What Investors Look For at YC's Spring 2026 Demo Day

Venture capital entering Y Combinator's June 2026 Demo Day is singularly focused on capital efficiency, proprietary data moats, and AI-native workflows that automate entire job functions rather than merely augmenting human labor. Investors are aggressively penalizing fragile "AI wrappers" built on public APIs, instead directing premium valuations toward founders who can demonstrate defensible unit margins, deep vertical expertise, and rapid physical-world deployments.

The Everyday Hook: Why the Spring 2026 Cohort Matters

Imagine a near-future scenario where a single text prompt does not just draft a marketing email, but autonomously negotiates a commercial lease, updates your company's enterprise resource planning (ERP) software, pays the resulting invoice, and then physically dispatches a drone to inspect a supply chain bottleneck. That is the baseline economic reality currently being built by the Y Combinator Spring 2026 (P26) batch 12.

For the general public, the artificial intelligence hype cycle of the early 2020s felt largely like magic tricks on a screen - chatbots that could write sonnets or pass the bar exam. But for the 1,500 invite-only investors gathering in San Francisco on Tuesday, June 16, 2026, the focus has shifted entirely from digital novelties to the physical and economic infrastructure of daily life 3.

The P26 cohort, consisting of 123 highly vetted startups, represents a profound maturation of the AI economy 2. These companies are not building parlor tricks; they are building the operating systems for autonomous financial advisors, AI-powered healthcare intake coordinators, and modular robotic pitstops for self-driving cars 45. Understanding what venture capitalists (VCs) are looking to fund at this exact moment offers a crystal-clear window into how consumer technology, workplace software, and global industries will function by the end of the decade.

Because official Demo Day performance metrics for P26 will not crystallize until the actual event, venture analysts are carefully projecting expectations based on the unprecedented metrics of the preceding Winter 2026 (W26) batch and early leaked traction from current P26 founders 67. What the data reveals is a venture landscape that has lost its patience for untested ideas but retains an unlimited appetite for disciplined, highly technical execution.

