Disruptive innovation in media and content industries

Theoretical Framework of Disruptive Innovation

The theory of disruptive innovation provides a rigorous structural explanation for how established, well-managed companies can lose market dominance to smaller entrants with fewer resources. Originally articulated by Harvard Business School professor Clayton M. Christensen in 1995, the framework has become a foundational concept in business strategy, though its precise mechanical definitions are frequently misapplied in popular business literature 122. Disruptive innovation does not merely describe any sudden technological breakthrough or radical shift in a market. Instead, it defines a specific evolutionary process wherein a new product or service initially takes root in simple, undemanding applications at the bottom of a market, or creates a completely new market entirely, before relentlessly moving upmarket to displace established competitors 1.

Core Definitions of Innovation Trajectories

The theoretical framework distinguishes explicitly between sustaining innovations and disruptive innovations. Sustaining innovations represent incremental or breakthrough improvements to existing products, designed to satisfy the escalating demands of an incumbent company's most profitable customers 134. In the media industry, the transition from analog television to high-definition digital broadcasting, or the continuous improvement of publishing layouts and print quality, are classic sustaining innovations. Incumbents typically excel at sustaining innovations because their resource allocation processes, cost structures, and corporate values - collectively referred to as the Resources, Processes, and Values (RPV) framework - are optimized to pursue higher profit margins in established markets 356.

Disruptive innovations, conversely, are typically characterized by initially inferior performance according to the historical metrics valued by mainstream customers. They succeed by offering alternative benefits, such as lower costs, greater convenience, or drastically simplified user experiences 17. Christensen categorized these disruptive threats into two distinct trajectories:

- Low-End Disruption: This occurs when an entrant utilizes a low-cost business model to capture the least profitable segment of an existing market. Incumbents, motivated by the desire to maintain high margins and satisfy their most demanding clients, rationally choose to retreat upmarket rather than engage in a price war for their least demanding customers 178.

- New-Market Disruption: This occurs when an entrant targets "non-consumers" - individuals who previously lacked the financial resources, technical skill, or access to participate in a market. The innovation establishes an entirely new value network outside the incumbent's existing ecosystem, slowly improving in quality until the incumbent businesses' products are rendered obsolete 179.

The Phenomenon of Incumbent Overshoot

A critical mechanism driving disruptive innovation is "incumbent overshoot." As established companies continually invest in sustaining innovations to serve high-end customers, their products inevitably become too complex, expensive, or feature-heavy for the actual needs of the broader market 3811. This overshoot creates a strategic vacuum at the lower end of the market. Because the incumbent's internal metrics dictate that investments must yield high returns, management allocates resources away from defending the low end, viewing the disruptor's initial product as financially unattractive and technologically inferior 359.

Over time, the disruptive technology matures. Because the disruptor operates on a fundamentally different, often more scalable business model, it is able to improve its performance trajectory at a rate faster than customers' ability to absorb new features. Eventually, the disruptor's offering meets the performance standards of mainstream consumers, at which point the incumbent is rapidly displaced, having retreated into an ever-shrinking niche of high-end users 2612.

Academic Critiques and Boundary Limitations

While widely adopted, disruptive innovation theory has faced rigorous academic scrutiny regarding its predictive power, methodology, and universality. Researchers such as Andrew King and Baljir Baatartogtokh analyzed the original 77 case studies used by Christensen and concluded that only 9% of the examples strictly adhered to all four premises of the theory: incumbents overshooting needs, incumbents possessing but failing to exploit response capabilities, entrants on a sustaining trajectory, and incumbent displacement 1011. The researchers found that in nearly 80% of the reviewed cases, the sustaining innovations of incumbents did not actually overshoot what mainstream customers desired 11.

