What to Expect From the June 2026 FOMC Meeting

The Federal Reserve is overwhelmingly expected to hold its benchmark interest rate steady at a target range of 3.50% to 3.75% during its June 16 - 17 meeting. A resurgence in energy-driven inflation has effectively eliminated the possibility of summer rate cuts, shifting market focus toward the growing risk of rate hikes by year-end. Under the new leadership of Chairman Kevin Warsh, investors are also bracing for a significant pivot away from the Fed's traditional forward guidance, signaling a more unpredictable era for monetary policy.

The Dawn of the Warsh Era

When the Federal Open Market Committee (FOMC) convenes in June 2026, it will do so under a fundamentally new philosophical framework. Kevin Warsh was sworn in as the 17th Chair of the Federal Reserve on May 22, 2026, inheriting what is widely considered the most politically charged and economically complex environment in a generation 12. Replacing Jerome Powell, whose term expired in mid-May, Warsh steps into the role amid intense scrutiny, stubborn inflation, and a bond market highly sensitive to leadership changes 14.

The transition marks a stark pivot in how the central bank will operate and communicate with the public. Since the aftermath of the 2008 financial crisis, the Federal Reserve has increasingly relied on hyper-transparency and "forward guidance" - the practice of telegraphing policy moves well in advance to prevent market tantrums. Powell institutionalized this approach with extensive post-meeting press conferences and a heavy reliance on economic projections to guide investor expectations 2.

Warsh, conversely, views this level of predictability as a vulnerability. He has publicly criticized the Fed's reliance on forward guidance, arguing that providing too much certainty limits the central bank's agility and fosters an unhealthy market dependency on Fed intervention 23. Observers expect Warsh to reintroduce a degree of ambiguity to monetary policy. He has indicated that the Fed should react strictly to incoming data rather than pre-committing to a specific path, a stance that has some analysts warning of increased financial market volatility as investors lose their traditional central bank "safety net" 27.

A Contentious Confirmation and the Independence Question

Warsh's path to the chairmanship was not without friction. He was confirmed by the Senate in a narrow 54 - 45 vote on May 13, 2026, marking the closest confirmation margin for a Fed chair in the modern era 17. His swearing-in ceremony took place in the East Room of the White House, a venue not used for this purpose since Alan Greenspan's appointment in 1987 17.

The ceremony highlighted the immense political pressure Warsh faces. President Donald Trump has been a vocal critic of high interest rates, repeatedly urging the central bank to lower borrowing costs to stimulate economic growth 48. During the swearing-in, the President remarked that Warsh understands a booming economy is a positive development and suggested that growth would allow the United States to manage its national debt 8.

This places the new Chair in a delicate position. Warsh has historically been viewed as a monetary hawk - an official who prioritizes inflation control and a lean balance sheet over short-term economic expansion 4. While he has emphasized that the Federal Reserve will maintain its independence from the executive branch, his early decisions will be heavily scrutinized to see whether he bends to political desires for rate cuts or holds firm against lingering inflationary pressures 456. A recent Brookings Institution survey of Fed watchers identified maintaining monetary policy independence from the White House as Warsh's single biggest challenge 6.

Dismantling the Communication Framework

One of the most immediate changes expected under Warsh is a reduction in the frequency and volume of Fed communication. He has argued that policymakers "talk too much" and that press conferences should ideally be reserved for moments when the central bank has "important news" to deliver, rather than occurring automatically after every FOMC meeting 312.

Furthermore, Warsh is a vocal critic of the Summary of Economic Projections (SEP) - specifically the famous "dot plot." First introduced by Ben Bernanke in 2012, the dot plot charts each anonymous FOMC member's projection for future interest rates 1213. Warsh believes that policymakers tend to hold onto these forecasts longer than they should, and that the market's obsession with the dots can compound policy errors by boxing the Fed into rigid forward guidance 312.

While the June 16 - 17 meeting is scheduled to include an updated SEP, analysts will be listening closely during Warsh's inaugural press conference to see if he attempts to downplay the dot plot's significance or hints at dismantling the practice entirely in future quarters 614.

