Comparing Public and Private Colleges on Cost and Outcomes

Stepping onto a sprawling university campus today can evoke the exact same visceral reaction as stepping onto a luxury car dealership lot: sheer, unadulterated sticker shock. With heavily advertised prices bordering on the astronomical, the prospect of acquiring a bachelor's degree appears financially insurmountable to the casual observer. The relentless media narrative surrounding the soaring cost of tuition only amplifies this anxiety, leaving prospective students and their families to wonder if the pursuit of higher education is still a rational economic decision.

Direct Answer: The modern higher education landscape is not a monolith with a single, insurmountable price tag. Rather, it is deeply fragmented into four distinct economic sectors - in-state public, out-of-state public, private non-profits, and private for-profits. Each sector operates on entirely different financial models, pricing strategies, and student outcomes. The true cost of attendance is rarely the advertised price, and the ultimate economic return is dictated less by the name printed on the diploma and significantly more by the specific field of study chosen by the student.

The Bottom Line: To navigate the economics of higher education successfully, prospective students and policymakers must fundamentally divorce the advertised sticker price from the actual net price paid. More importantly, they must prioritize the selection of an academic major over institutional prestige. Empirical data definitively proves that the alignment of a degree with labor market demand yields a substantially higher lifetime return on investment (ROI) than the selectivity of the college attended. Understanding these nuances is the only way to mitigate risk and maximize value in the contemporary educational marketplace.

FAQ: Why Does the Price of College Resemble a Car Dealership? (The MSRP Analogy)

To understand the bewildering nature of college pricing, one must first understand the concept of the Manufacturer's Suggested Retail Price (MSRP) in the automotive industry. When a vehicle is listed with a high MSRP, it anchors the consumer's expectation of value. It signals luxury, quality, and exclusivity. However, very few buyers actually pay the MSRP. Dealerships routinely offer factory rebates, dealer discounts, and negotiation margins that drastically lower the "out-the-door" price. The buyer feels they have secured a premium asset at a steep discount, while the dealership successfully maintains its high-value brand positioning.

Higher education operates on an almost identical psychological and economic pricing model, widely known within the industry as the "high-tuition, high-discount" model 1.

Institutions advertise exceedingly high tuition rates - often approaching or exceeding $80,000 per year at elite private non-profits - which serves as a primary signaling mechanism for prestige and academic rigor 123. This advertised figure is the educational equivalent of the MSRP. However, this figure is highly misleading for the vast majority of students. Underneath this "sticker price" lies a complex apparatus of institutional discount rates. Colleges effectively return a massive portion of their tuition revenue back to students in the form of merit scholarships and need-based grants 12.

The data indicates that at private universities, the institutional discount rate is higher than ever, frequently exceeding 50% across the board 1. In some instances, smaller or mid-tier private colleges return as much as 60% to 70% of their tuition revenue to students via financial aid just to fill seats 1. This creates a fragile, opaque ecosystem that heavily relies on meeting specific enrollment targets to remain solvent.

To accurately assess the financial burden, one must understand two distinct terms: * Sticker Price (Published Price): This is the total published cost of tuition, fees, housing, and food for a student residing on campus, alongside estimated indirect costs like books and transportation 2. * Net Price: This is the actual, out-of-pocket cost a student and their family must cover after all non-repayable grant aid and scholarships are subtracted 22.

This pricing strategy allows universities to engage in sophisticated price discrimination. Wealthy families who can afford to pay the full sticker price do so, effectively subsidizing the education of lower-income students who pay a heavily discounted net price. Consequently, reacting to the sticker price of a university without utilizing a net price calculator is akin to walking away from a car lot because the MSRP was too high, without ever sitting down at the desk to ask the dealer for the actual sale price 23.

FAQ: What Are the Distinguishing Economic Features of In-State Public Universities?

Public four-year institutions represent the bedrock of American higher education. They are generally large, state-subsidized enterprises designed to provide accessible, high-quality education to the residents of their specific state.

