Why New Power Waits Years to Connect to the Grid

The grid interconnection queue is the mandatory, multi-phased engineering and regulatory study process that proposed power generation and storage facilities must complete to safely attach to the high-voltage transmission system. In the simplest terms, it is the waiting line for the electric grid. Currently, this process is fundamentally broken, serving as the single largest structural barrier to the global clean energy transition. Across the United States, Europe, and the United Kingdom, antiquated administrative frameworks have collided with an unprecedented surge in renewable energy development, resulting in massive backlogs. In the United States alone, over $2,300\text{ GW}$ of proposed generation and storage capacity is actively waiting for grid access - an amount that exceeds the entire existing electrical capacity of the nation 12. To alleviate this paralysis, federal regulators and regional grid operators are implementing sweeping structural reforms, transitioning away from antiquated "first-come, first-served" serial study models to "first-ready, first-served" cluster study frameworks designed to prioritize mature projects and penalize speculative development.

The Everyday Hook: Bills, Blackout Risks, and the Clean Energy Paradox

While the grid interconnection queue operates as an arcane regulatory mechanism, its failures directly and profoundly impact everyday citizens through escalated utility bills, heightened blackout risks, and a delayed transition to clean energy.

When new, highly efficient, and low-cost renewable energy projects are trapped in bureaucratic purgatory, grid operators are forced to rely on older, more expensive, and less efficient fossil-fuel power plants to meet surging electricity demand 33. This demand is currently accelerating at a historic pace due to the broader electrification of heating and transport, alongside the explosive growth of artificial intelligence and hyperscale data centers 54. The United States Department of Energy (DOE) and the International Energy Agency (IEA) project that energy usage from data centers alone will double or triple by 2028, commanding an increasing share of the nation's power load 4.

Because the transmission system lacks the capacity to integrate new generation to meet this demand, consumers are bearing the financial brunt. The financial penalty of grid interconnection delays is quantifiable and staggering. Research indicates that for every $\$1\text{ billion}$ in well-planned, large-scale transmission investment that is delayed, consumers lose between $\$150\text{ million}$ and $\$370\text{ million}$ annually in net benefits 358. These losses manifest through postponed reliability improvements, foregone economic efficiencies, and reduced access to lower-cost generation 5. A stark example materialized recently in the PJM Interconnection market - the largest grid operator in the United States, serving 13 states and the District of Columbia. In PJM, the failure to connect new, cheaper generation resources cost consumers an estimated $\$7\text{ billion}$ in a single capacity auction. Capacity prices spiked violently because the supply margin shrank, driven by power plant retirements, increased load, and severe delays in bringing new renewable energy projects online 36.

Furthermore, interconnection bottlenecks directly endanger grid stability and increase blackout risks. The United States has a transmission capital stock that is aging out, with over $70\%$ of infrastructure past the midpoint of its 50-year life expectancy 3. Delaying interconnection prevents modern, grid-enhancing technologies - like advanced inverter-based resources (IBRs) and high-capacity battery storage systems - from deploying. These new assets are essential for balancing the grid and providing critical ancillary services during extreme weather events induced by climate change, such as severe heat waves and polar vortexes 310.

