Venture Capital Funding, Valuations, and Exits in 2026

The global venture capital market in 2026 has reached historic funding highs driven almost entirely by a concentrated artificial intelligence arms race, leaving the rest of the startup ecosystem to navigate an austere, highly selective environment. For founders and investors, success now requires adapting to a sharply bifurcated landscape where AI infrastructure commands massive premiums, while traditional sectors must prove rigorous capital efficiency ahead of an impending wave of trillion-dollar mega-IPOs.

The $300 Billion Quarter: An Era of Extremes

To understand the venture capital landscape in 2026, one must look past the top-line numbers, because the headlines paint a picture of an industry in an unprecedented boom. In the first quarter of 2026 alone, global venture funding shattered all previous records, with investors deploying an estimated $300 billion across 6,000 startups 123. To put this into perspective, this single quarter saw a 150% increase in deployed capital compared to both the previous quarter and the same period a year prior 13. In just three months, the market absorbed nearly 70% of the total venture capital spent throughout the entirety of 2025 23.

The United States and Canada were the primary beneficiaries of this capital tsunami, securing a staggering $252.6 billion from seed- through growth-stage rounds 4. This effectively dwarfed the previous all-time North American quarterly record of $95.7 billion set during the pandemic-era peak of Q3 2021 4.

However, describing this as a broad market recovery would be fundamentally inaccurate. The 2026 venture market is defined by a phenomenon analysts are calling "The Great Bifurcation." Capital is not flowing evenly; it is surging toward a microscopic percentage of the market. In the U.S., a staggering 73.2% of the total Q1 deal value was consumed by just five transactions 567.

