Cultural Dimensions and Consumer Behavioral Economics

Structural Asymmetries in Behavioral Science Evidence

The foundational theories of behavioral economics and cognitive psychology rely heavily on empirical data drawn from highly specific demographic subsets, creating a profound structural asymmetry in the understanding of human decision-making. The realization that behavioral science predominantly reflects populations characterized as Western, Educated, Industrialized, Rich, and Democratic (WEIRD) has catalyzed critical re-evaluations of what constitutes universal human behavior 1234. Historically, populations classified as WEIRD represent approximately 12% of the global demographic makeup; however, comprehensive audits of studies published between 2003 and 2007 revealed that 96% of psychological and behavioral samples were drawn exclusively from these contexts 4. This dominance has led to a systematic conflation of culturally specific cognitive heuristics with universal human nature.

Follow-up audits on major journal publications between 2014 and 2017 demonstrated only nominal progress, indicating that 95% of samples continued to originate from WEIRD populations, frequently utilizing convenience samples of university students from the United States and Western Europe 34. Furthermore, an evaluation of high-tier general psychological science journals published by the British Psychological Society between 2021 and 2023 found that participants from Latin America, Eastern Europe, the Middle East, and Africa combined accounted for only 8.7% of the total aggregate samples 3. Despite accounting for roughly 17% of the global population, African cohorts contribute to less than 1% of the aggregate behavioral science sample size 4.

The academic drive to expand cross-cultural behavioral research has inadvertently fostered a secondary bias: the overwhelming overrepresentation of Confucian East Asian societies as the primary empirical proxy for "non-WEIRD" cultures 12. Driven by robust social and technological infrastructure, East Asian nations have become the default comparative baseline for cross-cultural behavioral studies 1. An exhaustive analysis of 1,466,019 scientific abstracts, supplemented by coverage of 60 large-scale cross-cultural psychological projects encompassing 3,722,940 participants across 153 countries, quantified this dominance 12. The resulting data indicates the entrenchment of a rigid WEIRD-Confucian comparative binary that neglects vast portions of the global population and fundamentally distorts the global distribution of behavioral phenomena.

This structural omission renders entire macro-cultural regions virtually invisible within the evidence base. Regions such as Middle Africa, Central Asia, Latin America, the Caribbean, and Pacific Island societies remain chronically underrepresented in behavioral economics research 12. This regional blindness compromises the external validity of core behavioral economic phenomena, obscuring whether specific cognitive heuristics - such as loss aversion, present bias, and the endowment effect - are universally inherent to human cognition or merely artifacts of culturally localized socialization and historical development.

Psychometric Frameworks of Cultural Variation

To systematically analyze the divergence of economic behaviors across populations, researchers deploy specialized psychometric frameworks that quantify and map macro-level cultural values. While multiple models exist, they vary significantly in their dimensional architecture, predictive validity, and underlying assumptions regarding the interaction between individual cognition and societal structure.

Hofstede Cultural Dimensions Theory

The most prevalent framework utilized in cross-cultural economics is Geert Hofstede's Cultural Dimensions theory, originally developed through extensive factor analysis of employee surveys across multinational IBM subsidiaries in the 1970s 56. Hofstede's model identifies six continuous dimensions that measure societal values rather than individual psychological traits: Power Distance Index (PDI), Individualism versus Collectivism (IDV), Masculinity versus Femininity (MAS), Uncertainty Avoidance Index (UAI), Long-Term versus Short-Term Orientation (LTO), and Indulgence versus Restraint (IVR) 67.

These dimensions function as aggregate cultural indicators that predict how societies organize institutions, distribute power, and manage systemic risk. For example, a high Power Distance score indicates a society's deep structural tolerance for hierarchical inequality and strict authority gradients, whereas a high Uncertainty Avoidance score reflects a collective discomfort with ambiguity, often manifesting in rigid social codes, robust bureaucratic institutions, and a reliance on absolute truths 678. While highly influential and widely cited, Hofstede's methodology faces modern statistical criticism for its mechanistic reliance on variance reduction techniques and its early geographic limitations, which initially excluded Soviet states and mainland China 568. The reliance on high-level factor analysis means the dimensions capture substantial aggregate variance but frequently overlook granular subcultural nuances and individual-level deviations, prompting researchers to seek supplementary models 58.

