Artificial Intelligence Startup Funding and Valuations in 2026

Macro Venture Capital Landscape

The global venture capital environment in the first quarter of 2026 experienced an unprecedented influx of capital, driven almost entirely by the artificial intelligence sector. Aggregate data indicates that global venture funding during this single quarter reached historic highs, with estimates ranging from $255.5 billion to approximately $300 billion across roughly 6,000 funded companies 123. Within this vast capital deployment, artificial intelligence companies captured between 80% and 81% of all venture dollars, effectively transforming the asset class from a diversified technology portfolio into a highly concentrated, AI-dominated landscape 234. To provide historical context, the capital deployed into artificial intelligence in the first quarter of 2026 alone surpassed the full-year 2025 total of $254.4 billion 1.

Despite these record-breaking headline figures, the underlying distribution of capital reveals a highly distorted, barbell-shaped market structure. Deal volumes have not expanded proportionally with capital deployment. Instead, total transaction counts fell 15% quarter-over-quarter to roughly 7,000 globally, marking the lowest level of deal activity since late 2016 and representing a 61% decline from the market peak in 2022 45. Early-stage deal counts similarly fell by 30% year-over-year 2. This divergence indicates that the 2026 venture capital record is entirely a function of concentrated mega-rounds rather than the organic, broad-based growth of the wider startup ecosystem 34.

