Business model innovation and incumbent adaptation challenges

The competitive lifespan of corporate business models has compressed dramatically, declining from an average of fifteen years a half-century ago to fewer than five years in the contemporary economic environment 1. In a global market characterized by rapid technological advancement, shifting demographics, and accelerating digital transformation, achieving sustainable competitive advantage requires organizations to look beyond the continuous refinement of existing products or the incremental optimization of internal processes. Business model innovation (BMI) has subsequently emerged as the critical determinant of long-term corporate survival, outperforming traditional product innovation in both durability and financial return 2.

However, historical and empirical evidence demonstrates that established market incumbents consistently struggle to navigate disruptive business model transitions. Rather than suffering from a lack of technological capability or capital, incumbents are frequently paralyzed by deep-rooted organizational, cognitive, and structural barriers. This analysis examines the conceptual boundaries of business model innovation, deconstructs the architecture of disruptive business models, and explores the theoretical mechanisms - specifically Resource Dependence Theory, fear of cannibalization, and cognitive dominant logic - that explain incumbent failure. Furthermore, it outlines structural strategies, such as organizational ambidexterity, autonomous spin-offs, and corporate venture capital, that legacy organizations deploy to overcome these entrenched vulnerabilities.

Conceptual Foundations of Business Model Innovation

To analyze why incumbents struggle to replicate disruptive models, it is necessary to establish the definitional boundaries of business model innovation and distinguish it from traditional forms of corporate innovation.

Distinction from Product and Process Innovation

In corporate strategy, innovation is traditionally categorized into three primary domains: product, process, and business model innovation 34.

Product innovation focuses on the development of novel goods or the enhancement of existing services. It represents a tangible change in what a company sells, driven by technological advancements, shifting consumer preferences, or the need to solve specific user problems 35. Process innovation, conversely, is an internal optimization strategy. It entails the implementation of new technologies, operational frameworks, or manufacturing capabilities designed to reduce production costs, improve quality, or accelerate time-to-market 45. Both product and process innovations are generally incremental; they reinforce the existing market trajectory and sustain the firm's established competitive positioning 56.

Business model innovation operates on a structurally different and highly complex plane. It involves simultaneous, mutually supportive changes to an organization's value proposition and its underlying operating model 17. A business model encapsulates four core components: the customer value proposition (how the firm creates value), the target market segment (for whom value is created), the value chain and operating model (how value is delivered), and the revenue mechanism (how the firm captures value and generates profit) 287. BMI occurs when an organization alters two or more of these foundational elements to deliver value to the market in a fundamentally new way 2. It does not necessitate the invention of a new product; rather, it reinvents the mechanism through which an existing product or service interfaces with the market 45.

The COMETS framework (Cooperation, Organization, Market, Execution, Technology, and Strategy) provides a structured lens to compare the requirements of new product development versus business model innovation 8. While product development focuses on technological execution and market delivery within existing strategic parameters, BMI requires a fundamental reorganization of cooperative networks and corporate strategy, presenting significantly higher organizational complexity 8.

Value Proposition and Operating Model Architecture

The architecture of a business model dictates its vulnerability and its strength. At the value proposition level, changes can address the choice of target segment, the product or service offering, and the revenue model 1. At the operating model level, the focus is on how to drive profitability and competitive advantage through decisions regarding where to play along the value chain, what cost model is necessary to ensure attractive returns, and what organizational structure and capabilities are essential to success 12.

The complexity of these interdependent elements means that BMI is not a single-function strategy, such as merely enhancing a sourcing approach or altering a sales tactic. It involves a multidimensional orchestration of activities across the entire enterprise 2. For example, transitioning from a traditional hardware sales model to a software-as-a-service (SaaS) or product-as-a-service (PaaS) model fundamentally alters revenue recognition, customer relationship management, product engineering, and internal incentive structures simultaneously 1.

Imitability and Cross-Functional Complexity

The strategic superiority of business model innovation lies in its imitability profile. Product innovations are highly visible to competitors and, barring stringent intellectual property protections, can be reverse-engineered and commoditized relatively quickly 4. Process innovations, while internal and somewhat opaque, frequently rely on standardized enterprise software or manufacturing equipment that competitors can procure on the open market 45.

