How 2026 Medicare Changes Affect Insulin and GLP-1 Costs

In 2026, Medicare Part D introduces a strict $2,100 annual cap on out-of-pocket prescription drug spending and implements historic price negotiations for ten major brand-name medications. Additionally, a temporary federal program launching in July 2026 - the Medicare GLP-1 Bridge - will finally allow eligible beneficiaries to access certain weight-loss drugs for a flat $50 monthly copay. Meanwhile, insulin costs remain firmly capped at $35 per month, offering vital, ongoing financial relief for millions of seniors managing diabetes.

The New Financial Architecture of Part D

The 2026 plan year marks the full realization of the structural redesign of the Medicare Part D prescription drug benefit, initiated by the Inflation Reduction Act (IRA). For beneficiaries managing chronic conditions or utilizing specialty medications, the financial landscape is vastly more predictable, though the underlying economics for insurance plans have shifted dramatically.

How Does the $2,100 Out-of-Pocket Cap Actually Work?

Following the final elimination of the coverage gap (often referred to as the "donut hole") and the introduction of a $2,000 out-of-pocket cap in 2025, the spending limit is indexed to rise slightly in 2026. The new cap is set at $2,100 1212. This $100 increase reflects a statutory annual adjustment based on the percentage increase in average spending for covered Part D drugs 1.

The coverage phases for a standard 2026 Part D plan operate in three distinct stages:

- The Deductible Phase: The maximum allowable Part D deductible rises to $615 in 2026, up from $590 the previous year 121. Beneficiaries pay 100% of their covered medication costs out-of-pocket until this initial threshold is met.

- The Initial Coverage Phase: After the deductible is met, beneficiaries typically pay a 25% coinsurance (or a flat copay, depending on the plan's specific tier design) for covered drugs. During this phase, the financial burden is shared: the insurance plan covers 65%, drug manufacturers cover 10% via a mandatory discount program, and the Centers for Medicare & Medicaid Services (CMS) provides a 10% subsidy specifically on negotiated drugs 1.

- The Catastrophic Phase: Once a beneficiary's True Out-of-Pocket (TrOOP) spending hits the $2,100 limit, they enter the catastrophic phase. At this point, beneficiaries pay $0 for all covered prescription drugs for the remainder of the calendar year 123. In this phase, the financial liability shifts heavily to the insurers and manufacturers: plans cover 60% of drug costs, manufacturers cover 20%, and CMS covers the remaining 20% to 40% through government reinsurance 1236.

This hard cap applies universally to all Medicare beneficiaries with Part D prescription drug coverage, regardless of their income level. It encompasses deductibles, copayments, and coinsurance for covered drugs 7. However, it is vital to note what the cap excludes. It does not apply to monthly plan premiums, non-formulary drugs, or medications covered under Medicare Part B, such as certain physician-administered injectables or infused cancer therapeutics 7.

Why Are Prescription Drug Plans Changing Their Offerings?

The shift in catastrophic liability - forcing private Part D insurers to shoulder 60% of the costs, up from just 15% in the pre-IRA era - has fundamentally altered the economics of offering stand-alone Prescription Drug Plans (PDPs). Insurers are now exposed to significantly more financial risk for beneficiaries who take expensive specialty medications 4.

To mitigate the risk of extreme premium shocks for consumers, CMS implemented a voluntary Premium Stabilization Demonstration program. For 2026, CMS revised the parameters of this demonstration to reflect changing market conditions. The program limits year-over-year premium increases for participating plans to a maximum of $50 per month (an increase from the $35 limit in 2025) and provides a $10 per member per month uniform subsidy to the insurers from the federal government 456.

As a result of tighter profit margins and increased liability, the stand-alone PDP market has consolidated significantly. The total number of PDPs available nationwide dropped from 464 in 2025 to just 360 in 2026, marking the third consecutive year of market shrinkage 47. Major insurers like Elevance have exited the PDP market entirely, while others have scaled back their regional offerings to focus on more lucrative Medicare Advantage (MA-PD) markets 4.

