Disruptive Innovation in Agricultural Systems and Digital Platforms

Fundamentals of Disruptive Innovation Theory

The theory of disruptive innovation, initially articulated by academic researchers led by Clayton Christensen in the mid-1990s, provides a rigorous economic framework for understanding how seemingly robust, well-managed incumbent firms lose market dominance to entrants utilizing fundamentally different business models or technological trajectories 11. In broad corporate discourse, the term "disruption" is frequently misapplied to any breakthrough technology, rapid market shift, or successful startup. However, the theoretical definition is highly specific: a disruptive innovation is a process whereby a smaller enterprise with fewer resources successfully challenges established businesses by initially targeting overlooked or entirely new segments 23.

To apply this theory to modern agricultural technology, it is necessary to differentiate between sustaining and disruptive innovations. Sustaining innovations improve existing products along dimensions of performance that mainstream, high-end customers have historically valued 46. The motivating factor for an incumbent pursuing a sustaining innovation is profit maximization; by creating superior products for their most demanding customers, a business can pursue ever-higher profit margins 5. Established competitors almost universally win the battles of sustaining innovation because they possess the capital, engineering resources, and established customer bases required to out-execute new entrants 466.

Mechanisms of Disruptive Trajectories

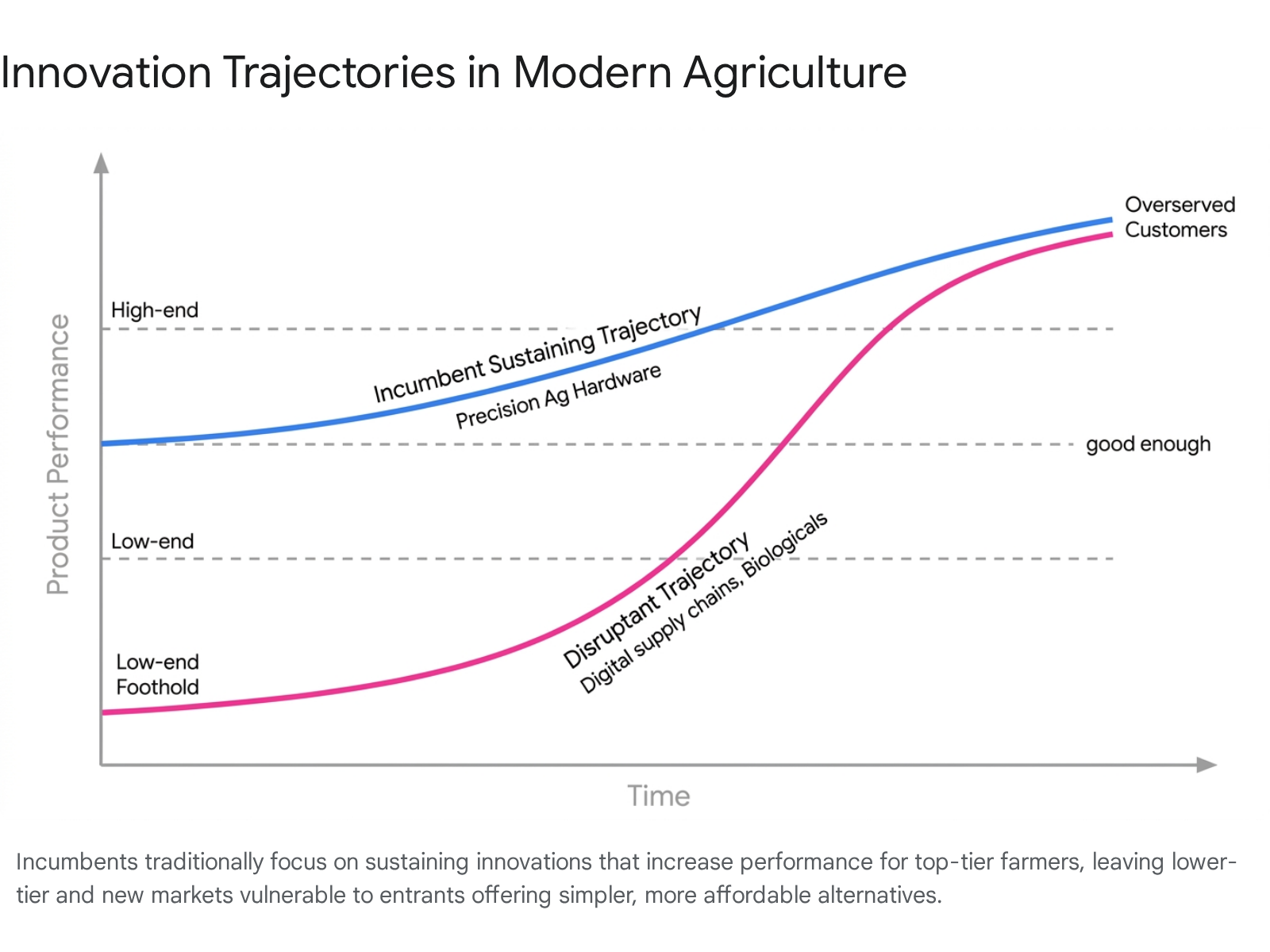

Disruptive innovations, conversely, follow a divergent trajectory. They do not initially attempt to compete with incumbent products on traditional performance metrics. Instead, they offer solutions that are often technologically inferior by established industry standards but introduce novel benefits such as affordability, simplicity, convenience, or accessibility 16. The theory posits that disruption typically occurs through two distinct market footholds.

The first pathway is the low-end foothold. Low-end disruption occurs when incumbents continuously improve their products to the point that they overshoot the performance requirements of their less demanding customers 17. Disruptors enter by providing a "good enough" product at a lower cost, operating on a highly efficient business model that yields attractive margins at discount prices 13. The second pathway is the new-market foothold. These disruptions target "non-consumers" - individuals or entities who previously lacked the financial capital, access, or technical expertise to participate in a market, thereby creating an entirely new value network 378.

