4 Scenarios for the Future of US-China Rivalry

Experts generally forecast the future of US-China relations through four primary scenarios: a persistent state of "Drift" defined by continuous friction, the fragmentation of the globe into two competing "Blocs," a multipolar "Networks" model of managed coexistence, or a catastrophic escalation into outright "War." The ultimate trajectory will depend on how the two superpowers navigate deeply intertwined supply chains, an accelerating technology race, and the shifting allegiances of middle powers.

The Evolution of Great Power Competition

As the global order progresses through the late 2020s, the relationship between the United States and China remains the most consequential geopolitical dynamic of the century 11. The era of unbridled economic engagement - rooted in the post-Cold War belief that integrating China into the global market would inevitably liberalize its political system - has definitively ended 2. In its place, a complex framework of strategic competition has emerged.

Despite periods of tactical stabilization, such as the one-year trade truce negotiated between US President Donald Trump and Chinese President Xi Jinping in Busan in late 2025 345, the structural realities of the rivalry remain deeply entrenched. Washington views Beijing as a systemic challenger aiming to reshape the international order, while Beijing perceives US actions as a coordinated campaign to encircle China and stifle its rightful economic and technological ascent 689.

This persistent suspicion has forced policymakers, multinational corporations, and allied nations to rigorously map out the future. Extensive scenario planning by global intelligence and research organizations - including PAX sapiens, the Carnegie Endowment for International Peace, and the Center for Strategic and International Studies (CSIS) - has crystallized the future of this bilateral relationship into four highly plausible scenarios 6711.

