Disruptive innovation in professional services firms

Theoretical Foundations of Disruptive Innovation

The theory of disruptive innovation, originally articulated by Clayton Christensen, describes a process wherein new market entrants target overlooked, overserved, or low-end segments with simpler, more accessible, and lower-cost solutions before systematically moving upmarket to challenge established incumbents 123. Historically, classical professional services firms (PSFs) - such as major law firms, elite management consultancies, and global accounting networks - have remained highly insulated from classical disruption 4. Their structural reliance on highly educated human capital, strict regulatory licensing requirements, deeply entrenched corporate relationships, and opaque value delivery mechanisms created substantial barriers to entry 45.

However, recent technological advancements have fundamentally altered the economic scaffolding of professional services. The deployment of advanced generative artificial intelligence (GenAI) and multi-agent workflows has initiated a structural reconfiguration across the legal, consulting, and accounting sectors. Analysis indicates that disruptive innovation accounts for approximately 70% of innovation-led returns, compared to merely 10% for sustaining innovations, making the current technological shift highly destabilizing for incumbents 3.

Sustaining Versus Disruptive Mechanisms

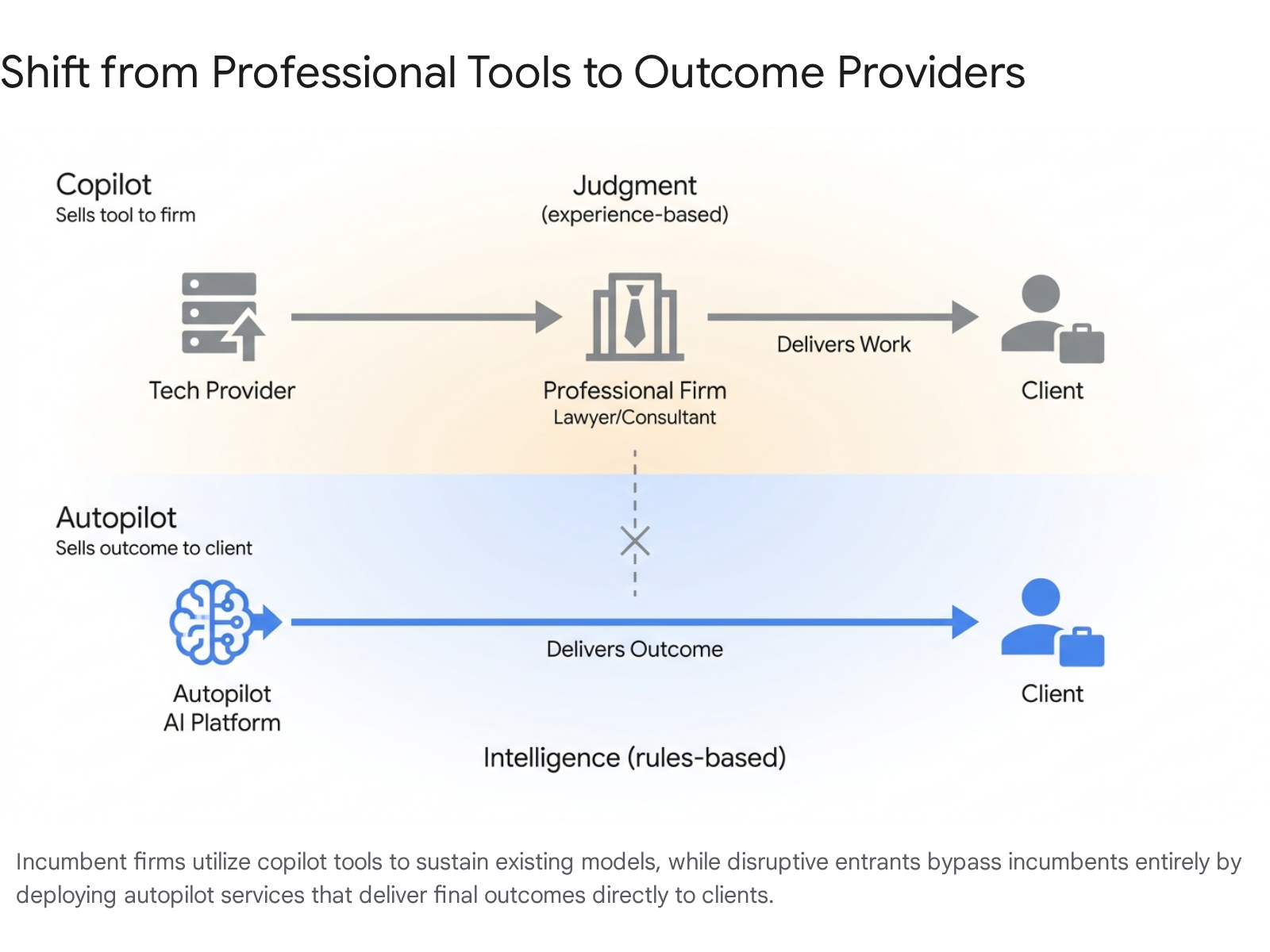

Innovation within professional services currently follows two distinct operational trajectories. Sustaining innovation focuses on maintaining and enhancing the existing products, services, and operational models of incumbent organizations to meet evolving customer needs 66. In the context of PSFs, this manifests primarily as the deployment of "copilot" technologies. Copilots are advanced software tools sold directly to professionals (e.g., lawyers, consultants, or accountants) to increase their individual productivity while preserving the traditional billing paradigms and organizational hierarchies of the firm 87. Incumbent firms utilize these tools to defend their market position, improve margins, and optimize internal processes without fundamentally altering their core value proposition 68.

Conversely, disruptive innovation in professional services is currently characterized by the emergence of "autopilot" or outcome-based models. Rather than selling software to an incumbent firm to make its employees more efficient, autopilot entrants sell the completed, finalized work directly to the end client 1112.

This model bypasses the traditional intermediary entirely. Because autopilot models treat AI improvements as margin-expanding advantages rather than competitive threats, they possess a fundamentally different cost structure. This enables them to underprice traditional firms while maintaining high profitability, initiating disruption from the bottom up 71112.

For technology startups and software vendors servicing the professional sectors, the transition from providing copilots to launching autopilots is a critical strategic inflection point 87. A startup building a copilot faces a strict innovator's dilemma: their software merely makes the incumbent more efficient, and their product differentiation is constantly threatened by rapid improvements in foundational large language models (LLMs) 71213. Autopilot firms, however, utilize AI not as an auxiliary feature, but as the core engine of labor substitution 711.