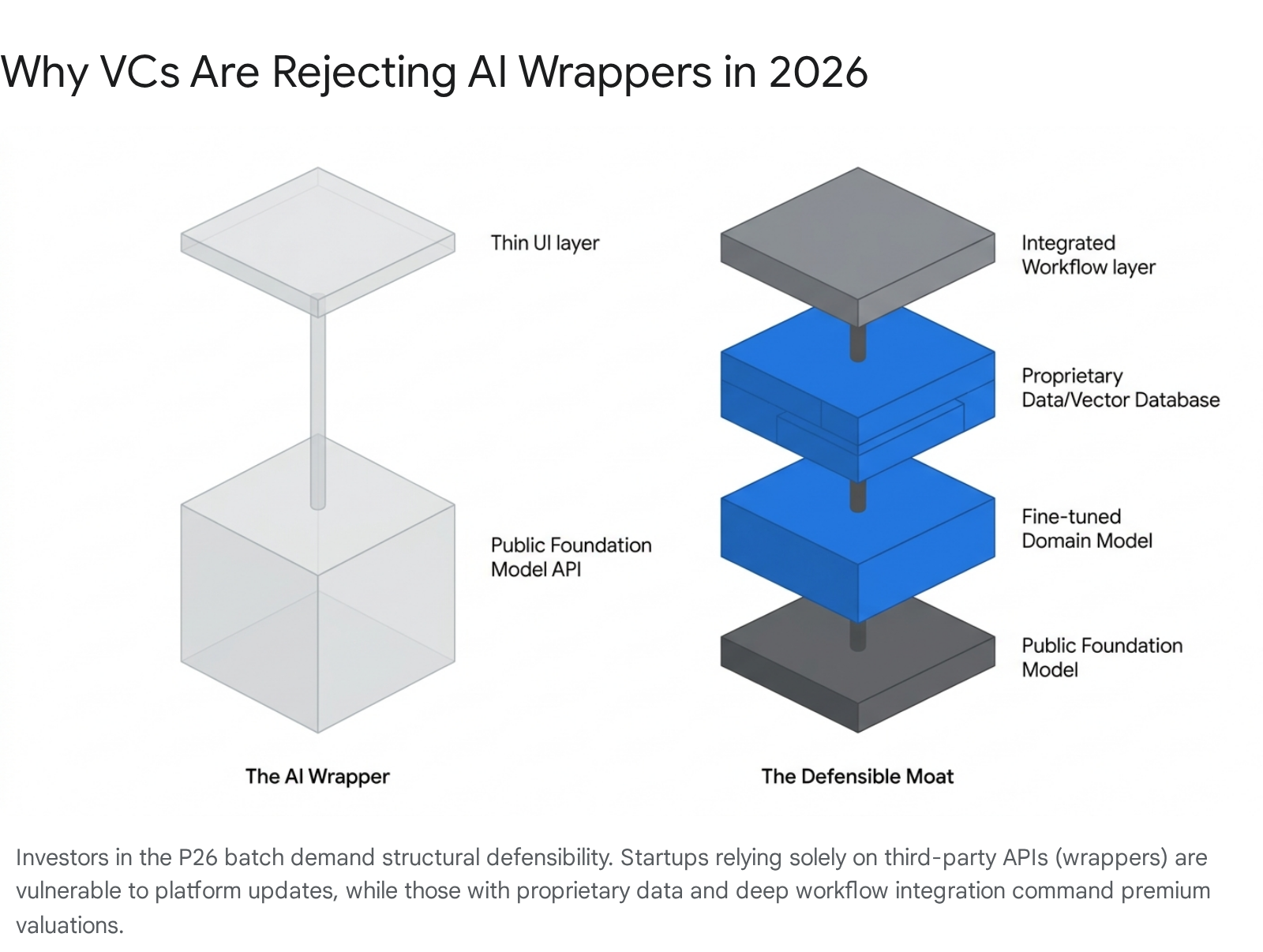

Misconception vs. Reality: The Death of the "AI Wrapper"

A dominant misconception remaining from the 2023 tech boom is that anyone who patches together an interface using OpenAI's ChatGPT or Anthropic's Claude API can raise millions in seed capital. The reality in 2026 is brutally different. Investors are experiencing extreme fatigue with "AI wrappers" - products that simply use a third-party foundation model, add a basic user interface, and possess no unique technical capability 88.

By early 2026, roughly 70% of 4,000 AI startup pitches analyzed in a major industry survey were dismissed by VCs specifically because they were categorized as wrappers 10. The fatal flaw of a wrapper is its complete lack of a "moat" - a defensible competitive advantage. As foundation models natively absorb more features year over year (adding memory, file uploads, web browsing, code execution, and autonomous reasoning), the thin layer of value provided by a wrapper evaporates overnight 8.

When evaluating startups at the P26 Demo Day, seed investors require founders to prove defensibility through three primary avenues:

1. Proprietary Data Moats

Simply calling an API does not distinguish a real AI company. True defensibility comes from owning proprietary datasets, graphs of domain-specific knowledge, and high-quality longitudinal workflow data 8. Startups that do not possess the underlying data that feeds their models are essentially renting intelligence. Conversely, startups building in regulated verticals with access to real, high-value industry datasets - such as legal, medical, or financial records - build a moat that foundation model companies cannot easily replicate 88.

2. Deep Workflow Integration

If a startup's AI product merely answers questions, it is a commodity 8. The new standard is workflow integration. If an AI product becomes embedded inside a company's operations - managing customer support pipelines, handling insurance claims, coordinating caregiver scheduling, or running internal documentation - it becomes incredibly difficult to replace 9. Investors look for "agentic" software that runs end-to-end operations seamlessly, operating alongside human workers or replacing manual bottlenecks entirely 19.