Schwartz Basic Human Values

Shalom Schwartz proposed an alternative architectural model based on the universal requirements of human existence, isolating ten basic individual value types - such as Conformity, Tradition, Security, Achievement, and Self-Direction - which can be collapsed into broad bipolar dimensions: Conservation versus Openness, and Self-Enhancement versus Self-Transcendence 69. Unlike Hofstede's purely nation-level focus, Schwartz's framework evaluates both individual-level priorities and aggregate culture-level priorities, establishing a circular continuum of related values 69.

Empirical comparisons suggest that Schwartz's model frequently demonstrates superior predictive power over Hofstede's dimensions in specific macroeconomic contexts. Research analyzing international trade flows, bilateral imports, and government consumption divergence indicates that Schwartz's Egalitarianism-Hierarchy distance is a more precise predictor of cross-border economic activity than Hofstede's equivalent dimensions 610. The structural differences between the two approaches highlight that cultural frameworks are not interchangeable; the choice of model directly impacts the variance explained in behavioral economic modeling.

Global Leadership and Organizational Behavior Effectiveness

The Global Leadership and Organizational Behavior Effectiveness (GLOBE) project provides another methodological evolution, expanding cultural assessment into nine distinct dimensions derived from data collected from 17,000 managers across 62 countries 1112. GLOBE adapts several of Hofstede's constructs but crucially bisects each dimension into "values" (how a society should operate ideally) and "practices" (how a society actually functions) 1113. Furthermore, GLOBE differentiates the broad concept of collectivism into "institutional collectivism" and "in-group collectivism," and introduces distinct dimensions such as Performance Orientation and Humane Orientation 1112.

The conceptual distinction between values and practices matters significantly in behavioral economics. For instance, while Hofstede's Uncertainty Avoidance index historically correlates negatively with corporate risk-taking, the GLOBE Uncertainty Avoidance "practices" dimension exhibits conceptually divergent - and sometimes entirely opposing - interactions with risk behavior 16. This discrepancy demonstrates that identical nominal labels across different psychometric models measure distinct psychological realities, requiring precise theoretical alignment when deploying these frameworks to predict market behavior 16.

| Psychometric Framework | Core Architectural Dimensions | Primary Analytical Differentiation | Methodological Foundation |

|---|---|---|---|

| Hofstede Cultural Dimensions 67 | Power Distance, Individualism/Collectivism, Masculinity/Femininity, Uncertainty Avoidance, Long-Term Orientation, Indulgence/Restraint | Evaluates national-level value orientations; relies on broad geographic clustering. | Mechanistic factor analysis of multinational employee surveys (IBM). |

| Schwartz Basic Human Values 69 | Conservation vs. Openness, Self-Enhancement vs. Self-Transcendence (comprising 10 distinct basic value types) | Maps value priorities based on universal biological and social needs; evaluates both individual and cultural levels. | Circumplex structure derived from global teacher and student surveys. |

| GLOBE Project 1112 | Performance Orientation, Humane Orientation, Institutional Collectivism, In-Group Collectivism, Assertiveness, Future Orientation, Gender Egalitarianism, Power Distance, Uncertainty Avoidance | Bisects every dimension into societal "Values" (ideals) and societal "Practices" (actual behavior). | Comprehensive multi-industry management surveys targeting leadership dynamics. |

Interactions Between Culture and Macroeconomic Indicators

The precise explanatory power of cultural dimensions in behavioral economics remains contested when isolating hard economic variables like gross domestic product (GDP) per capita, inflation, and market volatility. Exhaustive longitudinal studies analyzing consumer purchases across 22 product groups in over 50 countries covering a 30-year period (1990-2019) indicate that while cultural dimensions correlate strongly with consumer expenditure patterns, their unique explanatory variance diminishes significantly after national differences in GDP per capita are statistically controlled 14.

In robust regression models, cultural dimensions typically explain a very limited proportion of additional variance - often in the order of 0.00 to 0.01 - beyond what wealth and retail infrastructure predict 14. Despite these modest effect sizes, the persistence of culturally driven variance confirms that core societal values independently guide resource allocation, consumer choice, and economic behavior. Even when diverse populations possess equivalent purchasing power, the underlying cultural syntax dictates how that capital is deployed, saved, or risked.

