Who Qualifies for Employer GLP-1 Coverage in 2026

Direct Answer and Bottom-Line Summary

The landscape for employer-sponsored coverage of Glucagon-Like Peptide-1 (GLP-1) receptor agonists has fundamentally shifted as we progress through the 2026 plan year. Initially heralded as a universal, silver-bullet solution to the obesity epidemic, medications such as Wegovy, Zepbound, and Ozempic have subsequently created an unprecedented financial challenge for employer-sponsored health plans. The direct answer to whether employer-sponsored insurance will cover these medications is highly conditional: while nearly all health plans universally cover GLP-1 medications for the treatment of Type 2 diabetes, coverage for chronic weight management and obesity is increasingly subject to intense utilization management, strict clinical prerequisites, and emerging cost-containment strategies such as lifetime financial caps and mandatory lifestyle interventions.

The bottom line for the 2026 benefit enrollment period is that the era of unmitigated, "open access" to weight-loss injectables has permanently closed. Employers are caught between record-high demand from their workforce and staggering premium impacts that threaten the financial viability of their broader benefit offerings. Consequently, everyday employees are experiencing significant out-of-pocket sticker shock and navigating complex human resources (HR) and pharmacy benefit manager (PBM) red tape. Successfully accessing GLP-1 therapy today requires beneficiaries to proactively decode their Summary of Benefits and Coverage (SBC) documents, engage in mandatory behavioral modification programs, and meticulously prepare detailed clinical documentation for rigorous prior authorization (PA) approvals. Benefit leaders are no longer asking if these drugs work; they are asking how to finance them sustainably while maintaining equitable access for the patient populations that stand to achieve the most significant clinical return on investment.