3. Infrastructure and Cost Control

Wrapper startups often rely on an inherently flawed economic model: they face high inference costs per query, have low customer willingness to pay, and possess no strategy for optimizing infrastructure or GPU costs 8. Investors at YC are heavily favoring startups that control their own infrastructure. This includes smart model routing (knowing when to offload simple tasks to cheap models and complex tasks to expensive ones), fine-tuning proprietary small models, and establishing vector retrieval strategies 8.

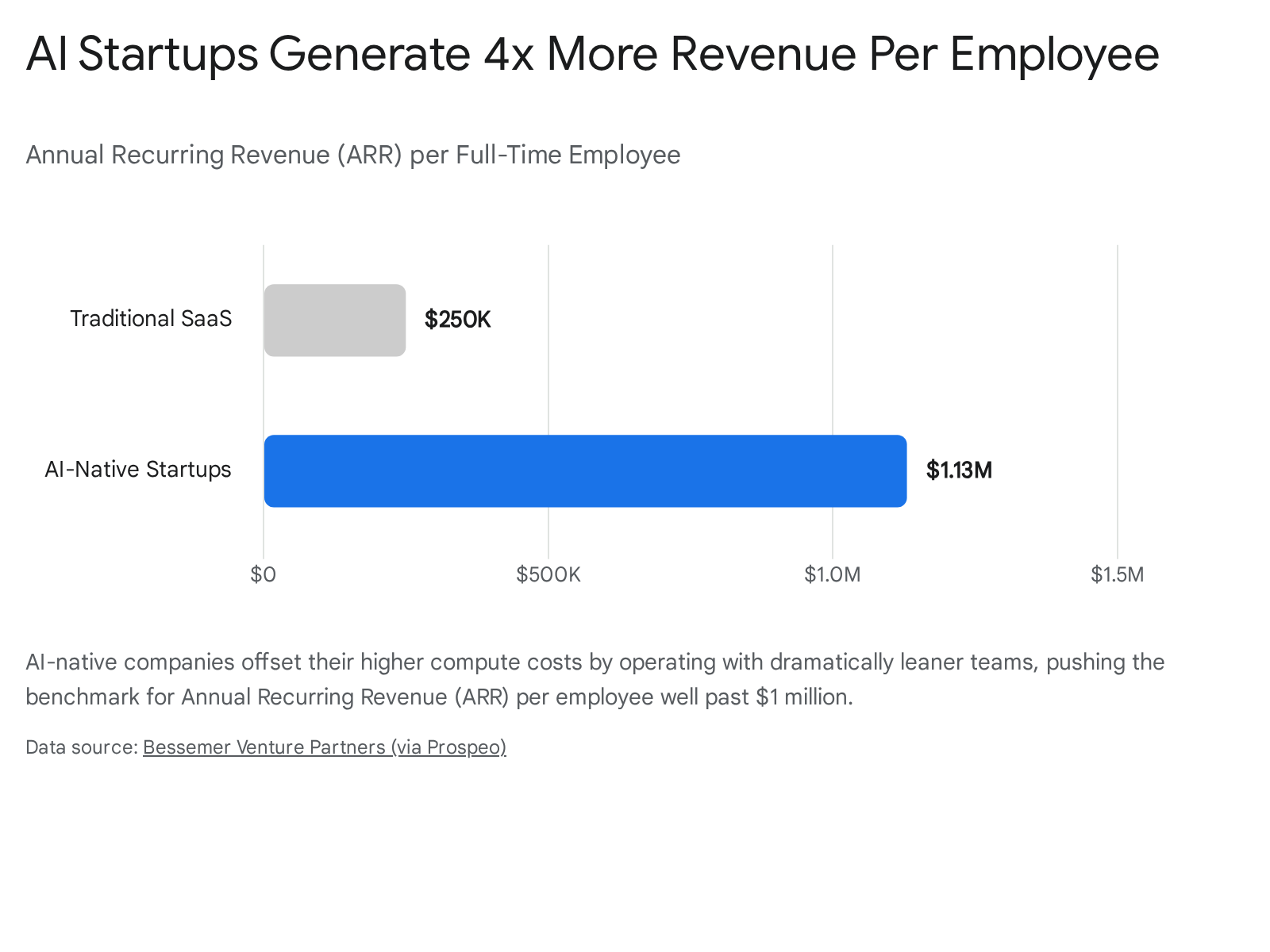

Traditional SaaS vs. Emerging AI Valuation Metrics

As the technology stack shifts, the fundamental financial equations investors use to value startups are undergoing a radical transformation. The classic Software-as-a-Service (SaaS) model was beloved by Wall Street and venture capitalists because it relied on incredibly high gross margins - often 80% or higher - since the marginal cost to serve an additional user was practically zero 12.

AI-native companies operate under entirely different physics. Every single time a user interacts with an AI agent, it triggers a compute-heavy query to a Large Language Model (LLM). This introduces a direct, inescapable variable cost 13. Consequently, AI-native startups typically run gross margins 25 to 30 percentage points below classic SaaS 1214.

Despite these inherently lower margins, investors are actively paying premium multiples for AI startups. The reason is velocity. Breakout AI companies - dubbed "Supernovas" by firms like Bessemer Venture Partners - are reaching $100 million in Annual Recurring Revenue (ARR) in 12 to 24 months, a milestone that traditionally took elite SaaS companies five to seven years 1516. Because AI assumes the heavy lifting of product development and customer service, these startups also scale with dramatically leaner human teams 1510.

| Financial Metric | Traditional SaaS Benchmark (2026) | AI-Native SaaS Benchmark (2026) | Investor Context & Market Reality |

|---|---|---|---|

| Gross Margin | 75% - 85%+ | 40% - 60% (often starting ~25%) | AI compute costs directly suppress margins. VCs accept this if startups show a clear path to optimizing inference costs over time 121410. |