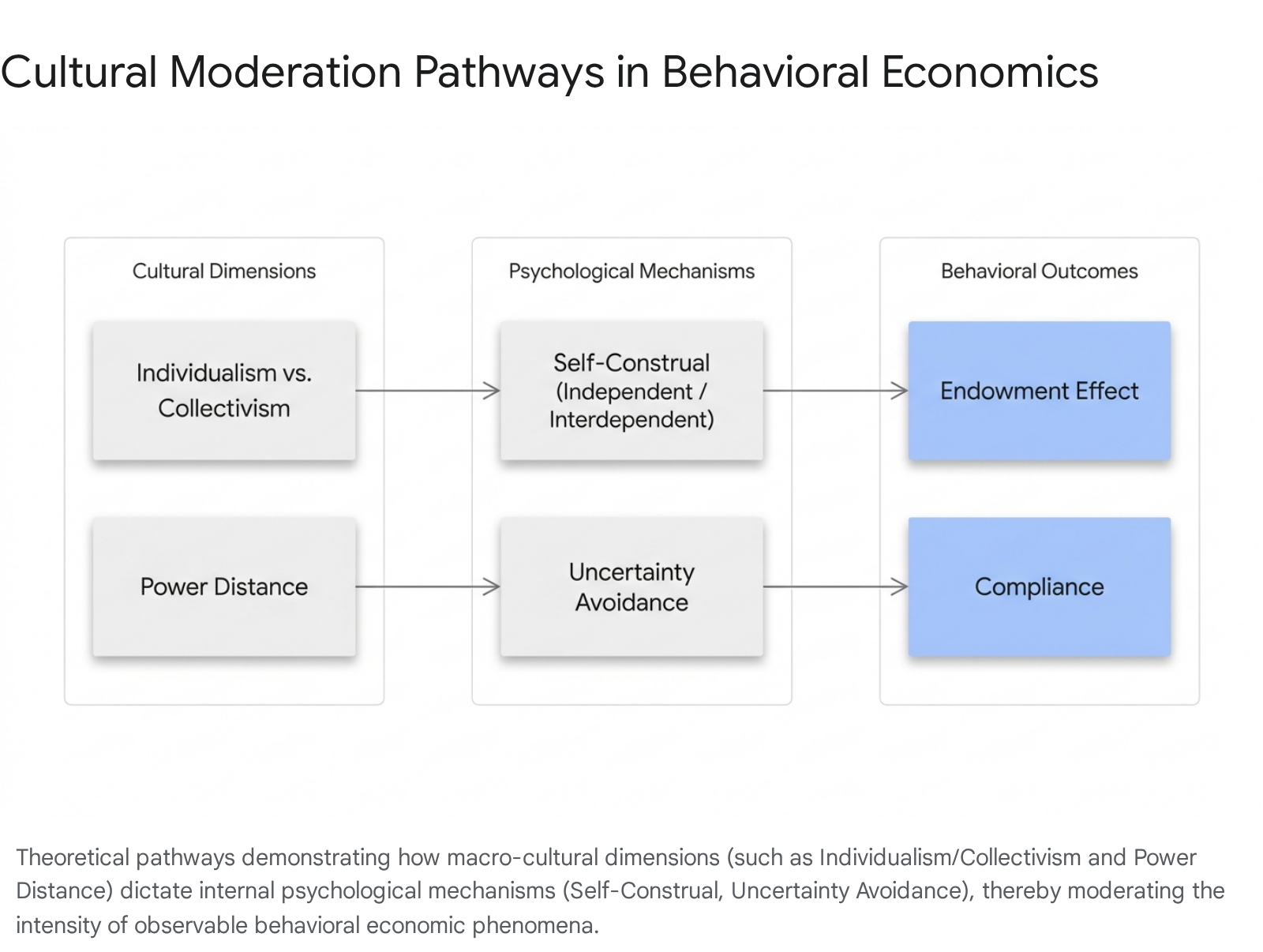

Cultural Moderation of Intertemporal Choice

The classical discounted utility model posits that individuals evaluate future rewards using a mathematically consistent exponential discounting rate, suggesting that time preferences between any equidistant periods remain constant regardless of when those periods occur 15. Behavioral economics identifies systematic human deviations from this standard, formalized mathematically in the quasi-hyperbolic discounting model, widely known as the $\beta-\delta$ model 161718. In this framework, $\delta$ represents the standard exponential discount factor measuring long-term patience, while $\beta$ represents a distinct "present bias" applied exclusively to immediate rewards 1618.