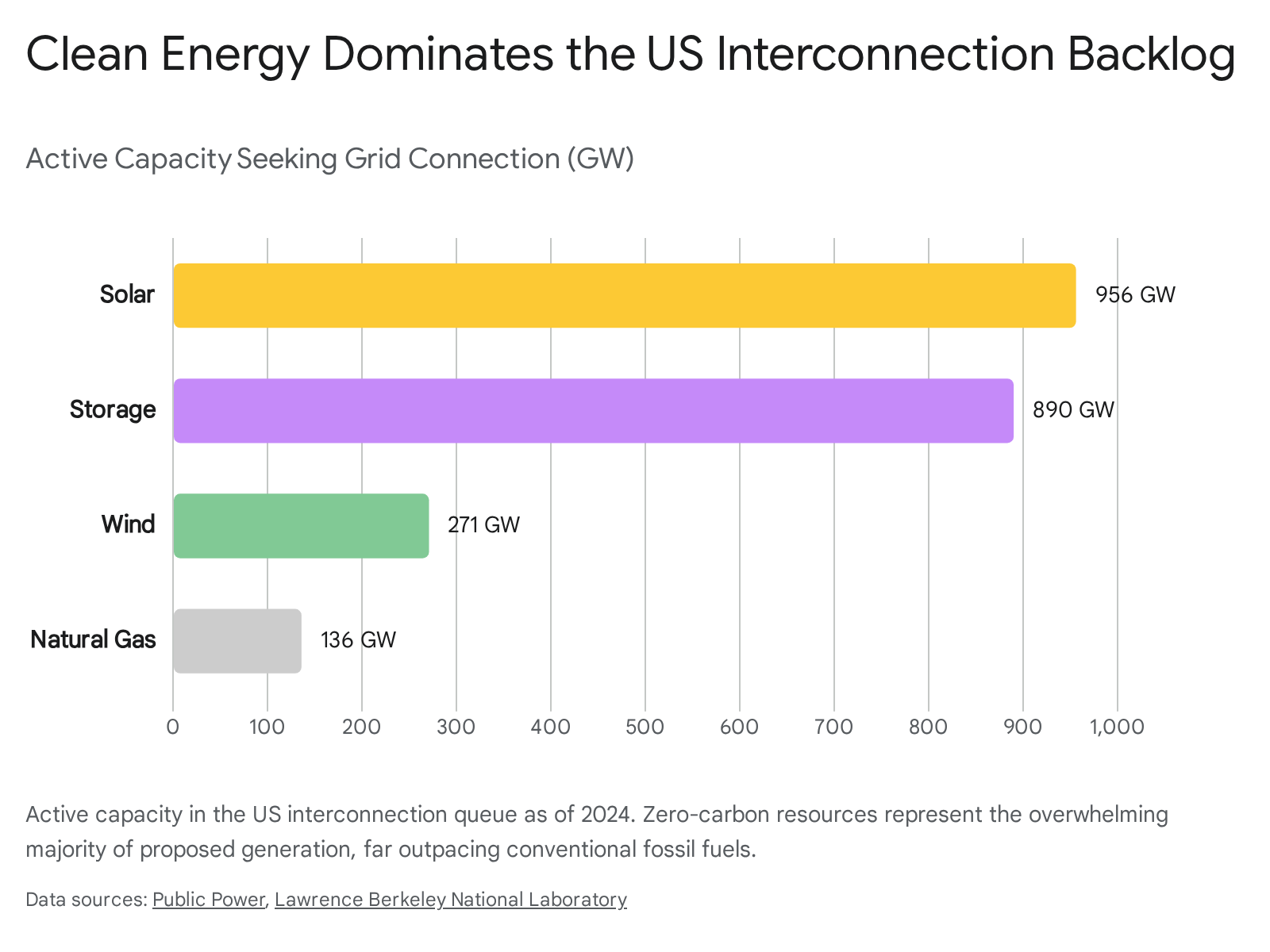

Correcting the Misconception: The United States' Funded Backlog

A pervasive misconception dominates public and political discourse surrounding the clean energy transition: the idea that the United States is simply not building enough renewable energy infrastructure to replace retiring fossil fuel plants. The empirical data firmly invalidates this notion. The primary challenge is not a lack of development appetite, technological capability, or capital funding; rather, it is a profound lack of physical transmission capacity and administrative grid access 311.

According to the Lawrence Berkeley National Laboratory's (LBNL) highly regarded Queued Up 2024 report, the total generation and storage capacity seeking grid interconnection exceeds $2,600\text{ GW}$ (with active capacity sitting around $2,300\text{ GW}$ by year's end) 17. To contextualize this figure, the combined solar and wind capacity currently in the queues equals the installed capacity of the entire existing U.S. power plant fleet 2.