The 2024 - 2026 Trajectory: The Evolution of a Coverage Crisis

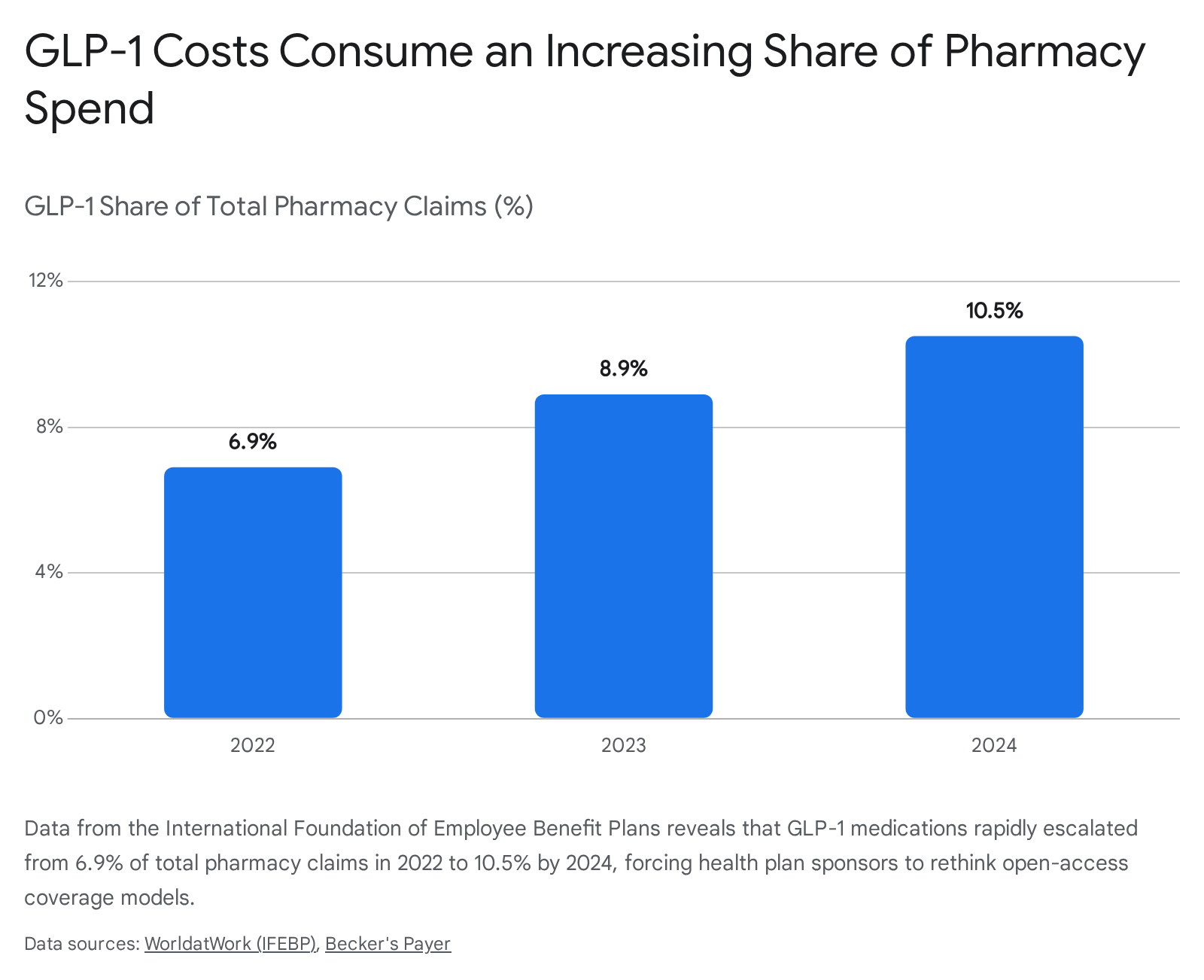

To accurately understand the restrictive 2026 benefit environment, it is necessary to analyze the explosive trajectory of GLP-1 utilization over the preceding three years. Historically, weight loss medications were inexpensive, largely ineffective, and highly marginalized within commercial insurance formularies 1. However, the introduction of highly effective GLP-1 receptor agonists entirely upended this paradigm.

In 2022, GLP-1s represented a relatively manageable 6.9% of total pharmacy claims for employer plans 23. This figure escalated at an unprecedented velocity. By 2023, as direct-to-consumer marketing intensified and clinical trial data confirmed monumental weight-loss efficacy, that number grew to 8.9% 3. In 2024, the situation reached a critical inflection point, with GLP-1 therapies consuming 10.5% of total annual insurance claims across the commercial market 23.

For over a quarter of the largest corporate employers, these medications came to account for more than 15% of their entire annual pharmacy spend 234.

During this initial boom period, coverage expanded rapidly as employers sought to remain competitive in tight labor markets and responded to immense employee pressure. Research from Mercer indicated that in 2024, 44% of employers with 500 or more employees offered coverage for obesity medications, up from 41% the prior year, while 64% of the largest companies (20,000+ employees) provided this benefit 56. By 2025, WTW (Willis Towers Watson) found that 57% of employers were covering GLP-1s for weight loss 7.

However, the underlying economic reality of covering a drug class that costs upwards of $12,000 to $15,000 per patient annually - for a clinical condition affecting over 42.4% of the U.S. adult workforce - proved mathematically unsustainable for many plan sponsors 8910. The net price for a 30-day supply of these medications, even after aggressive PBM rebate negotiations, ranges between $617 and $766 41112. With an estimated 57 million commercially insured adults eligible for these drugs based on BMI alone, the financial exposure is astronomical 410.

Simulations conducted by the Employee Benefit Research Institute (EBRI) revealed that widespread GLP-1 coverage could increase overall employer health insurance premiums anywhere from 5.3% to 13.8% depending on utilization rates 41214. Concurrently, total employer-sponsored health care costs are projected to rise by 6.7% in 2026, bringing the average annual cost per employee to nearly $18,500 1411. Employers were faced with the reality that they could not simply absorb these costs; they would eventually have to pass them down to the workforce via higher paycheck deductions, inflated deductibles, or reduced wage growth 1012.

Consequently, by 2026, the market entered a phase of aggressive recalibration. While the Business Group on Health (BGH) notes that 67% of surveyed employers still provide some form of weight management coverage, a distinct pullback is underway 1314. Approximately 10% to 15% of employers that previously covered these drugs are actively removing them or planning to drop coverage entirely by 2027 due to the absence of immediate return on investment (ROI) and severe premium inflation 71314. Furthermore, early data regarding long-term adherence presents a bleak picture for ROI: data from Prime Therapeutics demonstrates that only about 1 in 12 members remain on GLP-1 treatment after three years, meaning the vast majority of employer investment is lost when non-persistent employees regain the weight 51014.