A $\beta$ coefficient of less than 1 indicates a disproportionate preference for immediate gratification over delayed realization. This mathematical asymmetry drives dynamically inconsistent behaviors across global markets, such as severe procrastination, inadequate retirement saving, credit card debt accumulation, and poor adherence to preventative health measures 171920.

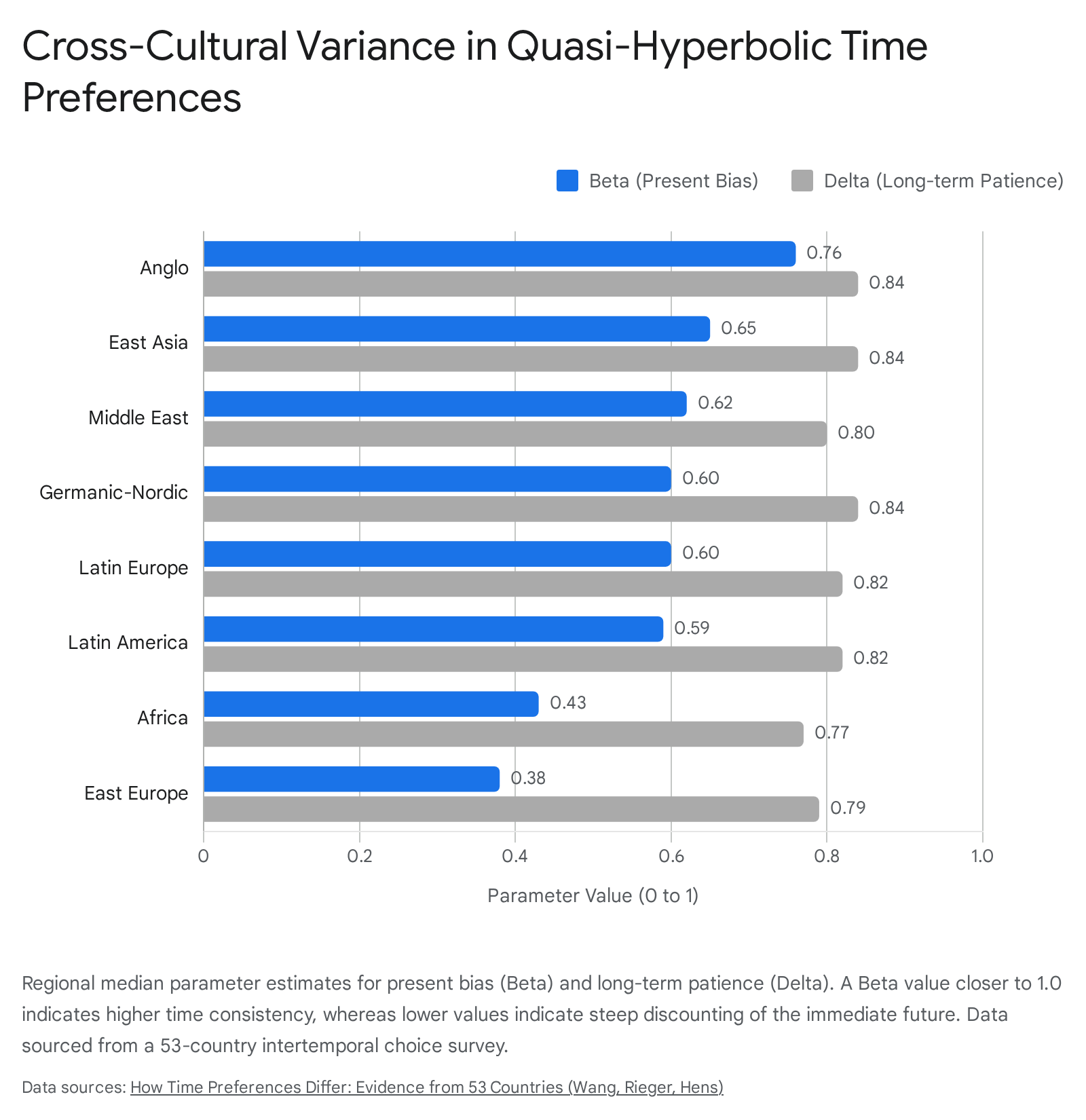

Quasi-Hyperbolic Discounting Across Global Clusters

Empirical evidence drawn from multinational datasets demonstrates profound, culturally bound heterogeneity in intertemporal preferences. Large-scale meta-analytical estimates of the $\beta$ parameter for monetary rewards aggregate around 0.938 (after correcting for publication bias), signifying a modest but statistically significant universal human present bias 18. However, relying on this global aggregate masks deep regional disparities that correlate with localized cultural values.

