What Is Sentiment Analysis and How Traders Use It

Financial sentiment analysis uses natural language processing to read thousands of news articles, earnings transcripts, and social media posts in real time to measure the market's collective mood. Rather than acting as a magic crystal ball that perfectly predicts the future, these advanced tools give traders a statistical edge by translating human fear, greed, and confidence into actionable, quantifiable data. While hedge funds have long dominated this space using massive computing power, a new generation of artificial intelligence tools is finally giving retail investors access to similar real-time market insights.

The Illusion of the Magic Crystal Ball

For decades, analysts and traders have relied on technical indicators and numerical barometers to gauge market psychology. Tools like the CBOE Volatility Index (VIX) - often called the "fear gauge" - or Put/Call ratios and the American Association of Individual Investors (AAII) sentiment surveys have served as the traditional measures of market mood 11. When the VIX spikes above 30, it historically signals widespread panic; when the AAII survey shows bullish investors exceeding 70%, contrarian traders begin preparing for a market top 1.

However, these traditional quantitative indicators share a critical flaw: they are lagging barometers. They reflect what the market has already done in response to fear or greed, not the underlying emotions currently forming in the market 13.

Furthermore, many novice traders fall into the trap of believing that algorithmic analysis or specific chart patterns can guarantee future performance. A common misconception in algorithmic trading is that artificial intelligence can serve as a flawless predictive engine. In reality, no trading platform or artificial intelligence model can guarantee profits 4. Advanced deep learning models are not a path to guaranteed riches, nor do they possess perfect foresight. Their success depends entirely on the quality of the strategy being executed, the integrity of the data analyzed, and the strict risk parameters followed 45.

Similarly, traditional technical analysis fails when divorced from broader market context. Chart patterns, such as a "Head and Shoulders" or a "Bull Flag," cannot accurately predict the future in isolation 6. Trading a bullish pattern during a broad macroeconomic downtrend is statistically likely to fail because prevailing market conditions consistently triumph over isolated technical setups 6. Financial sentiment analysis bridges this gap by providing the missing contextual layer. It measures the "mood" of the market, helping traders understand the fundamental psychological drivers behind short-term price action and volume spikes 34.

The Mechanics and Growth of Market Mood

Sentiment analysis, frequently referred to as opinion mining, is a specialized branch of natural language processing (NLP) that identifies and categorizes the tone of written text 28. By continuously ingesting unstructured data - such as live social media feeds, global news wires, Reddit forums, regulatory filings, and corporate communications - algorithms quantify the optimism, pessimism, or neutrality surrounding a specific stock, sector, or macroeconomic event 310.

The commercial demand for these capabilities has triggered explosive growth in the underlying technology sector. The global market for sentiment analytics platforms was valued at approximately $4.68 billion to $5.1 billion in 2024 1112. Driven by rapid advancements in machine learning and the proliferation of digital communication platforms, the market is projected to grow at a compound annual growth rate (CAGR) of over 14%, potentially reaching nearly $18 billion by 2034 1112. The retail and Banking, Financial Services, and Insurance (BFSI) sectors are currently the largest adopters of this technology, utilizing it heavily for customer retention, risk modeling, and algorithmic trading execution 12. Geographically, North America currently holds the largest market share due to its advanced artificial intelligence infrastructure, though the Asia-Pacific region is emerging as a high-growth sector driven by increasing digital transformation 1112.

Instead of replacing traditional financial metrics, sentiment data acts as an essential complementary feature. In sophisticated quantitative models, sentiment acts as an early warning system. A gradual shift in public perception or a sudden surge in negative social media chatter often precedes an actual drop in a company's stock price, giving sentiment-aware traders an anticipatory edge before the broader market reacts to the news 313.

The Evolution of Sentiment Extraction

The technology driving financial sentiment analysis has undergone a radical transformation over the last decade. It has evolved from rudimentary, rule-based word-counting exercises to highly sophisticated, context-aware reasoning engines capable of parsing dense financial jargon.

