Diffusion Models and GANs for Synthetic Market Data

1. Introduction: The Paradigm Shift in Quantitative Finance

The demand for high-fidelity synthetic financial time-series data has accelerated dramatically over the past half-decade. Driven by the dual imperatives of stringent data privacy regulations and the critical need to simulate counterfactual market environments for stress-testing and algorithmic trading optimization, the quantitative finance community has increasingly transitioned away from classical parametric models. Historically, the synthesis of market data relied heavily on stochastic processes - such as Geometric Brownian Motion, jump-diffusion models, and Autoregressive Conditional Heteroskedasticity (GARCH) variants. However, these classical econometric models are often too mathematically rigid to capture the full spectrum of empirical market phenomena. These phenomena, commonly referred to as "stylized facts," encompass heavy-tailed return distributions, volatility clustering, leverage effects, and highly complex, dynamic cross-asset correlations 122.

To overcome the structural limitations of parametric models, the machine learning community initially championed Generative Adversarial Networks (GANs), culminating in foundational frameworks such as Wiese et al.'s 2020 QuantGAN architecture 134. QuantGAN demonstrated the unprecedented capacity to capture long-range dependencies in financial data using Temporal Convolutional Networks (TCNs) embedded within an adversarial min-max framework 13. However, the landscape of deep generative modeling has experienced a profound paradigm shift between 2023 and 2026. Academic literature presented at premier machine learning conferences (NeurIPS, ICLR, ICML) and quantitative finance preprint repositories (SSRN, arXiv) has extensively documented the rising superiority of score-based diffusion models. These models bypass the notorious training instability of GANs, offering superior distributional coverage and exact likelihood estimation 5767.

This research report provides an exhaustive, nuanced re-evaluation of the synthetic market data landscape. It contrasts the core mathematical mechanisms of adversarial dynamics and score-matching, evaluates their disparate performances across distinct data frequencies - ranging from daily OHLCV to ultra-high-frequency Limit Order Books (LOB) - and defines the standardized quantitative metrics utilized to benchmark synthetic fidelity. Furthermore, it investigates a critical emerging vulnerability in generative AI: data privacy, memorization, and the novel cluster-medoid leakage phenomenon. Finally, this report addresses the prevailing misconception that diffusion models have rendered GANs obsolete, explicitly identifying algorithmic environments where QuantGAN and its adversarial successors remain mathematically and operationally indispensable 8912.

2. Core Mathematical Mechanisms: Adversarial Dynamics vs. Score-Matching

The theoretical divergence between Generative Adversarial Networks and diffusion models represents a fundamental split in how machine learning approximates complex, high-dimensional probability distributions. Understanding these contrasting mathematical mechanisms is vital for selecting the appropriate generative architecture for financial scenario modeling.

2.1 Generative Adversarial Networks: The Min-Max Game

Generative Adversarial Networks frame data synthesis as a zero-sum, two-player optimization game 41310. Let $p_{data}(x)$ represent the true underlying distribution of financial time series, and $p_z(z)$ represent a simple prior distribution, typically a standard multivariate Gaussian. The generator network, $G_\theta(z)$, maps this latent noise to the data manifold to produce synthetic samples. Simultaneously, the discriminator network, $D_\phi(x)$, attempts to distinguish between the empirical historical samples $x \sim p_{data}$ and the synthetic samples generated by the model.

The classic GAN objective minimizes the Jensen-Shannon (JS) divergence via the following min-max formulation:

$$\min_G \max_D V(D, G) = \mathbb{E}{x \sim p{data}}[\log D(x)] + \mathbb{E}_{z \sim p_z}[\log(1 - D(G(z)))]$$

In the context of financial time series, the foundational QuantGAN architecture adapts this framework by utilizing Temporal Convolutional Networks equipped with dilated causal convolutions for both the generator and discriminator 1311. This specific architectural choice allows the generator to capture the long-range temporal dependencies inherent in volatility clustering without suffering from the vanishing gradients typically associated with standard Recurrent Neural Networks (RNNs). To further stabilize the modeling of financial sequences, architectures like TimeGAN integrate supervised stepwise losses alongside the adversarial objective, embedding the data into a latent space where transition dynamics are explicitly penalized 111217.