| ARR per Full-Time Employee | $200,000 - $300,000 | $1.13 Million+ | AI startups require vastly smaller teams for the same output. In recent YC batches, up to 11% operate as solo founders 714. |

| CAC Payback Period | 12 - 18 months | 7.5 - 12 months | Because gross margins are lower, it takes longer to earn back acquisition costs. AI startups cannot survive the slow payback periods of legacy SaaS 1210. |

| Rule of 40 (Growth % + Profit %) | Target > 40% (Median ~35%) | 60% - 80%+ | AI companies frequently operate at a loss initially but compensate with explosive top-line growth, easily blowing past traditional efficiency rules 1410. |

| First-Year ARR Expectations | $2M - $5M | ~$40M (for "Supernova" breakouts) | The growth curve has completely warped. Investors now expect top-tier AI companies to achieve hyper-scale immediately 14. |

Note: Data reflects normalized venture benchmarks moving into mid-2026. Seed-stage companies at Demo Day are evaluated on early traction signals that point toward these mature benchmarks 1415.

Deconstructing the CAC Payback Reality

One of the most critical adjustments investors are making in 2026 revolves around the Customer Acquisition Cost (CAC) payback period. In classic SaaS, a 12-month payback period calculated against an 80% gross margin was considered healthy 12. However, if an AI startup operates at a 50% gross margin, that same financial dynamic mathematically stretches the true payback period out to 7.5 months. If a founder pitches a traditional 12-month payback while operating on AI margins, they are quietly accepting a recovery period that is severely prolonged in cash terms 12.

This is why P26 investors are ruthlessly vetting go-to-market strategies. Founders must prove they can generate $1 of revenue for less than $1 of burn 18. The era of "growth at all costs" - subsidizing heavy marketing spend with endless VC cash - has definitively ended 1819.

What Are the Dominant Themes in the P26 Batch?

Beyond the underlying economics, the precise composition of the YC P26 batch reveals exactly where smart capital is placing its bets. Analyzing the 123 companies slated to present highlights a fascinating pivot: software is no longer enough. The market is returning to physical engineering, highly regulated industries, and tools built specifically for developers 2.