The Intelligence Versus Judgment Continuum

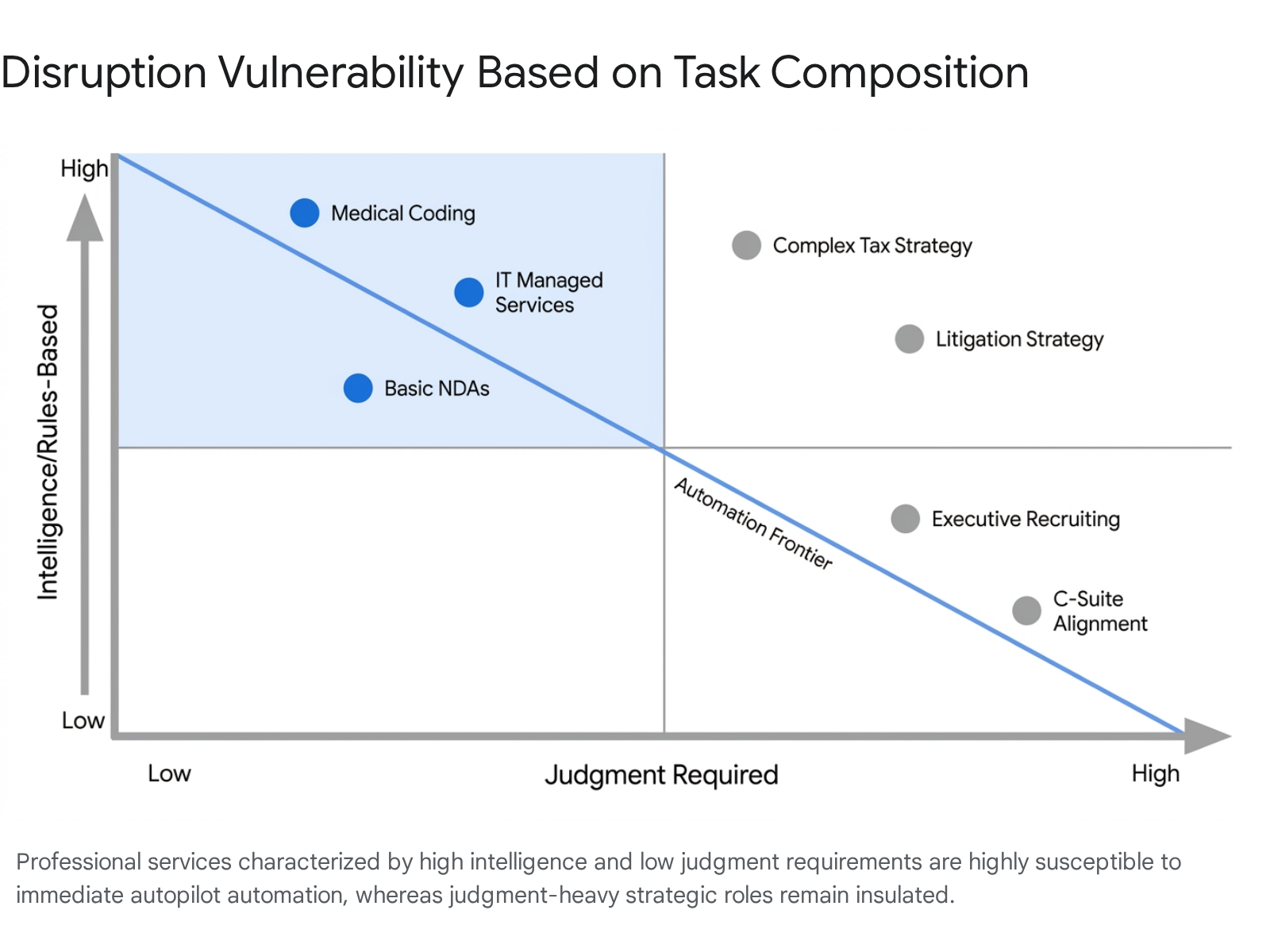

The vulnerability of a given professional service to technological disruption is largely determined by its position on a continuum between "intelligence" and "judgment" 712.

Intelligence, in this economic framework, refers to complex but fundamentally codifiable, rules-based cognitive labor 712. Examples include translating clinical notes into standardized ICD-10 medical billing codes, structuring financial data, conducting regulatory landscape research, reviewing standard non-disclosure agreements (NDAs) against clause libraries, or executing routine IT managed services tasks 71214. Judgment, by contrast, requires experiential intuition, emotional intelligence, taste, and the synthesis of highly ambiguous variables 712. Examples of judgment include aligning corporate stakeholders around a strategic pivot, assessing cultural fit during an executive search, or structuring a multi-layered commercial negotiation 7119.

Software engineering was the first professional category to experience systemic AI integration because coding - translating specifications into functional logic - is predominantly an intelligence-based task 710. Generative AI systems have now crossed the capability threshold required to autonomously execute intelligence-heavy tasks across other verticals 7. Consequently, professional services heavily weighted toward intelligence are experiencing the most acute disruption, as autonomous agents capture low-end and mid-market outsourced functions 12.

Over time, as these systems ingest vast amounts of proprietary data regarding successful outcomes, the theoretical frontier between intelligence and judgment will shift. As AI models accumulate domain-specific data detailing what good judgment looks like, disruptive entrants will incrementally automate increasingly complex advisory functions, pushing the boundary of what requires human intervention 712.

Disruption in Management Consulting

The management consulting industry, estimated at $350 billion globally, has traditionally relied upon a standard and highly lucrative value chain: research, analysis, framework application, presentation generation, and client management 11. For decades, elite firms like McKinsey & Company, Boston Consulting Group (BCG), and Bain & Company (collectively referred to as MBB) executed the first four layers of this chain by deploying large teams of junior analysts and associates 11.

