Success rates of solo versus team founders

The fundamental calculus of startup formation has long been governed by a persistent venture capital heuristic: founding teams inherently outperform solo entrepreneurs. Historically, the global entrepreneurial ecosystem codified this preference into its capital allocation structures, with premier accelerators and institutional investors exhibiting a pronounced, systemic bias toward multi-founder configurations. However, an influx of empirical data generated between 2023 and 2026 suggests that this foundational assumption requires rigorous reevaluation. Driven by the democratization of artificial intelligence, the permanent integration of remote work paradigms, and profound macroeconomic shifts, the viability, survival probability, and economic footprint of the solo founder have expanded dramatically. Simultaneously, granular analyses of team dynamics indicate that the mere presence of co-founders is not a panacea; rather, specific team sizes, the exact nature of their heterogeneity, and the presence of confounding variables such as prior entrepreneurial experience and industry focus dictate ultimate outcomes.

This report systematically deconstructs the empirical reality of startup success rates, contrasting the performance of solo founders against multi-founder teams. By explicitly contrasting academic literature with industry databases, disaggregating the definition of success into baseline survival, venture capital acquisition, and unicorn capitalization, and expanding the geographic scope to encompass Asia, Europe, and Latin America, the analysis provides a comprehensive, data-driven framework for understanding modern entrepreneurial viability.

Academic Literature versus Industry Data: A Methodological Contrast

The debate regarding solo versus team founders is frequently distorted by divergent methodological frameworks. A critical distinction must be drawn between academic literature - originating from institutions such as the National Bureau of Economic Research (NBER), the Wharton School, and the Massachusetts Institute of Technology (MIT) - and industry data derived from commercial platforms like PitchBook, Crunchbase, and Y Combinator. These two domains measure fundamentally different proxies for "success."

Academic studies typically optimize for baseline survival, long-term revenue generation, and macroeconomic firm creation. For example, Wharton researchers Jason Greenberg and Ethan Mollick utilized a dataset of crowdfunded companies to measure actual survival longevity and revenue creation, concluding that solo founders often outlive teams 123. NBER working papers consistently measure "entrepreneurial spawning" (the transition from wage employment to firm creation) and the subsequent survival rates of those entities, often finding that solo ventures, gig-economy spawned businesses, and remote-work spawned startups display remarkable resilience and quality, even if they do not immediately secure institutional capital 456. MIT research frequently focuses on the translation of academic research into real-world results, tracking how solo spinouts from university labs achieve commercial viability through highly specialized technological applications 7.

Conversely, industry data relies on institutional capital milestones - such as priced venture rounds, post-money valuations, and billion-dollar exits - as the primary metrics of success. First Round Capital's retrospective analyses, Y Combinator batch statistics, and Carta's ownership reports explicitly track venture capital allocation, equity dilution, and portfolio returns 881011. This creates a massive accelerator and investor selection bias. Because top-tier accelerators like Y Combinator historically restrict solo founder admission to approximately 10 percent 2, the resulting industry data disproportionately reflects the success of teams. Therefore, when industry reports state that teams outperform solo founders, they are often reporting that teams are superior at navigating a venture capital ecosystem that was explicitly designed to fund teams. To achieve a nuanced understanding of founder viability, one must synthesize the academic reality of business survival with the industry reality of capital acquisition.

Disaggregating Success: Survival, Capitalization, and Outlier Growth

Empirical evidence dictates that startup success cannot be treated as a monolithic outcome. It must be disaggregated into three distinct vectors: baseline survival (longevity and operational continuity), capital acquisition (the ability to secure institutional venture backing), and exceptional growth (achieving unicorn status or high-value exits). When evaluated across these separate axes, the performance profiles of solo founders and teams diverge significantly.

Baseline Survival and Operational Longevity

Contrary to the prevailing venture capital narrative, academic literature indicates that solo founders exhibit remarkable resilience when measured by raw survival rates. In the Wharton study examining companies that collectively generated hundreds of millions in revenue, organizations established by solo founders survived significantly longer than those started by teams 12. Furthermore, in for-profit ventures, solo entrepreneurs were found to be approximately two and a half times more likely to survive than their team-founded counterparts, and 55 percent less likely to dissolve their businesses compared to teams of three 3.