Furthermore, historian Jill Lepore and various technology analysts have critiqued the framework for assuming a deterministic outcome that ignores the strategic agency of incumbents and external market dynamics. Lepore famously characterized the concept as a "secular religion" providing an atavistic explanation for corporate failures, while analysts note that many successful market entries functioned more as sustaining innovations that targeted mainstream consumers directly, rather than originating in low-end or new-market footholds 561213. For instance, Apple's iPhone is often debated; Christensen initially dismissed it as a sustaining innovation to the cellular phone, missing its true identity as a new-market disruptor to the personal computer 6. Despite these ongoing academic debates, the underlying principles regarding resource allocation, capability rigidities, and the dangers of ignoring asymmetric competition remain highly relevant tools for analyzing the structural transformation of the media and content industries.

Media Economics and the Zero Marginal Cost Paradigm

The application of disruptive innovation to the media sector is fundamentally intertwined with the macroeconomic transition from physical product economies to digital platform economies. This transition is governed heavily by the principle of zero marginal cost, a paradigm that alters the foundational unit economics of content distribution 1415.

The Dissipation of Physical Barriers to Entry

Traditional media entities - print newspapers, broadcast television networks, and physical music distribution conglomerates - relied heavily on the high fixed costs of physical infrastructure. The necessity of owning printing presses, delivery truck fleets, broadcast transmission towers, and retail distribution networks created formidable barriers to entry 16. These capital-intensive requirements protected incumbents from immediate disruption, ensuring that only highly capitalized entities could compete on a national or global scale 1420.

Digitalization has systematically dismantled these physical barriers. The zero marginal cost paradigm, popularized by economic theorist Jeremy Rifkin, dictates that once the initial fixed cost of developing a digital product or platform architecture is covered, the cost of reproducing and distributing an additional copy to a new user asymptotically approaches zero 1420. This economic reality completely undercuts the traditional economies of scale that legacy media relied upon to maintain their competitive moats 1415.

Platform Economics and Content Aggregation

Platforms such as YouTube, Spotify, and Netflix successfully leveraged this zero marginal cost architecture to decouple content distribution from physical constraints 14. Consequently, digital content providers can experiment with low-end disruptions and new-market creation without the financial penalties associated with physical manufacturing and distribution 20.

This shift necessitates a reconceptualization of cost accounting within the media industry. Because variable costs essentially vanish in digital distribution, competitive advantage transfers rapidly from companies that control physical distribution channels to those that control discovery algorithms, user data ecosystems, and audience attention 141517. In this environment, a digital startup can scale to millions of users globally in a fraction of the time it would take a legacy broadcaster to expand its terrestrial transmission footprint, accelerating the pace at which disruptive threats mature and move upmarket 2018.

Disruption in Traditional Broadcasting and Pay Television

The traditional broadcasting and cable television industry provides a definitive, real-time example of incumbent overshoot leading to low-end disruption. For decades, multi-channel video programming distributors (MVPDs) extracted continuously increasing profit margins by bundling hundreds of channels into expensive packages. These comprehensive packages far exceeded the actual viewing habits and desires of the average consumer, representing a textbook case of overshooting market needs 1920.

The Cord-Cutting Trajectory and Demographic Shifts

The emergence of streaming video-on-demand (SVOD) initially took root as a classic low-end disruption. Early entrants, most notably Netflix, offered a highly restricted, delayed library of archival content delivered via mail and later over early broadband internet. This initial offering lacked the immediacy, live programming, sports access, and comprehensive catalogs of premium cable, appealing primarily to price-sensitive consumers or movie enthusiasts willing to accept lower convenience for specific content access 1. Traditional broadcasters and studios largely ignored these platforms as existential threats, or eagerly licensed their archival content to them, viewing streaming as a supplementary syndication revenue stream rather than a direct competitor to their core business 12.

However, as internet bandwidth improved - serving as the critical technological enabler - streaming platforms followed the exact trajectory predicted by Christensen. They moved aggressively upmarket by investing billions in high-quality original programming, directly competing for mainstream awards and audiences 219. The resulting consumer exodus from traditional Pay TV has been severe and sustained. The United States Pay TV penetration rate, which peaked at approximately 88% in 2010, has collapsed dramatically over the subsequent decade 21.

