How Algorithmic and Manual Swing Trading Differ

Algorithmic trading automates market decisions using pre-programmed code and high-speed execution, entirely removing human emotion from the moment a trade is placed. Manual swing trading relies on human analysis and intuition to hold positions over days or weeks, offering the flexibility to adapt to sudden market shifts. While algorithms provide unmatched discipline and scalability, academic data shows that neither approach guarantees profitability without rigorous risk management and a proven mathematical edge.

The Evolution of Retail Market Participation

The financial markets have undergone a profound structural and technological shift over the past two decades. What was once a landscape dominated by human intuition, physical trading floors, and manual chart analysis has been heavily financialized, digitized, and accelerated. Today, automated trading systems and algorithms account for over 70% of the equity volume in United States markets, with similar saturation occurring in global derivatives and foreign exchange markets 12. This technological revolution has not only transformed institutional finance but has fundamentally altered the competitive environment for the retail investor.

For the modern retail participant, the choice of how to interact with these markets generally falls into two distinct philosophies: manual swing trading and algorithmic trading. The debate between these two methodologies is no longer simply about which yields higher theoretical returns. Instead, it requires a comprehensive understanding of how technology shapes execution, how risk is managed across different time horizons, and how individual traders interact with a highly complex market microstructure 34. Furthermore, the proliferation of retail-facing quantitative tools has blurred the lines between the discretionary trader and the systems engineer, creating a new paradigm where computational logic competes directly with human adaptability.

To determine the optimal approach, one must dissect the core mechanics of each style, examine rigorous academic data on retail profitability, and understand the profound psychological and regulatory implications of automating financial risk.

The Architecture of Manual Swing Trading

Manual swing trading is a traditional, discretionary approach to the financial markets that relies entirely on human cognition, real-time observation, and intuitive decision-making 456. The term "swing" refers to the specific time horizon of the strategy. Rather than engaging in high-frequency day trading - where positions are opened and closed within the same trading session - or long-term investing, a swing trader seeks to capture short-to-medium-term market momentum, holding positions for a period ranging from several days to several weeks 37.

In a manual swing trading framework, the individual trader is responsible for every phase of the execution lifecycle. This process begins with extensive market screening and analysis. Manual traders typically synthesize multiple streams of information to form a directional bias. They rely heavily on technical analysis, utilizing charting platforms to interpret price action, support and resistance levels, and technical indicators such as the Relative Strength Index (RSI) or Moving Average Convergence Divergence (MACD) 46.

Beyond basic price and volume data, sophisticated manual swing traders often incorporate deep contextual analysis. For example, in derivatives markets, experienced manual traders read live option chain data, tracking intraday open interest shifts, put-call ratio changes, and max pain positioning. This allows them to adapt their directional bias in real-time based on where institutional money is actively moving - a nuanced synthesis of data that is notoriously difficult to program into a retail-level algorithm 1. Furthermore, manual traders incorporate fundamental analysis and macroeconomic context, adjusting their strategies based on central bank policy announcements, corporate earnings reports, and geopolitical developments 34.

The paramount advantage of manual swing trading is cognitive flexibility and adaptability. A human trader possesses the unique ability to recognize broad, unprecedented shifts in market regimes. During periods of extreme volatility or high-fear environments - such as a sudden spike in the Volatility Index (VIX) driven by an unforeseen global crisis - a manual trader can quickly synthesize the qualitative nature of the news, recognize that historical price patterns are temporarily invalid, and choose to drastically reduce their position sizing or abstain from the market entirely 129. This discretionary veto power is a critical risk management tool that prevents catastrophic losses during "black swan" events.

However, the manual approach carries severe inherent limitations. Because execution relies on human physical reaction, order placement is inherently slow. A human trader requires hundreds of milliseconds, or often seconds, to process a visual signal, make a decision, and manually submit an order ticket 12. In highly volatile markets, this latency can result in significant slippage, where the price of the asset moves unfavorably before the order is filled. More importantly, manual trading is constantly besieged by human emotional frailty and cognitive biases, which often degrade the mathematical expectancy of an otherwise sound strategy 34.

The Mechanics of Algorithmic Trading

Algorithmic trading, frequently referred to as automated or quantitative trading, represents a complete departure from discretionary execution. It is a method of buying and selling financial instruments using computer programs to automatically execute trades based on highly specific, predefined mathematical criteria 412. Once the underlying logic is coded, the algorithm monitors live market data feeds and executes orders autonomously, operating at speeds and scales that are physically impossible for a human being 1213.

