What the September 2026 Dot Plot Says About Rate Cuts

Despite widespread optimism earlier this year that borrowing costs would fall, the Federal Reserve is highly unlikely to cut interest rates at its September 2026 meeting. A resurgence in inflation driven by global energy shocks, a surprisingly resilient labor market, and the arrival of a fiercely hawkish new Fed Chair have dramatically shifted the economic landscape. Instead of rate cuts, financial markets are now increasingly bracing for the possibility that borrowing costs will remain elevated - or even rise - through the end of the year.

What Is the FOMC Dot Plot Telling Us?

To understand why a September 2026 rate cut is now off the table, we must first look at where expectations stood in the spring. Four times a year, the Federal Open Market Committee (FOMC) releases its Summary of Economic Projections (SEP) 12. This release includes the famous "dot plot" - a visual chart mapping out where each central bank official expects interest rates to end up over the coming years. It serves as the primary mechanism the Fed uses to telegraph its future policy intentions to the public.

At the conclusion of the March 17 - 18, 2026 meeting, the Federal Reserve opted to hold the federal funds target range steady at 3.50% to 3.75% 345. The accompanying dot plot revealed that the median expectation among the 19 Fed officials who submitted projections was to reduce the target rate to 3.4% by the end of 2026 6. Because the Fed typically adjusts rates in quarter-point (0.25%) increments, a target of 3.4% implied that the committee was tentatively planning for just one more rate cut before the year's end 47.

However, beneath this headline median, the March dot plot revealed a deeply divided committee and a subtle shift toward a tighter monetary stance. The projections showed a remarkable clustering: 14 of the 19 officials placed their dots narrowly between the 3.25% and 3.75% ranges, indicating a strong consensus that the era of aggressive rate cutting was over 67. Only a small minority foresaw deeper cuts.

More notably, the committee's projection for the longer-run federal funds rate - often considered a proxy for the "neutral rate" that theoretically neither stimulates nor restricts the economy - was revised upward from 3.0% to 3.1% 45. This upward revision, representing the highest median estimate since 2016, sent a quiet but unmistakable signal to financial markets: the days of ultra-low, pandemic-era borrowing costs were permanently behind us 45.