The Great Divide: Type 2 Diabetes vs. Obesity Coverage

The fundamental architecture of 2026 pharmacy benefits is defined by a rigid demarcation between the treatment of Type 2 diabetes and the treatment of obesity. This divide is the primary source of employee confusion and frustration, as the exact same active pharmaceutical ingredients (e.g., semaglutide, tirzepatide) are treated entirely differently depending on the specific diagnostic code attached to the prescription by the provider 192021.

For Type 2 diabetes, GLP-1 medications like Ozempic, Mounjaro, and Rybelsus remain almost universally covered as an undisputed standard of care 11422. Health plans and employers explicitly recognize diabetes as a long-established, severely debilitating chronic disease where strict glycemic control is paramount to preventing catastrophic downstream medical events such as neuropathy, limb amputations, diabetic retinopathy, and renal failure.

Conversely, coverage for the obesity-specific formulations of these exact same drugs - such as Wegovy, Zepbound, and Saxenda - remains highly contested and philosophically divisive 192021. Despite the American Medical Association formally classifying obesity as a chronic disease in 2013, many health plan sponsors still view obesity interventions through the antiquated lens of "lifestyle conditions." A comprehensive survey by the Pharmaceutical Strategies Group (PSG) asked healthcare payers to rate their view of obesity medications on a scale from 1 (purely a lifestyle condition) to 10 (a chronic disease requiring pharmaceutical intervention). The average score hovered right in the middle at 5.4, underscoring the deep ambivalence within the industry 1.

Consequently, a dual reality exists within the same corporate workforce: an employer may fully cover Ozempic for a diabetic employee while systematically denying Wegovy for an obese employee, even if the latter suffers from pre-diabetes, severe metabolic syndrome, or cardiovascular risk 20. This divide places immense strain on the provider-patient relationship. Providers frequently attempt off-label prescribing - submitting an Ozempic prescription for a non-diabetic patient to secure coverage - which has triggered immense scrutiny from health plans. Over 75% of health plans report moderate to high concern regarding the off-label use of GLP-1s, prompting them to enforce draconian audits on diagnostic coding 1.

When employers make the financial decision to sever weight-loss coverage entirely, they force employees into precarious medical situations. If a patient was successfully managing their obesity and pre-diabetes on a GLP-1, the sudden loss of employer coverage effectively renders them uninsured for that life-altering therapy 2015. This triggers an abrupt halt to care, resulting in a highly probable, rapid regain of weight and a reversal of cardiovascular benefits 215. This clinical division highlights a profound debate in healthcare economics: whether to treat obesity proactively as the root cause of metabolic decline, or to wait until the patient's condition irreversibly progresses into Type 2 diabetes before authorizing pharmaceutical intervention 224.

Addressing Common Misconceptions

The rapid integration of GLP-1s into the cultural zeitgeist, fueled by celebrity endorsements, social media trends, and aggressive pharmaceutical advertising, has spawned several pervasive misconceptions. These myths continuously complicate HR communications and severely distort employee expectations heading into the 2026 Open Enrollment period. Clarifying these fallacies is essential for an objective understanding of the current benefit landscape.

Misconception 1: "FDA Approval Guarantees Insurance Coverage"

Perhaps the most prevalent and deeply rooted misconception among the general workforce is the belief that because the U.S. Food and Drug Administration (FDA) has explicitly approved drugs like Wegovy and Zepbound for chronic weight management, employer health plans are legally and ethically obligated to cover them 2116. This is fundamentally false.