The comprehensive INTRA study, which evaluated time preferences across 53 countries, successfully mapped median hyperbolic discounting functions across distinct macro-cultural clusters 1521. The data revealed that populations in Anglo-American and Germanic-Nordic cultures exhibit the lowest degree of present bias (with median $\beta$ values of 0.76 and 0.60, respectively) alongside high absolute long-term patience ($\delta = 0.84$) 15. Conversely, African and Eastern European samples demonstrated profound present bias, yielding median $\beta$ coefficients of 0.43 and 0.38, respectively, indicating highly impulsive short-term economic behaviors 15. Latin American and Middle Eastern cohorts displayed intermediate discounting tendencies, with $\beta$ coefficients averaging 0.59 and 0.62 15.

Economic Predictors and Uncertainty Avoidance

The regional discrepancies in intertemporal choice correlate directly with both systemic macroeconomic stability and cultural dimensional architecture. Macroeconomic stability - specifically evaluated through higher GDP per capita, lower inflation rates, and lower economic growth volatility - fosters longer-term patience and systematically reduces the steepness of immediate discounting 1522. When the economic environment is predictably stable, the rational incentive to consume immediately diminishes.

Culturally, societies scoring high on Hofstede's Uncertainty Avoidance index exhibit markedly higher present bias 22. The societal discomfort with an ambiguous, unstructured future incentivizes individuals to extract utility immediately rather than risk future non-realization, operating under the heuristic that a certain gain today is vastly superior to an uncertain gain tomorrow 22. Furthermore, cultures scoring high in Hofstede's Long-Term Orientation and Individualism discount the future less steeply, demonstrating a greater collective resistance to immediate temptations and a higher capacity for sustained savings 22.

Age and demographic experience also interact with these biases. Survey data evaluating American males across varying levels of financial experience demonstrated that adolescents (aged 13-19) were 11.1 percentage points more likely to exhibit present bias compared to adults over the age of 20 26. This data suggests that neurological development and localized financial socialization further modulate the raw expression of quasi-hyperbolic discounting 26.

Future Bias Anomalies

While present bias ($\beta < 1$) dominates the behavioral economics literature and forms the basis of most policy nudges, empirical investigations occasionally capture statistically significant instances of "future bias" ($\beta > 1$) 1619. Under future bias, individuals paradoxically assign greater weight to future utility than present utility, effectively preferring to delay gratification even when immediate consumption would yield superior objective outcomes 1920.

Though theoretically debated - primarily because the standard $\beta-\delta$ parameterization is structurally optimized to capture present-biased impulsivity - cross-cultural surveys indicate meaningful subpopulations exhibiting these exact preferences 1923. For instance, a 2020 cross-sectional study conducted in Iran during the initial waves of the COVID-19 pandemic identified 13.4% of respondents as definitively future-biased, alongside 38.4% exhibiting standard present bias and 48.2% operating as consistent exponential discounters 19. Similarly, cross-country analyses of vaccination attitudes found that while the majority of global respondents exhibited exponential consistency ($\beta = 1$), future bias occurred more frequently in highly specific cultural demographics, such as certain vaccine-hesitant cohorts in South Korea where 34% of the sample yielded $\beta > 1$ 16. Future bias implies a hyper-focus on delayed outcomes, heavily influenced by localized cultural doctrines that prioritize strict asceticism, intergenerational security, or the moral superiority of delayed gratification over present satisfaction 20.

| Cultural Cluster | Median Present Bias ($\beta$) | Median Long-Term Patience ($\delta$) | Implied Behavioral Tendency |

|---|---|---|---|

| Anglo-American | 0.76 | 0.84 | High time consistency; robust long-term financial planning. |

| East Asia | 0.65 | 0.84 | Moderate immediate discounting; high long-term patience. |

| Middle East | 0.62 | 0.80 | Moderate present bias; slightly elevated long-term discounting. |

| Latin America | 0.59 | 0.82 | Pronounced present bias; prioritization of immediate liquidity. |

| Eastern Europe | 0.38 | 0.79 | Severe present bias; extreme preference for immediate rewards. |

| Africa | 0.43 | 0.77 | Severe present bias; steep overall temporal discounting. |

Note: Data derived from the 53-country INTRA survey assessing quasi-hyperbolic discounting parameters 15.

