Algorithmic versus discretionary swing trading

Mechanics of Swing Trading

Financial market participation is structurally defined by the time horizon of the investments and the decision-making framework employed to execute them. Swing trading occupies a distinct operational duration within this spectrum, deliberately targeting the capture of short- to medium-term price movements that unfold over a period of several days to several weeks 1234. Unlike high-frequency trading (HFT) or intraday scalping, which rely on microsecond latency arbitrage and order-book imbalances within a single trading session, swing trading requires the structural assumption of overnight risk 126. Conversely, it differs fundamentally from long-term position trading or traditional buy-and-hold investing, which span months to years and rely heavily on macroeconomic cycles, monetary policy trends, or deep fundamental value realization 124.

The primary objective of a swing trading strategy is to identify financial assets exhibiting localized momentum or mean-reverting characteristics, enter the market at strategic inflection points, and exit when the anticipated price movement reaches a predetermined target or demonstrates technical exhaustion 23. Because the multi-day holding period allows for significant price discovery, macroeconomic data releases, and volatility expansion, swing traders must optimize capital efficiency while systematically managing the psychological pressure of holding positions through overnight gaps and multi-session drawdowns 346.

Within this specific time horizon, practitioners universally divide into two methodological camps: algorithmic (systematic) trading and discretionary trading. Algorithmic trading relies on predefined, mathematically codified rules to autonomously identify market setups, size positions according to volatility metrics, and execute trades without active human intervention during the live market session 783. Discretionary trading, on the other hand, relies on the human practitioner's cognitive synthesis of technical indicators, fundamental catalysts, and experiential intuition to make the final determination on market entry, exit, and risk management 7810.

| Trading Style | Holding Period | Primary Catalyst | Execution Mechanism | Human Involvement |

|---|---|---|---|---|

| Scalping / HFT | Milliseconds to minutes | Order book imbalances, latency | Purely Algorithmic | Strategy design and infrastructure |

| Day Trading | Minutes to hours | Intraday momentum, breaking news | Discretionary or Algorithmic | Active monitoring, session-bound |

| Swing Trading | Days to weeks | Technical patterns, sector rotation | Discretionary, Systematic, or Hybrid | Daily review, overnight risk management |

| Position Trading | Weeks to months | Macroeconomic cycles, deep value | Discretionary or Systematic | Periodic rebalancing and fundamental review |

The debate between systematic and discretionary approaches in the swing trading timeframe serves as a microcosm for a much broader epistemological question in the behavioral and social sciences: does empirical evidence favor rigid, rules-based statistical models over the nuanced, context-aware judgment of human experts?