This survival advantage for solo founders becomes coherent when the primary vectors of startup mortality are examined. Market data indicates that 90 percent of startups fail over their lifecycle, with 20 percent collapsing in the first year and 70 percent failing between years two and five 121314. While 42 percent collapse due to an absence of market need and 29 percent deplete their capital, up to 23 percent fail explicitly due to team issues and co-founder conflict 1215. By definition, the solo founder entirely eliminates the risk of co-founder conflict - a friction point that is responsible for a substantial majority of early-stage structural failures. Furthermore, when analyzing post-mortem data from 2020 through 2024, team breakdown remains the third most common cause of startup death, often compounding other operational errors 16.

Additionally, the survival data is heavily influenced by capitalization models. Investors exhibit a profound selection bias toward teams, leading multi-founder startups to raise capital earlier and in larger quantities 2. This influx of early venture capital often forces premature scaling - a leading cause of startup mortality. Because solo founders face higher friction in raising capital, they are frequently forced to bootstrap, focus on strict unit economics, and delay scaling until product-market fit is empirically proven. Bootstrapped startups demonstrate a 58 percent five-year survival rate compared to just 32 percent for venture-backed startups, indicating that the financial discipline imposed by a lack of early capital contributes directly to the solo founder's longevity advantage 17.

The Venture Capital Acquisition Gap

While solo founders excel in baseline survival, they face a severe and persistent disadvantage in capital acquisition. Institutional investors view shared decision-making, distributed operational loads, and complementary skill sets as fundamental risk mitigation mechanisms. Consequently, the venture capital ecosystem actively selects against the solo founder.