The Traditional Value Chain and Vulnerability

The foundation of every traditional consulting engagement is research - including market sizing, competitive analysis, regulatory landscape reviews, and industry benchmarking 11. At legacy firms, this labor is performed primarily by Business Analysts and first-year Associates, who historically spent 30% to 50% of their working hours gathering, cleaning, and organizing information 11.

This layer of the value chain faces a projected AI automation exposure exceeding 90% 11. AI systems deployed by 2026 can perform this foundational intelligence work at a quality level that meets or exceeds the median junior consultant, doing so at a marginal cost approaching zero 11. The irony of this disruption is profound: major consulting firms have collectively published over 2,000 reports advising clients on enterprise AI adoption, effectively writing the playbook for the displacement of their own legacy business models 11. McKinsey's own research estimates that generative AI could automate 60% to 70% of current work activities across industries, a metric that directly applies to their internal workflows 11.

Structural Reorganization from Pyramids to Obelisks

The traditional consulting firm is structured as a wide-based pyramid, utilizing a high leverage ratio of junior staff to generate billable hours supporting a narrow apex of senior partners 11121314. This century-old model is currently collapsing under the economic realities of automation. As generative AI systems automate the analytical work that previously required large entry-level cohorts, the wide base of the pyramid becomes an unnecessary overhead expense 121421.

In response, major firms are being forced to transition toward a narrower "obelisk" or "tower" organizational model 12142122. This emerging architecture minimizes generalist analyst roles and instead relies on three primary functions: * AI Facilitators: Early-career, tech-savvy consultants who design data pipelines, refine AI-driven workflows, and manage prompt engineering 121421. * Engagement Architects: Experienced mid-level consultants who define client problems, interpret AI-generated outputs, and translate data into actionable strategic frameworks 121421. * Client Leaders: Senior partners dedicated almost exclusively to relationship management, navigating complex corporate politics, and guiding overall firm strategy 121421.

