Who Replaces Jerome Powell and What It Means for Rates

Kevin Warsh has officially succeeded Jerome Powell as the Chair of the Federal Reserve following a highly contested Senate confirmation in May 2026. While the incoming administration has exerted intense pressure for rapid interest rate cuts, Warsh inherits a complex economic landscape dominated by 3.8% inflation and persistent global energy shocks. Consequently, consumers should expect everyday borrowing costs - including mortgage and auto loan rates - to remain elevated in the near term as the central bank navigates this unprecedented leadership transition.

The Search for a New Central Bank Chief

The conclusion of Jerome Powell's four-year term as Federal Reserve Chair on May 15, 2026, marked the end of an era defined by pandemic-era stimulus, aggressive rate hikes, and intense political friction 12. Anticipating this transition, the incoming Trump administration launched an extensive search spearheaded by Treasury Secretary Scott Bessent, who initially interviewed eleven candidates before narrowing the field to five finalists 32.

The shortlist represented a mix of institutional continuity and sweeping reform. Candidates included current Fed Governors Christopher Waller and Michelle Bowman, BlackRock's Chief Investment Officer of Global Fixed Income Rick Rieder, National Economic Council Director Kevin Hassett, and former Fed Governor Kevin Warsh 334. Early in the process, prediction markets heavily favored Hassett - a staunch supporter of the administration's tariff policies who was viewed as highly likely to enact immediate rate cuts. At one point, Polymarket odds placed Hassett's chances at 66%, with Warsh trailing at 31% 78.

However, President Trump ultimately focused on what he called "the two Kevins," pushing both candidates on whether they could be trusted to support significant interest rate cuts 85. The president has explicitly outlined a desire to push borrowing costs down to 1% or lower by 2027 to ease the financial burden on homebuyers and reduce the cost of servicing the $30 trillion national debt 85. Despite Hassett's initial frontrunner status, Warsh emerged as the administration's ultimate choice. Trump formally nominated Warsh on March 4, 2026, viewing him as a highly credible figure who could command respect on Wall Street while simultaneously delivering on a mandate for institutional reform 67.

The Nominee: Kevin Warsh's Return to the Fed

Kevin Warsh, a 56-year-old financier and attorney, is no stranger to the inner workings of the Federal Reserve. A graduate of Stanford University and Harvard Law School, Warsh began his career in the mergers and acquisitions department at Morgan Stanley before serving as an economic adviser in the George W. Bush administration 89. Bush appointed him to the Federal Reserve Board of Governors in 2006, where he served as a key lieutenant to then-Chair Ben Bernanke 814.

During his first tenure at the Fed, Warsh played a critical role in navigating the 2008 global financial crisis, helping to coordinate the rescue of AIG and the sale of Bear Stearns to JPMorgan Chase 14. He eventually resigned in 2011, driven by deep disagreements over the central bank's heavy reliance on quantitative easing and large-scale bond-buying programs 1016. After leaving the Board, Warsh spent years as a fellow at Stanford's Hoover Institution, cementing his reputation as a vocal critic of the Fed's expanding footprint in the economy 214.

Warsh's confirmation also introduces a stark shift in the personal demographics of the central bank's leadership. With an estimated net worth between $170 million and $226 million - derived largely from private finance and his marriage to Jane Lauder, an heiress to the Estée Lauder fortune - Warsh is the wealthiest Fed Chair nominee in history 81711. This substantially surpasses the wealth of his predecessor, Jerome Powell, whose net worth is estimated between $75 million and $100 million from his career at the Carlyle Group 11.

A Historic and Contentious Confirmation

The path to Warsh's swearing-in was one of the most polarized in modern financial history. His nomination advanced through the Senate Banking Committee but immediately encountered a roadblock from within his own party. Outgoing Republican Senator Thom Tillis placed a hold on the nomination, demanding the resolution of an ongoing Justice Department criminal investigation into Jerome Powell 81912.

The investigation, spearheaded by U.S. Attorney Jeanine Pirro, centered on statements Powell made to Congress regarding alleged cost overruns in a $2.5 billion renovation of the Fed's Washington, D.C. headquarters 121322. Critics, including Powell himself, dismissed the probe as a thinly veiled political mechanism designed to coerce the Fed into lowering interest rates or forcing Powell into an early resignation 1323. Once the Justice Department formally dropped the criminal inquiry in late April, Tillis lifted his hold, clearing the way for a full Senate vote 1914.