Because disruptive innovations initially generate lower profit margins in smaller or unproven markets, incumbent market leaders are rationally motivated to ignore them, focusing instead on their highly profitable core clientele 16. As disruptors systematically improve their offerings over time, they relentlessly move upmarket. Disruption is ultimately achieved when the entrant's product performance meets the standards of mainstream customers, allowing the entrant to displace established competitors using its lower-cost or structurally superior business model 13. In the context of global agriculture, identifying which technologies represent sustaining improvements versus actual disruptive threats is critical for forecasting shifts in value capture among heavy equipment manufacturers, chemical suppliers, and input distributors.

Precision Agriculture as a Sustaining Innovation

The prevailing narrative surrounding precision agriculture - encompassing global positioning systems (GPS), automated machinery, drone-assisted monitoring, soil and crop sensors, and variable-rate technology (VRT) - often mischaracterizes these advancements as disruptive 11910. Evaluated strictly through the lens of innovation theory, precision agriculture functions overwhelmingly as a sustaining innovation for incumbent agricultural equipment manufacturers 1112.

Hardware and Digital Integration by Incumbents

Large-scale equipment providers such as John Deere and AGCO have leveraged the Internet of Things (IoT), artificial intelligence (AI), and advanced robotics to create better-performing, higher-margin products designed for their most demanding, well-capitalized customers: large commercial farming operations 161718. These technologies do not redefine the fundamental business model of equipment manufacturing or open agriculture to non-consumers. Rather, they entrench the dominance of major manufacturers by raising the barrier to entry and extending the performance trajectory of traditional heavy machinery 411.

The sophistication of these sustaining innovations is substantial, driving measurable gains in resource efficiency and yield protection. For instance, John Deere's "See & Spray" technology utilizes boom-mounted cameras and onboard processors capable of scanning over 2,500 square feet per second at speeds up to 15 miles per hour 191314. By identifying individual weeds and triggering distinct spray nozzles (via the ExactApply system), the machinery applies herbicides precisely to target plants rather than indiscriminately broadcasting chemicals across an entire field 1914.