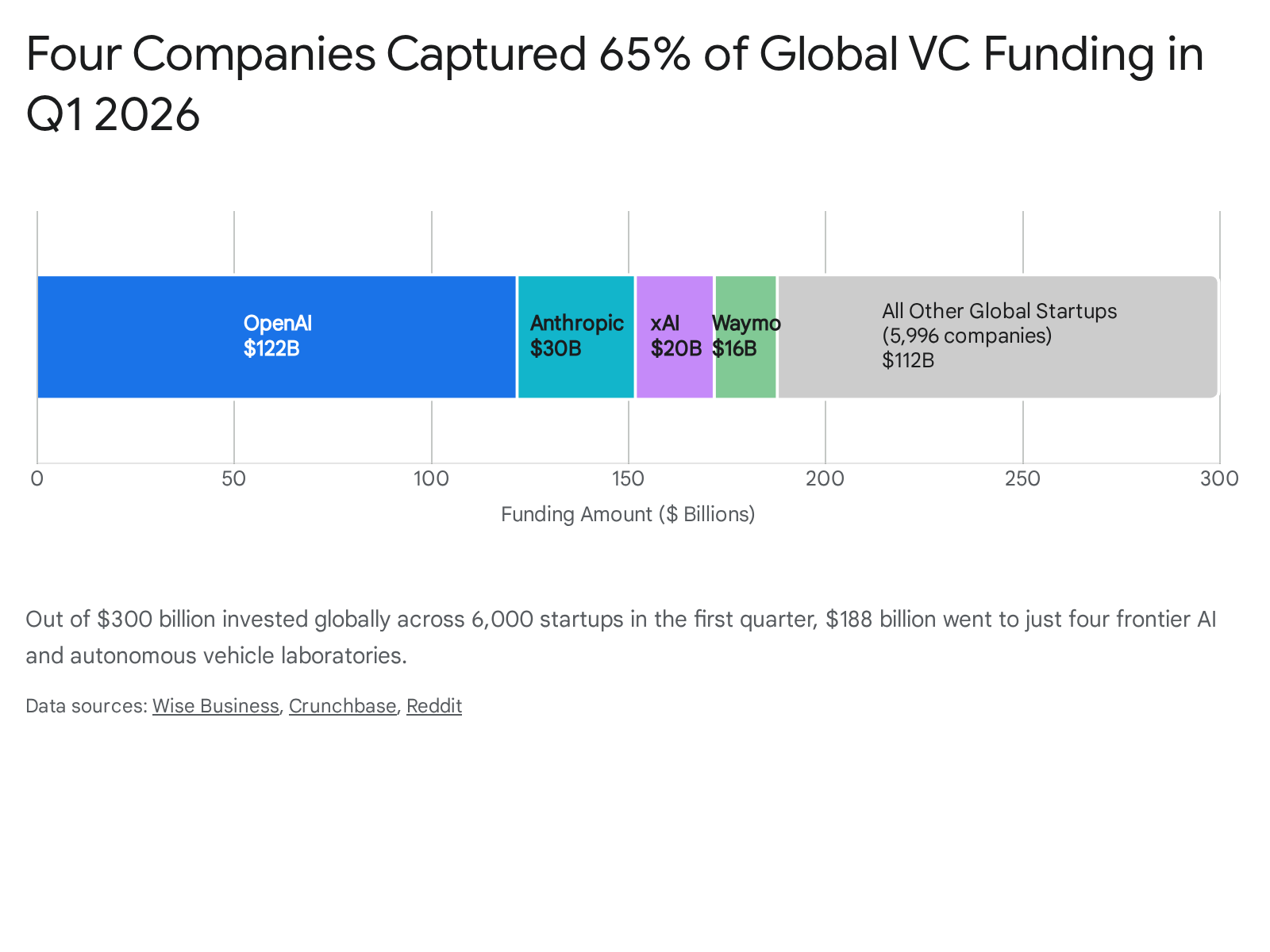

Globally, the concentration is equally severe. Just four frontier technology companies - OpenAI ($122 billion), Anthropic ($30 billion), xAI ($20 billion), and autonomous driving company Waymo ($16 billion) - collectively raised $188 billion 1288. This means that four companies captured 65% of all global venture capital in a single quarter 8.

This hyper-concentration highlights the reality for the average founder. While dollar volumes surged by 190% year-over-year in North America, the actual number of deals completed dropped by 26% 8. Investors are increasingly writing much larger checks to a significantly smaller pool of perceived winners 8. The bottom 50% of the startup market received merely 7% of total deployed capital 9.

Debating the Data: Are We Missing the Middle?

The massive influx of capital at the top has sparked a debate among industry analysts regarding how venture data is tracked. Traditional data providers rely heavily on survey-based approaches to track fund closures and deal sizes 11. Some industry insiders argue that this methodology is creating a false narrative of a "quiet year" for everyday fundraising. Because many emerging fund managers do not voluntarily report their activities, the reality of the middle market may be stronger than the declining deal counts suggest 11. Reports from independent groups note that limited partners (LPs) were wiring capital aggressively into new funds throughout late 2025 and early 2026, indicating that while capital is concentrated, the underlying ecosystem is far from frozen 11.

Startup Valuations: A Stage-by-Stage Breakdown

The concentration of capital into massive "consensus deals" is pushing valuations and round sizes higher across the entire venture lifecycle 610. To understand the market, it is essential to look at the shifting benchmarks required to raise capital at each specific stage of growth.

Pre-Seed and Seed: SAFEs and Expanding Floors

At the earliest stages of company building, the median post-money valuation hit an all-time high of $24 million in late 2025 and early 2026, up from $18 million the previous year 111213. Seed round sizes themselves are trending up toward $4 million to $5 million 14.

The mechanics of early-stage funding have also solidified. Unpriced instruments - specifically Simple Agreements for Future Equity (SAFEs) - have become the absolute default. In Q1 2026, convertible notes accounted for a record low of just 7% of pre-seed rounds, proving that founders and investors alike prefer the speed and standardized simplicity of the SAFE model 13. The geography of early-stage funding is also shifting subtly; the U.S. South overtook the Northeast in overall pre-seed share, with Miami eclipsing both Los Angeles and Boston as a primary hub for early-stage capital 13.

Series A and B: The Missing Middle

The Series A and B stages represent the most dramatic shifts in investor expectations. A few years ago, a Series A round might have averaged $8 million to $10 million; today, the average sits between $13 million and $15 million, with the median pre-money valuation jumping to $62 million 61014.

To justify these valuations, startups must present immaculate unit economics. For a Series A, top-quartile companies are generating nearly $6.9 million in Annual Recurring Revenue (ARR), with the median sitting around $2.8 million 17. By Series B, where the median pre-money valuation has reached $118.9 million, investors expect to see median ARR of $8.4 million, with the best companies pushing $14.9 million 1715. Investors at this stage are no longer funding experimentation; they are funding highly predictable, scalable revenue engines with payback periods (the time it takes to recover the cost of acquiring a customer) ideally under 12 months 19.