In reality, the federal Employee Retirement Income Security Act (ERISA), which governs the vast majority of self-funded corporate health plans in the United States, does not mandate coverage for obesity medications 1120. Employers possess nearly absolute discretion in designing their pharmacy formularies and determining which drug classes to include or exclude based on budgetary constraints 16. Furthermore, the judicial system has consistently upheld the right of insurers and employers to exclude weight-loss drugs. Recent rulings, such as the February 2026 U.S. Court of Appeals for the First Circuit decision upholding an insurer's right to exclude weight-loss coverage, confirm that doing so does not violate the Americans with Disabilities Act (ADA) or constitute disability discrimination 202627. FDA approval simply validates that a drug is safe and clinically effective for a specific indication; it carries absolutely no mandate regarding financial reimbursement by private payers.

Misconception 2: "GLP-1s Are Merely Vanity Drugs"

Critics and hesitant plan sponsors frequently frame GLP-1s as cosmetic "vanity drugs" utilized by individuals seeking to shed a few aesthetic pounds 21. Clinical reality and FDA labeling strictly contradict this narrative. The clinical footprint of GLP-1s has expanded dramatically far beyond aesthetics.

According to FDA guidelines, these medications are indicated exclusively for individuals with a Body Mass Index (BMI) over 30, or a BMI over 27 accompanied by at least one severe weight-related comorbidity such as hypertension, dyslipidemia, or obstructive sleep apnea 82116. Dr. Kristin Baier, VP of clinical development at Calibrate, notes that treating obesity with GLP-1s is fundamentally disease prevention, actively lowering the risk of 13 types of cancer, liver disease, sleep apnea, and clinical depression 8. Furthermore, landmark clinical trials have led to FDA approvals for Wegovy to reduce the risk of major adverse cardiovascular events (heart attacks and strokes), and for the treatment of Metabolic Dysfunction-Associated Steatohepatitis (MASH), a severe liver disease 72617. These data points firmly solidify GLP-1s as critical, life-saving chronic disease interventions, not cosmetic aids.

Misconception 3: "Compounded 'Generic' Semaglutide is Safe and Equivalent"

Driven by the exorbitant out-of-pocket sticker shock of brand-name GLP-1s (often exceeding $1,000 a month), a massive secondary market has emerged. Many desperate employees have turned to medical spas, unregulated telehealth startups, and compounding pharmacies offering "generic," "natural," or "homeopathic" semaglutide at a fraction of the cost 212930.

A dangerous misconception is that these compounded products are identical in safety, quality, and efficacy to their FDA-approved counterparts. William Soliman, M.D., former pharma executive and founder of the Accreditation Council for Medical Affairs (ACMA), explicitly warns that compounded versions do not undergo the FDA's rigorous testing for standardized manufacturing and labeling 17. The FDA has issued multiple warnings regarding adverse events linked to dosing errors and unknown salt formulations in compounded vials, with some resulting in hospitalizations 1731. As a result, commercial employers systematically and rigorously exclude these unverified, compounded products from their benefit plans, enforcing strict adherence to standardized, manufacturer-packaged treatments to shield themselves from immense medical liability 1731. Data indicates that patients are aware of this; a 2026 Navitus survey showed that nearly 60% of users are aware of safety concerns tied to compounded GLP-1s, and 86% stated they would gladly pay more for an FDA-approved medication if given the choice 17.

Misconception 4: "Once You Start, You Can Never Stop"

There is a widespread belief that starting a GLP-1 commits a patient to a lifetime of weekly injections, with 100% of the weight returning the moment the drug is discontinued 831. While obesity is a chronic disease requiring long-term management, the idea of permanent pharmaceutical dependency is nuanced. Clinical experts point out that the greatest savings and most durable outcomes occur when individuals learn lasting lifestyle and behavior changes in parallel with taking the medication 2. Structured weaning programs, supported by intensive nutritional and behavioral therapy, are showing promise in helping certain patients maintain a significant portion of their weight loss post-medication, challenging the absolute notion of indefinite, lifelong administration 2832.

FAQ: Understanding the Everyday Employee Experience

To accurately frame the GLP-1 coverage issue, it is vital to shift focus to the everyday employee experience. The pursuit of GLP-1 therapy is currently characterized by intense operational friction, devastating out-of-pocket sticker shock, and labyrinthine HR red tape.

Why am I experiencing such severe out-of-pocket sticker shock?