The Limitations of Lexicons and Dictionaries

Early iterations of financial sentiment analysis relied entirely on lexicon-based approaches, most notably the Loughran-McDonald dictionary 1445. These systems functioned by scanning a text and assigning polarity scores based on a pre-defined list of "positive" and "negative" words. While computationally simple and highly interpretable, static dictionaries are inherently rigid 14.

Lexicon methods consistently struggle with the nuances of human communication, particularly in specialized domains like finance 67. For instance, a dictionary model might flag the word "liability" or "debt" as inherently negative, even though these terms are entirely neutral and standard in corporate balance sheet reporting. Furthermore, static dictionaries are blind to context, sarcasm, and negation. A headline stating, "Apple reports record revenue despite concerns over supply chain disruptions," contains both positive and negative elements; a dictionary model cannot easily deduce that the phrasing represents a nuanced, net-positive economic reality 8.

The Transition to Machine Learning

To address the glaring shortcomings of static dictionaries, data scientists introduced traditional machine learning models, such as Support Vector Machines (SVM), Logistic Regression, and Naïve Bayes classifiers 1467. These models introduced data-driven classification, allowing algorithms to be trained on historical financial texts to recognize broader statistical patterns in language.

While this improved flexibility, traditional machine learning models still required extensive manual feature engineering 67. They assumed a single overall sentiment at the whole-document level, failing to capture the multi-faceted nature of risk where a single article might express bullish sentiment regarding a company's revenue but bearish sentiment regarding its regulatory outlook 7. They also struggled with complex sentence structures and the subtle semantic shifts common in volatile economic climates.

The Large Language Model Revolution

The true breakthrough in sentiment analysis arrived with the advent of transformer-based Large Language Models (LLMs). Models like FinBERT (a version of Google's BERT architecture specifically fine-tuned on massive financial corpora), RoBERTa, and generative autoregressive models like GPT-4, OPT, and LLaMA have shifted the paradigm toward deep contextual learning 1489.

Unlike earlier models, LLMs do not simply count words; they utilize self-attention mechanisms to understand the deep semantic relationships between words, capturing phrasing, negations, and subtle contextual cues 78. FinBERT, for example, has demonstrated up to 97.35% accuracy on financial phrase banks 1.