Theoretical Foundations of Decision Making

Actuarial and Clinical Judgment Frameworks

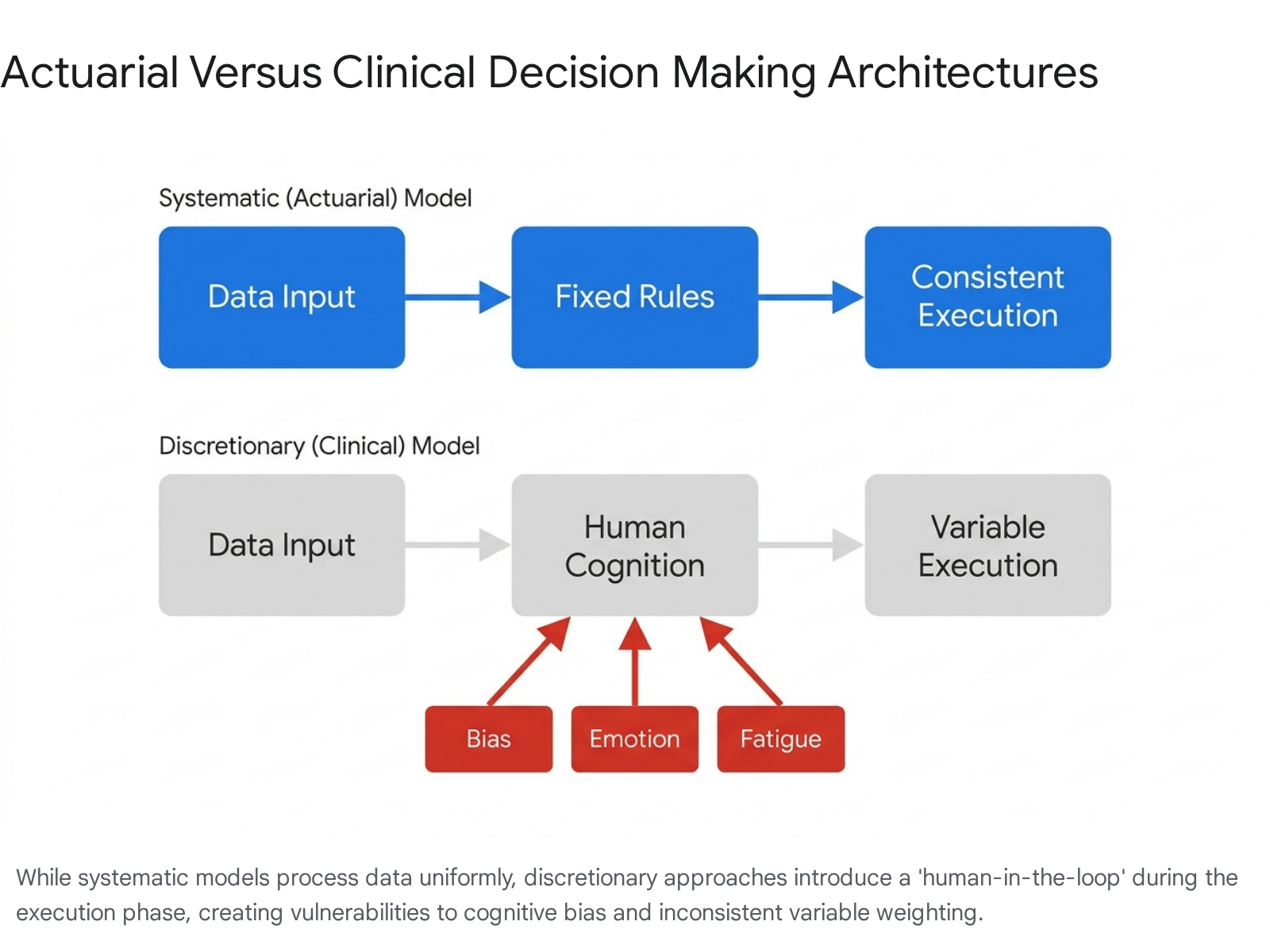

The debate between systematic rules and human discretion in financial markets is deeply anchored in cognitive psychology, specifically the extensive research on "clinical versus actuarial judgment" pioneered by Paul E. Meehl in 1954 4567. Meehl established a rigorous framework for comparing two fundamentally distinct methods of decision-making. The clinical method involves a human decision-maker processing information, weighing variables, and arriving at a conclusion based on experience, intuition, and unstructured synthesis 415817. The actuarial (or statistical/systematic) method entirely eliminates the human judge during the execution phase; conclusions rest solely on empirically established, pre-specified mathematical relations between data inputs and targeted outcomes 41517.

Meehl's foundational research, alongside decades of subsequent meta-analyses by scholars such as William Grove, Robyn Dawes, and David Faust, demonstrated a consistent and overwhelming asymmetry: actuarial methods equal or outperform human clinical judgment in roughly 94% of diverse predictive domains 4589. This superiority holds true across highly varied fields, including medical diagnoses, academic performance forecasting, business failure prediction, and criminal recidivism assessments 69191011. The central premise identified by these psychologists is that human experts are susceptible to fatigue, emotional bias, outcome fixation, and inconsistencies in variable weighting. If a systematic model is fed the exact same data inputs as a human expert, the model will output the same decision uniformly. The human expert, influenced by recency bias, mood, or environmental context, routinely arrives at different conclusions on different days despite identical underlying data 8919.