Despite their success, the adversarial nature of GANs leads to severe optimization challenges. Architecturally, GANs attempt a "single jump" from noise to complex data while fighting a discriminator. If the discriminator converges too rapidly and achieves near-perfect classification, the gradients passed back to the generator vanish, entirely halting the learning process 1013. Furthermore, GANs are notoriously susceptible to mode collapse - a mathematical phenomenon where the generator discovers a small, localized subset of realistic market patterns and exclusively generates those, completely failing to map the broader distribution 351420. In quantitative finance, mode collapse is catastrophic, as the model may generate standard low-volatility trading days perfectly while entirely omitting the rare, tail-risk events and flash crashes that are critical for robust stress testing 1014. While advanced variants utilizing the Wasserstein distance and gradient penalties (WGAN-GP) mitigate extreme gradient vanishing, they frequently struggle to encapsulate the full diversity of multi-asset market environments 321.

2.2 Diffusion Models: Reverse SDEs and Score-Matching

In stark contrast to the adversarial paradigm, diffusion models abandon the two-player game entirely. Instead, they rely on a thermodynamically inspired framework governed by Stochastic Differential Equations (SDEs) and score-matching 5622.

A diffusion model operates via two continuous-time processes. The forward process incrementally corrupts a real financial time series $x_0 \sim p_{data}$ into pure Gaussian noise $x_T \sim \mathcal{N}(0, I)$ over a fixed time horizon $t \in [0, T]$. This degradation is modeled precisely by an SDE:

$$dx_t = f(x_t, t)dt + g(t)dw_t$$

where $w_t$ represents a standard Wiener process, $f(\cdot)$ is the drift coefficient, and $g(\cdot)$ is the diffusion coefficient 522.

The generative breakthrough relies on Anderson's theorem, which dictates that the forward SDE can be perfectly reversed to synthesize pristine data from noise, provided the model has access to the score function of the marginal probability density, defined as $\nabla_x \log p_t(x)$. The reverse generative SDE is mathematically formulated as:

$$dx_t = [f(x_t, t) - g(t)^2 \nabla_x \log p_t(x)]dt + g(t)d\bar{w}_t$$

Because the true score $\nabla_x \log p_t(x)$ is intractable and evaluating the full partition function is computationally prohibitive, diffusion models employ a neural network $s_\theta(x_t, t)$ to approximate the gradient of the log-density. This is achieved through Denoising Score Matching, an objective that minimizes the Fisher Divergence between the true score and the modeled score 51516. The network learns to predict the specific noise $\epsilon$ that was injected at timestep $t$, optimizing the $L_2$ distance:

$$\mathcal{L}(\theta) = \mathbb{E}{t, x_0, \epsilon} \left[ | \epsilon - s\theta(x_t, t) |^2 \right]$$

By decomposing the generation of financial time series into a sequence of simple, locally Gaussian denoising steps, diffusion models transform a highly non-convex, fragile adversarial game into a stable, single-objective regression problem 1025.

2.3 Theoretical Implications for Market Modeling

The mathematical dichotomy between these two frameworks has profound implications for financial modeling. First, score-matching provides a stable, fully differentiable learning objective. Automatic differentiation can seamlessly propagate loss through the entire denoising trajectory, whereas adversarial networks are mathematically fragile and prone to non-convergence due to their Nash Equilibrium dynamics 1025. Second, because the forward diffusion process smooths the entire data manifold into a tractable Gaussian prior, the reverse process naturally traverses and reconstructs the entirety of the original distribution. This guarantees broad mode coverage, ensuring that rare tail events and anomalous macroeconomic regimes are inherently preserved in the synthetic output. GAN generators, driven only by the objective to fool the discriminator, have no mathematical incentive to cover the full distribution 3101425. Finally, diffusion models offer explicit, tractable mechanisms for log-likelihood estimation via Ordinary Differential Equation (ODE) formulations, providing researchers with a rigorous metric of model fit, whereas GANs remain strictly implicit models 1017.