The algorithmic workflow transforms the retail trader from an active market participant into a system architect and risk manager. The process begins with hypothesis generation. A quantitative trader observes a market inefficiency, a recurring statistical pattern, or a theoretical pricing anomaly, and translates this observation into a strict set of testable rules 12. These rules dictate every aspect of the trade, encompassing the entry conditions, the exact position sizing based on account equity, the trailing stop-loss parameters, and the precise exit criteria 1314.

Once the logic is defined, the algorithm must undergo rigorous backtesting. By running the programmed rules against years of historical tick data, the trader can empirically evaluate the strategy's theoretical performance. This historical simulation reveals critical performance metrics, including the expected win rate, the profit factor, the Sharpe ratio, and the maximum historical drawdown - the largest peak-to-trough drop in portfolio value 3315. If the historical performance meets the trader's risk parameters, the algorithm is deployed into a live environment via an Application Programming Interface (API) connected to a brokerage account 21316.

Algorithms excel in areas where human traders inherently struggle. The primary advantage is absolute consistency and emotional sterilization. Because the system follows defined rules without deviation, it eliminates the hesitation, fear, and greed that routinely sabotage manual traders 293. Furthermore, algorithmic trading offers infinite horizontal scalability. While a human swing trader can realistically monitor only a handful of charts simultaneously, an automated system can scan thousands of equities, currency pairs, or commodity futures across multiple timeframes, 24 hours a day, reacting to signals in 10 to 50 milliseconds 123.

Common retail algorithmic strategies include trend following, which seeks to capture sustained directional moves; mean reversion, which capitalizes on the statistical tendency of prices to return to their historical averages after extreme overbought or oversold conditions; and statistical arbitrage, which attempts to exploit temporary pricing inefficiencies between highly correlated assets 2131417. Despite these powerful capabilities, algorithmic trading introduces entirely new categories of risk, including software bugs, connectivity failures, and the rapid degradation of theoretical edges in live markets.

Comparative Execution Dynamics

To fully understand the divergence between these two methodologies, it is helpful to view them across the primary vectors of market execution.

| Operational Vector | Algorithmic Trading | Manual Swing Trading |

|---|---|---|

| Execution Latency | Ultra-fast; typically executes within 10 to 50 milliseconds upon signal generation 12. | Slow; limited by human processing and physical reaction times, often taking 500+ milliseconds 12. |

| Emotional Interference | Zero during execution; the system adheres strictly to coded parameters regardless of volatility 93. | Exceptionally high; decisions are vulnerable to fear, greed, hesitation, and cognitive fatigue 7418. |

| Contextual Adaptability | Extremely rigid; algorithms will continue executing into unforeseen macro events unless manually disabled 12. | Highly fluid; humans can interpret breaking news, qualitative data, and shift strategies instantly 13. |

| Market Scalability | Virtually unlimited; can monitor and trade hundreds of independent instruments concurrently 24/7 2919. | Strictly limited; constrained by human attention span, screen space, and biological necessity 24. |

| Strategy Validation | Highly empirical; relies on extensive computational backtesting across historical datasets 33. | Largely subjective; difficult to backtest intuition, making performance tracking highly vulnerable to hindsight bias 34. |

The Academic Verdict on Retail Profitability

A pervasive narrative marketed by algorithmic platform vendors and online trading educators is that automation acts as a panacea for the retail trader's struggles. The marketing rhetoric suggests that by simply removing human emotion and increasing execution speed, profitability is virtually guaranteed. However, a deep review of regulatory data, brokerage statistics, and rigorous academic literature reveals a much harsher reality regarding retail trader performance.