Enrollment Scale and Demographics

Public four-year universities operate on massive economies of scale. In the fall of 2021, nearly half (48%) of all undergraduate students in the United States were enrolled in public four-year institutions 3. By 2024, public four-year universities accounted for approximately 7.4 to 8.2 million undergraduate students out of the roughly 15.3 million to 16.7 million total undergraduates nationwide 458.

Because these institutions are state-funded, their enrollment sizes are typically the largest in the country, often resembling small cities with tens of thousands of students on a single campus. This scale allows them to offer a vast array of majors, extensive extracurricular networks, and massive research facilities. However, this scale can sometimes come at the cost of larger introductory class sizes and less personalized administrative support compared to private liberal arts colleges.

Overall enrollment at these institutions has seen a recent post-pandemic rebound. The National Student Clearinghouse Research Center reported that in Spring 2025, total postsecondary enrollment rose by 3.2% (+562,000 students), with undergraduate enrollment specifically growing by 3.5% 5. This growth is notable among minority populations, with Black (+10.3%) and multiracial (+8.5%) undergraduate students seeing the largest growth 5. The racial and ethnic makeup of public four-year institutions is generally the most representative of the overall U.S. population compared to other sectors 3.

The Financial Proposition

The economic advantage of the in-state public university lies in state taxpayer subsidies, which directly suppress the tuition costs for state residents. State and local funding per student for public higher education averaged $11,680 in the 2023 - 2024 academic year, significantly offsetting the actual cost of educational delivery 6.

For the 2024 - 2025 academic year, the College Board reported that the average published sticker tuition and fees for full-time, in-state undergraduate students was $11,610 12. Moving into the 2025 - 2026 academic year, this figure rose slightly to $11,950 (a 2.9% increase before adjusting for inflation) 6. When factoring in room and board, the total sticker cost of attendance reaches approximately $28,840 to $29,910 annually 12.

However, applying the MSRP analogy, the net price tells a much more favorable economic story. After adjusting for federal, state, and institutional grant aid, the average net tuition and fees paid by first-time, full-time in-state students at public four-year universities peaked in 2012-13 at $4,450 (in constant 2025 dollars) and has subsequently declined to an estimated $2,300 to $2,480 for the 2024 - 2026 academic cycles 2610. When adding the necessary costs of living, the total net cost of attendance averages roughly $20,780 to $20,800 per year 11.

Post-Graduation Debt

Because the net cost is highly subsidized and relatively low, in-state public university graduates generally carry the most manageable debt loads among four-year graduates. The average post-graduation debt for a student earning a bachelor's degree at a public university is approximately $31,960 1213.

More remarkably, looking at the entire cohort, about half of all students at four-year public universities finish their bachelor's degrees without any debt whatsoever 7. Nearly eight in ten (78%) graduate with less than $30,000 in debt, and only 4% leave with more than $60,000 7. For those who do borrow, this represents a relatively modest and manageable amount of student debt, especially when viewed against the lifetime earnings premium a bachelor's degree provides.

FAQ: How Do Out-of-State Public Universities Alter the Value Proposition?

When a student crosses state lines to attend a public university in another state, the economic calculus shifts violently. Out-of-state public education operates largely as a revenue-generating mechanism for state school systems that have faced decades of fluctuating or declining state legislative appropriations.

The Cross-Subsidization Strategy

Public universities charge out-of-state students a massive premium because these students and their families do not pay taxes into the state's educational coffers. For the 2024 - 2025 academic year, the average published tuition and fees for out-of-state undergraduates was $30,780, and is projected to rise to $31,880 for the 2025 - 2026 academic year 2615. This represents an enormous leap from the $11,950 charged to in-state residents 6.

When housing, food, and other indirect expenses are added, the total advertised cost of attendance for an out-of-state student skyrockets to between $46,730 and $49,080 per year 12.

Net Price and the Lack of Aid

The critical danger of out-of-state public education is that the institutional discount rate is exceedingly low for non-residents. States rarely offer generous need-based grants to out-of-state students, reserving those funds for their own taxpayers. Consequently, the sticker price and the net price for out-of-state students are often uncomfortably close.