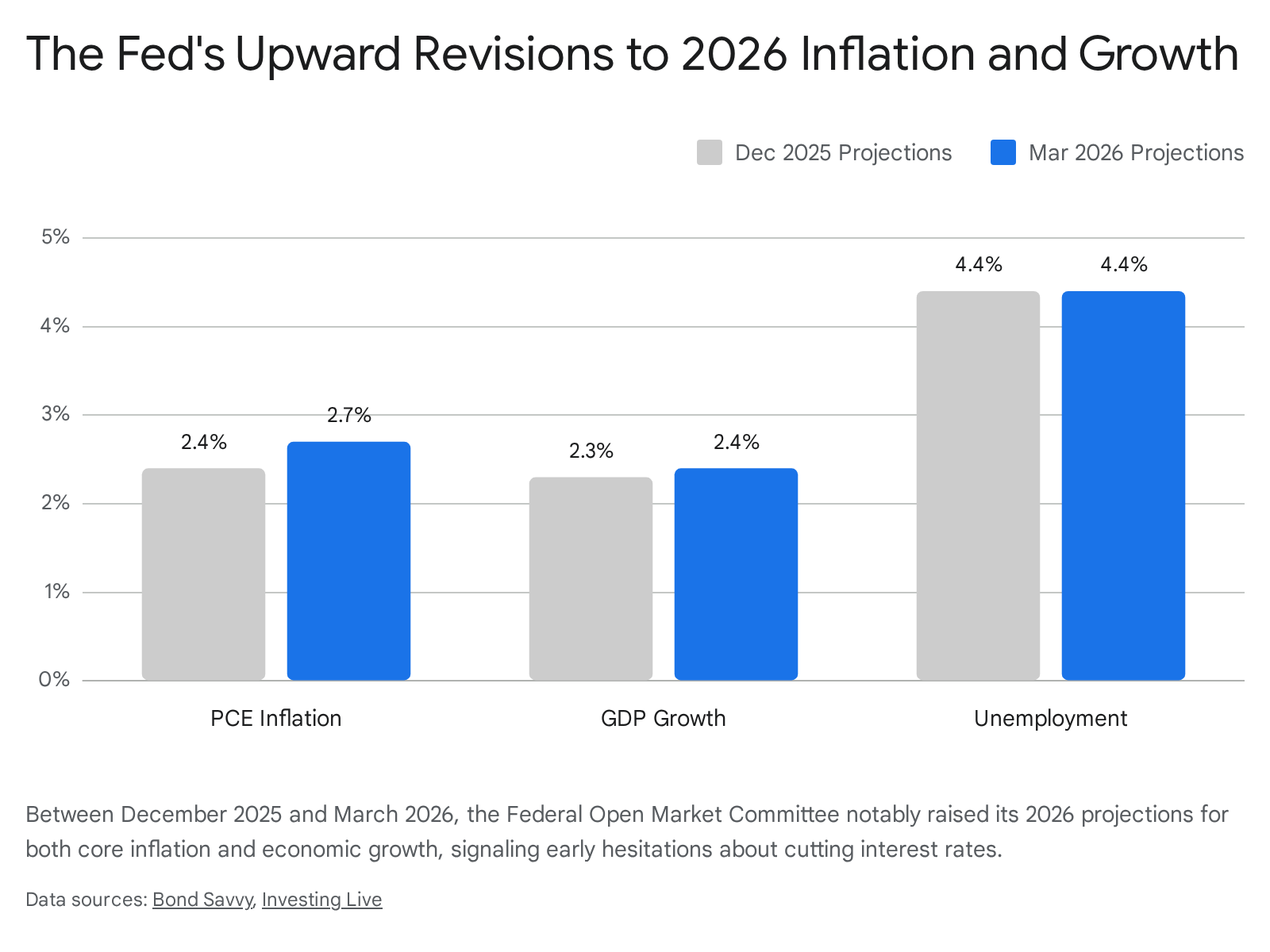

The March vs. December Projections

The Federal Reserve is fundamentally a data-dependent institution, and the data arriving in the spring of 2026 consistently pointed away from rate cuts. The March projections themselves reflected this reality, as officials were forced to confront worsening economic metrics compared to their previous forecasts.

Officials revised their expectations for 2026 core Personal Consumption Expenditures (PCE) inflation - the Fed's preferred gauge that strips out volatile food and energy prices - up to 2.7%, a significant jump from the 2.4% they had projected just three months prior in December 2025 67. They also nudged up their expectations for 2026 gross domestic product (GDP) growth from 2.3% to 2.4%, while keeping the projected unemployment rate steady at 4.4% 67.

The economic rationale here is clear-cut: a central bank cannot justify lowering interest rates to stimulate an economy that is already growing robustly, especially when inflation is reaccelerating. By late April, the real-world data confirmed the Fed's mathematical fears. The core PCE price index rose by 3.3% year-over-year, marking an increase from the previous month and hovering uncomfortably high above the Fed's official 2% target 8.

Why Have Interest Rate Expectations Shifted?

If the March dot plot left the door slightly ajar for a single rate cut later in the year, subsequent geopolitical and macroeconomic developments have firmly slammed it shut. The economic environment heading into the fall of 2026 is defined by three overlapping forces: energy price shocks, sticky domestic inflation, and a remarkably resilient labor market.

The Geopolitical Oil Shock

The most significant external shock to the U.S. economy in 2026 has been the escalation of conflict in the Middle East, particularly involving Iran 91011. This geopolitical crisis has disrupted global supply chains and forced closures or severe delays in critical maritime choke points like the Strait of Hormuz. Consequently, the global energy market has been thrown into disarray, pushing crude oil prices near $100 per barrel earlier this year 4.