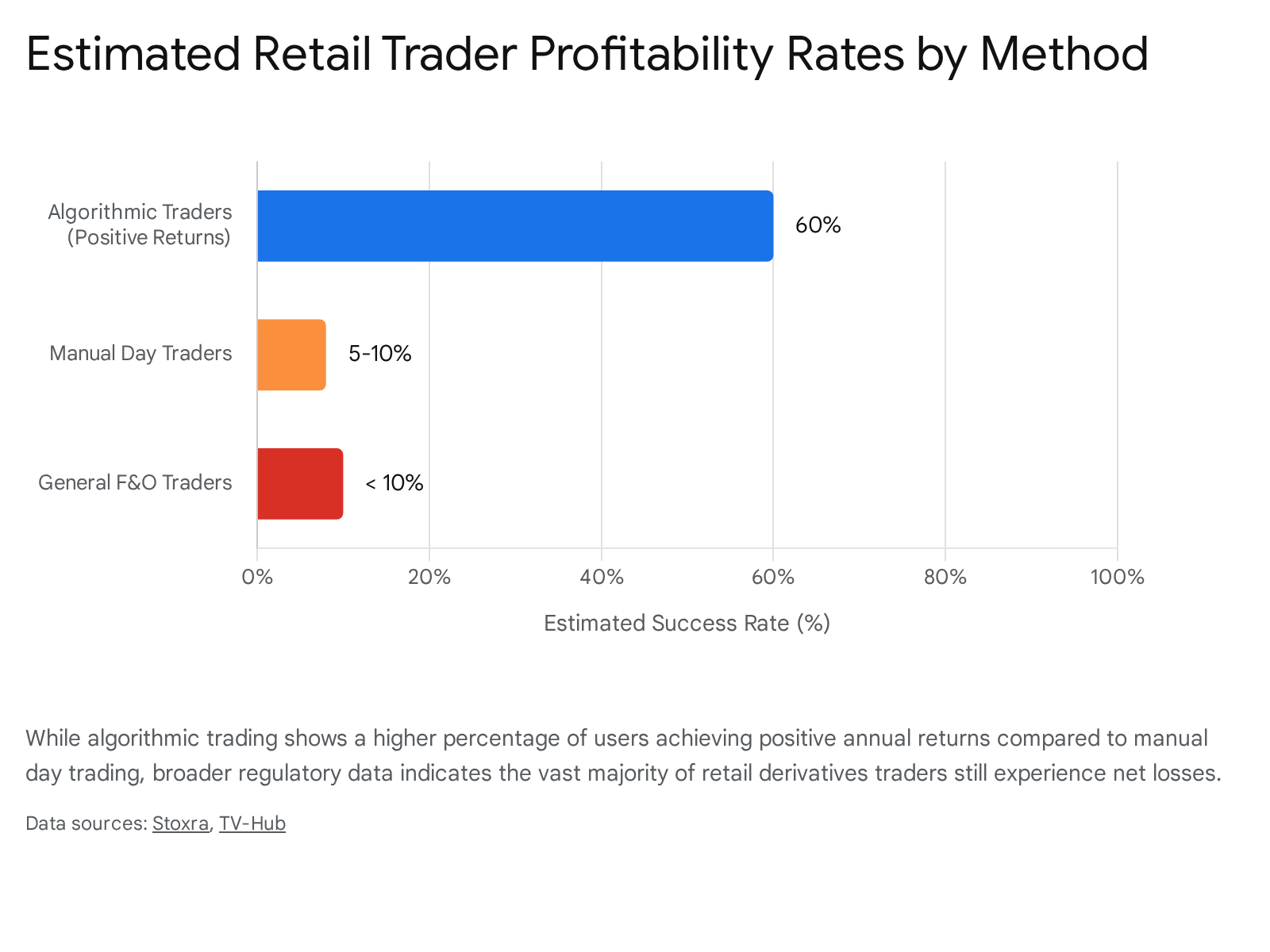

The baseline expectation for retail trading success is overwhelmingly negative. Data published by the Securities and Exchange Board of India (SEBI) and supported by international regulatory studies demonstrates that over 90% of individual futures and options traders experience net capital losses. Crucially, this high failure rate persists regardless of whether the retail participants employ discretionary manual strategies or sophisticated algorithmic systems 1. Furthermore, massive multi-year studies of global markets, such as those tracking the Taiwanese equity market, indicate that only 1% to 3% of active retail traders are predictably and consistently profitable after accounting for transaction fees, slippage, and spread friction 20.

Within this bleak broader landscape, some industry reports suggest a slight statistical edge for automation. Various platform analyses indicate that roughly 60% of retail algorithmic traders show positive annual returns, compared to a success rate of just 5% to 10% for manual day traders 2122.

Automation does effectively eliminate the most common profit-killing human errors, such as revenge trading, missing stop-loss triggers due to hesitation, and fatigue-driven miscalculations 22.

However, achieving a "positive return" in nominal terms is a low benchmark that can be highly misleading. A significant portion of these profitable retail algorithmic systems generate nominal gains that completely fail to outperform a basic, passive buy-and-hold strategy in a broad market index fund like the S&P 500 22. When evaluating risk-adjusted returns - often measured by the Sharpe ratio - successful retail quantitative traders generally achieve modest annual returns of 10% to 20%, far removed from the explosive, triple-digit gains frequently advertised in online forums 1519.

