How VCs Evaluate the YC Summer 2026 Batch

On September 10, 2026, venture capitalists evaluating Y Combinator's Summer (S26) batch will prioritize startups demonstrating immediate operational revenue over theoretical prototypes. Driven by a fundamental shift in the accelerator's investment thesis, global investors are aggressively targeting founders who leverage AI-native systems to completely replace human labor in professional services, alongside those building deep technology in space, defense, and agentic infrastructure. The era of funding a polished presentation and a waitlist is definitively over.

The Evolution of Due Diligence: Revenue Over Demos

For over a decade, early-stage venture capital operated on a predictable and somewhat forgiving rhythm. A founding team could enter an accelerator with a compelling idea, build a minimum viable product (MVP), and use Demo Day to raise seed capital based on potential and vision. In the macroeconomic reality of 2026, that era has definitively closed, replaced by a hyper-competitive startup environment where MVPs hold no value unless they already behave like scalable businesses 1.

The fundamental catalyst for this shift is the democratization of software development. With the rise of "vibe coding" and advanced AI developer tools like Cursor, a significant percentage of Y Combinator founders now use artificial intelligence to generate up to 95% of their codebase 23. Because almost any founder can spin up a polished application in a matter of days, a functional prototype no longer serves as a competitive moat. Investors attending the S26 Demo Day are overwhelmed with startups that already work, shifting the baseline for early-stage evaluation from theoretical potential to operational execution 14.

Founders frequently fall into the psychological trap of believing their product is simply lacking marketing distribution 1. Venture capitalists evaluating the S26 batch universally reject this narrative. In the modern framework, marketing does not create demand; it reveals it. If a product is not converting users, retaining them, and generating revenue in a controlled environment, scaling traffic will only accelerate churn and expose weak onboarding 1. Investors expect distribution to be at least partially proven before capital enters the picture.

This new standard was set aggressively during the preceding Winter 2026 (W26) batch. During that cohort, an unprecedented 14 companies reached $1 million in Annual Recurring Revenue (ARR) before Demo Day even concluded 56. One standout company, Pocket, achieved an astonishing $27 million ARR at the seed stage, shipping 30,000 hardware units with 50% month-over-month growth 7. Another, Luel, a marketplace for real-world human data, reached a $2 million ARR run-rate in just six weeks 89. Consequently, "pre-revenue" is no longer an expected norm, and "pre-validation" is viewed as an immediate disqualifier 4.

Financial Scrutiny and the Unit Economics Reality

Beyond top-line revenue, the depth of financial scrutiny at the seed stage has intensified. VCs evaluating the S26 cohort demand clean, historically accurate financial books that can withstand immediate institutional due diligence 10. Messy management accounts or inconsistent revenue recognition are viewed as signals that the founding team lacks operational maturity 10.

Investors are heavily scrutinizing unit economics, specifically Customer Acquisition Cost (CAC) and Lifetime Value (LTV). A commercially viable LTV:CAC ratio of 3:1 or better is expected, alongside a clear understanding of the payback period 10. If a startup's payback period extends beyond 24 months at the pre-Series A stage, investors view it as a massive liability. Furthermore, not all revenue is treated equally. Venture capitalists place a heavy premium on predictable, recurring revenue (MRR or ARR) and closely monitor gross churn. High churn rates instantly destroy an otherwise compelling growth narrative 10.