On May 12, 2026, the Senate voted 51-45 to confirm Warsh to the Board of Governors, filling the seat vacated by Stephen Miran 6819. The following day, the Senate confirmed Warsh as the 17th Chair of the Federal Reserve by a narrow 54-45 margin 6815. The vote fell almost entirely along party lines, with Senator John Fetterman standing as the sole Democrat to break ranks and support the nomination 141516. The historically tight margin underscored deep partisan anxieties regarding the future independence of the central bank 1414.

Because Powell's official term as Chair expired on Friday, May 15, the Federal Reserve Board voted 5-1 to name Powell the "chair pro tempore" to bridge the brief gap before Warsh could officially take the reins 116. Warsh was formally sworn in on May 22, 2026, by Supreme Court Justice Clarence Thomas in a White House ceremony - a highly unusual setting for a Fed Chair, echoing Alan Greenspan's swearing-in under Ronald Reagan in 1987 81727.

Jerome Powell's Unprecedented Stand

While Warsh has assumed the chairmanship, Jerome Powell has not vacated the premises. Breaking 75 years of institutional precedent, Powell announced his intention to remain on the Federal Reserve's Board of Governors indefinitely 21328.

The Federal Reserve Act dictates that while the Chair serves a specific four-year term, members of the Board of Governors are appointed to staggered 14-year terms to insulate them from political election cycles 323. Powell's underlying term as a governor does not expire until January 31, 2028 2316. Historically, outgoing chairs resign their governor seats immediately to avoid creating a "shadow chair" dynamic that might undermine their successor 229.

Powell's refusal to step down is an explicit defense of the central bank's independence. Throughout the spring of 2026, Powell faced intense pressure from the executive branch, culminating in the DOJ investigation 1315. Powell publicly condemned the administration's actions as an "unprecedented" battering of the institution, vowing to stay on the Board until the attacks on the Fed's autonomy were "well and truly over with transparency and finality" 213. Consequently, Warsh must now lead a deeply divided Federal Open Market Committee (FOMC) where his predecessor retains a powerful voting seat and immense institutional loyalty 3017.

The Legal Limits of Firing a Fed Official

President Trump has repeatedly signaled his desire to fire Powell entirely, setting the stage for a monumental clash over the legal limits of executive power 2332. Under the Federal Reserve Act of 1913, governors can only be removed "for cause" - a standard generally interpreted by legal scholars as requiring evidence of serious misconduct, fraud, or malfeasance, rather than mere disagreements over interest rate policy 222332.

This legal boundary was recently tested in the high-profile Supreme Court case Trump v. Wilcox 2218. The administration had fired officials from the National Labor Relations Board (NLRB) and the Merit Systems Protection Board (MSPB) without cause, challenging the longstanding precedent of Humphrey's Executor, which protects independent agency heads from at-will presidential dismissal 3419.

While the Supreme Court issued a 6-3 emergency stay allowing the removal of the NLRB and MSPB officials to proceed pending further litigation, the majority order explicitly carved out the Federal Reserve 3436. Chief Justice John Roberts noted that the Court's ruling had no bearing on the constitutionality of for-cause removal protections for the Federal Reserve Board, describing the Fed as a "uniquely structured, quasi-private entity" with distinct historical traditions 341936. In a forceful dissent, Justice Elena Kagan warned that the administration's actions threatened to shatter the independence of bipartisan administrative bodies entirely 3419. For now, the Supreme Court's carve-out suggests the President lacks the legal authority to unilaterally fire Powell from his governor seat, guaranteeing a tense coexistence between Powell and Warsh 2334.

A Regime Change in Monetary Policy

Warsh has made it clear that his tenure will not be a continuation of the status quo. He has openly criticized the Powell-era Federal Reserve, arguing that the institution lost its way, suffered from "mission creep," and committed a massive policy error by misjudging the inflation surge of 2021 and 2022 103738. At his confirmation hearing, Warsh promised to lead a "reform-oriented" central bank, advocating for a fundamental "regime change" in how the Fed operates and interacts with financial markets 273940.

The incoming chair's strategy differs from his predecessor's in three critical areas: communication, balance sheet management, and market intervention.