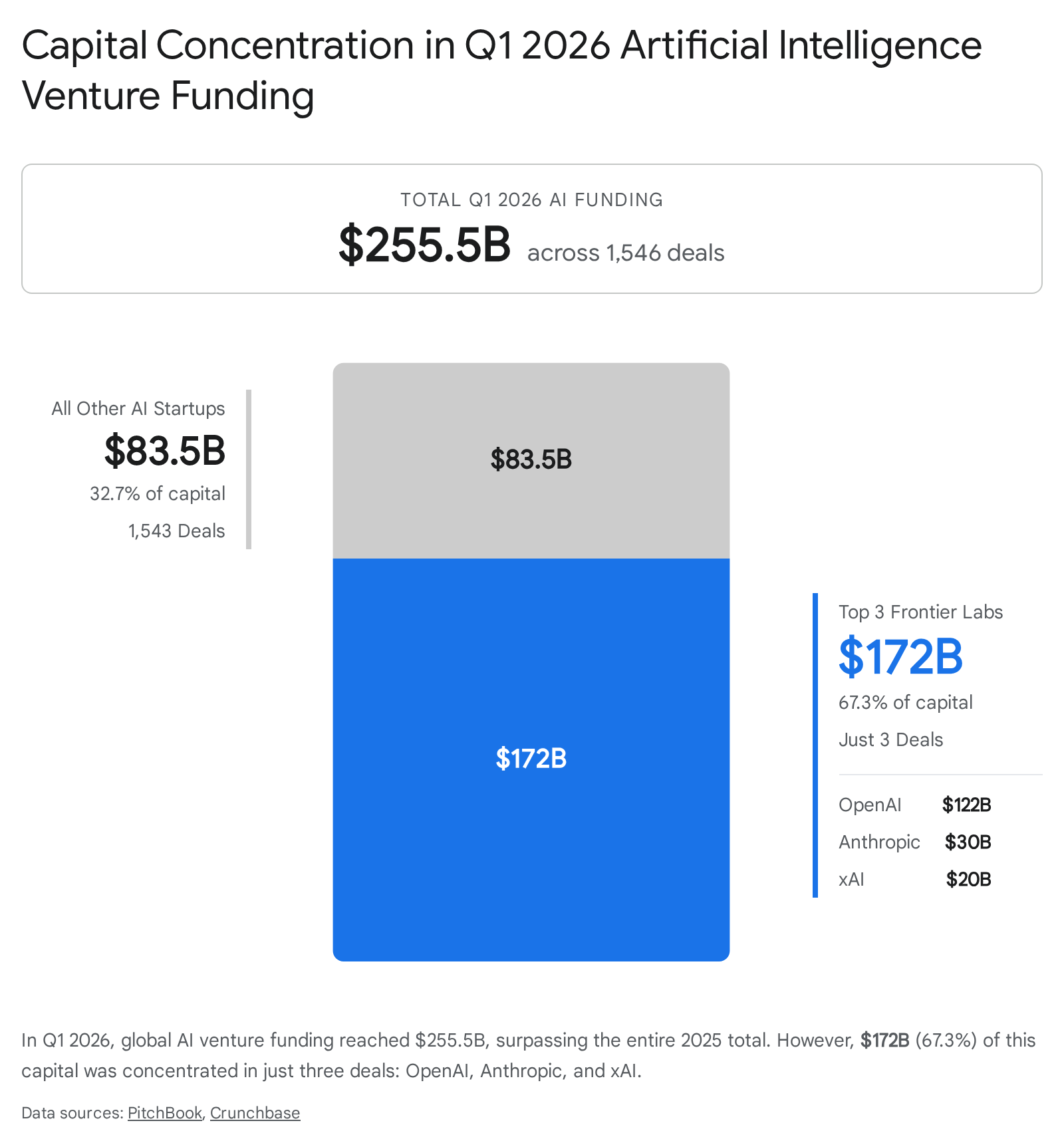

The data underscores an extraordinary concentration of capital at the absolute apex of the market. In the first quarter of 2026, three foundational model companies - OpenAI, Anthropic, and xAI - accounted for 67.3% of the capital, absorbing approximately $172 billion of the $255.5 billion deployed globally in the AI sector 5.

OpenAI closed a historic $122 billion round at an $840 billion valuation, Anthropic secured a $30 billion Series F at a valuation ranging between $350 billion and $380 billion, and xAI finalized a $20 billion round 157. When combined with Waymo's $16 billion Series D in the autonomous systems segment, these four transactions alone constituted roughly 65% of all global venture investment across all sectors for the quarter 2.

This concentration fundamentally distorts traditional venture capital benchmarks. The $83.5 billion that remained for the other 1,543 AI deals in the first quarter of 2026 still represents a robust funding environment by historical standards, but it reveals that investors are placing massive, structural bets on infrastructure and foundational platforms 5. Nontraditional investors, including sovereign wealth funds such as Singapore's GIC and the UAE's MGX, alongside corporate venture arms from Amazon, Nvidia, and SoftBank, have crowded into these mega-rounds 58. These investors are seeking pre-IPO equity in platforms they view as the structural digital substrate of the next macroeconomic cycle 5. As these foundational companies generate unprecedented annualized revenues - OpenAI reportedly topped $25 billion, and Anthropic surpassed a $30 billion run-rate - their capital demands have outgrown what traditional venture capital can provide, requiring Wall Street and sovereign entities to fill the liquidity gap 5.

The resulting market exhibits a pronounced two-tier effect. At one end, capital is practically limitless for AI-native companies building defensible infrastructure, securing robust enterprise compute contracts, or developing foundational model architectures 7. At the other end, capital remains available but is distributed with stringent discipline to startups competing for a smaller pool of sub-$500 million funds 7. These investors are imposing rigorous technical and financial due diligence, resulting in a thinning of the middle market where companies without verifiable traction or defensible technical moats struggle to close rounds entirely 79.

| Segment | Capital Raised (Q1 2026) | Deal Count | Percentage of Total AI Capital |