Data indicates that out-of-state students are charged an average net cost of roughly $49,100 per year 11. This means they capture very little of the grant aid that heavily discounts private or in-state public education.

From an ROI perspective, attending a mid-tier public university out-of-state is frequently one of the poorest financial decisions a family can make. The student pays private-school prices without receiving private-school financial aid, the smaller class sizes, or the exclusive alumni networks typically associated with premium tuition costs. Unless the out-of-state university offers a highly specialized, top-ranked program not available in the student's home state, or provides massive, anomalous merit aid, the ROI is severely diluted by the exorbitant net cost.

FAQ: Are Private Non-Profit Institutions Worth the Premium Price?

Private non-profit colleges and universities - a broad category ranging from elite Ivy League institutions to small regional liberal arts colleges - represent the most prestigious, yet most economically complex, sector of higher education.

Enrollment and Scale

Unlike their public counterparts, private non-profit institutions intentionally restrict enrollment to maintain low student-to-faculty ratios, foster intimate academic environments, and preserve exclusivity. There are more than 1,700 private, non-profit colleges in the U.S., enrolling students across all 50 states 8. However, their total undergraduate enrollment is significantly smaller than the public sector. In 2024, private non-profit 4-year institutions enrolled approximately 2.83 million undergraduates 4.

The scale of these institutions is starkly different. The median enrollment size for a four-year private, non-profit institution is extraordinarily small at just 1,255 students, with one out of five having fewer than 250 students 8.

The Fragile Financial Ecosystem

The sticker price at private non-profits is notoriously high, generating intense media scrutiny. For the 2024 - 2025 year, average tuition and fees alone were $43,350, climbing to an estimated $45,000 for the 2025 - 2026 year 26. Total cost of attendance, including room and board, averaged between $60,420 and $63,000, with many elite, highly selective institutions now pushing past $80,000 to $90,000 annually 1211.

Yet, this sector relies heavily on the aforementioned "high-tuition, high-discount" model. Because of massive institutional endowments (at elite schools) and aggressive discounting strategies (at regional schools), the average net tuition and fees paid by a first-time, full-time student at a private non-profit dropped to an estimated $16,910 for the 2025-2026 academic year 6. The total average net cost of attendance, which factors in living expenses, settles around $36,150 to $36,200 11.

While elite, highly selective private universities have massive endowments that allow them to offer generous, debt-free financial aid packages to middle- and lower-income families, smaller regional private colleges do not have this luxury 17. These smaller schools use tuition discounting simply to survive and attract students, creating an unsustainable trajectory where they return up to 70% of revenue to students just to meet enrollment targets 1.

Post-Graduation Debt

Despite the heavy discounting, the net cost remains tangibly higher than in-state public options. Consequently, the average private non-profit university student graduates with approximately $39,510 in student loan debt 13, with other estimates pointing to an average borrowed amount of $33,910 to $42,449 to complete a bachelor's degree 18.

FAQ: What is the Reality of Private For-Profit Colleges in the Modern Economy?

The private for-profit sector operates on a fundamentally different structural model: a corporate model designed to generate financial returns for investors and shareholders while providing educational services. Historically, this sector experienced explosive, rapid growth in the 1990s and 2000s, but it has faced severe regulatory scrutiny, lawsuits, and declining enrollments in recent years due to highly disproportionate debt-to-earnings outcomes 9.

Target Demographics

For-profit colleges enroll a distinct demographic that differs sharply from traditional four-year public and non-profit universities. Their students are disproportionately older, female, African American, and far more likely to be single parents 9. Additionally, many students entering for-profit institutions are less likely to have graduated from high school with a traditional diploma 9. As of 2024, enrollment in four-year, for-profit institutions sits at roughly 640,000 undergraduate students, representing a small fraction of the total student body nationwide 4.

Cost, Debt, and Outcomes

The published tuition at for-profit institutions averages roughly $15,868 per year 1020. While this initially appears cheaper than private non-profits, the financial architecture works against the student. For-profit colleges offer virtually no institutional grant aid, largely because their primary fiduciary directive is to pass profits to shareholders, not to discount revenue for students 20. Consequently, students must rely almost entirely on federal and private student loans to cover their educational and living expenses 2021.