By contrast, business model innovation is deeply integrated into the firm's organizational structure. Because it orchestrates cross-functional dependencies - merging novel pricing strategies, redefined customer relationships, and entirely new supply chain logistics - it is exceedingly difficult for competitors to replicate without undergoing massive internal reorganization 211. Consequently, firms that successfully execute BMI enjoy a more durable competitive advantage and yield financial returns that significantly outperform those generated by mere product or process improvements 2. Empirical research indicates that business model innovators have historically earned an average premium that is more than four times greater than that enjoyed by product or process innovators 2.

| Innovation Typology | Primary Objective | Locus of Change | Capital & Resource Requirements | Risk Profile | Imitability by Competitors |

|---|---|---|---|---|---|

| Product Innovation | Increase revenue and market share via new features or offerings. | External (The Offering) | Highly concentrated in Research & Development (R&D). | Moderate to High | High (easily reverse-engineered or copied). |

| Process Innovation | Reduce operational costs, enhance efficiency, and improve quality. | Internal (The Operations) | Concentrated in manufacturing, IT, and supply chain. | Low | Moderate (often relies on accessible third-party technology). |

| Business Model Innovation | Create, deliver, and capture value through fundamentally new structural logic. | Systemic (The Organizational Logic) | Diffused across the entire enterprise; requires cross-functional capital. | Very High | Low (requires profound structural and cultural mimicry). |