The core reason for employee sticker shock is the intersection of high list prices and modern benefit design. Without employer coverage, the retail cash price of a GLP-1 medication ranges from $1,000 to $1,300 per month, an impossible sum for the average worker 5910. However, even when an employer plan does provide coverage, the pervasive shift toward High-Deductible Health Plans (HDHPs) means employees often bear the full brunt of the negotiated rate (typically $617 to $766) until their massive annual deductible is met 41112.

This financial burden has severe clinical consequences. Research indicates that high upfront cost-sharing directly reduces medication adherence. A recent study found that HDHP enrollment is associated with a 5% drop in adherence to cardiovascular risk medications 17. In the Navitus survey, 24% of GLP-1 users reported paying more than $250 out-of-pocket per prescription fill, while nearly 8% pay $500 or more 17. When employees face these costs, it leads to stop-and-start therapy; they take the drug when they can afford it and stop when they cannot. This intermittent usage diminishes clinical effectiveness, heightens the risk of adverse side effects, and ultimately wastes the employer's premium dollars, creating a scenario where nobody wins 217.

What is "Step Therapy," and why is my plan forcing me to take older medications?

To systematically control escalating costs, PBMs heavily utilize a utilization management mechanism known as step therapy. To understand step therapy, consider a real-world home repair analogy: If a homeowner discovers a minor leak under their sink, they do not immediately hire a luxury, high-end contractor to replace the entire plumbing system. They first try applying a low-cost sealant. If the sealant fails, they hire a basic, affordable plumber. Only if the basic plumber completely fails to resolve the issue do they escalate to the highest-cost, specialized plumbing service.

Similarly, in the pharmacy benefit world, step therapy requires a patient to actively try and formally "fail" on older, vastly less expensive weight-loss medications (such as oral Contrave, Qsymia, or Orlistat) before the health plan will unlock coverage for a premium, high-cost GLP-1 injectable 11123334. The Institute for Clinical and Economic Review (ICER) notes that while step therapy through non-GLP-1 obesity medications can be clinically reasonable for members with modest weight loss goals, it often serves as a bureaucratic delay mechanism 3418.

While step therapy successfully suppresses employer spending in the short term, it creates immense psychological frustration for the employee, who correctly views this operational friction as a deliberate barrier to receiving the most effective, modern standard of care 3418. Furthermore, when the processes are confusing or slow, it becomes a severe health equity issue. Employees with fewer financial resources, lower health literacy, or limited time to constantly call their PBM are disproportionately likely to abandon therapy altogether, feeling they are receiving "second-class care" compared to executives who can navigate the red tape or pay cash 3418.

Why is HR making me join a lifestyle or diet program just to get my medication?

A rapidly growing trend among employers - currently utilized by roughly 38% to 49% of those covering weight-loss drugs - is making GLP-1 coverage strictly contingent upon mandatory, ongoing participation in a structured behavioral modification or lifestyle program 14141633.

Benefit leaders and clinical directors recognize that GLP-1s are not magic; they are most effective, and weight loss is most durable, when chemically induced appetite suppression is paired with foundational dietary changes and increased physical activity 82131. By partnering with third-party behavioral health vendors (such as Noom, Virta Health, WeightWatchers, or Omada Health), employers ensure the medication acts as a physiological catalyst for holistic health improvement rather than a standalone crutch 21236.

The financial ROI on these integrated programs is substantial. For instance, Jennifer Jones, director of clinical solutions at Noom Health, noted that implementing structured step therapy and lifestyle program requirements dropped one employer group's annualized GLP-1 spend from $6.2 million to just $1.3 million 2. Every dollar invested in structured weight management programs generated a return of 4.2x 2. From a behavioral economics perspective, this requirement also functions as a gentle but effective deterrent; the added time commitment naturally filters out employees who are merely curious about the drug, reserving the expensive resource for those genuinely dedicated to long-term chronic condition management 1133.

How do I navigate the Prior Authorization (PA) appeals process?

If coverage exists, it will almost certainly be hidden behind a towering PA wall. If an initial PA is denied, or if an employee genuinely cannot tolerate the severe gastrointestinal side effects of a required step-therapy medication, they must utilize the plan's formal "exception pathway" 34.