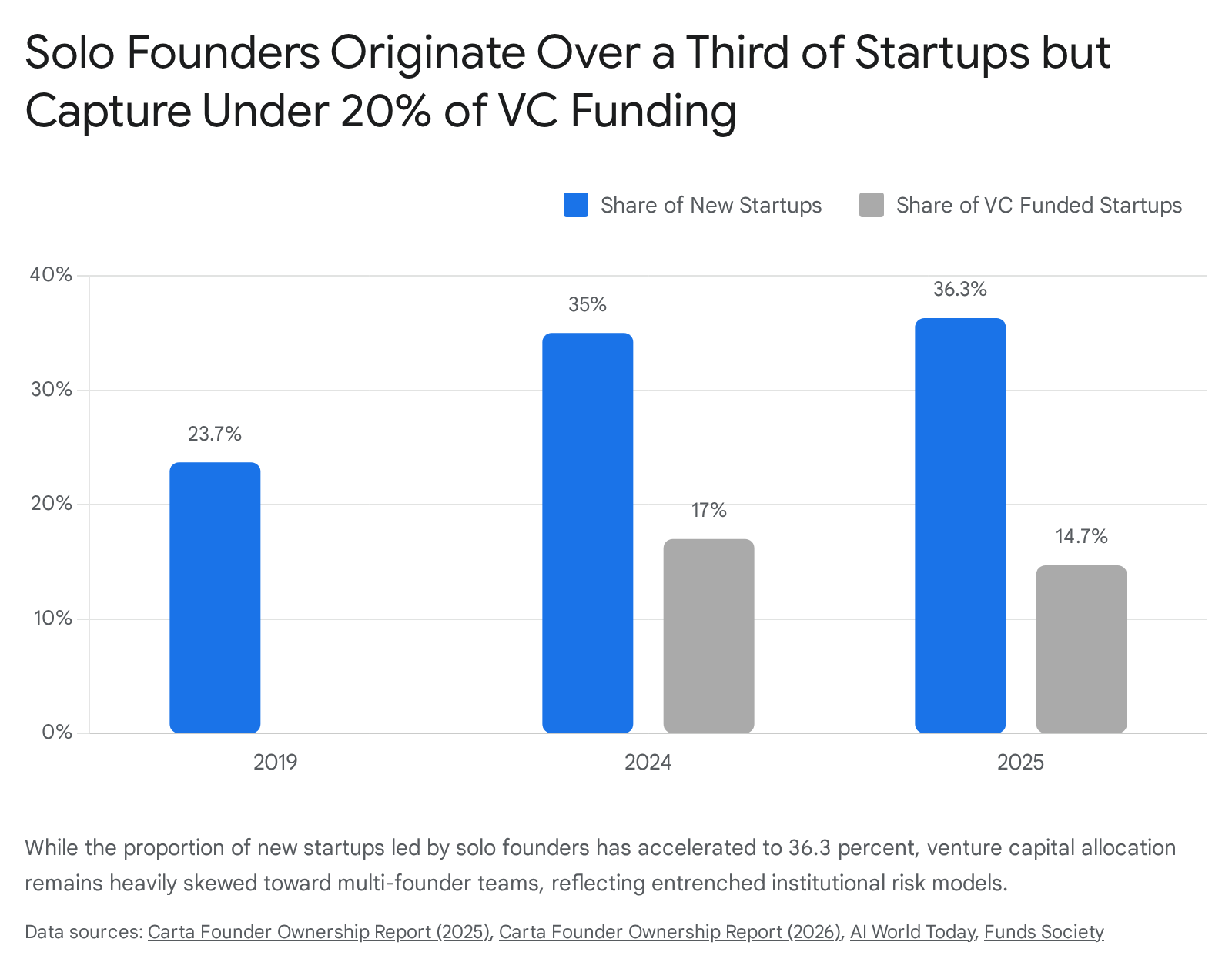

Data from Carta's 2025 and 2026 Founder Ownership Reports quantifies this disparity with high precision. In 2024, solo founders established 35 percent of all new startups in the United States 910. By the first half of 2025, that figure climbed to 36.3 percent, representing a near doubling of the solo founder proportion since 2019 112122. However, despite originating more than one-third of all new enterprises, solo-led companies accounted for only 14.7 to 17 percent of the startups that successfully closed a priced venture capital round 9101121.

Industry data underscores the economic logic driving this investor preference: First Round Capital's ten-year retrospective analysis revealed that teams with more than one founder outperformed solo founders in their portfolio by 163 percent in revenue generation, and solo founders suffered a 25 percent penalty in their initial seed valuations 8823. Similarly, the presence of a co-founder serves as a hedge against catastrophic operational failure; NBER data measuring startup performance post-founder mortality shows that the premature death or departure of a key founding member drops revenue by 31 percent and employment by 15 percent, illustrating the extreme vulnerability of organizations reliant on a single individual's human capital 1225.

However, the fundraising landscape itself is shifting, making venture capital less necessary for early survival. The median time between funding rounds extended dramatically from 451 days in 2021 to 744 days by the end of 2024, forcing all founders to optimize for longer runways and stricter unit economics 13. As capital becomes more expensive and harder to secure, the bootstrapped solo founder model becomes increasingly competitive.

Unicorn Capitalization and Successful Exits

When optimizing for extreme outlier success - the unicorn valuation of one billion dollars or more - the data presents a complex narrative. Achieving unicorn status is a highly anomalous statistical event, carrying a probability of roughly 0.00006 percent 13. The U.S. venture market, despite producing over 714 unicorns historically, only sees about 1 in 60 VC-backed companies achieve this status, with Europe seeing 1 in 135 1327.

While institutional investors rely on teams to reach these valuations, analysis of actual liquidity events reveals that solo founders are highly capable of generating massive returns. Data derived from the Crunchbase API analyzing over 6,191 successful exits (defined by IPO or M&A) revealed that 52.3 percent of these highly successful liquidity events were driven by solo founders 228. Furthermore, a deep dive into the last 100 billion-dollar tech exits in the United States showed that 11 percent of these mega-exits were driven by single-founder companies, proving that while teams are more common (with two-founder teams representing 47 percent of these exits), solo founders are demonstrably capable of achieving the highest echelons of venture success 29.

A comprehensive 2025 study on European unicorns provided critical insights into how team composition influences the velocity of scaling to unicorn status. The research concluded that larger founding teams are actually associated with an extended time-to-unicorn status 14. The empirical reality is that excessive team size introduces severe coordination challenges, structural frictions, and complex decision-making bottlenecks that inhibit hyper-agility 14. This friction is mitigated by optimizing for specific types of heterogeneity. The European data revealed that while diversity in the level of education among founders slows scaling (due to status asymmetries), diversity in the type of education (e.g., pairing a highly technical engineering founder with a commercial management founder) significantly shortens the time to achieve unicorn status 14.

Beyond the Binary: The Spectrum of Team Size

Moving beyond the strict binary of the solo founder versus the team, empirical data explicitly contrasts the performance of specific team sizes, revealing a clear hierarchy of efficiency and a market shift toward smaller configurations.

The two-person founding team, or dyad, remains the statistical optimum for securing institutional capital and scaling traditional software enterprises. Carta's venture market data indicates that two-founder teams represent 45.9 percent of all historical configurations and remain the most common structure among startups that successfully raise venture funding 13910. In 2025, 36 percent of all startups that closed rounds on Carta had two founders, a rate that rose to 40 percent specifically within the Software-as-a-Service (SaaS) industry 15. These dyads are increasingly opting for egalitarian structures, with 45.9 percent of two-person teams dividing their equity equally in 2024, up from 31.5 percent in 2015 910.