The Mechanics of Disruptive Business Models

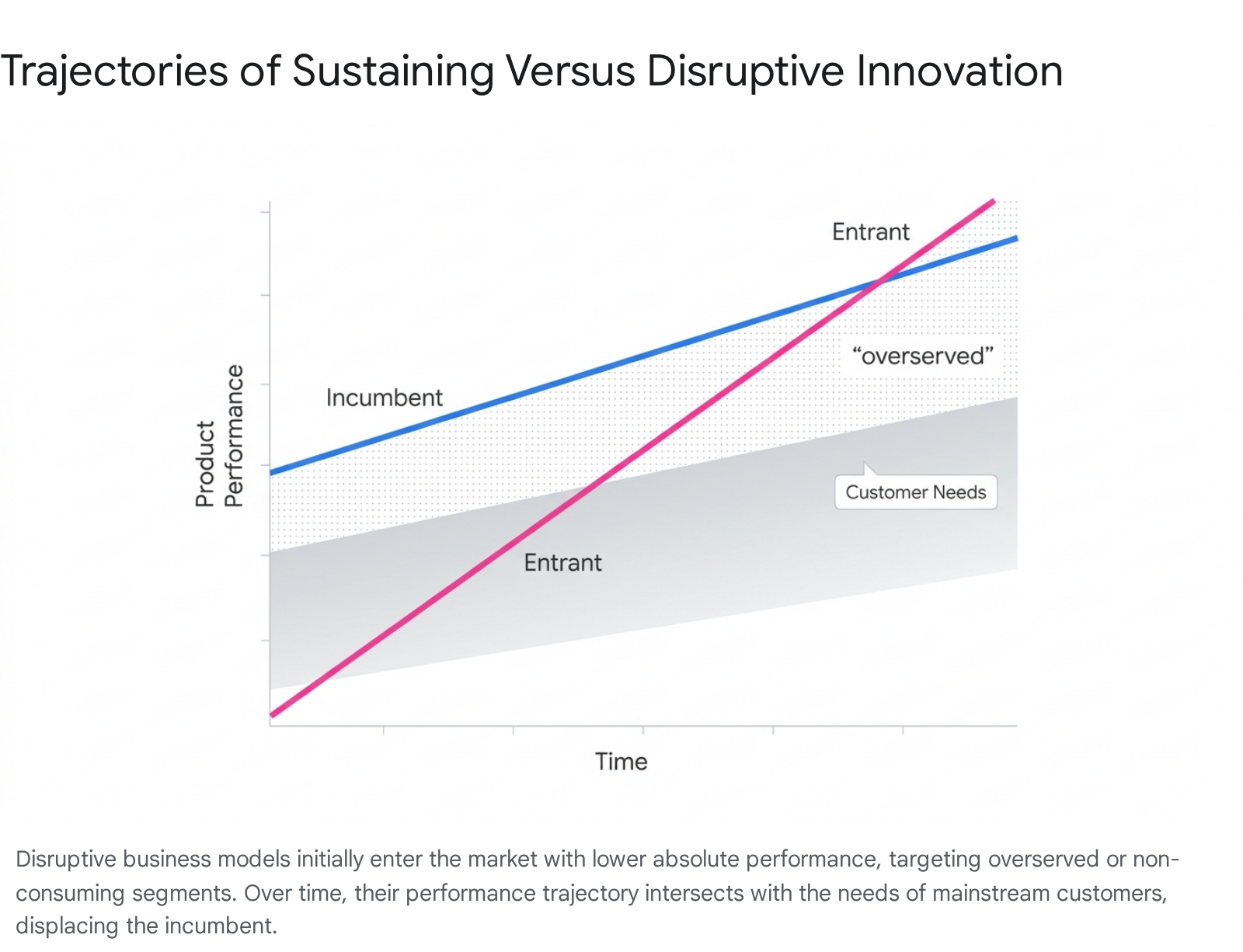

Business model innovation frequently serves as the delivery mechanism for market disruption. Disruptive innovations, a concept formalized by academic research, are not necessarily breakthrough technological advancements that make good products better. Rather, they are innovations that make products and services simpler, more accessible, and more affordable, thereby opening them to a vastly larger population 91011.

Asymmetric Competition and Non-Consumption

The theory of disruptive innovation dictates that disruption typically initiates at the bottom of a market or in an entirely new market segment 91012. Incumbent organizations instinctively pursue "sustaining innovations" - incremental improvements designed to satisfy their most demanding, highest-paying customers. This relentless march upmarket inadvertently overserves the lower tiers of the market and ignores consumers who lack the resources or expertise to participate in the traditional market 1011.

Disruptive business models capitalize on this vacuum. Entrants leverage BMI to target these overserved or ignored segments with offerings that are initially inferior in absolute performance but superior in cost, convenience, and simplicity 1113. By doing so, the disruptor engages in asymmetric competition. They do not fight the incumbent for its core customers; instead, they compete against non-consumption, bringing entirely new consumers into the market ecosystem 13. As the disruptor refines its model and improves its technological capabilities, it relentlessly moves upmarket, eventually displacing the incumbent whose rigid cost structures and business models cannot compete at lower price points 912.

A classic illustration of this phenomenon is the displacement of blockbuster video rentals by streaming services. The incumbent optimized its business model to extract maximum value from late fees and physical store networks. The disruptor introduced a business model (subscription-based, zero late fees, DVD-by-mail) that was initially inferior for consumers seeking immediate gratification. However, it captured a niche market, evolved into streaming as broadband infrastructure matured, and eventually rendered the asset-heavy business model obsolete 910.

Market Leapfrogging and Infrastructure Substitution

The mechanics of disruptive business model innovation are particularly evident in emerging markets, where geographical and infrastructural contexts facilitate technological and commercial "leapfrogging." When a market lacks entrenched legacy infrastructure, entrants are unburdened by the need to integrate with or compliment outdated systems, allowing them to engineer radical business models from the ground up 14.

A profound example is the evolution of mobile payment business models. In advanced Western economies, mobile payments generally rely on a "card-complementing" business model. Because these markets possess deep, legacy credit card and banking networks, innovation is layered on top of existing financial rails, effectively acting as a digital skin for legacy systems 1516. Conversely, in emerging markets across Africa and Asia, massive unbanked populations and an absence of legacy financial infrastructure enabled the rapid adoption of "card-substituting" technologies 15.

Platforms like Kenya's M-Pesa bypassed traditional banking models entirely, allowing users to deposit, transfer, and withdraw funds via mobile text and a network of local physical agents 1520. This structural leapfrogging drastically reduced transaction costs, catered directly to non-consumers, and created an entirely new financial ecosystem built exclusively around mobile telecommunications 1415. Advanced and developing economies thus display a non-monotonic relationship with mobile payment adoption; leapfrogging allows some developing nations to surpass advanced economies in mobile financial maturity 1516.