Exception pathways are where plans theoretically prove that their utilization management is individualized rather than rigid 34. This process requires the physician to submit a formal, documented appeal stating exactly why the formulary alternative is medically contraindicated or has already failed. Persistence is absolutely crucial here; PBM systems are algorithmically designed to naturally suppress utilization through administrative friction 34. Successfully navigating appeals requires the employee to act as a relentless project manager, ensuring their doctor's office submits the correct clinical chart notes, lab results, and BMI histories on time.

The Employer Playbook: Emerging Cost-Containment Strategies and Guardrails

The immense economic strain of GLP-1s has forced employers, consulting partners (e.g., Mercer, Aon, WTW), and PBMs to innovate rapidly. To avoid the disastrous binary choice of either bankrupting the corporate health plan or alienating the entire workforce with total exclusions, organizations are deploying sophisticated "managed access" strategies 2633.

Elevating Clinical Thresholds Beyond the FDA Label: Instead of blindly adopting the FDA's baseline criteria (a BMI of 30, or 27 with a comorbidity), many sophisticated plans are elevating the eligibility threshold to artificially restrict the eligible population 1133. A large self-funded employer might legally require a baseline BMI of 35, 40, or higher, or mandate the presence of multiple severe, documented comorbidities 91011. For example, Fairview Health Services only offers GLP-1 weight loss coverage to employees with a BMI of 40 or above 10. This strategy effectively triages the costly medication to the highest-risk populations who stand to gain the most significant cardiovascular and metabolic benefits, filtering out lower-risk uses and protecting the plan's financial stability 918.

Implementing Lifetime and Annual Financial Caps: One of the most controversial, yet increasingly prevalent, strategies in 2026 is the imposition of strict dollar amount or duration limits. Unlike standard maintenance medications for blood pressure or cholesterol, which are covered indefinitely, some employers are structuring GLP-1 benefits with a definitive expiration date 111237.

For instance, the Mayo Clinic instituted a strict lifetime cap of $20,000 per person for weight-loss medications 10. Other employers opt for duration limits, such as a maximum of 12 or 24 months of total coverage 937. The rationale is highly financial: it caps the employer's ultimate financial liability, transforming an infinite, recurring cost into a predictable, mathematically bounded expense 91237. It also psychologically frames the medication as a temporary metabolic "reset" rather than a lifelong dependency 9. However, clinical experts vehemently push back against this strategy. Obesity is biologically a chronic condition, and terminating GLP-1 therapy generally results in rapid weight regain, potentially negating all clinical gains and rendering the employer's initial $20,000 investment entirely wasted 291518.

Alternative Funding and Direct-to-Consumer Models: Employers are also exploring alternative funding solutions to bypass the opaque markups of traditional PBMs. By establishing direct partnerships with Direct-to-Consumer (DTC) telehealth platforms (like Ro) or utilizing manufacturer-direct channels (like LillyDirect or NovoCare), employers can facilitate access to these medications at heavily discounted cash prices 12121319. Furthermore, some employers are implementing targeted Health Reimbursement Arrangements (HRAs), allowing employees to use pre-tax employer funds to purchase the drugs on the retail market, maintaining a strict budgetary ceiling for the employer while completely removing the liability from the core medical plan 11.

Comparative Analysis of 2026 Coverage Models

To summarize the varying degrees of access currently prevalent in the market, the following table outlines the three dominant coverage archetypes utilized by corporate health plans in 2026:

| Coverage Model | Core Characteristics | Employer Financial Impact | Employee Experience |

|---|---|---|---|

| Diabetes-Only Exclusion | Covers GLP-1s strictly for FDA-approved Type 2 Diabetes diagnostic codes. Complete exclusion for any obesity or weight management indication. | Highly controlled, stable, and predictable. Successfully avoids the massive 5-13% premium spikes associated with widespread obesity coverage. | Extremely high frustration for obese and pre-diabetic employees. Forces out-of-pocket cash payments of $1,000+/month, leading to therapy abandonment. |