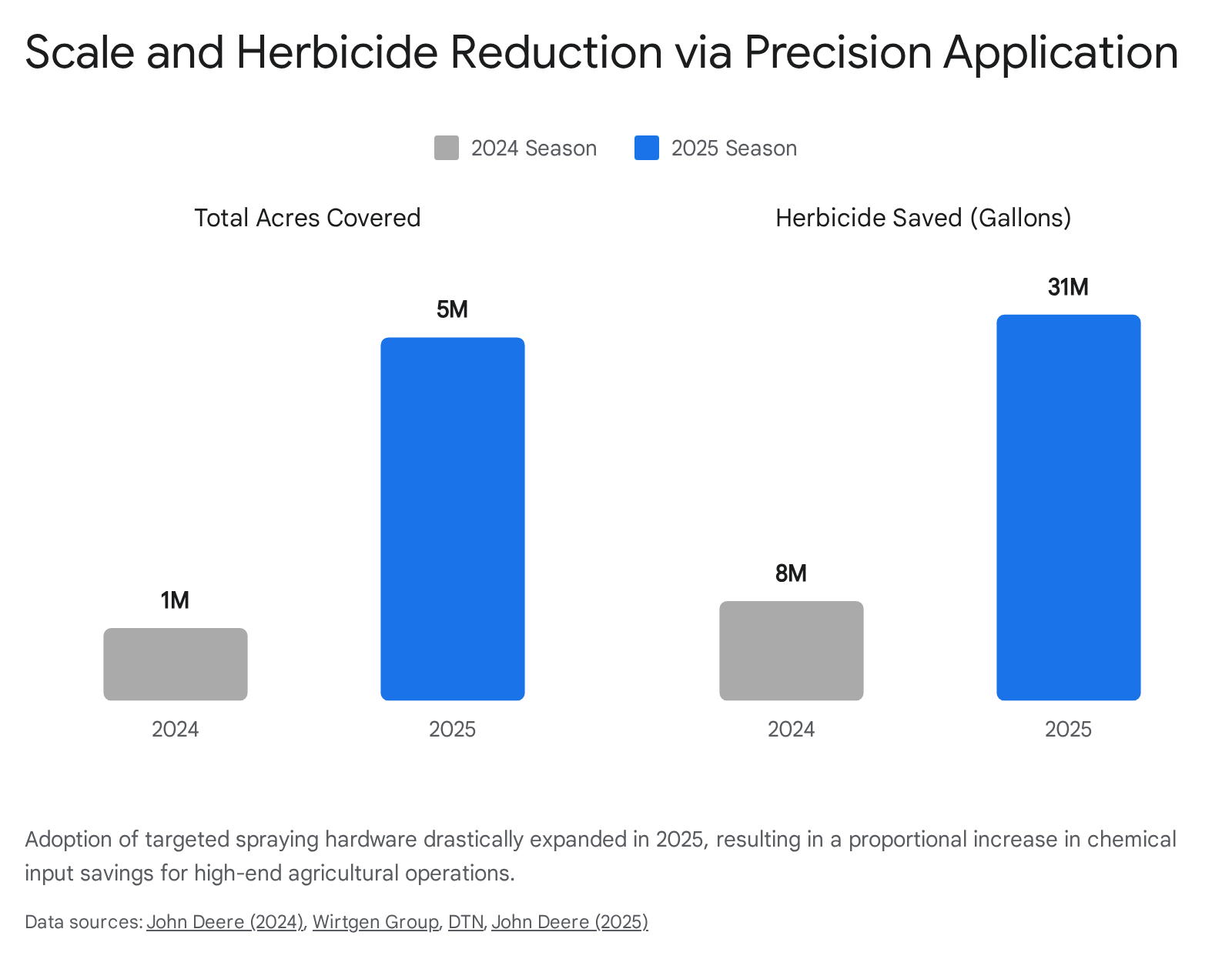

The adoption scale and efficiency metrics of this technology emphasize its sustaining nature. In 2024, the technology covered over 1 million acres, saving an estimated 8 million gallons of herbicide mix and demonstrating an average herbicide savings of 59% on corn, soybean, and cotton fields 1922. By the 2025 growing season, adoption expanded dramatically, with the technology utilized across 5 million acres of farmland 1314. During this period, users reduced non-residual herbicide use by an average of nearly 50%, resulting in savings of approximately 31 million gallons of herbicide mix 1314.

Furthermore, third-party field studies demonstrated that this targeted application reduced crop injury, yielding an average increase of 2 bushels per acre in soybeans, with upper-range performance reaching 4.8 additional bushels per acre 1423.