Zero-carbon resources - specifically solar, wind, and battery storage - comprise the overwhelming majority of this queued capacity. By the end of 2024, there were approximately $10,300$ active projects in the U.S. interconnection queues. Solar energy projects led the queue with a staggering $956\text{ GW}$ of active capacity, followed closely by battery storage at $890\text{ GW}$, and wind at $271\text{ GW}$ 18. In stark contrast, proposed fossil fuel generation is a fraction of the pipeline, with active natural gas capacity sitting at just $136\text{ GW}$ 18.

The passage of the Inflation Reduction Act (IRA) of 2022 supercharged this market, incentivizing the entry of over $1,200\text{ GW}$ of capacity into the queues in response to massive tax credits and economic incentives for clean energy 24.

The reality is that the renewable energy pipeline is overflowing. The bottleneck is strictly logistical and infrastructural. As the LBNL report concludes, while developer interest is unprecedented, the growing backlog represents a significant structural and regulatory constraint for plants seeking grid connection 9.

Mapping the Grid Interconnection Queue

Before construction can commence, every energy developer must prove that their proposed facility will not destabilize the existing electrical grid. This involves a rigorous, multi-phased engineering evaluation. Though exact terminology and specific state-level nuances vary across Regional Transmission Organizations (RTOs) and Independent System Operators (ISOs) like NYISO, CAISO, and ERCOT, the queue fundamentally follows a standardized progression of increasingly complex studies.

| Phase | Description and Purpose | Typical Outcome & Deliverables |

|---|---|---|

| Interconnection Request (IR) & Screening | The developer submits a formal application, technical specifications, and an initial monetary deposit to the grid operator. In many modern systems, proof of "site control" (land rights) is now required here 10. | The project officially enters the queue, receives a timestamp, and is grouped for evaluation. |

| Feasibility Study (Often Optional) | A preliminary, high-level analysis determining whether plugging the project into the grid would cause obvious localized electrical problems or severe congestion 1011. | Provides a non-binding, preliminary cost estimate for potential grid system upgrades 12. |

| System Impact Study (SIS) | A detailed, mathematically intensive simulation testing the project's impact on the broader network. Grid engineers create power flow models for the initial year of operation, applying adverse conditions to stress transmission facilities (e.g., peak load, N-1 contingencies, transient stability studies) 10111314. | Identifies specific, required transmission system upgrades to maintain reliability and assigns estimated costs to the developer. |

| Facilities Study | An exhaustive engineering, architectural, and design evaluation detailing the exact physical equipment, construction milestones, and labor required to connect the project (e.g., substation expansions, new breakers, telemetry points) 1014. | Yields highly detailed, binding cost allocations and timelines that the developer must formally accept to proceed 1112. |

| Interconnection Agreement (IA) | A legally binding, multi-party contract signed by the developer, the transmission owner, and the grid operator, outlining the final construction plan, operating restrictions, and financial responsibilities 1012. | The project is authorized to begin procurement and physical construction of interconnection facilities. |

| Commercial Operations Date (COD) | Following construction, the facility undergoes synchronization testing, telemetry validation, and commissioning. Once all safety protocols are cleared, the plant is integrated 14. | The project officially begins injecting power into the market and earning commercial revenue. |

While this structured, step-by-step approach historically guaranteed grid safety and open access, the sheer volume of modern applications has completely overwhelmed the administrative and engineering capacities of transmission providers, breaking the intended timeline.

Why Does It Take Years to Connect to the Grid?

Over the past decade, the timeline from a project's initial Interconnection Request to its Commercial Operations Date has stretched to unprecedented lengths. For projects completed and built between 2000 and 2007, the median wait time was less than two years. By 2023, the median duration had soared to approximately five years, with some complex projects and data centers facing potential delays of up to a decade or more 137.

The core issue stems from an outdated administrative framework - specifically, the legacy "serial" study process - colliding with a rapidly expanding market. Historically, grid operators processed interconnection requests on a strict "first-come, first-served" basis 2122. In this serial model, grid engineers would study Project A, determine the required grid upgrades, and then evaluate Project B assuming Project A's upgrades were in place. However, if Project A's developer realized the assigned upgrade costs were too high and dropped out of the queue, the underlying power flow assumptions for the entire grid changed. The grid operator was then forced to conduct an exhaustive "restudy" for Project B, Project C, and so forth 22.

