Incumbent response strategies and survival outcomes in the AI era

Introduction: Reevaluating Creative Destruction in the 2020s

The acceleration of artificial intelligence (AI) and digital disruption throughout the 2020s has fundamentally recalibrated the competitive dynamics between nascent technology ventures and established corporate incumbents. Classical theories of strategic management and innovation have long been anchored in the Schumpeterian concept of creative destruction, which presupposes that technological revolutions inevitably precipitate the demise of legacy firms as they are outmaneuvered by agile entrants. This foundational baseline assumes that incumbents suffer from path dependence, bureaucratic inertia, and a rigid adherence to legacy business models. However, empirical market data and recent organizational research spanning the post-2020 period - particularly from 2023 to 2026 - reveal a profound deviation from this orthodox narrative 12. Far from succumbing to widespread extinction, a significant proportion of incumbent firms are demonstrating remarkable resilience through sophisticated capital allocation, ecosystem orchestration, and hybridized organizational architectures.

The integration of generative AI, large language models (LLMs), and pervasive cloud architectures does not merely substitute human labor or augment existing software; it restructures the very architecture of knowledge work and enterprise value creation 34. This period marks a permanent structural separation of traditional attention metrics from actionable commercial traffic, accelerating what industry analysts term the "zero-click" economy 5. In this highly volatile environment, corporate survival is not a binary state but a path-dependent process of continuous resource recombination and strategic adaptation 2. To accurately understand how legacy firms navigate this landscape, it is necessary to move beyond elementary foundational theories of structural ambidexterity. Modern survival requires a nuanced examination of how organizations govern external boundary-spanning networks, how they deploy corporate venture capital defensively and offensively, and how geographic contexts - particularly the divergence between Western and Asian market strategies - shape systemic digital resilience.

Deconstructing the "Dinosaur Myth": Empirical Evidence of Incumbent Resilience

The pervasive assumption that large incumbents are too slow, path-dependent, and bureaucratic to survive rapid technological shifts - often termed the "dinosaur myth" - is overwhelmingly contradicted by contemporary macroeconomic and firm-level data. The survival and dominance of established corporations during the recent waves of digital disruption underscore a capacity for strategic renewal that the dinosaur myth systematically ignores.

Market Realities, Concentration of Gains, and the SaaS Transformation

Throughout 2024 and 2025, amidst media warnings of a "SaaSpocalypse" and fears of widespread AI-driven displacement, global equity markets demonstrated immense incumbent strength 36. The S&P 500 achieved a massive 25% return in 2024, reaching 61 new all-time highs, largely driven by established technology, telecommunications, and legacy conglomerates adapting to, rather than being destroyed by, emerging AI paradigms 78. While this growth is highly concentrated - with a select group of mega-cap firms (the "Magnificent Seven") accounting for a disproportionate share of index returns - the underlying corporate earnings across the broader, equal-weighted S&P 500 still posted a robust 11.1% increase 79. This resilience is not limited to the technology sector; financial institutions, consumer goods companies, and legacy industrials have leveraged substantial capital reserves to internalize AI capabilities, effectively neutralizing the disruptive threat posed by pure-play startups 4.

The assumption that startups universally outcompete incumbents is further undermined by data from the National Bureau of Economic Research (NBER). Empirical analyses of over 96,000 US venture-backed startups from the modern era reveal that founders are collectively wiped out in 74% of cases, and only 16% of individual founders receive a positive financial payoff upon exit 5. Furthermore, technology-based startups experience a substantially lower fifth-year survival rate compared to the broader economy, with only a fraction achieving the hyper-growth necessary to challenge incumbents 6. In contrast, incumbent firms with high digital and AI maturity exhibit an exceptional ability to execute large-scale technological transformations. Research indicates that the top 30% of established companies - the "Champions" - deliver major IT implementations (such as €1 billion ERP transformations) on time and under budget, effectively using their vast scale as an insulator against disruption 4.