These are classic sustaining improvements: they optimize yield, increase operational speed, and improve input efficiency for existing high-end customers who can afford premium equipment or expensive carbon-fiber boom retrofit kits 101122. The high capital cost and sophisticated operational requirements of such machinery deliberately target the upper tiers of the market, reinforcing the incumbent's pricing power and profit margins without disrupting the core business of selling and maintaining heavy agricultural equipment.

Dealership Network Evolution

The dealership networks that distribute and maintain agricultural equipment are simultaneously adapting to this sustaining technology trajectory. Historically reliant on margin capture from the sale and mechanical repair of new heavy machinery, dealerships are currently facing complex macroeconomic headwinds. Higher interest rates - which rose by an average of 1.5% to 2.0% in 2024 - and lower commodity prices have significantly depressed new equipment sales and discouraged massive capital investments by farmers 2425. For example, in 2025, AGCO reported a net sales decline of 4.7% in its third quarter, with the most significant sales declines occurring in high-horsepower tractors and combines across North America 13.

Despite these challenges in traditional hardware movement, precision agriculture technology sales have provided a crucial stabilizing effect for equipment dealerships 2426. According to the 2025 Precision Farming Dealer Benchmark Study, over 49% of surveyed dealers reported an increase in total precision revenue, compared to only 27% the prior year 26. While over half of the dealers surveyed estimated their total precision revenue was $500,000 or less, 11% reported between $2 million and $3 million, and 4% brought in more than $5 million 26. Notably, hardware sales represented 50% of this total precision revenue, with service and support accounting for 20% 26.

As physical machinery becomes more durable and farmers hold assets longer due to budget constraints, dealerships are transitioning from hardware merchants to technology consultants, data advisors, and sustainability partners 1626. This transition involves expanding high-quality pre-owned machinery programs, offering subscription-based Agriculture Technology-as-a-Service (Agri-TaaS) models, facilitating drone leasing, and providing predictive maintenance software 161724. In this environment, the dealership remains highly relevant to the high-end farmer, sustaining the incumbent distribution network by actively shifting the organizational value proposition from mechanical steel to integrated silicon and software services.

Asymmetric Disruption of Chemical Incumbents

While advanced precision agriculture functions as a sustaining innovation for hardware manufacturers, it simultaneously acts as a profound disruptive force against incumbent agricultural chemical companies (such as Bayer, BASF, and Syngenta). This dynamic represents a powerful example of asymmetric disruption, wherein a technology that sustains and enhances one sector inadvertently destroys the foundational business model of an adjacent sector 191528.

Demand Destruction via Precision Application

The traditional business model of agrochemical incumbents is intrinsically reliant on immense volume: the mass production, distribution, and whole-field broadcast application of broad-spectrum herbicides, pesticides, and fertilizers 15. The economics of synthetic chemistry dictate this volume dependency. Developing a new chemical active ingredient is a highly capital-intensive endeavor, currently costing over $300 million and requiring a 12-year research, development, and regulatory approval cycle 15. Furthermore, the industry is facing rising regulatory hurdles and declining success rates in countering growing pest resistance 15. To recoup these massive investments, major chemical companies must prioritize broad-spectrum products with massive global market potential, essentially banking on farmers indiscriminately applying these chemicals across entire fields 15.

Precision agriculture fundamentally undermines this volume-dependent paradigm. By transitioning from whole-field broadcast spraying to plant-specific micro-dosing, tools like autonomous robotic weeders and intelligent sprayer booms functionally destroy chemical demand. As precision application scales across millions of acres, the reported 50% to 76% reduction in herbicide volume applied directly translates to a proportional contraction in revenue for chemical suppliers on those acres 191322. For chemical incumbents, this is not a technological failing of their specific herbicide formulations, but a structural collapse of their revenue mechanism. As the market for bulk, non-targeted agricultural chemicals inevitably contracts, the high-fixed-cost R&D models of legacy chemical giants become increasingly unsustainable 1415.

The Emergence of Biological Inputs

Compounding the threat of precision application is the rapid rise of agricultural biologicals - a diverse class of crop protection and enhancement products derived from natural materials such as bacteria, yeast, plants, and minerals 1528. The shift toward biologicals represents a textbook example of a disruptive innovation entering from the margins and scaling upward.