|---|---|---|---|

| Top 3 Frontier Labs (OpenAI, Anthropic, xAI) | $172.0 Billion | 3 | 67.3% |

| All Other AI Startups | $83.5 Billion | 1,543 | 32.7% |

| Total Global AI Venture Funding | $255.5 Billion | 1,546 | 100.0% |

Valuation Dynamics and Revenue Multiples

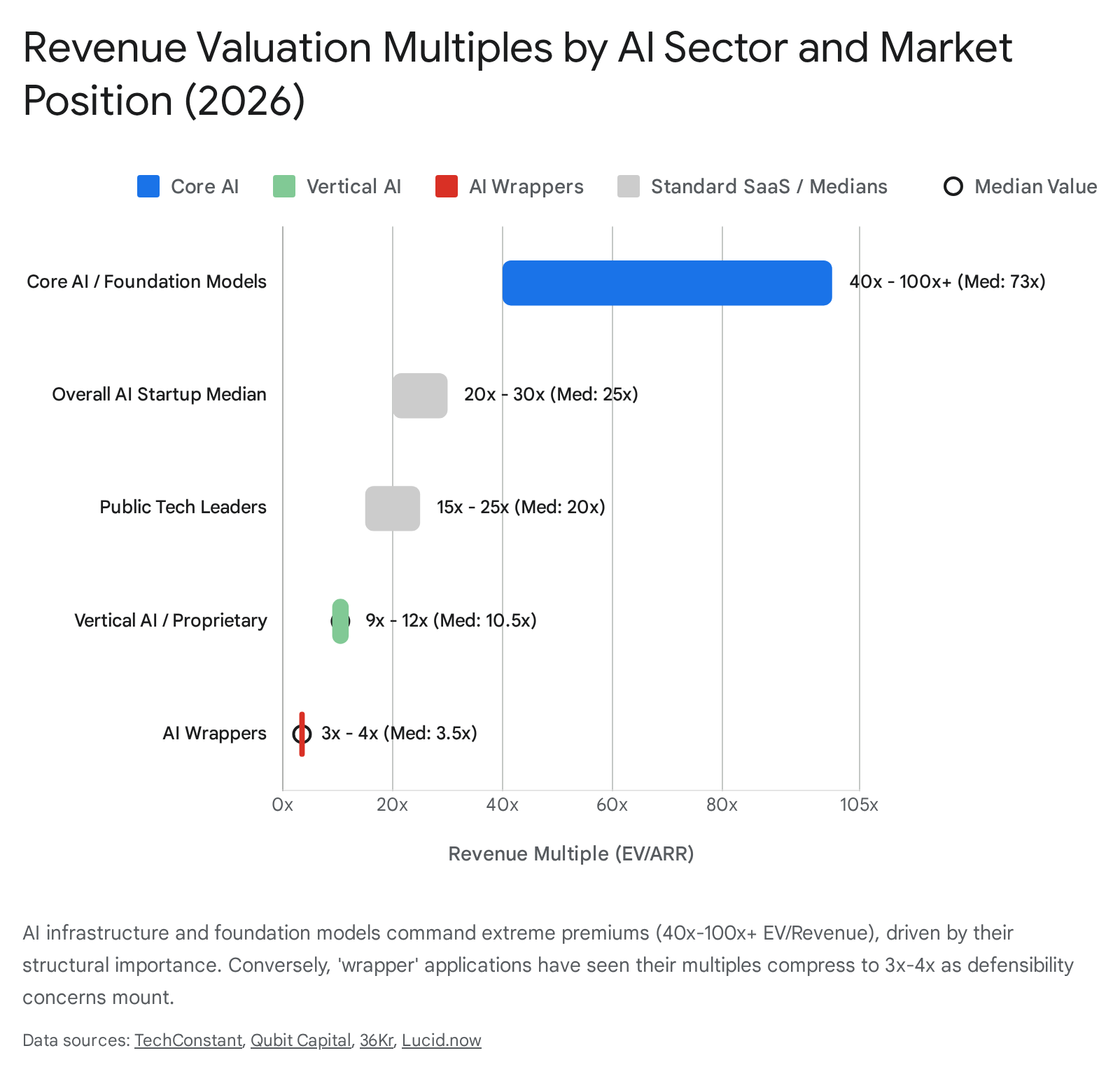

Valuing artificial intelligence startups in 2026 requires a structural departure from the conventional revenue multiple approaches utilized during the previous decade of Software-as-a-Service (SaaS) expansion. Traditional discounted cash flow models and comparable analysis frequently fail to capture the exponential growth dynamics, data asset accumulation, and intellectual property value inherent in AI platforms, leading investors to accept structurally higher valuation multiples 67.

In 2026, AI startups command median revenue multiples of 25x to 30x, which is approximately four to five times higher than the multiples seen in public SaaS companies, which typically trade closer to 6x 78. However, relying on a broad "AI multiple" obscures the reality that the valuation landscape is highly segmented based on a company's specific technical position within the AI value chain.