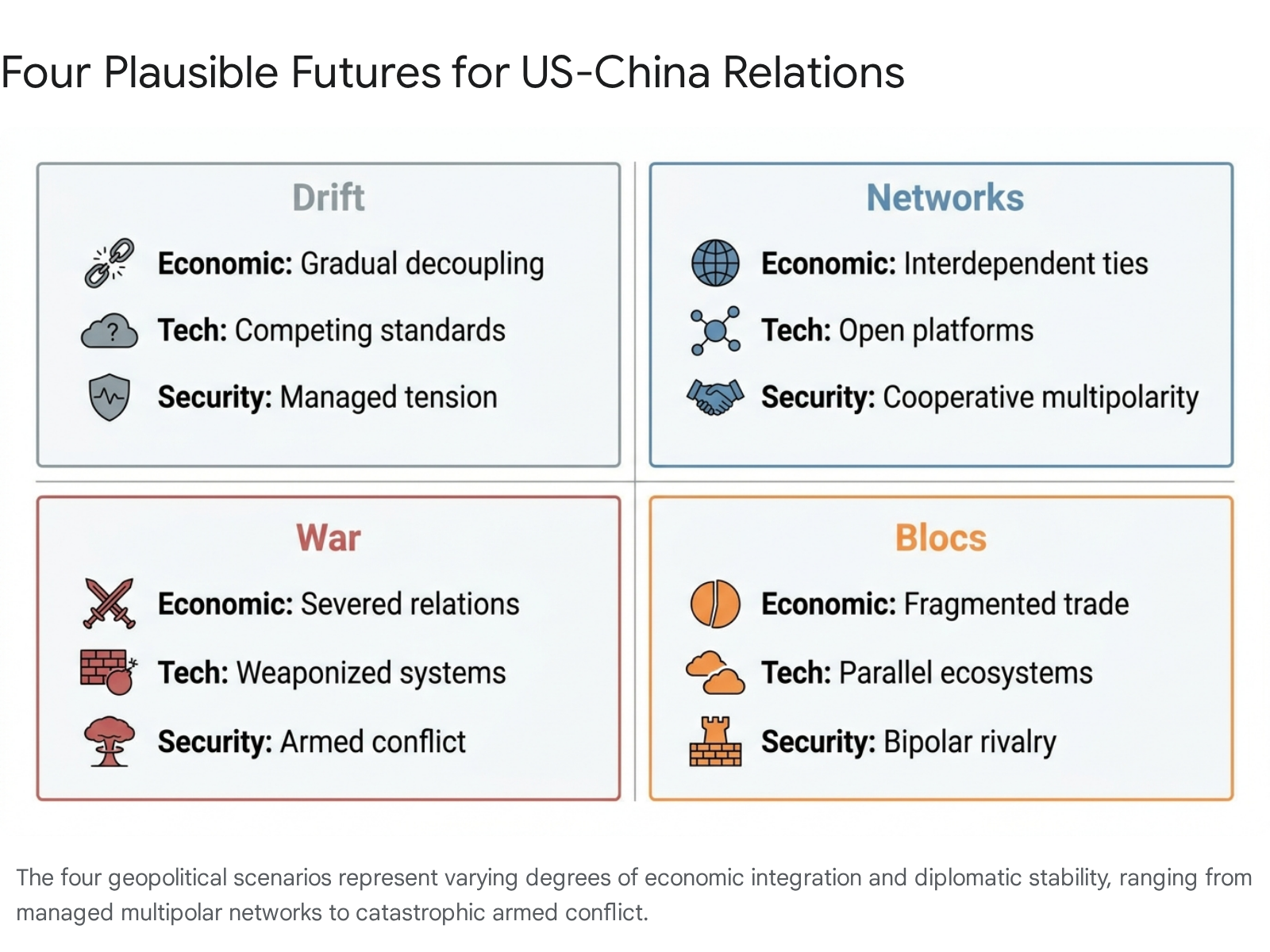

What Are the 4 Scenarios for the Coming Decade?

To understand where global trade and security are heading, analysts evaluate the future across multiple dimensions: the core bilateral relationship, macroeconomic health, political security, and technological integration. The following matrix summarizes how these four dimensions manifest across the primary scenarios forecasted for the 2030s 611.

| Scenario Focus | 1. Strategic Drift | 2. Competing Blocs | 3. Networks / Coexistence | 4. Kinetic Conflict (War) |

|---|---|---|---|---|

| Primary Relationship | Continuous tension & crisis management. | Strategic disengagement; separate spheres. | Uneasy but stable multipolar coexistence. | Open hostility; diplomatic breakdown. |

| Economic Impact | Impeded growth, high volatility, tariff wars. | Asymmetric slow growth, duplicated supply chains. | Predictable growth, managed interdependence. | Total economic devastation, global recession. |

| Technology Sector | Disordered decoupling, sudden export bans. | Two separate, incompatible tech ecosystems. | Selective decoupling restricted to dual-use tech. | Full militarization of technological development. |

| Security Posture | Persistent distrust, close-call military encounters. | Two heavily armed, opposing global coalitions. | Defense-dominance, potential arms control treaties. | Direct armed conflict in the Indo-Pacific. |

Scenario 1: Strategic Drift and Continuous Friction

The first and most immediately visible scenario is "Drift." In this future, the US-China relationship stumbles from crisis to crisis, managed primarily through reactive, on-the-brink diplomacy rather than proactive strategy 11.

Under the Drift scenario, continuous tension becomes the baseline. Both nations remain fiercely focused on economic growth and military security, but their interactions are defined by deep, persistent distrust 11. The global economy suffers from impeded growth and elevated volatility as tariffs are weaponized as instruments of long-term industrial policy rather than short-term bargaining chips 612.

Technological development in this scenario is characterized by "disordered decoupling." Supply chains are upended haphazardly by sweeping executive orders and retaliatory export controls 11. For instance, if the US blocks the sale of critical software or advanced processors, China retaliates by tightening export controls on the rare earth minerals - such as gallium, germanium, and antimony - that are vital to Western defense and electronics manufacturing 13148.