The Hard Stuff is Back: Hardware and Deep Tech

Perhaps the most counterintuitive trend in the age of generative AI is the venture world's aggressive return to atoms over bits. Roughly one in eight companies in recent YC cohorts (spanning both the P26 and the preceding W26 batches) are building physical products. This includes robotics, drones, wearables, space hardware, and biotechnology 5711.

Because the "easy" software application layer has been widely commoditized by large foundation models, ambitious founders are applying AI to physical-world problems where competition remains thin and barriers to entry are incredibly high 6.

Notable physical innovations emerging in the P26 batch include: * Defense and Space: 9 Mothers is engineering AI-powered point defense turrets designed to engage fast-moving FPV drones, while Dispatch is developing dedicated spacecraft specifically for returning cargo from orbit 2. * Consumer Wearables and Health: Anoria is developing a wearable device that reads human emotions to actively enhance emotional intelligence, while Imperfect serves as an AI training coach connected directly to athletes' biometric wearables 2. * The Valuation Proof: Hardware is no longer viewed as a sluggish, capital-intensive trap. In the previous batch, a consumer hardware startup named Pocket walked into Demo Day with an astonishing $27 million in ARR, driven largely by hardware sales. This completely upended the traditional venture belief that only pure software can scale fast enough to justify seed economics 61121.

Vertical AI in Regulated Markets

General-purpose agents - the "do anything" horizontal tools - are rapidly losing flavor among investors, primarily because tech giants like Google and Microsoft eventually build those features natively 822. Instead, the P26 batch is heavily concentrated on hyper-specific, vertical AI. Startups operating in healthcare, legal technology, and financial services are surging. Healthcare alone now comprises nearly 10% of YC cohorts 623.

Investors heavily favor these markets because they feature "hard regulatory moats," complex legacy workflows, and massive existing budgets 6. In the P26 batch, a company like Zatanna operates as an adaptive AI intake coordinator specifically for medical offices 5. Another standout, Harbor, acts as an AI system-of-record designed to automate clinical trial data 2. The rapid ascension of previous YC alumni like Harvey (specializing in legal AI) and Legora, both of which hit unicorn valuations shortly after their respective demo days, has provided investors with a proven, highly lucrative template for vertical AI success 62223.

The Agentic Infrastructure Layer

With the explosion of autonomous agents taking on white-collar work, a massive new "builder-for-builders" software layer has emerged. Startups are no longer just building AI tools for end consumers; they are building the picks and shovels required to monitor, sandbox, and secure the AI itself 27.

Roughly 17% of recent batches are focused purely on developer infrastructure 7. Companies like Indexable (providing sandbox infrastructure for AI agents to fork environments rapidly) and Arga Labs (an automated code validation platform post-deployment) are foundational bets for investors. VCs recognize that as Fortune 500 companies increasingly deploy AI agents, keeping those agents reliable in production environments becomes a mission-critical, high-margin business 24.

Global Venture Capital Perspectives in 2026

While Y Combinator is headquartered in San Francisco, the investor audience dialing into the June 2026 Demo Day is aggressively global 324. The macroeconomic funding climate has largely recovered from the severe high-interest-rate drought of 2023 and 2024. Inflation has cooled, interest rates have stabilized, and liquidity is returning to the markets 19. However, capital deployment strategies are highly nuanced across different geographic regions.

| Global Region | 2026 Investment Climate & VC Focus | Key Market Dynamics |

|---|---|---|

| North America | Highly concentrated AI dominance. Focus on infrastructure, defense tech, and vertical SaaS 12. | Capital is abundant but barbell-shaped; mega-rounds for AI winners, high scrutiny for early-stage 19. |

| Europe | Deep Tech, AI, and Science-driven innovation. Limited Partners rank deep tech as a top priority 1213. | Record-breaking AI deals (61.3% of VC value in early 2026). Focus on robotics, biology, and climate tech 12. |

| Middle East | Unprecedented liquidity. Sovereign wealth heavily backing AI infrastructure and fintech 13. | Q3 2025 saw a record $1.2B in VC raised. Surging M&A activity to build regional tech champions 13. |

| Asia-Pacific | Steady deal volume, heavy focus on AI leapfrogging legacy supply chains and manufacturing 12. | Companies scaling to $100M revenue much faster than historically possible due to AI efficiencies 27. |

| Latin America | Maturing ecosystem focused on fintech, digital commerce, and stablecoin adoption 2413. | A year of liquidity preparation (secondaries and pre-IPO). 39 unicorns established, focusing on profitability 2413. |