Late-Stage: The Decacorn Pipeline

At Series C and beyond, the market becomes severely bifurcated. The median Series C pre-money valuation surged to $579 million in Q1 2026, up from $167.2 million in 2020, with median deal sizes hitting $75 million 610.

For companies that cannot maintain explosive growth rates, this stage is perilous. A "down round" - raising capital at a lower valuation than the previous round - can devastate employee morale and heavily dilute founder ownership 2016. While the overall share of down rounds declined slightly in early 2026, many mature companies are simply choosing not to raise, relying on venture debt or severe cost-cutting to extend their runway until exit conditions improve 1718.

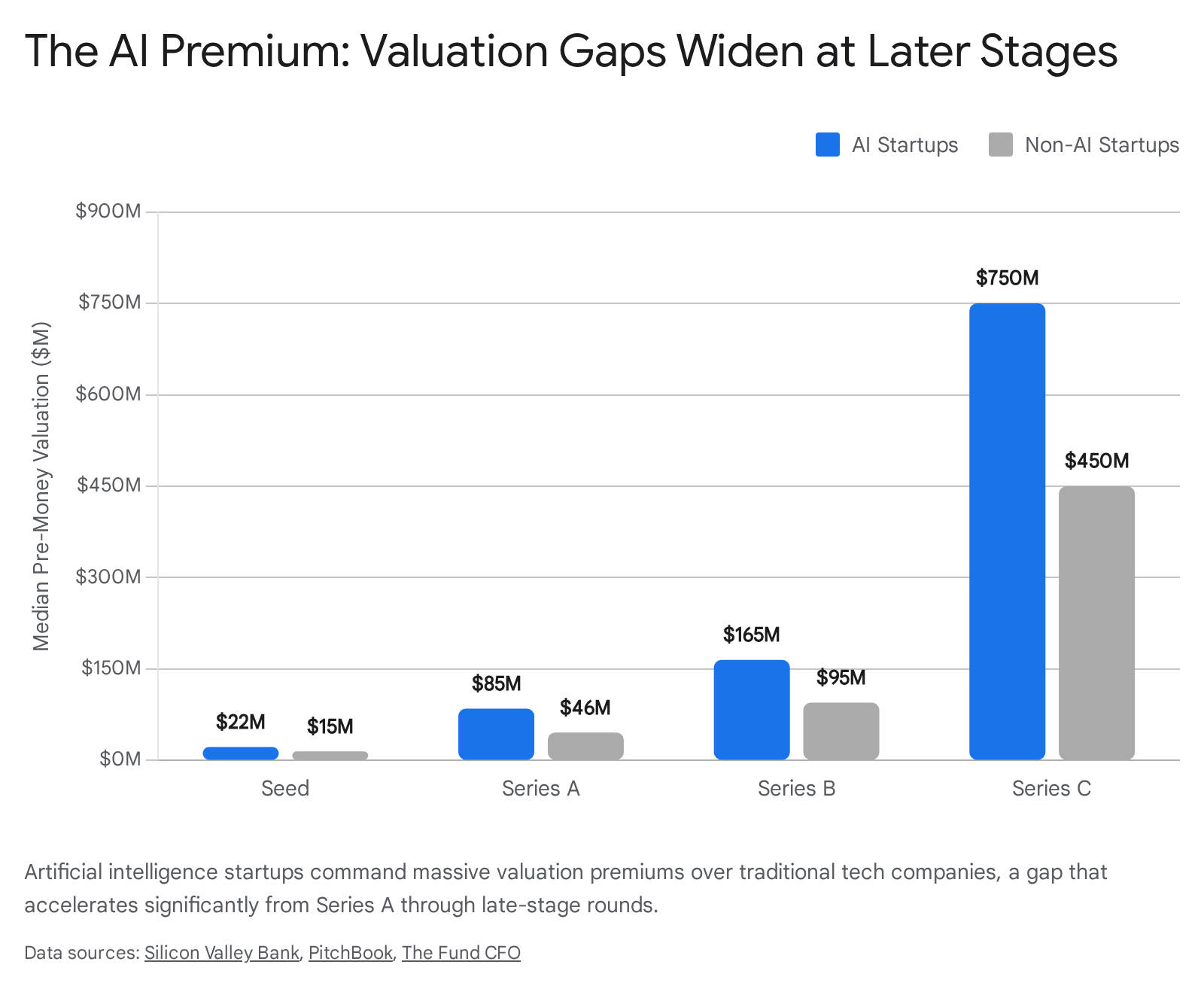

The Unprecedented AI Valuation Premium

It is impossible to discuss 2026 valuations without isolating the impact of Artificial Intelligence. Simply put, AI companies play by an entirely different set of rules. At the Series A stage, AI startups command an 84% valuation premium over their non-AI peers 19. By Series D and beyond, that premium balloons to 222% 9.