Data indicates a stark and accelerating divergence between households paying for traditional television and those relying entirely on alternative digital delivery. In 2018, Pay TV households numbered 90.3 million against 37.3 million non-Pay TV households. By 2023, this gap had narrowed to 62.8 million Pay TV households versus 68.9 million non-Pay TV households, marking the inflection point where cord-cutters and "cord-nevers" became the majority. Forecasts project that by the end of 2026, the number of non-Pay TV households in the United States will surge to 80.7 million, while traditional subscribers will fall to an estimated 57.2 million 2223.

| Year | US Pay TV Households (Millions) | US Non-Pay TV Households (Millions) | Penetration Status |

|---|---|---|---|

| 2018 | 90.3 | 37.3 | Cable Dominance |

| 2019 | 84.4 | 44.6 | Early Acceleration |

| 2020 | 77.5 | 50.9 | Pandemic Acceleration |

| 2021 | 71.6 | 58.3 | Continued Erosion |

| 2022 | 66.4 | 64.3 | Approaching Parity |

| 2023 | 62.8 | 68.9 | Inflection Point (Non-Pay TV Overtakes) |

| 2026 (Forecast) | 57.2 | 80.7 | Streaming Dominance 2223 |

This structural decline is sharply delineated by demographic factors, pointing to an impending generational cliff. According to 2025 demographic data, while 64% of adults aged 65 and older retain a cable or satellite subscription, only 16% of adults aged 18 to 29 do so. This younger cohort represents "cord-nevers," constituting a generational extinction event for traditional linear television models, as legacy providers fail to acquire the future customer bases required to sustain their infrastructure costs 2128.

Streaming Economics and the Re-Bundling Phase

Despite the triumph of streaming in capturing audience attention - accounting for a record-breaking 47.5% of total TV viewing time by December 2025, eclipsing broadcast and cable combined - the economic realities of the disruption have matured into a highly complex phase 2128. Streaming platforms have largely completed their trajectory upmarket, and the early financial advantages enjoyed by consumers during the low-end disruption phase have severely eroded.

As streaming services invest heavily in premium content to combat user churn in an oversaturated market, their individual subscription costs have risen sharply. By 2025, a consumer attempting to replicate the breadth of a traditional cable package by subscribing to the premium, ad-free tiers of the top streaming platforms (such as Netflix Premium, Disney+ Premium, Hulu, HBO Max, and Apple TV+) would face a monthly bill of approximately $140 2024. This cumulative cost meets or explicitly exceeds the cost of traditional premium cable packages, demonstrating that the disruptors have inherited the high-cost structures of the incumbents they displaced 20.

In response to consumer price sensitivity and the need for new revenue streams, major streaming platforms have aggressively introduced ad-supported tiers. By offering lower-priced subscriptions subsidized by advertising, the digital video ecosystem has come full circle, increasingly resembling the traditional television economics it originally sought to disrupt 2425.

Incumbent Adaptation and the Moat of Live Sports

Faced with this existential threat, legacy media companies face the difficult task of self-disruption. The Walt Disney Company provides a prominent case study of an incumbent attempting a successful pivot. Recognizing the decline of the traditional multi-channel video programming distributor (MVPD) ecosystem, Disney launched Disney+ in late 2019 2627. This required sacrificing highly lucrative licensing revenues to reclaim its content for its own direct-to-consumer platform, a classic example of an incumbent accepting short-term margin compression to compete against a disruptor 2628. By leveraging its massive IP portfolio (Marvel, Star Wars, Pixar) and utilizing its theme parks and merchandise as part of a coherent value network, Disney successfully scaled to hundreds of millions of global subscribers, establishing itself as a formidable player in the streaming era 2628.

