How the CLARITY Act Would Change Crypto in 2026

The CLARITY Act is a proposed federal law that aims to permanently resolve cryptocurrency regulatory ambiguity by dividing market oversight between the Securities and Exchange Commission and the Commodity Futures Trading Commission. By classifying sufficiently decentralized tokens as commodities and introducing strict operational rules for digital asset exchanges, the bill seeks to bring the offshore crypto industry safely back to the United States. If passed by the Senate in 2026, the legislation would fundamentally rewrite the structural rules for blockchain developers, retail traders, and institutional investors in the digital asset market.

The Origins of a Structural Market Overhaul

For more than a decade, the United States cryptocurrency industry operated without a dedicated statutory framework. The resulting void sparked a prolonged jurisdictional tug-of-war between two powerful federal agencies: the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) 12. The core of the dispute centered on the legal definition of a digital asset. The SEC historically viewed the vast majority of crypto tokens as unregistered securities, pursuing an aggressive strategy of regulation by enforcement against major exchanges, token issuers, and decentralized protocols 13. Conversely, the CFTC claimed authority over tokens it viewed as commodities - most notably Bitcoin and Ether - but lacked the statutory power to oversee the spot, or cash, markets where everyday retail trading actually occurs 14.

This overlapping authority forced cryptocurrency businesses to operate in a persistent legal gray area. Digital asset exchanges faced immense legal risks when listing new tokens, software builders had no clear compliance pathway for launching decentralized networks, and institutional capital remained largely sidelined due to the sheer unpredictability of the regulatory environment 54. By the beginning of 2026, the economic consequences of this ambiguity had become starkly apparent. Industry data revealed that nearly eighty-eight percent of centralized exchange trading volume had migrated to non-U.S. platforms, while the share of blockchain developers based in the United States had plummeted to just nineteen percent, representing a severe drop over the previous decade 7.

The Digital Asset Market Clarity Act of 2025, widely known as the CLARITY Act and formally designated as H.R. 3633, was drafted specifically to arrest this capital flight. Introduced by House Financial Services Chairman French Hill, the legislation represents the most comprehensive attempt in U.S. history to bring the digital asset industry under a formal, predictable regulatory umbrella 25. The bill passed the House of Representatives in July 2025 with robust bipartisan support, securing a 294-134 vote that included seventy-eight Democrats crossing the aisle 25. The legislation subsequently advanced through the Senate Banking Committee in May 2026 in a 15-9 vote, positioning it for a highly anticipated and fiercely debated floor vote 96.

Dividing Jurisdiction: The SEC and the CFTC

The central innovation of the CLARITY Act is a functional taxonomy that sorts every digital asset into specific regulatory categories based on the asset's underlying economic reality and the decentralization of its network. This framework effectively ends the border dispute between market regulators by replacing the traditional, decades-old securities analysis with a modernized statutory rulebook 1712.

Investment Contract Assets Under the SEC

Tokens sold primarily to raise capital for a project - functioning much like a traditional startup equity fundraising round - remain firmly under the jurisdiction of the SEC. If a centralized development team is actively building a network and investors are purchasing the token with the expectation of profiting from that specific team's managerial and entrepreneurial efforts, the CLARITY Act classifies the asset as an investment contract asset 15.

The SEC retains full, unmitigated authority over these primary market offerings. This ensures that network founders and corporate entities must still provide transparent financial disclosures to the public, protecting retail investors from informational asymmetry 38. Furthermore, the legislation imposes strict disposition restrictions on these assets, severely limiting the amount of tokens that company insiders and founders can resell over a twelve-month period to prevent market manipulation and predatory dumping on retail buyers 9. Under this framework, traditional securities remain securities, fraud remains strictly illegal, and the SEC retains its full enforcement authority over digital asset securities 78.

Digital Commodities Under the CFTC

The CLARITY Act's most consequential structural shift is handing the CFTC exclusive regulatory authority over the spot markets for digital commodities 110. The bill defines a digital commodity as an asset whose value is intrinsically linked to the programmatic operation of a functional blockchain network, driven by supply and demand dynamics rather than the ongoing efforts of a centralized corporation 31112. Bitcoin and Ether are explicitly recognized as falling into this category 413.