| Managed Access with Clinical Guardrails | Covers obesity indications but requires intense Prior Authorization, elevated BMI thresholds (> 35), step therapy, and mandatory lifestyle coaching participation. | Moderate and sustainable. Mitigates run-away costs by naturally suppressing utilization through friction and ensuring ROI through better adherence and lifestyle change. | Heavy administrative "red tape." Employees must actively navigate complex approvals, fail older drugs, and log diet/exercise metrics to maintain prescriptions. |

| Capped / Tiered Financial Benefit | Broad initial access for obesity but introduces a strict lifetime dollar cap (e.g., $15,000 to $20,000) or duration cap (e.g., 12 to 24 months), paired with high co-insurance. | Predictable maximum exposure per employee. Shifts the significant long-term financial burden directly to the workforce over time. | Initial relief followed by a devastating financial "cliff." Employees face total loss of coverage once the cap is reached, risking immediate and total weight regain. |

Geographic and Industry Context: The Lottery of Coverage

The likelihood of an employee receiving GLP-1 coverage in 2026 is not determined by clinical need, but rather by the geographic location of their residence and the specific macroeconomic sector in which they work. It is a literal lottery of coverage.

The State Mandate vs. Public Funding Paradox

A fascinating and deeply contradictory dichotomy exists in the regulatory environment between the public and private sectors.

On one hand, progressive state legislatures are aggressively pushing individual and fully-insured group health plans to cover anti-obesity medications. In 2025, North Dakota became the first state to mandate commercial insurance coverage for GLP-1s by adding them to the state Essential Health Benefit (EHB) benchmark plan 2720. California rapidly followed suit with AB 575, directing plans to cover outpatient anti-obesity medications and behavioral therapy 2021. Colorado and Connecticut also passed laws expanding commercial or state-employee access 20. For fully-insured employers in these states, the decision to cover GLP-1s has been legally forced upon them 1627.

Conversely, the public sector itself is collapsing under the immense financial weight of these exact identical drug costs. Faced with spiraling budget deficits and surging Medicaid utilization (which grew from $1 billion in 2019 to nearly $9 billion in 2024), massive public payers are aggressively restricting or entirely terminating GLP-1 weight-loss coverage for low-income populations 2223. State Medicaid programs in New Hampshire, Pennsylvania, Rhode Island, and South Carolina have entirely dropped coverage for weight loss 2223. Michigan restricted access strictly to the morbidly obese (BMI > 40) 2223. Most notably, California Governor Gavin Newsom proposed eliminating Wegovy and Ozempic weight-loss coverage from Medi-Cal to save the state an estimated $85 million in 2025-26, and up to $680 million by 2028-29 15.

This creates a deeply fractured, inequitable landscape where a corporate employee with a fully-insured plan in California is legally guaranteed access to Wegovy via state mandates, while a low-income resident across the street on Medi-Cal is abruptly cut off from the exact same life-saving medication 1521.

Industry Disparities: Tech Giants vs. Retail Operators

Coverage likelihood also varies drastically by employer size, profit margin, and industry sector. Large, self-funded corporations - particularly in the high-margin technology, consulting, and financial sectors - treat comprehensive health benefits as vital talent attraction and retention tools 122233. These massive entities (employing 5,000+ to 20,000+ workers) possess the deep capital reserves and sophisticated PBM contracting leverage necessary to absorb and actively manage GLP-1 costs 1233. Consequently, coverage rates in these cohorts hover near a robust 64% to 69% 36.

Conversely, smaller, fully-insured businesses, or large employers operating in low-margin, high-turnover industries like retail, hospitality, and manufacturing, are fundamentally incapable of absorbing a 5% to 10% annual premium hike for a single drug class 1133. For these employers, the ROI math simply does not align. While a GLP-1 might prevent a costly heart attack ten years in the future, the high turnover rate in retail means that long-term cardiovascular savings will likely benefit a completely different, future employer 51333. Therefore, for employers with transient workforces, excluding GLP-1s is viewed as an act of financial self-preservation.