Emergence of Ecosystem Platforms and Super-Apps

The card-substituting leapfrog paved the way for the "Super-App" business model - a uniquely Asian BMI paradigm that Western incumbents have systematically failed to replicate 171819. A super-app, such as WeChat, Alipay, Grab, or Gojek, bundles a multitude of services - ride-hailing, food delivery, logistics, e-commerce, and digital lending - into a single, unified digital platform underpinned by an integrated digital wallet 1819202122. The global super-app market is projected to expand significantly, with Asia-Pacific accounting for the vast majority of this growth due to mobile-first populations 19.

The super-app business model fundamentally changes the mechanics of corporate value capture. These platforms often begin with high-frequency, low-margin core services, such as mobility or food delivery, to acquire massive user bases and construct an impenetrable data moat 192227. However, their long-term profitability and economic viability rely on cross-selling high-margin financial services, advertising, and merchant solutions 192227. Grab, for instance, reported that while its mobility and delivery segments drove initial volume, its financial services revenue grew by 37 percent year-over-year in recent quarters, alongside high-margin advertising revenue sourced from merchants seeking visibility within the platform ecosystem 1922.

By functioning as orchestrators of a massive digital ecosystem, super-apps lock in users and capture value at every node of the consumer's daily life, effectively operating as a parallel digital infrastructure 172123. WeChat, operated by Tencent, offers access to millions of "mini-programs" within its main interface, allowing third-party developers to access its user base without requiring users to download separate applications 172129.

Western incumbents, constrained by siloed application mentalities, strict regulatory divisions between banking and consumer technology, and deeply entrenched legacy payment models, struggle to orchestrate the multidimensional ecosystems required to compete with this paradigm 18192924.

Digital Platform Lock-in and Modularity

The transition from linear "pipeline" business models to digital platform models introduces new strategic dynamics, particularly concerning ecosystem orchestration and vendor lock-in. Companies adopting digital platforms must navigate the gravitational pull of data; as platforms accumulate user data and tailor algorithms to specific business needs, switching costs increase exponentially 25.

This deep platform lock-in presents a strategic dilemma. While heavy customization of digital platforms improves immediate operational efficiency, it increases data gravity and platform stickiness, leaving the firm vulnerable to vendor pricing power 25. Organizations must therefore develop a distinct set of capabilities, including continuous market scanning, financial operations analytics, and strict data sovereignty protocols, to maintain modularity 2526. Maintaining control over internal data models and designing modular extensions helps preserve agility and reduces the switching costs that otherwise paralyze legacy firms attempting to adopt digital ecosystem strategies 25.

Theoretical Drivers of Incumbent Inertia

Despite vast financial resources, advanced technical capabilities, and deep market experience, corporate incumbents frequently fail to adapt to disruptive business model innovations 27. This failure is rarely due to managerial incompetence; rather, it is a structural inevitability explained by several overlapping theoretical frameworks, chief among them Resource Dependence Theory, the fear of cannibalization, and cognitive rigidity.

Resource Dependence Theory and Capital Allocation

Resource Dependence Theory (RDT) posits that organizations are not entirely autonomous entities; their survival is contingent upon the acquisition of resources from external actors within their environment 282930. In a corporate context, a firm's most critical external actors are its customers and its investors. Consequently, while corporate executives appear to direct organizational strategy, RDT suggests that customers and investors ultimately dictate how a company allocates its capital and resources 31.

This theory elucidates the innovator's dilemma. Incumbent firms are rational actors designed to maximize shareholder value. Therefore, their resource allocation processes are heavily biased toward sustaining innovations that promise high margins and satisfy the immediate demands of their most profitable legacy clients 1131. When an internal engineering team proposes a disruptive business model - which initially targets unproven market segments, promises lower gross margins, and alienates current high-paying customers - the organization's resource allocation mechanisms naturally reject it. The innovation starves because it cannot secure the financial backing or executive sponsorship required to scale, as it fails to satisfy the immediate needs of the resource providers 31.