To sustain their margins and attempt to self-disrupt, incumbents are aggressively deploying internal proprietary AI platforms. McKinsey has deployed "Lilli," a proprietary AI assistant used by 72% of its workforce, which has reportedly reduced research and synthesis time by approximately 30% 12142122. Similar internal tools, such as BCG's "Deckster" and "Gene" platforms, and Bain's "Sage," are actively reshaping internal operations by automating standard analytical workflows 11121421. Consequently, MBB firms have begun quietly reducing incoming associate and business analyst class sizes by an estimated 15% to 25%, with broader industry projections suggesting junior consultant roles face a 40% to 50% reduction by 2030 11.

The Hourglass Workforce and the Expertise Crisis

The shift from a pyramid to an obelisk structure creates a severe downstream vulnerability known as the "hourglass workforce" or the "mid-tier squeeze" 1516. As AI tools compress the value gap between junior employees and senior partners, the middle tier of professional services is hollowed out 1516.

In the traditional professional apprenticeship model, mid-level employees spent years performing routine analytical and drafting tasks. While repetitive, this labor served a vital developmental purpose: it was the primary mechanism through which professionals acquired the domain expertise, pattern recognition, and nuanced judgment necessary to become senior partners 1617. A senior professional relies heavily on the "scar tissue" developed through years of observing edge cases and model failures 1617.

By eliminating the mid-tier trenches where human judgment is forged, the consulting industry faces an impending crisis regarding the origin and training of its future leadership class 1617. When entry-level personnel use AI to build complex financial models without years of experience seeing how those models fail in practice, the organization becomes highly dependent on senior partners who are increasingly too far removed from the granular details to catch nuanced errors 16.

The Emergence of AI-Native Boutique Firms

While mega-firms attempt to reform their internal structures, the most acute disruptive innovation is being driven by a new category of competitor: the AI-native boutique consultancy. Firms such as Unity Advisory, Monevate, SIB, Xavier AI, and Perceptis are architected entirely around AI-augmented delivery models from inception, unburdened by legacy pyramid structures 12141819.

These entrants, often founded by former MBB and Big Four partners, exhibit radically different operational characteristics compared to incumbents 1820. They operate with inverted staffing ratios - often deploying one junior technologist to support multiple senior experts - and utilize small teams of three to eight professionals per engagement rather than the typical six to fifteen 11. By relying on machine learning algorithms and no-code tools to generate up to 80% of first-draft deliverables, these boutiques can execute complex scopes of work in two to four weeks, a timeline that traditional firms would scope at eight to twelve weeks 1118.

The competitive dynamics heavily favor these agile entrants in the mid-market. Because they lack the massive overhead and bureaucratic bloat of traditional pyramids, AI-native boutiques can underprice MBB firms by 40% to 60% while simultaneously generating higher profit margins 1118.

| Operational Metric | Traditional Incumbent (e.g., MBB) | AI-Native Boutique |

|---|---|---|

| Organizational Structure | Wide Pyramid (High Junior Leverage) | Narrow Obelisk / Tower (Senior-Heavy) |

| Team Size per Engagement | 6 to 15 personnel | 3 to 8 personnel |

| Typical Delivery Velocity | 8 to 12 weeks | 2 to 4 weeks |

| Pricing Strategy | Billable Hours / High Overhead | Outcome-Based / 40-60% below market rate |

| Primary AI Utilization | Sustaining (Efficiency for existing staff) | Disruptive (Core engine of deliverable creation) |

This automation fundamentally invalidates the traditional billable-hour revenue model 29. As AI generates massive workflow efficiencies, clients are increasingly unwilling to pay for time spent building presentation decks; instead, they demand fees mapped to measurable key performance indicators (KPIs) like cost savings and project velocity 21. This has led to the rapid standardization of outcome-based and fixed-price arrangements 2021. Furthermore, specialized boutiques are increasingly productizing their intellectual property, transitioning consulting from a pure service business to a "services-as-software" model 2921.

The Rise of the Fractional Executive Model

In tandem with structural automation, the delivery of senior professional expertise is shifting toward the fractional executive model. The number of fractional leaders - seasoned professionals who offer C-suite guidance (e.g., fractional CFOs, CMOs, General Counsel) to multiple organizations on a part-time basis - doubled from 60,000 globally in 2022 to an estimated 120,000 by 2024 223223.

This model aligns perfectly with the disruptive demands of modern scale-ups and mid-market enterprises. These companies require high-level strategic judgment that AI cannot provide, but they operate on tight budgets that preclude full-time executive salaries or massive consulting retainers 322324. Fractional executives typically work 10 to 15 hours a month for three to four different clients, generating substantial income while providing companies with extreme flexibility 2232. Data indicates that 52.8% of fractional professionals earn $100,000 or more annually, with roles heavily concentrated in tech, SaaS, and healthcare 2232.

Specialized talent platforms have emerged to facilitate this disruption. Platforms such as Catalant (focusing heavily on strategy consultants for enterprise clients), NeoGig (focusing on operational executives), and Toptal connect enterprises directly with vetted fractional experts 232435. By providing direct access to senior talent, these platforms bypass traditional consulting firm distribution channels entirely, capturing a market segment that legacy consultancies find too small to service profitably 2235.