Diplomatically, the Drift scenario sees institutions like the World Trade Organization (WTO) increasingly sidelined or paralyzed 6. Flashpoints in the South China Sea and the Taiwan Strait remain highly active, with naval and air assets operating dangerously close to one another. The risk of an accidental collision spiraling into a broader diplomatic crisis remains exceptionally high, forcing both nations to dedicate immense resources to crisis management rather than collaborative global governance 11.

Scenario 2: The Formation of Competing Blocs

If the friction of the Drift scenario proves unsustainable, the global order may harden into "Blocs." This scenario envisions a return to a Cold War-style bipolarity, where the world is split into two distinct, competing geopolitical spheres of influence 611.

In a Blocs scenario, the United States and China act to oppose each other comprehensively across military, economic, and diplomatic domains 11. Strategic disengagement becomes the norm. The technological ecosystem bifurcates entirely, forcing countries to choose between an American-led internet and digital infrastructure or a Chinese-led alternative.

This bifurcation results in asymmetric, slow global economic growth. Multinational corporations are forced to duplicate supply chains - one serving the West and the other serving China and its allies - at an astronomical cost to efficiency and profitability 816. Developing nations in Latin America, Africa, and Southeast Asia are increasingly pressured to align with a single bloc, receiving infrastructure investment and security guarantees in exchange for geopolitical loyalty 6.

While a bipolar world might theoretically imply a "G2" condominium where Washington and Beijing jointly manage global affairs, security analysts widely dismiss this outcome. Surveys of international relations experts indicate that over 70% are deeply skeptical of a functional G2 framework, viewing it as unworkable given the fundamental ideological incompatibilities and zero-sum security mentalities driving both capitals 910. The Genron NPO global expert survey shows that only 1.4% of experts believe a G2 framework is currently functioning 10. Instead of joint management, the Blocs scenario yields deeply fragmented supply chains and unclear, competing global rules.

Scenario 3: Networks and Realistic Coexistence

The most optimistic - yet highly complex - future is the "Networks" or "Competitive Coexistence" scenario. This pathway assumes that both Washington and Beijing recognize the catastrophic costs of outright war and complete economic decoupling, ultimately settling into a tense but manageable equilibrium 211.

A landmark report by the Carnegie Endowment for International Peace envisions this "calmer waters" scenario materializing by the mid-2030s 1112. By that time, this scenario projects that China and the United States will achieve rough economic parity, diminishing Washington's anxieties about being eclipsed and cooling Beijing's ambitions for absolute global dominance 11. Both nations accept that some technological limitations are natural, and the drive for decoupling hits a ceiling, leaving core economic interdependence intact.

In this multipolar world, selective decoupling occurs only in the most highly sensitive military and dual-use technologies 11. Meanwhile, robust trade continues in consumer goods, agriculture, and non-critical manufacturing. Because their economies remain intertwined, this mutual vulnerability acts as a powerful deterrent against provocative military actions, such as a blockade of Taiwan 511.

A defining feature of the Networks scenario is the ability of the two superpowers to carve out "islands of consensus." Despite fierce geopolitical rivalry, Washington and Beijing find mechanisms to cooperate on existential global challenges. This includes establishing norms for the deployment of artificial intelligence, engaging in nuclear arms control as China's arsenal expands, and cooperating on global health and climate change 511. The relationship is stabilized by complex networks, international intermediaries, and a pragmatic acceptance of ideological differences.

Scenario 4: Escalation to Kinetic Conflict (War)

The final and most devastating scenario is "War." This future posits that the escalating tensions of the 2020s breach diplomatic guardrails, resulting in direct kinetic armed conflict between the world's two preeminent military powers 611.

The triggers for this scenario are well-documented: an accidental military collision in the South China Sea, a miscalculation over disputed territories (such as the Senkaku Islands), or, most critically, a crisis over Taiwan 813. If Washington significantly deepens its political and military commitment to Taipei, or if Beijing concludes that peaceful unification is permanently foreclosed and launches an amphibious assault or blockade, open conflict becomes nearly inevitable 1114.