Because energy is a foundational input for almost every good and service in the modern economy - from manufacturing plastics to transporting groceries - this oil shock has quickly seeped into domestic consumer prices. Wall Street analysts note that this "energy cost passthrough" is a primary reason why headline and core inflation measures are proving so stubborn 1112.

The Federal Reserve acknowledged this directly; during their late-April FOMC meeting, officials explicitly stated that the conflict in the Middle East was adding significant upside uncertainty to the inflation outlook 1112. Raising interest rates cannot magically reopen shipping lanes, end wars, or pump more oil out of the ground, a reality acknowledged by Fed centrists like Richmond Fed President Tom Barkin 13. However, central bankers are deeply fearful that if energy prices remain high, consumers will begin to expect higher inflation permanently. Once inflation expectations become "unanchored," the phenomenon becomes self-fulfilling as workers demand higher wages to cover their living costs, leading businesses to raise prices further. To prevent this psychological shift, the Fed is highly motivated to keep monetary policy tight.

Tariffs, Shelter, and the "Supercore"

Beyond the immediate sting of energy prices, the structural components of U.S. inflation are also resisting gravity. Economists point to the implementation of new import tariffs as a contributing factor to the sticky prices seen on store shelves. Estimates suggest that tariff-related price pressures have added as much as 0.5 percentage points to year-over-year core PCE inflation, and this impact could grow to 0.8 percentage points by mid-2026 before eventually fading 14.

Furthermore, while shelter inflation (the cost of housing and rent) has slowly begun to decelerate from its pandemic-era peaks, "supercore" inflation remains uncomfortably elevated 15. Supercore inflation tracks the cost of core non-housing services - a broad category that includes everything from auto insurance and healthcare to dining out and haircuts, representing roughly half of all private consumption 15. Because service sector businesses are highly labor-intensive, the prices they charge are tightly linked to the wages they must pay their employees. As long as wages are rising, supercore inflation is incredibly difficult to stamp out.

A Resilient, Cooling Labor Market

The traditional trigger for a central bank rate cut is a rapidly deteriorating job market. The Federal Reserve operates under a "dual mandate" mandated by Congress: to ensure stable prices and to promote maximum employment 916. If the unemployment rate were to suddenly spike, signaling an impending recession, the Fed might be forced to cut rates in September to save jobs, even if inflation remained slightly above the 2% target.

However, the U.S. labor market in 2026 has refused to break. While it is certainly cooling compared to the frenetic, unsustainable hiring pace of 2022 and 2023, it remains fundamentally healthy. The U.S. economy added 115,000 jobs in April 2026 1019. While this represents a moderation from previous boom years, it is still a solid pace of hiring that indicates employers are retaining their staff and feel confident enough to expand 1019.

Simultaneously, the unemployment rate has remained relatively static, hovering around 4.4% 26. Because job gains are still positive and wage growth remains solid enough to support consumer spending, the FOMC simply lacks the economic justification to rush into a rate cut 1017. As analysts at Goldman Sachs noted, a combination of lower monthly inflation prints and significant labor market softening is a hard prerequisite for any policy easing - and neither condition has been met heading into the fall 1112.

How Does the New Fed Chair Change the Outlook?

Perhaps the most definitive reason why a September rate cut is highly improbable is the recent transition of power at the very top of the Federal Reserve. Jerome Powell's term as Fed Chair concluded in May 2026, and he was officially succeeded by Kevin Warsh, who was sworn in as the 17th Chair of the Federal Reserve on May 22 1822.

The transition from Powell to Warsh represents a seismic shift in the central bank's philosophical approach to monetary policy. Warsh, a former Fed governor and Wall Street financier, brings a deeply hawkish, anti-inflationary track record to the role 1819.

Kevin Warsh's Hawkish Stance

Throughout his confirmation process, Warsh openly criticized the Fed's delayed response to the initial pandemic inflation spike. During congressional testimony, he referred to the central bank's delayed inflation response as a "fatal policy error," arguing that once inflation takes hold in an economy, it is significantly more expensive and difficult to eradicate 18. He has forcefully advocated for a "regime change" in how the central bank conducts policy, signaling a departure from the more accommodating tone of his predecessor 1822.