Models are constructed by humans operating in the "System 2" rational mode of thinking. Once constructed, these models are implemented systematically, devoid of the "System 1" emotional biases that inherently corrupt real-time human decision-making 9. Consequently, evidence suggests that in stable, probabilistic environments, the performance of a stand-alone algorithmic model represents a ceiling on performance, not a floor 9.

The Broken Leg Problem in Financial Forecasting

Despite the robust statistical evidence favoring algorithms, human practitioners frequently argue that quantitative models lack the contextual awareness necessary to navigate unprecedented market events. Meehl termed this heuristic exception the "broken leg" problem 7823.

The heuristic operates as follows: an actuarial formula may possess a highly validated 90% accuracy rate in predicting that a specific individual will attend the cinema on a Friday night based on historical behavioral data. However, if a human observer discovers that the individual broke their leg on Friday morning, the human can override the algorithm and accurately predict non-attendance 72324. The algorithm fails in this instance because "broken leg" was an exogenous variable not included in its historical training data.

In financial markets, discretionary swing traders rely heavily on identifying these "broken leg" scenarios. Sudden geopolitical conflicts, unprecedented central bank interventions, unpriced regulatory shifts, or black-swan economic data present circumstances where historical correlations instantaneously break down 232425. Proponents of discretionary trading argue that humans can synthesize qualitative, unstructured data that algorithms cannot parse effectively, allowing them to adapt when market momentum suddenly shifts without clear quantitative precursors 825.

However, academic research indicates that human intervention usually degrades the long-term performance of systematic models. The fundamental vulnerability is that human traders routinely misidentify standard market noise as "broken leg" anomalies 79. When humans are permitted to override a proven algorithm, the number of incorrect modifications generally vastly exceeds the number of correct modifications 79. The urge to tinker with a functioning system introduces the exact cognitive biases that the algorithm was explicitly designed to circumvent, transforming a localized attempt at optimization into a systemic performance drag.

Psychological Vulnerabilities in Discretionary Execution

If algorithms possess a theoretical edge defined by Meehl's research, understanding exactly how and why discretionary traders underperform in practice is critical. Behavioral finance has exhaustively quantified the "performance drag" caused by human psychology, identifying several specific mechanisms that mechanically erode the returns of discretionary swing traders.

Overconfidence and Trading Frequency

One of the most consequential studies on discretionary trading behavior was conducted by Brad M. Barber and Terrance Odean, who analyzed the detailed trading records of 66,465 households at a large discount brokerage from 1991 to 1996 121314. Their research demonstrated a severe negative correlation between trading frequency and net portfolio returns. The most active quintile of traders earned an annualized return of 11.4%, significantly trailing the broader market return of 17.9% and the 18.5% return generated by the least active "buy-and-hold" quintile over the same period 12142915.

Barber and Odean attributed this excessive trading frequency entirely to human overconfidence. Discretionary traders routinely overestimate the precision of their private information and their ability to interpret public signals 1331. This bias is notably gendered; because psychological research indicates men display higher levels of overconfidence in culturally perceived male domains like finance, theory predicted men would trade more frequently than women. The empirical data confirmed this prediction with striking precision: men traded 45% more frequently than women, reducing their net returns by 2.65 percentage points annually due to transaction costs and poor timing, compared to a 1.72 percentage point reduction for women 1315. The disparity was even more pronounced among single demographics, with single men trading 67% more than single women 1315.

Furthermore, overconfidence scales violently with the use of leverage. Research indicates that margin investors exhibit higher portfolio turnover and engage in more speculative trades than cash-only investors 1617. As overconfident discretionary traders utilize margin, they amplify both explicit transaction costs and exposure to idiosyncratic risk. The monthly turnover of cash investors was measured at 6.9%, while margin-experienced investors turned over 15.2% of their portfolios monthly, systematically degrading their Sharpe ratios 143116.

Loss Aversion and the Disposition Effect

The profitability of any swing trading system is mathematically determined by its win rate and its risk-reward ratio - the size of average winners relative to average losers 4. Discretionary traders frequently sabotage their risk-reward ratios due to a cognitive bias known as the "disposition effect" 12141516.