The June 2026 Decision: Why a Rate Hold Is Inevitable

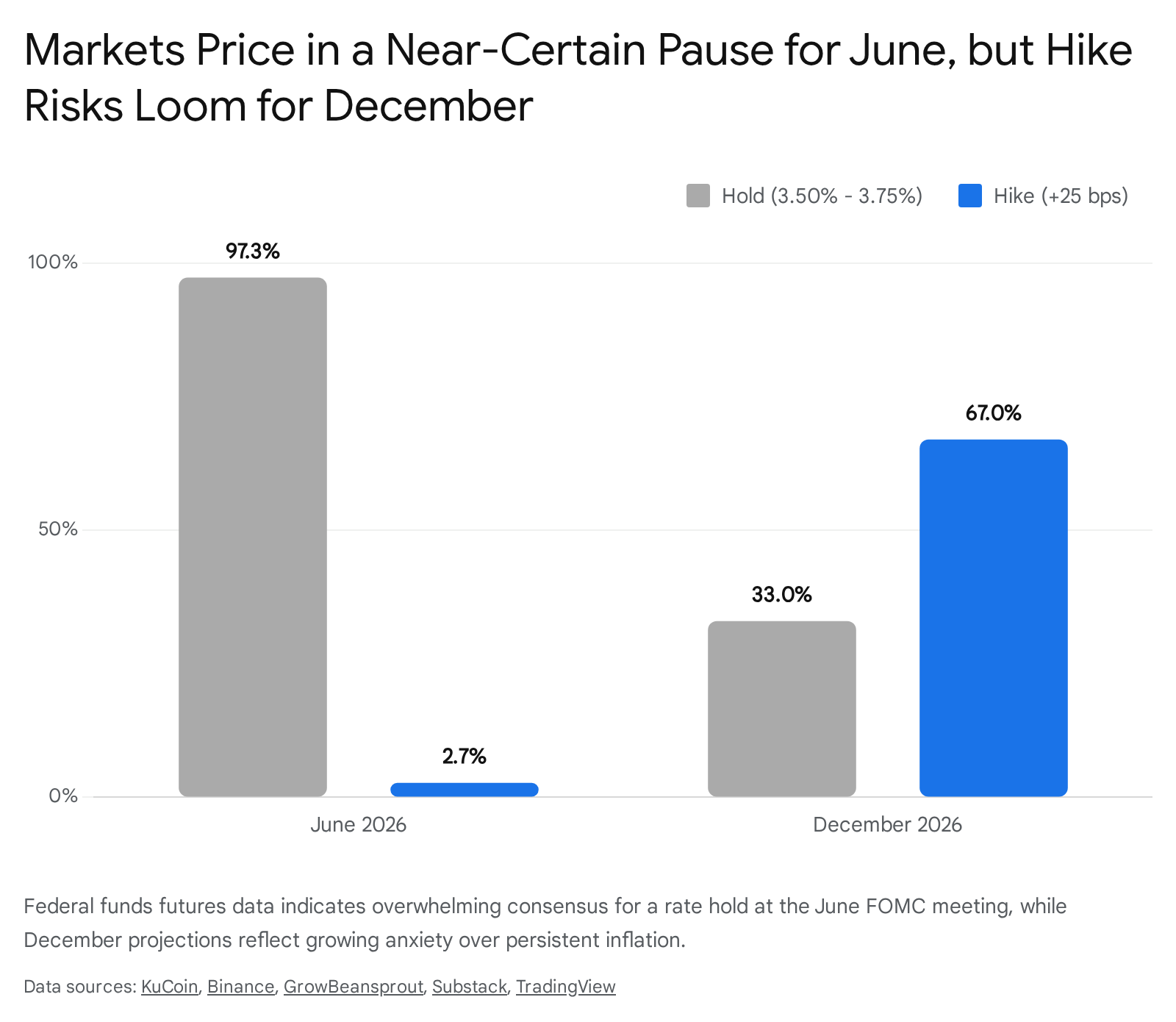

Despite the change in leadership and the political desire for cheaper money, the outcome of the June FOMC meeting is effectively locked in. Financial markets and economic analysts are in near-unanimous agreement that the committee will hold the federal funds target rate steady at 3.50% to 3.75% 7157.