Transformation of the Legal Services Market

The legal services market, a highly regulated environment historically defined by the billable hour, is experiencing rapid segmentation. Disruptive innovation in law is heavily influenced by jurisdictional compliance, creating stark contrasts in how different global regions adopt multidisciplinary models and AI automation.

Regulatory Moats and Multidisciplinary Practices

The trajectory of legal innovation diverges sharply between the United Kingdom and the United States, dictated primarily by regulations governing professional ownership.

The UK has served as a global pioneer in legal deregulation following the implementation of the Legal Services Act of 2007 (LSA) 2526. This legislation authorized the creation of Alternative Business Structures (ABS), a framework that permits non-lawyers to own equity stakes in law firms and share in management and profits 2526. Under the ABS regime, the "Big Four" accounting networks (PwC, EY, Deloitte, and KPMG) have successfully secured licenses from the Solicitors Regulation Authority (SRA) to operate as fully integrated multidisciplinary practices (MDPs) 26. Moving beyond simple co-location of services, the Big Four utilize an "integrated solutions" approach, embedding legal advice directly into their broader suite of corporate consulting, finance, tax, and technology offerings 2627.

Conversely, the US market remains highly restricted due to the American Bar Association's (ABA) Model Rule 5.4, which strictly prohibits non-lawyer ownership of law firms and fee-splitting with non-lawyers 264041. This rule acts as a severe structural barrier against private equity capital and multidisciplinary consolidation 40. Despite these bans, the Big Four continue to expand in the US by exploiting regulatory gaps, providing advisory services where law and consulting overlap - such as risk compliance, forensics, and merger due diligence - for companies that are not their audit clients 26.

However, a dual-track market has emerged in the United States 40. States like Arizona and Utah have launched regulatory sandboxes or formally eliminated Rule 5.4 to permit ABS frameworks 4041. Arizona alone approved over 100 ABS entities by mid-2025, prompting immediate entry by institutional capital and major players, notably allowing KPMG to launch KPMG Law US 4041. In non-ABS states, private equity firms navigate these restrictions by utilizing Management Services Organization (MSO) structures. This model separates the administrative, marketing, and technological assets of a firm into an MSO owned by outside investors, while the legal practice remains owned by lawyers, thereby capturing investment returns without violating bar rules 40.

Expansion of Alternative Legal Service Providers (ALSPs)