Rooted in Daniel Kahneman and Amos Tversky's Prospect Theory, which established that the psychological pain of losing money is roughly twice as intense as the pleasure derived from an equivalent financial gain 1218, the disposition effect describes the human tendency to realize gains prematurely while holding losing positions indefinitely 12141519. Odean's research found that discretionary traders are 1.5 times more likely to sell a winning equity position than a losing one 12.

By cutting winners short to secure a psychological victory and holding losers to avoid the finality of realizing a loss, discretionary traders mathematically invert optimal swing trading mechanics. This behavior actively destroys the positive expectancy of their strategies. The disposition effect alone is estimated to reduce annual returns by 3% to 5% 1218. Systematic algorithms, devoid of emotional attachment to asset prices, mechanically trail stop-losses and execute exits based strictly on technical criteria, completely eliminating the disposition effect from the portfolio execution process 820.

Outcome Fixation and Revenge Trading

The most acute form of discretionary performance destruction occurs during periods of emotional tilt, commonly manifesting as "revenge trading" 12291921. When a discretionary trader experiences an unexpected loss or a sequence of drawdowns, acute emotional responses - such as anger, frustration, and fear - trigger physiological arousal and intense outcome fixation 193839.

In a desperate attempt to immediately repair their emotional state and recoup financial losses, traders frequently abandon their predefined rules and risk parameters 1921. Research indicates that revenge trades are characterized by extreme immediacy and excessive risk; they frequently occur within 10 minutes of a realized loss, utilizing position sizes up to 2.5 times larger than the trader's standard baseline risk 21. This impulsive, risk-seeking behavior in the domain of losses transforms manageable, routine drawdowns into catastrophic account failures. Internal brokerage data highlights that 33.7% of early account breaches in funded trader programs are the direct result of high-frequency revenge trading following an initial loss sequence 2922. Algorithmic systems are entirely immune to outcome fixation and revenge trading, operating with identical position sizing and entry parameters regardless of the preceding sequence of returns 82023.

| Cognitive Bias | Behavioral Manifestation in Discretionary Trading | Quantitative Impact on Performance |

|---|---|---|

| Overconfidence | Excessive trading frequency, margin utilization, and underestimating risk. | Reduces net annual returns by roughly 6.5% for the most highly active traders 12131415. |

| Disposition Effect | Selling winning positions prematurely to lock in psychological gains while holding losers. | Actively reduces annual returns by an estimated 3% to 5% 1218. |

| Loss Aversion | Removing hard stop-losses, averaging down into losing trades, ignoring invalidation levels. | Inverts risk-reward ratios, accelerating severe portfolio drawdowns 181922. |

| Revenge Trading | Immediate re-entry within minutes of a loss using oversized, highly leveraged positions. | Primary driver of total account liquidation; position sizes often 2.5x normal risk limits 2122. |

Structural Limitations of Algorithmic Systems

While the psychological literature severely indicts human vulnerabilities, declaring absolute victory for algorithmic swing trading ignores the profound structural and mathematical pathologies inherent in quantitative finance. Algorithms do not possess human emotions, but they are designed, parameterized, and deployed by humans, making them highly susceptible to meta-level cognitive errors during the research and development phase 924.