According to the CME FedWatch Tool, which calculates the probability of future Fed moves based on federal funds futures trading, markets are pricing in a roughly 97% to 99% chance that rates will remain unchanged on June 17 7171819.

The shift in market expectations over the past few months has been profound. Earlier in the year, investors confidently priced in a series of rate cuts for 2026. Major institutions, including Goldman Sachs and Barclays, had initially forecast cuts in the spring and early summer 208.

However, by late May, the dialogue completely inverted. The combination of persistent inflation and geopolitical instability has forced a massive recalibration across Wall Street. J.P. Morgan recently withdrew its outlook for near-term easing, now predicting that the Fed's next move will actually be a rate hike in 2027, while Macquarie forecasts a hike in the fourth quarter of 2026 20. Morgan Stanley, too, has revised its expectations, suggesting the Fed may stay on hold entirely through 2026 9.

The Looming Risk of December Rate Hikes

The market is now actively hedging against the possibility of borrowing costs going up rather than down. Looking ahead to the final FOMC meeting of the year on December 8 - 9, 2026, futures markets are assigning an increasingly high probability - ranging from roughly 58% to 67% - of a 25-basis-point rate hike 823. Such a move would push the target range up to 3.75% - 4.00%.

This pivot creates a fascinating tension for the June meeting. In March 2026, the median FOMC dot plot projected that the Fed would cut rates slightly, ending the year at roughly 3.4% 2410. The June release of the SEP will have to reconcile these dovish springtime forecasts with the hawkish reality of the summer, likely resulting in upward revisions to the projected year-end interest rate path 26.

The Resurgence of Sticky Inflation

To understand why the Fed is abandoning its plans for rate cuts, one must look at the recent trajectory of consumer prices. Throughout much of 2024 and 2025, the U.S. economy experienced a welcome period of "disinflation."

For consumers, it is vital to distinguish between disinflation and deflation. Deflation is a sustained drop in overall prices (negative inflation), which economists generally fear because it can lead to deferred consumer spending, shrinking corporate profits, and deep recessions 111213. Disinflation, on the other hand, means prices are still rising, but the rate of that increase is slowing down 1112. If inflation drops from 8% to 4%, the economy is experiencing disinflation 11.

The problem facing the Fed in June 2026 is that this disinflationary trend has stalled. Prices are no longer cooling off at an acceptable pace.

Analyzing the PCE and CPI Data

The Bureau of Economic Analysis reported that the Personal Consumption Expenditures (PCE) price index - the Fed's preferred inflation gauge - rose 3.8% year-over-year in April 2026 3014. The Consumer Price Index (CPI) similarly clocked in at 3.8% for April, marking its highest reading since May 2023 3215. Both metrics remain distressingly far from the Federal Reserve's mandated 2% target 22.

In the March SEP, Fed officials had projected that PCE inflation would settle around 2.7% by the end of 2026 241016. The April reading of 3.8% shatters those expectations, forcing policymakers to reconsider their models. Underlying inflation is also showing signs of persistence; while goods inflation has fluctuated, service-sector inflation - often driven by wages and housing costs - remains elevated 17.

The Strait of Hormuz and the Global Energy Shock

The primary culprit behind this renewed inflationary pressure is a massive negative supply shock stemming from geopolitical conflict. The ongoing war involving Iran has led to the closure of the Strait of Hormuz, the world's most critical energy chokepoint 1436. This disruption has sent global oil prices surging and scrambled global supply chains 237.

Prediction markets currently place the probability of the Strait reopening by the end of June at a mere 38%, indicating that the investing crowd views elevated energy costs as the central scenario for the foreseeable future, rather than a tail risk 14. While increased U.S. commercial oil exports and restrained Chinese demand have prevented a full-blown global energy crisis, the baseline cost of fuel has risen enough to bleed into the broader economy 14.