Loss Aversion and Reference-Dependent Preferences

Prospect theory fundamentally altered economic modeling by proposing that individuals evaluate outcomes relative to a specific reference point, processing potential losses differently than equivalent gains 2425. This deep psychological asymmetry is quantified by the loss aversion coefficient ($\lambda$). In the original theoretical formulations by Tversky and Kahneman, the $\lambda$ parameter was estimated at 2.25, suggesting that human beings process losses as psychologically twice as impactful as gains of the exact same magnitude 24.

Meta-Analytic Estimates and Geographic Heterogeneity

While loss aversion is heavily entrenched in behavioral finance literature, applying an aggregate parameter cross-culturally obscures vast macroeconomic and psychological variations. A comprehensive meta-analysis encompassing 607 empirical estimates extracted from 150 articles published between 1992 and 2017 found the mean aggregate $\lambda$ coefficient to be 1.955, with a 95% probability of the true universal value falling between 1.820 and 2.105 242627.

However, macro-level international estimations reveal that $\lambda$ ranges dramatically across countries, dropping to near loss-neutrality (1.1) in certain contexts and spiking up to extreme aversion (5.0) in others 2528. An analysis distinguishing specific cultural clusters determined that participants in Eastern Europe exhibit the highest average loss aversion globally, whereas participants in African nations demonstrate the lowest baseline loss aversion 29. Specific behavioral studies tracking professional sports betting and localized financial market behaviors indicate that German populations consistently possess below-median loss aversion relative to other developed nations, challenging assumptions about universal European risk profiles 28.

Precautionary Savings and Income Uncertainty

The intensity of loss aversion is not static; it is heavily moderated by socio-demographic factors, particularly baseline income and localized cultural power dynamics. Lower-income demographics consistently register higher levels of loss aversion, primarily because the marginal utility cost of a financial loss threatens basic subsistence more severely than a proportional gain improves their quality of life 2830.

In reference-dependent models of intertemporal consumption, this dynamic yields a powerful "precautionary saving motive" 30. The economic models developed by Kőszegi and Rabin demonstrate that loss aversion plays a diametrically opposed role regarding future consumption compared to immediate financial trades. Experimental and field data confirm that when exposed to equivalent levels of income risk, individuals with higher degrees of loss aversion accumulate significantly greater savings today 30. They do this specifically to protect against the severe psychological and economic utility drop associated with their future consumption falling below their established reference points 30.

Cultural Moderators of Loss Aversion

Cultural architecture fundamentally dictates how loss aversion is expressed. High levels of Hofstede's Power Distance and Masculinity strongly predict higher absolute loss aversion 29. In highly hierarchical, masculine, or strictly competitive societies, relative status is guarded aggressively; the psychological and social penalty of losing status, wealth, or rank is magnified 29. Consequently, individuals in these environments exhibit hyper-cautious economic behaviors to preserve their social and economic endowments, viewing losses as existential threats to their place within the societal hierarchy 29.

The Endowment Effect and Cultural Self-Construal

The endowment effect - the well-documented phenomenon where an individual demands a significantly higher price to sell an object they currently own (Willingness-to-Accept, WTA) than they would be willing to pay to acquire the exact same object (Willingness-to-Pay, WTP) - is traditionally attributed directly to loss aversion 4313233. Under this classical interpretation, giving up a physical possession is coded cognitively as a loss, which looms larger than the corresponding gain of acquiring it 32. However, recent rigorous cross-cultural replications reveal that the endowment effect is not universally uniform; its magnitude is deeply intertwined with cultural self-construal and specific strategic behaviors 3133.

Divergences Between Individualist and Collectivist Societies

The magnitude of the WTA-WTP gap diverges significantly when comparing populations classified as WEIRD against those originating from interdependent, non-WEIRD backgrounds. Within-subject experimental designs demonstrate that Western participants consistently exhibit enhanced financial valuation for items they own, whereas East Asian participants frequently do not demonstrate an observable endowment bias 431.