This serial methodology triggered cascading bottlenecks. As the volume of applications surged under the incentives of the IRA, the restudy loops became endless. The withdrawal of a single large project could delay dozens of downstream projects by months or years 22. Modernizing this architecture required a shift from the serial process to a "cluster" study process. Under a cluster model, operators group requests geographically and study their cumulative impact simultaneously, eliminating the redundant cascading delays of the serial framework and allowing multiple projects to share the costs of a single, larger transmission upgrade 1021.

Beyond administrative friction, the physical realities of the grid contribute heavily to the delay. There is a severe shortage of high-voltage transmission lines, meaning nearly every new large-scale generation project triggers the need for substantial physical network upgrades 4. Furthermore, there is a critical shortage of specialized transmission engineers capable of running complex power flow models (such as transient stability and short-circuit analyses), leaving understaffed utility planning departments buried under an insurmountable backlog 411.

Why Do So Many Projects Cancel?

Entering the interconnection queue does not guarantee a project will be built. In fact, historical data from LBNL reveals an immense attrition rate. Only $13\%$ of the capacity that submitted interconnection requests from 2000 to 2019 had reached commercial operations by the end of 2024. A staggering $77\%$ of that capacity was formally withdrawn 18. For solar projects, the success rate is even bleaker, with only about $14\%$ of historical proposed solar capacity ever coming online 915.

Furthermore, developers are holding onto these failing projects longer than ever before. In 2024, massive volumes of withdrawn projects had been sitting in the queue for four to five years - a massive expenditure of time and capital before walking away. In California (CAISO), the median project sat in the queue for over 5.5 years before ultimately withdrawing 24. The year 2024 saw a massive spike in withdrawals, with nearly $296\text{ GW}$ of capacity removed from queues across the country 24.

Projects cancel for three primary, interrelated reasons:

- Speculative Queuing: Historically, entering the queue was relatively inexpensive and required minimal proof of commercial viability. Developers often submitted multiple applications for a single intended project across different points on the grid. They viewed the queue as an exploratory tool to find the cheapest interconnection point, fully intending to withdraw the majority of their applications once cost estimates were returned 109. This speculation clogged the system with "zombie projects" that had no realistic chance of construction, drawing away critical engineering resources 25.

- Exorbitant Grid Upgrade Costs: When studies are finally completed, developers are frequently hit with massive, unexpected bills for necessary transmission network upgrades. The data shows that interconnection costs for withdrawn projects average around $\$599/\text{kW}$, compared to just $\$240/\text{kW}$ for completed projects 26. These unpredictable, multi-million dollar capital requirements routinely destroy a project's financial model, forcing an immediate withdrawal 3.

- Community Opposition and Permitting Hurdles: Even if a project survives the engineering queue and can afford the upgrade costs, it faces the hurdle of local zoning, permitting, and community acceptance. Surveys of energy developers highlight that community opposition - often centered on land use, aesthetics, or "energy privilege" (wealthier communities resisting infrastructure) - is a leading cause of late-stage cancellations 16. These failures are catastrophic for developers; the average unrecoverable sunk costs for a canceled project are estimated at $\$2\text{ million}$ for solar and $\$7.5\text{ million}$ for wind 16.

Comparing the Markets: PJM, CAISO, ERCOT, and MISO

Different regional grid operators process interconnection queues with varying degrees of success. An analysis of major U.S. markets reveals stark differences in wait times, dropout rates, and the efficacy of recent reforms.