The history of Xerox's Palo Alto Research Center (PARC) serves as a profound historical illustration of RDT in action. Xerox developed groundbreaking technologies, including the graphical user interface and ethernet networking. However, the corporate parent failed to commercialize these innovations because they did not align with the company's existing business model, which relied on the architecture of revenues derived from high-volume copier sales 32. Because the technological opportunity disrupted the firm's current business model rather than reinforcing it, the internal resource allocation processes constrained the selection of new target markets, allowing external entrants to eventually capitalize on the innovations 32.

Cannibalization Dynamics and Core Business Protection

Compounding the resource allocation dilemma is the profound corporate fear of product cannibalization. Cannibalization occurs when a company introduces a new product or business model that directly competes with, and diminishes the market share or revenue of, its existing core offerings 3933.

For established incumbents, the core business represents a massive sunk cost in infrastructure, branding, and institutional knowledge. Protecting these lucrative cash cows becomes the overriding strategic imperative 3442. As a result, incumbents routinely shelve or delay business model innovations that threaten their legacy operations. Kodak, for example, invented digital photography technology but notoriously delayed its commercialization to protect its highly profitable film and chemical processing divisions 393443. By the time they fully embraced the digital model, external competitors had overtaken them. Similarly, Nokia faltered during the smartphone transition because its feature phone business was too entrenched to pivot quickly 34.

Organizations that successfully navigate disruptive transitions frequently embrace "proactive self-cannibalization." They recognize that if they do not cannibalize their own market share, a disruptor eventually will 42. Apple explicitly embraced self-cannibalization when it introduced the iPhone, fully aware that the device would devastate the sales of its highly profitable iPod line. By accepting the destruction of one business model, Apple secured the foundation for a vastly more lucrative, ecosystem-driven smartphone platform 3334. In the absence of this proactive destruction, incumbents are inevitably eaten from below.

Cognitive Rigidity and Dominant Managerial Logic

Beyond resource constraints, incumbents suffer from severe cognitive barriers. The leadership teams of established firms operate under a "dominant logic" - a deeply ingrained set of heuristics and cultural beliefs regarding how the firm creates value and generates profit 1132.

When confronted with a disruptive business model that contradicts this dominant logic, managerial cognitive frameworks often fail to accurately assess the threat or opportunity. The inherent complexity and uncertainty of an unproven business model make it difficult for executives to project financial returns, leading to a bias toward the status quo 113536. Furthermore, because disruptive innovations often utilize entirely different metrics for success - such as user acquisition, network effects, and ecosystem engagement, rather than immediate gross product margins - incumbents applying legacy financial modeling techniques incorrectly dismiss the disruptive model as economically unviable 3236.

This cognitive rigidity is not exclusive to massive multinational corporations. Surveys of small and medium-sized enterprises (SMEs) demonstrate that a lack of managerial know-how and an inability to perceive the need for change are primary barriers to business model innovation across firm sizes 1135. Without the appropriate cognitive representations to develop strategic sensitivity, leadership remains blind to shifting market paradigms 37.

Organizational and Structural Barriers to Replication

Even when an incumbent's leadership accurately perceives a threat and demonstrates a willingness to embrace business model innovation, the firm's physical and organizational structure often prevents successful execution.

Operational Inflexibility and Legacy Assets

Incumbents are built for operational efficiency and the continuous exploitation of their existing value chains. Their organizational structures, IT systems, supply chain logistics, and employee incentive programs are heavily optimized for their specific legacy business model 11353839.

Attempting to implement a new business model within this rigid architecture frequently leads to severe institutional friction. A transition from a traditional manufacturing pipeline model to a digital platform operating model requires an entirely different operational cadence 2526. Pipeline models rely on linear supply chains and sequential value creation; platform models require ecosystem orchestration, API integrations, third-party vendor management, and modular data architectures 2526. For an incumbent, maintaining legacy operations while simultaneously attempting to rewire its enterprise architecture to support a platform model creates devastating operational complexities, resulting in slow execution that allows agile digital-native disruptors to seize market share 2526.