3. Evaluating Computational Efficiency and Inference Dynamics

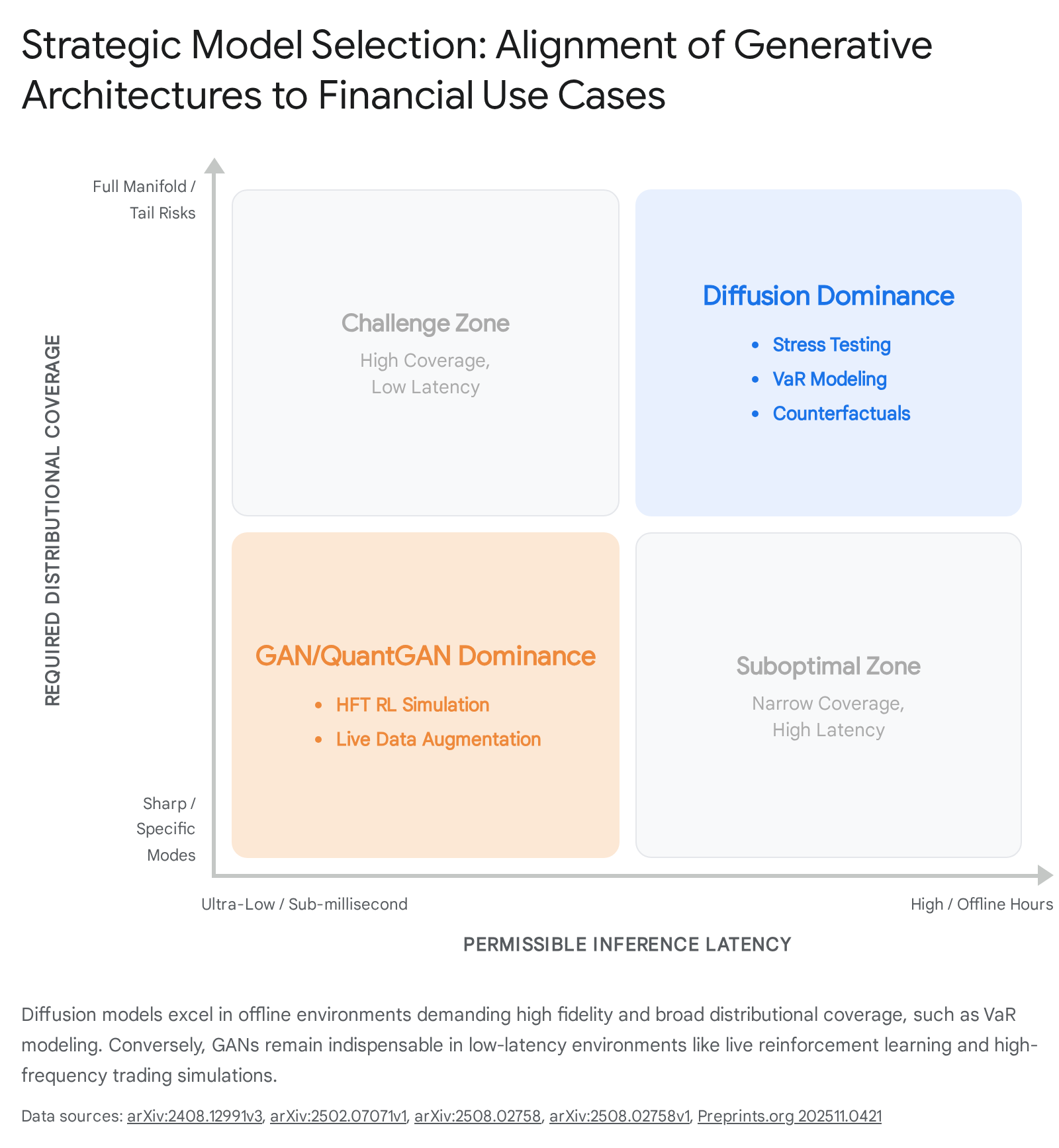

While the theoretical stability and distributional mapping of diffusion models position them as superior generative mechanisms, their practical deployment in quantitative finance is strictly governed by computational efficiency. The transition from theoretical supremacy to operational viability reveals a severe latency bottleneck for diffusion architectures 81317.