This striking cross-cultural variance challenges the universality of the pure loss aversion mechanism as the sole driver of the endowment effect. In Western, individualistic cultures, the human self is construed as autonomous, highly distinct, and independent 34. Consequently, when an object is incorporated into a Western individual's endowment, it gains massive subjective value through psychological "self-association" - the object functionally becomes an extension of the self, inherently inflating its perceived worth 31. In collectivist cultures, where the self-concept is highly interdependent, relational, and deeply embedded in larger social groups, the self-enhancement motive applied to inanimate objects is severely blunted 3135. This lack of object-self fusion significantly compresses the WTA-WTP gap.

Ownership Memory and Strategic Valuation

The moderation of this economic bias by cultural self-construal is further evidenced by specific cognitive memory tasks. The "ownership effect in memory" is a metric of self-referential processing, assessing how well individuals remember specific items they own compared to identical items owned by others 31. Research indicates that the absolute strength of the endowment bias correlates strongly with the ownership effect in memory among Western participants, reinforcing the direct neurological link between object valuation and independent self-concept 31.

Conversely, this cognitive correlation is entirely absent in East Asian participants 31. This absence suggests that distinct "buy-sell strategic behaviors" - responses to the market context of the transaction rather than pure psychological attachment or loss aversion - may actually drive pricing behaviors in interdependent cultures 3133. In these contexts, individuals do not feel more strongly about keeping an item than acquiring it, fundamentally decoupling the endowment effect from loss aversion 33.

Social Proof and Herding Behavior

Decision-making in highly ambiguous or high-stakes environments relies heavily on cognitive heuristics such as social proof and herding, where individuals unconsciously substitute their own private information with the observed actions of the majority 4136. While human beings universally exhibit susceptibility to social influence, the absolute effect size, contextual triggers, and underlying motivations for compliance are powerfully moderated by the societal individualism-collectivism spectrum.

Collectivism and Compliance Rationales

Cross-cultural compliance experiments demonstrate that individuals embedded in collectivist societies (e.g., Poland, India, China) exhibit significantly higher baseline rates of conformity and susceptibility to social proof than those in highly individualist societies (e.g., the United States) 373839. A pivotal psychological mechanism differentiating these outcomes is the internal locus of justification for the compliance.

In controlled comparative studies, individualistic participants comply primarily to maintain internal commitment and consistency; they act in alignment with their own past behaviors or stated beliefs to preserve a unified self-image 3839. In stark contrast, collectivist participants base their compliance heavily on peer history and the external validation of group consensus, utilizing the actions of similar others as definitive proof of the correct behavior 3839.

This dynamic extends directly into critical public policy execution and crisis management. During the COVID-19 pandemic, researchers evaluating mass adherence to safety practices found that underlying societal orientation heavily influenced behavioral compliance 39. While raw self-preservation motivations drove individualistic compliance in Western nations, robust collectivist orientations amplified adherence to safety protocols significantly more when social proof mechanisms explicitly highlighted communal benefits and group harmony 39. Similarly, in human-computer interaction (HCI) field experiments conducted in rural India, interventions specifically controlling for response bias successfully elicited highly critical technological feedback by leveraging negative social proof. This demonstrated that marginalized participants were highly responsive to feedback they perceived as originating authentically from their in-group peers, altering their behavioral outputs to match the synthetic group norm 37.

Financial Market Herding in Emerging Economies

In global financial markets, cultural orientations toward group cohesion manifest rapidly as systemic herding behavior, directly impacting asset pricing, liquidity, and overall market volatility. Research focused on emerging consumer markets, particularly in Sub-Saharan Africa and the Middle East, underscores how these culturally embedded cognitive biases frequently override classical rational finance principles 41.

On the Nairobi Securities Exchange (NSE), intense fluctuations in trading volumes and asset indices have been empirically linked directly to herd behavior, where retail investors emulate majority actions to mitigate perceived individual risk 41. In highly collectivist and high-uncertainty-avoidance environments, moving aggressively against the herd carries severe psychological and reputational penalties. Consequently, retail investors and smaller institutions default to mimicry, inadvertently inflating speculative asset bubbles, encouraging premature selling of profitable assets, and severely dampening long-term market efficiency 4146.

Cognitive Biases in Professional Financial Environments

The traditional economic assumption that sophisticated, highly trained financial professionals are immune to cognitive biases is routinely contradicted by modern behavioral finance research. However, the manifestation and impact of systemic biases - such as overconfidence and the representativeness heuristic - among professionals is filtered heavily through their distinct cultural origins and the rigid institutional environments in which they operate 4041.