Under the proposed law, any cryptocurrency exchange, broker, or dealer that facilitates the trading of digital commodities must register directly with the CFTC 13. This represents a massive expansion of the CFTC's historical mandate, which traditionally focused on derivatives and futures rather than underlying cash markets 4. Registered entities must comply with rigorous rules regarding customer fund segregation, continuous anti-money laundering reporting, and strict anti-fraud oversight 39. By creating specialized registration categories - such as the Digital Commodity Exchange, Digital Commodity Broker, and Digital Commodity Dealer - the act allows platforms to operate legally in the United States without the looming threat of retroactive SEC enforcement 1210.

The Mature Blockchain Transition Test

To bridge the conceptual gap between an early-stage startup venture and a mature, globally decentralized network, the CLARITY Act introduces a novel legal mechanism known as the mature blockchain test. This provision recognizes that a token may begin its lifecycle as a security but eventually evolve into a commodity 23.

Legal scholars frequently compare this dynamic to the traditional Howey test using an agricultural analogy. Selling a subdivided parcel of an orange grove alongside a centralized management and profit-sharing contract constitutes a securities transaction, because the buyer relies entirely on the seller's efforts to cultivate the fruit and generate profit. However, the oranges themselves, when eventually sold downstream at a grocery store, are simply commodities 1420. The CLARITY Act codifies this separation, establishing a statutory firewall between the initial capital-raising investment contract and the underlying digital asset 20.

For a token to graduate from SEC oversight to CFTC oversight, the network must prove it has achieved sufficient decentralization 221. The statutory criteria for maturity dictate that no single entity or affiliated group of persons can control twenty percent or more of the token supply or the network's outstanding voting power 2. Furthermore, the network's underlying software code must be entirely open-source, and the token must possess practical, functional utility beyond mere financial speculation 2. For older, more established blockchain networks, the law imposes an additional hurdle, requiring that at least half of all outstanding tokens be held by individuals or entities entirely unaffiliated with the original founding team 2.

Summary of the CLARITY Act Asset Taxonomy

| Asset Classification | Primary Federal Regulator | Definition & Market Characteristics | Regulatory Impact on Intermediaries |

|---|---|---|---|

| Digital Commodity | Commodity Futures Trading Commission (CFTC) | Decentralized assets where value derives intrinsically from network utility (e.g., Bitcoin, Ether). | Exchanges, brokers, and dealers must register with the CFTC to facilitate spot market trading. |

| Investment Contract Asset | Securities and Exchange Commission (SEC) | Tokens reliant on a centralized team's essential managerial efforts for value appreciation. | Issuers must file formal financial disclosures; insiders face strict legal limits on token resale volumes. |

| Payment Stablecoin | Banking Regulators / FDIC / OCC | Fiat-pegged digital assets governed primarily under the parallel GENIUS Act. | Issuers face 1:1 reserve requirements; exchanges are prohibited from paying passive, deposit-like yield. |

Capital Formation and the "Regulation Crypto" Framework

Historically, launching a digital token in the United States required entrepreneurs to navigate a complex web of securities laws designed during the Great Depression. The sheer cost and legal risk of compliance drove many blockchain startups to launch exclusively in offshore jurisdictions. In anticipation of the CLARITY Act's passage, the SEC under Chairman Paul Atkins moved to create a complementary administrative framework in early 2026, widely referred to as Regulation Crypto Assets 221516.

This proposed administrative safe harbor is designed to provide bespoke pathways for blockchain innovators to raise capital domestically while maintaining appropriate retail investor protections. The framework operates in tandem with the CLARITY Act's broader structural reforms and introduces two highly anticipated exemptions for software builders 1517.