The consequences of the War scenario extend far beyond the immediate theater of combat. Even if confined geographically to the Western Pacific, the conflict would result in profound global economic devastation. Major industrial hubs along China's southeastern coast and Taiwan's advanced semiconductor foundries could be destroyed 8. Global supply chains would instantly paralyze, the World Trade Organization would likely collapse, and global GDP growth would suffer a massive, sustained contraction 68. Furthermore, the conflict would spark an intense militarization of all technological development, fundamentally altering the trajectory of human innovation for decades 11.

What Is the Difference Between De-risking and Decoupling?

To navigate the likelihood of these scenarios, it is critical to parse the language driving modern geoeconomics. In recent years, the concept of "decoupling" - a complete severing of trade, investment, and technological ties between two economies - has dominated political rhetoric. However, recognizing the catastrophic economic fallout of a total bilateral divorce, Western policymakers pivoted to a more nuanced framework: "de-risking" 1516.

First popularized by European Commission President Ursula von der Leyen in early 2023, de-risking implies a targeted reduction of vulnerabilities without turning entirely inward 1617. The US administration swiftly adopted this terminology to placate anxious European allies and a domestic business community fearful of losing access to the Chinese market 161518.

The Three Layers of Supply Chains

The functional difference between decoupling and de-risking is best understood through the analogy of the global supply chain, which has effectively fractured into three distinct layers :

- Strategic Goods (The "Small Yard, High Fence"): This accounts for roughly 20% of US-China trade and includes foundational 21st-century technologies such as advanced semiconductors, quantum computing, and biotechnology 9. In this layer, the strategy is explicitly one of decoupling. Washington actively seeks to sever China's access to these technologies through strict export controls to maintain a military and technological edge.

- Dual-Use Technologies (The Gray Zone): This massive segment involves commercial goods that have potential military applications. It presents a constant de-risking dilemma for multinational corporations, as items can swiftly transition from "business-as-usual" to prohibited status based on sudden geopolitical shifts .

- Consumer and Commodity Goods (The Catch-All): This layer encompasses non-sensitive items such as apparel, toys, and basic agricultural products. Absent a total breakdown in relations, robust trade in this sector is expected to continue indefinitely, anchoring the remaining economic interdependence .

While Western officials insist that de-risking is a purely defensive measure to protect supply chain resilience, Chinese state media and policymakers view the distinction as merely semantic. To Beijing, de-risking is simply "decoupling in disguise" - a targeted strategy designed to permanently constrain China's development and force it into the lower tiers of global value chains 15192021.

The Technological and Economic Battlegrounds

The friction over decoupling versus de-risking is currently playing out across three critical economic battlegrounds. The outcomes in these sectors will dictate whether the world leans toward the "Blocs" or the "Networks" scenario.

The Semiconductor Chokehold

The most intense front in the US-China rivalry remains the semiconductor supply chain. Advanced chips are the lifeblood of both modern economies and advanced military systems. The ongoing "Chip War" highlights the practical difficulties of the decoupling strategy 3122.

For example, US efforts to restrict China's access to top-tier artificial intelligence processors and extreme ultraviolet (EUV) lithography machines have severely disrupted global markets. When the US government placed strict export controls on advanced chips, companies like Nvidia were forced to engineer purpose-built, lower-performance chips (like the H20) to maintain access to the lucrative Chinese market 831. Subsequent policy reversals and the imposition of heavy tariffs on chips passing through the US have created profound uncertainty 31.

This dynamic places allied nations in an impossible position. In Europe, the Netherlands was heavily pressured by Washington to restrict the export of ASML's irreplaceable lithography machines to China, cutting off billions in revenue for a domestic company that had historically thrived on global free trade 33. Similarly, South Korean memory chip giants Samsung and SK Hynix, which have invested billions in manufacturing facilities inside China, require constant diplomatic maneuvering just to secure the equipment needed to keep their foundries operational 33.