The Execution Gap: Maturity and Path Dependence

The difference between an incumbent that thrives and one that falls to the dinosaur myth lies in execution maturity. The waste from failed implementation is dramatic; an average delay of one year in a large-scale tech program leads to additional costs of about 0.5% of revenues, or up to €250 million for a €50 billion legacy company 4. However, incumbents that systematically manage interdependencies and bridge the gap between business and technological collaboration successfully rewire their legacy systems. In sectors like software and financial services - which were early victims of digital disruption - incumbents now show higher-than-average rates of transformation success, proving that exposure to disruption builds long-term institutional antibodies and enhances survival rates 14.

Geographic Divergence: Western Constraints vs. Asian Agility

A critical, yet often underappreciated, factor in incumbent survival is regional and institutional context. Recent empirical studies highlight a stark divergence in digital transformation strategies between North American/European firms and their Asian counterparts. Evaluating survival patterns necessitates contrasting the regulatory-heavy, defensive posture of Western incumbents against the highly integrated, state-supported agility of Asian conglomerates, chaebols, and emerging market multinationals (EMMs).

The Fragility of the Western Ecosystem Moat

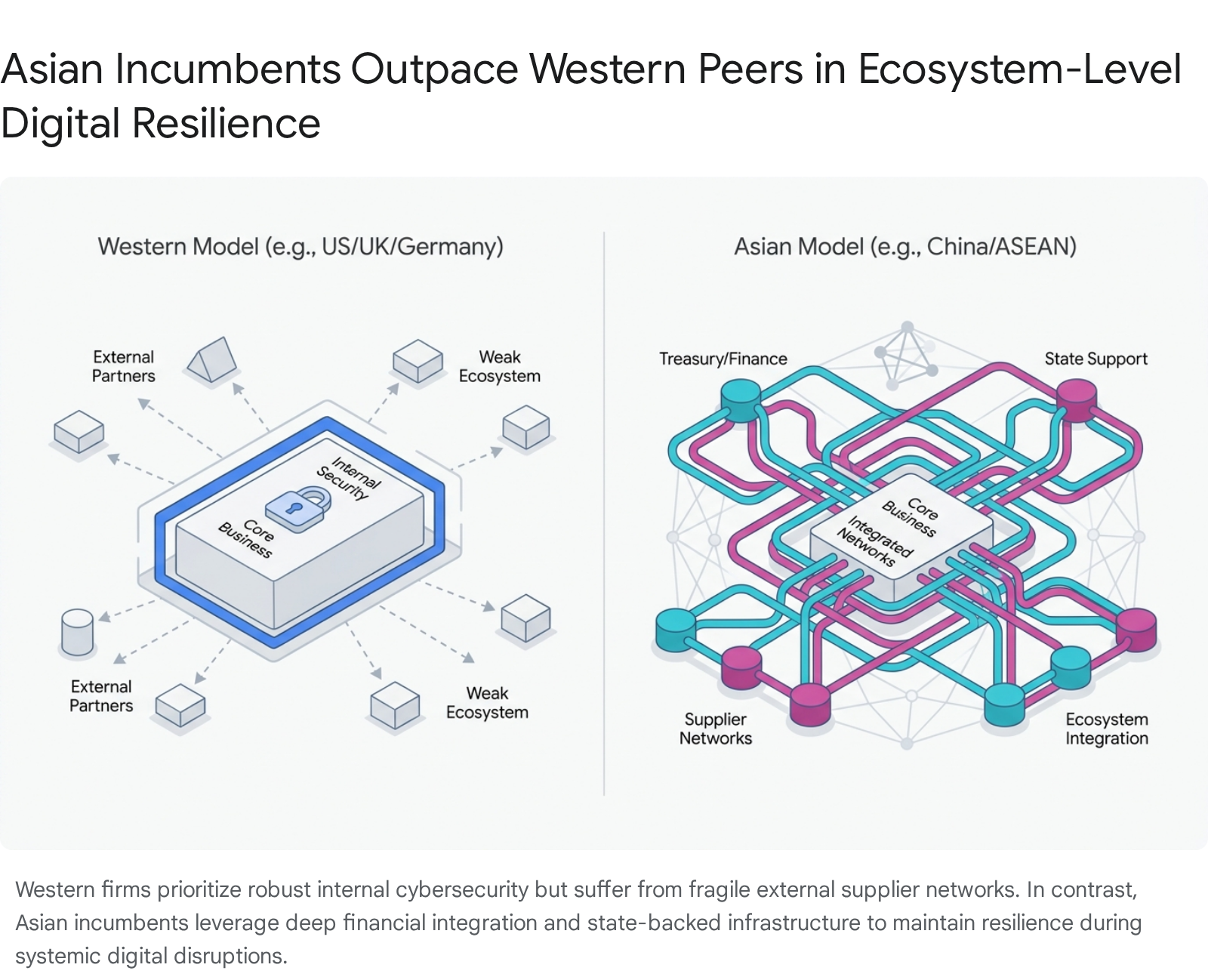

Western incumbents - despite significant capital outlays - frequently exhibit severe vulnerabilities in ecosystem governance and physical infrastructure resilience. A comprehensive 2026 Economist Impact study revealed that organizations in the United States, the United Kingdom, and Germany are materially underprepared for large-scale digital disruptions that extend beyond their immediate organizational boundaries 1314. While these firms possess strong internal foundations, such as robust cybersecurity and regulatory compliance frameworks (with Germany leading policy confidence at 70%), their digital resilience collapses at the ecosystem level 1315. Fewer than 20% of US and UK executives express confidence in cross-sector collaboration with suppliers during disruption events, indicating siloed information sharing and weak partner governance 1314.