The first pathway is the startup exemption, which functions as a time-limited registration runway for early-stage cryptocurrency projects. This exemption allows developers to raise up to five million dollars over a four-year period without triggering the full, burdensome suite of traditional public company securities compliance 2215. Instead of filing traditional prospectuses, these startups must provide the public with principles-based disclosures outlining the token's mechanics, technological goals, and risk factors, a requirement that closely mirrors the industry standard of publishing a detailed technical whitepaper 15.

The second pathway is a much larger fundraising exemption aimed at established projects preparing for wider market entry. This provision permits issuers to raise up to seventy-five million dollars in any twelve-month period 221517. To utilize this higher threshold, projects must submit a formal disclosure document to the SEC that includes audited financial statements and a detailed discussion of the issuing entity's financial condition 2215. To prevent the dangerous concentration of network control, this exemption also stipulates that no single buyer can end up holding more than ten percent of the total token supply 26. By providing these clear, tiered capital-raising pathways, the legislation aims to repatriate blockchain innovation and reverse the decade-long trend of talent bleeding to foreign markets 722.

The Stablecoin Yield Compromise

One of the most fiercely contested components of the CLARITY Act involves the treatment of stablecoins - digital assets pegged one-to-one with a fiat currency like the U.S. dollar. The debate over stablecoins cannot be understood without first examining the Guiding and Establishing National Innovation for U.S. Stablecoins Act, commonly known as the GENIUS Act, which was signed into federal law by President Trump in July 2025 1819.

The GENIUS Act established the foundational prudential framework for dollar-denominated stablecoins. It mandated that permitted payment stablecoin issuers maintain identifiable reserves backing all outstanding tokens on a strict one-to-one basis, limiting those reserves to highly liquid assets such as U.S. currency, short-term Treasury securities, and approved repurchase agreements 192021. Crucially, the GENIUS Act explicitly prohibited the issuers of stablecoins from paying any form of interest or yield to token holders, effectively ensuring that stablecoins functioned purely as payment instruments rather than unregistered money market funds 212620.

However, the GENIUS Act contained a perceived loophole: while the direct issuers of stablecoins could not pay yield, the law did not explicitly prevent third-party cryptocurrency exchanges or decentralized lending platforms from offering lucrative returns to users who parked their stablecoins on those platforms 2620. This dynamic triggered intense pushback from the traditional banking sector. Banking trade associations and lobbyists argued that if cryptocurrency exchanges were permitted to offer high, passive interest rates on stablecoin balances, it would spark a massive outflow of retail deposits from regional and community banks into unregulated crypto platforms, thereby threatening the stability of the traditional financial system 2223.

To salvage the CLARITY Act and secure vital bipartisan support in the Senate Banking Committee, Senators Thom Tillis and Angela Alsobrooks brokered a complex compromise embedded in Section 404 of the legislation 62425. The finalized statutory language extends the GENIUS Act's restrictions, explicitly prohibiting covered digital asset service providers, including exchanges and brokers, from paying U.S. customers any passive, deposit-like interest or yield on their stablecoin balances 29.

Simultaneously, the compromise preserves the ability of the cryptocurrency industry to function by permitting narrowly defined, activity-based rewards. Exchanges and platforms are legally allowed to distribute yield to users if that yield is genuinely tied to active participation in a network, such as staking, facilitating payments, executing transfers, or providing liquidity to a trading pool 52122. This nuanced distinction aims to insulate the banking sector from direct deposit competition while allowing blockchain networks to utilize economic incentives to bootstrap network utility and adoption 2125.

Navigating the Decentralized Finance (DeFi) Carve-Out

A persistent existential threat to the blockchain industry has been the fear that software developers could be held criminally or civilly liable for the illicit actions of users interacting with open-source code. Decentralized finance, or DeFi, relies on automated smart contracts that allow users to lend, borrow, and trade assets peer-to-peer without a centralized intermediary 2626.

Section 409 of the CLARITY Act directly addresses this friction point by establishing an exclusion for decentralized finance activities. The legislation clarifies that software developers who write, publish, or maintain open-source code, and network participants who merely validate transactions, are not automatically classified as financial intermediaries, brokers, or money transmitters 8926. This protection, which incorporates language from the subsidiary Blockchain Regulatory Certainty Act, ensures that non-custodial actors - those who never actually take legal or technical control of a user's funds - are exempt from the heavy registration burdens applied to centralized exchanges 2927.