Conversely, the data reveals rapidly diminishing returns - and declining market prevalence - for larger founding teams. Over the past decade, startups with three, four, or five founders have become steadily less common. By 2024, only 16 percent of new startups featured three founders, 7 percent featured four, and a mere 4 percent featured five, marking the lowest levels for large teams in the past ten years 910. This decline is reflected in successful exit data as well; in the analysis of the last 100 billion-dollar tech exits, four-founder teams represented only 11 percent, and teams of five or more represented a rare 6 percent 29.

The drag associated with large founding teams is further evidenced by equity dilution mechanics. When a team consists of four or five founders, the equity pool is heavily fragmented before the first employee is hired or the first investor is boarded. Consequently, founder ownership declines sharply; by Series C, the median employee equity pool (16.8 percent) outstrips the median founder ownership (16.1 percent) 15. The optimal configuration for venture-backed hyper-growth remains the two- or three-person team possessing highly complementary, non-overlapping skill sets, mirroring the "barbell" scaling pattern observed in successful Y Combinator companies that start with 3 to 5 employees and only expand to 50+ after establishing product-market fit 10.

Macroeconomic and Technological Catalysts (2023 - 2026)

The traditional calculus of team size has been irrevocably altered by two massive, concurrent shocks to the entrepreneurial ecosystem: the integration of generative artificial intelligence as operational infrastructure, and the macroeconomic entrenchment of remote work.

Artificial Intelligence as the Synthetic Co-Founder

The most profound shift driving the recent surge in solo entrepreneurship is the deployment of generative artificial intelligence and large language models (LLMs). The acceleration of solo-founded startups corresponds precisely with the mainstream adoption of AI coding assistants and agentic tools 2122. Artificial intelligence fundamentally rewrites the relationship between team size and output, functioning as a synthetic co-founder that collapses the cost of product development and compresses execution timelines.

Empirical evidence demonstrates that no-code machine learning platforms and LLM agents enable solo founders to automate coding, market research, design, and customer operations, slashing early-stage hiring costs by up to 90 percent 32. A 2024 MIT Center for Collective Intelligence (CCI) study analyzing 370 results from 106 experiments found that human-AI collaborations excel particularly in creative tasks, content generation, and customer interaction, effectively replacing the need for early marketing or operations co-founders . However, the MIT study also noted that human-AI teams fell short in complex decision-making tasks, suggesting that while AI can replace operational headcount, it cannot fully replace the strategic judgment of a human co-founder .

Financially, the leverage AI provides is staggering. AI-native startups are rewriting revenue-per-employee benchmarks; multiple companies in late 2025 crossed the $1 million to $5 million Annual Recurring Revenue (ARR) threshold with fewer than five employees, leveraging AI to handle the operational load traditionally managed by dozens of human workers 34. Case studies indicate that AI-enabled one-person ventures are scaling to $127,000 in average annual revenue rapidly, with extreme outliers reaching $90,000 in Monthly Recurring Revenue (MRR) without a traditional team 32.

However, this technological leverage introduces a new vulnerability regarding defensibility. If AI collapses the cost of building software, technical novelty ceases to be a competitive moat. Consequently, solo founders must rely on proprietary data, deep domain expertise, and entrenched customer relationships to defend their margins against hyper-competition 22. Furthermore, the rise of AI is driving a shift in capital requirements from human labor to computing power. Inference costs for AI companies now average 23 percent of revenue, compressing gross margins to 50-60 percent and making them resemble industrial operations with significant cost of goods sold (COGS) rather than traditional 90 percent margin SaaS businesses 35.

The Entrepreneurial Spawning of Remote Work

The normalization of remote and hybrid work environments has acted as a massive macroeconomic catalyst for entrepreneurial formation. In 2023, full days worked from home accounted for 28 percent of paid workdays in the United States, remaining persistent at 25 percent through 2025 1617.

A landmark NBER working paper established a causal link between remote work and "entrepreneurial spawning." By analyzing internet traffic and tracking IPv4 addresses to measure firm-level remote work, researchers found that employees at firms with higher shares of remote workers during and after the pandemic were significantly more likely to transition from wage employment to starting their own businesses 416. Specifically, a one-standard-deviation increase in firm-level remote work increased transitions to entrepreneurship by 30 percent among job switchers 4. The study estimates that at least 11 percent of the post-pandemic increase in new firm entry can be explained by remote work-induced spawning 4.