Backtest Overfitting and Statistical False Discoveries

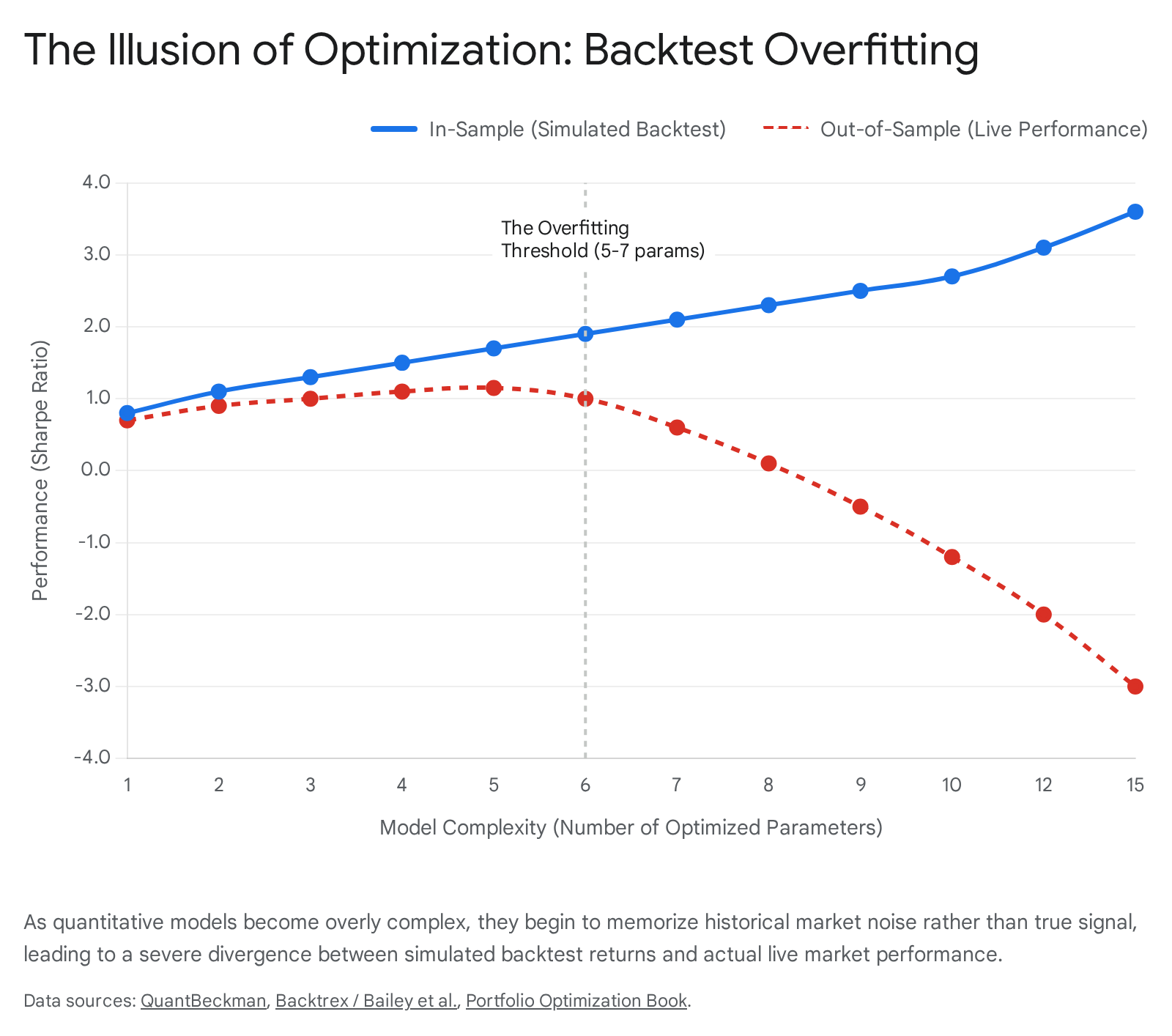

The most pervasive and dangerous flaw in algorithmic strategy development is backtest overfitting 242526. A backtest utilizes historical market data to simulate how a systematic trading strategy would have performed in the past. Modern high-performance computing allows quantitative researchers to test millions or billions of parameter combinations - varying moving average lengths, stop-loss percentages, volatility filters, and threshold triggers - to find the "optimal" settings for maximum historical yield 2627.

However, financial time-series data is notoriously noisy, autoregressive, and non-stationary. By exhaustively testing variations on a finite dataset, an algorithm ceases to identify a genuine underlying economic market signal and instead begins to precisely memorize the random noise of that specific historical dataset 24262728. This represents a catastrophic failure to manage the bias-variance tradeoff. An overfit mathematical model will produce a flawless equity curve and an exceptionally high Sharpe ratio "in-sample" (during the backtest phase), but will collapse immediately when deployed "out-of-sample" in live trading, because the specific noise sequences it memorized will never perfectly repeat 262728.