This premium is driven by a mix of genuine technological promise and the sheer cost of building foundational AI models. Startups require massive rounds just to secure compute power and hardware 11. However, this concentration leaves traditional software-as-a-service (SaaS), consumer, and hardware founders fighting for a much smaller slice of the capital pie, requiring them to operate with a level of financial discipline that was largely ignored during the 2021 boom 1925.

| Funding Stage | Median Pre-Money Valuation (All Sectors) | Typical Round Size | Revenue / Traction Benchmark |

|---|---|---|---|

| Seed | $18.4 - $24.0 Million | $4.0 - $5.0 Million | Pre-revenue / Initial pilot traction |

| Series A | $62.0 Million | $19.6 Million | $2.8M - $6.9M ARR |

| Series B | $118.9 Million | $29.4 Million | $8.4M - $14.9M ARR |

| Series C | $579.0 Million | $75.0 Million | $16.0M+ ARR |

Data aggregated from Q1 2026 market benchmarks. Note: AI-specific companies routinely exceed these medians by 80% to 200% depending on the stage 61011141715.

Geographic Trends: How Global Hubs are Evolving

While the United States remains the epicenter of the venture capital universe - accounting for 83% of the global funding total in Q1 - international ecosystems are maturing, specializing, and displaying unique structural advantages 3.

Europe: Deep Tech, Defense, and Profitability

European venture funding hit $25.7 billion in Q1 2026, marking its third consecutive quarter of growth and signaling a definitive end to its post-2022 slump 2620. The United Kingdom led the continent, absorbing $7.4 billion, while France ($2.9 billion) and Germany ($1.9 billion) followed 26.

The European market is diverging from the American model in several key ways. First, European investors place a much higher premium on capital efficiency and regulatory readiness 28. Remarkably, nearly 90% of VC-backed IPOs in Europe over the last year were EBITDA-positive, standing in stark contrast to the heavily unprofitable growth models often championed in Silicon Valley 29.

Second, the geographic and sector focus within Europe is shifting. France has established itself as the continent's undisputed leader in frontier AI laboratories, hosting heavily funded companies like Mistral and Advanced Machine Intelligence (which raised $1 billion in Q1) 2620. In Germany, a massive reorientation is underway. Munich is displacing Berlin as the country's primary magnet for capital. While Berlin spent the last decade building a reputation for consumer internet and B2C startups, Munich's focus on deep-tech, defense, and aerospace aligns perfectly with today's geopolitical realities and investor priorities 2621.

Asia-Pacific: Demographics, State Support, and Rapid IPOs

Venture investment in Asia rebounded strongly to $31.8 billion in Q1 2026, stabilizing after several turbulent years 2223. However, the dynamics of Asian venture capital differ significantly from the West, largely due to demographic pressures and capital structures.

In Japan, a severe labor shortage driven by a rapidly aging population is forcing aggressive integration of robotics and applied AI 23. Because deep-tech and hardware carry high research costs and long payback periods, Japanese venture rounds frequently involve collaborative investments between traditional VC funds, corporate entities, and government-backed programs 23.

In China, the AI funding pipeline operates under a distinct timeline. While U.S. AI giants like OpenAI and Anthropic can raise tens of billions in the private markets to fund their infrastructure, Chinese AI firms face a relative funding gap for compute infrastructure despite state support 33. Consequently, they are turning to the public markets much earlier to secure capital. Q1 2026 saw significant public listings from Chinese AI developers like Zhipu AI and MiniMax Group 33.

Meanwhile, India experienced a robust 30% quarter-over-quarter rebound, with startup funding surging to $4.76 billion 24. Notably, India saw a massive spike in venture debt funding, which tripled to nearly $693 million as founders sought to scale without diluting their equity in a tight valuation market 24.