Resolving the Barber and Odean Paradox (2024)

To understand why retail traders consistently fail despite access to institutional-grade technology, one must look to behavioral finance. A landmark 2024 academic study by prominent financial economists Brad M. Barber, Shengle Lin, and Terrance Odean investigated a persistent paradox in modern financial literature. The paradox is this: at short time horizons, retail order imbalances - the net difference between retail buying and selling volume - actually positively predict future stock returns. Yet, despite this predictive power, the average retail investor's trades consistently lose money 567.

Barber and his colleagues discovered that the resolution to this paradox lies in understanding exactly how retail capital is deployed and concentrated across the market. The statistical models that showed retail trades predicting future returns weighted all stocks equally in their calculations. However, in reality, retail purchases are not evenly distributed. They are heavily concentrated in highly salient, "attention-grabbing" stocks - equities experiencing abnormal trading volume, extreme recent price fluctuations, or massive media and social network coverage 57.

Retail investors face an asymmetric attention problem: when deciding what to buy, they must choose from thousands of available equities, heavily biasing their selection toward whatever is currently making headlines. Conversely, when deciding what to sell, they generally only consider the handful of stocks they already own 7. The researchers found that these attention-grabbing stocks subsequently experience severe underperformance, dragging down the aggregate returns of the retail cohort 57.

The financial impact of this behavioral bias is devastating. The study demonstrated that long-short quantitative strategies based on extreme quintiles of retail order imbalance earned a dismal annualized return of -14.8% among stocks with heavy retail trading volume 5626. Furthermore, the study noted that small retail trades - which serve as a reliable proxy for less sophisticated, undercapitalized investors - were the most highly concentrated in these attention-grabbing assets and performed significantly worse than larger trades 567. This rigorous academic evidence proves that the failure of the retail trader is not solely a consequence of slow manual execution or a lack of automation; it is fundamentally an issue of flawed strategy, poor market selection, and overwhelming adverse behavioral biases. If a retail trader uses an algorithmic platform to automate the purchasing of attention-grabbing stocks, they simply accelerate the destruction of their capital.