The outcomes in this sector represent a statistical anomaly compared to the rest of higher education, leading to its controversial status: * Highest Debt Loads: For-profit students borrow the most, graduating with an average debt ranging from $40,970 to $47,730, and in some metrics up to $49,700 131820. * High Default Rates: Because these degrees often lack strong labor market signaling, graduates frequently experience underemployment or unemployment. The three-year loan default rate for private for-profit students is 14.7%, vastly higher than the 6.39% rate at private non-profits 21. * Low Completion: College students who enroll at for-profits are statistically the least likely to actually complete their degree program, often leaving them with the worst possible outcome: student debt without the wage premium of a completed degree 9.

Comparative Visual Aid: Institutional Sector Analysis

To synthesize the vast discrepancies in pricing, scale, and debt across the primary higher education sectors, the following table presents a direct comparison utilizing 2023 - 2025 aggregated data. This allows for a clear, side-by-side evaluation of the economic realities facing students based on institutional choice.

| Institutional Sector | Average Sticker Price (Tuition + Room & Board) | Average Net Price (Total Out-of-Pocket COA) | Average Enrollment Size (Institutional Median/Scale) | Average Post-Graduation Debt (Bachelor's) |

|---|---|---|---|---|

| In-State Public (4-Year) | ~$28,840 - $29,910 | ~$20,780 | 10,000+ (Large Scale) | ~$31,960 |

| Out-of-State Public (4-Year) | ~$46,730 - $49,080 | ~$49,100 | 10,000+ (Large Scale) | High (Limited Grants) |

| Private Non-Profit (4-Year) | ~$60,420 - $63,000 | ~$36,150 | 1,255 (Small/Intimate) | ~$39,510 |

(Note: Private For-Profit institutions are excluded from this specific visualization due to their fundamentally different corporate structure and lack of institutional grant aid, but average post-graduation debt in that sector is the highest at $47,730).

FAQ: What is the True Scale of the Post-Graduation Debt Crisis?

The discussion of higher education costs invariably leads to the student loan debt crisis - a topic of immense political and economic debate. As of early 2025, total student loan debt in the United States reached a staggering $1.77 trillion, making it the second-largest category of consumer debt behind mortgages 1322. Approximately 42.7 million to 43.6 million borrowers carry this debt, with the overwhelming majority (92.4%) funded directly by the federal government rather than private lenders 2223.

The Distribution of Debt

While the macro number of $1.77 trillion is intimidating, the micro-level distribution reveals critical nuances that are often lost in popular media narratives. The "average" student loan debt per borrower is approximately $38,883 22. However, this average is heavily skewed by a small percentage of extremely high-balance borrowers.

To understand the reality of the crisis, one must look at the distribution brackets: * Roughly 53% to 56% of borrowers owe less than $20,000 in student debt 1810. * Approximately 17% of borrowers owe less than $5,000 22. * Conversely, about 8.4% of borrowers (approximately 3.6 million people) owe more than $100,000 182225.

The Graduate Degree Escalator

A significant portion of the $1.77 trillion crisis is not driven by traditional undergraduate bachelor's degrees, but by graduate and professional education. The federal government places strict statutory limits on how much an undergraduate can borrow (e.g., $31,000 total for a dependent undergraduate over four years) 10. However, graduate students can borrow up to the full cost of attendance (minus other aid) through the federal Grad PLUS loan program 10.

As a result, borrowers holding master's degrees owe an average of $69,140, while law school and medical school graduates average $140,000 and $200,000 in debt, respectively 18. The average outstanding balance on a Grad PLUS loan alone is $65,111 18. Thus, the narrative that bachelor's degree graduates are uniformly drowning in six-figure debt is statistically false; extreme debt burdens are overwhelmingly concentrated among those holding advanced degrees or those who attended high-cost private institutions without completing their degrees 1011.

Geographic and Demographic Disparities

Debt burdens are not distributed equally across the country or across demographic groups. The economic strain is highly localized.