Central banks face a unique dilemma during an energy shock: they cannot print oil, nor can they directly lower the cost of imported commodities 1819. When an external supply shock drives up energy prices, the Fed's traditional tool of raising interest rates is relatively ineffective at addressing the root cause.

However, policymakers are acutely aware of the risk of "second-round effects." If businesses begin permanently raising the prices of their goods to cover higher transportation and fuel costs, and workers simultaneously demand higher wages to afford more expensive gasoline, a temporary supply shock can trigger a persistent wage-price spiral 1920.

The Hawkish Chorus Grows

Several Fed officials have already voiced concerns about these mounting risks. St. Louis Fed President Alberto Musalem recently warned that if disinflation does not resume in the next one to two quarters, a rate hike may be necessary, explicitly stating that risks have tilted more toward inflation than a weakening labor market 30. Fed Governor Lisa Cook echoed this sentiment, noting she is prepared to raise rates if price pressures do not ease in a timely manner 30.

Even traditionally dovish voices, such as Fed Vice Chair for Supervision Michelle Bowman, have conceded that if geopolitical disruptions persist well into the second half of 2026, it could force a shift in her approach to the balance of risks, nodding to the potential for a rate hike 20. Minneapolis Fed President Neel Kashkari has also warned that officials must pay attention to the risk that inflation expectations could become unanchored 20.

The Labor Market: Navigating Tenuous Resilience

While the Federal Reserve battles inflation on one front, it must monitor the health of the labor market on the other. The central bank operates under a dual mandate established by Congress: to ensure both stable prices and maximum employment 21.

Thus far in 2026, the U.S. labor market has exhibited a tenuous but undeniable resilience. The April Employment Situation report revealed the addition of 115,000 nonfarm payrolls 3222. While this figure nearly doubled the consensus forecast of roughly 62,000 to 65,000 jobs, it represented a deceleration from the 185,000 jobs added in March 2244.

The unemployment rate has remained stubbornly flat at 4.3% 2244. While higher than the extreme lows seen in previous years, 4.3% still points to a relatively healthy jobs market that has not yet succumbed to the crushing weight of higher borrowing costs.

Key US Labor Market Indicators (April vs. May 2026)

Ahead of the June FOMC meeting, policymakers will receive a critical piece of the puzzle: the May nonfarm payrolls report, scheduled for release by the Bureau of Labor Statistics on June 5 2244. The table below outlines the actual figures from April against the market consensus for May, highlighting the specific metrics the Fed will be watching.

| Economic Metric | April 2026 (Actual) | May 2026 (Market Consensus) | Implications for the Federal Reserve |

|---|---|---|---|

| Nonfarm Payrolls (NFP) | +115,000 | +85,000 to +96,000 | Slower growth indicates cooling demand, potentially easing the pressure to hike rates 2244. |

| Unemployment Rate | 4.3% | 4.2% to 4.3% | A stable rate suggests the labor market is loosening without collapsing into recession 2244. |

| Avg. Hourly Earnings (MoM) | +0.2% | +0.3% | Accelerating wage growth threatens to feed into service-sector inflation 2244. |

| Labor Force Participation | Softening | Continued softening expected | Fewer active workers can artificially keep unemployment low while constraining total economic output 22. |

If the May jobs report comes in significantly stronger than expected - particularly if average hourly earnings run hot and job creation exceeds 100,000 - it will validate the hawkish voices on the committee. A robust labor market gives the Fed cover to maintain "higher for longer" rates, or even hike them, to crush inflation 2244.

Conversely, if the labor market cracks - for example, if job growth plummets below 50,000 or turns negative, and the unemployment rate ticks up to 4.4% or higher - the market narrative will rapidly shift from inflation fears to recession anxieties 44. In that scenario, the Fed would face the nightmare scenario of stagflation: rising prices coupled with rising unemployment and stagnant growth 14.