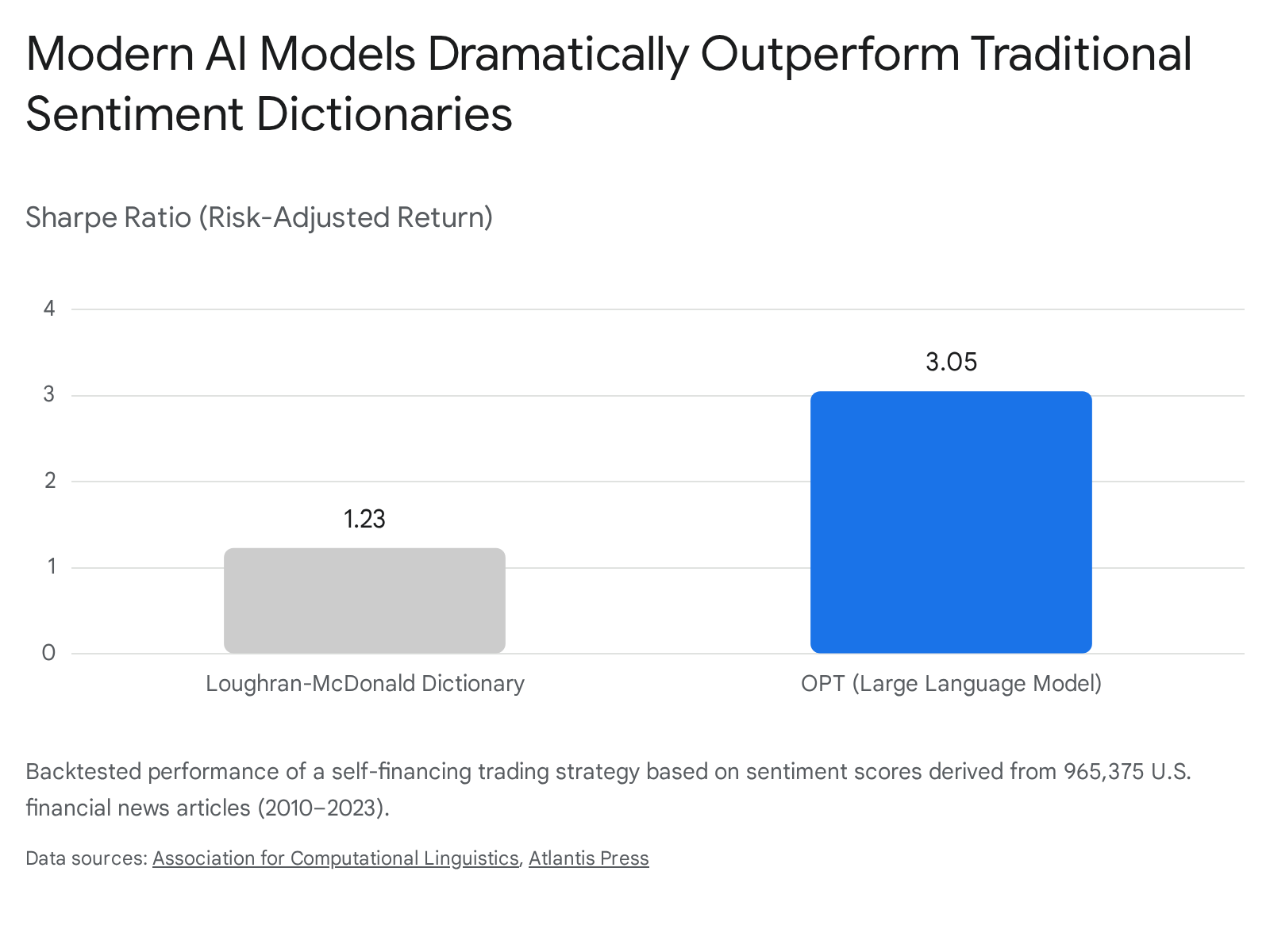

The performance gap between LLMs and legacy systems is profound. In a massive study analyzing 965,375 U.S. financial news articles published between 2010 and 2023, researchers found that GPT-based models significantly outperformed traditional methods. The advanced LLM achieved a directional prediction accuracy of 74.4% for stock market returns 4510.

When deployed in a simulated self-financing trading strategy over the sample period, the LLM-driven strategy generated a Sharpe ratio (a standard metric of risk-adjusted return) of 3.05, compared to a mere 1.23 for the dictionary-based benchmark model 45.

Further innovations, such as Direct Preference Optimization (FinDPO), have allowed researchers to transform discrete sentiment predictions into continuous, rankable probabilities, allowing algorithms to maintain substantial positive returns even when accounting for realistic transaction costs 9.

Decoding the Signals: News Media Versus Social Media

Not all textual data impacts the financial markets equally. A core operational task of modern financial sentiment analysis is distinguishing between the slow, steady drumbeat of traditional financial news and the rapid, highly volatile spikes of social media chatter. Empirical research indicates that these two mediums interact with asset prices in fundamentally different ways, requiring distinct algorithmic strategies 1112.

Traditional Financial News: The Slow Burn

Traditional news media - such as reports from Bloomberg, Reuters, Forbes, or The Wall Street Journal - is highly curated. It is typically grounded in corporate fundamentals, regulatory filings, central bank policy, or verified macroeconomic data 121314.

Because traditional news often conveys structural changes to a company's fundamental valuation, its impact on stock prices tends to be persistent. News signals have a slower "decay rate." A negative earnings report or a major macroeconomic policy shift covered by major outlets will influence institutional buying and selling behavior for days, weeks, or even months 1213. Interestingly, negative news tends to have an asymmetric effect; bad news often lingers longer in the market's collective memory and produces more persistent volatility than positive news 1226.

Social Media Chatter: The Fast Decay

Conversely, social media platforms like Twitter (X), Reddit, and StockTwits represent the immediate, unfiltered emotional reactions of retail investors, market commentators, and automated bots 1327.