Table 1: State-Level Variations in Average Student Debt (Selected Highlights)

| State | Average Debt per Borrower | Nationwide Ranking |

|---|---|---|

| Maryland | $43,116 | Highest |

| Georgia | $41,775 | 2nd Highest |

| Virginia | $39,599 | 3rd Highest |

| North Dakota | ~$30,000 | Lowest |

Data sourced from Office of Federal Student Aid and Education Data Initiative 27.

Furthermore, student debt exacerbates existing racial wealth disparities. According to the Federal Reserve's Survey of Consumer Finances, the burden of debt falls disproportionately on minority populations.

Table 2: Average Student Loan Debt by Race and Ethnicity (2022)

| Demographic Group | Average Student Loan Debt |

|---|---|

| Black, non-Hispanic adults | $53,430 |

| Adults of other races | $51,810 |

| White, non-Hispanic adults | $46,140 |

| Hispanic adults | $26,460 |

Data sourced from the Federal Reserve Survey of Consumer Finances 25.

Black borrowers historically face higher debt levels and slower repayment trajectories. This is due to systemic labor market wage gaps, lower levels of intergenerational wealth to assist with tuition, and a higher likelihood of attending for-profit institutions, which carry heavier debt loads and lower ROIs 2511.

FAQ: Does the Prestige of the Institution Outweigh the Choice of Major? (The ROI Equation)

For generations, American families have obsessed over college rankings and brand-name prestige, operating under the assumption that an elite institutional name on a diploma is the ultimate key to lifetime economic security. However, comprehensive longitudinal research, particularly from the Georgetown University Center on Education and the Workforce (CEW), has mathematically dismantled this assumption.

The Baseline Premium of a Bachelor's Degree

First, it must be established that obtaining a bachelor's degree remains the safest overall economic bet. Prime-age workers (ages 25 - 54) with a bachelor's degree earn 70% more at the median ($81,000) than workers with only a high school diploma, and they face much lower unemployment rates (2.9% vs. 6.2%) 121314. Over a 40-year career, this translates to a median lifetime earnings premium of roughly $1.2 million compared to a high school graduate 71731.

Even when economists rigorously discount this figure for the "time value of money" - accounting for the years spent out of the workforce studying and the upfront cost of tuition - the net present value premium remains a highly positive $593,000 to $786,000 31.