Furthermore, legacy technology infrastructures remain a profound structural drag for over 60% of Western organizations, limiting their ability to rapidly deploy generative AI 1415. In Europe, the strategic focus heavily prioritizes keeping data flow democratic and transparent through the General Data Protection Regulation (GDPR) and initiatives like Gaia-X 7. While this protects consumer rights, it frequently creates rigidities that slow the rapid algorithmic iteration required to combat digital disruption from foreign entrants.

Asian Incumbents: Deep Integration and Sovereign Resilience

Conversely, Asian incumbents - ranging from state-backed Chinese enterprises to Southeast Asian conglomerates - exhibit distinct survival mechanisms tailored to high-growth, volatile environments. Asian firms generally embed digital transformation deeper into their core financial and treasury functions, creating a highly integrated approach to risk and investment 8. The strategic models differ fundamentally: while the US model is privately funded and market-based, the Chinese digital competitiveness model relies heavily on state-directed financing, unified digital infrastructure, and a focus on maintaining sovereign technological control 7.

Case studies of non-Western incumbents underscore this regional resilience. When subjected to severe geopolitical sanctions and supply chain embargoes, Asian telecommunications giant Huawei successfully navigated the disruption not through immediate structural separation, but through deep supply chain diversification, immense domestic R&D investment, and state-aligned ecosystem support 9. The region's broader macroeconomic metrics reflect this agility. Developing Asian economies progressed faster than the rest of the world in digitalization indices between 2020 and 2024 10. By late 2025, enterprise adoption of generative AI in the Asia-Pacific region surged to 42%, demonstrating how Asian EMMs are leveraging digital leapfrogging to capture market share 20.

Moreover, Asian incumbents have absorbed the "seven pillars of western wisdom" regarding science and technology, while avoiding the "deskilling of leadership" observed in other emerging markets 21. This allows Asian firms to execute long-term strategic plans with high bureaucratic competency. However, they face unique regional risks; the Asia-Pacific region recorded 195 internet shutdowns in 2025 - accounting for over half of all global incidents - highlighting the severe infrastructural and political volatility these resilient incumbents must seamlessly navigate 22.