| Regional Grid Operator | Median Wait Time to Operation (Queue to COD) | Queue Volume & Structural Challenges | Reform Status & Performance Metrics |

|---|---|---|---|

| CAISO (California) | Over 5.5 years (highest median for withdrawn projects) 24. | The queue is packed with solar and BESS (battery) projects. Received a record-breaking $523\text{ GW}$ of new requests in recent cycles, overwhelming the operator 226. | CAISO holds a relatively good completion rate for older projects (pre-2020) but has struggled with extreme cluster delays recently. Currently implementing intra-cluster prioritization to fast-track mature projects under FERC Order 2023 1718. |

| PJM (Mid-Atlantic/Midwest) | 3 to 4 years 24. | Massive backlog due to historical reliance on the serial study process. In early evaluations, PJM scored a "D-minus" for lack of proactive regional transmission planning 1719. | Overhauled the queue in 2023 to a strict "first-ready, first-served" system. Fast-tracked over $26\text{ GW}$ of viable projects using AI tools and readiness deposits to filter out speculative entries 518. |

| ERCOT (Texas) | Less than 3 years 9. | Exploded to over 2,000 requests by 2025 due to rapid solar/battery growth. ERCOT operates uniquely as it is not subject to federal (FERC) interconnection procedures 59. | Holds the best historical completion rate ($42.6\%$). Processes applications rapidly, but its lack of proactive transmission expansion leads to severe congestion and high levels of curtailment (wasted power) once projects are built 1719. |

| MISO (Midcontinent) | 3 to 4 years 24. | Faced immense backlogs that forced the operator to completely halt new interconnection requests in 2022 to implement procedural overhauls 2. | Implemented strict queue caps, interactive tracking maps, and "express lanes" for specific cycles targeting high-priority data center loads to ensure speculative projects do not block the pipeline 5. |

Who Pays for Grid Upgrades? The "Highway" Analogy

A fundamental, systemic conflict at the heart of the interconnection crisis is the allocation of costs for necessary grid upgrades. Currently, the U.S. power system relies heavily on a "participant funding" mechanism where the interconnecting generator - the renewable energy developer - must bear almost the entire cost of increasingly expensive, large-scale transmission upgrades required to safely attach their project to the grid 2021.

To understand why this is economically problematic, consider the "Highway Analogy" 20. Regional power grids are essentially interstate highway systems, designed to move power from where it is generated to where it is needed by homes and businesses. Under the current cost allocation model, a developer trying to build a new wind or solar farm is essentially being asked to shoulder the financial burden of adding an entirely new lane to that electron highway 20. However, once built, that new lane reduces congestion and improves reliability for everyone - benefitting all drivers (consumers and other energy producers) on the system.

This dynamic creates a classic "free-rider" problem in economics 2022. When developers are saddled with the runaway costs of broad system upgrades, low-cost renewable resources are killed. Costs have spiraled out of control; what once was a $\$50/\text{kW}$ cost for new interconnections in certain regions has surged to $\$448/\text{kW}$ and is still rising 20. Economic modeling conducted by ICF Resources for the American Council on Renewable Energy (ACORE) found that the actual, system-wide benefits of these transmission upgrades are often double what is calculated in siloed RTO planning exercises 20. Furthermore, two-thirds of these upgrades, if built, would deliver significant shared grid benefits that other users would not pay for 20. Until federal regulators mandate broad, inter-regional transmission planning and allocate the costs of grid upgrades to all beneficiaries (the rate base) rather than solely the interconnecting developer, the queue will remain a financial graveyard for otherwise viable clean energy projects 2023.

Practical Takeaways: Community Solar and Grid Stability

The interconnection bottleneck is not merely an abstract problem for utility-scale corporate developers; it directly limits consumer choices, hampers local community initiatives, and compromises grid resilience.

- Community Solar Availability: Community solar models allow renters, small businesses, and individuals who cannot install rooftop panels to subscribe to a centralized local solar array and receive direct credits on their utility bills 243625. However, community solar projects - which typically connect at the distribution grid level - face the same interconnection delays and queue backlogs as massive utility-scale arrays 25. In Illinois, for example, the utility Ameren has faced intense criticism for studying its $1,700$ pending community solar applications one at a time, resulting in a multi-year backlog 24. Conversely, the neighboring utility ComEd expedites deployment by studying hundreds of proposals concurrently 24. These delays are critical because federal tax credits under the IRA require projects to begin construction by specific deadlines. If a community solar project is stuck in an interconnection queue for three years, it may lose its financing entirely, directly depriving local residents of affordable, clean energy access 243626. To combat this, developers are increasingly front-loading project planning, engaging utilities before construction even begins to align permitting and interconnection schedules 26.