However, this statutory safe harbor is not an absolute free pass for the DeFi sector. The legislation draws a sharp distinction between operating an autonomous protocol and operating a financial intermediary. If a purported DeFi platform retains administrative keys that allow developers to unilaterally freeze, move, or alter customer assets, the platform is deemed non-decentralized and must register with the appropriate federal agencies 29. Furthermore, while non-custodial developers are exempt from basic registration, the CLARITY Act explicitly preserves the authority of both the SEC and the CFTC to aggressively prosecute fraud, market manipulation, and intentional sanctions evasion across all decentralized networks 262627.

Safeguarding the Retail Investor

While the cryptocurrency industry has largely championed the CLARITY Act for its operational clarity, the legislation is fundamentally engineered as a consumer protection bill. The sweeping regulations are heavily informed by the catastrophic market failures of 2022, most notably the collapse of the FTX exchange, which resulted in billions of dollars in lost retail deposits 78.

The cornerstone of the act's consumer protection framework is a strict anti-commingling mandate. Digital commodity exchanges and brokers must hold all customer funds in segregated accounts, entirely separate from the company's own operational capital 3737. If a registered platform suffers insolvency, customer assets cannot be utilized to satisfy the demands of the exchange's corporate creditors. To reinforce this, Title VII of the CLARITY Act explicitly amends federal bankruptcy laws, legally defining both digital commodities and ancillary assets as protected customer property in the event of a Chapter 7 liquidation proceeding 9.

Transparency and market integrity are also heavily prioritized. Tokens listed on regulated exchanges will be subject to mandatory plain-language disclosures. Retail buyers will have access to standardized information detailing the token's technological risks, the economic models driving its value, and the identities of the founding team 79. The legislation also requires intermediaries to implement robust cybersecurity programs and provide the public with educational materials on how to detect fraud and safely self-custody digital assets 9.

From a tax compliance perspective, the CLARITY Act significantly tightens the reporting perimeter. The legislation expands the Bank Secrecy Act's definition of a financial institution to include digital commodity brokers and dealers 9. This alignment with traditional finance means that cryptocurrency platforms will be legally obligated to issue Form 1099-DA to their users. Consequently, retail investors will see their digital asset transactions automatically reported to the Internal Revenue Service in a manner functionally identical to traditional stock market trades executed through a conventional brokerage 2.

The Illicit Finance Debate and National Security

Despite strong bipartisan support in the House, the CLARITY Act has faced fierce resistance in the Senate regarding its approach to anti-money laundering controls and national security. Law enforcement veterans, anti-corruption advocates, and national security experts have issued stark warnings that the legislation, in its current form, contains dangerous loopholes that could be exploited by hostile state actors and transnational criminal syndicates 2829.

In May 2026, minority staff on the Senate Banking Committee released a highly critical advisory memo detailing these vulnerabilities. The memo synthesized intelligence reports indicating that drug cartels, terrorist organizations, and rogue states are increasingly relying on digital assets to finance their operations and evade global sanctions 2428. The primary critique centers on the bill's treatment of decentralized finance. Critics argue that by exempting non-custodial DeFi protocols from the strict Bank Secrecy Act requirements that govern traditional banks, the CLARITY Act effectively creates a law-free zone for money laundering 2829.

Specifically, opponents point to the legislation's failure to close the so-called Tornado Cash loophole. They argue that sophisticated cryptocurrency mixers and tumblers allow sanctioned entities to obfuscate the origin of stolen funds, and that the current bill does not impose sufficient monitoring obligations on the centralized platforms that eventually interact with these decentralized tools 2829.

Proponents of the legislation counter that the CLARITY Act is the most comprehensive digital asset law enforcement bill drafted to date. They note that the bill integrates digital assets directly into the Bank Secrecy Act, expands the sanctioning authority of the Office of Foreign Assets Control, and authorizes an additional thirty million dollars annually to fund the Financial Crimes Enforcement Network (FinCEN) 7927. The act also mandates a series of rapid studies by the Treasury and the Department of Justice to analyze the illicit use of digital asset mixers and foreign intermediaries, laying the groundwork for targeted future rulemakings 9.