Social media is highly sensitive to the "herd effect," where traders, particularly individuals lacking deep informational advantages, blindly follow large volumes of positive or negative sentiment 1315. This dynamic frequently leads to rapid, short-term price fluctuations and massive spikes in trading volume, rather than long-term fundamental revaluations 1213.

Furthermore, social media sentiment decays incredibly fast. A viral narrative or a high-profile corporate bankruptcy might spike a stock's mention volume by over 500% for a few hours or days, but public attention and emotional intensity fade rapidly before the crowd moves to the next trending ticker 16.

The Latency and Decay Rate of Information

The distinction between these two data sources dictates how quantitative models are built.

| Feature | Traditional Financial News | Social Media Chatter |

|---|---|---|

| Primary Drivers | Fundamentals, macroeconomic data, earnings | Emotions, hype, retail trends, "herd effect" |

| Market Impact | Persistent price adjustments, long-term trends | Short-term volatility, sudden volume spikes |

| Signal Decay Rate | Slow (Days to Weeks) | Extremely Fast (Minutes to Days) |

| Algorithmic Use Case | Predictive models, long-term portfolio rebalancing | High-frequency trading, event-driven scalping |

Studies examining Granger causality - a statistical test used to determine whether one time series is useful in forecasting another - reveal complex dynamics between news, social media, and market returns. During periods of relative economic stability, news sentiment often significantly predicts future stock returns 13. However, during acute crisis periods, such as the initial shock of the COVID-19 pandemic, the relationship can invert. In these high-stress environments, extreme stock market crashes actually preceded changes in news and social media narratives, proving that the flow of financial information is deeply reflexive and responsive to price action 13.

When analyzing specific technology firms, the impact also varies by market capitalization. For instance, Twitter sentiment strongly correlates with trading volume and volatility for companies like Amazon and Microsoft, but appears less influential for Apple, whose massively established institutional trading base dilutes the effect of retail social media chatter 12.

How Institutional Traders Generate Alpha

For hedge funds and institutional asset managers, generating "alpha" - returns exceeding a standard benchmark like the S&P 500 - requires a distinct informational advantage. Natural language processing has graduated from an experimental tool to a core operational requirement for how these entities survive in the modern market 813.

High-Frequency Trading and Algorithmic Execution

In the modern quantitative landscape, speed is arguably as critical as accuracy. Before a human analyst can even process the end of a spoken sentence by a central bank chairman during a live economic broadcast, an institutional artificial intelligence has already transcribed the audio, analyzed the semantic tone, evaluated the macroeconomic implications, and executed thousands of trades in the $7 trillion daily forex market 45.

High-frequency trading (HFT) firms feed real-time sentiment data directly into their execution algorithms. A study analyzing low-latency news signals ("news about the news") found that institutional algorithms often react to sentiment data within the first 5 seconds of its release 14. This hyper-fast reaction can sometimes lead to algorithmic overreaction, which human traders then correct and mean-revert roughly 30 seconds later 14. By combining real-time sentiment streams with live order book data, these systems execute event-driven scalps to capitalize on micro-windows of opportunity before retail traders or traditional media can react 1330.

Forecasting Earnings and Corporate Events

Hedge funds deploy sophisticated multimodal sentiment models to analyze corporate earnings calls and regulatory announcements. Rather than merely waiting for the final revenue numbers to be published, algorithms evaluate the linguistic tone, hesitation, and specific phrasing used by a CEO or CFO during official communications. By comparing the real-time sentiment against historical baselines, an algorithm can anticipate whether a company is likely to beat, match, or miss expected performance expectations 1331.

Risk Management and Trade Crowding

A less discussed but equally critical application of sentiment analysis for institutional players is defensive risk management 832. In quantitative finance, a "crowded trade" occurs when too many investors - both retail and institutional - take the exact same position on a specific asset. If the market narrative suddenly shifts, the collective rush to exit the position causes liquidity to evaporate, triggering severe short squeezes and compounding losses 1734.