Financial Metrics and Evaluation Friction

A major organizational barrier lies in how new ventures are evaluated. BMI projects are frequently measured against the same financial hurdles and key performance indicators (KPIs) as the core business. Because disruptive business models often start with lower performance and narrower margins, they naturally fail these evaluations in their infancy 1140. Success in transformational innovation is seen only over extended time horizons, and applying classic corporate KPIs stifles the motivation and willingness to experiment with untested business models 1140.

Capability Constraints and Human Capital Deficits

The successful deployment of a novel business model requires specialized skill sets that are rarely present in legacy organizations. As companies pivot toward data-driven, AI-enabled business models, they require advanced capabilities in predictive analytics, dynamic pricing, and ecosystem orchestration 2341.

Incumbents often lack the internal human capital necessary to build and scale these technologies. Moreover, existing middle managers, whose compensation and prestige are tied to the legacy model, often view the new business model as a threat to their authority and actively resist its implementation 113542. This widespread organizational resistance severely bottlenecks the innovation process, resulting in "innovation theater" - high-profile corporate innovation labs that generate prototypes but consistently fail to achieve commercial scale 34.

Contemporary Manifestations of Business Model Innovation

The necessity of business model innovation is currently being accelerated by two dominant global macro-trends: the imperative for environmental sustainability and the rapid advancement of artificial intelligence. Both trends require incumbents to structurally reinvent how they deliver value.

The Circular Economy and Product-as-a-Service

Sustainability pressures and resource volatility are forcing incumbents to abandon traditional linear "take-make-dispose" models in favor of Circular Economy business models 434445. The transition to circularity is not merely an environmental compliance exercise; it is a profound business model innovation that decouples economic growth from finite resource extraction 4546. Global research indicates that circular business models could generate substantial economic value, with estimates suggesting a $4.5 trillion opportunity globally by 2030, and a potential €48 billion annual opportunity in the Nordics alone 454748.

Scaling circularity profitably requires addressing significant operational complexities, including reverse logistics, consumer adoption friction, and the redesign of the value chain 4950. One of the most effective circular BMI architectures is the Product-as-a-Service (PaaS) model. Under PaaS, the manufacturer retains ownership of the physical asset and monetizes its usage or performance over time, thereby incentivizing the production of highly durable, modular, and repairable goods 515253.

Philips successfully implemented this through its "Circular Lighting" service, wherein customers pay for illumination rather than purchasing physical light bulbs 5253. Similarly, Rolls-Royce's "Power by the Hour" model provides aviation engine maintenance services based on usage, ensuring engines are refurbished regularly and extending their lifecycle 5253. Consumer brands are also proving the viability of product life-extension models. Patagonia's Worn Wear program repairs and resells used clothing, and IKEA has launched buyback and resell services, demonstrating that circular models can yield topline revenue growth while reducing supply chain risks and raw material costs 515365. Data suggests that circular offerings can deliver 15 to 20 percent topline growth and 10 to 15 percent material cost savings while maintaining margins comparable to linear models 49.

| Circular Business Model | Core Mechanism | Economic Benefit | Industry Examples |

|---|---|---|---|

| Product-as-a-Service (PaaS) | Company retains ownership; customer pays for usage or performance. | Predictable recurring revenue; incentivizes durability. | Philips (Circular Lighting), Rolls-Royce (Power by the Hour) |

| Product Life Extension | Repair, refurbishment, and recommerce of existing goods. | Creates secondary markets; enhances brand loyalty and margins. | Patagonia (Worn Wear), IKEA (Buyback & Resell), Fairphone |

| Resource Recovery | Extracting value from waste streams to create new materials. | Reduces raw material dependency; mitigates supply chain risk. | Loop Industries, Interface (Carpet recycling), Tesla (Battery reuse) |

Generative Artificial Intelligence and Service Transformation

The integration of Generative Artificial Intelligence (GenAI) is driving another wave of fundamental business model shifts. Organizations are transitioning to new business model architectures, categorized by researchers into models such as "Customer Proxy," "Modular Creator," and "Orchestrator" 23.