Bailey, Borwein, Lopez de Prado, and Zhu (2014) formally quantified this phenomenon, developing the Probability of Backtest Overfitting (PBO) framework and Combinatorially Symmetric Cross-Validation (CSCV) techniques to assess mathematical validity 26272930. Their mathematical proofs demonstrate that once a researcher tests more than a relatively small number of parameter combinations (often as few as 50) on a single dataset, the probability that the resulting strategy is overfit approaches certainty 2729. Because researchers often only publish or deploy the single best-performing variation out of thousands of tests, the vast majority of highly profitable algorithmic backtests are statistical mirages, representing false discoveries through data snooping rather than legitimate predictive edge 24262949.

Data Integrity and Simulation Biases

Systematic swing trading strategies are entirely dependent on the structural integrity of the data used for their development. Two structural data biases routinely invalidate algorithmic models before they even reach the optimization phase: survivorship bias and look-ahead bias 242527.

Survivorship bias occurs when a historical dataset only includes financial assets that actively trade today, implicitly omitting companies that went bankrupt, were delisted, or were acquired 24252831. For example, an algorithm testing a mean-reversion strategy on the current S&P 500 constituents over a twenty-year period will appear immensely profitable because the dataset has been retroactively cleansed of catastrophic corporate failures like Enron, WorldCom, or Lehman Brothers 2425. Research utilizing the Center for Research in Security Prices (CRSP) database reveals that survivorship bias artificially inflates annualized backtest returns by 1.6% (from 7.4% to 9.0% between 1926 and 2001), and can improperly inflate a strategy's Sharpe ratio by up to 0.5 points 253151. Furthermore, maximum drawdowns are routinely underestimated by an average of 14 percentage points, masking the true risk the algorithm would have faced 31.

Look-ahead bias is a temporal contamination error where the simulation algorithm utilizes data that would not have been available at the exact moment of the simulated trade execution 24252728. Common examples include executing a trade based on the current day's closing price before the market has actually closed (using close[0] instead of close[1]), or utilizing corporate financial statement data based on the fiscal quarter-end date rather than the actual, delayed publication date 252728. These subtle coding errors produce algorithmic models that simulate perfect market timing, an impossible feat in live discretionary or systematic execution.

Institutional Performance Comparisons

Moving beyond theoretical vulnerabilities of psychology and backtesting, academic evaluations of institutional hedge funds provide objective data on the performance of systematic versus discretionary management at scale. By isolating funds into distinct stylistic classifications, researchers can compare the real-world execution of these two competing philosophies.

Risk-Adjusted Returns in Developed Markets

A landmark study by Harvey, Rattray, Sinclair, and van Hemert (2016), published in The Journal of Portfolio Management, analyzed over 9,000 hedge funds from 1996 to 2014, classifying them as either systematic or discretionary using algorithmic textual analysis of fund prospectuses 323334. The researchers sought to test the prevalent "algorithm aversion" among institutional capital allocators, who frequently presume discretionary human managers are inherently superior to rigid models 3234.

The empirical results dismantled the presumption of human superiority, though the exact nature of outperformance varied significantly by asset class. Within macro strategies, systematic funds significantly outperformed discretionary macro funds, delivering an annualized return of 4.9% compared to 1.6% for their human counterparts 3234. While systematic macro exhibited higher annualized volatility (10.9% versus 5.1%), the risk-adjusted performance - measured by the appraisal ratio - remained marginally in favor of the systematic approach 32.

Within equity strategies, the raw return profile favored humans: discretionary equity managers generated higher absolute returns than systematic equity managers 3234. However, deeper factor attribution analysis revealed that the outperformance of discretionary equity managers was primarily derived from higher exposure to static risk factors (such as simple long exposure to the broader equity market), rather than true alpha or idiosyncratic stock-selection skill 3234. When returns were adjusted for portfolio volatility and these inherent factor exposures, the risk-adjusted returns were virtually identical, with systematic equity yielding a 1.1% appraisal ratio versus 1.2% for discretionary 3234. Similarly, Abis (2017) analyzed mutual funds and found that systematic funds exhibited only slightly lower alphas (by approximately 0.2%) than discretionary funds 35.