For the broader linear television ecosystem, general entertainment and scripted content have migrated almost entirely to streaming. Linear networks have sharply reduced investments in new scripted shows throughout 2025 and 2026, filling schedules with reruns and lower-cost unscripted programming 19. This defensive posture creates a self-reinforcing cycle of declining viewership. Consequently, linear television is increasingly reliant on a single sustaining category to prevent total collapse: live sports. Sports broadcasting rights remain the primary anchor holding the traditional bundle together, drawing massive, synchronized audiences that advertisers still crave. However, even this final moat is beginning to fracture, as technology giants and streaming platforms aggressively bid for exclusive digital broadcasting rights, accelerating the final unraveling of the linear television model 192023.

Structural Disruption of the Publishing and Journalism Sector

The application of disruption theory to print journalism and publishing highlights a catastrophic failure of legacy incumbents to adapt to new-market disruptors. These disruptors fundamentally altered the advertising revenue model, stripping newspapers of their historical local monopolies.

The Collapse of the Print Advertising Monopoly

Traditional newspapers historically operated as local monopolies or duopolies, monetizing community attention through high-margin classifieds and print advertising 16. The advent of digital platforms did not initially offer better investigative journalism; rather, platforms like Google, Facebook, and later retail media networks offered superior targeting, precise measurability, and a zero marginal cost distribution model that traditional print could not replicate 16.

By 2026, the global advertising market has experienced a profound structural shift, transitioning fully into what industry analysts term the "Algorithmic Era." Worldwide advertising investment is forecast to surpass $1 trillion for the first time, growing at a robust rate of 5.1% to 7.1% year-over-year, depending on the macroeconomic forecasting model utilized 2930. Crucially, this massive growth is overwhelmingly concentrated in digital channels, which are projected to capture over 68.7% - and upwards of 73% according to some estimates - of total global ad spend 2936.

Advertising budgets are flowing rapidly to platforms that possess closed-loop measurement, rich first-party data ecosystems, and artificial intelligence-driven optimization capabilities 2930. Within this trillion-dollar ecosystem, retail media networks are the fastest-growing digital channel, expanding at 14.1% annually by sitting closest to the point of consumer purchase intent 293138. Online and social video are expanding at 11.4% to 11.5%, directly capturing historical television brand budgets, while Connected TV (CTV) grows at 9.5% 2931.

In stark contrast, traditional print media continues its structural contraction. Newspaper and magazine print advertising is projected to decline between 3.0% globally and up to 12.9% in the United States year-over-year in 2026 293032. While digital advertising revenues for some newspapers are finally overtaking print revenues, the overall digital growth (+1.3% CAGR projected through 2029) is entirely insufficient to offset the massive legacy losses 32. The consequence is a "two-speed market," where digital-native categories funnel their budgets almost entirely to major tech platforms, leaving legacy publishers fighting over a stagnant, shrinking pool of traditional brand budgets 30.

Legacy Adaptation and the Local News Vacuum

In the face of this severe disruption, successful legacy adaptation is rare. The New York Times is frequently cited as one of the few legacy media companies to successfully pivot and sustain profitability in the digital age. Its strategy aligns with disruption theory by abandoning reliance on legacy print ad margins and executing a digital-first, product-oriented strategy 33. Rather than merely digitizing the daily paper, the Times expanded beyond hard news into highly engaging digital verticals, including Games, Cooking, Audio, and affiliate commerce. By utilizing digital scaling, the organization built a robust, profitable subscription ecosystem that ultimately outpaced and outlasted digital-native competitors like BuzzFeed and Vice Media 33.

Conversely, the local news market exemplifies market failure and the emergence of non-traditional alternatives. Burdened by the fixed costs of physical newsrooms, printing infrastructure, and delivery logistics, traditional local papers are collapsing under their own weight 1641. As seasoned journalists face mass layoffs due to budgetary constraints, a vacuum of localized information emerges 4134.

In this void, platforms like Nextdoor are emerging as new-market disruptors. Nextdoor utilizes an existing digital network of verified neighbors rather than employing professional journalists, effectively lowering local content creation and distribution costs to zero 16. While media critics correctly argue this user-generated model diminishes journalistic quality, accountability, and depth, from a disruptive innovation perspective, it represents a classic market entry. It provides a "good enough," hyper-local information network to suburban and urban populations that have been largely abandoned by financially unviable legacy local newsrooms 16. Some analysts caution against government subsidies aimed at saving legacy newspapers, arguing that subsidizing obsolete, high-fixed-cost business models creates "zombie firms" that stifle necessary market innovations 16.