The bar for raising subsequent rounds has also risen significantly, forcing seed investors to be highly selective. A median Series A company in 2026 is raising at around $2.5 million in trailing revenue, while top-quartile revenue growth rates have compressed across every stage 11. Because the median seed company must grow revenue roughly 11x to reach median Series A benchmarks, only about 3% of seed companies successfully graduate to Series A within 12 months 11. Evaluators at the S26 Demo Day are calculating these exact graduation odds before offering a term sheet.

| Financial Metric | The Traditional YC Era (Pre-2023) | The 2026 Reality (W26/S26 Batches) |

|---|---|---|

| Primary Evaluation Focus | Product vision and founder pedigree | Demonstrated traction and ARR 14 |

| Typical Demo Day Traction | Beta testing, waitlists, early pilots | Paying customers, frequently $1M+ ARR 5 |

| Series A Revenue Benchmark | ~$1 million trailing revenue | ~$2.5 million trailing revenue 11 |

| Expected Runway Focus | 18 months | 24 - 30 months minimum 11 |

| Seed to Series A Graduation Rate | High historical conversion | ~3% within 12 months 11 |

The NFL Draft Analogy: Capital Allocation Strategies

To understand the mechanics of how venture capitalists evaluate a massive, 200-company Y Combinator batch in 2026, industry analysts increasingly compare the process to the NFL Draft 1213.

In professional sports drafts, elite franchises do not simply pick the best player in isolation; they execute a complex capital allocation strategy. They construct portfolios, balance risk, and convert uncertainty into optionality on a compressed, highly public timeline 12. Venture capitalists approach YC Demo Days with an identical methodology. The "picks" require immense pre-event research into the founders' backgrounds, team dynamics, unit economics, and total addressable market 1314. The organizations that consistently outperform are those that understand relative value, knowing when to accumulate more shots on goal and when to concentrate capital 12.

Algorithmic Batch Scoring and Vibe Investing

Institutional investors are bringing an unprecedented level of quantitative rigor to the S26 batch. Firms like Rebel Fund, which exclusively back YC startups, have developed proprietary machine-learning algorithms (such as Rebel Theorem 4.0) to predict startup success based on historical data 15. By scoring the batch weeks before the actual presentations, these funds identified that 35% of the preceding W26 startups fell into the top 20% of all YC companies ever evaluated 1516. This algorithmic approach allows investors to bypass the hype of a stage pitch and target highly specific targets before the broader market recognizes their value 16.

However, the "NFL Draft" environment also necessitates rapid qualitative judgments. Due diligence timelines have compressed from weeks to mere days, or sometimes hours 6. In this high-velocity environment, investors must also rely on "vibe investing" - rapidly assessing a founder's resilience, clarity, and domain expertise during a 15-minute introductory meeting 17. Because early-stage products pivot frequently, evaluators are ultimately underwriting the founding team's capacity to navigate complex markets and adapt to failure 17.

The Bookface Dynamic: When Founders Hold the Leverage

Perhaps the most unique aspect of Y Combinator Demo Days is the inversion of traditional venture capital power dynamics. At a standard pitch meeting, the investor holds the leverage. On September 10, the most sought-after YC founders will hold all the cards 17.

A top-tier S26 startup might be raising $2 million at a $20 million valuation, yet have over $15 million in active investor interest 17. In these scenarios, capital becomes a highly commoditized utility. Venture capitalists must rapidly pitch the founders on their specific, non-financial value-add - be it procurement access, recruiting networks, or regulatory expertise 17.

Furthermore, investors must strictly deliver on these promises. Y Combinator maintains an internal, founder-only platform known as Bookface, where investors are ruthlessly ranked and reviewed based on how they treat entrepreneurs 17. A single bad interaction, a pulled term sheet, or a failure to provide promised support can permanently blackball a venture capitalist from future YC deals. This transparency forces investors to evaluate S26 startups not just as financial assets, but as high-stakes partnerships where their own firm's reputation is continuously on the line.