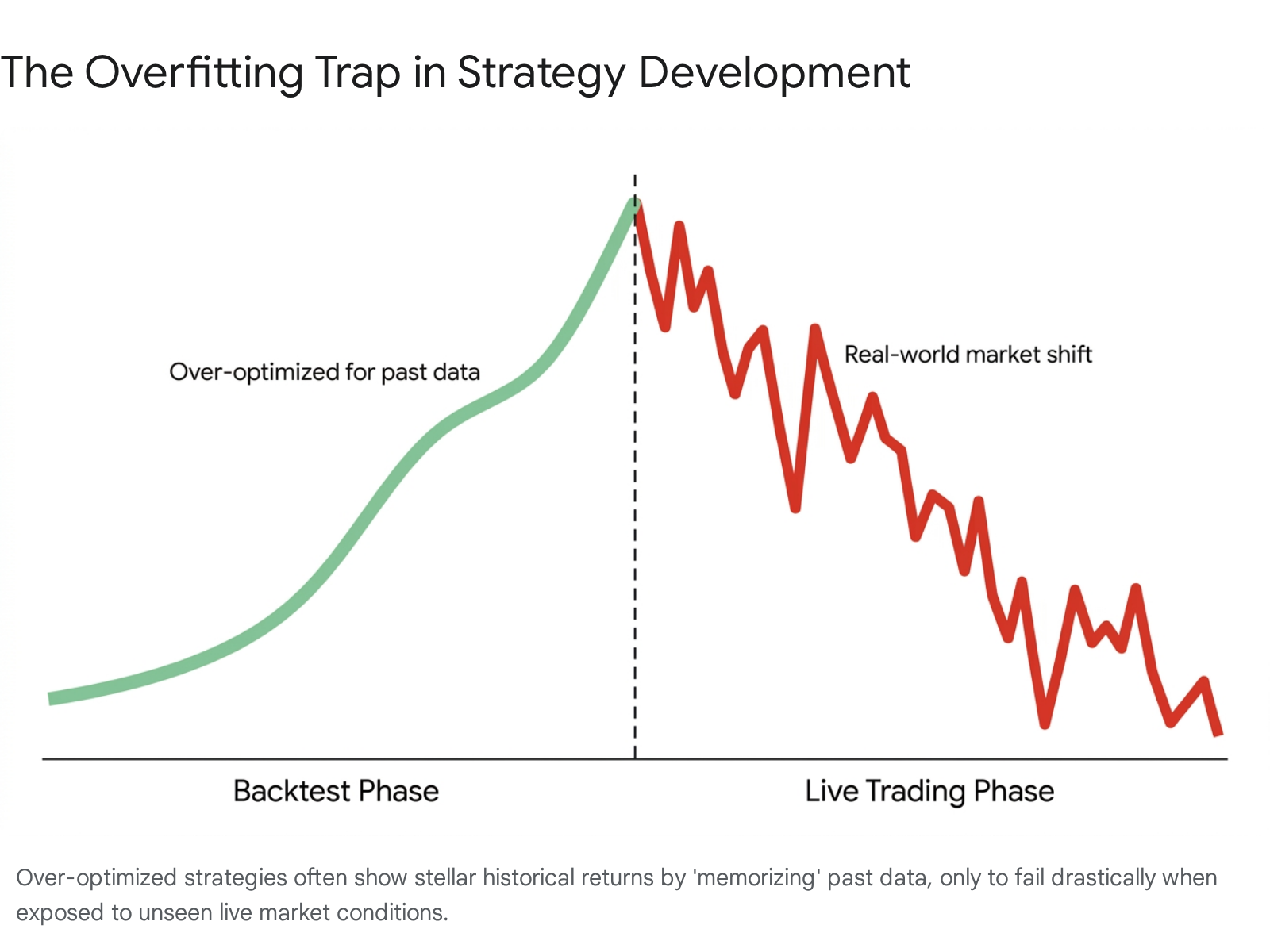

The Overfitting Trap and Strategy Decay

When an algorithmic trader discovers that their system is failing, they often blame the market rather than the code. However, the primary structural reason that retail algorithmic strategies fail to generate sustained live profits is a mathematical phenomenon known as "overfitting" or "curve-fitting" 119.

The algorithmic design process relies heavily on backtesting against historical data. Because modern platforms offer immense computational power, a retail developer can easily run thousands of permutations of a strategy, adjusting variables - such as moving average lengths, RSI thresholds, and specific day-of-the-week entry conditions - until the historical equity curve looks like a perfectly smooth, upward-sloping line, boasting massive theoretical returns.

This process is fundamentally flawed. By optimizing the parameters too heavily, the developer inadvertently builds a system that perfectly memorizes the random statistical noise of the past, rather than discovering a robust, persistent structural edge 1922.

Extensive quantitative studies of algorithmic strategies reveal that heavily optimized backtest Sharpe ratios have near-zero predictive power for live, forward-looking returns. Over-fitted strategies routinely lose up to 80% of their theoretical, backtested profits immediately upon going live in unseen market conditions 22.

Furthermore, even if a retail algorithm identifies a genuine market inefficiency and avoids the overfitting trap, it remains vulnerable to "alpha decay." As markets evolve and institutional participants discover similar inefficiencies, the profit margin associated with the strategy erodes 20. The typical live lifespan of a retail algorithmic strategy before strategy decay renders it unprofitable is remarkably short, often lasting only 6 to 12 months 1. After this period, the strategy requires intensive human intervention, recalibration, and re-validation, proving that algorithmic trading is never a truly passive endeavor 119.

High-Frequency Trading vs. Retail Algorithms

A dangerous misconception among retail investors is the belief that utilizing basic algorithmic execution software allows them to compete on a level playing field with massive Wall Street institutions. It is imperative to clearly delineate the boundaries between Retail Algorithmic Trading and institutional High-Frequency Trading (HFT).

HFT represents an ultra-sophisticated subset of algorithmic trading that currently accounts for approximately 50% of total U.S. equity and Treasury trading volume 227. The core operational principle of HFT is ultra-low latency. These institutional systems execute thousands of complex orders within microseconds (millionths of a second) 12131427. Achieving this level of speed requires astronomical capital expenditures. HFT firms spend tens to hundreds of millions of dollars on bespoke hardware, field-programmable gate arrays (FPGAs), direct microwave tower transmission networks, and crucial "co-location" agreements, wherein the firm's proprietary servers are physically installed inside the same data centers that house the actual exchange matching engines 13202728.

Retail algorithmic traders operate in an entirely different universe. They access the markets through standard retail brokerages, routing their automated orders over public internet connections or commercial cloud-based Virtual Private Servers (VPS). Consequently, even a highly optimized retail algorithm requires roughly 10 to 50 milliseconds to transmit a signal and receive an execution fill 1. While this is vastly faster than human reaction time, it is an eternity compared to institutional systems. Because retail algorithms cannot compete on speed, any retail strategy attempting to capture microsecond inefficiencies, execute high-frequency arbitrage, or scalp fractional pennies will face certain failure 219.