Emergent Disruption from Platform Envelopment and Algorithms

The contemporary media landscape is currently undergoing a secondary, more aggressive wave of disruption, driven by mobile-first ecosystems, algorithmic video feeds, and the centralization of digital services. These emergent forces threaten not only legacy broadcasters and publishers but also the foundational "Web 2.0" digital native platforms.

Super Apps as Regional Media Gatekeepers

In the Asia-Pacific region, the media ecosystem has been heavily disrupted by the evolution of "Super Apps." Platforms such as WeChat in China, KakaoTalk in South Korea, and Grab in Southeast Asia originated as simple, single-purpose utilities - such as instant messaging or ride-hailing 18353637. Utilizing powerful network effects, these platforms gradually integrated external services, including seamless payments, e-commerce, third-party mini-programs, and comprehensive news delivery 3537.

Through this strategy of platform envelopment, these super apps have effectively become the primary digital public sphere in their respective markets, bypassing traditional web browsers and portals entirely 3638. In South Korea, KakaoTalk reaches 94% of domestic smartphone users, while Naver functions as the dominant news mediator, controlling the primary interface through which citizens consume journalism 38. This centralization heavily disrupts traditional broadcasters by controlling the distribution chokepoints of information. However, this disruption carries significant societal externalities; these platforms have been heavily criticized by media scholars for acting as unchecked mediators that foster environments susceptible to disinformation, fake news, and political manipulation, operating outside the rigorous ethical frameworks traditionally maintained by legacy journalism 4138.

Algorithmic Discovery and the TikTok Model

TikTok represents a formidable new-market disruption within the social media and digital video sectors, fundamentally altering how content is distributed and monetized. Previous social networks, such as Facebook, Instagram, and Twitter, relied heavily on explicit user-curated social graphs. To generate a content feed, users had to actively build networks of friends, family, or specific accounts to follow 4739.

TikTok bypassed the social graph entirely by utilizing an intensely sophisticated recommendation algorithm - the "For You" page. This system evaluates passive user behavior, analyzing micro-interactions such as watch time, re-watches, and swipe velocity to serve highly tailored content without requiring the user to actively build a network 4739. By doing so, TikTok shifted the paradigm from an "information and social networking" platform to a pure "entertainment and algorithmic discovery" platform 47.

This algorithmic disruption dramatically lowers the barrier to entry for content production. Creators can achieve massive, global reach based purely on the engagement value of a single video, without needing an established follower base. The application's rapid integration of native e-commerce functionalities and its emerging utility as a visual search engine for younger demographics demonstrate a disruptive expansion that blurs the boundaries between media consumption, informational search, and retail. This paradigm shift is compelling digital marketers to drastically alter their omnichannel strategies, moving budgets away from traditional platforms to chase the highly engaged, algorithmically sorted audiences on TikTok 4739.

