What Studies Show About Solo vs Co-founded Startups

Direct Answer: Extensive startup outcome studies reveal a compelling paradox: while venture capital unequivocally favors co-founded teams - awarding them the vast majority of funding - solo founders frequently demonstrate higher long-term survival rates and generate more revenue in for-profit ventures. Recent 2024 and 2025 data indicates that the proportion of solo-founded startups is surging beyond 36%, driven by AI productivity multipliers and a strategic desire to avoid co-founder conflict, which remains the leading cause of early-stage startup failure.

Bottom Line: Co-founding teams raise significantly more capital and benefit from shared emotional burdens, making them ideal for highly capital-intensive sectors. However, they suffer from high internal friction and slower decision-making. Solo founders, conversely, retain substantially more equity and execute with unmatched velocity. By leveraging a network of "co-creators" rather than formal co-founders, single founders can bridge skill gaps while maintaining strategic control, though they face critically higher risks of severe burnout and professional isolation.

Introduction

Consider the agonizing, circular twenty-minute debate over where a group of friends should go for dinner: competing preferences, silent compromises, and the ultimate settlement on a mediocre venue just to end the discussion. Now multiply those stakes by millions of dollars, years of a career, and the looming stress of potential bankruptcy. This is the reality of early-stage startup decision-making. The question of whether to build a company alone or to share the burden with co-founders is arguably the most consequential strategic choice an entrepreneur will make.

For decades, the global entrepreneurial ecosystem has been governed by rigid narratives regarding team composition. Investors, incubators, and business schools have largely operated on the assumption that a founding team of two or more individuals is an absolute prerequisite for success. However, as the macroeconomic environment tightens into a post-ZIRP (Zero Interest-Rate Policy) reality in 2024 and 2025, and as artificial intelligence dramatically alters human capital requirements, the empirical data is beginning to tell a drastically different story.

This exhaustive research report synthesizes recent venture capital datasets from PitchBook, Crunchbase, Y Combinator, and Carta, alongside peer-reviewed organizational science literature. By unpackaging the financial, psychological, and operational mechanics that dictate startup survival, this analysis explores the nuanced realities of solo versus co-founded startup outcomes. Furthermore, the analysis expands beyond the United States to examine the differing realities of European, Asian, and emerging technological ecosystems.

Deconstructing the Mythology: Silicon Valley Dogma vs. The Lone Genius

To objectively evaluate the data, it is first necessary to deconstruct the competing cultural mythologies that cloud the entrepreneurial landscape and influence capital allocation.

The Silicon Valley Dogma

The dominant narrative in venture capital - often referred to as the "Silicon Valley Dogma" - is the archetype of two brilliant minds iterating in a garage. From Hewlett and Packard, to Jobs and Wozniak, to Page and Brin, the technology industry's foundational lore relies heavily on the dynamic duo 112. This has codified a widespread belief that starting a business requires a portfolio of complementary skills (for instance, the popular framework of a technical "hacker," a business "hustler," and a design "hipster") that rarely exist within a single individual 4.

Consequently, a profound systemic bias has emerged. Elite accelerators like Y Combinator historically prefer two-person teams, explicitly noting that single founders face a substantially higher bar for entry due to a perceived "bus factor" of one - the risk that the company collapses if the single founder is incapacitated 567. Venture capitalists actively pattern-match against this dogma, often using a founder's ability to recruit a technical co-founder as a proxy for the strength of the business idea and the founder's persuasive capabilities 8. If a founder cannot convince a peer to join them, the logic goes, how will they convince customers or subsequent investors?

The Myth of the Lone Genius

Conversely, popular culture frequently propagates the "Myth of the Lone Genius" - the hermitic visionary who single-handedly disrupts an entire industry through sheer intellectual force 3. Figures like Elon Musk or Jeff Bezos are frequently cited in mainstream media as solitary architects of the future. The reality, however, is that "lone geniuses" do not build companies in a vacuum 1. Amazon and Dell, often heralded as solo-founded triumphs, were built utilizing extensive networks of early employees, advisors, and benefactors who operated behind the scenes .

The empirical reality exists in the nuanced space between these two extremes. Successful solo founders are rarely isolated hermits, and successful teams are rarely harmonious, conflict-free dream teams.

The Data Reality: Funding, Survival, and Exit Outcomes

The statistical footprint of the modern startup ecosystem reveals a complex interplay between venture capital preferences and actual business survivability.