A central pillar of Warsh's economic philosophy is his distaste for the massive expansion of the Fed's balance sheet. Following the 2008 Great Recession and the 2020 pandemic, the Fed engaged in quantitative easing (QE) - creating money electronically to buy government bonds and mortgage-backed securities, deliberately driving down long-term interest rates 3. Warsh views this $6.7 trillion balance sheet as a primary driver of asset bubbles and wealth inequality, arguing that it disproportionately benefits those who already own stocks and homes 1920.

Under Warsh's leadership, the Fed is expected to prioritize quantitative tightening (QT) - the active shrinking of the balance sheet by allowing bonds to mature without reinvestment, or outright selling them - over aggressively managing short-term interest rates 1820. While Warsh has suggested that a smaller balance sheet might eventually allow for lower policy rates in the distant future, his immediate, stated priority is restoring the Fed's credibility as a fierce inflation fighter 1822.

The Fight for Central Bank Independence

The Warsh appointment also brings a complex, highly scrutinized political dynamic to the forefront. President Donald Trump, who ultimately supported Warsh's nomination, has frequently and publicly pressured the Federal Reserve to lower interest rates to spur economic growth 1122. Trump has stated he would let Warsh "do what he wants to do" regarding rates, marking a shift from his earlier demands for ultra-low rates, but the underlying tension remains palpable 11.

Historically, Federal Reserve chairs go to great lengths to establish their independence from the executive branch early in their tenure. Given Warsh's hawkish reputation and his pledge not to act as a "sock puppet" for political interests, market analysts heavily doubt he would capitulate to political demands for an unwarranted rate cut just months before the midterm congressional elections 1318. Cutting rates in September while inflation is climbing would deeply damage Warsh's credibility on Wall Street and signal a dangerous loss of institutional independence to global markets.

The Historic April 2026 FOMC Dissent

The internal politics of the FOMC validate the view that the institution is drifting further away from rate cuts. The meeting on April 28 - 29, 2026, was a watershed moment for the modern Federal Reserve. While the committee ultimately voted to hold the target rate at 3.50% - 3.75%, the vote was notably fractured at 8-4 112521.

A vote with four dissenters is incredibly rare in modern central banking; it marked the most divisive FOMC decision since October 1992 1121. This fracture reveals a committee deeply unsettled by the current economic data. The dissenters were not unified in their reasoning, reflecting the complex crosscurrents in the economy. Governor Stephen Miran cast a dovish dissent, arguing in favor of an immediate 25-basis-point rate cut, citing low job gains and the need to protect the labor market 457.

However, the other three dissenters pulled in the exact opposite direction. According to the meeting minutes, these hawkish members explicitly opposed the policy statement's language that suggested an "easing bias" (the implication that the Fed's next move would be a cut) 1121. Furthermore, a majority of Fed officials highlighted that actual "policy firming" - a rate hike - would become appropriate if inflation continued to run persistently above the 2% target 1121.

Influential figures like Fed Governor Chris Waller have publicly stated that they can "no longer rule out rate hikes further down the road if inflation does not abate soon" 13. When the central bank is actively debating whether to raise rates and struggling to maintain internal consensus, the probability of a smooth, coordinated September rate cut effectively falls to zero.

What Do Major Banks Predict for Late 2026?

As the macroeconomic data hardened and the reality of Warsh's new leadership set in, major financial institutions drastically revised their interest rate models. The consensus among the world's largest banks has shifted dramatically. At the start of the year, many forecasted multiple cuts in 2026; today, they expect none, or are even modeling the possibility of a hike.