This phenomenon occurs because remote work significantly lowers the barrier to entrepreneurial experimentation. By eliminating commute times (saving an average of 72 minutes per day) and reducing employer monitoring, remote work provides aspiring founders with the temporal flexibility and downside risk protection necessary to develop a minimum viable product while maintaining their primary wage income 438. Crucially, the businesses spawned by remote workers demonstrate higher quality than average new firms; their initial employment is 38 percent higher, and their likelihood of receiving venture capital funding is 171 percent higher 4.

Conversely, the remote environment presents complex challenges for team-based productivity and human capital development. Further NBER research utilizing data from 2019 to 2024 revealed the "power of proximity": physical co-location increases coding feedback among software engineers by 18.3 percent and improves code quality, particularly for younger, less-tenured employees who rely on proximity for rapid skill acquisition 18. However, this comes at a cost, as experienced engineers were found to write less code when sitting near colleagues due to the informal mentorship tasks they assumed 18.

Another hidden driver of solo startup formation is a growing crisis in traditional workplace satisfaction. A July 2025 NBER working paper identified a catastrophic rise in "young worker despair," noting that among workers aged 18-24, the proportion reporting complete mental despair (30 out of 30 days of bad mental health) rose by 140 percent since the 1990s 40. This psychological distress with traditional corporate structures is pushing younger professionals toward the autonomy of solo entrepreneurship and the gig economy. A separate NBER study on the gig economy found that gig workers are about 1 percentage point more likely to start new businesses, utilizing platform work to lower the downside risk of founding a company 6.

Geographic Divergence: Asia, Europe, and Latin America

The dynamics of startup formation and team viability are not globally uniform. Distinct regional variations in capital maturity, regulatory environments, and structural economic gaps dictate the optimal approach for founders outside the United States.

The Asia-Pacific (APAC) Region: Maturation and High Attrition

The Asian startup ecosystem presents a landscape of immense scale coupled with severe attrition, forcing founders to adopt highly resilient team structures. The total value created by the Indian startup ecosystem exceeded $450 billion, with robust IPO activity in 2025 including multi-billion dollar listings 4142. However, the environment is highly saturated. In 2025 alone, India recorded over 11,000 startup shutdowns, representing a 30 percent year-over-year increase, driving baseline failure rates to approximately 90 percent 15. China exhibits a similarly aggressive environment with an 80 percent failure rate, driven by hyper-competition and rapid copycat dynamics that compress margins almost immediately after a product launch 15.

In response to these punishing conditions, the demographic profile of the successful APAC founder relies heavily on experience and total commitment. A 2026 survey of the Asia-Pacific ecosystem revealed that 70 percent of regional founders are over the age of 45, challenging the stereotype of the young tech prodigy 43. These mature founders display intense dedication, with 56 percent working on their startups exclusively full-time, compared to only 50 percent of U.S. founders who maintain secondary jobs 43. The data indicates that in highly competitive Asian markets, the successful founder profile relies on deep industry experience and a relentless focus on execution. Furthermore, in specialized sectors like ASEAN Generative AI startups, 92 percent are strictly B2B focused, requiring complex enterprise sales cycles that heavily favor multi-founder teams with established corporate networks over solo operators 44.

Latin America (LatAm): Structural Gaps and Lean Agility

The Latin American ecosystem is defined by a rapid rebound in capital and an intense focus on resolving deep structural market inefficiencies. Following a severe market correction, VC funding in the region rebounded by 13.8 percent in 2025 to reach $4.1 billion, with Brazil and Mexico capturing 78.5 percent of the total capital 45. The region currently hosts roughly 40 unicorns, highlighting a maturing ecosystem capable of generating massive returns 4519.

Latin American founders operate in environments characterized by uneven infrastructure, large unbanked populations, and strained public systems. Consequently, 61 percent of all regional funding is directed toward Fintech, where startups address massive gaps in financial inclusion 4547. The ecosystem remains starkly imbalanced regarding gender diversity; only 5 percent of the founders in the top 100 LatAm startups are women, although this represents a slow improvement from pre-2013 cohorts which were exclusively male 48. Given the lower operating costs in the region - typically 40 to 60 percent lower than in the United States - founders in Latin America can achieve significantly longer runways with smaller seed injections. This environment allows lean, agile founding teams to iterate on fundamental infrastructural solutions without the immediate pressure of massive Series A burn rates, making small team configurations highly viable 45.