Hedge funds use social media tracking and news sentiment to detect when public excitement or institutional positioning is reaching dangerous extremes. By recognizing when a trade is overly crowded or when a specific sector is signaling hidden vulnerabilities, funds can proactively adjust their exposure 133217. This allows them to de-risk their portfolios ahead of a downturn or employ contrarian strategies - selling into periods of retail euphoria to protect their capital from inevitable mean-reversion 3218.

The Democratization of Data: Institutional Versus Retail Access

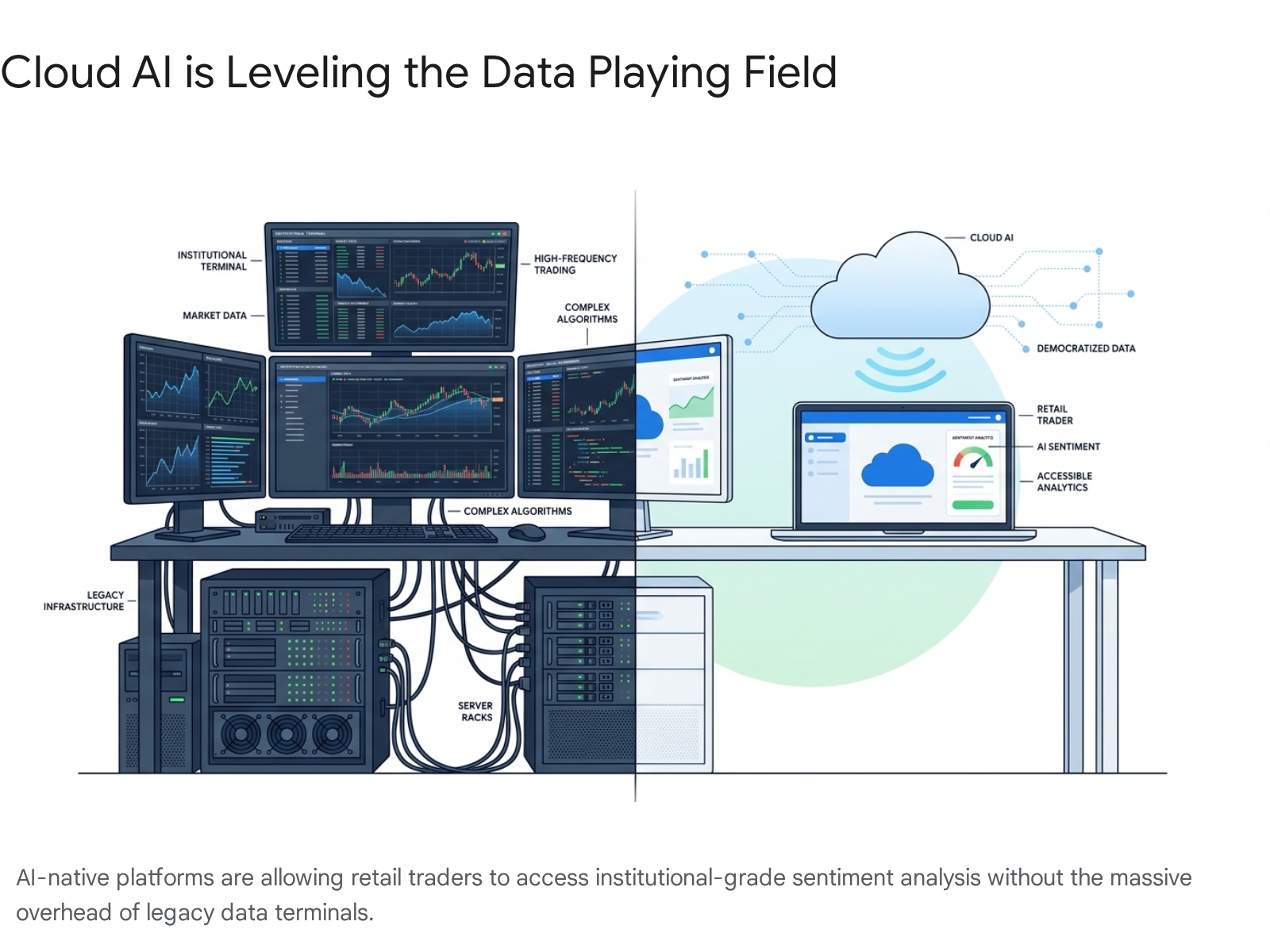

Historically, the extensive data infrastructure, proprietary network connections, and immense computing power required to run global sentiment analysis were exclusively available to elite Wall Street institutions 3637. Today, however, a massive technological shift is altering the balance of power.

The Bloomberg Terminal Monopoly

For decades, the undisputed standard for professional financial data has been the Bloomberg Terminal. It is an elite hardware and software ecosystem providing real-time data, news feeds, messaging, and trade execution across global asset classes 383940. However, the cost is staggering. The price of a single Bloomberg Terminal subscription has risen by roughly 60% over the past sixteen years, currently costing approximately $24,000 to $32,000 per user, per year 383941. Furthermore, enterprise API access (B-PIPE) can range from $50,000 to $200,000 annually 41.

For a large investment bank or a multi-billion-dollar hedge fund, this expense is viewed as an unavoidable cost of doing business. But for a retail investor, a solo swing trader, or a small quantitative startup, a Bloomberg Terminal is prohibitively expensive 384019.

The Rise of Cost-Effective AI Alternatives

The rapid decrease in cloud computing costs, the proliferation of open-source artificial intelligence frameworks, and the rise of API-first data providers have disrupted this monopoly 3740. Today, retail traders are armed with AI-native platforms that can replicate 70% to 80% of a Bloomberg Terminal's practical sentiment and fundamental analysis utility for a fraction of the legacy cost 384019.