Companies developing large language models, foundational architectures, and core infrastructure frequently trade at 40x to 50x revenue multiples, with select outliers exceeding 100x 6. OpenAI achieved its recent valuation based on an annualized revenue of roughly $11.6 billion, implying a revenue multiple of approximately 73x, while Anthropic achieved its valuation on an even higher relative multiple 4. Core AI infrastructure companies averaged an impressive 79.7x enterprise value-to-revenue multiple in the first quarter of 2026 7. Defenders of these extreme valuations argue that cutting-edge AI companies are building the foundational infrastructure that will support the entire future economy, similar to how early investments in cloud platforms like AWS and Azure were eventually justified by massive ecosystem returns 4.

In stark contrast to infrastructure premiums, the valuation logic applied to the application layer is increasingly ruthless. A central theme of the 2026 valuation landscape is the systematic repricing and discounting of "AI wrappers." Wrappers are categorized as thin interface layers built atop third-party foundation model APIs without proprietary datasets, custom model training, or meaningful retrieval-augmented generation architectures 8. While these applications commanded high premiums during the initial generative AI boom, their multiples have since collapsed, with wrappers currently struggling to maintain 3x to 4x ARR multiples 8.

The logic driving this collapse is rooted in technical defensibility. Upstream foundation model providers continually expand their capability surfaces, releasing native features that rapidly render integration layers redundant 8. The integration of multimodal awareness directly into mobile operating systems natively absorbs the surface area previously occupied by contextual AI assistants 13. Venture capitalists now apply a straightforward operational test during due diligence: if a startup cannot seamlessly switch its foundation model provider within thirty days without catastrophic service disruption, its defensibility thesis is fundamentally compromised 8.

Consequently, the application market is splitting. While wrappers face severe valuation compression, vertical AI companies - those utilizing proprietary pipelines, custom fine-tuned models on highly specific industry data, and operating deeply within legacy enterprise workflows - maintain resilient 9x to 12x ARR multiples 8. For comparative context, the most highly valued publicly listed technology companies generally trade at 15x to 25x revenue, underscoring the specific premium private markets are assigning to defensible AI ecosystems 4.

Funding Stages and Unit Economic Requirements

The funding environment for AI startups in 2026 represents a sharp return to fundamental business disciplines. Investors have largely abandoned the speculative, growth-at-all-costs methodologies of the early 2020s, favoring highly disciplined evaluations of capital efficiency, unit economics, and demonstrable paths to profitability 79.

Pre-Seed and Seed Market Characteristics

At the earliest stages of capital formation, the market demonstrates a profound bifurcation. AI startups at the seed stage enjoy a 42% valuation premium over their non-AI peers, reflecting investor conviction in accelerated growth trajectories 101617. The median pre-money valuation for AI companies at the seed stage in 2026 sits at approximately $17.9 million, though some datasets track the top quartile reaching up to $24 million 7101611.

Round sizes at the seed stage have grown accordingly. While the global median seed round size across all industries is approximately $3.1 million, AI-specific seed rounds carry a median of $4.6 million 9. Specialized sectors such as healthcare AI and generative media frequently execute seed rounds between $4 million and $5 million 9. Startups operating in the consumer application space generally see smaller seed rounds averaging $1.5 million to $2.5 million 9. Founder dilution at this stage typically ranges from 15% to 20% 9.

However, mathematical averages at the seed stage are highly skewed by mega-seed anomalies that blur traditional stage definitions. Companies such as Safe Superintelligence raised a $2 billion seed round at a $32 billion valuation prior to achieving product revenue, and Thinking Machines Lab secured a $2 billion seed round at a $12 billion valuation 916. Excluding these multi-billion-dollar outliers, investors in standard $2 million to $5 million seed rounds require strict validation metrics. They demand pilot customers, design partners, and early users that prove market demand, alongside a credible path to achieving under twelve months of customer acquisition cost recovery 1619.

Series A Benchmarks

By Series A, institutional venture capital shifts focus from underwriting technical vision to demanding repeatable revenue mechanics. The median Series A pre-money valuation for AI startups rests at approximately $51.9 million, maintaining an 84% premium over non-AI peers 1112. Series A funding round sizes typically range between $8 million and $15 million, which is roughly 20% larger than the median round sizes achieved by non-AI companies at the same stage 1611.