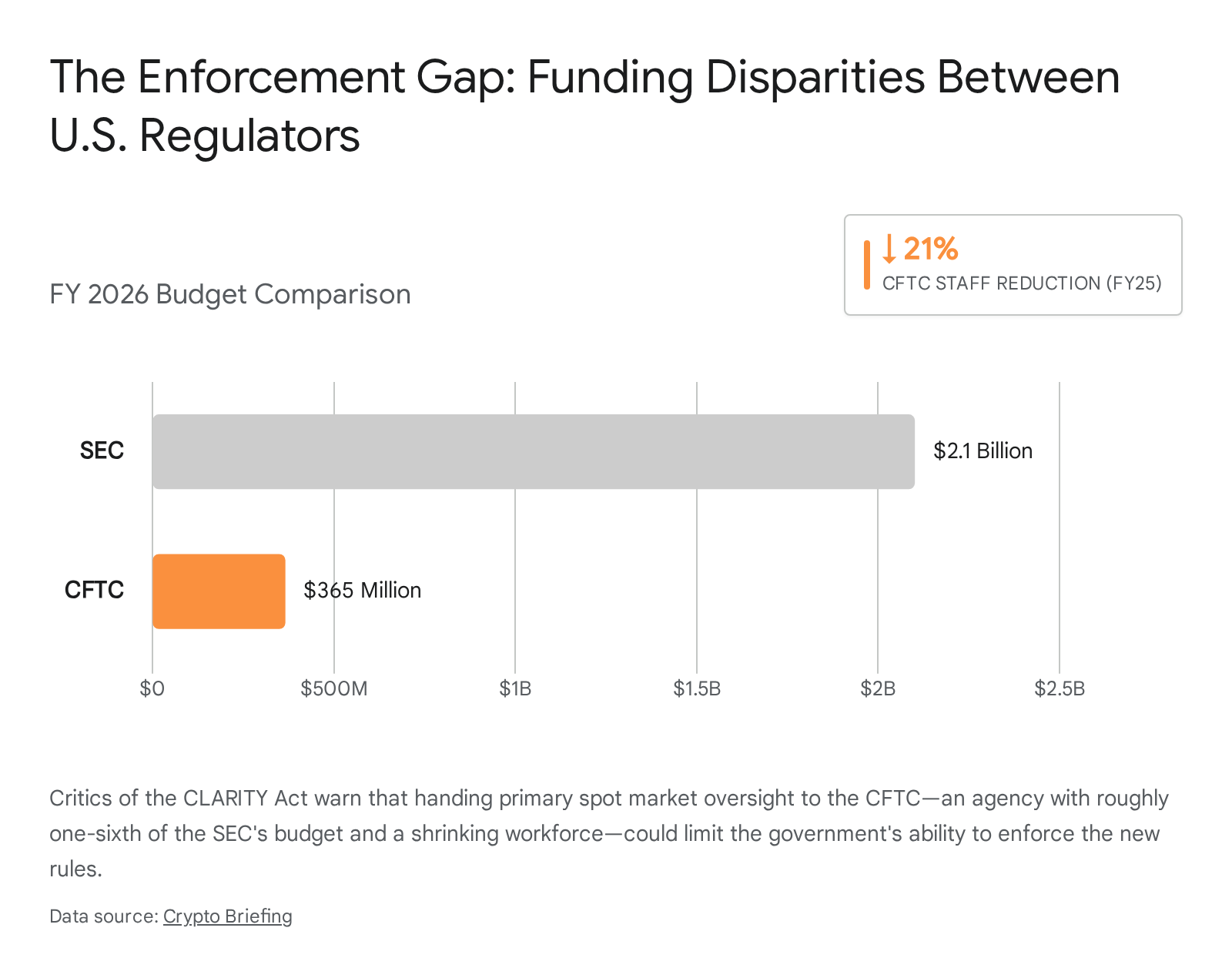

The Enforcement Gap: Resourcing the CFTC

A secondary, highly pragmatic critique of the CLARITY Act focuses on the operational capacity of the federal government to actually enforce the new regulatory framework. The legislation mandates a sweeping transfer of authority, handing the primary oversight of a multi-trillion-dollar digital commodity spot market to the Commodity Futures Trading Commission 140.