3.1 The Latency Bottleneck: Rapid Sampling vs. Iterative Generation

The primary drawback of the diffusion paradigm is its immense inference latency. Generating a single synthetic time-series path requires solving the reverse SDE, which functionally equates to passing data through the neural network hundreds or even thousands of times in a sequential, iterative manner 7. Empirical benchmarks from late 2025 and 2026 clearly highlight this computational intensity. Generating 100 sample paths over a nearly 20-year horizon utilizing Diffolio, a state-of-the-art multivariate diffusion framework, requires 2 minutes and 37 seconds of inference time on an NVIDIA RTX A6000 GPU, yielding an average latency of approximately 23.81 milliseconds per individual diffusion step 1727.

For models simulating ultra-high-frequency Limit Order Books, the computational burden is exponentially higher. The TRADES diffusion framework requires approximately six hours of computation time to generate a single hour of active market simulation when utilizing a standard 100-step diffusion process 18. While researchers employ techniques such as Denoising Diffusion Implicit Models (DDIM) to accelerate sampling by skipping steps, doing so introduces a severe trade-off between speed and performance. Applying a single-step DDIM acceleration to TRADES reduces computational time by a factor of 100, but catastrophically degrades predictive fidelity, increasing the Mean Absolute Error (MAE) of the generated paths from 1.213 to 3.146 18.

Conversely, Generative Adversarial Networks possess a distinct topological advantage at inference time. The generation of a synthetic sample via QuantGAN, TimeGAN, or modern Transformer-GANs requires only a single, deterministic forward pass through the Generator network 132930. This structural reality allows GANs to synthesize entire batches of time-series trajectories in mere fractions of a millisecond. Advanced GAN architectures explicitly designed for high-frequency financial simulation, such as DigMA, generate individual limit orders at a latency of approximately 0.017 milliseconds per order, rendering them orders of magnitude faster than any equivalent diffusion process 8.

| Model Architecture | Training Time (Average) | Inference Latency (100 Paths / Horizon) | Structural Inference Mechanism |

|---|---|---|---|

| QuantGAN / SigCWGAN | 2 Hours, 4 Minutes | ~3 Seconds | Single Forward Pass |

| TimeVAE | < 1 Minute | < 1 Second | Single Forward Pass |

| Diffolio (Diffusion) | 3 Hours, 18 Minutes | 2 Minutes, 37 Seconds | Iterative Denoising (Sequential) |

| Diffusion-TS | 9 Hours, 29 Minutes | 4 Hours, 32 Minutes | Iterative Denoising (Sequential) |

| TRADES (LOB Diffusion) | Highly Variable | 6 Hours (per 1hr simulated data) | Iterative Denoising (Sequential) |

Table 1: Comparative computational efficiency across prominent generative architectures, illustrating the severe inference latency inherent to diffusion models. Data synthesized from 2025/2026 benchmarking studies 9172718.

3.2 Resource Allocation and Offline vs. Online Paradigms

This stark disparity in latency mathematically bifurcates the application of these models into two distinct paradigms: Offline High-Fidelity Simulation and Online Low-Latency Simulation. Diffusion models are ideally suited for offline computations where accuracy supersedes speed. Applications such as overnight Value-at-Risk (VaR) calculations, the generation of historical counterfactuals for regulatory stress testing, and the synthesis of massive, high-fidelity datasets to train downstream predictive models can easily absorb the extended inference times required by diffusion 91219. In these contexts, the computational cost is entirely justified by the flawless alignment of the synthetic cross-asset correlation matrix with empirical reality 1727.

In contrast, GANs are fiercely optimized for online and near-real-time environments. In High-Frequency Trading (HFT) and algorithmic market-making, reinforcement learning (RL) agents often require interaction with highly responsive, live-simulated environments. The RL agent must execute an action and immediately receive a synthesized market reaction. The iterative, multi-step delay of a diffusion model would cripple the RL training loop. Here, the instantaneous generation speed of architectures like QuantGAN and its derivatives makes them the only viable choice for dynamic agent-environment interactions 82033.

4. Broadening the Scope: Handling Different Frequencies of Financial Data

The mathematical efficacy of a generative model is highly dependent on the granularity and structural characteristics of the financial data it attempts to replicate. Market data fundamentally falls into two distinct categories: Low-to-Medium Frequency (Daily/Minute OHLCV) and Ultra-High Frequency (Limit Order Book data).