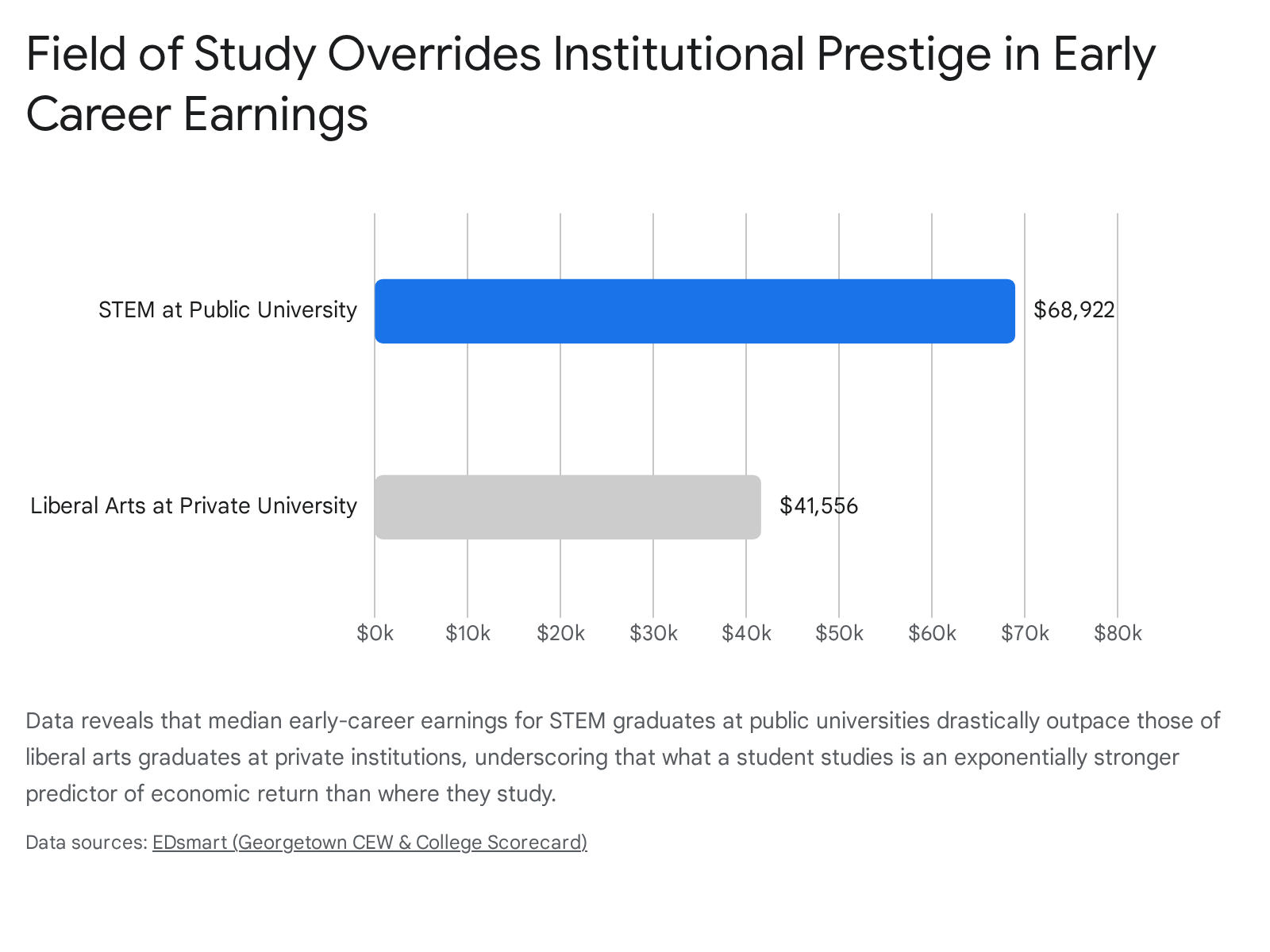

The Prestige Paradox: Major > Institution

While the overall college premium is positive, the variance within the college-educated population is extreme. The Georgetown CEW research proves that what you study matters up to three times more than where you study it 32.

Median earnings vary significantly by specific major, ranging from $51,000 to $146,000 annually 13. For example, early-career workers with a major in Computer Science enjoy a median salary of $86,000, while those majoring in Communication Disorders earn just $34,000 15. A major in early childhood education pays $3.3 million less over a career than a major in petroleum engineering 16.

This creates a phenomenon known as the "Prestige Paradox." Consider two hypothetical students. Student A attends a mid-tier public university and majors in a STEM field (Science, Technology, Engineering, or Mathematics). Student B attends an elite, highly selective private liberal arts college and majors in the humanities. * The median earnings for a STEM major at a public university are $68,922 32. * The median earnings for a liberal arts major at a private university are $41,556 32.

Despite lacking the elite brand name, the public university STEM graduate will out-earn the elite private school humanities graduate by an average of $27,365 per year 32. Over a 40-year career, this difference approaches $1.1 million - effectively negating the entire concept of the institutional prestige premium for the vast majority of students 32.

Sub-Baccalaureate Credentials and Double Majors

The ROI conversation extends beyond just the four-year degree. Sub-baccalaureate credentials (certificates and associate's degrees) often yield incredibly fast returns. A one-year information-technology certificate holder can earn up to $72,000 per year, compared with $54,000 for the average bachelor's degree holder 16. In fact, 30% of associate's degree holders make more than the average four-year degree holder early in their careers 16. While the 40-year ROI of a bachelor's degree eventually outpaces the associate's degree, the speed to market and lower cost of two-year programs present a highly viable alternative for students 14.

Furthermore, for students pursuing the humanities, data suggests that "double majoring" can be an effective hedge. Combining a liberal arts major with a STEM or business major yields higher returns than a single liberal arts major alone, providing the student with both the hard quantitative skills demanded by the market and the soft analytical skills fostered by the humanities 17.