However, regulatory scholars and fiscal analysts warn that the CFTC is vastly under-resourced for this monumental task. During the 2025 fiscal year, the CFTC experienced a severe twenty-one percent reduction in its workforce, dropping from 708 to 556 full-time employees 40. Furthermore, the budgetary disparity between the nation's two primary financial regulators is vast. The CFTC currently operates on an annual budget of approximately $365 million. In stark contrast, the SEC - which would be shedding the majority of its cryptocurrency oversight responsibilities under the new framework - operates with a budget of roughly $2.1 billion 40.

Critics argue that imposing Dodd-Frank-level regulatory requirements on an agency that just lost a fifth of its staff guarantees a regime of regulation without enforcement 40. Without a massive, proportional increase in congressional funding, the CFTC may lack the technological infrastructure, specialized personnel, and litigation resources necessary to effectively police global cryptocurrency exchanges and monitor highly complex on-chain trading activities 4030.

Global Competitiveness: CLARITY vs. International Frameworks

The political urgency propelling the CLARITY Act forward in 2026 is heavily driven by intense international competition. While the United States spent years mired in domestic jurisdictional disputes, foreign regulatory bodies aggressively advanced their own comprehensive digital asset frameworks, threatening to permanently displace American leadership in global financial technology 3731.

The most prominent competitor to the U.S. framework is the European Union's Markets in Crypto-Assets (MiCA) regulation. MiCA represents a highly centralized, unified regulatory regime covering all twenty-seven EU member states 4332. Once a crypto-asset service provider secures authorization from a national regulator in a single member country, it gains the ability to seamlessly passport its operational license across the entire European bloc 32. MiCA imposes stringent requirements on the industry, including tiered minimum capital thresholds ranging from fifty thousand to one hundred and fifty thousand euros depending on the services offered, and mandates highly detailed public whitepapers prior to any token launch 3743.

However, as MiCA's final transitional periods expire in July 2026, the European market is experiencing severe operational friction. Industry analysts estimate that the sheer cost of MiCA compliance - running between five hundred thousand and two million euros annually per entity - is forcing a massive wave of consolidation 45. At least thirty smaller European exchanges have announced plans to exit the market entirely rather than bear the regulatory burden, effectively handing control of the regional industry to an oligopoly of heavily capitalized incumbents 45. Technology experts have also heavily criticized MiCA's structural design, warning that by locking highly dynamic decentralized technologies into static, rigid legal definitions, the EU risks stifling peer-to-peer innovation and rapidly rendering its own laws obsolete 4633.

By contrast, the proposed U.S. CLARITY Act relies on a perimeter-based regulatory philosophy. Rather than forcing all crypto assets into a single regulatory monolith, the U.S. framework maintains the traditional split between commodities and securities, but finally draws a bright, statutory line between them 4348. While this dual-agency approach creates a more complex compliance environment for firms offering multiple services, analysts argue that the CLARITY Act's flexibility - particularly its dynamic mature blockchain test and specific safe harbors for non-custodial developers - will ultimately prove far more conducive to early-stage technological experimentation than the rigid European model 4333.

Beyond Europe, jurisdictions across Asia and the Middle East have already implemented live, highly efficient frameworks. The Monetary Authority of Singapore oversees both spot and derivative crypto markets under a single, unified regulator, applying a strict but clear licensing regime with high minimum capital requirements 37. Similarly, the Virtual Assets Regulatory Authority in Dubai and the Securities and Futures Commission in Hong Kong have established robust, active enforcement and licensing environments that mandate strict asset segregation and deep operational transparency 37. For the United States, the CLARITY Act represents a critical, albeit delayed, effort to catch up to these established global baseline standards 37.