Europe: The Dominance of Deep Tech

The European startup ecosystem is increasingly defined by its pivot away from traditional SaaS and toward Deep Tech and hardware innovation. In 2024, the United Kingdom attracted $4.2 billion and Germany secured $2.7 billion in deep tech venture capital, fueled by dense concentrations of academic research institutions and industrial corporate partners 49.

This sectoral shift fundamentally alters the solo versus team calculation. While SaaS companies can be efficiently built by solo founders leveraging AI, deep tech - encompassing advanced robotics, space tech, quantum computing, and next-generation semiconductors - demands highly specialized, multidisciplinary scientific teams 4950. The returns justify this increased operational complexity: a 2024 report by Hello Tomorrow revealed that European hardware-focused startups deliver a gross internal rate of return (IRR) of 27 percent, vastly outperforming software counterparts that average a 13 percent IRR 51. In Europe's most lucrative growth sectors, the successful scaling entity is inherently a diverse, highly educated scientific team, effectively rendering the solo founder model non-viable for capital-intensive frontier technologies.

Confounding Variables: Experience, Diversity, and Industry Sector

To accurately assess success rates, one must control for massive confounding variables that transcend the basic head-count of a founding team. Founder experience, team diversity, and the specific industry sector exert disproportionate influence on ultimate outcomes, often overriding the baseline statistics of team size.