Despite fewer choices, the aggressive bid negotiation tactics employed by CMS have kept consumer costs stable. CMS data indicates that the average monthly premium for a stand-alone Part D plan will actually decrease slightly, dropping from roughly $38.31 in 2025 to $34.50 in 2026 712. Furthermore, the 2026 national base beneficiary premium - the mathematical starting point used to calculate individual plan premiums - is set at $38.99 5613.

| Plan Type | 2025 Average Premium | 2026 Average Premium | Market Trend Notes |

|---|---|---|---|

| Stand-Alone PDP | ~$38.31 | ~$34.50 | Total available plans dropped from 464 to 360. Premium increases capped at $50/month max 4712. |

| Medicare Advantage (MA-PD) | ~$13.32 | ~$11.50 | Most enrollees continue to have access to plans with a $0 separate drug premium, utilizing federal rebate dollars to offset costs 4712. |

Table 1: Comparison of average monthly Medicare Part D premiums. Note that actual premiums vary widely by state and specific plan selection 4712.

The Medicare Prescription Payment Plan (M3P)

To help beneficiaries manage their out-of-pocket costs without experiencing severe cash-flow crises early in the year, 2026 marks the second operational year of the Medicare Prescription Payment Plan (M3P) 214.

Smoothing Out Costs Over the Year

The M3P is a voluntary, opt-in program designed to smooth out medication costs. It does not reduce a beneficiary's total drug expenses or save them money in the aggregate 141516. Instead, it amortizes out-of-pocket expenses across the calendar year. When a participating beneficiary fills a prescription at the pharmacy, they pay $0 at the counter. Their insurance plan then sends them a monthly bill, dividing their total accumulated out-of-pocket costs by the number of months remaining in the year 1516.

There are no late fees or interest charges associated with the M3P 16. Regardless of whether a beneficiary uses the payment plan, their total spending remains strictly bound by the $2,100 out-of-pocket cap 141516.

Auto-Renewal and Retroactive Enrollment

A significant administrative update for 2026 requires that Part D plans automatically renew the M3P enrollment for beneficiaries who opted into the program in 2025 141516818. However, there is a catch: this auto-renewal only applies if the beneficiary remains enrolled in the exact same plan benefit package 148. If a beneficiary switches Part D plans during the Fall Open Enrollment period, they will be automatically disenrolled from the payment program and must actively opt-in again with their new insurer 148.

For beneficiaries who experience a sudden, catastrophic health event early in the year and face an immediate, unaffordable pharmacy bill, the M3P allows for a retroactive election. If a patient requires an urgent fill that could jeopardize their life or health, they have a 72-hour window after the claim is adjudicated to opt into the M3P. The plan will then process the election retroactively and reimburse the patient for the upfront cost-sharing within 45 days, converting the expense into a monthly bill 818.

Insulin Costs Under the 2026 Rules

For the millions of Medicare beneficiaries managing diabetes, the pricing structure for insulin remains one of the most protected benefits in the program. The $35 monthly cap on covered insulin products continues unchanged in 2026 1392010.

This strict cap applies to a 30-day supply of any insulin covered by a beneficiary's Part D plan (such as pens and vials), as well as insulin administered via traditional pumps, which are covered under Medicare Part B as durable medical equipment 2010.

TrOOP Accounting and Deductible Exemptions

The most critical financial nuance regarding the insulin cap is how it interacts with the broader Part D benefit redesign - specifically the $615 deductible and the $2,100 catastrophic cap.

The $35 insulin copay is completely exempt from the Part D deductible 13910. Beneficiaries pay no more than $35 from the very first prescription fill of the year, even if they have not paid a single dollar toward their $615 general deductible.

Furthermore, every dollar spent on these $35 insulin copays does count directly toward the beneficiary's $2,100 True Out-of-Pocket (TrOOP) limit 10. If a beneficiary requires multiple types of covered insulin or expensive branded medications for other conditions, their steady $35 payments will incrementally push them closer to the catastrophic phase, after which their insulin - and all other covered drugs - will cost $0 for the rest of the year 22010.

The Medicare GLP-1 Bridge Program

The most heavily scrutinized Medicare development for 2026 surrounds glucagon-like peptide-1 (GLP-1) receptor agonists. These revolutionary medications have proven highly effective for weight loss, but their high list prices have put them out of reach for many seniors.

Why Does Medicare Historically Exclude Weight-Loss Drugs?

The barrier to GLP-1 access is statutory. The Medicare Modernization Act of 2003 explicitly prohibited Part D plans from covering any medication prescribed solely for "anorexia, weight loss, or weight gain" 22111225.