Global Analyst Reporting and Heuristics

A comprehensive textual and statistical analysis of 1,575 equity recommendation reports authored by analysts from major international investment banks across Latin America, the United States, Europe, and Japan investigated the global footprint of professional financial biases 4042. The research evaluated exactly how overconfidence and the representativeness heuristic affected linguistic tone, narrative structure, and ultimate Earnings Per Share (EPS) predictive accuracy 40.

The findings revealed that systemic overconfidence systematically inflated the narrative optimism and structural complexity of the reports 4042. Analysts operating under these specific cognitive tendencies utilized a substantially more assertive, definitive tone and greater visual content - characteristics traditionally rewarded in aggressive, masculine corporate cultures that value extreme certainty 4042. Crucially, however, this overwhelming overconfidence did not correspond to superior substantive accuracy in the actual EPS forecasts 4042.

In contrast, the representativeness heuristic - where individuals erroneously judge the probability of an event based solely on its resemblance to a known prototype - showed no consistent statistical impact on report composition or error rates across the global sample 4042. Ultimately, rigid institutional affiliation, rather than geographic origin, gender, or native language, emerged as the dominant variable affecting actual predictive success. This suggests that rigorous, standardized corporate protocols can successfully overwrite raw cultural biases in highly structured analytical tasks, though they fail to eradicate the biased narrative tone 42.

Executive Decision-Making in Middle Eastern Markets

Outside of the highly standardized environments of multinational banks, behavioral biases exert profound, unmitigated effects on executive decision-making. A focused study of 133 Small and Medium Enterprise (SME) managers in Morocco highlighted the absolute dominance of emotional and heuristic biases in corporate resource allocation 41. Within this specific Middle Eastern/North African context, highly optimistic managers consistently overestimated future cash flows and routinely engaged in much more frequent, high-risk capital investments than standard financial modeling would advise 41.

Furthermore, the data identified mimicry as a highly influential factor in executive decision-making, with Moroccan executives heavily influenced by the strategic choices of local industry peers rather than isolated financial data 41. Interestingly, intuition bias served a positive, adaptive function in this market; it enabled managers to leverage tacit, culturally embedded knowledge to bypass systemic bureaucratic delays and execute timely investments 41. Unlike the findings in Western professional samples, pure overconfidence displayed no significant independent effect on SME investment frequency in the Moroccan cohort. This divergence explicitly indicates that localized cultural frameworks dictate exactly which specific behavioral biases dominate corporate strategy and risk-taking 41.

Analytical Constraints and Methodological Recommendations

The accumulated empirical literature makes it unequivocally clear that transplanting behavioral economic phenomena derived from WEIRD populations directly to global consumer markets without rigorous cultural calibration generates fundamentally flawed economic models and ineffective public policies 443. Addressing these severe structural deficiencies requires substantial methodological reform within the discipline.

Scaling and Sample Diversity

The historical reliance on simple bipolar comparisons (for example, comparing solely the United States against China) artificially restricts the understanding of behavioral phenomena and frequently results in false dichotomies 12. Researchers have established that accurately evaluating the impact of cultural dimensions demands massively scaled data sets. There is an urgent academic call for a transition away from isolated comparative studies toward midsize (7+ countries) and large-scale (50+ countries) cross-cultural research designs 12. As evidenced by the INTRA study on intertemporal preferences 15 and the extensive meta-analyses on loss aversion 26, massive sample sizes and multinational coverage are strictly required to parse the statistical noise of localized institutional and macroeconomic variables from genuine, deeply rooted cultural divergence.

Integrating Distinct Cultural Baselines

Future behavioral economic research and applied policy design must prioritize establishing distinct baseline calibrations for different geographic and macro-cultural zones. Public policy designs that erroneously assume universal human responses to standard "nudges" or choice architecture - such as automatic enrollment programs or social proof messaging campaigns - risk severe failure if they ignore the local Hofstede or Schwartz dimensional makeup of the target population 844.

By recognizing that phenomena like the endowment effect are intimately tethered to independent self-construal 31, that steep intertemporal discounting is heavily exacerbated by high societal uncertainty avoidance 22, and that loss aversion is magnified by high power distance 29, economists can develop targeted, culturally sensitive interventions. Only by systematically accounting for the dimensional architecture of global cultures can behavioral economics accurately reflect the immense diversity of human decision-making and market behavior.