Ending the Era of Forward Guidance

Since the 2008 financial crisis, the Federal Reserve has heavily relied on "forward guidance" - using press conferences, speeches, and economic projections (such as the famous "dot plots") to explicitly telegraph future interest rate moves to the public 1641. Warsh believes this extreme transparency has created an unhealthy dependency, where Wall Street relies on the Fed to eliminate uncertainty rather than properly pricing risk 1641.

Under Warsh, the Fed is expected to become significantly less communicative and less predictable 1641. He intends to limit pre-announced policy signaling and restrict public communications from Fed officials about the future rate path 1416. By increasing market uncertainty, Warsh hopes to force investors to rely on actual economic data and market discipline rather than central bank safety nets 1641.

Aggressive Balance Sheet Reduction

Under Jerome Powell, the Fed actively utilized its balance sheet - which ballooned to nearly $9 trillion before settling around $6.7 trillion - as a primary tool to influence long-term interest rates 163742. By purchasing vast quantities of government bonds and mortgage-backed securities, the Fed artificially suppressed long-term borrowing costs 1642.

Warsh views this dynamic as deeply flawed. He vehemently opposes the normalization of quantitative easing (QE) and argues that the Fed's massive balance sheet exposes the institution to unnecessary political pressure 37. Warsh favors a rapid, deliberate shrinking of the balance sheet, preferring to use the federal funds rate as the singular, primary tool for managing the economy 1037. This would involve allowing long-dated bonds to mature without reinvestment, forcing private markets to absorb the supply 16.

Re-plumbing Wall Street

Warsh also aims to reduce the Fed's day-to-day footprint in the short-term funding and repo markets - the complex infrastructure often referred to as Wall Street's plumbing 4344. Rather than constantly intervening to smooth over liquidity mismatches, Warsh wants to establish strict, rule-based criteria for when the Fed steps in 4344. Limiting emergency actions to predefined thresholds would force private-sector banks to manage their own liquidity risks, fundamentally altering how capital flows through the financial system 4344.

| Policy Dimension | The Powell Era (2018 - 2026) | The Warsh Era (2026 - Present) |

|---|---|---|

| Primary Policy Tools | Active use of both the Fed Funds Rate and the Balance Sheet. | Heavy reliance on the Fed Funds Rate; views the balance sheet as unhelpful. |

| Market Communication | High transparency, heavy reliance on "forward guidance" and quarterly dot plots. | Reduced signaling, limits on official speeches, embraces healthy market uncertainty. |

| Balance Sheet Trajectory | Peaked near $9 trillion, currently ~$6.7 trillion with cautious runoff. | Expected to accelerate runoff, refusing to use QE as a routine economic stimulant. |

| Market Intervention | Frequent, active presence in repo and short-term funding markets to ensure liquidity. | Hands-off approach; prefers strict, automatic triggers for emergency intervention only. |

The "Warsh Shock" and Financial Market Turmoil

The financial markets reacted violently to the confirmation of Warsh's nomination, an event analysts quickly dubbed the "Warsh Shock" 45. In the weeks prior to the announcement, institutional investors had placed highly leveraged bets that Trump would appoint a dovish loyalist - such as Kevin Hassett - who would aggressively cut rates and weaken the U.S. dollar to stimulate growth 82945.

When the administration officially pivoted to Warsh, a candidate with a historic reputation as an orthodox "inflation hawk," those leveraged narrative traps unraveled instantaneously 4520. The resulting market repricing triggered what was termed the "Great Metal Flush" 45. Spot silver plummeted 31.4% to $78.53 an ounce in a single day - its worst drop since March 1980 2. Gold futures shed roughly 11.4% of their value, dropping to $4,745, as the U.S. dollar surged on expectations that interest rates would stay higher for longer under Warsh's disciplined leadership 23745.