European investors attending Demo Day are highly receptive to YC startups building complex systems like autonomous robotics and foundational infrastructure, prioritizing scientific depth over consumer apps 1213. Meanwhile, Middle Eastern investors are looking for startups that can immediately scale across emerging markets, bringing massive sovereign wealth liquidity to competitive funding rounds 13.

In developing markets across Asia and Latin America, businesses are leveraging AI to "leapfrog" traditional legacy software entirely. YC companies targeting global supply chains - such as Saudara.ai, an AI-native sourcing agency connecting businesses with vetted Indonesian suppliers - appeal directly to APAC investors looking to modernize regional trade 2. Furthermore, the stablecoin market has grown into a $250 billion asset class, providing the backbone for a new global financial system in regions where local currencies face volatility, a trend LATAM investors are watching closely 13.

FAQ: Practical Takeaways for Founders

Do I need massive revenue to raise at Demo Day in 2026? While Pre-Seed and Seed investors still occasionally bet on exceptional technical teams without revenue, the baseline has risen significantly. Investors now expect clear early validation - often looking for $300K to $500K in ARR for a highly competitive Seed round 28. However, raw growth is no longer enough; unit economics matter deeply. Startups have successfully entered the P26 batch with $70K in Monthly Recurring Revenue (MRR), using the intense YC program as a forcing function to double that figure within weeks 293031.

How do I defend my startup against an OpenAI or Anthropic model update? If your entire product can be rendered obsolete by a foundation model releasing a new native feature, you do not have a durable company; you have a feature 89. Founders must build defensibility from day one. This means owning proprietary data, deeply embedding your product into a customer's core workflow (e.g., integrating with their internal ERP and bank accounts), or building in vertical niches with high compliance and regulatory barriers (like medical billing or industrial supply chains) 8822.

Should I hide the fact that I used AI coding agents to build my product? Absolutely not. In 2026, investors expect it. The speed of software development has compressed exponentially. YC partners actively push founders to use tools like Cursor, Claude Code, and OpenAI's Codex to ship features faster 323334. The expectation is that a two-person founding team today can achieve in weeks what took a team of five senior engineers a full year to build in 2022. This hyper-efficiency is exactly what enables the rise of the "solo founder," who remarkably made up 11% of the preceding W26 cohort 57.

Is the "YC Premium" valuation still a reality? Founders continually balance the prestige and network of YC against the cost of equity. YC currently takes 7% to 14% of a company in exchange for $500,000, establishing an implied entry valuation of roughly $3.5 million to $7 million 33. While standard seed rounds in the broader 2026 market average a $16 million valuation, investors historically pay a massive premium post-Demo Day for YC companies 18. Data published prior to the W26 batch indicated that top-quartile YC investments yielded an 8x return, and some observers predicted up to a 10% unicorn hit rate for recent cohorts - drastically higher than the industry average 6.

Bottom line

The Y Combinator P26 Demo Day marks a definitive end to the speculative, "growth-at-all-costs" era of software and the dawn of disciplined, AI-native automation. Investors are hunting for heavily defensible companies equipped with proprietary data, deep workflow integration, and sustainable unit economics that explicitly account for high AI compute costs. While traditional SaaS multiples have cooled, immense capital is flowing into founders solving complex physical-world problems through hardware, highly regulated vertical AI, and the underlying infrastructure required to safely scale autonomous systems across the global economy.