Market Structure Impacts and Ghost Liquidity

The dominance of institutional HFT has fundamentally altered the microstructure of the market, introducing systemic impacts that directly affect retail trading. Michael Lewis's highly influential book Flash Boys brought global attention to the potentially predatory nature of certain HFT strategies, characterizing them as a form of "legalized front-running" 2889. The primary concern raised by critics is that HFT algorithms can detect the initial routing signals of large institutional or retail orders and race ahead of them - using superior speed infrastructure - to purchase the available liquidity and immediately sell it back to the original buyer at a marginally higher price 2810.

While defenders of HFT accurately note that the practice has dramatically tightened bid-ask spreads and increased apparent market liquidity, regulators and academics note that this liquidity is often fragile 228. HFT introduces the phenomenon of "ghost liquidity" - massive buy or sell limit orders that populate the order book but vanish within milliseconds when a price level is approached. This algorithmic order cancellation makes it exceedingly difficult for slower participants, particularly retail traders, to execute their trades at anticipated prices 289.

Due to these structural disadvantages, realistic retail algorithmic strategies must operate on significantly longer time horizons. Successful retail quantitative strategies, such as longer-term trend following, swing-based mean reversion, or portfolio rebalancing algorithms, execute over periods ranging from minutes to weeks 2121427. On these extended timeframes, the microsecond speed advantages and ghost liquidity tactics of HFT firms become mathematically irrelevant to the strategy's outcome.

Institutional vs. Retail Infrastructure Breakdown

| Metric | High-Frequency Trading (HFT) | Retail Algorithmic Trading |

|---|---|---|

| Execution Horizon | Microseconds to milliseconds 1327. | Minutes, hours, days, or weeks 21227. |

| Infrastructure Required | Exchange co-location, bespoke FPGAs, microwave networks 1327. | Cloud VPS, retail brokerage APIs, standard internet 21216. |

| Capital Barrier | Tens to hundreds of millions of dollars 2728. | Highly accessible; $500 to $10,000+ 21232. |

| Strategy Archetypes | Market making, latency arbitrage, order book imbalance 13149. | Trend following, mean reversion, momentum 21214. |

The Psychology of Trading: The Marathon vs. The Machine

It is a widely accepted axiom among market professionals that trading success is heavily dependent on psychology and emotional control, often outweighing pure technical analysis in importance 4. The assumption that transitioning to algorithmic trading solves all psychological problems is inaccurate; automation merely shifts the emotional burden to different phases of the trading lifecycle.

The Emotional Crucible of the Swing Trader

For the manual swing trader, navigating the market requires profound emotional endurance. Because swing trades develop over days or weeks, the trader's battle is a slow marathon, not a frantic sprint 7. The manual trader must wait patiently, sometimes for weeks, for a specific technical setup to materialize without forcing a suboptimal entry. Once a position is established, they must endure the deep psychological discomfort of holding positions overnight, subjecting their capital to unpredictable after-hours news cycles and opening price gaps 7.

Manual traders are perpetually besieged by universal cognitive biases. Fear frequently causes premature exits from highly profitable positions, leading traders to abandon their mathematical edge and leave substantial gains unrealized 741833. Conversely, greed and loss aversion lead manual traders to hold onto losing positions far beyond their predefined stop-loss levels, hoping against statistical probability for a market reversal 1833. Risk management for a discretionary trader is fundamentally an exercise in intense self-management, requiring the trader to view their capital with severe emotional detachment and strict discipline 3334. The failure to master this internal psychological landscape is the primary reason the vast majority of manual traders fail.

The Hidden Psychology of the System Manager

Algorithmic trading effectively resolves the issues of hesitation and panic at the exact moment of execution. A programmed bot will trigger a stop-loss order instantly, devoid of hope or regret 2311. However, the human architect behind the algorithm is not immune to psychological distress.

The profound psychological trap for algorithmic traders occurs during periods of strategic drawdown. Because financial markets are dynamic, even the most robust algorithms will experience extended periods where their specific logic is out of sync with the current market regime, resulting in consecutive losses 15. During these drawdowns, the retail quant experiences severe anxiety, often compounded by the "black box" nature of their automated system 11. The psychological pressure frequently causes the trader to intervene manually, abruptly disabling the algorithm just before the mathematical edge would have eventually normalized the equity curve 115.