Reassessing Organizational Ambidexterity: The Structural Separation Debate

To survive technological upheavals, incumbents rely on organizational ambidexterity - the capacity to simultaneously exploit existing competencies for steady revenue while exploring new, disruptive innovations for future viability. Foundational theories, heavily influenced by Tushman and O'Reilly (1996) and March (1991), traditionally advocated for structural ambidexterity: the strict physical and managerial separation of exploitative (legacy) and exploratory (innovative) business units 111213. This structural separation, often taking the extreme form of corporate spin-offs, divestitures, or highly autonomous skunkworks, was theoretically designed to protect fragile new ventures from the stifling bureaucracy, rigid metrics, and resource cannibalization inherent to the parent organization.

Modern Critiques of the Spin-Off Assumption

Recent empirical research from 2024 and 2025 rigorously challenges the generalized assumption that structural separation is universally superior to deep contextual integration. In highly dynamic, AI-driven environments, agility and resource recombination are paramount. The strict separation of units advocated by traditional theorists can inadvertently create rigid silos, hindering the cross-pollination of data, algorithmic capabilities, and complementary assets required for true digital business model innovation (DBMI) 1226.

When empirically examining the survival rates and financial performance of corporate and academic spin-offs versus internal ventures, the data paints a highly nuanced picture:

- Spin-off Survival vs. High-Growth Capabilities: Academic spin-offs (ASOs) and corporate spin-offs do exhibit generally higher absolute survival rates compared to independent, unfunded startups. This is largely due to their initial resource endowments, inherited institutional legitimacy, and the backing of Technology Transfer Offices (TTOs) 272829. However, while they survive the initial "valley of death," they frequently fail to scale. Empirical literature from 2023 - 2025 confirms that the vast majority of spin-offs do not display high-growth attributes, often languishing as stagnant, small enterprises that underperform in job creation and cash flow generation compared to other young innovative companies 2714.

- Parent Company Value Destruction: The assumption that shedding disruptive units maximizes parent company shareholder value is heavily contested by modern financial analysis. Empirical event studies of corporate spin-offs reveal that while there may be minor short-term positive abnormal returns upon announcement (averaging approximately 3.4%), the long-term reality is starkly different 15. Parent companies often generate negative buy-and-hold abnormal returns (e.g., -4.11%) in the 12 to 18 months following a spin-off 15. This destruction of long-term value occurs because the parent firm loses access to the exploratory synergies, technological spillovers, and talent pools needed to remain competitive against emerging threats 3233. In contrast, the spun-off entities themselves may generate positive abnormal returns (+13.76%), demonstrating a highly asymmetric distribution of value that ultimately harms the incumbent core 15.

The Shift Toward Contextual Ambidexterity and Internal Agglomeration

Rather than relying on divestitures and hard structural barriers, top-tier strategy literature now emphasizes contextual ambidexterity. This approach integrates exploration and exploitation fluidly within the same organizational boundaries, driven by a unified culture that balances temporal flexibility and dynamic resource sharing 122616.

In the context of artificial intelligence, proprietary data from the legacy business is the precise fuel required to train new exploratory machine learning algorithms. Separating the two units structurally destroys the primary competitive advantage the incumbent holds over a nimble startup 17. Modern incumbents succeed by operating as "theory-led" entities, guiding capability development through deeply integrated internal agglomeration 3637. Recent spatial analyses of multi-unit firms reveal that internal agglomeration - the co-location of related but distinct activities within the firm's boundaries - is driven largely by labor similarity. Keeping exploratory and exploitative units proximately close enhances the cross-fertilization of human capital, reduces coordination costs, and ensures that the legacy business is directly infused with disruptive innovations 36.

Furthermore, maintaining an appropriate balance between exploring new possibilities and exploiting old certainties is critical for avoiding organizational demise. The interaction of ambidextrous learning means that exploratory learning increases the depth of exploitative learning, while the effectiveness of exploitative learning provides the cash flow necessary to fund further exploration 1638.

Boundary-Spanning Architectures: Ecosystems, Platforms, and Alliances

As traditional structural separation proves inadequate for the complexities of the digital epoch, incumbents are increasingly adopting external, boundary-spanning organizational forms. Moving from a linear, pipeline-based product model to a platform-based ecosystem allows incumbents to externalize the financial risks of exploratory R&D while capturing the massive value of multi-sided network effects 1840.