The Funding Paradox

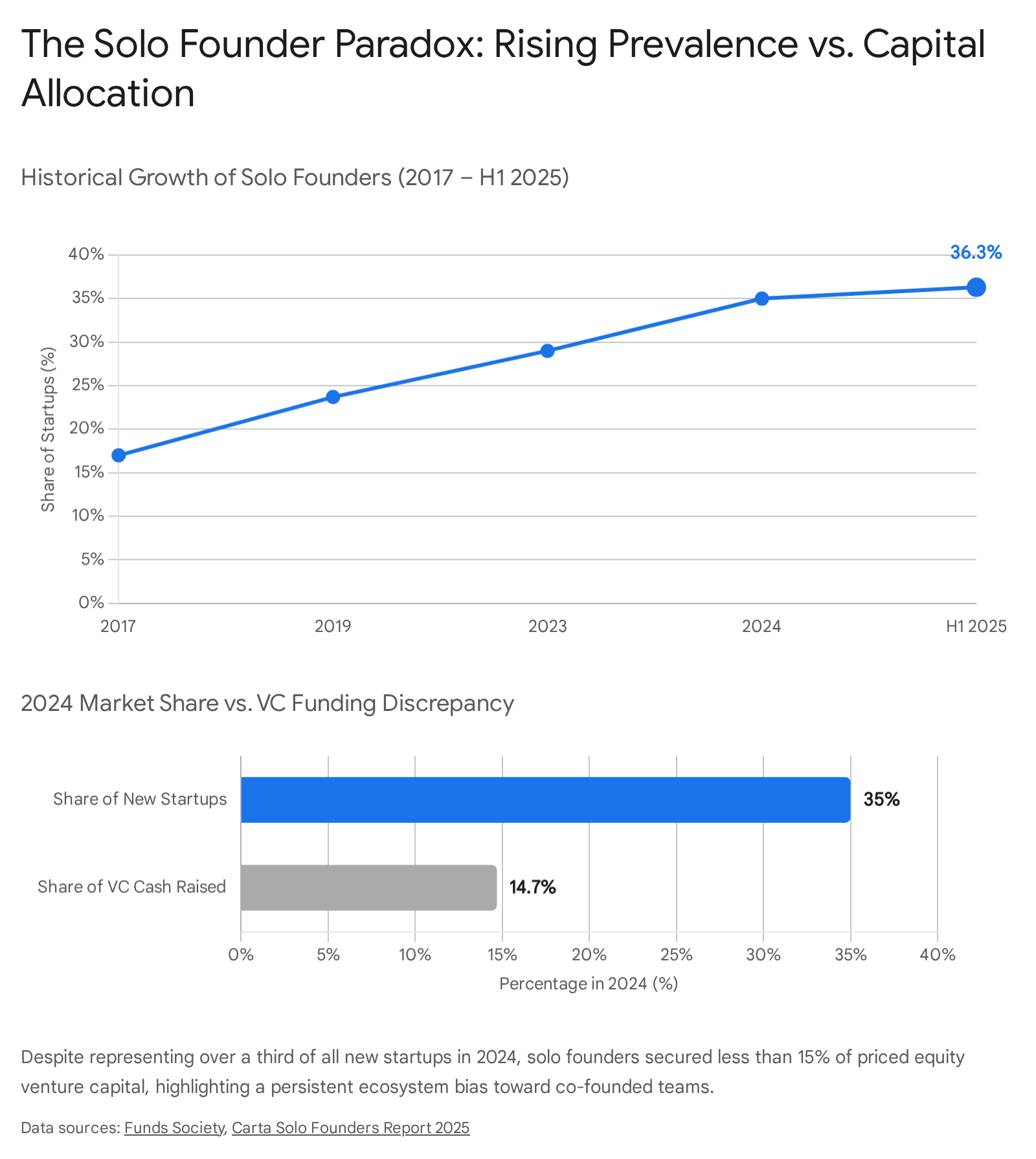

Recent data collected by equity management platform Carta, based on anonymized data from over 45,000 U.S. startups founded between 2015 and 2024, confirms a massive structural shift in the entrepreneurial landscape. The proportion of startups launched by a solo founder has more than doubled over the past decade. In 2017, solo founders accounted for only 17% of new startups. By 2024, this figure reached 35%, and further accelerated to 36.3% in the first half of 2025 45. Conversely, companies launched with three, four, or five founders have plummeted to their lowest levels in a decade 4.

Despite this undeniable surge in solo company creation, a severe funding disparity remains.