Practical Takeaways: Navigating Open Enrollment and Prior Authorizations

For employees approaching the 2026 Open Enrollment period or attempting to initiate therapy, understanding the bureaucratic mechanics of employer-sponsored coverage is essential to avoid lengthy delays and financial distress. The following actionable steps are critical:

1. Aggressively Scrutinize the Summary of Benefits and Coverage (SBC): During Open Enrollment, employees must not assume that a generally "good" or "expensive" health plan automatically includes obesity care. Beneficiaries must actively request and read the fine print of the SBC and the plan's specific 2026 drug formulary 19. Employees should look for explicit, named exclusions regarding "weight loss," "anti-obesity medications," or "chronic weight management." If the literature is vague, employees must contact HR or the insurance provider's member services prior to locking in their plan to ask a direct, unambiguous question: "Does this specific plan tier cover GLP-1 receptor agonists specifically for the diagnosis of obesity, or is coverage strictly limited to Type 2 Diabetes?" 1929.

2. Maximize FSA and HSA Tax-Advantaged Eligibility: Even if an employer strictly excludes GLP-1s from the pharmacy benefit, employees can leverage tax-advantaged accounts to significantly soften the blow of out-of-pocket cash payments. Under Internal Revenue Service (IRS) guidelines, GLP-1 medications qualify as eligible medical expenses for Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) provided they are formally prescribed to treat a diagnosed disease such as obesity, diabetes, or heart disease 111926. Securing a formal Letter of Medical Necessity (LMN) from a prescribing physician is highly recommended to ensure strict compliance during any potential tax audits 11.

3. Meticulously Prepare Documentation for Prior Authorization (PA): If coverage exists, it will be heavily guarded by a PA requirement. Employees must act as their own assertive project managers in the clinical process. Before the doctor submits the electronic prescription to the pharmacy, the patient should ensure their medical chart is fully updated and explicitly documents: * An up-to-date, accurate BMI calculation (ensuring it mathematically meets the plan's specific elevated threshold, whether > 30 or > 35) 92129. * Detailed clinical notes verifying any qualifying comorbidities (e.g., hypertension, dyslipidemia, pre-diabetes, sleep apnea) 92129. * A heavily documented history of previous, unsuccessful weight-loss attempts or completion of required step therapy protocols involving lower-cost medications 122216.

4. Explore Manufacturer Rebates and Alternative Retail Channels: If all employer-sponsored channels are exhausted, or if the employee is stuck in the deductible phase of an HDHP, they should look toward the pharmaceutical manufacturers themselves. Both Novo Nordisk and Eli Lilly offer robust Patient Assistance Programs (PAPs) and manufacturer copay savings cards that can significantly reduce out-of-pocket retail cash prices for eligible, commercially insured patients 92019. Additionally, the advent of Direct-to-Consumer telehealth platforms launched directly by manufacturers (such as LillyDirect) or massive retail partnerships (like Costco's weight loss program) provides streamlined access to cash-pay options that frequently bypass traditional retail pharmacy markups entirely 121119.

Conclusion: The Horizon of GLP-1 Benefits

The 2026 employer-sponsored GLP-1 landscape represents a monumental paradigm shift in how corporate America interacts with population health, chronic disease management, and pharmacy benefit economics. The narrative has evolved far beyond a simplistic debate over cosmetic weight loss; it is now an intricate, high-stakes financial and clinical calculation involving downstream medical savings, employee retention, health equity, and the severe legal constraints of ERISA and ADA compliance.

Looking forward, the commercial market will absolutely not return to the unbridled "open access" days of early 2023. Instead, the future will be defined by highly structured, hyper-managed care. Employers will increasingly accept and treat obesity as a valid chronic disease, but they will demand objective, data-driven accountability from both the patient (via lifestyle programs) and the pharmaceutical industry (via outcomes-based contracting).

Relief for health plan budgets may eventually arrive via the pharmaceutical pipeline. As highly anticipated oral GLP-1 formulations like Eli Lilly's orforglipron approach FDA approval, and as genuine generic alternatives for older generation GLP-1s (like liraglutide/Victoza) finally enter the supply chain, pricing pressures may naturally ease through sheer market competition 571419. Until that time, however, benefit leaders will continue to rely on mandatory lifestyle integration, rigid step therapy, and stringent clinical guardrails to ensure that these revolutionary, yet fiercely expensive, medications are deployed exactly where they can generate the most durable, life-saving health outcomes.