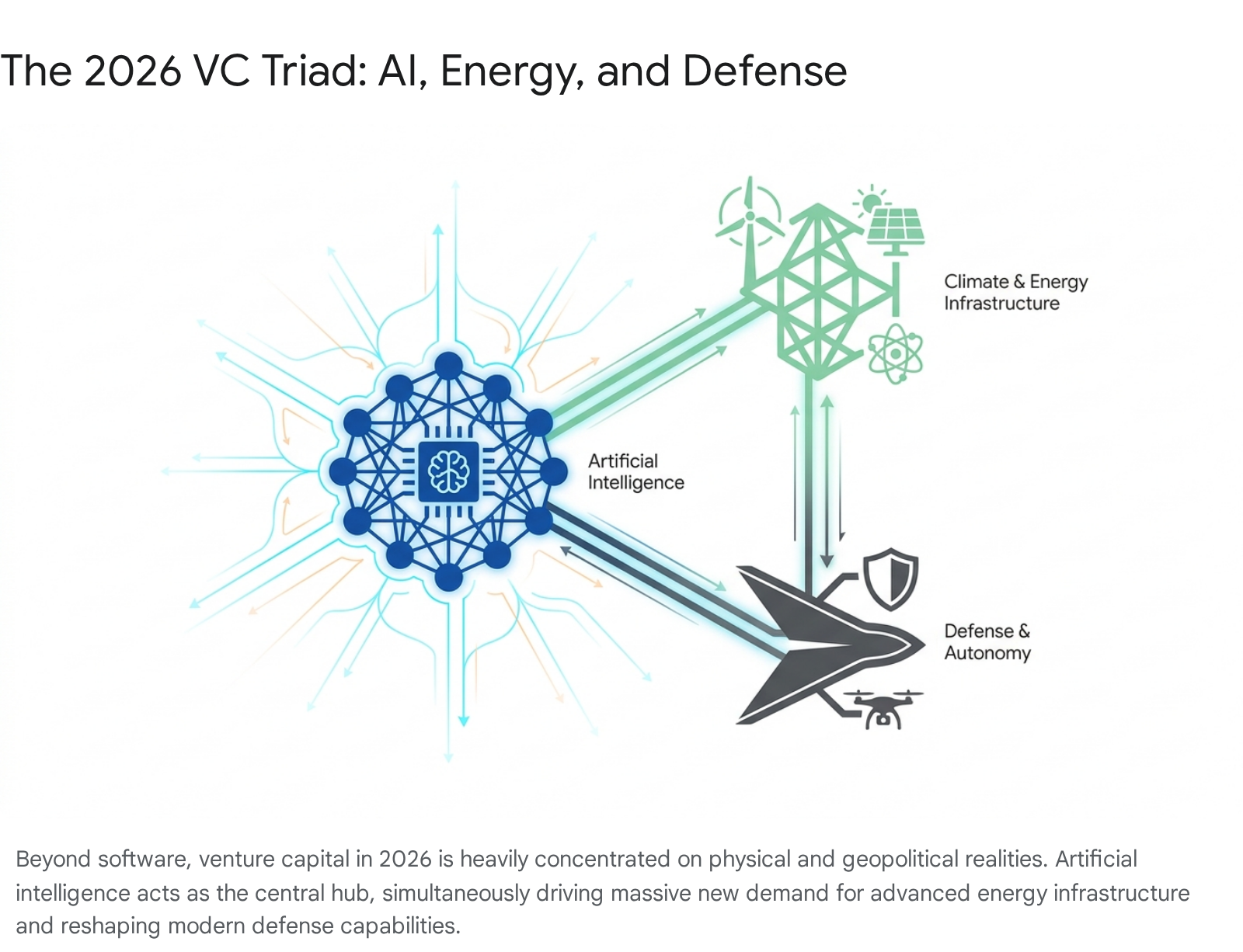

Sector Spotlight: Where the Smart Money is Flowing

Beyond the overarching shadow of foundational AI models, capital in 2026 is aggressively pursuing sectors grounded in physical reality, regulatory shifts, and geopolitical necessity.

Climate Tech and Energy Infrastructure

Climate technology venture capital reached $14.3 billion in Q1 2026, the strongest quarter since mid-2023 25. Interestingly, Europe has pulled ahead of North America as the primary hub for climate investment, claiming the three largest global deals of the quarter - including a $1.5 billion raise for UK-based Low Carbon Materials and $1.2 billion for German renewable platform Cloover 2526.

A major catalyst for this sector is the AI boom itself. The staggering energy requirements of new AI data centers have created an urgent need for massive, reliable power generation. Consequently, VC investment in nuclear fission, dispatchable energy sources (like geothermal), and advanced grid optimization has soared 252728. Investors recognize that the software revolution is ultimately bottlenecked by the physical power grid, making clean energy infrastructure a mandatory companion to AI portfolios.