The operational hurdles for securing Series A capital in 2026 are exceptionally high. Institutional funds deploying $100 million vehicles demand $3 million to $5 million in Annual Recurring Revenue, a significant increase from the $2 million threshold common in 2021 21. Absolute revenue is secondary to growth efficiency; investors mandate a minimum of 3x year-over-year growth, gross margins between 65% and 80%, and net revenue retention exceeding 120% 1921. Startups must also demonstrate sub-twelve-month CAC payback periods and possess documented sales playbooks that prove revenue generation is systemic rather than reliant on founder hustle 1921.

Series B and Late-Stage Expansion

The valuation gap between AI and legacy software expands substantially at Series B, a phase characterized by the global scaling of validated go-to-market motions and international expansion readiness. In 2026, the median Series B valuation for AI companies surged to $143 million, though some tracking platforms like Carta reported medians closer to $118.9 million for primary rounds 7161113.

Round sizes reflect the intensive capital requirements necessary to scale AI operations. AI startup Series B rounds average $25.6 million to $29.4 million, roughly 28% larger than those of the broader startup population 1113. At this stage, startups are expected to demonstrate $10 million to $20 million in ARR, predictable growth rates exceeding 100% year-over-year, and net revenue retention reliably above 130% 1619. Founder dilution at Series B is often lower than at Series A, typically settling between 10% and 20% 13.

| Stage | Median Round Size (AI) | Median Pre-Money Valuation (AI) | ARR Requirement | Expected ARR Multiple |

|---|---|---|---|---|

| Seed | $4.6 Million | $17.9 Million | $500K - $1.5M | 10x - 25x |

| Series A | $8.0M - $15.0M | $51.9 Million | $3.0M - $5.0M | 12x - 18x |

| Series B | $25.6M - $29.4M | $143.0 Million | $10.0M - $20.0M | 8x - 12x |

Sector-Specific Investment Trends

Beyond infrastructure and foundation models, the venture landscape is heavily contoured by industry-specific applications and shifts in both consumer and enterprise adoption.

Vertical Artificial Intelligence

While horizontal platforms absorb the largest absolute dollar amounts, industry-specific "Vertical AI" companies dominate the highest volume of deal activity. Throughout 2025 and accelerating into 2026, capital has flowed decisively toward specialized, sector-specific use cases. Across 4,395 venture capital financings totaling $186 billion in 2025, vertical startups captured 53% of the total deal volume and 30% of the capital deployed 14. If the twelve largest mega-rounds exceeding $1 billion are excluded from the dataset, vertical AI applications accounted for 51% of all deployed capital 14.

The vertical AI market is anchored by traditional pillars such as Healthcare and Financial Services, which combined for nearly 1,100 deals in 2025 14. However, emergent verticals have demonstrated explosive growth, notably Manufacturing and Industrials, Legal Tech, and Architecture, Engineering, and Construction 14. Legal tech saw massive capital infusions, highlighted by Clio's $850 million round and Filevine's $400 million raise, as legacy software providers rapidly integrated AI capabilities to defend market share 14. The manufacturing sector experienced a 41% increase in deal count over the course of 2025, driven by AI systems optimizing supply chains and autonomous factory precision 14.

The economic fundamentals of vertical AI are proving highly resilient. ChartMogul data analyzing 3,500 software companies indicates that AI-native vertical products priced above $250 per month achieve 70% gross revenue retention and 85% net revenue retention, performing equivalently to established B2B SaaS standards 10. Products priced below $50 per month, however, experience a low 23% gross revenue retention, highlighting the churn risks associated with low-cost consumer AI experimentation 10. In public markets, vertical software generally outperforms horizontal SaaS equivalents, as industry-specific AI creates deeper customer integrations and significantly higher switching costs 24.