Ecosystem Orchestration vs. Complementation

An ecosystem is fundamentally defined by modularity and multilateral dependencies, where unhierarchical, interdependent firms coordinate to create a cohesive value proposition 1841. As technologies become deeply interconnected, incumbents face a critical strategic choice: orchestrate the ecosystem and define the core architecture, or operate as a complementor within an ecosystem built by a digital native (e.g., ByteDance, Amazon, Google) 1943.

Orchestrating an ecosystem yields profound survival advantages but carries high initial risks. Digital platform ecosystems exhibit a co-evolutionary mechanism driven by cross-category innovation. For example, longitudinal analyses of platforms reveal a two-stage evolution: in the category emergence stage, platforms establish a core business via algorithmic recommendations to gain legitimacy; in the category spanning stage, they utilize "platform envelopment" to expand into adjacent markets, generating massive technological spillovers 20. By opening their core infrastructure to third-party developers and startups, incumbents can run thousands of exploratory experiments simultaneously. If a complementary startup succeeds, the platform captures a share of the value through access fees or data harvesting; if the startup fails, the platform bears zero financial risk 4120.

Empirically, multi-sided platforms receive significantly higher volumes of venture capital investment across more staging rounds than traditional pipeline businesses, despite facing the immense "chicken-and-egg" paradox of scaling both supply and demand simultaneously 21. To mitigate the threat of digital entrants, incumbent producers often pivot fluidly between competitive and cooperative strategies - engaging in phased "selective coopetition" - to defend their market position while integrating external innovations 41.

Strategic Alliances and Joint Ventures in Emerging Markets

For incumbents operating in asset-heavy, highly regulated, or geopolitically sensitive environments where platform dynamics are difficult to engineer, strategic alliances and joint ventures serve as vital boundary-spanning tools. These structures allow firms to pool resources and internalize external innovations without the heavy commitment, antitrust scrutiny, and integration failure rates of a full acquisition.

Alliances are particularly potent for Emerging Market Multinationals (EMMs). In regions characterized by institutional voids, rapid economic volatility, and constrained access to global capital, strategic alliances allow EMMs to share risk and access localized knowledge networks 4647. While empirical studies across the technology and pharmaceutical industries confirm that alliances significantly enhance innovation output, market performance, and competitive advantage, they are fraught with severe coordination challenges. The primary systemic limitations include the risk of opportunistic behavior and unintended knowledge spillovers to direct competitors 47. Consequently, survival in an alliance-driven strategy requires rigorous, trust-based governance structures and robust intellectual property protections 47.

Tactical Response Matrix: Mapping Incumbent Strategies

To synthesize the various organizational forms deployed to navigate digital disruption, the following table compares specific response strategies against their primary advantages, limitations, and empirically observed survival rates.

| Tactical Response Strategy | Description | Primary Advantages | Systemic Limitations | Empirical Survival & Performance Outcomes |

|---|---|---|---|---|

| Deep Integration (Contextual Ambidexterity) | Fluidly embedding exploratory AI/digital units within the legacy corporate structure. | Maximizes proprietary data synergies; leverages existing human capital; minimizes labor displacement 1736. | High risk of organizational inertia; legacy core may cannibalize resources meant for high-risk exploration 16. | Highly resilient in data-rich industries; superior for long-term parent firm value preservation compared to divestiture 1517. |

| Structural Separation (Spin-offs) | Creating distinct, legally or geographically separated entities for exploratory ventures. | Protects new ventures from legacy bureaucracy; clarifies financial metrics for investors 1215. | Severs access to proprietary parent data; introduces high type 2 error rates in viability assessments 3322. | High absolute survival rate for the spin-off, but predominantly low-growth. Parent firm often suffers negative abnormal returns (-4.11%) 1415. |