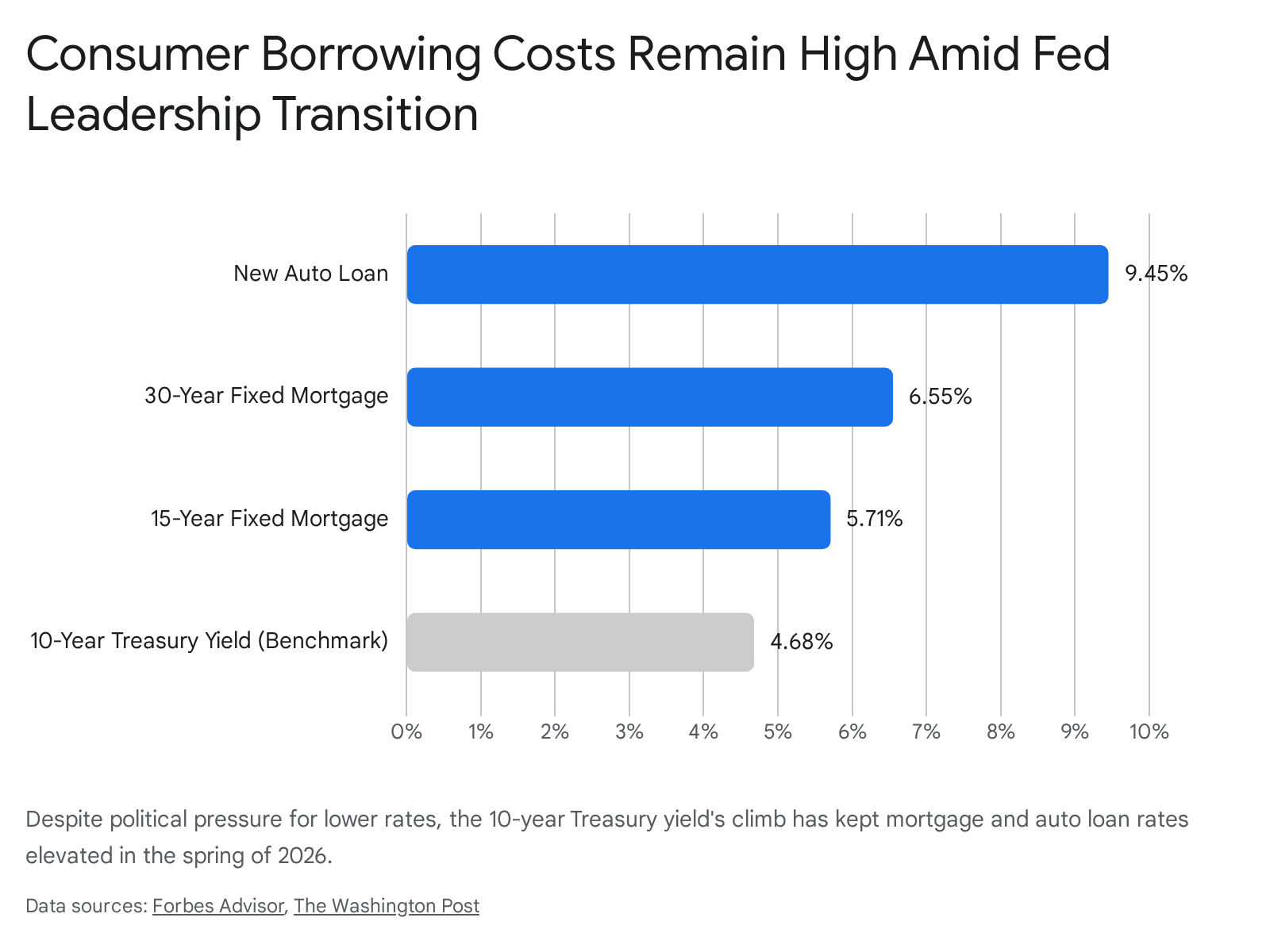

Simultaneously, the bond market began to hemorrhage. The anticipation of Warsh shrinking the Fed's balance sheet meant that the central bank would step back as a major buyer of U.S. Treasuries 2942. Private markets were suddenly forced to price in the absorption of massive amounts of government debt 29. This dynamic, combined with the U.S. government's high deficit borrowing - which has grown to roughly 6% of GDP to finance defense and epic investments in artificial intelligence - drove long-term bond yields significantly higher 12. In late May 2026, the 30-year Treasury bond yield hit 5.18%, its highest point since 2007, while the benchmark 10-year Treasury note climbed to 4.68% .

What This Means for Everyday Borrowing Costs

President Trump's demands for the Fed to slash interest rates to 1% face a severe collision with macroeconomic reality. Warsh inherits an environment where immediate, deep rate cuts are highly problematic due to a resurgence of stubborn inflation 81721.

In the spring of 2026, inflation reaccelerated noticeably. The Consumer Price Index (CPI) hit 3.8% year-over-year in April - its highest level in three years 143941. Producer prices (PPI) spiked by 6% month-over-month 1441. The primary driver of this inflationary wave is a global energy shock triggered by the U.S.-Israel war with Iran, which has disrupted the Strait of Hormuz and pushed oil prices over $100 a barrel 171421. U.S. gasoline prices soared by nearly 53% following the initial strikes in the Middle East, acting as a massive tax on the American consumer 2250.