Comparing Global Crypto Regulatory Frameworks (2026)

| Jurisdiction | Core Regulatory Philosophy | Agency Oversight Structure | Approach to DeFi & Innovation |

|---|---|---|---|

| United States (Pending CLARITY Act) | Perimeter-based; divides assets by economic reality (security vs. commodity). | Dual-agency: SEC oversees securities, CFTC oversees spot commodities. | Highly flexible; specific safe harbors exist for non-custodial software developers. |

| European Union (MiCA) | Centralized, disclosure-heavy framework with high compliance barriers. | Single-market passporting via national regulators, coordinated by ESMA. | Rigid statutory categories; heavily criticized for stifling decentralized innovation. |

| Singapore (MAS) | Unified, strict risk-management and consumer protection focus. | Unified oversight: MAS regulates both spot and derivative crypto markets. | Highly selective licensing; prioritizes institutional stability over rapid retail expansion. |

| UAE / Dubai (VARA) | Specialized, crypto-native regulatory hub designed to attract global firms. | Dedicated agency (VARA) governs virtual assets with reciprocal national licensing. | Highly accommodating, offering tailored rulebooks for specific digital asset activities. |

The Political Reality: Will the Bill Pass in 2026?

Despite advancing through the House and clearing the Senate Banking Committee, the CLARITY Act faces a precarious and rapidly closing legislative window in 2026. The realities of the American political calendar dictate that complex, highly negotiated bipartisan legislation rarely advances late in a midterm election year, as congressional attention inevitably shifts toward local campaigning and away from structural financial reform 34.

Staff from the Senate Banking Committee and the Senate Agriculture Committee are currently engaged in intense negotiations to merge their respective legislative drafts into a single, unified bill suitable for a full Senate floor vote 226. Legislative analysts and predictive markets view the end of May 2026 as a critical inflection point; if the merged bill is not scheduled for floor consideration before the summer recess, it is highly likely to be shelved 34. Should the bill fail to pass before the November midterms, the industry risks facing a newly configured Congress in 2027 that may possess a vastly different posture toward digital asset regulation 5.

Furthermore, the legislation remains entangled in a high-profile debate over political ethics and conflicts of interest. President Trump, who has positioned himself as a vocal champion of the CLARITY Act and the broader cryptocurrency industry, currently holds a massive family portfolio in digital assets, reportedly valued in the billions 3035. Senate Democrats have utilized this dynamic to demand stringent conflict-of-interest amendments that would explicitly prevent elected officials and their immediate families from profiting off the very industries they are attempting to regulate 35. The inclusion or rejection of these ethical guardrails represents a massive partisan friction point, threatening the fragile coalition required to secure the sixty votes necessary to overcome a Senate filibuster 935.

Despite these formidable legislative hurdles, the financial markets are already reacting to the rising probability of the bill's passage. Because institutional capital and global exchanges price in regulatory trajectory rather than waiting for absolute legal certainty, the CLARITY Act is actively reshaping industry behavior in real time. Compliance departments are restructuring product offerings to align with the proposed SEC and CFTC divide, altcoin developers are auditing their networks to prepare for the mature blockchain test, and banking institutions are quietly laying the groundwork to integrate digital commodities into traditional financial services 412. Whether the bill is signed into law in the summer of 2026 or delayed by political gridlock, the framework established by the CLARITY Act has definitively set the parameters for the future of American digital finance.

Bottom line

The CLARITY Act represents a monumental shift in U.S. financial policy, aiming to replace a decade of regulatory ambiguity and enforcement lawsuits with a clear, statutory rulebook for digital assets. By granting the CFTC jurisdiction over decentralized commodities, establishing capital-raising safe harbors under the SEC, and mandating strict consumer protections, the legislation is designed to repatriate the offshore crypto industry and unlock institutional capital. However, the bill's ultimate success in 2026 remains highly uncertain, dependent on overcoming deep partisan divides over illicit finance loopholes, CFTC funding deficits, and election-year political friction.