| Deal Size Tier | Number of Vertical AI Deals (2025) | Percentage of Total Deal Volume |

|---|---|---|

| $1M - $5M | 1,733 Deals | 39.0% |

| $5M - $15M | 1,357 Deals | 31.0% |

| $15M - $30M | 591 Deals | 13.0% |

| $30M+ | 506 Deals | 12.0% |

| $100M+ (Mega-Rounds) | 208 Deals | 5.0% |

Consumer Artificial Intelligence and Autonomous Systems

Venture investment into business-to-consumer AI startups surged to $89 billion in 2025 across 668 deals, representing a 72.5% year-over-year increase in deal value 15. However, this headline growth was overwhelmingly driven by mega-deals in leading consumer-facing platforms. Excluding these outliers, consumer AI fundraising totaled a much more measured $17.5 billion 15. Investors in the consumer sector increasingly favored later-stage and venture-growth rounds, which captured nearly 95% of deployed capital, while pre-seed and seed activity in consumer AI contracted amid rising valuation thresholds and intense scrutiny regarding monetization and user churn 15.

In parallel, capital deployment into hardware and autonomous systems has accelerated as investors search for physical layer moats that are resistant to software commoditization. Autonomous machines posted a record quarter in early 2026 at $29 billion across 118 deals, fueled largely by Waymo's $16 billion Series D 1. Defense technology and dual-use AI applications have similarly seen historic funding levels, with companies like Anduril raising $5 billion across two rounds in 2025, reflecting growing investor and government interest in autonomous defense systems and AI-driven decision architectures 326.

Geographic Distribution of Venture Capital

The global distribution of AI venture capital highlights a stark polarization between North America and the rest of the world, driven by deep capital markets, sovereign strategic priorities, and infrastructural constraints.