In 2024, while solo founders launched 35% of all startups, they accounted for only 17% of the companies that successfully closed a venture capital round before the end of the year, capturing a mere 14.7% of the total cash raised in priced equity rounds 45. Crunchbase data confirms that 37% of VC-backed companies feature a two-person founding team, with 25% featuring three founders 13. This reinforces a self-fulfilling prophecy: investors fund teams because they believe teams succeed, and teams appear to succeed because they receive the majority of the working capital necessary to survive the early stages 13.

Interestingly, the "solo founder penalty" regarding valuation appears to be largely a misconception at later stages. The Carta Founder Ownership Report 2025 proves that when solo founders do raise capital, they achieve valuations, dilution rates, and round sizes that are nearly identical to multi-founder teams from Priced Seed to Series B 1415. Solo founders are, however, significantly less likely to raise a pre-seed round within their first year. Instead of taking early dilution via SAFEs or convertible notes, they often rely on lower burn rates to tinker and pivot, effectively skipping ahead to a priced equity round faster than their co-founded counterparts 1415.

Survival and Revenue Generation

When evaluating actual business outcomes rather than fundraising ability, the narrative shifts entirely. A landmark academic study by NYU Stern Professor Jason Greenberg and Wharton's Ethan Mollick ("Sole Survivors: Solo Ventures versus Founding Teams") analyzed 3,526 ventures to bring empirical discipline to an inquiry that has historically relied on intuition 467. The dataset utilized companies crowdfunded via Kickstarter between 2009 and 2015, ensuring a broad sample size not artificially constrained by venture capital selection bias 618.

The researchers discovered that ventures started by solo entrepreneurs survive longer and generate more revenue than those founded by teams - particularly two-person teams. Specifically, solo founders were 2.6 times more likely to successfully sustain an ongoing for-profit venture than teams of three or more 188. Furthermore, they were 54% less likely to dissolve or suspend their business than three-person teams, and 41% less likely to do so compared to two-person teams 188. (It is worth noting a distinct exception: in the non-profit sector, teams were about twice as likely to survive as solo ventures, likely due to the highly collaborative nature of non-profit stakeholder management) 618.

Data from Crunchbase regarding successful exits further validates this outperformance. Of the startups that achieve a successful exit, 52.3% were led by a single founder 1320. Furthermore, research from Joseph Shin at the University of Washington found that solo founders who achieve "unicorn" status (a valuation exceeding $1 billion) tend to reach that milestone more rapidly than ventures with multiple founders 9. Globally, over 300 solo-founded startups currently hold unicorn status, proving that the absolute upper echelons of venture success are entirely accessible to single operators 20.

Beyond the Balance Sheet: Mechanisms of Success and Failure

To understand why the empirical survival data contradicts venture capital dogma, one must look beyond financial metrics to the behavioral, psychological, and organizational mechanics of early-stage companies. The following FAQ-style analysis explores these underlying drivers.

FAQ 1: Do co-founders mitigate risk, or inherently create it?

The primary theoretical argument for building a founding team is risk mitigation. Investors believe that sharing the burden of execution across multiple highly committed individuals creates a resilient safety net. However, organizational science indicates that adding co-founders often introduces the single greatest risk to a startup: human friction.

According to renowned research by Harvard Business School Professor Noam Wasserman, 65% of high-potential startups fail due to conflict among co-founders 182223. This friction is typically rooted in diverging visions, unaligned strategic priorities, or bitter disputes over equity distribution. As a startup scales, early equity allocations often fail to reflect the evolving, disproportionate contributions of the founders, leading to deep resentment.

While multi-founder teams are increasingly opting for equal equity splits to avoid early awkwardness - rising from 31.5% in 2015 to 45.9% of two-person teams in 2024 - this democratic approach often paralyzes leadership when critical, unpopular pivots are required 422. The necessity to navigate fragile egos and mediate disputes diverts immense energy away from productive activities and customer acquisition 189. A solo founder's structure guarantees zero risk of co-founder dissolution, removing the statistical apex predator of early-stage startups 189.

FAQ 2: How does team size impact the velocity and quality of decision-making?

In a rapidly shifting, technologically volatile market, execution speed is a sharper competitive advantage than comprehensive, risk-averse expertise. Teams naturally default to consensus-building. While teams are highly effective at avoiding catastrophic mistakes, they do so at the cost of momentum 24.