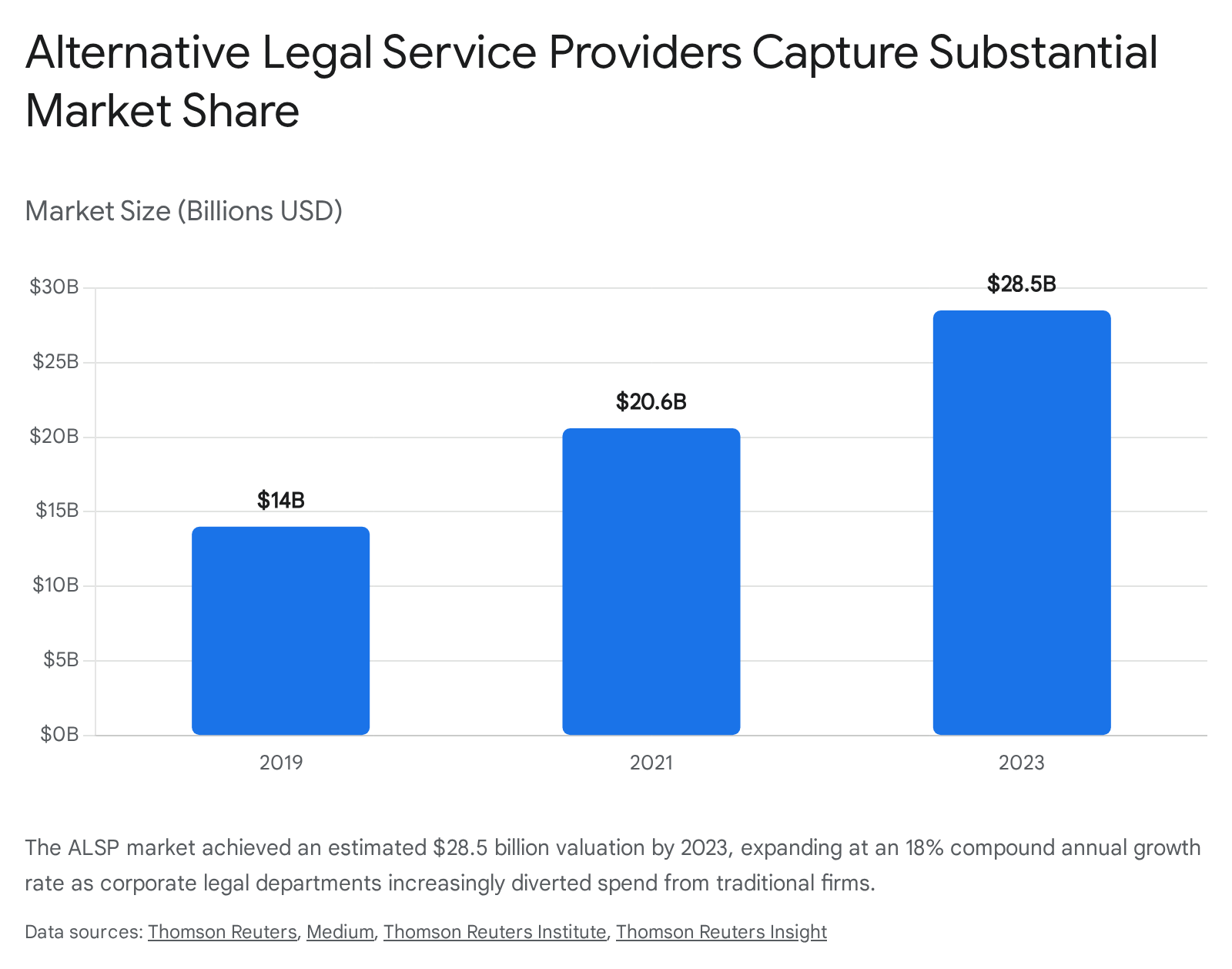

The most prominent manifestation of disruptive innovation in the legal sector is the rapid expansion of Alternative Legal Service Providers (ALSPs). ALSPs operate outside the traditional law firm partnership model, leveraging technology, rigorous process optimization, and labor arbitrage (often through offshore delivery centers) to deliver specific legal functions at significantly lower costs 284329.

The total ALSP market reached an estimated $28.5 billion in 2023, driven by a robust 18% compound annual growth rate from 2021 29304631.

This growth significantly outpaces that of traditional legal services 29. ALSPs initially gained traction by focusing on high-volume, low-complexity tasks such as e-discovery and basic document review 434849. However, mirroring the classic trajectory of disruptive innovation described by Christensen, ALSPs have steadily moved upmarket into more complex, higher-margin offerings 2843. Current service lines include sophisticated contract lifecycle management, regulatory compliance tracking, M&A due diligence, entity management, and intellectual property support 28434832.

Law Firm Affiliates and Captive ALSPs

The ALSP landscape has bifurcated into distinct competitive categories: independent providers and law firm affiliates 2930. Independent ALSPs, such as Axiom, QuisLex, and Elevate, sell their services directly to corporate law departments, capturing work that would previously have gone to outside counsel 4349.

In response to this existential threat, traditional law firms have launched "captive" or affiliate ALSPs - wholly owned subsidiaries designed to offer the same technology-driven efficiency while keeping the client revenue within the broader firm's ecosystem 43293334. Examples include Cleary Gottlieb's ClearyX, Hogan Lovells' ELTEMATE, and Ashurst Advance 4334.

The strategy of building captive ALSPs is proving highly effective for incumbents. The law firm affiliate segment grew from $500 million in 2019 to $1 billion in 2021, reaching $1.8 billion in 2023 33. Corporate clients view these integrated models favorably; among law departments that maintain external counsel panels and utilize ALSPs, 45% include at least one law firm-affiliated ALSP on their panel, compared to 25% that include an independent ALSP 2930. Furthermore, law firms that maintain their own captive ALSPs demonstrate a deeper understanding of the alternative delivery model, with 62% of such firms also engaging independent ALSPs to supplement their capabilities, compared to just 23% of firms without an affiliate 29.

| ALSP Market Segment | Description | Market Dynamics (2023) | Notable Examples |

|---|---|---|---|

| Independent ALSPs | Standalone businesses utilizing tech and process optimization. Sell directly to corporate legal departments and law firms. | Dominates total market share. Highly favored for specialized expertise and cost-efficiency. | Axiom, QuisLex, Elevate, UnitedLex |

| Law Firm Affiliates (Captives) | Wholly owned subsidiaries of traditional law firms designed to compete with independent ALSPs. | $1.8B specific market size. Rapid growth. Highly integrated into corporate counsel panels. | ClearyX, ELTEMATE, Ashurst Advance |

| Big Four Legal Networks | Accounting giants leveraging ABS frameworks to offer integrated multidisciplinary legal solutions globally. | Aggressive expansion in Europe and Asia-Pacific. Heavy focus on tax, M&A, and compliance. | PwC Legal, EY Law, KPMG Law, Deloitte |

Artificial Intelligence and Pricing Model Pressures

Generative AI is accelerating the disruption of the traditional legal pyramid by automating transactional and research tasks. Legal tech spending reached an estimated $27 billion in 2023, with enterprise AI adoption in legal departments soaring 13. Tasks such as contract review, regulatory filings, and due diligence are highly intelligence-based and are readily automated by specialized large language models, such as those deployed by startups like Harvey AI and Casetext 713. Short-term studies indicate productivity uplifts of 30% to 50% in document review and research through AI integration 13.