The Orchestrator model, for example, utilizes AI to assemble an ecosystem of complementary products and services without predetermined processes, allowing financial services firms to provide fully managed, continuously optimized wealth solutions 23. Furthermore, GenAI enables dynamic pricing models that respond in real-time to market conditions and the licensing of AI models as "AI-as-a-Service" (AIaaS), creating entirely new revenue streams 41.

Empirical data reveals a stark division between incumbents that embrace these digital BMIs and those that do not. Companies with strong innovation cultures spend an average of 55 percent more on digital technologies to develop strategic differentiation . Furthermore, Asian firms employing "microproduction" archetypes - matching supply with demand at an extreme pace using AI-native services - have achieved staggering revenue growth, exemplified by companies like Shein, which rapidly scales personalized, small-batch products at unit costs previously associated only with mass production .

Strategic Mechanisms for Incumbent Adaptation

To overcome cognitive rigidity, resource dependence, and organizational inertia, market-leading incumbents have developed specialized structural frameworks designed to foster business model innovation without immediately jeopardizing the core enterprise.

Structural Ambidexterity and Autonomous Venturing

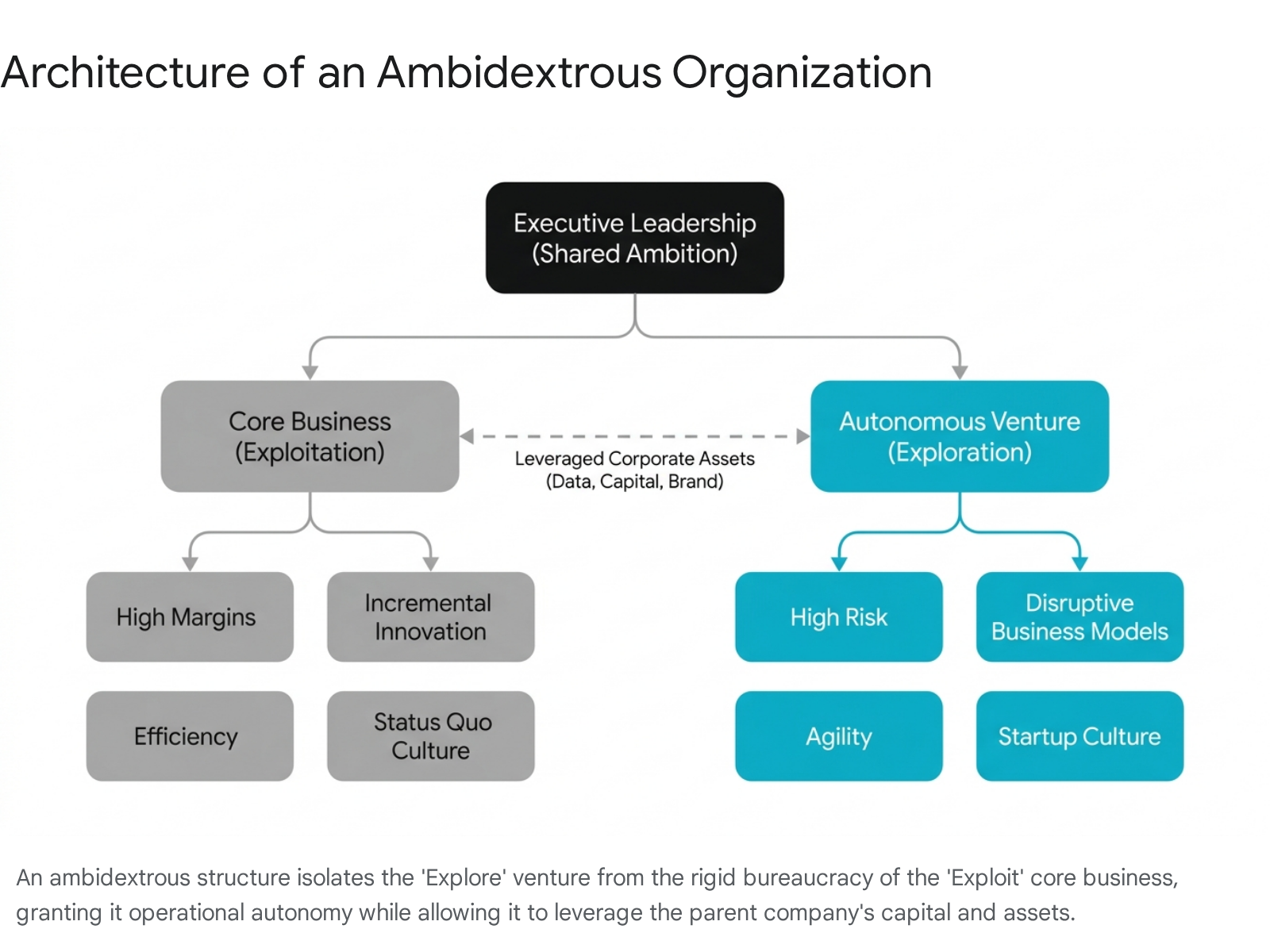

The most theoretically sound and empirically validated strategy for managing the tension between legacy operations and disruptive innovation is the implementation of an ambidextrous organizational structure 40676854. An ambidextrous organization is explicitly designed to balance two inherently conflicting objectives: exploitation and exploration.

Exploitation involves the continuous optimization, incremental innovation, and cost reduction of the firm's existing, profitable core business. Exploration involves the pursuit of radical, highly uncertain business model innovations that promise future growth 64067. Because exploration requires an entirely different culture, risk tolerance, and operational speed, ambidextrous organizations physically and structurally separate the exploration unit from the core business 6768.

This autonomous explore unit is granted the freedom to operate with startup-like agility. It establishes its own processes, defines its own culture, and is insulated from the short-term financial demands and bureaucratic reporting structures of the legacy organization 68. However, it retains selective access to the parent company's vast strategic assets - such as customer data, capital, brand equity, and supply chain leverage 6870.