Furthermore, algorithmic trading can breed dangerous technological overconfidence. Traders who have visually confirmed a stunning, optimized backtest often lack the psychological restraint to manage risk appropriately, deploying the untested system with excessive leverage. When the inevitable live market drawdown occurs, the oversized losses trigger panic, demonstrating that even a fully automated system can be ruined by poor human risk management 1519.

The 2026 No-Code Revolution

Historically, the algorithmic trading landscape resembled an exclusionary fortress, guarded by the necessity of deep programming expertise in languages like Python, C++, or MQL5, and the complex management of raw data feeds and broker APIs 3321237. Retail traders without computer science backgrounds were relegated to manual trading or purchasing questionable, pre-packaged "black box" trading bots.

By 2025 and 2026, this paradigm was shattered by a massive wave of technological democratization. The algorithmic trading market expanded aggressively into the retail sector, driven by the explosive growth of "no-code" and "low-code" Software as a Service (SaaS) platforms 337381314. Platforms such as Tradetron, Composer, TradingView, QuantConnect, and Capitalise.ai revolutionized access by allowing users to construct complex, multi-leg trading algorithms using visual, drag-and-drop interfaces 315321241. Moreover, the integration of generative Artificial Intelligence (AI) and Large Language Models (LLMs) enabled retail traders to generate functional trading logic using simple, plain English prompts, bypassing the need to understand programming syntax entirely 12371543.

The Illusion of Automated Competence

While no-code platforms have successfully democratized the tools of automated execution, they have not democratized financial wisdom. The ease of building a strategy has led to a flood of poorly constructed retail algorithms, and research clearly indicates that the vast majority of retail users on no-code platforms still fail to achieve long-term profitability 15.

Successful quantitative trading demands a rigorous understanding of concepts that a drag-and-drop interface cannot automatically bestow. A trader must understand market regime recognition - knowing when a macro-environment has shifted from ranging to trending. They must grasp complex risk-return relationships, understand the mathematical realities of maximum drawdowns, and possess the statistical knowledge required to distinguish between genuine, repeatable alpha and mere random luck in a backtest 15.

The critical danger of the no-code revolution is that it allows inexperienced retail participants to construct systems with remarkable speed. However, a trader who lacks a foundational understanding of market mechanics will simply use these advanced platforms to automate their own flawed logic, executing poorly conceived strategies with greater frequency and efficiency, thereby accelerating their financial losses 1522.

The Financial Drag: Hidden Infrastructure Costs

When analyzing the viability of algorithmic trading, retail participants frequently underestimate the severe financial drag created by the fixed overhead required to operate a reliable automated system.

Manual swing trading is highly cost-efficient. It generally requires only a funded brokerage account, basic internet access, and perhaps a nominal fee for a charting platform 13. The costs are predominantly variable, tied directly to the commissions and spread friction of the trades executed.

In contrast, deploying a professional-grade automated system - even at the retail level - requires robust technological infrastructure. While an institutional algorithmic trading system can incur initial build capital expenditures (CAPEX) exceeding $120,000, along with hundreds of thousands in specialized payroll and fixed data licensing fees, retail costs are lower but still highly impactful 441617.

A serious retail algorithmic trader must account for persistent monthly overhead to ensure execution reliability. This includes: 1. Platform Subscriptions: Access to advanced strategy builders, no-code visual editors, and cloud-based backtesting engines typically costs between $50 and $200+ per month 1215. 2. Virtual Private Servers (VPS): To prevent algorithmic downtime caused by local power outages or home network instability, traders must lease remote cloud servers to host their software, ensuring 24/7 connectivity to the exchange 161247. 3. Market Data Feeds: Algorithms require clean, uninterrupted streams of tick data to function accurately; institutional-quality API data is rarely provided for free.

These fixed infrastructure costs typically total between ₹1,500 and ₹10,000+ per month (or roughly $20 to $150+ USD) depending on the geographic market and data requirements 1. Consequently, a retail algorithmic trader faces a massive hurdle rate: they must generate significantly higher gross profits than a manual trader simply to reach a breakeven net profitability 1. For undercapitalized traders with small accounts, these fixed monthly costs disproportionately consume any generated alpha, making the automated endeavor mathematically futile regardless of the strategy's quality.