By 2025, the ability of AI platforms to automate non-reserved legal services has fundamentally diminished the need for large teams of junior associates 4128. This dynamic places intense pressure on the billable hour. As top 100 US law firms surged billing rates by 10% between 2023 and 2024, cost-conscious corporate clients increasingly pushed back against time-based billing 35. Clients demand fixed-fee arrangements, greater pricing transparency, and the routing of high-volume tasks directly to ALSPs or tech-enabled mid-sized firms 283655. According to Thomson Reuters research, corporate law departments anticipate shrinking their spending with traditional law firms that refuse to adopt alternative delivery and pricing models 3036.

Global Disparities in Legal Market Performance

The impact of technological and strategic disruption is generating highly varied market performance across regions. In the UK, the legal market remains highly attractive to outside investment due to liberalized structures, with corporatized law firms achieving 21% annual growth between 2022 and 2024, far outpacing traditional LLPs 37. London remains a premier hub for international commercial litigation, further fueling demand for tech-enabled dispute resolution 38.

In Australia, the legal market in 2024 - 2025 behaved dynamically, characterized as a race between the prestigious "Big 8" law firms and aggressive "Large" market entrants 3940. Australian firms lead globally in the adoption of generative AI, utilizing it to boost efficiency and training 3940. Initially, Large firms outpaced the Big 8 in growth and profitability by scaling rapidly; however, shifting macroeconomic conditions ultimately favored the established Big 8 firms, allowing them to stabilize transactional losses and leverage their premium rate strength to reclaim market share 3940. Despite a slight decline in lawyer utilization across the sector - partially attributed to the efficiency gains of GenAI - overall firm-wide demand increased by 3.2% 3941.

Automation and Consolidation in Accounting

The accounting and audit industry is currently managing a severe, structural human capital crisis alongside rapid technological automation. While a strict regulatory moat protects the certification of practitioners, the underlying daily workflows are highly susceptible to AI substitution, creating a volatile environment ripe for disruption.

The 150-Hour Rule and the Human Capital Crisis

Unlike management consulting, the accounting profession is guarded by the Certified Public Accountant (CPA) designation. Historically, the "150-hour rule" - which mandates a fifth year of university education (30 additional credit hours beyond a standard bachelor's degree) to achieve licensure - acted as a mechanism to elevate professional quality and create a barrier to entry 4243.

However, robust academic research by MIT and others demonstrates that the 150-hour rule has failed to measurably improve CPA service quality or reduce audit failures 42. Instead, it has acted as a severe deterrent to market entry. The requirement imposes massive opportunity costs on students - estimated at up to $100,000 when combining tuition for an extra year (e.g., a master's degree) and a year of foregone starting salary 4445. The research quantifies a stark outcome: the 150-hour rule caused a 26% decline in minority entrants into the field, disproportionately affecting candidates unable to afford the additional financial burden 42.

This regulatory bottleneck has resulted in a structural labor shortage, with the United States losing an estimated 340,000 accountants over the past five years 149. Concurrently, roughly 75% of licensed CPAs had reached retirement age by 2019, triggering a mass exodus of senior expertise 46. This extreme scarcity of human capital has inadvertently become the primary catalyst for rapid disruptive innovation; firms are adopting AI and automation faster than almost any other profession simply to fulfill existing client mandates 14966.

Legislative Responses and Mobility Challenges

The talent crisis has sparked a highly publicized legislative conflict regarding professional licensing. State CPA societies, responding to member pressure over staffing shortages, have actively pursued legislative reform to bypass the 150-hour rule. In 2025, Ohio spearheaded licensing reform by passing House Bill 238, allowing an alternative pathway to licensure requiring only a bachelor's degree (120 hours) coupled with two years of work experience 47. By mid-2025, over 25 states - including Minnesota, California, and Texas - had introduced or passed similar legislation to create alternative pathways 444547.

These state-level efforts face intense resistance from national associations, specifically the American Institute of Certified Public Accountants (AICPA) and the National Association of State Boards of Accountancy (NASBA) 434445. The national bodies argue that diverging from the uniform 150-hour standard threatens "substantial equivalency" and interstate mobility, potentially restricting CPAs licensed under alternative 120-hour pathways from practicing across state lines 434445. Despite this resistance, the momentum for reform underscores the desperation of firms unable to staff standard engagements.

Private Equity Consolidation and Mid-Tier Mergers

The mid-market accounting sector is undergoing a massive wave of consolidation, driven predominantly by private equity (PE) investment. In 2024 and 2025, PE capital flooded the accounting M&A market, targeting mid-tier and regional firms 664849.