At his confirmation hearing, Warsh firmly stated, "Inflation is a choice, and the Fed must take responsibility for it" 38. He warned that "low inflation is the Fed's shield," suggesting that the central bank cannot maintain its independence if it allows prices to spiral out of control to appease politicians 37. Consequently, the FOMC held the federal funds rate steady at a range of 3.50% to 3.75% during its most recent meetings, with futures markets pricing in a 97% chance of an extended pause 7142223.

For everyday Americans, the transition has done little to alleviate financial pressure. Because consumer loans are intricately pegged to the long-term Treasury yields that spiked during the "Warsh Shock," the cost of financing homes and vehicles remains painfully high .

In late May 2026, the average rate on a 30-year fixed-rate mortgage climbed back to roughly 6.55% to 6.75% 24. Shorter-term home financing also saw increases, with the 15-year fixed mortgage hovering around 5.71% to 6.05% 2453. Jumbo mortgage rates, required for loans exceeding standard conforming limits, sat near 6.83% 23. Auto buyers are feeling even more severe distress; average interest rates on new car loans hit 9.45% in the spring, pushing the typical monthly vehicle payment to a staggering $757 .

The AI Disinflation Theory

If Warsh cannot immediately cut rates due to the Iran war and energy shocks, how will he satisfy the administration's demands for cheaper borrowing? Warsh has heavily championed a macroeconomic theory suggesting that the ongoing boom in Artificial Intelligence (AI) will serve as a massive disinflationary force 394154.

In a Wall Street Journal op-ed published prior to his nomination, Warsh argued that AI integration is currently unlocking unprecedented corporate productivity gains 54. In economic terms, when labor productivity surges, an economy can grow rapidly without triggering inflation, because the supply of goods and services outpaces demand 3054. Warsh believes that this AI-driven supply-side growth will eventually cool persistent price pressures, giving the Federal Reserve the mathematical justification it needs to lower the policy rate safely later in his term, perhaps by late 2026 or early 2027 4154. However, several of his FOMC colleagues remain skeptical, warning that massive capital investments into AI infrastructure and data centers are currently adding to short-term price pressures rather than relieving them 30.

Global Central Bank Ripple Effects

Warsh's appointment has generated considerable anxiety far beyond Wall Street, unsettling international policymakers who rely on the Federal Reserve as an anchor of global financial stability 56.

During his confirmation hearings, Warsh hinted that while the Fed must remain strictly independent in setting domestic interest rates, it should coordinate much more closely with the presidential administration and Congress on matters of international finance 56. This assertion alarmed foreign central bankers. The Federal Reserve plays a pivotal role in stabilizing the global economy during crises by providing U.S. dollar liquidity swap lines to other nations, ensuring that foreign markets do not run out of the world's reserve currency 5657.

An unnamed European Central Bank (ECB) policymaker warned that if the Fed becomes a "less reliable" partner internationally, or if the U.S. government outright politicizes these swap lines to extract foreign policy or trade concessions, it could generate severe market turbulence and accelerate the dollar's declining global market share 5657.

Furthermore, peer institutions are dealing with the exact same geopolitical inflation shocks as the United States 21. The ECB has clearly signaled that a rate hike is likely in June 2026, noting that the inflationary damage from the Middle East conflict is already impacting the Eurozone 17. The Bank of England (BoE) is also weighing an "active hold" or a potential rate hike, pulling back from previous plans to cut rates multiple times this year 17. If foreign central banks raise their interest rates to combat inflation while the U.S. is pressured to cut or pause, it will create significant yield differentials, placing additional stress on global currency markets and the broader financial regime 1757.

Bottom line

Kevin Warsh steps into the Federal Reserve chairmanship promising a sweeping "regime change" that favors a smaller balance sheet, reduced forward guidance, and less central bank intervention in financial markets. However, his ambitions to lower borrowing costs are severely constrained by sticky 3.8% inflation fueled by the ongoing U.S.-Israel war with Iran. While everyday consumers and the White House eagerly await relief on 6.5%+ mortgages and 9.4%+ auto loans, rates are highly likely to remain elevated until either geopolitical tensions subside or Warsh's theory of AI-driven productivity successfully cools the broader economy.