Factor Exposures and Alpha Generation

A critical differentiator highlighted by the Harvey et al. (2016) study is how each style structurally generates its returns. Discretionary managers rely far more heavily on established risk factors to generate yield 3234. Discretionary equity funds rely heavily on equity market beta, while discretionary macro funds maintain significant exposure to the FX carry factor and equity markets 3234.

Systematic funds, conversely, generate returns that are less easily explained by traditional risk premia, suggesting higher levels of genuine, uncorrelated alpha 3234. Furthermore, systematic and discretionary excess returns exhibit relatively low correlation to one another - ranging from 0.05 to 0.43 depending on the universe - indicating that the two approaches capitalize on vastly different market inefficiencies and serve as excellent diversifiers within a broader institutional portfolio 35.

| Hedge Fund Strategy | Absolute Return Profile | Risk & Volatility Profile | Factor Attribution | Appraisal / Risk-Adjusted Ratio |

|---|---|---|---|---|

| Systematic Macro | Higher (4.9% annualized) | Higher Volatility (10.9%) | Low reliance on traditional beta | Marginally superior 3234 |

| Discretionary Macro | Lower (1.6% annualized) | Lower Volatility (5.1%) | Moderate factor reliance | Inferior risk-adjusted 3234 |

| Systematic Equity | Moderate | Lower overall market exposure | High genuine alpha | Comparable (1.1%) 3234 |

| Discretionary Equity | Higher Raw Returns | Higher idiosyncratic risk | High reliance on market beta | Comparable (1.2%) 3234 |

Influence of Market Environments

The efficacy of algorithmic versus discretionary swing trading is not universally static; it is highly contingent upon the specific market environment, the liquidity of the underlying assets, and the availability of structured, machine-readable data.

Information Asymmetry in Emerging Markets

Algorithms require vast quantities of clean, structured, and continuous historical data to train predictive models 56. Consequently, systematic strategies excel in Developed Markets (DM) like United States equities or G10 currencies, where data is ubiquitous, regulatory reporting is standardized, markets are highly efficient, and liquidity allows for frictionless execution 565736.

In Emerging Markets (EM), however, the operational landscape structurally favors human discretionary trading 563738. Emerging markets suffer from pronounced data scarcity, less reliable financial reporting, lower analyst coverage, and significant political and regulatory instability 56573861. The fundamental relationships that drive algorithmic models in DM frequently break down in EM; for example, the traditional correlation between rising interest rates and currency appreciation often inverses in EM due to severe capital flight risks 56.

In these low-validity, high-asymmetry environments, qualitative human judgment holds a distinct informational advantage. Discretionary managers can parse unstructured data - such as sudden shifts in local government policy, changes in management quality, or infrastructure modernization - that quantitative models cannot accurately index 573738. This is evidenced by the massive "active share" (a metric defining how far a portfolio deviates from its benchmark index) maintained by discretionary EM managers. Active share in EM equities often exceeds 80% or 93%, allowing human managers to generate significant alpha over passive or systematic counterparts by avoiding state-owned enterprises or highly indebted sectors that dominate the indices 373839.

Liquidity and Capacity Constraints

Furthermore, emerging markets feature substantially lower liquidity and higher transaction costs compared to developed markets 5636. Algorithmic strategies, which often rely on higher turnover and the rapid execution of statistical arbitrage, suffer severe performance degradation due to slippage and market impact costs in illiquid EM environments 2456. Discretionary swing traders, who typically hold positions for longer durations and require fewer total transactions, are far less penalized by wider bid-ask spreads 356. The overall capacity of pure quantitative strategies is thus naturally capped in emerging markets, forcing institutions to rely on human stock-pickers, particularly in the highly inefficient EM small-cap sector 563738.