While US restrictions aim to stall China's AI development, they simultaneously incentivize Beijing to accelerate its drive for total technological self-sufficiency. Bolstered by massive state subsidies (the "Big Fund"), Chinese domestic chipmakers like ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC) are rapidly expanding their market share, fundamentally restructuring the $600 billion global semiconductor industry 83334. Furthermore, major technological leaps, such as Huawei's development of a 7nm chip despite sanctions, suggest that broad export bans may be spurring domestic Chinese innovation rather than suppressing it 8.

The Weaponization of Critical Minerals

If the United States holds the advantage in semiconductor design, China holds the trump card in critical raw materials. China currently dominates the global supply chain for rare earth elements, controlling roughly 69% of global mining production, 92% of processing, and 93% of rare earth magnet manufacturing 3.

As the US weaponizes export controls on technology, Beijing has demonstrated a willingness to respond in kind. Restrictions on the export of gallium and germanium - vital elements for chip manufacturing and green energy infrastructure - serve as stark reminders of Western vulnerability 8. Analysts project that China will maintain effective dominance over rare earths for years to come, providing Beijing with a potent lever to counter Western economic coercion and complicating any rapid transition toward a "Blocs" or entirely decoupled scenario 3.

The Illusion of Total Supply Chain Separation

Despite political rhetoric urging reshoring and decoupling, empirical economic data reveals a more nuanced reality. Washington's push for "friendshoring" and the "China+1" strategy has prompted multinationals to diversify production to countries like Vietnam, Mexico, and India to reduce exposure to tariffs 2324.

Consequently, World Bank and IMF data show that China's share of direct US imports fell from 22% in 2017 to 16% in 2022, directly correlated to US tariffs 2425. However, supply chains remain deeply intertwined. The countries replacing China as direct exporters to the US are themselves heavily integrated into Chinese supply chains 24. To displace China on the final export side, these developing nations are importing massive quantities of Chinese intermediate goods 2324. Put simply, globalization is not unwinding; it is merely being rerouted through third parties, making a clean "Blocs" scenario highly improbable in the near term 24.

How Middle Powers Are Navigating the Crossfire

The US-China rivalry does not exist in a vacuum. The behavior of middle powers, regional alliances, and the Global South will heavily influence the geopolitical trajectory of the next decade.

Southeast Asia's Shifting Allegiances

The Association of Southeast Asian Nations (ASEAN) finds itself squarely on the geopolitical fault line. Historically, ASEAN states have fiercely resisted pressure to choose sides, pursuing a strategy of delicate hedging to extract economic benefits from China while relying on the US as an offshore security guarantor 26.

However, recent data suggests this balance is shifting. A comprehensive 2026 survey of regional elites by the Singapore-based ISEAS-Yusof Ishak Institute revealed that if forced into a hypothetical choice between the two superpowers, a narrow majority of Southeast Asians (52%) would now align with China over the United States (48%) 2728.

This shift is not uniform; it reveals distinct sub-regional camps. Support for China is overwhelmingly strong in Muslim-majority nations like Indonesia (80.1%) and Malaysia (68%), driven in part by domestic backlash against US foreign policy in the Middle East, specifically regarding the war in Gaza 29. Furthermore, traditional US allies like Thailand have drastically shifted their economic alignment toward Beijing 29. Conversely, nations with active maritime disputes with Beijing in the South China Sea, such as the Philippines and Vietnam, overwhelmingly retain their preference for Washington 2829.

The survey underscores a broader regional fatigue. Southeast Asia feels increasingly uneasy about China's entrenched economic influence, yet simultaneously alienated by the transactional, "America First" foreign policies emanating from Washington 263031.

Japan's Quest for Autonomy

For Japan, the intensification of US-China rivalry presents an existential strategic challenge. As a frontline state allied with the US but economically deeply intertwined with China, Tokyo faces the dual threat of outright military conflict over Taiwan or a slow, geoeconomic squeeze through sub-threshold coercion 44.