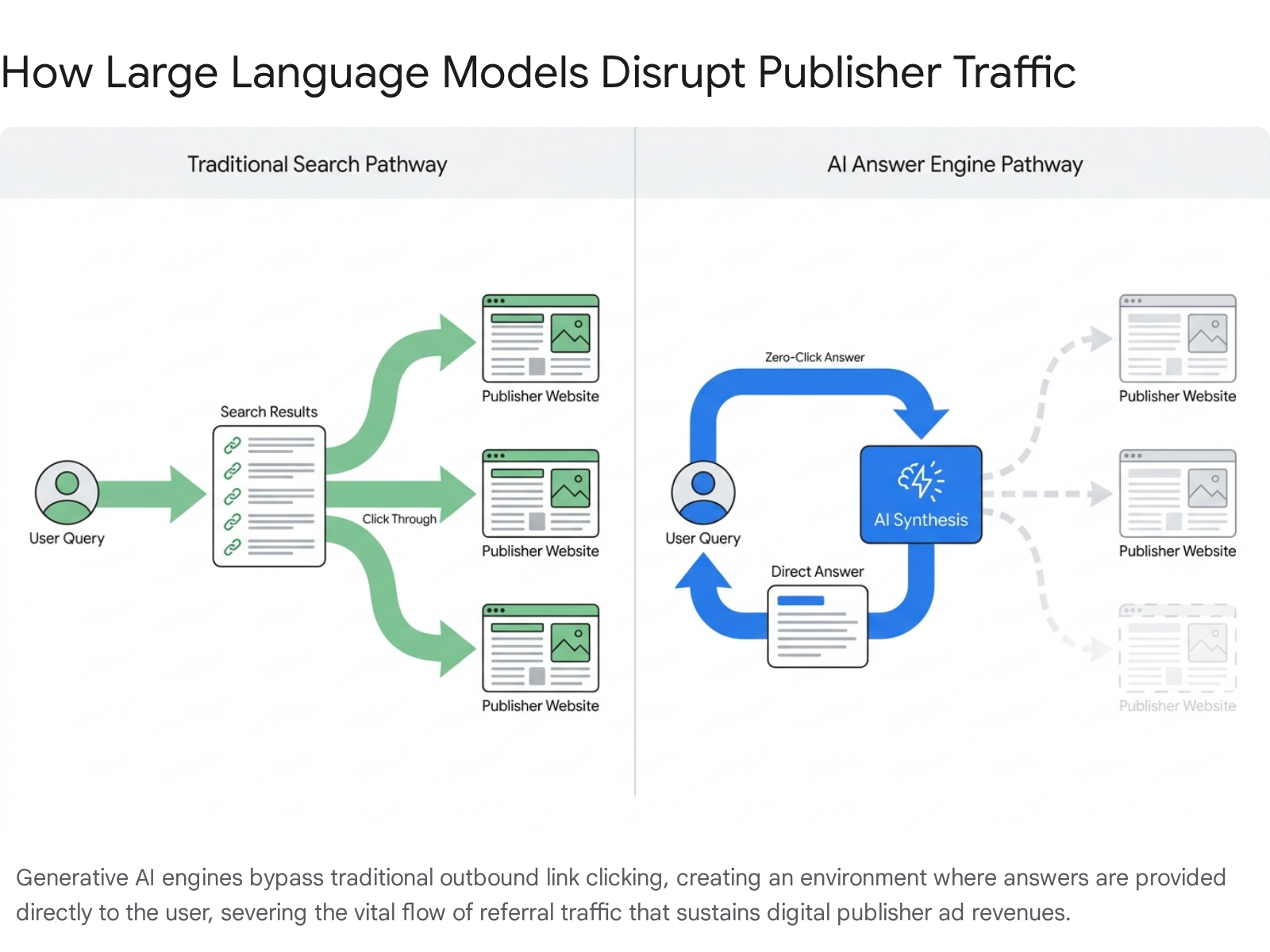

Large Language Models and the Threat to Referral Traffic

The most immediate and arguably existential threat to digital publishers entering 2026 is the integration of Large Language Models (LLMs) and generative artificial intelligence into global search engines 4940. Traditionally, digital media relied upon an implicit, symbiotic economic contract with search engines: publishers invested resources to create free content, and search engines indexed that content, providing outbound referral traffic that publishers subsequently monetized via display advertising, affiliate links, and subscription funnels 49.

The Zero-Click Environment and Search Transformation

AI Overviews and conversational answer engines - such as ChatGPT, Anthropic's Claude, Perplexity, and Google's integrated AI interfaces - disrupt this foundational model by summarizing information, synthesizing data, and answering user queries directly on the search results page. This paradigm creates a "zero-click" environment, where the user receives the necessary information without ever needing to navigate to the original publisher's website 5141.