- Grid Stability and Resilience: The transition to a decarbonized economy relies heavily on integrating flexible loads and robust battery energy storage systems (BESS). However, the queue backlog prevents these stabilizing assets from coming online. As aging fossil fuel plants retire and severe weather events become more frequent, the lack of new dispatchable storage and advanced inverter-based resources leaves the grid highly vulnerable to voltage collapses and rolling blackouts 310.

FERC Order 2023: The Blueprint for U.S. Queue Reform

Recognizing that the existing framework was fundamentally unjust, unreasonable, and incapable of supporting the energy transition, the Federal Energy Regulatory Commission (FERC) issued Order No. 2023 in July 2023. This ruling, along with its subsequent clarification in Order No. 2023-A in March 2024, represents the most significant set of interconnection reforms since the pro forma procedures were created two decades ago 213940.

FERC Order 2023 mandates that all FERC-jurisdictional transmission providers transition away from the serial "first-come, first-served" model and adopt a "first-ready, first-served" cluster study approach 102141. By grouping geographically linked projects and studying them simultaneously within a strict 150-day cluster study process, operators can dramatically increase efficiency and improve cost allocation by sharing the financial burden of network upgrades proportionally among the cluster members 2141.

Order 2023 introduces several stringent mechanisms to enforce accountability, deter speculation, and integrate modern technology:

- Increased Financial Commitments & Site Control: To enter a cluster study, developers must now demonstrate strict commercial readiness. This includes submitting a non-refundable application fee, substantial monetary study deposits (ranging from $\$55,000$ to $\$250,000$ depending on project size), and proving actual "site control" (evidence of land rights) to ensure the project is legitimate 103940.

- Severe Withdrawal Penalties: If a developer withdraws an interconnection request after entering the cluster, they face steep financial penalties. These penalties increase as the project advances through the study phases, ensuring that developers do not hold queue positions for speculative purposes, thereby decreasing the risk of cost-shifts to lower-queued projects 39.

- Accountability for Grid Operators: Historically, FERC only required grid operators to use "reasonable efforts" to meet study deadlines, meaning they faced no consequences for multi-year delays 21. Order 2023 eliminates this standard. Transmission providers now face strict financial penalties ranging from $\$1,000$ to $\$2,500$ per business day for failing to complete cluster studies, restudies, and facilities studies on time 2141.

- Technological Integration and Co-location: Order 2023 explicitly addresses modern energy portfolios. It requires grid operators to allow multiple generating facilities (e.g., a solar plant and a battery storage system) to co-locate behind a single point of interconnection and share a single interconnection request 103941. Furthermore, it allows battery storage systems to specify realistic operating restrictions (e.g., agreeing not to charge from the grid during peak load hours), which prevents grid engineers from wildly overestimating the necessary transmission upgrades 1040.

- Transparency and Heatmaps: Grid operators must now maintain publicly available visual representations - or "heatmaps" - showing the estimated available transmission capacity across their footprint. This allows developers to intelligently site their projects in areas with existing transmission headroom, avoiding congested nodes before they even apply 41. Furthermore, operators must evaluate Alternative Transmission Technologies (ATTs) - such as dynamic line ratings and advanced power flow control - which can increase grid capacity faster and cheaper than stringing new high-voltage wires 1040.

While FERC Order 2023 provides a robust regulatory framework, its full impact will take time to materialize. RTOs and utilities are currently implementing complex transitional studies to clear out legacy backlogs before fully adopting the new cluster rules 42.

Global Context: Bottlenecks in the UK and Europe

The interconnection crisis is not uniquely American; it is a systemic vulnerability threatening the electrification goals of the entire developed world. Across Europe and the United Kingdom, grid operators are struggling to update planning scenarios rooted in outdated market assumptions, acting as a systemic handbrake on the clean energy transition 2744.