Until recently, Medicare beneficiaries could only obtain GLP-1s if they had a qualifying co-morbidity that bypassed the weight-loss exclusion. For instance, medications like Ozempic and Mounjaro are covered broadly (usually with prior authorization) because their primary FDA indication is for type 2 diabetes 222613. In 2024, the popular drug Wegovy gained Medicare coverage specifically for cardiovascular risk reduction in patients with established cardiovascular disease (defined as a prior heart attack, stroke, or symptomatic peripheral artery disease) 2226. Similarly, Zepbound became coverable for moderate-to-severe sleep apnea 22.

If a doctor prescribed Wegovy or Zepbound purely for obesity without one of these specific co-morbidities, Medicare was legally required to deny the claim 2226. Patient advocacy groups and medical associations have long pushed Congress to pass the Treat and Reduce Obesity Act to repeal this prohibition, but the legislation has remained stalled 28.

How the Temporary Bridge Operates

To circumvent this statutory roadblock without an act of Congress, CMS is launching the Medicare GLP-1 Bridge on July 1, 2026 2914153233. Utilizing Section 402 demonstration authority - which allows the Secretary of Health and Human Services to test new methods of payment and care delivery - the Bridge creates a separate, temporary pathway for beneficiaries to access weight-loss drugs 251416.

Under the Bridge program, eligible Part D beneficiaries will pay a flat, predictable $50 monthly copay for specific FDA-approved weight-loss medications 291415333536. Because the program operates entirely outside the standard Part D benefit structure, the financial accounting is entirely distinct from a beneficiary's normal drug coverage.

Financial Mechanics: What Counts Toward TrOOP?

The separation of the Bridge from standard Part D means that insurers bear zero financial risk for the drugs dispensed through this program 163717. Instead, CMS uses a single central processor (Humana) to manage prior authorizations, adjudicate claims, and pay pharmacies directly 1636371819.

CMS has negotiated a net price of $245 per monthly supply with participating pharmaceutical manufacturers 1228291620. When a patient fills their prescription, the pharmacy collects the $50 copay from the patient, and the central processor reimburses the pharmacy for the remaining cost (the Wholesale Acquisition Cost minus the $50 copay, plus a standard dispensing fee) 36.

This external structure has vital implications for the patient's out-of-pocket maximums: * No TrOOP Contribution: Neither the $50 patient copay nor the $245 net price paid by CMS counts toward the beneficiary's $2,100 true out-of-pocket (TrOOP) cap 151635372021. * No Deductible: The medications are entirely exempt from the standard $615 Part D deductible 15. * No Extra Help Overlap: Low-Income Subsidy (LIS) beneficiaries do not receive additional cost-sharing reductions on the $50 copay. It remains a flat $50 for all qualifying participants, which may pose an affordability barrier for the poorest seniors 153517.

Strict Clinical Eligibility Requirements

The Bridge program does not cover all GLP-1s. It is strictly limited to formulations indicated for chronic weight management. Currently, the eligible drugs are Wegovy (semaglutide injection and tablets), Zepbound (tirzepatide, strictly the KwikPen formulation, excluding single-dose vials), and Foundayo (an oral formulation) 1112261333.

Medications like Ozempic and Mounjaro are intentionally excluded from the Bridge. Because their primary FDA indication is for type 2 diabetes, they remain eligible for standard Part D coverage, and beneficiaries must obtain them through their regular insurance formulary 131720.

Beneficiaries do not automatically qualify for the Bridge simply by being on Medicare. A medical provider must submit a prior authorization request directly to the CMS central processor (not the patient's insurance plan) proving the patient is enrolled in a qualifying Part D plan and met specific clinical criteria at the initiation of their GLP-1 therapy 2932331822.

| Baseline BMI Requirement | Additional Required Diagnoses to Qualify for the Bridge |

|---|---|

| BMI of 35 or higher | None required. Obesity alone qualifies the patient 121332331820. |

| BMI of 30 to 34.9 | Must have at least one of the following: Heart failure with preserved ejection fraction, uncontrolled hypertension (on 2+ medications), or chronic kidney disease (Stage 3a or higher) 13321820. |

| BMI of 27 to 29.9 | Must have at least one of the following: Pre-diabetes, previous myocardial infarction, previous stroke, or symptomatic peripheral artery disease 13331820. |

Table 2: Clinical eligibility criteria for the Medicare GLP-1 Bridge program launching July 1, 2026. Note that providers must also attest that the medication is accompanied by structured lifestyle and nutritional modifications 121320.