Platforms such as Koyfin, TIKR, and Hudson Labs utilize the exact same underlying natural language processing technologies to scan SEC filings, summarize corporate earnings calls, and provide real-time sentiment scoring 3919. To put the economic shift into perspective, an automated AI corporate research query utilizing modern APIs might cost between $0.08 and $0.15 per execution, creating a massive cost-efficiency advantage over traditional data licenses 41.

{

"concept": "A conceptual illustration showing the stark contrast between the traditional, high-barrier institutional trading setup (Bloomberg terminals, massive server racks) and the modern, democratized retail setup (a laptop utilizing cloud-based AI tools).",

"reasoning_for_value": "The text explains a major shift in the financial landscape: the democratization of sentiment data. A visual representation of this 'David vs. Goliath' shift breaks up the heavy text and immediately communicates the concept of AI leveling the playing field for retail investors.",

"title": "Cloud AI is Leveling the Data Playing Field",

"visual_type": "Conceptual Illustration",

"generation_method": "IMAGE",

"justification_of_choice": "This is a conceptual, narrative-driven point about accessibility and market structure, not a specific data plot. An IMAGE generation is required to illustrate the qualitative difference between expensive legacy infrastructure and lightweight modern AI applications. Code cannot generate this illustrative metaphor.",

"caption": "AI-native platforms are allowing retail traders to access institutional-grade sentiment analysis without the massive overhead of legacy data terminals.",

"data_specification": {

"source_snippets_ids": [

64,

66,

68

],

"data_structure": "N/A - Image generation based on concept.",

"mapping": "N/A"

},

"design_and_interaction": {

"layout": "A split-screen or side-by-side illustration. Left side: A heavy, expensive institutional desk (multiple glowing screens, servers). Right side: A clean, minimalist setup with a single laptop displaying an AI interface and a cloud icon.",

"aesthetics": {

"style": "Editorial & Journalistic",

"color_palette": "Background: #FFFFFF. Institutional side: Darker, complex colors (navy, dark gray). Retail side: Light, modern, accessible colors (white, soft blue #1A73E8).",

"additional_details": "Keep the style modern flat-vector or clean 3D isometric to look professional and suitable for a financial research site."

},

"interactivity": "Static visual with no interactivity.",

"animation": "No animation."