The Exception: The Top 1% of Elite Outcomes

There is one notable caveat to the "Major > Institution" rule. While the median outcomes aggressively favor the choice of major, elite universities disproportionately control access to the absolute highest echelons of the labor market - the top 1% 17. Graduates of the most selective Ivy League-tier institutions have access to exclusive alumni networks and direct pipelines to top-tier finance, management consulting, and high-level corporate roles that are often entirely closed off to regional public university graduates 17. Ivy League alumni make up less than 1% of U.S. college graduates yet over 20% of the nation's top 1% of earners 17.

However, for the 99% of students who are not heading to elite Wall Street firms, the combination of a high-demand major and a low-cost public institution provides the highest mathematically probable return on investment 32.

FAQ: How Should Families Navigate College Selection Today? (Practical Takeaways)

The modern higher education environment requires a tactical, highly analytical approach. Applying a strategy of calibrated uncertainty, families must recognize that while historical data strongly supports the value of a degree, the future labor market remains in a state of flux.

1. Ignore the Sticker Price and Utilize Net Price Calculators Never eliminate a private college based solely on its published tuition rate. Because of discount rates exceeding 50%, a private non-profit might actually cost less out-of-pocket than an out-of-state public university 11011. Families must aggressively utilize Net Price Calculators, required on every college website, to reveal their specific expected costs based on their financial information and the student's academic record 2.

2. Optimize for the First Job and Align Major with Demand The labor market is becoming increasingly unforgiving for graduates without hard skills. While the humanities foster critical thinking and citizenship, the immediate economic returns are structurally constrained 3236. If a student pursues a low-ROI major, they must fiercely mitigate their student loan debt, as they will lack the salary velocity to pay off large balances 36. Conversely, high-ROI majors like engineering can tolerate higher debt loads, though minimizing borrowing remains optimal.

3. Factor in Artificial Intelligence and Automation Calibrated uncertainty is required when viewing today's salary data through the lens of emerging technology. Generative AI is rapidly altering the demand for entry-level cognitive work 37. In a 2025 Gallup and Lumina Foundation survey, 47% of college students reported considering switching their majors due to the potential impact of AI 37. Between 2022 and 2025, early-career workers in AI-exposed occupations (like software development and clerical work) experienced relative employment declines 37. Recent computer science graduates boast high median earnings ($79,000) but are also facing the highest unemployment rate in all STEM fields (6.8%) as AI reduces demand for entry-level coding 1437. Conversely, fields requiring intense human interaction (nursing, healthcare) or physical world manipulation face far less disruption 1415. A degree program's ROI today may not perfectly mirror its ROI a decade from now.

4. Reject the Out-of-State Public Trap Unless an out-of-state public university offers a highly specialized, top-ranked program not available in the student's home state, or provides massive merit aid that brings the cost down to in-state levels, paying the $49,000+ net cost is generally a poor deployment of capital 11. It offers neither the subsidized affordability of an in-state school nor the prestigious networking power of an elite private institution.

Conclusion

Just as purchasing a vehicle based solely on the MSRP or the hood ornament often leads to deep financial regret, selecting a college based purely on its advertised price or historical prestige is an outdated, high-risk strategy in the modern economy.

Direct Answer: The data is unequivocal. To extract the maximum economic value from higher education, students must leverage the high-tuition/high-discount model to their advantage, aggressively favoring in-state public institutions or heavily discounted private non-profits to minimize debt. They must recognize that out-of-state public universities often represent the worst mathematical value, and that for-profit institutions carry excessive risks regarding debt and default.

The Bottom Line: Ultimately, the greatest financial risk in higher education is not attending a less prestigious school; the greatest risk is borrowing heavily to fund a degree that the labor market does not value. While the future trajectory of the workforce under the influence of artificial intelligence dictates a healthy dose of calibrated uncertainty, the fundamental math remains unchanged: the skills acquired through a chosen major will dictate a graduate's lifetime earnings far more powerfully than the name of the institution printed on their diploma.