Crucially, patients whose primary diagnoses include type 2 diabetes, obstructive sleep apnea, or noncirrhotic metabolic dysfunction-associated steatohepatitis (MASH) are entirely ineligible for the Bridge program, even if they meet the BMI requirements 20. CMS requires these patients to seek coverage through their standard Part D plans, utilizing the statutory carve-outs that already exist for those specific conditions 1720.

The Delay of the BALANCE Model

The GLP-1 Bridge was originally conceived as a brief, six-month stopgap, scheduled to end on December 31, 2026. Its purpose was to provide immediate access while a permanent, integrated solution - the BALANCE (Better Approaches to Lifestyle and Nutrition for Comprehensive hEalth) Model - prepared to launch in January 2027 12331723.

The Original Long-Term Plan

The BALANCE Model is a highly ambitious initiative developed by the Center for Medicare and Medicaid Innovation (CMMI) under Section 1115A authority. This authority allows CMS to test service delivery models that improve care quality while reducing or maintaining program expenditures 1224.

The model was designed to integrate GLP-1 coverage directly into standard Medicare Part D and state Medicaid programs. Under BALANCE, CMS would negotiate directly with drug manufacturers to secure deep supplemental rebates. In exchange, participating insurance plans would be required to cover the medications and pair them with evidence-based behavioral and lifestyle interventions 37232425. The thesis was that treating obesity as a root cause would reduce downstream healthcare utilization (e.g., fewer heart attacks and knee replacements), thereby maintaining overall cost neutrality for the Medicare system 2324.

Why Major Insurers Backed Out

Participation in the BALANCE Model was strictly voluntary for drug manufacturers, state Medicaid agencies, and Medicare Part D plans 172326. For the model to move forward in the Medicare market, CMMI required a "critical mass" of participation from Part D sponsors - specifically, enough plans to cover 80% of eligible beneficiaries 3726.

However, the April 20, 2026, deadline for Part D sponsors to commit to the model passed without meeting this threshold. Two of the largest health insurers in the nation, UnitedHealthcare and Aetna, refused to opt in 2728.

The hesitation from major insurers was largely financial. Under the newly re-architected Part D benefit, insurers are responsible for 60% of catastrophic drug costs. Integrating high-cost, high-demand GLP-1 medications into their standard formularies presented an enormous financial risk, even with the promise of CMS-negotiated rebates 127. Without the participation of sponsors covering millions of enrollees, CMS was forced to announce an indefinite delay of the Medicare portion of the BALANCE Model, pushing potential implementation to 2028 or later 1719262729.

Extending the Bridge and Advancing Medicaid

To prevent millions of seniors from losing access, CMS immediately extended the temporary GLP-1 Bridge program through December 31, 2027 17192629. This 18-month extension ensures beneficiaries can continue utilizing the $50 copay structure while CMS collects real-world data on GLP-1 utilization and costs to reassure hesitant insurers 192326.

While the Medicare integration stalled, the Medicaid portion of the BALANCE Model is proceeding as planned. Because state Medicaid programs bear different financial risks and are structurally distinct from private Part D insurers, states are adopting the model on a rolling basis. State Medicaid agencies have until July 31, 2026, to apply, and can launch the model for their populations at any point between May 2026 and January 2027 192324262729.

TrumpRx and Cash-Pay Alternatives

Operating parallel to Medicare's specific benefit channels is a new federal direct-to-consumer platform launched in early 2026: TrumpRx.gov. While not a Medicare program itself, it offers a vital alternative for seniors who fail to meet the strict BMI or co-morbidity requirements of the GLP-1 Bridge.

The Most-Favored-Nation Executive Order

The pricing on TrumpRx is driven by a series of "Most-Favored-Nation" (MFN) agreements secured by the Trump administration. An Executive Order signed on May 12, 2025, directed the Department of Health and Human Services to tie U.S. drug prices to international benchmarks, ensuring Americans pay no more than the lowest price offered in comparable nations within the Organisation for Economic Co-operation and Development (OECD) 13031533233.

By threatening tariffs and regulatory action against non-compliant manufacturers, the administration reached voluntary agreements with 17 major pharmaceutical companies 1323334. These agreements force manufacturers to offer their drugs at MFN prices directly to consumers via the TrumpRx platform, bypassing traditional pharmacy benefit managers entirely 2553333536.