The Premium on Serial Experience

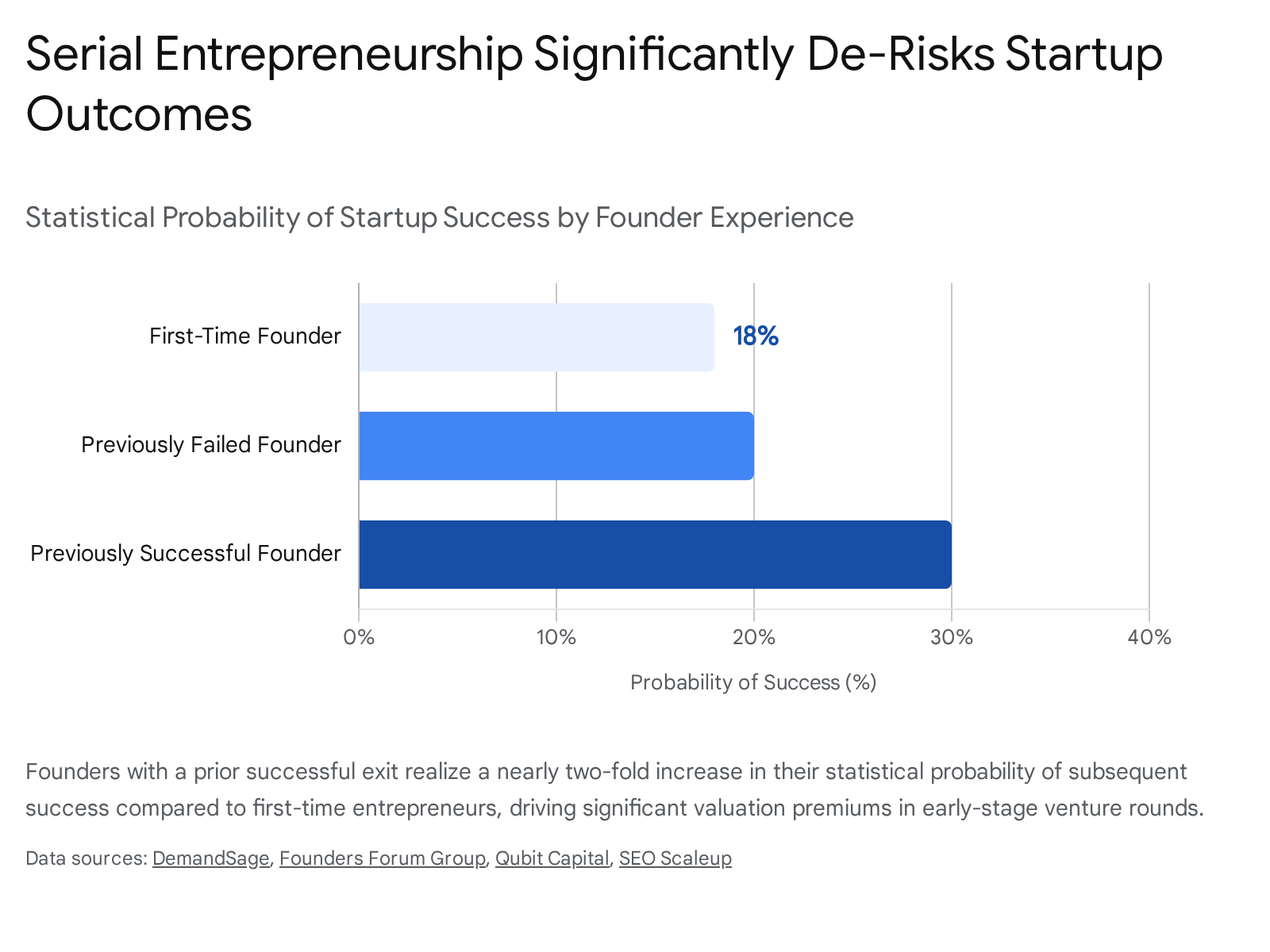

Prior entrepreneurial experience drastically alters baseline failure rates, serving as one of the strongest predictive signals for venture capitalists. Across global datasets, first-time founders exhibit a baseline success rate of just 18 percent 12175253. Conversely, serial founders who have previously launched a successful business or taken a company public enjoy a success rate of 30 percent with their subsequent ventures 12175253. Even founders whose previous ventures failed demonstrate a slightly elevated success rate of 20 percent, indicating that the mere act of operating a startup builds critical human capital 1252.

Sophisticated venture capitalists explicitly price this experience into their valuations. Research indicates that second-time founders close funding rounds roughly twice as fast as first-timers and command valuation premiums of 10 to 20 percent on comparable deals 16. Investors view prior failure not as a strict negative, but as empirical proof that a founder's judgment has been stress-tested under adverse conditions, providing a level of operational maturity and crisis management capability that first-time founders lack 16.

Synergies of Diversity: Immigrant and Gender Dynamics

The internal demographic composition of a team serves as a powerful multiplier of success. A comprehensive NBER study utilizing data from over 90,000 U.S.-based startups founded between 2000 and 2022 revealed that mixed immigrant-native founding teams consistently outperform both single-origin native teams and single-origin immigrant teams 20. Three years post-inception, these mixed teams are 20 percent larger by employment, generate larger revenue, and are significantly more likely to secure external venture funding 20. The synergy derived from combining the localized market knowledge of native founders with the diverse operational perspectives of immigrant founders creates a measurable, structural competitive advantage.

Similarly, gender diversity heavily impacts capital efficiency, despite existing within a deeply inequitable funding environment. Companies founded solely by women captured only 1 to 2 percent of total U.S. venture capital in 2024, down from roughly 2 percent in 2023 13. Globally, all-female teams received just 2.3 percent of deployed VC capital, while all-male teams commanded 83.6 percent 13. Despite this severe capital starvation, diverse teams display superior operational discipline. First Round Capital's retrospective analysis indicated that their investments in companies with at least one female founder outperformed all-male teams by 63 percent, illustrating that capital efficiency and sustainable growth are highly correlated with gender-diverse leadership 855.

Industry-Specific Multipliers

Finally, the viability of a solo founder versus a team is entirely dependent on the specific industry sector. Analytical frameworks assessing startup outcomes apply heavy baseline multipliers based on sector dynamics:

| Industry Sector | Success Multiplier | Baseline Success Rate | Key Structural Dynamics |

|---|---|---|---|

| Fintech | 2.5x | ~7.5% | High regulatory barriers create deep defensive moats. Demands larger founding teams (median of 12 employees) for compliance and integration 810. |

| Developer Tools | 1.8x | ~5.4% | Highly technical audience allows for lower customer acquisition costs (CAC) and strong word-of-mouth distribution 8. |

| Healthcare / HealthTech | 1.15x | ~3.45% | Longer development cycles prevent premature scaling; intense regulatory requirements force rigorous validation prior to launch 856. |

| B2B SaaS | 0.8x | ~2.4% | Severe market saturation compresses margins; heavily reliant on AI tooling to maintain capital efficiency 8. |

| B2C Consumer Apps | 0.6x | ~1.8% | Plagued by extreme competition, high platform dependency, and massive user acquisition costs 8. |

| Deep Tech / Hardware | N/A (Outlier) | Low Volume, High IRR | Requires highly specialized, capital-intensive scientific teams. Generates massive returns (27% IRR in Europe) but renders solo founders functionally non-viable 355051. |