Historically, biologicals were viewed by mainstream agribusiness as inferior to synthetic chemicals. They possessed shorter shelf lives, variable efficacy depending on environmental conditions, and narrower spectrums of control 152930. Consequently, they were attractive primarily to niche organic markets, high-value specialty crops, or utilized merely as a last resort 1529. Following the patterns predicted by disruptive innovation theory, major agrochemical incumbents largely ignored these biological alternatives for decades, focusing their capital instead on highly profitable, broad-spectrum synthetics to serve their most demanding, high-yield customers 11529.

However, recent advancements in synthetic biology, artificial intelligence in bioprospecting, and advanced industrial fermentation have rapidly improved the performance, stability, and formulation of biological products 283016. The agricultural biotechnology sector has transitioned from a focus on intellectual property and patent coding to a "Biological-Industrial" model focused on high-throughput physical infrastructure and automated R&D hubs required to scale production 32. Startups leveraging these technologies - such as Living Models, which uses AI to interpret DNA as a language to accelerate seed development, or Tropic, which secured $105 million to scale gene-edited crop production - are compressing commercialization timelines from twelve years down to under five years 32.

Furthermore, biologicals face substantially lower regulatory hurdles compared to synthetic chemistries, allowing manufacturers to bring innovations to market with much greater speed and agility 30. As the performance of biological seed treatments, biostimulants, and bioinsecticides becomes "good enough" for mainstream row-crop farmers, they are steadily moving upmarket 37.

| Input Characteristic | Traditional Synthetic Chemicals | Emerging Biological Inputs |

|---|---|---|

| Development Cost & Time | High capital requirement (>$300M); 12-year average commercialization cycle 1532. | Lower capital threshold; commercialization compressed to under 5 years 3032. |

| Application Mechanism | Broad-spectrum; historically reliant on volume-heavy broadcast application 1415. | Highly targeted; enhances soil microbiomes and integrates with precision micro-dosing 1529. |

| Regulatory Environment | High friction; increasing regulatory hurdles and public scrutiny regarding environmental impact 1529. | Lower friction; naturally derived materials face streamlined regulatory pathways 2930. |

| Market Trajectory | Mature market; growth rate of approximately 3.7% annually; facing generic commoditization 1533. | Disruptive growth phase; 13.8% annual growth rate; expanding from specialty to row crops 3033. |

Biologicals are now positioned as essential tools that enhance root development, nutrient uptake, and stress tolerance, integrating seamlessly into modern sustainability and regenerative agriculture frameworks 152934. The global market for biologicals, currently estimated at $9 billion to $15 billion, is projected to reach $25 billion by 2035, capturing up to 25% of the overall global crop protection market 3033. This growth represents a direct capture of market share from synthetic chemical inputs. Unable to justify the massive R&D costs for traditional chemicals in a shrinking volume market, legacy chemical firms are being forced to restructure their portfolios or attempt expensive, late-stage acquisitions of the deep-biotech startups that have already secured a foothold 151632.

Transformation of Agricultural Logistics and Distribution

Beyond the manufacturing of physical inputs, the theory of disruptive innovation is aggressively reshaping agricultural distribution and supply chain logistics. Traditional agricultural networks are heavily layered, relying on a deeply entrenched cascade of intermediaries - commission agents, regional wholesalers, sub-wholesalers, and localized retail storefronts 173618.

Inefficiencies of Traditional Supply Chains

The traditional multi-tiered supply chain suffers from severe structural and economic inefficiencies. Information asymmetry and a lack of real-time tracking lead to poor demand forecasting, excessive inventory buffers, and highly volatile pricing 18193920. For farmers, this fragmentation results in a system where they bear the brunt of price risk while capturing only a marginal fraction of the consumer food dollar 4121.

Furthermore, for perishable goods such as fresh fruits and vegetables, the extended transit time required to navigate various middlemen results in staggering post-harvest losses. Globally, post-harvest loss rates during storage and transportation are estimated at 25% to 30%, primarily due to inconsistent temperature control, poor packaging, and fragmented cold-chain infrastructure 173943. Incumbents within this system - such as regional wholesalers and cooperative distributors - have historically relied on these structural frictions to justify their margins, aggregating fragmented supply from smallholder farmers and routing it to fragmented demand at the retail level 3618.