4.1 Low-to-Medium Frequency: OHLCV and Macroeconomic Regimes

Open-High-Low-Close-Volume (OHLCV) data is structured as a regular, synchronous, multivariate time series representing aggregated market activity over fixed intervals. For this data type, the primary modeling challenges involve capturing volatility clustering, heavy-tailed return distributions, and complex cross-sectional dependence between multiple assets over long horizons 11727.

While QuantGAN pioneered the replication of single-asset volatility clustering, generating cohesive multivariate portfolios remained challenging for adversarial networks due to the difficulty of stabilizing a discriminator across dozens of correlated dimensions 3421. Recent advances in diffusion models have excelled in this specific regime. Architectures like Diffolio employ hierarchical attention mechanisms within the diffusion U-Net, explicitly decoupling asset-specific noise processing from systematic, market-level cross-sectional dependencies 1727. Furthermore, models integrating Transformer architectures into the diffusion framework (such as TransFusion) have demonstrated the ability to stretch sequence generation lengths up to 384 contiguous time steps without suffering from the compounding errors and temporal drift that plague RNN-based GAN generators 2035.

4.2 Microstructure and Ultra-High Frequency: The Limit Order Book (LOB)

The Limit Order Book represents the complex micro-level physics of the financial market. Unlike OHLCV data, LOB data is entirely asynchronous, event-driven, and highly dimensional, tracking individual bids, asks, volumes, and cancellations at multiple price depths on a microsecond basis. Synthesizing realistic LOB data is exponentially more complex because the generative model must ensure the absolute structural integrity of the order book - for example, preventing synthetic bids from crossing asks - while replicating the intricate feedback loops triggered by market impact 133336.

Early adversarial attempts, such as LOBGAN, frequently suffered from mode collapse, resulting in synthetic order books that lacked necessary liquidity depth and resilience. This caused simulated prices to drift unrealistically when probed by experimental trading agents 1318. The 2025 and 2026 literature highlights a definitive pivot toward conditional diffusion models for LOB simulation. Frameworks such as TRADES treat LOB streams as continuous temporal sequences strictly conditioned on the immediate past state of the market 13183738. By substituting standard convolutional architectures with spatial-temporal transformers within the diffusion process, TRADES successfully captures complex bid-ask dynamics and demonstrates high responsiveness to algorithmic agents, albeit at the previously discussed cost of high inference latency. Additionally, innovations like LOBDIF leverage diffusion to decouple and predict the joint time-event distribution of order streams, breaking away from the rigid assumptions of traditional stochastic point processes 3940.

5. Standardized Synthetic Time-Series Evaluation Metrics

The proliferation of synthetic financial data generation necessitates highly rigorous, standardized evaluation frameworks. Qualitative visual inspections - such as PCA or t-SNE scatter plots - are considered wholly insufficient for institutional quantitative finance 2242. The literature from 2023 onwards has consolidated around three primary axes of quantitative evaluation: Discriminative Scores, Predictive Scores, and the preservation of temporal dependencies 12434445.

5.1 Fidelity and Realism: The Discriminative Score

The Discriminative Score (DS) evaluates the empirical realism of the synthetic data by measuring how effectively an external machine learning classifier can distinguish between the true historical data and the generated synthetic data 224344. The methodology involves mixing real and synthetic datasets and training a post-hoc classifier, typically an LSTM or Transformer, to perform a binary classification task.

The Discriminative Score is defined as absolute deviation from random guessing: $DS = |\text{Accuracy} - 0.5|$. A lower score indicates superior model performance. An accuracy of 50% yields a DS of 0, implying that the classifier is guessing at random and the synthetic data is statistically indistinguishable from the real market data. Because RNN-based classifiers fail on exceptionally long sequences, the field has introduced the Long-Sequence Discriminative Score (LDS), utilizing a Transformer-based classifier to evaluate fidelity over extended temporal horizons 2035.

5.2 Functional Utility: The Predictive Score

While a model may generate highly realistic data distributions, it must also preserve the underlying conditional relationships necessary for downstream financial tasks, such as algorithmic forecasting. This utility is evaluated using the Predictive Score (PS), which operates on a rigorous "Train on Synthetic, Test on Real" (TSTR) paradigm 224323.