The United Kingdom: NESO and the TMO4+ Reforms

In the UK, the grid connection queue is larger by far than anywhere else in Europe. The energy regulator Ofgem estimates average waiting times of 5.5 years, with some developers facing astonishing 15-year delays 27. Over £200 billion worth of projects are trapped in the queue 27. Realizing the "first-come, first-served" model was paralyzed by speculative "zombie projects" with no realistic hope of completion, the newly formed National Energy System Operator (NESO) is implementing sweeping connections reform 2545.

Mirroring the U.S. transition, the UK is moving to a "first ready, first served" model known as TMO4+ (Target Model Option 4+) 4528. Under this framework, projects must pass strict maturity milestones - such as securing land rights and submitting planning consents (Gate 2 criteria) - to obtain a confirmed connection point and date 4528. To facilitate this massive restructuring, NESO took the drastic step of pausing all new applications to the transmission network in early 2025 to reorder the queue, ruthlessly terminating stalled contracts to free up capacity for shovel-ready projects critical to the government's Clean Power 2030 Action Plan 254529.

The European Union: 1,700 GW Stuck in Planning

Across the European continent, the grid is failing to keep pace with the renewable power transformation. A comprehensive 2025 report revealed that an estimated $1,700\text{ GW}$ of renewable and hybrid capacity is currently trapped in grid connection queues across 16 countries 112744. This lack of grid access resulted in €7.2 billion in renewable electricity being curtailed (wasted) across just seven countries in 2024, passing the costs directly to electricity bill payers 4430.

The European Union Agency for the Cooperation of Energy Regulators (ACER) highlighted that managing grid congestion cost the EU EUR 4.2 billion in 2023 alone 3132. The European challenge is severely compounded by a lack of cross-border transmission integration. ACER found that transmission system operators (TSOs) in the highly meshed Core region (comprising 13 countries including Germany, France, and the Netherlands) were only making $54\%$ of physical cross-border capacity available for trade, far below the legally mandated $70\%$ rule 51. This underutilization drives extreme price volatility; for instance, higher cross-zonal capacity could have prevented roughly half of the severe high-price events seen during the 2024 summer in South-East Europe 51.

Recognizing that power grids risk becoming the primary roadblock to decarbonization, the European Commission launched an expansive EU Action Plan for Grids in late 2023 333454. The Commission estimates that €584 billion in targeted investments are required by 2030 to digitize, modernize, and expand both transmission and distribution networks, addressing a reality where 40% of Europe's distribution grids are more than 40 years old 113354. Concurrently, the EU is advancing an "Energy Highways" initiative to resolve acute geographical bottlenecks and is mandating harmonized definitions for available grid hosting capacities to ensure developers can seamlessly identify viable interconnection points across borders 3354.

Bottom Line Summary

The global transition to a sustainable energy economy has fundamentally shifted its focal point. For the past decade, the emphasis was heavily placed on lowering the cost of generating clean power; today, the imperative is building the physical and administrative infrastructure necessary to deliver it. The massive interconnection queues in the United States, the UK, and Europe serve as stark indicators that regulatory frameworks designed for slow, incremental grid expansion are wholly incompatible with the rapid, decentralized scale-up of renewable energy.

Resolving the interconnection bottleneck requires a paradigm shift from reactive to proactive grid planning. Reforms like FERC Order 2023 in the U.S. and TMO4+ in the UK are critical, necessary steps. By utilizing strict commercial readiness criteria to filter out speculative congestion and grouping projects to allocate study costs more efficiently, grid operators are stabilizing the queue. However, administrative streamlining is only half the solution. Long-term success mandates a fundamental shift in cost allocation - treating major transmission lines as public "highways" rather than private driveways - alongside massive, proactive capital investments to expand physical grid capacity ahead of generation demand. Without these structural and financial commitments, the clean energy pipeline will remain gridlocked, sacrificing economic efficiency, consumer affordability, and urgent climate targets.