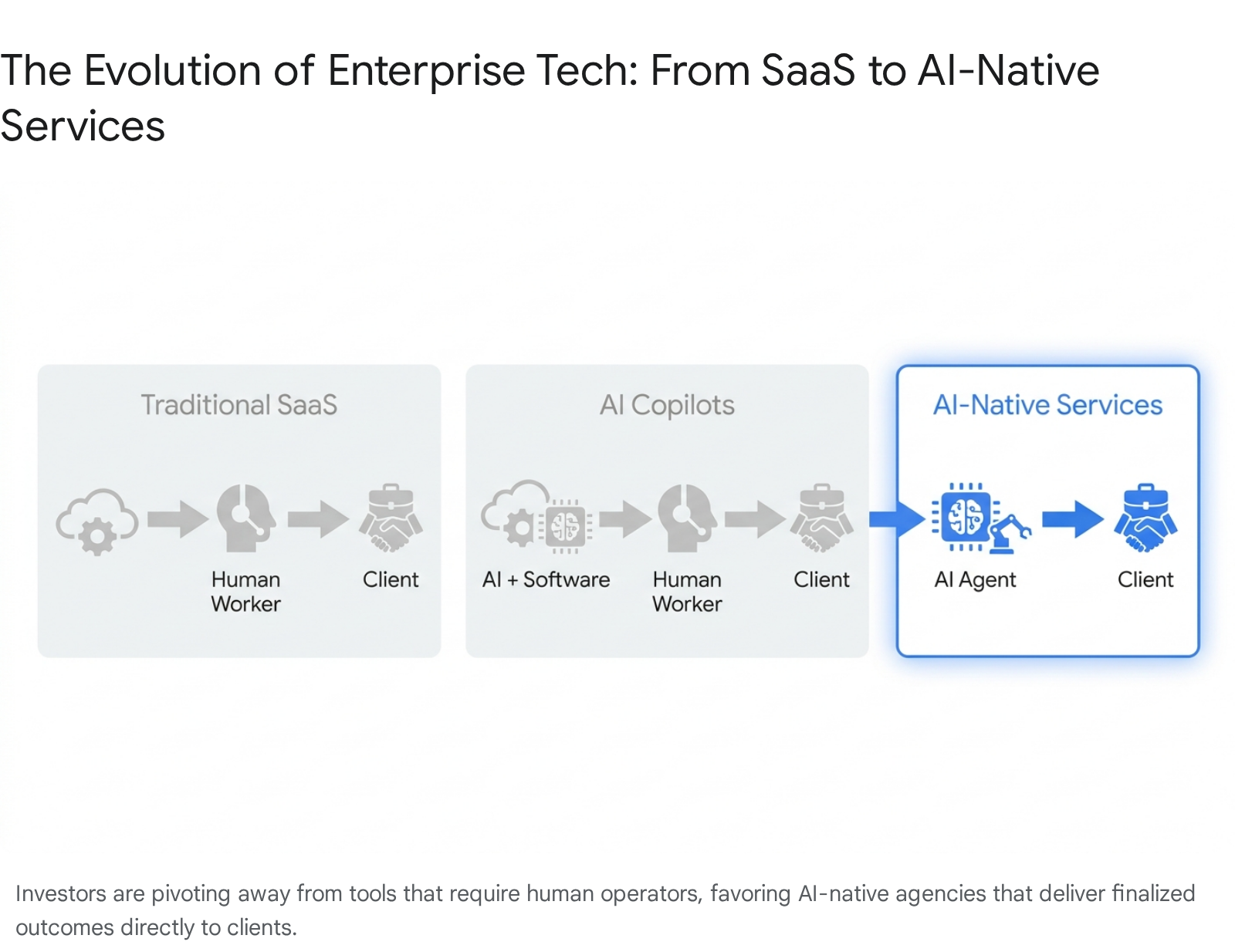

Decoding the S26 Mandate: From SaaS to AI-Native Services

Y Combinator does not keep its preferences secret. Prior to the S26 batch, the accelerator published a highly specific "Request for Startups" (RFS) authored by its group partners. This document serves as a direct, uncompromising roadmap for where Silicon Valley's most patient capital believes the next generation of trillion-dollar businesses will emerge 21819. For VCs evaluating the September Demo Day, the startups that successfully execute on these specific RFS categories represent the most compelling investment targets.