Digital Marketplace Intermediation

Digital platforms and AgTech e-commerce entities are disrupting this model by enabling direct-to-farm (B2B) or farm-to-consumer (B2C) value chains. These platforms function as classic new-market disruptors: they introduce unprecedented operational transparency and algorithmic efficiency, initially capturing low-margin, high-friction transactions before scaling upmarket to dominate broader market segments 173622. The global e-commerce market for agricultural products, valued at $46.52 billion in 2025, is projected to reach $116.23 billion by 2035, driven by a compound annual growth rate (CAGR) of 9.6% 23.

In the input sector, platforms like Farmers Business Network (FBN) apply standard digital retail principles to agricultural supplies 162223. By offering price transparency and direct procurement, they bypass traditional brick-and-mortar agricultural retailers, lowering operational costs for farmers but actively squeezing the margins of local incumbent dealers 224624.

In the output sector - distributing farm produce directly to buyers - companies like Pinduoduo in China and NinjaCart in India demonstrate the transformative economic power of digital logistics, significantly altering market dynamics in developing and hyper-scaled agricultural economies.

Supply Chain Optimization in China Pinduoduo has revolutionized agricultural distribution in China through a direct procurement model utilizing its "Farmland Cloud Group Buying" and "Duoduo Grocery" systems 172526. By shifting from the traditional e-commerce model of consumers searching for products to products algorithmically finding consumers, Pinduoduo connects farmers directly with end-users and community convenience stores 172526. By completely bypassing traditional wholesalers, Pinduoduo has demonstrably shortened the supply chain. Empirical data indicates that this model increases farmers' incomes by an average of 10% to 15% while simultaneously reducing consumer prices by approximately 5% 1726. The integration of predictive AI and big data aligns supply directly with hyper-local demand, effectively minimizing the need for extended cold-chain warehousing and ensuring rapid next-day fulfillment 172527.

Agri-Tech Logistics in India Operating within India's highly complex agricultural market, NinjaCart moves over 1,400 tonnes of fresh produce daily, directly connecting more than 20,000 farmers to 60,000 retailers 39. Through the implementation of a proprietary enterprise resource planning (ERP) system named BiFrost, integrated RFID traceability, and advanced demand forecasting algorithms, NinjaCart has reduced agricultural supply chain wastage from a traditional industry average of 25% down to just 4% 3941. This massive logistics efficiency allows the platform to pay farmers roughly 20% more revenue than traditional mandi (wholesale market) systems 3951. Furthermore, the platform ensures transparent, same-day digital payments, eliminating the farmer's historical reliance on high-interest local money lenders 394128.

| Supply Chain Metric | Traditional Agricultural Supply Chain | Digital / Direct-to-Farm Platforms (e.g., NinjaCart, Pinduoduo) |

|---|---|---|

| Intermediation Layer | Highly fragmented; relies on multiple commission agents, wholesalers, and physical retailers 173618. | Direct connection between producer and end-retailer/consumer; bypasses physical middlemen 252629. |

| Information Flow | Asymmetric; poor demand forecasting; reliance on historical intuition and localized knowledge 3941. | Symmetric and transparent; AI-driven predictive analytics; real-time pricing and market visibility 392526. |

| Post-Harvest Loss | Extremely high; up to 25% - 30% spoilage due to delays, excessive handling, and cold-chain gaps 173943. | Dramatically reduced; approximately 4% wastage due to optimized routing and rapid clearing of inventory 3941. |

| Farmer Compensation | Low value capture; margins are eroded by intermediary fees and delayed payment cycles 412129. | Increased by 10% - 20%; rapid or same-day digital payments mitigate credit dependency 173941. |

| Logistics Mechanism | Decentralized, uncoordinated freight; high incidence of empty backhauls 1819. | Integrated network; IoT/GPS tracking; algorithmic load consolidation and route optimization 18414325. |

The comparative advantages of these digitally integrated direct-to-farm supply chains over traditional models highlight an existential threat to traditional distribution intermediaries. By fundamentally altering the cost structure and efficiency of getting agricultural goods to market, digital platforms operate as quintessential disruptors, redefining the value network of the agricultural economy.

Data Governance and Incumbent Defense Mechanisms

As physical inputs - both hardware and chemicals - become commoditized or subject to demand destruction, digital data has emerged as the most critical and highly contested asset class in modern agricultural value chains 3031. The control, ownership, and monetization of farm-level data sit at the absolute center of the struggle between new disruptive platforms and legacy incumbent businesses.