The AI Paradox: Deflationary Miracle or Inflationary Catalyst?

A fascinating economic and philosophical debate is currently unfolding within the Federal Reserve regarding the macroeconomic impact of Artificial Intelligence (AI). This debate will fundamentally shape Kevin Warsh's tenure and the future path of interest rates.

Capital expenditure (CapEx) related to AI infrastructure - such as data centers, advanced semiconductors, and power generation - has exploded. Investment banks estimate that combined CapEx from the largest tech hyperscalers will reach $800 billion in 2026, up from previous estimates of $450 billion, and surpass $1.16 trillion by 2027 9.

Warsh's Productivity Optimism

Warsh has historically leaned into the optimistic view of technological advancement. He argues that AI could unleash a massive productivity boom in the United States 24. In economic terms, higher productivity means workers and systems produce more output per hour, which allows wages and corporate profits to grow without triggering inflation.

If AI acts as a structural deflationary force by streamlining operations, optimizing supply chains, and replacing costly labor, the Fed might be able to afford lower interest rates in the long run 4. Proponents of this view argue that the Fed should look past short-term inflation blips because the AI revolution will eventually push costs down organically .

The Demand Shock Reality

However, this view is heavily contested by other members of the FOMC and leading economists. Officials like Chicago Fed President Austan Goolsbee and Fed Governor Lisa Cook worry that in the short term, the AI boom is actually highly inflationary 30.

Building vast data centers requires immense amounts of electricity, copper, cooling equipment, and specialized construction labor - resources that are already strained by the geopolitical environment 914. Furthermore, the wealth effect created by soaring tech stocks can induce consumers to spend more 30.

Cook and Goolsbee argue that the immediate surge in corporate spending is layering a massive new demand shock on top of existing supply chain frictions. By front-loading hundreds of billions of dollars in infrastructure spending before the productivity gains are fully realized, the AI boom is competing for scarce resources and driving up prices today 30. If this view holds sway at the June meeting, the Fed will be highly reluctant to cut rates, fearing that cheaper capital would only throw more fuel on the AI spending fire.

Consumer Pain: The Mortgage Market Reacts

The realization that the Federal Reserve is unlikely to cut rates anytime soon has reverberated violently through consumer credit markets, most notably in housing. Borrowers who started 2026 with hopes of declining mortgage rates have been severely disappointed by the spring and summer reality 23.

The historical data over the first half of 2026 demonstrates a clear disconnect between the Federal Reserve's overnight policy rate and consumer borrowing costs. While the effective federal funds rate has remained constant at roughly 3.62%, the 10-year U.S. Treasury yield - which acts as the benchmark for long-term borrowing - climbed to approximately 4.45% in response to inflation shocks and deficit concerns. Consequently, average 30-year fixed mortgage rates were pulled sharply upward, rising from early-year lows of 5.75% to reach 6.53% by late May.

Mortgage rates do not directly mirror the federal funds rate; rather, they track the 10-year Treasury yield, which fluctuates based on investor expectations about future economic growth, inflation, and global risk 2425. When inflation spiked in April due to the Middle East conflict, bond investors demanded higher yields to compensate for the eroded purchasing power of their future returns. This immediately translated into more expensive home loans 3724.

Institutional Forecasts for 2026 - 2027 Housing

Loan officers note that the jump back into the mid-6% range has visibly slowed mortgage applications and shifted buyer psychology 37. Unfortunately for prospective homebuyers, major housing finance institutions project that mortgage rates will remain elevated for the foreseeable future.

- Mortgage Bankers Association (MBA): Forecasts that rates will average roughly 6.40% over the next 12 months, driven by sticky inflation that keeps secondary market yields high 36.

- Fannie Mae: Slightly more optimistic, forecasting an average of 6.30%, though they note that elevated energy prices from the Strait of Hormuz closure will continue to apply upward pressure 3624.

- Wells Fargo Economics: Projects an average of 6.17%, citing a "conflict premium" that is currently driving up the 10-year Treasury yield 36.