Defense Tech and the Geopolitical Reality

Geopolitical instability has officially cemented defense technology as a tier-one venture capital category. Global venture investment in defense tech hit $29 billion last year, nearly tripling the volumes seen five years prior 29.

This trend was sharply accelerated by early 2026 military campaigns in the Middle East, notably the joint U.S. and Israeli "Operation Epic Fury" against Iranian infrastructure 2930. The operation reportedly involved the first large-scale combat integration of artificial intelligence tools for targeting, alongside the widespread use of autonomous drones 31.

For venture capitalists, the lessons from these conflicts are clear: modern militaries are shifting procurement away from singular, multi-billion-dollar platforms toward cheaper, mass-produced, expendable systems 29. Capital is flowing heavily into startups building "attritable autonomy" (cheap drone swarms), counter-drone technologies, and domestic propulsion supply chains 29. Companies in this space are also proving to be highly lucrative M&A targets for legacy defense contractors looking to quickly acquire modern software and hardware capabilities 29.

Fintech's Pragmatic Rebound

After a brutal correction following the 2021 peak - when sky-high valuations met the reality of rising interest rates - financial technology (Fintech) is showing genuine signs of a revival 32. In Q1 2026, global fintech funding reached $12 billion 33.

However, the nature of fintech investment has matured. The focus has shifted away from consumer-facing challenger banks toward unglamorous but highly sticky B2B solutions. Investors are backing embedded finance infrastructure, SME lending, and regulatory compliance technology (RegTech) 26. The U.S. continues to dominate volume with $6.3 billion, but European fintechs are notably outperforming on capital efficiency metrics 2633.

The Exit Landscape: Unlocking $4.4 Trillion

A venture capital ecosystem functions as a cycle: LPs provide capital to GPs, who invest in startups, which eventually exit (via IPO or acquisition), returning cash back to the LPs. For several years, this cycle has been effectively jammed. Over $4.4 trillion in paper value is currently locked inside private U.S. unicorns alone 3435. Because institutional investors have suffered four consecutive years of negative net cash flows, they are hesitant to fund new ventures until they see returns from their existing portfolios 35.

On paper, Q1 2026 appeared to break this drought, posting an all-time record of $347.3 billion in exit value 57. However, this figure is highly distorted. Roughly 72% of that total ($250 billion) was generated by a single transaction: the internal consolidation merger of Elon Musk's xAI into SpaceX 10. Removing this outlier reveals an exit market that remains cautious. M&A deals are happening, but 86.8% of recent acquisitions carried undisclosed valuations, a strong indicator of markdowns and muted returns 19.

The 2026 Mega-IPO Pipeline

The true test of the market lies in the second half of 2026. A cohort of massive technology companies is preparing to test the public markets in what could be the most significant wave of IPOs in history. If successful, listings from just three companies - SpaceX, OpenAI, and Anthropic - could generate nearly $2.5 trillion in exit value, surpassing all VC-backed IPOs of the 21st century combined 567.

SpaceX: The aerospace giant is targeting a mid-2026 IPO with an estimated valuation between $1.5 trillion and $2 trillion 36374838. If it raises its targeted $50 billion, it would easily eclipse Saudi Aramco's 2019 record ($29 billion) as the largest IPO in history 3639. SpaceX's financial profile has evolved dramatically; its Starlink satellite internet segment now drives the majority of its $18.7 billion revenue, boasting over 10 million subscribers and strong operating margins 373840. Interestingly, the S-1 filing revealed a massive $1.25 billion monthly compute contract with Anthropic, linking the success of the space company directly to the AI boom 40. Wall Street is already seeing mutual funds stockpile cash to absorb this unprecedented listing 37.

OpenAI: The poster child of the generative AI revolution is reportedly targeting a confidential filing for a late 2026 or early 2027 IPO, aiming for a valuation around $1 trillion 3641424344. Despite generating an impressive $20 billion in revenue in 2025, OpenAI faces deep structural challenges. The sheer cost of AI compute means the company is projecting up to $14 billion in losses for 2026, and profitability is not expected until the 2030s 43. Investors will have to decide if they are willing to stomach dot-com era losses for the promise of owning the foundational layer of the future economy.