| Ecosystem Orchestration (Platforming) | Developing a modular digital platform allowing third parties to create complementary value. | Externalizes R&D risk; captures massive network effects; facilitates rapid, cross-category scaling 1820. | Vulnerable to "chicken-and-egg" scaling paradoxes; requires relinquishing strict hierarchical control over product 21. | Winner-takes-all dynamics. High failure rate initially, but surviving orchestrators achieve near-monopolistic resilience 1821. |

| Strategic Alliances & Joint Ventures | Formal, non-equity or equity partnerships to co-develop or share digital capabilities. | Rapid access to external knowledge; risk-sharing in highly uncertain or capital-intensive emerging markets 47. | High coordination costs; significant risk of IP leakage and opportunistic behavior by partners 47. | Enhances competitive advantage and survival in high-tech sectors, though heavily dependent on robust governance 47. |

Tactical Capital Allocation: CVC, R&D, and the "Killer Acquisition" Debate

Incumbent survival relies as much on financial mechanics as it does on organizational design. The tactical allocation of capital - specifically the nuanced interplay between internal Research and Development (R&D), offensive Corporate Venture Capital (CVC), and defensive Mergers and Acquisitions (M&A) - dictates a firm's trajectory in the AI era.

The "Killer Acquisition" Debate: Myth versus Reality

In the late 2010s, a prevailing theory emerged in antitrust and economic literature suggesting that massive incumbents consistently execute "killer acquisitions" - buying nascent, highly innovative startups solely to terminate their projects and preempt future competition 2324. Foundational studies rooted in the pharmaceutical sector provided the bedrock for this theory, estimating that 5.3% to 7.4% of acquisitions fell into this category, characterized by immediate and permanent terminations of overlapping drug development projects, particularly when the acquirer's market power was heavily entrenched by distant patent expirations 2351.

However, the uncritical application of the killer acquisition hypothesis to the digital and AI sectors has recently been challenged by extensive academic scrutiny. Comprehensive empirical evaluations in 2024 and 2025 indicate that the narrative of systemic, anti-competitive suppression by "Big Tech" is heavily overstated in the digital economy 5253. In reality, evidence suggests that the vast majority of acquisitions by major tech incumbents (e.g., GAFAM) are motivated by complementarity rather than suppression 52.

Rather than creating a monopolistic "kill zone," these acquisitions frequently operate as "cultivation zones," where post-acquisition innovation output actually rises, especially in technological domains where the acquirer has prior experience and continues to make follow-on investments 52. Furthermore, "reverse killer acquisitions" - where the incumbent discontinues its own legacy program in favor of the newly acquired, superior startup technology - are increasingly common, proving that M&A serves as a critical mechanism for self-disruption and modernization rather than mere entrenchment 5225. While regulatory bodies like the UK's Competition and Markets Authority (CMA) have introduced the Digital Markets, Competition and Consumers Act 2024 to tighten jurisdictional thresholds regarding nascent acquisitions, the empirical base proving systemic harm in non-pharma sectors remains remarkably thin 5253.

The Strategic Primacy of Offensive Corporate Venture Capital (CVC)