Impact on Medicare Beneficiaries

TrumpRx.gov does not sell medications itself; rather, it acts as a portal connecting patients to manufacturer-run direct-to-consumer programs (such as LillyDirect or NovoCare) or approved mail-order pharmacies 283637. The platform offers steep discounts on drugs commonly excluded by insurance, including in-vitro fertilization therapies, migraine medications, and crucially, GLP-1 weight-loss drugs 343560.

Through TrumpRx, the cash price for GLP-1s drops dramatically. Ozempic and Wegovy are available for roughly $350 per month (down from list prices exceeding $1,000). Zepbound falls to approximately $299 to $346 per month depending on dosage 2528353660. Furthermore, future oral GLP-1s currently under FDA review are expected to launch on the platform at roughly $149 per month 2835.

For a Medicare beneficiary, this presents a unique choice. If they qualify for the GLP-1 Bridge, they will pay just $50 a month 3336. However, if their BMI is 28 but they have no other qualifying co-morbidities, Medicare will deny them coverage 3320. In this scenario, TrumpRx serves as a fallback, allowing them to purchase the drug for $350 cash. However, because these purchases bypass insurance completely, none of the money spent through TrumpRx will count toward a beneficiary's $2,100 Part D TrOOP cap 2536.

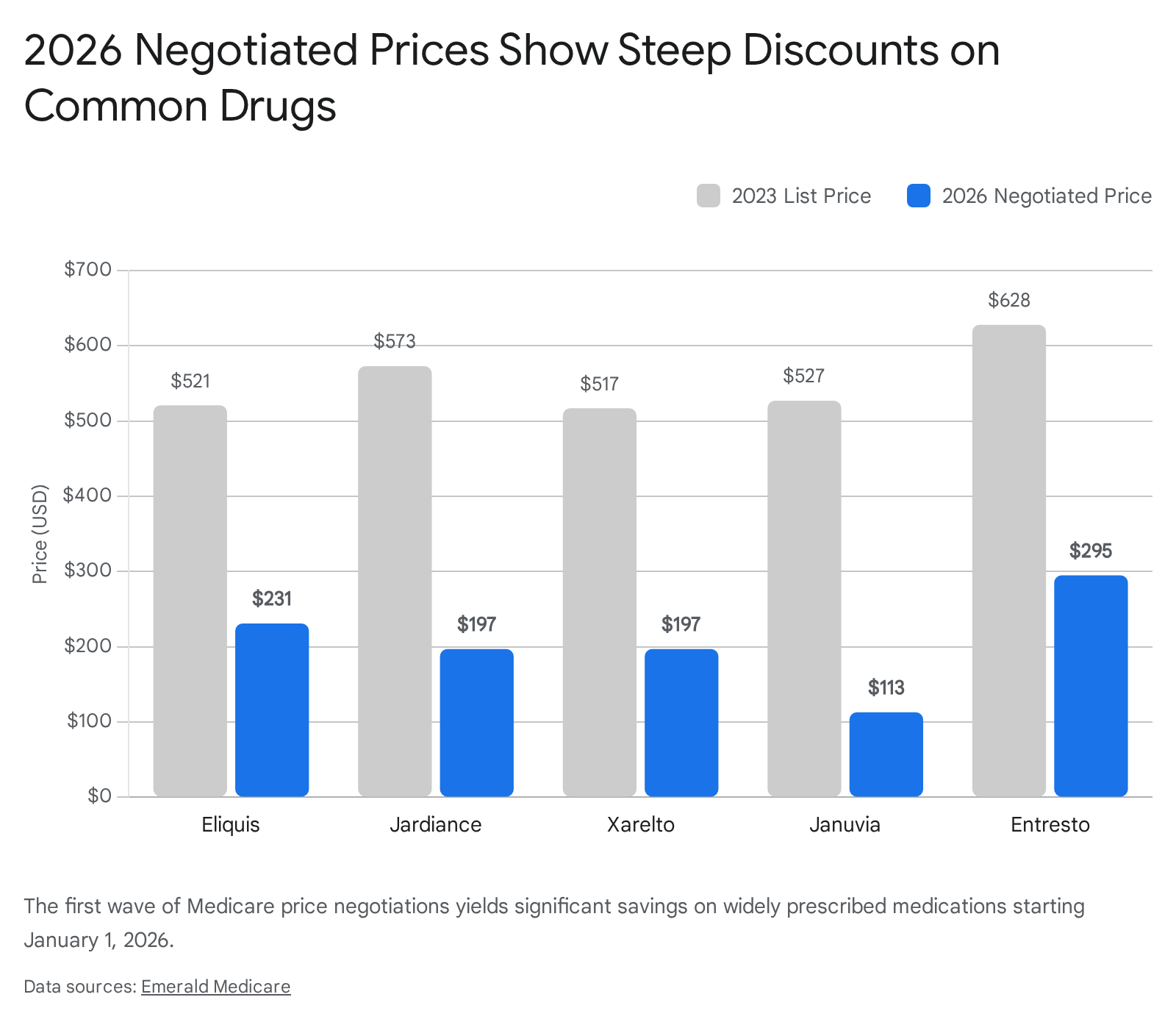

Historic Negotiated Drug Prices Take Effect

Beyond weight-loss and insulin, January 1, 2026, marks a watershed moment in the broader Medicare landscape: the first ten prescription drugs negotiated directly by CMS under the Inflation Reduction Act reach their new Maximum Fair Prices 13839.

The First Ten Drugs Selected

These ten medications were selected by CMS because they accounted for a massive portion of gross Medicare spending - nearly $46.4 billion (19% of all Part D spending) in 2022 alone - and lacked genuine generic or biosimilar competition in the market 3840.

The resulting negotiations yielded discounts ranging from 38% to 79% off the drugs' 2023 list prices 383941.

The ten medications span treatments for serious chronic illnesses, including diabetes, blood clots, heart failure, and autoimmune conditions.

| Drug Name | Primary Indications | 2023 List Price | 2026 Negotiated Price | Est. Discount |

|---|---|---|---|---|

| Januvia | Type 2 Diabetes | ~$527 | ~$113 | ~79% |

| Fiasp / NovoLog | Diabetes (Insulin) | ~$495 | ~$119 | ~76% |