Farm Data Typologies and Ownership Conflicts

The data generated by a modern farming operation can be categorized into a hierarchical structure. At the base are environmental facts, such as raw rainfall or soil moisture levels. Above this sits agricultural operational data, representing the specific choices a farmer makes regarding planting rates, chemical applications, and harvest timing. At the apex is business data - the highly valuable, aggregated intelligence that technology companies utilize to train predictive algorithms and optimize supply chains 30. Furthermore, legal frameworks differentiate between "small data," which originates directly from an individual farm, and "big data," which is formed when tech companies aggregate small data across thousands of operations and combine it with macro-economic and meteorological inputs 32.

In the pursuit of maintaining market dominance, agricultural technology providers (ATPs) such as John Deere, Bayer (through its Climate FieldView platform), and Syngenta extract massive volumes of this agronomic data from their hardware and software ecosystems 32. While the philosophical and legal ownership of the raw data technically resides with the farmer, standard user agreements routinely grant ATPs broad, irrevocable rights to aggregate, analyze, and monetize the anonymized information 3032. By aggregating this intelligence, incumbents create powerful predictive engines that effectively lock farmers into their proprietary ecosystems. This strategy creates a massive data moat that is exceptionally difficult for new, smaller entrants to cross, solidifying the incumbent's position against potential digital disruption 3032.

Digital Platform Data Cooperatives

Conversely, digital disruptors are pioneering new models of data governance to break incumbent monopolies. Platforms like Farmers Business Network (FBN) operate on a contributory, cooperative data model 24. FBN aggregates crowdsourced pricing and agronomic performance data to provide unprecedented price transparency to the farmer, fundamentally challenging the historically opaque pricing structures of traditional input retailers 2433. To build trust and encourage data sharing, the FBN model explicitly prohibits the sale of member data to third-party data brokers, utilizing the aggregated insights solely to empower the farmer's purchasing and operational decisions 2433. FBN also adheres to the "Ag Data Transparent" certification, a set of industry principles ensuring safety, usability, and transparency guidelines regarding data collection and access 3334.

Simultaneously, advanced privacy-preserving technologies are emerging from academic and non-profit sectors to combat data exploitation while still fostering innovation. Initiatives such as the Food Security Sandbox (FSS), developed at Case Western Reserve University, utilize sophisticated cryptographic techniques including federated learning, differential privacy, and principal component analysis 35. These frameworks allow researchers and independent startups to build highly accurate predictive agricultural models - such as yield estimation or disease detection tools - without ever exposing the raw, sensitive data of individual farmers 35. By securing data at the source, these technologies have the potential to democratize AI development, lowering the barrier to entry for new disruptive entrants while protecting farmer sovereignty 35.

Cooperative Capital Defense Strategies

Faced with the dual threats of digital disintermediation and data monopolization, traditional agricultural retailers and localized cooperatives are not remaining passive. Recognizing that the trusted, hyper-local relationship between the agronomist and the farmer is their primary surviving competitive advantage, legacy incumbents are aggressively evolving their business models to internalize disruptive innovation rather than fight it directly 3637.

A prominent example of this strategic pivot is Land O'Lakes, one of the largest agricultural cooperatives in the United States. In late 2025, Land O'Lakes, in conjunction with several major regional cooperative partners including Keystone Cooperative, Central Valley Ag, and Alabama Farmers Cooperative, launched "AgRogue Growth Partners" 3637. Managed by the specialized venture capital firm Radicle Growth, this initiative pools approximately $100 million in capital to invest up to $7 million each in 10 to 15 early-stage AgTech companies 376263.

Crucially, this initiative operates as a hybridized defense strategy rather than traditional corporate venture capital. Agricultural startups historically face immense friction achieving adoption at the "farm gate" due to a lack of distribution infrastructure 3637. AgRogue directly addresses this bottleneck by utilizing the cooperative's vast, established network of over 800 retail partners to validate, field-trial, and rapidly scale the startups' innovations 6263. By directly investing in potential disruptors - focusing specifically on crop inputs, digital supply chains, and new business models - and leveraging retail trust to guarantee market access, the cooperative incumbents ensure they remain the primary conduit of technology to the farmer 376263. This proactive model effectively co-opts the mechanisms of disruption, securing the future relevance of legacy distribution networks within a rapidly digitizing agricultural economy.