Japanese strategic forecasters explicitly warn of the dangers of a "G2" scenario - a situation where an inward-looking US administration withdraws from Asian affairs in exchange for Chinese concessions elsewhere, effectively abandoning Japan to Chinese regional hegemony 4445. To prevent this, Japan is pursuing a strategy of "strategic autonomy and indispensability" 46. This involves radically increasing domestic defense spending (potentially up to 3.5% of GDP) while simultaneously building overlapping security and industrial networks with other middle powers like Australia, South Korea, and the Philippines to dilute its absolute reliance on Washington 444546.

India's Strategy of Multi-Alignment

India's approach to the rivalry is defined by what analysts term "the triangle of apprehension" 32. New Delhi views both Washington and Beijing with deep-seated suspicion. While China's pursuit of regional hegemony directly threatens India's border security and strategic interests in the Indian Ocean, the US's transactional diplomacy and willingness to weaponize tariffs frequently alienate Indian policymakers 32.

Consequently, India is actively resisting absorption into any rigid bloc. Instead, it is pursuing a policy of "multi-alignment" - leveraging its massive market scale to extract technological and military concessions from the West (the "China-plus-one" logic) while maintaining strategic autonomy 32. By expanding partnerships with other likeminded states and refusing to play a subordinate role to either superpower, India serves as a critical counterbalance that makes a strict bipolar "Blocs" scenario less likely 3248.

Europe's De-Risking Dilemma

The European Union finds itself in an increasingly precarious position. Caught between Washington's aggressive push for technology containment and Beijing's economic leverage, Europe is struggling to implement its stated "de-risking" strategy 49.

Forecasts indicate a pervasive pessimism within Europe regarding its ability to reduce economic dependencies on China or effectively combat Chinese manufacturing overcapacity. A survey by the Mercator Institute for China Studies (MERICS) found that 84% of European China experts were pessimistic about Europe's ability to reduce dependencies 33. Furthermore, analysts warn that Europe risks being structurally sidelined. If the US and China escalate tensions, Europe suffers the economic fallout; if Washington and Beijing broker bilateral truces, decisions affecting global trade are often made over the heads of European policymakers 34.

Beyond Hard Power: The Tourism Shift

The rivalry between the US and China is not limited to defense and high technology; it extends deeply into the realms of soft power and the broader global economy. The travel and tourism sector serves as a striking proxy for this shift.

Historically, the United States has been the undisputed global leader in tourism, a massive engine for cultural influence and economic growth. However, stringent immigration policies, geopolitical frictions, and a less welcoming international perception have led to a marked stagnation in US inbound travel 5235. In recent years, the US recorded a mere 0.9% growth in its tourism economy, coupled with a 5.5% drop in foreign arrivals 3554.

Meanwhile, China's travel and tourism economy has surged, expanding at a rate of 9.9% - more than double the global average 3554. The World Travel & Tourism Council (WTTC) projects that if current trends hold, China will surpass the United States as the world's top travel-driven economy within three to four years 3554. This shift is highly consequential. Dominance in global travel translates directly into enhanced commerce, skilled migration, stronger international partnerships, and an expansion of soft-power influence - metrics that are vital in a prolonged era of strategic competition 5254.

Bottom line

The US-China relationship has transitioned irreversibly into an era of structural, multi-domain competition. The four most plausible scenarios for the next decade range from a fragile, crisis-prone "Drift" to the catastrophic global fallout of an armed "War." While the extreme fragmentation of the global economy into competing "Blocs" remains a distinct risk driven by technology embargoes and supply chain weaponization, the sheer scale of economic interdependence makes complete decoupling practically impossible. Consequently, the most sustainable, albeit difficult, path forward is a "Networks" model of competitive coexistence, where both powers manage deep distrust while finding narrow avenues for cooperation on shared existential threats.