preemption represents a massive structural cost-saving measure for entities that operate outside the national exchange system. Non-listed Business Development Companies (BDCs), non-traded Real Estate Investment Trusts (REITs), issuers of Special Purpose Acquisition Rights Company (SPARC) rights, and companies issuing unlisted tokenized securities will now face a single, unified federal regulatory clearance path 11115. In standard statutory fashion, individual states explicitly retain their antifraud enforcement jurisdiction and their right to collect requisite notice filings and fees 115.

Investor Protection Safeguards and Exclusions

The systemic elimination of seasoning periods and public float thresholds removes highly objective, market-based proxies for an issuer's systemic stability and the depth of its market following. Acknowledging the inherent risk that less mature, highly volatile, or structurally opaque companies might abuse these newly expedited offering frameworks, the SEC instituted strict, targeted guardrails aimed at maintaining robust investor protection 1315.

The Strict Prohibition of BSP Issuers

To prevent speculative ventures and micro-cap bad actors from co-opting the shelf registration process to execute pump-and-dump schemes, the SEC established a new, highly restricted exclusionary category termed the "BSP issuer." This acronym encompasses blank check companies, shell companies (explicitly excluding business combination related shell companies), and penny stock issuers 3715.

Under the 2026 proposal, BSP issuers are strictly and universally prohibited from using Form S-3 315. Furthermore, they are barred from utilizing the new forward incorporation by reference accommodations on Form S-1, and they are categorically disqualified from accessing any of the enhanced registration or communication benefits associated with the ELI or SELI tiers 14.

Similarly, the SEC integrated the existing "ineligible issuer" concept directly into the baseline Form S-3 eligibility requirements. Issuers that have committed specified criminal violations, those facing recent SEC cease-and-desist orders for antifraud violations, or those subject to stop orders are barred 3738. Loss of Form S-3 eligibility for enforcement or qualitative reasons is a much harsher penalty under the 2026 rules than it was historically; whereas it previously only stripped a company of top-tier WKSI benefits, it now cuts off basic shelf access entirely, severing a company's primary lifeline to public capital 24.

Geographic Constraints on At-The-Market Programs

Because ATM programs involve continuous algorithmic sales directly into the secondary market, they require a deep, highly liquid trading environment. Without sufficient depth, the continuous issuance of shares can artificially collapse the stock price, harming existing retail shareholders 13. With Form S-3 eligibility slated to expand by an estimated 60 percent, thousands of thinly traded, unlisted micro-cap stocks would theoretically gain access to the ATM mechanism 1828.

To address these market structure and investor protection concerns, the SEC proposed amending Rule 415(a)(4) to severely restrict the geographic execution of ATM offerings. Under the revised rule, ATMs are limited strictly to securities that are listed and traded on a national securities exchange, or traded in specific unlisted markets affirmatively designated by the SEC 1518. The Commission outlined specific qualitative criteria for these designated markets, including mandatory information-reporting standards, minimum bid-price requirements, and minimum public-float requirements 317. The SEC explicitly noted that the OTCQX Best Market and OTCQB Venture Market tiers of the OTC Link ATS likely possess the requisite attributes to be designated as acceptable markets, while lower-tier, highly opaque "pink sheet" securities remain entirely excluded from ATM execution 11115.

The Exclusion of Foreign Private Issuers

Notably, the comprehensive 2026 Registered Offering Reform applies exclusively to domestic registrants; Foreign Private Issuers (FPIs) are expressly carved out of the proposal 71539. Under the draft rules, all FPIs are completely prohibited from using the newly modernized Form S-3 and Form S-1. This prohibition applies even if the FPI voluntarily elects to report on domestic forms (e.g., filing standard 10-Ks and 10-Qs instead of the FPI-specific 20-F) 7. FPIs must continue to rely on the legacy Form F-3 and Form F-1 structures, and the historical WKSI framework is retained entirely intact strictly for their use 1539.

This deliberate bifurcation is not a permanent policy statement but rather a procedural pause stemming from the SEC's June 2025 FPI Concept Release 263940. Following a comprehensive demographic review, the SEC noted severe, structural shifts in the non-U.S. issuer population. In 2003, when many FPI accommodations were codified, most FPIs were Canadian or British firms facing substantive, parallel regulation in mature home-country markets 404041. By 2023, the plurality of FPIs were incorporated in the Cayman Islands, headquartered in China, and traded exclusively on U.S. exchanges 4040. Because these entities effectively escape meaningful home-country oversight while still enjoying U.S. regulatory accommodations designed for dual-listed companies, the SEC is actively weighing whether to implement a "foreign trading volume test" or require FPIs to maintain a listing on a "major foreign exchange" to retain their status 4041. Consequently, the Commission opted to freeze the existing offering framework for FPIs until that parallel, highly complex regulatory overhaul is completed 3940.

Conclusion

The SEC's 2026 Registered Offering Reform signals a definitive regulatory paradigm shift, prioritizing real-time disclosure compliance and technological integration over historical metrics of issuer size, public float, and tenure. By eliminating the Form S-3 seasoning and public float requirements, the Commission has effectively collapsed the post-IPO capital-raising timeline. This structural compression grants newly public and smaller reporting companies unprecedented agility to access public capital, seamlessly transitioning from rigid Form S-1 resale registrations to evergreen shelf registrations and continuous At-The-Market programs. Furthermore, the transition from the legacy WKSI regime to the Eligible Listed Issuer and Seasoned Eligible Listed Issuer tiers democratizes top-tier offering flexibilities, properly rewarding exchange-listed issuers with frictionless market access regardless of their market capitalization.

Simultaneously, the proposal executes a careful balancing act regarding systemic stability and investor protection. By instituting strict statutory prohibitions against blank check, shell, and penny stock issuers, limiting ATM offerings to vetted, liquid trading markets, and enforcing rigid consequences for delinquent Exchange Act reporting, the SEC aims to sequester these powerful capital formation tools from the most volatile, opaque segments of the market. The universal preemption of state blue sky laws for all registered offerings further centralizes federal oversight and slashes compliance friction for non-traditional products, creating a more unified national market system. As market participants, legal advisors, and corporate issuers prepare for final adoption and implementation - projected for early 2027 - these sweeping reforms stand to fundamentally reshape the calculus of going public, theoretically making the U.S. registered equity markets more attractive, fluid, and responsive to modern macroeconomic realities.