The most profound shift in the S26 thesis is the active dismantling of the Software-as-a-Service (SaaS) business model. For two decades, Silicon Valley rewarded pure SaaS models: building scalable workflow tools with minimal human involvement, selling them on recurring subscriptions, and relying on the client's employees to operate the software 20. S26 investors view this model as vulnerable and increasingly obsolete.

The new mandate is to build "AI-Native Services." Instead of selling a software tool to help an accountant, an insurance broker, a recruiter, or a healthcare administrator do their job, YC is demanding founders build AI systems that execute the work entirely 182122.

The economic rationale underpinning this shift is massive: the total global spend on professional services vastly outweighs the total spend on software 1821. Because the majority of these services are already outsourced to human agencies, they are structurally primed for replacement by autonomous systems 21.

Investors evaluating S26 startups are looking for businesses that take ownership of the final outcome. Rather than selling a workflow dashboard to an accounting firm, the startup is the accounting firm, running on AI labor instead of human headcount 2223. This allows the startup to deliver services faster, cheaper, and at software-like margins, completely bypassing traditional SaaS distribution bottlenecks 20.

The Demise of the AI Wrapper

Venture capitalists are explicitly punishing founders building superficial applications on top of existing foundational models - commonly derided as "AI wrappers." Data indicates that true wrappers are declining in accelerator cohorts, while deep technology and proprietary applied AI architectures are surging 24.

Investors expect S26 founders to possess deep domain knowledge to navigate the severe regulatory, compliance, and go-to-market challenges of replacing legacy service firms 19. For example, the idea of an AI-native hedge fund - a system that autonomously allocates capital and develops trading strategies without human portfolio managers - requires founders who understand both complex quantitative finance and financial compliance regulations 222. Startups that possess this intersection of operational credibility and AI infrastructure are commanding the highest valuations at Demo Day 22.

| Startup Category | Investment Thesis | Example S26 Targets |

|---|---|---|

| AI-Native Agencies | Replace human-staffed service firms with autonomous models offering lower costs and software margins. | Accounting, legal services, tax audit, insurance brokerage 2123. |

| SaaS Challengers | Attack deeply entrenched legacy software (ERPs, chip design) whose codebases are vulnerable due to collapsed coding costs. | Industrial control systems, legacy CRMs 21. |

| Product Discovery (Cursor for PMs) | AI that synthesizes customer feedback to autonomously propose UI and data model changes, deciding what to build. | Product management optimization tools 2. |

| AI-Native Finance | Autonomous capital allocation and strategy development operating within compliance frameworks. | AI hedge funds, stablecoin infrastructure 222. |

Infrastructure for the Non-Human User

A defining characteristic of the S26 batch is the recognition that the next trillion users on the internet will not be human beings; they will be autonomous AI agents 1925. VCs are heavily evaluating startups based on their capacity to build the foundational infrastructure these agents require to function reliably.

The "Company Brain" and Institutional Memory

One of the most highly anticipated investment categories is the "Company Brain." YC partners, including Monzo founder Tom Blomfield, argue that the primary bottleneck to enterprise AI automation is no longer the reasoning capability of the foundational models, but rather the lack of structured domain knowledge 181925.

Critical company information lives in unwritten rules, isolated employee expertise, old support tickets, and fragmented Slack threads. AI agents frequently fail when they encounter these unstructured knowledge gaps 19. Investors are seeking startups that map this fragmented reality into an executable "skills file" - a dynamic, living map of how a company actually makes decisions 1819. This infrastructure allows agents to operate consistently rather than guessing, representing an enterprise opportunity as massive as the invention of the CRM or ERP 1920.

Furthermore, because AI agents do not have eyes and cannot click through visual interfaces designed for human cognition, existing software must be entirely rebuilt 1923. S26 investors are funding startups developing machine-readable interfaces - such as optimized APIs, Model Context Protocols (MCPs), and autonomous Command Line Interfaces (CLIs) - that allow agents to discover, sign up for, and utilize third-party tools without any human intervention 212325.