Summary of Major Bank Interest Rate Forecasts (Late May 2026)

| Financial Institution | Previous 2026 Forecast | Updated Forecast | Key Rationale |

|---|---|---|---|

| Goldman Sachs | Cuts in Sept. and Dec. 2026 | First cut delayed to December 2026, second in March 2027 | Energy cost pass-through keeping core PCE near 3%; solid April job gains removed urgency to ease. 101222 |

| J.P. Morgan | Rate cut in January 2026 | No cuts in 2026; forecasts a 25-basis-point hike in Q3 2027 | Labor market is not deteriorating rapidly; expects labor market to tighten and disinflation to be slow. 17 |

| Morgan Stanley | Cuts in Jan. and April 2026 | First cut postponed to mid-to-late 2026 | Stable unemployment and solid wage growth do not justify immediate emergency easing. 17 |

| Barclays | Rate cut in early 2026 | Postponed cut to late 2026 at the earliest | Requires material decline in inflation before considering an easing cycle. 1728 |

Goldman Sachs, previously a prominent voice predicting a September cut, formally pushed its forecast back to December 2026 in early May 1922. Their analysts bluntly stated that the April jobs report of 115,000 new payrolls "removed pressure on the Fed to cut rates soon," shifting the central bank's focus entirely to containing inflation 19. Furthermore, Goldman's internal models now suggest an unsettling 44% probability of a rate hike by April 2027, creating profound headwinds for risk assets like equities and cryptocurrencies 10.

J.P. Morgan has taken an even more aggressive stance, withdrawing its rate cut outlook entirely. The firm now predicts that the Federal Reserve's next definitive move will be a 25-basis-point rate hike in the third quarter of 2027 17. This reflects a belief that rolling geopolitical shocks and structural supply-chain changes have established a new normal, where inflation's floor is permanently higher than it was in the decade preceding the pandemic 9.

How to Read the CME FedWatch Tool

While bank economists produce long-term macroeconomic models, the futures market tells us exactly where institutional money is being wagered right now. The CME FedWatch Tool is the financial industry's standard barometer for monetary policy expectations. It calculates the probabilities of future Fed actions by analyzing the pricing of 30-Day Federal Funds futures contracts 1223. These are real financial instruments that allow traders to hedge against or speculate on the Fed's target rate.

To read the tool, one looks at the implied rate from the futures contract and compares it to the current target range. If futures are trading at a lower yield than the current target, the market expects a cut.

By late May 2026, the futures market had entirely abandoned the September rate cut narrative: * The June Meeting: Pricing indicates a near 99.9% probability that the Fed will maintain the current 3.50% - 3.75% rate at its June 16-17 meeting 1224. * The September Meeting: Market-based Fed Funds rate forecasts point to levels remaining near 3.7% through late 2026, indicating traders expect a hold through the fall 31. * Year-End 2026: Shockingly, the probability of a rate hike has overtaken the probability of a cut. According to late-May FedWatch data, there is a roughly 32.1% chance the Fed holds rates steady through December, and a combined 67.9% chance that the Fed implements one or more rate hikes before the year is out (with a 42.5% chance of a 25-basis-point increase specifically) 32.

When futures traders - who risk billions of dollars on these outcomes - are pricing in a two-thirds probability of a rate hike by year-end, a rate cut in September is mathematically unfeasible barring a catastrophic, sudden collapse of the U.S. economy.

The Global Central Bank Divergence

The Federal Reserve does not operate in a vacuum, but the U.S. economy currently finds itself on a very different trajectory than its global peers. To understand the Fed's current rigidity, it is helpful to contrast it with other major central banks.

Current Policy Rates of Major Central Banks (Mid-2026)

| Central Bank | Current Policy Rate | Context & Outlook |

|---|---|---|

| U.S. Federal Reserve | 3.82% - 3.86% | Holding steady; bias shifting from cuts toward potential hikes due to sticky inflation. 1125 |

| Bank of England (BoE) | 4.26% - 4.21% | High rates maintained; struggling with domestic inflation and energy shocks. 925 |

| European Central Bank (ECB) | 2.57% - 2.58% | Lower relative rates; managing weaker economic growth alongside imported energy inflation. 925 |

| Bank of Canada (BoC) | 2.66% | Moderate stance; highly sensitive to U.S. economic crosswinds. 25 |

| Bank of Japan (BoJ) | 1.23% - 1.18% | Gradually hiking rates from historic lows to combat rising domestic inflation. 1625 |

Data sourced from futures-based estimates and current tracking as of May 2026 25.