A forecasting model is trained exclusively on the synthetic dataset generated by the model (e.g., predicting the synthetic stock price at time $t+1$ given historical synthetic steps). This trained model is subsequently evaluated against the real, historical hold-out data. The PS is measured using standard error metrics like Mean Absolute Error (MAE). A lower Predictive Score indicates that the generative model successfully learned and replicated the true temporal dynamics and transition laws of the underlying market, effectively transferring valuable predictive signal into the synthetic space 4423.

| Generative Model | Discriminative Score (DS / LDS) | Predictive Score (PS / LPS) | Sequence Length Capability |

|---|---|---|---|

| QuantGAN | 0.283 ± 0.02 | 0.081 ± 0.01 | Short-to-Medium |

| TimeGAN | 0.237 ± 0.03 | 0.040 ± 0.01 | Short-to-Medium |

| GT-GAN | 0.434 ± 0.04 | 0.012 ± 0.00 | Short |

| CotGAN | 0.472 ± 0.02 | 0.012 ± 0.00 | Short |

| Sig-WGAN | 0.500 ± 0.00 | 0.028 ± 0.00 | Medium |

| TransFusion (Diffusion) | 0.400 ± 0.01 | 0.011 ± 0.00 | Extended (up to 384 steps) |

Table 2: Benchmark comparison of Discriminative and Predictive Scores across prominent generative models on standard financial datasets. Diffusion models demonstrating superior sequence length handling and predictive utility. Synthesized from 2024/2025 benchmarking studies 1220352324.

5.3 Stylized-Fact Fidelity and Temporal Dependencies

Beyond machine-learning-centric metrics, synthetic financial data must pass rigorous statistical tests grounded in classical econometrics. These tests evaluate whether the generated time series exhibit the "stylized facts" of global markets 4344:

- Autocorrelation Function (ACF): Evaluates the decay of temporal dependence. While raw asset returns exhibit near-zero autocorrelation, absolute or squared returns must exhibit slow-decaying autocorrelation, indicative of volatility clustering.

- Distributional Characteristics: Skewness Difference (SD) and Kurtosis Difference (KD) quantify the discrepancies in asymmetry and tail behavior between real and synthetic return distributions. Lower values confirm the preservation of heavy-tailed behavior, correcting a traditional weakness of vanilla Variational Autoencoders (VAEs) and early GANs 24344.

- Log-Determinant Divergence (LogDet): To capture the cross-sectional dependencies across multiple assets, the LogDet metric provides a spectral measure of discrepancy between the real and synthetic positive-definite correlation matrices, ensuring the global geometric alignment of generated portfolios 17.

6. Data Privacy, Memorization, and Security Vulnerabilities

A pervasive, yet fundamentally flawed, assumption in corporate finance is that synthetic data is intrinsically "safe" and immune to privacy regulations such as GDPR or CCPA. Generative models trained on highly sensitive, proprietary trading data - including proprietary alpha signals or deanonymized client order flows - are uniquely susceptible to data leakage and memorization 484950. As generative models grow in parameter size and mapping capacity, their propensity to inadvertently memorize exact training sequences amplifies drastically 502526.

6.1 Membership Inference Attacks (MIAs)

The primary vector for privacy auditing in synthetic financial data is the Membership Inference Attack (MIA). In an MIA, an adversary queries a model to mathematically determine whether a specific historical data record was included in its training set 226. If an MIA yields high classification accuracy, the model has functionally memorized its training data, representing a catastrophic privacy breach.

Standard econometric frameworks often exhibit high vulnerability to MIAs due to their rigid, deterministic structures; for example, ARIMA-GARCH models have demonstrated MIA accuracies as high as 56.8% in recent benchmarks, indicating significant partial memorization of real time-series patterns 253. Advanced generative models vary in their resistance. Carefully regularized adversarial models, such as TimeGAN, restrict MIA accuracy to approximately 51.1% (near random guessing), provided they are bounded by Differential Privacy (DP-GAN) noise injection techniques 253. However, the integration of differential privacy artificially degrades the statistical utility of the synthetic data, forcing quantitative teams into a zero-sum trade-off between alpha-generation capabilities and regulatory compliance 5026.