As of mid-to-late 2025, zero-click searches accounted for nearly 69% of all search volume, and Google's AI Overviews were triggering on 13.14% of all search queries, more than double the rate observed at the beginning of the year 5141. The impact on traditional SEO traffic is severe. Where an AI Overview appears, organic click-through rates for the top-ranking traditional publisher link fall dramatically, effectively cutting click-through rates by more than half (e.g., from 1.41% down to 0.64%) 41.

Conversion Quality versus Volume Deficits

While LLM-driven referral traffic currently represents a marginal fraction - typically less than 2% - of total referral traffic for most publisher websites, its growth velocity is alarming. Industry data reveals that AI referral volume tripled between January and December 2025 5142. Looking ahead, international media managers anticipate search referrals to plummet by over 40% across the next three years, stripping billions of pageviews from the open web ecosystem 40.

Intriguingly, this disruption presents a profound paradox for digital marketers. The traffic that does successfully arrive via LLM referrals is remarkably valuable, converting at approximately 18% 5142. This conversion rate vastly outperforms traditional SEO, social media, and pay-per-click channels, primarily because users utilizing LLMs arrive with highly specific, pre-qualified intent 5142. However, the exceptional quality of this traffic cannot mathematically compensate for the absolute loss of top-of-funnel volume. Consequently, mid-tier and scale-dependent digital publishers face a severe monetization crisis unless they can rapidly pivot their business models away from algorithmic search dependence toward direct brand loyalty, closed-ecosystem subscriptions, or enterprise content licensing agreements with the very AI developers disrupting their traffic 4940.

Strategic Predictions for Legacy Media Industries

Applying the rigorous historical lens of disruptive innovation to the current deluge of market data allows for several robust, strategic predictions regarding the future landscape of traditional publishing and broadcasting as they navigate the remainder of the 2020s.

First, the media industry will likely witness the final unraveling of the generalist bundle. Just as the traditional cable bundle has fragmented in favor of specific digital subscriptions, broad-spectrum digital news platforms will struggle to survive the AI-driven collapse of referral traffic. To survive, publishers will be forced to retreat into deep, highly specialized verticals - such as B2B market intelligence, hyper-local community curation, and premium lifestyle content 1649. By focusing on niches where first-party data is rich and direct audience relationships are paramount, publishers can bypass algorithmic gatekeepers entirely.

Second, the era of platform envelopment will accelerate. Traditional media companies will increasingly find themselves enveloped by larger technology ecosystems. As advertising consolidates heavily into programmatic, AI-driven environments - which are expected to capture upwards of 80% of all digital ad transactions - independent media entities will struggle to maintain standalone digital destinations. Instead, they will be forced to operate as content-supplying nodes within broader ecosystems owned by global tech conglomerates and emerging LLM developers 293843.

Third, traditional broadcasting will endure for the immediate future not through technological innovation, but through the immense financial inertia of massive, multi-year live sporting contracts. Live sports remain the final bastion holding the linear television model together. However, as well-capitalized technology giants continue to aggressively siphon these exclusive broadcasting rights to their proprietary streaming platforms, the linear broadcast model will likely face its terminal inflection point before the end of the decade, shifting entirely to digital delivery 1920.

Finally, the disruption of text-based search will force a massive resurgence in direct-to-consumer audio and video formats. As text referrals vanish into AI Overviews, publishers will pivot editorial resources heavily toward personality-driven video platforms (such as YouTube and TikTok) and audio formats like podcasts 40. These formats command highly engaged audiences and are currently far more difficult for Large Language Models to perfectly synthesize without losing the parasocial human connection and nuanced delivery that audiences fundamentally value 40.

In conclusion, the media and content industries have continuously validated the core strategic tenets of disruptive innovation theory. From the early transition to zero marginal cost distribution models, through the streaming wars, to the current algorithmic and generative AI-driven epoch, the fundamental reality remains unchanged: legacy incumbents optimizing for their current highest-margin structures consistently leave themselves vulnerable. New technologies that initially appear as inferior, low-margin tools consistently mature to rewrite the economic rules of the entire ecosystem.