The energy price shock emanating from the Middle East has heavily impacted Europe, pushing inflation higher across the continent 9. However, the European Central Bank and the Bank of England operate under different mandates than the Fed. Both the ECB and the BoE have "price stability" as their sole mandate, whereas the Fed balances inflation with employment 9.

More importantly, the European domestic economy lacks the overheating, robust consumer demand seen in the United States. While the ECB and BoE must manage imported energy inflation, their underlying economies are fundamentally weaker. This means they cannot sustain high interest rates as easily as the U.S. without triggering severe recessions 916. Meanwhile, the Bank of Japan is walking a completely different path, slowly hiking rates away from its historic sub-zero policies to combat its own newly rising inflation 1628. This global divergence underscores the unique resilience of the U.S. economy and further reduces the external pressure on the Federal Reserve to cut rates prematurely.

What This Means for Your Money

For the general public, the esoteric debates over dot plots, supercore inflation, and central bank balance sheets translate directly into the monthly cost of living. Because the Fed controls the baseline cost of money in the economy, a prolonged pause - or a potential hike - will keep consumer borrowing costs painfully elevated through 2026 and likely into 2027.

Mortgage Rates and the Housing Market

Mortgage rates are not set directly by the Fed, but they closely track the 10-year U.S. Treasury yield, which rises and falls based on long-term inflation expectations and overall Fed policy 3426. As it became clear the Fed would not cut rates this fall, the yield on the 10-year Treasury held firm near 4.45% in late May 2026 824.

Consequently, the average 30-year fixed-rate mortgage is hovering around 6.51% to 6.63%, with jumbo loans pushing closer to 6.7% and 15-year fixed mortgages sitting near 5.85% 2534. Industry analysts, including those at the Mortgage Bankers Association, project that mortgage rates will remain trapped in the mid-to-upper 6% range for the balance of the year. If the Iran conflict protracts and bond investors demand higher yields to offset inflation risk, average rates could easily tip over the 7% threshold 2636.

This dynamic creates a devastating "lock-in effect" for the housing market. Millions of homeowners secured 30-year mortgages at roughly 3% during the pandemic. Even if they wish to move, taking out a new loan at 6.5% would drastically increase their monthly payments. This effectively freezes existing home inventory, keeping home purchase prices artificially high due to a severe lack of supply 2527. Real estate analysts bluntly advise that buyers waiting on the sidelines for a dramatic drop in interest rates in 2026 will be deeply disappointed; if the financial math works for a family now, waiting for a rate cut is a losing strategy that may only result in paying higher overall home prices 25.

Auto Loans and Credit Cards

The story is equally grim for short-term consumer debt. Auto loan rates are expected to remain prohibitively high. Forecasts indicate that five-year new car loan rates will average around 6.7% for the remainder of 2026, dipping no lower than 6.4% in the absolute best-case scenarios 27. Four-year used car loans will average roughly 7.1% 27. Combined with the inflated sticker prices of vehicles, financing a car will remain a major financial hurdle for the average household.

Similarly, credit card annual percentage rates (APRs), which are directly tethered to the federal funds rate via the prime rate, will remain at historic highs. Consumers who carry month-to-month balances will continue to be heavily penalized by the Fed's ongoing fight against inflation 27.

Bottom line

The narrative that the Federal Reserve would swoop in with aggressive interest rate cuts in the fall of 2026 has been thoroughly dismantled by economic reality. A combination of persistent inflation exacerbated by Middle Eastern energy shocks, a labor market that refuses to buckle, and the appointment of the deeply hawkish Kevin Warsh as Fed Chair guarantees that rates will stay higher for longer. For consumers, businesses, and investors, the takeaway is clear: do not build financial plans around the expectation of a September rate cut, as the central bank is currently more likely to raise rates than lower them.