6.2 The Cluster-Medoid Leakage Phenomenon

Literature emerging in late 2025 and 2026 highlights a severe, model-agnostic vulnerability specific to high-fidelity deep generative models: Cluster-Medoid Leakage, often referred to as "Hidden Data Leakage" 485455.

The paradox of advanced architectures, particularly score-based diffusion models, is that achieving near-perfect distributional alignment requires the network to map the training manifold with extraordinary precision. Researchers discovered that even when a diffusion model generates purely "novel" data (avoiding any verbatim, one-to-one duplication), the synthetic outputs form dense geometric clusters whose overarching structure flawlessly mirrors the original dataset 4855.

An adversary with strictly black-box access only needs to repeatedly query the generator to obtain large batches of synthetic samples. By performing unsupervised clustering on this synthetic dataset, the adversary can identify the "medoids," or cluster centers. These medoids correspond precisely to the high-density regions of the real, hidden training data 4854. These structural neighborhoods act as highly accurate proxies for the proprietary data, allowing adversaries to reconstruct approximate sensitive records - such as distinct institutional trading behaviors, unique portfolio allocations, or confidential risk exposures - without ever requiring access to the model's internal weights or the original secure database 4854.

This revelation mandates a paradigm shift in financial AI governance. It proves that sample-level memorization checks are fundamentally insufficient; privacy guarantees must now mathematically account for structural, manifold-level distributional overlap 4854.

7. The Misconception of Obsolescence: The Ongoing Relevance of GANs

Given the theoretical elegance, mathematical stability, and superior distributional coverage of diffusion models, a common narrative has emerged suggesting that Generative Adversarial Networks are functionally obsolete. In the domain of quantitative finance, this is a dangerous misconception. The choice between an adversarial network and a diffusion model is not a simple hierarchy of quality; rather, it is a complex optimization problem dictated by stringent deployment constraints 27.

7.1 The Inherent Limits of the Diffusion Paradigm

The fatal flaw of the diffusion framework is its inherent reliance on Markovian sequences for sampling. As established in Section 3, reversing an SDE requires numerous sequential neural function evaluations. Despite ongoing research into distillation techniques - such as Distribution Matching Distillation or consistency models aimed at compressing diffusion into fewer steps - diffusion inference cannot natively compete with the instantaneous, single-step forward pass of a GAN generator 1330.

Furthermore, diffusion models rely on maximum likelihood estimation (MLE) equivalents, meaning their mathematical objective is to perfectly cover the entire data distribution 28. While this is highly beneficial for stress testing and assessing tail risks, it is not always the desired outcome. GANs, governed by their adversarial loss, naturally prioritize sample sharpness and plausibility over broad distributional coverage. If a financial institution only requires the generation of the most plausible, highly realistic scenarios for a specific market regime (without expending compute to map the complete tail probability space), a GAN will frequently provide sharper, less noisy samples in a fraction of the time 13.

7.2 Strategic Use-Cases for QuantGAN and Adversarial Variants

Therefore, architectures derived from Wiese et al.'s QuantGAN maintain explicit dominance in specific, highly lucrative sub-fields of quantitative finance:

- Low-Latency Online Learning and HFT: Deep reinforcement learning agents operating in simulated Limit Order Book environments require sub-millisecond latency for state-action-reward updates. Diffusion models introduce unacceptable operational drag. Fast adversarial generators remain the mandatory architecture for live agent training and High-Frequency Trading simulations 8912.

- High-Frequency Data Augmentation in Low-Data Regimes: In market environments where data is highly sparse - such as newly listed equities, illiquid alternative assets, or specific macroeconomic regime shifts - real-time trading algorithms require massive, instantaneous data augmentation to stabilize predictive models prior to execution. GANs, which take minimal time to train and fractions of a second to infer, provide the only viable mechanism for dynamic, on-the-fly augmentation 929.

- Directed Scenario Generation (Mode Seeking): Mode collapse, traditionally viewed as a fatal mathematical flaw, can be strategically leveraged as "mode seeking." If a quantitative analyst wishes to stress test an algorithm solely against specific types of historical market crashes or high-volatility regimes, conditional GANs can be directed to aggressively sample from that targeted mode. This produces highly concentrated, sharp adverse scenarios without wasting computational resources mapping standard, benign market noise 1314.