A 2023 analysis by TinySeed found that solo SaaS founders were more likely to reach profitability faster precisely due to reduced coordination overhead 22. A single founder can observe a market signal, validate it with customer feedback, and pivot the company's entire product roadmap in a single afternoon. In a multi-founder scenario, the same pivot requires internal lobbying, scheduled meetings, emotional management, and compromise, resulting in vastly slower reaction times 7.

This is supported by computational models of entrepreneurial decision-making. Research published by Neckebrouck et al. examining preference aggregation (based on the Sah & Stiglitz framework) found that while majority-voting teams excel in stable environments, unanimous approval architectures or solo-autonomy models vastly outperform in fast-changing contexts 2526. The necessity of consensus acts as an operational drag, whereas solo founders benefit from absolute clarity of vision and immediate execution capability. As the colloquial 24-hour rule among solo operators dictates: speed beats safety when markets change overnight 24.

FAQ 3: If solo founders lack broad expertise, how do they fill critical skill gaps?

A foundational criticism of the solo founder model is the breadth of required expertise. It is virtually impossible for one individual to possess elite engineering, marketing, financial, and operational acumen. If 14% of startup failures are due to a lack of key skills, how do solo founders survive? 20.

The answer is illuminated by "Configurational Theory." A 2022 study published in Organization Science ("Going Alone or Together? A Configurational Analysis of Solo Founding vs. Cofounding") extensively analyzed 70 entrepreneurial ventures to understand the mechanics of the solo founder phenomenon 13910. The researchers, Howell, Bingham, and Hendricks, discovered that successful solo founders do not actually build alone; rather, they strategically utilize a network of "co-creators" 13910.

Co-creators include early employees, alliance partners, fractional executives, and advisors. A solo founder might hire a brilliant engineer as Employee #1, granting them a generous salary and early-stage employee equity, but crucially, withholding the title, board seat, and equal voting power of a "Co-Founder." This allows the solo founder to access a "resource-seeking strategy" - acquiring the exact complementary skills needed - without surrendering strategic control or inviting the emotional volatility of a formal partnership 911.

Furthermore, research utilizing Construal Level Theory highlights that when lead entrepreneurs seek formal co-founders, they prioritize resource complementarity (skills), whereas potential co-founders prioritize interpersonal compatibility (culture and affective ties) 1230. This misalignment makes forming optimal "hybrid ties" incredibly difficult 123031. Solo founders bypass this complex matching problem entirely by engaging transactional co-creators.

FAQ 4: What is the true psychological cost of building alone?

While solo founders excel in operational velocity and equity retention, they face a severe, often unmanageable psychological burden. The absence of a peer with an equal emotional, reputational, and financial stake in the business creates a profound vacuum of support. In this specific domain, co-founded teams hold a massive advantage.

Recent 2025 survey data from Sifted paints a harrowing picture of founder mental health. Among the surveyed founders (where roughly a third were solo operators), 83% experienced high stress in the past year, 72% faced clinical mental health challenges ranging from anxiety to depression, and 54% reported suffering from severe burnout 133334. For solo founders, these numbers are exacerbated by extreme professional isolation. Over 70% of solo founders cite severe loneliness 20. A 2024 snapshot by Foundology revealed that 76% of founders report feeling lonely - a rate seven times higher than the general workplace average and 50% higher than corporate CEOs 35.

Clinical psychological research into solo founders highlights that the absence of a "peer witness" to share the entrepreneurial burden leaves the physical body as a repository for unacknowledged stress, drastically increasing the allostatic load and accelerating adrenal exhaustion 36. The solo founder must unilaterally internalize every failure, runway calculation, and personnel issue. The cognitive dissonance of projecting confidence to employees and investors while managing internal panic leads to immense emotional friction. Consequently, while the business entity itself may statistically survive longer, the human operator at the helm is at a drastically higher risk of psychological breakdown and burnout 3614.

Expanding the Geographic Scope: European and Asian Ecosystems

Entrepreneurial dynamics are heavily influenced by their geographic, cultural, and macroeconomic ecosystems. Outcome expectations and funding realities that hold true in Silicon Valley do not universally apply across the globe.

The European Ecosystem: The Premium on Teams and Academic Credentials

In Europe, the venture capital environment is notably more conservative and places a heavily weighted premium on robust, academically credentialed founding teams. The 2024 "State of European Tech" report by Atomico, alongside comprehensive decade-long data from NGP Capital, reveals stark differences from the U.S. market 15161741.