| Farxiga | Diabetes, Heart Failure, CKD | ~$556 | ~$178.50 | ~68% |

| Enbrel | Autoimmune (RA, Psoriasis) | ~$7,106 | ~$2,355 | ~67% |

| Jardiance | Diabetes, Heart Failure, CKD | ~$573 | ~$197 | ~66% |

| Stelara | Autoimmune (Psoriasis, Crohn's) | ~$13,836 | ~$4,695 | ~66% |

| Xarelto | Blood Clot Prevention | ~$517 | ~$197 | ~62% |

| Eliquis | Blood Clot Prevention | ~$521 | ~$231 | ~56% |

| Entresto | Heart Failure | ~$628 | ~$295 | ~53% |

| Imbruvica | Blood Cancers | ~$14,934 | ~$9,319 | ~38% |

Table 3: The first ten drugs subject to Medicare price negotiation, effective January 1, 2026 38404142.

How Reduced List Prices Lower Copays

The implications of these negotiated prices extend far beyond aggregate government savings. The direct benefit to the patient is profound because of how Medicare Part D coinsurance functions.

During the initial coverage phase (before a patient hits the catastrophic cap), beneficiaries typically pay a 25% coinsurance rate for expensive brand-name drugs 139. A drastically lower list price immediately results in a proportionally lower copay at the pharmacy counter. For example, a 25% coinsurance on a $500 drug is $125; the same coinsurance on the new negotiated price of $200 is just $50 394243.

CMS estimates that this dynamic will save the nearly 9 million Medicare enrollees who take these drugs approximately $1.5 billion in out-of-pocket costs in 2026 alone, while simultaneously generating $6 billion in savings for the Medicare program itself 1383941. Moving forward, maximum fair prices for 15 additional Part D drugs (which are expected to include blockbuster GLP-1s like Ozempic) are currently being negotiated in 2025 and will take effect in 2027 36173841.

Bottom line

In 2026, the financial exposure for seniors with high pharmaceutical needs is drastically curtailed by a strict $2,100 out-of-pocket cap, enduring $35 insulin caps, and massive list-price reductions on ten widely used brand-name drugs. The landscape for weight-loss medications is finally opening up with the July 2026 launch of the GLP-1 Bridge program offering a flat $50 copay for Wegovy and Zepbound. However, because the Bridge program operates entirely outside standard Part D coverage, beneficiaries must understand that these $50 payments will not count toward their annual TrOOP limit, and the long-term future of Medicare GLP-1 coverage remains uncertain following the delay of the permanent BALANCE model.