Enterprise Software and Fintech: Beyond AI and space, a tier of highly mature, cash-flow-positive companies is ready to list. Databricks (valued at $134 billion), Canva ($50 billion+), and Stripe ($120 billion) offer public market investors a more traditional, predictable SaaS revenue model compared to the capital-incinerating AI labs 36394145.

Secondaries Go Mainstream

Because the IPO window remains restrictive for the vast majority of startups, the secondary market has exploded. In a secondary transaction, existing shareholders (founders, employees, early investors) sell their equity to new private investors without the company going public. The global secondary market hit a record $226 billion in 2025, a 41% increase year-over-year 46. Once considered a niche tool, secondaries are now a core liquidity mechanism, allowing funds to return cash to LPs and providing financial relief to startup employees who have been waiting over a decade for a traditional exit 104647.

Macroeconomics: Interest Rates and the Labor Market

The venture capital ecosystem does not exist in a vacuum; it is highly sensitive to broader macroeconomic policy and labor trends.

The Federal Reserve's Holding Pattern

The end of the zero-interest-rate environment fundamentally altered VC math, and relief is not arriving quickly. In early 2026, the U.S. Federal Reserve maintained the federal funds rate at 3.50% - 3.75% 4849. Persistent inflation, exacerbated by volatile energy prices linked to Middle Eastern conflicts (such as Operation Epic Fury's disruption of the Strait of Hormuz), has kept the central bank cautious 304849. Futures markets project that the Fed is highly likely to hold rates steady through the summer, with some analysts even warning that further hikes cannot be entirely ruled out if oil shocks intensify 6150. For startups, this means the cost of capital remains high, and investors will continue to demand profitability over sheer growth 25.

Job Creation vs. AI Displacement

Despite the funding squeeze outside of AI, venture-backed companies remain a critical engine for economic growth. Data indicates that employment at VC-backed companies grows roughly eight times faster than at non-VC-backed firms, supporting over 9.2 million jobs in the U.S. alone 5152.

However, the nature of these jobs is shifting rapidly due to the very technology venture capital is funding. Enterprise VCs and labor analysts predict that 2026 represents a critical tipping point for AI in the workforce 53. While the AI sector is projected to create 800,000 highly specialized new roles, AI-driven automation is simultaneously expected to displace approximately 1.5 million jobs - primarily in administrative, data entry, and middle-management roles - creating a significant structural gap in the labor market 5153.

The 2026 Founder Playbook: How to Raise Capital Now

For entrepreneurs attempting to secure funding in a market that is deeply skeptical of anything without an "AI" label, the playbook has fundamentally changed. The era of raising massive rounds on a visionary pitch deck is over.

- Accept the New Math: Founders must build financial models that investors can trust. This means conservative, data-backed projections demonstrating clear unit economics, high gross margins, and a path to profitability. The "Rule of 40" (where a company's growth rate plus its free cash flow margin exceeds 40%) is heavily scrutinized 2554.

- Immaculate Corporate Hygiene: Due diligence is more rigorous than ever. A messy cap table, unresolved IP issues, or a poorly managed employee option pool (like failing to update a 409A valuation) will stall or kill a deal. Startups are expected to migrate off spreadsheets and use dedicated equity management software 1955.

- Bridge Rounds and Milestones: Rather than aiming for a massive Series A or B that risks a down round later, smart founders are raising smaller, milestone-driven bridge rounds 2556. The goal is to secure just enough runway to hit the specific ARR targets required to justify an up-round in the future 69.

- Targeted Outreach: Blasting pitch decks to hundreds of investors is highly inefficient. Funds are hyper-specialized by stage and sector. Founders must target VCs whose specific thesis aligns with their product, and secure warm introductions, which carry immense weight in a risk-averse market 69.

- Non-Dilutive Options: With equity capital so expensive, founders are increasingly turning to venture debt, revenue-based financing, and customer pre-sales to fund operations without giving up ownership 2557.

Bottom line

The venture capital market in 2026 is defined by extreme contradictions. While headline funding numbers are shattering records at $300 billion a quarter, that capital is intensely bottlenecked into a few dozen AI and defense technology giants. For the broader ecosystem, the market remains highly disciplined, demanding strict capital efficiency and clear paths to profitability. The immediate future of the asset class now relies heavily on the public markets; if the impending mega-IPOs from companies like SpaceX and OpenAI succeed, they will unlock trillions in trapped capital, potentially revitalizing the entire global startup economy. If they fail to launch, the liquidity drought for everyday startups will only deepen.