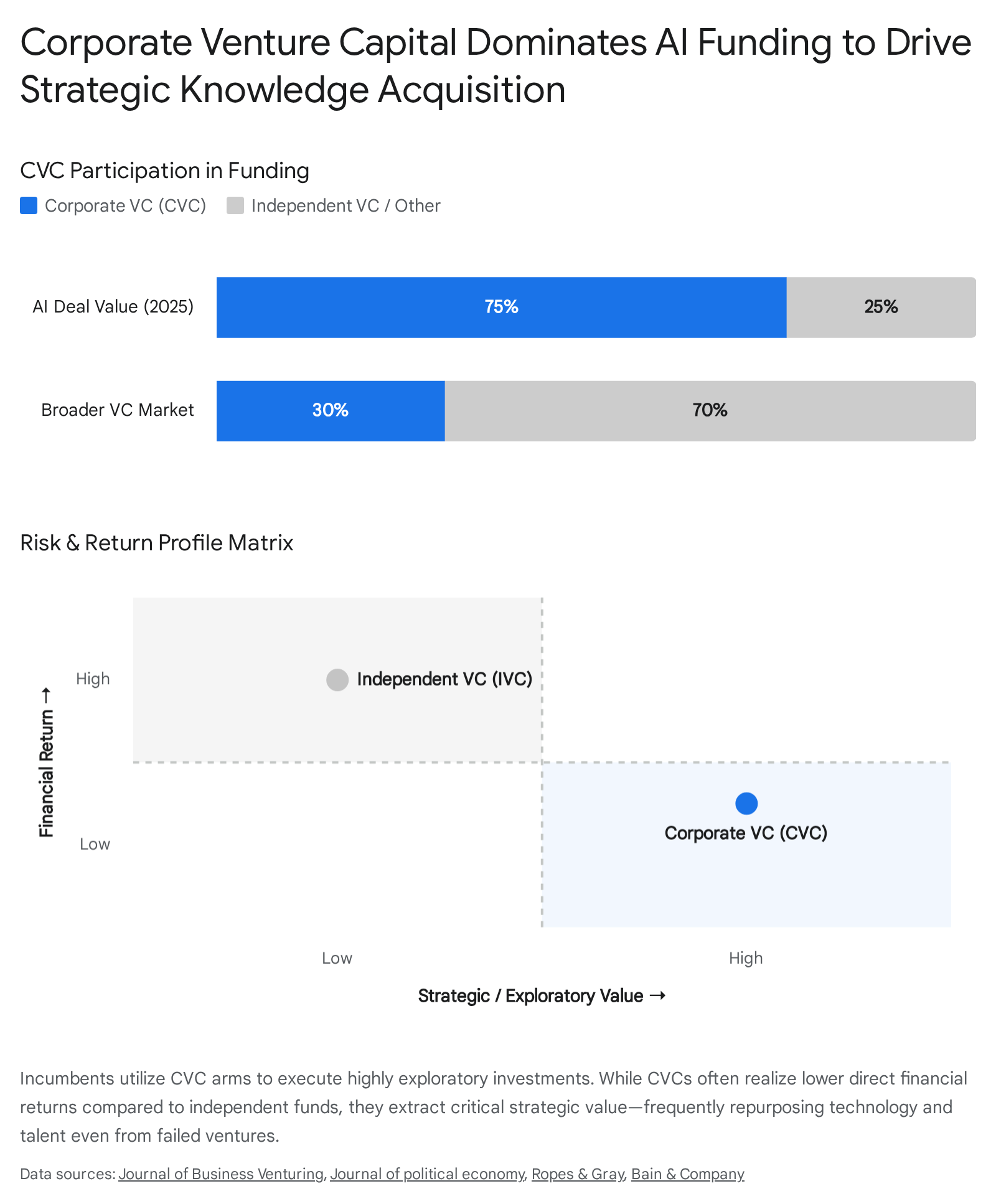

Rather than executing outright acquisitions - which can trigger antitrust scrutiny and destroy value through integration friction - incumbents are increasingly utilizing Corporate Venture Capital (CVC) as an offensive, exploratory mechanism. CVC participation has skyrocketed in the AI era; by the first half of 2025, CVCs participated in an unprecedented 68% to 75% of all AI venture funding deal value, heavily driven by Big Tech companies securing early access to foundational models and compute infrastructure 5526. Globally, annual VC investments in AI firms surged to $258.7 billion in 2025, accounting for 61% of total VC activity, underscoring the massive capital shifts required to fund generative AI 27.

CVC operates on a fundamentally different paradigm than Independent Venture Capital (IVC). While IVCs seek maximum financial returns and rapid exits, CVCs pursue dual objectives: financial viability and strategic corporate alignment 28. Consequently, CVCs often invest in riskier, highly exploratory ventures that IVCs deliberately avoid. Statistically, CVC investors pay higher prices for equity and earn lower direct financial returns, demonstrating a Total Value to Paid-In (TVPI) ratio 0.72 lower than that of independent funds 28.