}

}

This shift has led to a genuine democratization of market psychology. Independent retail traders no longer need a PhD in quantitative mathematics or a six-figure technology budget to incorporate advanced fear and greed metrics into their personal portfolios 137.

Compute Power and the Latency Divide

Despite the democratization of software, institutional traders still maintain a structural advantage in infrastructure. While retail traders can now access high-quality sentiment data, hedge funds operate on custom-built cloud infrastructure utilizing bare-metal graphic processing units (GPUs) and hyper-low-latency networking 362044.

In financial markets, integrating multiple data sources - such as combining social media sentiment with satellite imagery of retail parking lots or supply chain IoT sensors - requires immense temporal databases capable of aligning nanosecond-level market quotes with slower textual data 2044. A system that successfully analyzes sentiment but introduces significant processing latency will consistently underperform in a market where milliseconds dictate profitability 20. Therefore, while retail investors now have access to the intelligence, institutions still overwhelmingly win the race to execute upon it 3620.

Blind Spots: Geographic Diversity and Linguistic Nuance

Despite the aggressive marketing surrounding algorithmic trading, financial sentiment analysis is not flawless. The technology continues to grapple with severe limitations regarding language, context, and time.

Challenges in Non-Western Markets

While English-language financial models have reached impressive levels of sophistication, non-Western markets present a severe challenge. In Chinese and Japanese markets, sentiment analysis struggles significantly due to complex linguistic structures, segmentation issues, and a stark lack of large-scale annotated training data 2146.

Japanese text, for example, often lacks clear spaces between words. This means algorithms frequently misinterpret firm-specific proper nouns, blending them with specialized financial jargon and creating highly unreliable sentiment signals 22. Furthermore, research into the Japanese stock market indicates that if a Large Language Model carries an inherent, uncorrected company-specific bias from its general training data, it could inadvertently distort trading algorithms 46. If these biased LLMs become dominant in market operations, they could theoretically exert artificial upward or downward pressure on specific equities, distorting accurate price discovery 46. In many Asian markets, traditional multi-factor pricing models augmented with localized sentiment data are still required to out-perform generalized tools like ChatGPT 222324.

Sarcasm, Jargon, and Contextual Ambiguity

Human communication remains inherently messy. Even the most advanced NLP models occasionally stumble over sarcasm, irony, and internet slang, which are heavily prevalent on retail forums like Reddit and Twitter 310. Distinguishing signal from noise in a sea of retail chatter requires sophisticated filtering mechanisms.

Furthermore, financial text is littered with domain-specific jargon where the emotional meaning flips entirely depending on the macroeconomic context. For instance, the term "quantitative easing" was viewed as a positive, stabilizing intervention during the 2008 financial crisis. However, during the high-inflation environment of 2022, the exact same phrase was largely interpreted as an indicator of severe macroeconomic risk 25. Algorithms lacking broad historical context struggle to navigate these shifting definitions.

Model Decay and Performance Degradation

Financial language and market conditions evolve rapidly. A model trained to understand economic sentiment in 2019 may completely misinterpret the market realities of 2026. Researchers have documented an annual "decay rate" of 8 to 12 percentage points in the performance of financial sentiment analysis models over time 25. If these models are not continuously updated, retrained, and fine-tuned with new data, their predictive power degrades. This decay leads automated algorithms to execute trades based on outdated linguistic associations, emphasizing the need for continuous human oversight and dynamic model adaptation 25.

Bottom line

Financial sentiment analysis has evolved from simple dictionary-based word counting to sophisticated Large Language Models capable of interpreting the emotional and psychological pulse of the global market in real time. While institutional hedge funds heavily utilize these signals to execute high-frequency trades and navigate crowded market positions, a new wave of cloud-based AI platforms has successfully democratized this technology, offering retail investors institutional-grade insights at a fraction of legacy costs. However, sentiment analysis is not a guarantee of profitability; models remain vulnerable to rapid performance decay, struggle with non-English linguistic nuances, and must be utilized strictly as a statistical tool rather than an infallible predictive oracle.