United States Market Dominance

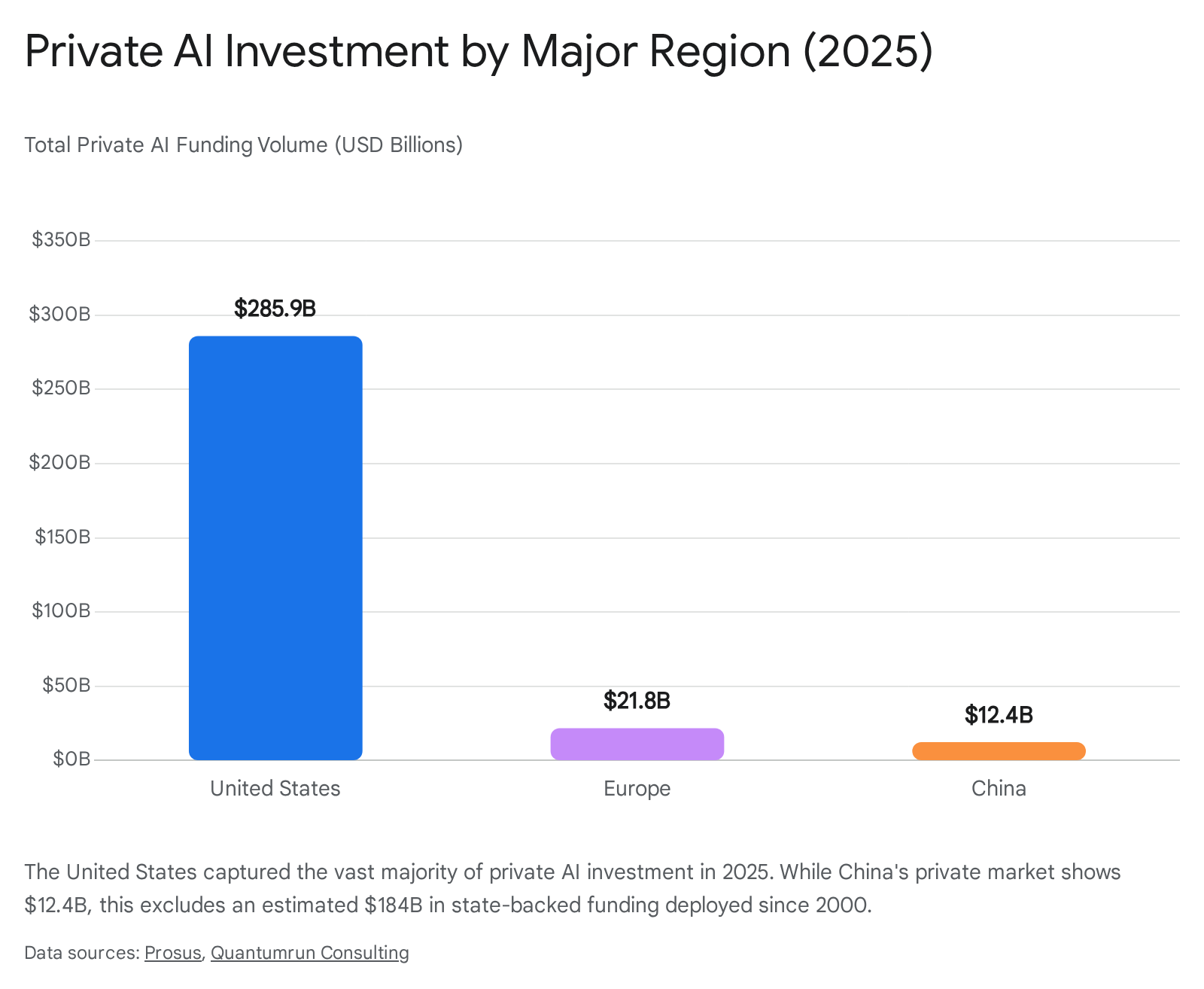

The United States remains the undisputed global engine of artificial intelligence funding. In 2025, U.S. private AI investment reached $285.9 billion, a 162% year-over-year increase from the $109.1 billion recorded in 2024 27. This dominance accelerated into the first quarter of 2026, where U.S.-based companies raised $250 billion, capturing 83% of all global venture capital across all sectors 2. The concentration within the U.S. is heavily localized; the San Francisco Bay Area alone raised $122 billion in AI funding, representing more than three-quarters of the domestic total 16. The vast majority of the world's hyperscalers, frontier-model labs, and deep capital syndicates operate within this ecosystem, creating a gravity well for international AI talent and capital 16.

European Scale-Up Vulnerabilities

Europe represents a geographic paradox characterized by robust early-stage creation paired with a severe late-stage capital deficit. European AI venture funding reached an all-time high of $21.8 billion in 2025, an increase of 58% over the prior year, with AI now accounting for over 30% of all European VC funding 16. London remains the undisputed AI capital of the continent, hosting approximately 1,700 VC-backed startups worth $125 billion, and raising $7.1 billion in 2025 alone 16. Other emerging hubs include Paris, Munich, and Zurich, which excel in deep tech and AI model development 16.

Despite possessing world-class talent and matching the U.S. in startup formation rates, Europe suffers from a structural scale-up vulnerability. European investors deploy 3x less capital at the breakout stage and 9x less at late stages compared to their U.S. counterparts 16. Consequently, over half of the capital used to scale Europe's most successful AI companies originates from foreign investors, effectively meaning that Europe incubates future category leaders for American investors to ultimately own 16. However, European startups maintain competitive strength in specialized domains such as robotics, AI-driven manufacturing, autonomous driving, and AI drug discovery 16. Furthermore, sovereign support is increasing, highlighted by France's commitment of €109 billion to AI-related programs across multiple sectors 29.

Chinese State-Led Consolidation

China's AI venture market has exhibited resilience but operates under vastly different mechanics than Western markets. In 2025, private AI investment in China stood at approximately $12.4 billion, growing 33% year-over-year 27. While this represents solid growth, the absolute funding gap between the U.S. and China widened to a multiple of 23x in private markets 27.

However, evaluating China solely through the lens of private venture capital is structurally flawed due to intense state intervention. Chinese government funds have reportedly deployed over $184 billion into AI firms since 2000, masking the relatively smaller private VC numbers 30.