Regulatory Scrutiny and Market Integrity Risks

As the volume of automated trading has surged, regulatory bodies such as the U.S. Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) have recognized the systemic risks posed by unchecked algorithmic execution. The deployment of unmonitored code is no longer viewed merely as an individual financial risk, but as a potential threat to broader market stability 184919.

FINRA and SEC Compliance Mandates

Regulatory frameworks, notably FINRA Rule 3110 (Supervision) and the SEC's Market Access Rule, require stringent oversight of all automated trading activities. Broker-dealers are mandated to establish comprehensive policies to review, test, and control algorithmic strategies before they are deployed into live production 18512053. These controls are designed to prevent catastrophic technological failures. The industry's primary cautionary tale remains the 2012 Knight Capital incident, wherein a flawed software deployment bypassed testing protocols, causing the firm's systems to rapidly acquire massive, unintended equity positions, resulting in a staggering $460 million loss in under 45 minutes 54.

While retail traders deploy significantly less capital than institutional prop desks, their algorithms remain subject to strict market integrity rules. FINRA actively utilizes cross-market automated surveillance systems to monitor for manipulative trading patterns 2156. If a retail trader poorly codes an algorithm, it may inadvertently execute rapid cancellation patterns or cross-trades that regulators classify as illegal "spoofing," "layering," or "wash trading" 215622. Firms that fail to monitor and halt these algorithmic anomalies face multi-million dollar penalties and intense enforcement actions 56.

Furthermore, regulators expect full transparency regarding how artificial intelligence and automated tools make decisions. In the notable enforcement action against BlueCrest Capital Management, the SEC emphasized that the failure to adequately disclose the use of algorithmic trading systems - and the specific risks and underperformance associated with those models compared to live traders - constitutes a severe regulatory breach 5859.

The Danger of Excessive Trading and Margin

Regulators routinely issue investor alerts highlighting the specific dangers associated with the velocity of automated trading. Algorithms can execute hundreds of trades per day, generating massive commission costs and continuous bid-ask spread friction that deeply erode the retail trader's principal 232425. FINRA explicitly warns that excessive intra-day trading strategies are extremely risky and generally inappropriate for individuals with limited resources or experience 23.

These risks are magnified exponentially when algorithmic systems are granted access to margin - borrowed funds provided by the brokerage 232526. A sudden, violent market fluctuation against an automated, highly-leveraged position can trigger severe margin calls, forcing the liquidation of the portfolio and potentially leaving the retail trader with debt obligations that exceed their initial investment 2325. The SEC explicitly cautions retail participants against relying on "black box" automated systems or social media copy-trading algorithms, reiterating that short-term trading in volatile markets carries profound risks of capital destruction 545826.

The Hybrid Approach: Synthesizing Code and Intuition

The debate over algorithmic trading versus manual swing trading frequently presents a false dichotomy, implying that a trader must completely abandon human judgment to harness computational power. The academic and empirical data does not support the claim that pure algorithms universally outperform manual execution in the retail sphere. Rather, performance depends intricately on the specific strategy architecture, the trader's capitalization, and the current macroeconomic regime 19.

Extensive market analysis indicates that the most successful and resilient retail traders are increasingly adopting a hybrid model 132. This methodology seeks to merge the distinct advantages of both approaches while mitigating their respective flaws.

In a hybrid framework, the trader utilizes the computational scale of algorithms to execute the heavy lifting: rapidly scanning thousands of global assets, validating hypotheses through historical backtesting, filtering out emotional noise, and enforcing rigid downside risk parameters such as automated trailing stops 134. However, the trader explicitly retains human discretionary oversight to manage complex, qualitative variables that machines struggle to parse. The human manager monitors the broader macroeconomic context, reads nuanced option chain positioning, evaluates geopolitical breaking news, and exercises the ultimate veto power over whether an automated signal should be allowed to execute into a fragile market 13227. By combining the relentless consistency of code with the adaptable intuition of a seasoned market participant, the hybrid trader creates a robust system capable of surviving the unpredictable shocks that routinely break purely automated programs.

Bottom line

Algorithmic trading utilizes computational power and pre-coded logic to execute trades with immense speed and emotional discipline, whereas manual swing trading relies on human analysis and adaptability to navigate market shifts over days or weeks. Despite the technological democratization brought about by recent no-code platforms, retail traders face extraordinarily high failure rates across both methodologies due to psychological lapses, high infrastructure costs, and flawed strategy optimization. Ultimately, automation is not a substitute for profound market knowledge; the most effective approach merges the rigorous scalability of algorithms with the nuanced, macro-contextual judgment of a human manager.