8. Comprehensive Comparative Evaluation

To synthesize the technical, operational, and mathematical differences between GANs and Score-Based Diffusion Models in the context of quantitative finance, the following table provides an exhaustive evaluation across five critical operational dimensions.

| Evaluation Dimension | Generative Adversarial Networks (e.g., QuantGAN, SigCWGAN) | Score-Based Diffusion Models (e.g., TRADES, Diffolio, TransFusion) |

|---|---|---|

| Training Stability | Low: Highly susceptible to non-convergence due to the delicate balance required in the two-player min-max game. Frequently suffers from vanishing gradients if the discriminator over-optimizes. | High: Exceptionally stable. Utilizes a single, mathematically rigorous score-matching objective (regression on injected noise) completely devoid of adversarial dynamics. |

| Inference & Sampling Speed | Ultra-Fast (Milliseconds): Generates synthetic time series in a single deterministic forward pass through the generator network. Ideal for real-time RL and HFT. | Slow (Seconds to Minutes/Hours): Requires hundreds of iterative passes through the denoising network (SDE reversal) to generate a single sample. |

| Mode Collapse Risk | High: The generator often mathematically optimizes by producing a narrow subset of realistic scenarios, failing to map the full diversity of market events or tail risks. | Minimal: The forward diffusion process smooths the entire data manifold to a Gaussian prior, ensuring the reverse process naturally traverses and maps the full empirical distribution. |

| Stylized-Fact Fidelity | Moderate: Excellent at capturing sharp, specific dynamics (like single-asset volatility clustering via TCNs), but struggles significantly with complex cross-asset correlations in multivariate settings. | Exceptional: Accurately reproduces heavy tails, leverage effects, and highly complex inter-asset correlation matrices (as validated by low LogDet divergence metrics). |

| Computational Cost (Compute & Energy) | Low to Moderate: Fast to train and exceptionally cheap at inference. Exhibits high parameter efficiency, making it viable for constrained operational environments. | Extremely High: Intensive neural function evaluations during both the training and inference phases result in significant GPU hours and vastly elevated operational energy costs. |

9. Conclusion and Future Directions

The evolution of synthetic financial time-series generation is fundamentally characterized by the ongoing tension between statistical fidelity and computational efficiency. The foundational work established by architectures such as QuantGAN proved unequivocally that deep learning could effectively replicate market microstructure and volatility clustering, paving the way for data-driven quantitative modeling free from rigid parametric constraints 111.

However, the recent ascendancy of score-based diffusion models marks a critical, mathematically rigorous turning point. By replacing fragile adversarial games with robust stochastic differential equations, models like Diffolio, TransFusion, and TRADES have solved the persistent issues of training instability and mode collapse 10132527. They offer unprecedented ability to map the full breadth of the financial data manifold, ensuring that vital, rare tail-risk events and complex cross-asset correlations are flawlessly preserved for applications such as regulatory stress-testing and robust portfolio optimization 2517.

Yet, as the empirical benchmarks in this report demonstrate, the triumph of diffusion models is severely constrained by their extreme latency bottlenecks. In ultra-low latency environments - where simulated Limit Order Books must interact synchronously with high-frequency reinforcement learning agents - QuantGAN and its adversarial descendants remain the premier, and functionally only, architectural choice 8912.

Looking forward, the frontier of synthetic market data research must address two critical challenges. First, the industry requires advances in distillation techniques (such as Consistency Models or Distribution Matching Distillation) capable of compressing the iterative diffusion process into a single-step generation, thereby bridging the latency gap between SDEs and GANs 30. Second, and more immediately pressing, the quantitative finance community must reconcile with the Cluster-Medoid Leakage phenomenon 4855. As generative models map financial manifolds with increasing perfection, the boundary between synthetic data and proprietary data dissolves. Developing new cryptographic or mathematically guaranteed differential privacy frameworks that protect structural manifold neighborhoods - without destroying the predictive utility and alpha of the synthetic data - will define the next era of AI-driven quantitative finance.