The Chinese venture capital focus has consolidated decisively around enabling infrastructure, compute hardware, and semiconductors, systematically deprioritizing consumer-facing software applications 31. Hardware investment in China surged from $0.9 billion in 2024 to $2.7 billion in 2025, with median deal sizes in semiconductors escalating to $35 million 31. Non-domestic investor participation in Chinese AI deals has contracted markedly, falling from historical peaks to just 7.1% of deal value in 2025 31. Despite lower private funding, Chinese technology firms continue to match frontier model capabilities rapidly; open-source models exhibiting elite capabilities have been replicated by Chinese labs in a fraction of the time and budget utilized by Western counterparts 32.

Emerging Hubs in Asia-Pacific and the Middle East

Emerging global hubs have experienced outsized growth as capital searches for efficient deployment outside saturated markets. The Asia-Pacific ecosystem, excluding China, is posting the fastest annual growth rates globally 33. Singapore has solidified its status as the regional digital hub, capturing 92% of Southeast Asia's total startup funding in early 2026, punctuated by DayOne Data Centers' $2 billion Series C round 33. Recognizing the demand for advanced AI capabilities, Western hyperscalers have heavily backed Asian infrastructure; Asia now hosts 349 cloud infrastructure services, more than double the 145 operating in the United States 17.

In the Middle East, particularly Saudi Arabia and the United Arab Emirates, sovereign wealth initiatives are pivoting rapidly into AI infrastructure and compute capacity. Saudi Arabia launched Project Transcendence, a $100 billion initiative focused on large-scale AI development 29. The Middle East has also overtaken Europe as the second-most valuable region for pre-seed deals, achieving average valuations of $3.7 million, signaling deep capital availability at the formation stages 9.

Exit Markets, Liquidity, and Structural Shifts

While private valuations and funding rounds break historic records, the liquidity and exit mechanisms that sustain the venture capital model remain under severe pressure.

Mergers, Acquisitions, and Initial Public Offerings

Exit activity weakened significantly into early 2026. Mergers and acquisitions fell by 14% overall, and Initial Public Offerings (IPOs) were cut in half 5. Of the acquisitions that did occur, 86.8% carried undisclosed valuations, a metric that typically signals private markdowns and muted returns for investors 12. For companies that successfully navigated to an IPO, the median step-up from their last private valuation was a marginal 1.1x, highlighting the risks associated with relying on stale private market pricing from the 2021-2022 era 12.

This dynamic has created a backlog of heavily funded, highly valued private unicorns. The total post-money valuation of active U.S. unicorns rests at $3.9 trillion, yet nearly half of these companies have not been revalued in the past three years, creating a looming "paper unicorn reckoning" 835. Venture funds are currently consuming more capital than they are returning to Limited Partners, experiencing negative net cash flows of $46.2 billion through the first three quarters of 2025 12. The venture ecosystem is therefore highly reliant on the anticipated liquidity events of apex companies - specifically SpaceX, OpenAI, and Anthropic - which could collectively generate more exit value than the entire IPO market has produced in years 12. The singular bright spot in M&A was SpaceX's $250 billion acquisition of xAI prior to its anticipated public offering, which stands as the largest AI-related transaction ever recorded, exceeding the combined value of all AI M&A over the prior three years 1.

Agentic Harnesses and the Future of Compute Scaling

Beyond financial metrics, the fundamental architecture of artificial intelligence deployment is shifting in 2026, carrying profound implications for future startup moats and valuations. Historically, achieving frontier capability was tightly linked to scaling training compute. However, the industry is increasingly focused on "agent harnesses," which systematically extract superior performance from existing models by structuring work over time 36. These systems break tasks into iterative steps, verify results, and utilize dynamic reasoning chains at runtime rather than relying solely on the zero-shot intelligence of a base model 36.

This technological shift unbundles performance from capital-intensive model training. Because agent harnesses rely on optimized inference pipelines, small teams with limited capital can compete on benchmark accuracy with foundation model labs. For instance, in late 2025, a startup named Poetiq topped the ARC-AGI-2 benchmark with under ten employees, utilizing test-time reasoning rather than custom training 36. If capability gains continue to migrate toward inference-time orchestration, value capture will shift away from pure compute arms races and toward software and systems engineering, fundamentally altering how investors assess technical defensibility in the coming years 36. The era of basic prompt engineering has definitively ended, giving way to an era of flow engineering where the primary moat is embedding intelligence securely into complex operational systems 13.