Yet, this explicit financial "underperformance" is a calculated trade-off. CVCs generate immense off-balance-sheet strategic value through organizational learning, technological window-dressing, and market intelligence 28. Crucially, CVCs extract immense value even from failed startups. Unlike traditional VCs whose assets and talent scatter upon venture failure, CVCs actively retain and repurpose the intellectual property, key personnel, and market insights of collapsed portfolio companies to accelerate their own internal digital transformations 28.

This unique capability to absorb and learn from exploratory failures transforms CVC from a mere financial instrument into a highly efficient, externalized R&D engine. Conversely, when CVCs eventually decide to fully acquire their own successful portfolio companies, the data shows this can paradoxically destroy shareholder value, estimating that average returns to acquisitions of CVC portfolio companies are more than 1.5% lower than average returns to non-CVC investments, primarily because the benefits of ecosystem independence are lost 59.

Sustaining vs. Disruptive R&D Allocation

Internal capital allocation toward R&D represents the final pillar of incumbent survival. However, raw R&D intensity does not guarantee resilience; it must be calibrated accurately. Research establishes an inverted-U relationship between R&D intensity and institutional investment value; optimal R&D secures competitive advantage, but overinvestment becomes a severe financial burden that exhausts organizational slack and accelerates failure 29.

Capital structure also plays a pivotal role in survival. Empirical analyses of over 2,800 firms indicate a significant negative correlation between R&D expenditures and total/short-term debt ratios 30. Because the outcomes of disruptive R&D are highly uncertain and intangible assets cannot be easily collateralized, resilient incumbents fund exploration through equity and retained earnings rather than risky debt 30.

Furthermore, there is a systemic imbalance in modern R&D allocation. Driven by market pressures for immediate returns, private sector spending is increasingly skewed toward sustaining, applied research and experimental development (representing 2.3% of U.S. GDP), rather than the disruptive, fundamental basic research (just 0.5% of GDP) required to navigate paradigm shifts like quantum computing and advanced AI 3132. Nevertheless, incumbents that successfully survive long-term disruptions are those that maintain unwavering R&D commitments even during broader macroeconomic crises. Maintaining strong business diversification combined with sustained R&D intensity during periods of financial distress serves as a potent catalyst for long-term viability, providing the strategic flexibility necessary to outlast brittle, hyper-focused competitors who indiscriminately slash budgets during downturns 33. This survival advantage is further highlighted in emerging markets, where longitudinal Cox Proportional Hazard modeling demonstrates that high ecosystem health combined with rigorous internal R&D provides the highest protective factor against firm failure 34.

Conclusion

The empirical landscape of the mid-2020s definitively dismantles the myth of the inevitably doomed incumbent. While digital disruption and the deployment of generative AI possess the capability to unseat unprepared enterprises, legacy organizations are wielding sophisticated strategic instruments to not merely survive, but to actively dominate the new technological epoch.

The evidence points to three central tenets for modern corporate survival. First, geographic and institutional frameworks matter profoundly; the highly integrated, ecosystem-aware, and state-synthesized strategies seen in emerging Asian markets offer a fundamentally more resilient blueprint than the structurally siloed, regulation-constrained approaches prevalent in the West. Second, the orthodox assumption that structural separation - such as divestitures and spin-offs - is the optimal route for disruptive innovation is flawed in data-driven industries. Deep contextual ambidexterity, which allows the fluid sharing of proprietary data, algorithms, and human capital across an organization's internal agglomerations, generally results in superior long-term value preservation for the parent firm.

Finally, incumbents are mastering advanced, boundary-spanning capital allocation. By deploying Corporate Venture Capital to explore risky frontiers and absorb the lessons of failed startups, orchestrating modular platforms to capture multi-sided network effects, and utilizing strategic acquisitions to cultivate rather than kill new technologies, established firms are continuously refreshing their competitive moats. In the rapidly evolving AI era, survival belongs to those incumbents that eschew rigidity, operating instead as dynamic, boundary-spanning networks rather than static, isolated fortresses.