Hybrid Centaur Trading Architectures

The empirical evidence presents a fascinating dichotomy: systematic models definitively conquer human cognitive biases, prevent emotional revenge trading, and eliminate the performance drag of the disposition effect 72023. Yet, human discretionary traders maintain a distinct superiority in navigating unprecedented regime shifts, analyzing unstructured qualitative data, and operating in low-liquidity, high-asymmetry environments 232456.

In modern financial markets, the frontier of swing trading is moving away from a binary choice between "man" or "machine" and toward highly integrative decision architectures 4064. This synthesis is frequently termed the "Centaur" model or "Human-in-the-Loop" (HITL) algorithmic trading 65666768. Borrowed from advanced freestyle chess - where teams of humans and algorithms operating collaboratively consistently defeat both solo human grandmasters and solo supercomputers - the Centaur model allocates tasks based strictly on the comparative advantages of silicon and carbon 76741.

The Centaur Trading Model

In a hybrid swing trading architecture, the machine acts as the primary engine for information acquisition, signal generation, and quantitative risk allocation. The algorithm processes vast datasets to identify statistical anomalies, mean-reversion setups, and momentum shifts far faster than human cognition allows, entirely devoid of fatigue or emotional tilt 40644271.

However, rather than executing autonomously into the live market, the algorithm presents the opportunity to a human expert who serves as a supervisory filter. The human's role is not to calculate standard probabilities or manually execute the trade, but to provide contextual interpretation, verify prevailing market regimes, and veto trades that are mathematically sound but contextually flawed - the precise "broken leg" scenarios Meehl warned of 406467. Organizations utilizing this model maintain rigid risk parameters where humans can alter thresholds, impose risk caps, or cancel trades due to external contextual risks, but they cannot force the system to take a trade that violates the base quantitative rules 4373.

Empirical Validation of Hybrid Systems

A rigorous 2024 academic study by Carlo Zarattini and Marios Stamatoudis empirically validated the exponential power of this hybrid approach in a specific swing trading context 44. The researchers analyzed 9,794 overnight stock gap events between 2016 and 2023. A purely mechanical, systematic strategy attempting to buy all of these gaps possessed a significant negative statistical edge, consistently losing money with cumulative daily losses reaching -0.25R (Risk Units) after eight days 44.

The researchers then introduced an experienced discretionary technical trader to act as a filter. To ensure a rigorous evaluation and prevent forward-looking bias, specialized software was utilized to anonymize charts, isolating the trader's intuition from external fundamental noise 44. The human trader was permitted to override the algorithm, selecting only the roughly 18% of setups that exhibited favorable multi-week structural context, such as early momentum cycle gaps or multi-month range breakouts 44.

The introduction of human discretionary judgment completely transformed the algorithmic output. The strategy shifted from a losing proposition to a highly profitable system. With additional human micromanagement regarding profit targets and trailing stop-losses, average trade profitability reached a local maximum of 0.80R by day four 44. In a simulated portfolio risking only 0.25% per trade, this hybrid methodology generated a 3,968% total return over eight years 44. The study definitively proved that intuition and contextual pattern recognition - when applied as a strict filter to a mechanical base - can generate alpha that neither system could achieve independently 44.

Regime Shift and Volatility Management

The hybrid model is particularly vital during sudden macroeconomic shocks. Purely algorithmic swing trading strategies - such as trend-following or statistical arbitrage - are heavily calibrated to historical volatility environments. When market regimes violently shift (e.g., during the 2008 global financial crisis or the 2020 pandemic volatility expansion), historical correlations between asset classes instantly break down, and rigid algorithmic models often experience catastrophic drawdowns because the rules of the market have fundamentally altered 252442.

During these systemic shocks, human experts provide the necessary oversight to override algorithmic trading size, pivot from predictive historical models to reactive qualitative assessments, or halt algorithmic execution entirely to preserve capital 2564. By utilizing the machine for computational heavy-lifting and the human for ethical oversight, macroeconomic regime detection, and abstract contextualization, institutions achieve a robustness that successfully insulates the portfolio against both human emotional fragility and algorithmic brittleness 40646641.