The Agentic Security Threat

As AI agents gain the autonomy to browse the internet, execute workflows, and move financial assets, they introduce unprecedented cybersecurity vulnerabilities. When a human is phished, they might hand over a password; when an autonomous agent is phished, it can systematically compromise an entire enterprise backend at machine speed 26.

Evaluators at Demo Day are actively hunting for AI security startups. During the preceding W26 batch, companies like Crosslayer Labs - founded by a team including a Princeton professor - gained massive investor traction by monitoring DNS and BGP routing to detect website spoofing specifically targeting autonomous agents 26. Security infrastructure tailored for the age of agentic workflows is viewed not as an optional feature, but as a mandatory prerequisite for enterprise AI adoption.

The Resurgence of Physical-World Technology

While software defined the previous decade, the S26 batch marks a massive pivot back to the physical world. Geographic data and historical modeling demonstrate a sharp decline in pure consumer software companies, which comprised only about 5% of recent cohorts 16. Instead, the most intense investor FOMO (Fear Of Missing Out) is clustering around hard technology, robotics, aerospace, and defense 1627.

Space Infrastructure and Lunar Ambitions

Space technology is experiencing a venture capital renaissance, driven by the collapse in payload costs pioneered by reusable rockets from SpaceX 25. Infrastructure projects that were economically laughable a decade ago are now rapidly approaching commercial viability 25.

At Demo Day, investors are evaluating highly ambitious "moonshot" startups that blend software precision with advanced engineering. Recent examples include Beyond Reach Labs, which designs satellite solar arrays that expand from the size of a table to a football field in orbit, and GRU Space, which is literally developing a "moon factory" to turn lunar soil into building materials for permanent extraterrestrial infrastructure 89. While inherently high-risk, venture capitalists view these space-adjacent bets as the next generation of trillion-dollar monopolies, heavily validating the founders who can execute them 825.

Counter-Swarm Defense as Systems Engineering

Defense technology has also shed its taboo status among Silicon Valley investors. However, YC is not looking to fund traditional munitions manufacturers. The modern warfare landscape has been radically altered by the advent of cheap, autonomous drone swarms 1925.

Against a swarm of hundreds of coordinated drones approaching simultaneously, legacy defense systems fail predictably: they run out of multi-million-dollar interceptor missiles before the adversary runs out of $500 drones 1925. Investors evaluating the S26 batch view drone defense not as a weapons problem, but as a real-time, distributed software systems problem 1925. The startups expected to win defense contracts will resemble modern cybersecurity networking platforms like Cloudflare, prioritizing signal processing, AI orchestration, and software engineering over kinetic ballistics 19.

This trend extends seamlessly into agriculture and heavy industry. Startups leveraging AI vision, precision robotics, and biological alternatives to dramatically reduce pesticide usage or automate metal mills are viewed as highly defensible, generational opportunities 2225.

Global Venture Capital Dynamics

The competition for YC allocations on September 10 is not limited to Silicon Valley insiders. Global venture capital flows heavily influence how the S26 batch is evaluated, with different international regions deploying capital based on unique domestic macroeconomic pressures 282930.

European Focus on Deep Science

European venture capital experienced a notable fundraising slump in 2025, but the ecosystem is rebounding by leaning heavily into deep science and technical founders 2931. Backed by significant structural investments - including over €200 billion in government funding for AI and infrastructure - European VCs are aggressively scouting YC Demo Days for startups that bridge the gap between artificial intelligence and hard scientific research 2829.

Investors from the region are particularly interested in founders acting as technical CEOs, focusing on predictive therapeutics, robotics, and advanced materials engineering. The European thesis heavily prioritizes startups with deep intellectual property moats over pure software plays 29.