Comparative Analysis of Major Studies

To synthesize the diverging empirical conclusions regarding startup team composition, the following structured comparison isolates the methodologies and findings of the ecosystem's most definitive recent studies.

| Source | Success Definition | Solo Rate | Team Rate | Caveats |

|---|---|---|---|---|

| Wharton / NBER (Mollick et al., 2023) 123 | Business Survival & Total Revenue Generation. | Superior. 2.5x more likely to survive in for-profit ventures. | Inferior. 55% higher likelihood of dissolution vs. solo. | Analyzed crowdfunded companies, not VC-backed unicorns. Proves solo founders excel in baseline survival but not necessarily hyper-scaling. |

| First Round Capital (10-Year Study) 8823 | Overall Portfolio Valuation & Revenue Growth. | Inferior. 25% lower seed valuations. | Superior. Multi-founder teams generated 163% more revenue. | Data is exclusive to a single, elite VC's portfolio. Inherently contains severe venture selection bias prioritizing teams. |

| Carta (Founder Ownership Reports 2025/2026) 9102115 | Startup Formation Rate vs. VC Funding Acquisition. | High Formation (36%). Poor VC Funding (14.7-17%). | Low Formation. Dominant VC Funding (Teams of 2 capture highest share). | Focuses solely on capital acquisition and equity distribution, not long-term business survival or product-market fit. |

| European Unicorn Study (2025) 14 | Time-to-Unicorn ($1B+ Valuation). | N/A (Solo founders absent from the dataset). | Variable. Speed relies on diverse types of education. | Highlights that excessive team size and diverse education levels actually increase friction and delay scaling. |

| Crunchbase / Exits Data 228 | Successful Liquidity Event (M&A or IPO). | 52.3% of successful exits came from solo founders. | 47.7% of successful exits came from teams. | M&A exits for solo founders are often smaller-scale acquisitions rather than massive IPOs; average team size at exit across the set was 1.85. |

| NBER (Choi et al., 2021) 12 | Startup Performance Post-Founder Mortality. | N/A (Focuses on loss of founders). | Highly Vulnerable. Loss of a key founder drops revenue 31%. | Demonstrates the extreme fragility of early-stage teams; organizational capital is entirely embedded in key personnel, exposing single points of failure. |

| MIT CCI Human-AI Study (2024) | Task Performance & Output Quality. | Enhanced. Human-AI teams excel in creative/generative tasks. | Challenged. Teams still required for complex decision-making. | Proves AI acts as a viable "synthetic co-founder" for content and coding, but cannot replace human strategic judgment. |

Conclusion

The empirical landscape defining entrepreneurial success in the 2023 - 2026 operating environment has fractured the simplistic binary that teams definitively outperform solo founders. The reality is profoundly contextual, governed by the desired operational outcome, the technological leverage applied, and the macroeconomic realities of the target geography.

If the objective is pure operational survival, cash-flow positivity, and the avoidance of fatal internal conflict, the solo founder model is statistically superior. Empowered by generative AI acting as a synthetic co-founder and the operational flexibility of remote work, solo founders are increasingly bypassing the institutional venture capital ecosystem entirely. By substituting massive capital injections with automation and extreme operational discipline, they are driving a historic surge in solo-business formation and demonstrating unprecedented first-year profitability.

Conversely, if the objective is securing institutional capital, driving hyper-growth, and dominating highly regulated or deeply technical sectors (such as Fintech or European Deep Tech), the multi-founder team remains an absolute necessity. Venture capital operates on a power-law distribution that requires rapid scaling and aggressive market capture - a velocity that necessitates divided labor, complementary skill sets, and the risk mitigation inherent in a two- or three-person dyad. Furthermore, the strategic combination of diverse experiences - specifically serial entrepreneurial backgrounds, mixed immigrant-native origins, and gender diversity - creates a structural competitive advantage that solitary operators cannot replicate.

Ultimately, the traditional venture capital bias against the solo founder is slowly becoming a historical artifact in the realm of lightweight software and digital services. However, as the frontier of technology shifts toward complex hardware, space tech, and biological sciences, the specialized, multidisciplinary team will remain the vital engine of outlier economic growth. Success in the modern era relies not on a rigid adherence to team size, but on flawlessly aligning the structural composition of the founders with the specific capital, technical, and geographic requirements of the market they seek to disrupt.