Examples of successful ambidextrous structures include Google X (Alphabet's innovation factory), Procter & Gamble's Connect+Develop unit, and Amazon's dual focus on retail efficiency and exploratory ventures 676854.

The Spin-Along Approach and Geographic Separation

A potent variation of structural ambidexterity is the "spin-along" or autonomous corporate spin-off strategy 5556. When a technological opportunity fundamentally conflicts with the firm's dominant logic, creating a separate legal and geographical entity is often the only viable path to commercialization, circumventing the resource allocation constraints of the parent 3236.

A historical benchmark for this strategy is Hewlett-Packard's transition from laser-jet to ink-jet printing. Recognizing that lower-margin, disruptive ink-jet technology would be rejected by the highly profitable laser-jet division in Idaho, HP established a completely separate ink-jet organization in Washington state 31. This geographical and organizational separation allowed the new unit to develop its own cost structures, pursue lower margins initially, and target new consumers without the threat of internal sabotage. Ultimately, this approach successfully dominated the ink-jet market and preserved HP's overall market leadership 31.

Corporate Venture Capital and Serial Business Building

Corporate venture capital (CVC) and dedicated venture-building incubators offer another systematic mechanism to build entirely new businesses 2757. By partnering with external venture builders or operating internal startup studios, incumbents can utilize proven entrepreneurial methodologies - such as rapid prototyping and lean agile development - while backing the ventures with corporate capital 27.

When executed correctly, corporate venturing mitigates the risks of BMI. Research by BCG Digital Ventures indicates that their specific corporate venturing model delivers a success rate of 66 percent, compared to the 20 to 30 percent success rate typical of traditional venture capital 27. Organizations identified as "serial business builders" - those that consistently launch multiple autonomous ventures outside their core - generate significantly higher returns on investment and achieve organic growth rates well above industry averages 58. According to McKinsey data, 72 percent of respondents whose companies built new ventures using proven external business concepts reported above-average growth for their industries .

Ultimately, whether transitioning to a digital super-app ecosystem, scaling an AI-orchestrated platform, or pioneering a circular service model, the mandate for modern incumbents is clear. They must overcome the gravitational pull of their legacy success, aggressively restructure to mitigate resource dependency, and institutionalize the capacity for continuous, radical business model innovation.