For consumers looking to buy a home or refinance between June 2026 and May 2027, the implication is clear: the era of 3% or 4% mortgages is firmly in the rearview mirror. Waiting on the sidelines for a sudden Fed rescue is a risky strategy, particularly as a sudden drop in rates could unleash pent-up demand and trigger intense bidding wars that push underlying home prices even higher 3649.

Global Spillovers: A World Held Hostage by U.S. Rates

The Federal Reserve's inability to lower interest rates is exporting economic strain across the globe. Because the U.S. dollar is the world's primary reserve currency, high U.S. interest rates attract global capital seeking yield, which strengthens the dollar at the expense of foreign currencies 50. This dynamic forces other central banks to make uncomfortable, often damaging choices to defend their own economies.

The European Central Bank's Defensive Stance

Unlike the United States, Europe is grappling with incredibly fragile economic growth. Earlier in the year, the European Central Bank (ECB) was widely expected to cut rates to stimulate its sluggish member economies. However, the energy shock from the Middle East hits Europe particularly hard due to its reliance on imported fuel.

Consequently, ECB policymakers are now signaling a likely rate hike in June 2627. Observers characterize this as an "insurance hike" designed to anchor inflation expectations and prevent imported energy costs from sparking a wage-price spiral 28. ECB President Christine Lagarde faces the unenviable task of tightening monetary conditions to fight inflation, even if it risks suffocating the continent's meager economic recovery 528. Across the channel, the Bank of England is maintaining a wait-and-see approach, with Governor Andrew Bailey signaling no rush to raise rates but acknowledging that cuts are likely off the table for the summer 26.

The Bank of Japan and the Yen's Critical Defense

The situation in Japan is arguably the most dramatic consequence of U.S. monetary policy. Japan has historically maintained ultra-low or negative interest rates to combat decades of domestic deflation 1429. However, the massive, persistent gap between U.S. rates (3.50%+) and Japanese rates has caused the Yen to plummet in value against the dollar, crossing the psychologically critical 160 Yen per dollar threshold in the spring of 2026 1455.

A weak Yen makes importing energy and food prohibitively expensive for Japan, crushing domestic consumers 55. In response, the Japanese Ministry of Finance is believed to have spent roughly 10 trillion Yen (approximately $63 billion) in April and May directly intervening in foreign exchange markets to artificially prop up the currency 5530.

Currency intervention, however, is a temporary bandage. To truly stop the bleeding and close the yield gap with the U.S., the Bank of Japan (BoJ) must raise its own interest rates. Swap markets currently price in a nearly 80% chance that the BoJ will hike rates at its own June 16 meeting 14. If Japan tightens monetary policy aggressively to defend the Yen, it risks stalling its fragile transition toward a normal, growing economy and dramatically inflating the cost of servicing its massive public debt burden 55.

Emerging Markets and Structural Warnings

The broader global picture reflects these localized struggles. The International Monetary Fund (IMF) and the World Bank have repeatedly warned that the combination of geopolitical fragmentation, unpredictable trade tariffs, and stubbornly high interest rates in the U.S. is creating a highly precarious environment for emerging markets 1931.

While the resilience of the U.S. economy has kept global growth afloat - projected by the IMF at roughly 3.3% for 2026 - the structural frictions preventing capital flow to developing nations remain severe 31. High U.S. rates draw investment away from emerging markets, increasing their debt servicing costs. The World Bank recently warned that, despite pockets of resilience, the 2020s are shaping up to be the weakest decade for global growth since the 1960s .

Bottom line

The June 2026 FOMC meeting marks a critical juncture for the U.S. economy and global financial markets. Chairman Kevin Warsh will almost certainly lead the committee to hold rates steady at 3.50% to 3.75%, bowing to the reality that energy shocks and an AI-driven capital expenditure boom have stalled disinflation. While the immediate policy rate will remain unchanged, investors must navigate a new era of Fed communication with less forward guidance, elevated mortgage costs, and the growing, uncertain risk that the central bank's next move may be a rate hike rather than a cut.