Asian Markets and Cross-Border Scale

In Asia, venture capital has stabilized after a period of post-boom volatility. Investors from this region, including major corporate funds and state-backed entities, are heavily concentrated on semiconductors, AI infrastructure, and robotics 2830.

Cross-border venture firms, such as the $2 billion Sky9 Capital, specifically scout YC Demo Days for technical founders looking to scale AI and deep tech applications globally 32. For founders building from an Asian origin market with ambitions to navigate both US and Asian regulatory and procurement landscapes, these international VCs offer localized expertise that domestic US investors cannot match 32.

Latin American Maturation and Stablecoins

Latin American venture capital has entered a highly disciplined, post-boom phase. The regional "growth-at-all-costs" mindset has been replaced by a strict demand for capital efficiency, operational resilience, and clear paths to liquidity 2933.

Investors looking at YC from LatAm are highly selective, focusing primarily on FinTech, AgroTech, and HealthTech solutions that can compound value in complex, volatile operating environments 33. A massive focus for these investors is stablecoin infrastructure. In markets plagued by currency crises - such as Argentina, which experienced 118% inflation in 2024 - stablecoins have transitioned from speculative crypto assets to critical financial lifelines 29. Startups building compliant, cross-border payment rails utilizing stablecoins are highly prized by emerging market evaluators 2229.

| Region | Primary Investment Focus at YC S26 | Macro Market Condition in 2026 |

|---|---|---|

| North America | Agent infrastructure, defense, SaaS replacement | Bifurcated: Mega-rounds for AI leaders, tight seed market 1119 |

| Europe | Deep tech, scientific discovery, robotics | Recovering from a slump, driven by technical CEOs and state funding 2931 |

| Asia | Semiconductors, cross-border AI, hard infrastructure | Stabilized, driven heavily by public-private corporate capital 30 |

| Latin America | FinTech (stablecoins), AgroTech, HealthTech | Disciplined, focusing on capital-efficient scale-ups and resilience 33 |

Evaluating the 2026 Founder Profile

Ultimately, early-stage venture capitalists are underwriting people. However, the profile of a fundable founder and software engineer has shifted drastically in 2026.

The rise of AI coding assistants has completely commoditized baseline programming skills. In recent YC batches, a quarter of the startups used tools like Cursor to generate over 95% of their initial codebase 3. When anyone can spin up a product, raw technical execution speed is no longer sufficient. Marketing, positioning, and trust do not come bundled with AI-generated code 3. Consequently, venture capitalists are evaluating founders based on their capacity for systems thinking and their deep, localized domain expertise 1922.

The "T-Shaped" Agentic Practitioner

Investors are actively seeking teams comprised of "T-shaped" engineers: individuals who possess broad competency across product management, business context, and user communication, anchored by deep, specialized expertise in a specific domain that AI cannot yet reliably replicate 34.

Furthermore, the most in-demand technical skill is no longer writing syntax; it is orchestration. VCs are prioritizing "Agentic Practitioners" who understand how to deploy, monitor, and troubleshoot complex systems of interacting AI models 263536. These builders are evaluated on their ability to manage data pipelines, handle versioning and rollbacks, optimize inference for scale, and ensure compliance in environments where machines are making autonomous decisions 37. Startups led by founders who treat AI as an operating system component rather than a novelty feature are the ones securing the massive valuations at Demo Day 2235.

Bottom line

For investors evaluating Y Combinator's Summer 2026 batch on September 10, the traditional startup playbook has been fundamentally rewritten. Venture capitalists are demanding immediate revenue validation and clean unit economics, actively ignoring polished prototypes in favor of operational businesses. The most lucrative funding is flowing toward founders who leverage agentic infrastructure to replace human service labor entirely, alongside those tackling complex, physical-world problems in space, defense, and heavy industry. While it remains uncertain how regulatory frameworks will adapt to autonomous AI agencies, the startups that demonstrate early traction in these hard-tech sectors are commanding unprecedented leverage in the venture capital market.