The strategic rationale and valuation calculus for accounting M&A have shifted radically due to AI. Traditional metrics based purely on an existing "book of business" are being overshadowed by a firm's technological stack 48. Boutique firms that have successfully built proprietary AI automation for tax planning or data analytics command significant valuation premiums, attracting investors who view technological IP as the new gold standard 48.

Private equity strategies increasingly focus on acquiring multiple mid-tier firms, rolling them up onto a unified, cloud-based AI platform, and offshoring or automating routine tasks to drastically reduce operational costs 6648. Furthermore, large enterprises are engaging in strategic M&A to "buy rather than build" AI capabilities, purchasing tech-enabled accounting and advisory boutiques to rapidly accelerate their digital transformation 4950.

Deployment of Multi-Agent Systems by the Big Four

To offset the talent pipeline crisis and defend their market dominance from agile, PE-backed mid-tier consolidators, the Big Four accounting networks are deploying autonomous, agentic AI systems at an unprecedented scale 51. These platforms are not simple generative chatbots; they are "multi-agent" ecosystems designed to orchestrate complex, multi-step financial workflows globally 5152.

Key examples of these enterprise AI operating systems launched around 2025 include: * PwC Agent OS: Following a multibillion-dollar investment, PwC launched an internal operating system designed to host digital teammates capable of scaling across thousands of clients, executing audit and advisory workflows continuously 51. * Deloitte Zora AI: Positioned specifically as an "AI-powered procurement specialist," Zora is designed to alleviate massive bottlenecks in finance by automating the scanning, extraction, validation, and posting of invoices in minutes 51. * EY.ai Agentic Platform: Faced with the challenge of monitoring daily tax law changes across over 150 countries, EY deployed a platform embedding more than 150 specialized AI tax agents. This system supports EY's 80,000 global professionals by functioning as a digital colleague that combines EY's tax expertise with the infinite scalability of AI 51.

Within these frameworks, the role of the human accountant is fundamentally transforming. Professionals are transitioning from manual data processors to "AI supervisors" and strategists 51. The AI agents execute the intelligence-heavy data reconciliation and initial drafting, while human professionals govern the exceptions, manage client relationships, and ensure rigorous regulatory compliance 5152.

Pure-Play Autopilots in Accounting and Tax

While incumbents deploy sustaining multi-agent systems, pure-play disruptive startups are launching autopilot services targeting specific accounting and healthcare finance verticals 7149.

Because 80% to 90% of the underlying work in tax advisory and accounting is pure intelligence (rules-based calculation and jurisdictional compliance), it is highly susceptible to full automation 7149. Startups such as Rillet are building AI-native Enterprise Resource Planning (ERP) systems designed to autonomously close financial books, directly replacing outsourced bookkeeping functions 7953. In the tax sector - a $30 to $35 billion market - startups like TaxGPT, Skalar, and Ravical are utilizing AI to handle complex, multi-jurisdictional tax compliance for SMBs, deepening their data moats with every new jurisdiction processed 79.

The $50 to $80 billion outsourced US healthcare revenue cycle management market is particularly vulnerable. Medical coding requires translating clinical notes into roughly 70,000 standardized ICD-10 codes 79. While healthcare is assumed to be judgment-heavy, the billing layer is almost purely intellectual and rules-based. Autopilot firms like Anterior are deploying AI to deliver accurate coding outcomes at a fraction of the cost of traditional outsourced medical billing firms, effectively disrupting legacy labor-arbitrage models 79.

Conclusions and Future Outlook

The theory of disruptive innovation accurately models the current trajectory of the law, consulting, and accounting industries. Driven by the rapid maturation of generative AI, the foundational unit of value in professional services is irreversibly transitioning from billable human hours to scalable, automated outcomes.

Incumbent firms that attempt to rely solely on sustaining innovations - utilizing AI merely as an efficiency tool for junior staff while maintaining bloated pyramid hierarchies and time-based billing - will face severe margin compression. Agile, AI-native boutiques unburdened by legacy structures are already demonstrating the ability to execute complex scopes of work significantly faster and at half the cost of traditional mega-firms. Concurrently, the rise of the fractional executive model and independent alternative service providers offers corporate clients direct access to high-level strategic expertise without the overhead of massive institutional retainers.

The survival of legacy professional services entities necessitates a painful but mandatory strategic restructuring toward the obelisk model. This requires prioritizing senior strategic judgment, deep multidisciplinary integration, and the proactive cannibalization of their own traditional revenue streams through outcome-based pricing and "services-as-software" platforms. Ultimately, the future of professional services belongs to organizations that recognize artificial intelligence not as a subordinate tool to enhance human labor, but as the primary engine of task execution, elevating human professionals strictly into roles of governance, relationship management, and complex strategic judgment.