In the European ecosystem, larger teams yield massive fundraising advantages. Top-performing teams with four co-founders raised an astonishing 244% more capital than the baseline 16. Furthermore, academic credentials play a massive role: teams featuring a PhD founder secured a 66% funding premium, and teams with serial founders (previous founding experience) raised 45% more 16. Conversely, European solo founders faced a steep penalty, raising 42% less capital than the baseline 16.

This stark contrast to the U.S. suggests that in Europe - where large growth-stage funding ($100M+ rounds) plummeted by over 56% in the second half of 2024 - investors are aggressively seeking the perceived risk mitigation of deeply credentialed, multi-disciplinary teams 18. The ecosystem is experiencing a "flight to quality," heavily favoring collective safety over singular velocity 18.

However, within the Central and Eastern European (CEE) subset, a different reality emerges. CEE founders demonstrate a highly pragmatic approach, focusing on early revenue generation and bootstrapping over rapid scaling 43. With 92% of all VC-backed deals in the region localized to the pre-seed and seed stages, CEE startups (which achieved a collective enterprise value of €213 billion in 2023) rely heavily on capital efficiency, a domain where solo founders historically excel 43.

Asia and Emerging Markets: Rapid Growth and Resetting Expectations

Asia's startup trajectory is dominated by the massive scale of China and India, which saw domestic and international investors pour over $80 billion and $40 billion respectively into startups in 2024 1920. The volume of "unicorn" generation in these regions trails only the United States, with China hosting 438 unicorns and India hosting 117 as of 2025 46.

However, the broader Southeast Asian (SEA) ecosystem is currently undergoing a severe market correction and a reset of expectations. For the past decade, SEA was aggressively billed by venture capital as the "next China or India," leading to euphoric capital deployment across the region's 670 million inhabitants 21. Recent critical analyses by tier-one venture firms like Lightspeed indicate that this narrative was fundamentally flawed; 89% of Southeast Asian cities lack the urban middle-class income base required to scale hyper-consumer platforms rapidly 21.

Furthermore, the OECD's 2024/2025 "Start-up Asia" reports highlight that opportunities in these emerging markets are highly concentrated in capital cities and heavily male-dominated, with only 15.4% of startups featuring at least one female founder 22. In these tightening environments where consumer spending power is fragmented, the blitzscaling model favored by large, VC-backed co-founding teams is failing. Survival in SEA increasingly relies on the lean, agile, and highly adaptable operational frameworks that are characteristic of solo founders or small, highly cohesive execution teams 4923.

The AI Paradigm Shift: The Rise of the Synthetic Co-Founder

It is impossible to analyze the 2024 - 2025 surge in solo founders without addressing the technological catalyst behind it: Artificial Intelligence. The jump from solo founders representing 23.7% of the market in 2019 to 36.3% in early 2025 correlates directly with the widespread deployment of generative AI, large language models (LLMs), and workflow automation 5.

AI tools are acting as massive operational force multipliers, effectively serving as "synthetic co-founders." A single non-technical operator can now prototype software applications, automate sophisticated outbound marketing campaigns, generate legal templates, and construct full-stack revenue engines without ever needing to write a line of code or recruit a technical partner 551. Specialized AI agent platforms like Tanka are explicitly marketing themselves as solutions to "solo founder overload," providing persistent memory and specialized capabilities to mimic a human partner's output 33.

This is not merely a theoretical shift; it is already producing decacorn-scale outcomes. Startups like Midjourney (founded by David Holz) and the highly influential prediction market Polymarket (founded by Shayne Coplan, which processed over $17 billion in trading volume in January 2026 alone) operate with massive global scale while fundamentally maintaining a solo-founder or highly concentrated core leadership ethos 145253. As AI continues to commoditize technical execution and middle-management tasks, the venture capital premium historically placed on having a "technical co-founder" will inevitably diminish. This technological leverage will likely push the ratio of solo founders even higher in the latter half of the decade.

The "Solo Tax" vs. The Equity Premium: A Comparative Analysis

The strategic decision between building solo or as a team requires navigating a complex series of tradeoffs. The following table synthesizes the distinct advantages, vulnerabilities, and outcomes of each model based on the aggregate 2024 and 2025 empirical datasets.

| Key Metric / Operational Dynamic | Solo Founder Startups | Co-Founded Teams (2+ Members) | Distinct Advantage |

|---|---|---|---|

| Early Equity Retention | Starts at 100%. By Series B, holds roughly 50% more personal equity than a lead co-founder. 1415 | Splitting equity early drastically reduces individual payouts. 45.9% of duos split equally. 4 | Solo Founders. Vastly superior personal financial outcomes at exit. |

| Venture Capital Access | Faces a steep barrier to entry. Captures only 14.7% of total VC cash deployed. 5 | Highly favored by VCs. 37% of VC-backed startups are duos. 4-person teams raise 244% more in Europe. 1316 | Co-Founded Teams. Substantially easier path to institutional capital. |

| Decision-Making Velocity | Rapid. Zero consensus overhead. Capable of instant strategic pivots. 24 | Slower. Requires alignment, debate, and consensus, causing operational drag. 72454 | Solo Founders. Speed and momentum beat safety in early stages. |

| Conflict & Dissolution Risk | 0% risk of co-founder conflict. 189 | 65% of high-potential startups fail due to interpersonal co-founder friction. 182223 | Solo Founders. Eliminates the primary cause of startup death. |

| Skill Set Breadth | Narrow initially. Must rely on "co-creators" (advisors, contractors, early hires) to fill gaps. 9 | Broad. Can possess deep technical, commercial, and operational skills from Day 1. 455 | Co-Founded Teams. Immediate access to diverse, high-level competencies. |

| Psychological Resilience | High risk of severe isolation. 76% report loneliness; 54% experience burnout. 13333435 | Shared emotional burden. Mutual support mitigates the psychological extremes of founding. 1455 | Co-Founded Teams. Vastly superior mental health and emotional sustainability. |

Practical Takeaways for Aspiring Entrepreneurs

The aggregate data requires entrepreneurs to apply a framework of calibrated uncertainty: there is no universal "correct" model. The optimal structure depends entirely on the founder's psychology, the capital intensity of the sector, and their geographic location.

For aspiring founders evaluating this dilemma, the empirical findings yield several actionable directives:

- Align Team Structure with Capital Requirements: If the venture requires massive upfront capital expenditure (e.g., hardware manufacturing, deep-tech, biotechnology, or highly regulated fintech), building a credentialed team is highly recommended. Venture capitalists and grant programs demand robust teams to underwrite heavy capital risks, especially in European markets where team size directly correlates with funding volume 1416. Conversely, if the venture is a B2B SaaS, a consumer application, or an AI-enabled service, the solo path is statistically viable and financially superior over the long term.

- Employ the "Co-Creator" Strategy: Solo founders should aggressively hire for their weaknesses, but they should be exceedingly cautious about giving away formal "co-founder" status to do so. Employee #1 should be compensated with appropriate early-stage equity (e.g., 1% to 5%) and a competitive salary, deliberately avoiding the 50/50 splits that lead to paralyzing deadlock 922. Establish an "advisory constellation" by giving 0.25% to 1% to industry veterans who provide specialized expertise without ego, conflict, or voting rights 22.

- Establish Asymmetric Decision Frameworks: If an entrepreneur chooses to build a co-founding team, they must proactively prevent consensus paralysis. Implement rigid frameworks where specific founders hold absolute veto or unilateral decision-making power over their specific domains (e.g., the technical founder has absolute authority over architecture, the CEO over sales). Treat the startup as a hierarchy of aligned experts rather than a pure democracy 2425.

- Proactively Engineer Emotional Infrastructure: Solo founders cannot afford to ignore the staggering 54% burnout rate and the profound risks of isolation 1334. Because they lack a co-founder to share the psychological load, solo entrepreneurs must actively construct external peer circles. Joining mastermind groups, engaging executive therapists, and interacting with specialized founder networks are not luxuries for the solo founder - they are critical operational requirements to prevent somatic stress and total business collapse 3614.

Conclusion

The persistent venture capital bias toward co-founded teams - rooted deeply in the nostalgic mythology of Silicon Valley and the risk-aversion of institutional capital - is increasingly misaligned with objective outcome data. While co-founders undeniably ease the early fundraising process, provide broader immediate skill sets, and offer a crucial emotional safety net, they introduce a nearly terminal level of organizational friction.

The empirical evidence unequivocally demonstrates that solo founders, unencumbered by the need for consensus and immune to co-founder conflict, execute with greater velocity, survive longer in the market, and retain vastly superior financial outcomes upon exit. Supported by the accelerating leverage of artificial intelligence and the strategic utilization of transactional "co-creators," the solo founder is no longer an anomaly to be penalized by investors. Rather, it represents a highly efficient, rapidly growing blueprint for the future of global enterprise creation.