SpaceX IPO Valuation

Market Context and Public Offering Mechanics

On June 12, 2026, Space Exploration Technologies Corp. (SpaceX) formally transitioned to the public markets, listing on the Nasdaq under the ticker symbol SPCX and executing the largest initial public offering in global financial history 121. Pricing 555.6 million Class A shares at a fixed $135 per share, the company raised approximately $75 billion in primary capital 45. This capital raise eclipsed the previous $29 billion record set by Saudi Aramco in 2019, instantly establishing SpaceX with an implied market capitalization of approximately $1.75 trillion to $1.77 trillion 146. At this valuation, SpaceX ranks among the ten most valuable public companies in the world, positioned slightly above the market capitalization of Tesla at the time of the debut 17.

The transition from a privately held aerospace manufacturer to a publicly traded, multi-trillion-dollar conglomerate reflects a profound structural evolution. The Form S-1 registration statement, filed publicly on May 20, 2026, reveals that SpaceX has diversified far beyond its origins as a launch provider 189. Following an all-stock acquisition of the artificial intelligence firm xAI in February 2026, the company now operates as a vertically integrated holding entity composed of three distinct reporting segments: Space (launch services and defense), Connectivity (Starlink broadband and mobile), and Artificial Intelligence (xAI, the X platform, and advanced orbital computing infrastructure) 51011.

The public offering generated extraordinary demand, with the order book closing multiple times oversubscribed 7. Retail investors were allocated an unusual 30% of the offering, while institutional demand exceeded $250 billion, anchored by major allocations including a reported $5 billion commitment from BlackRock 213. Despite this voracious market appetite, the offering's valuation implies a trailing price-to-sales multiple of roughly 94x based on 2025 consolidated revenues of $18.67 billion 156. This aggressive multiple has catalyzed an intense debate among institutional analysts regarding execution risk, ongoing cash burn, and the viability of the company's multi-decade timeline for orbital infrastructure deployment 223.

Private Market Valuation Trajectory

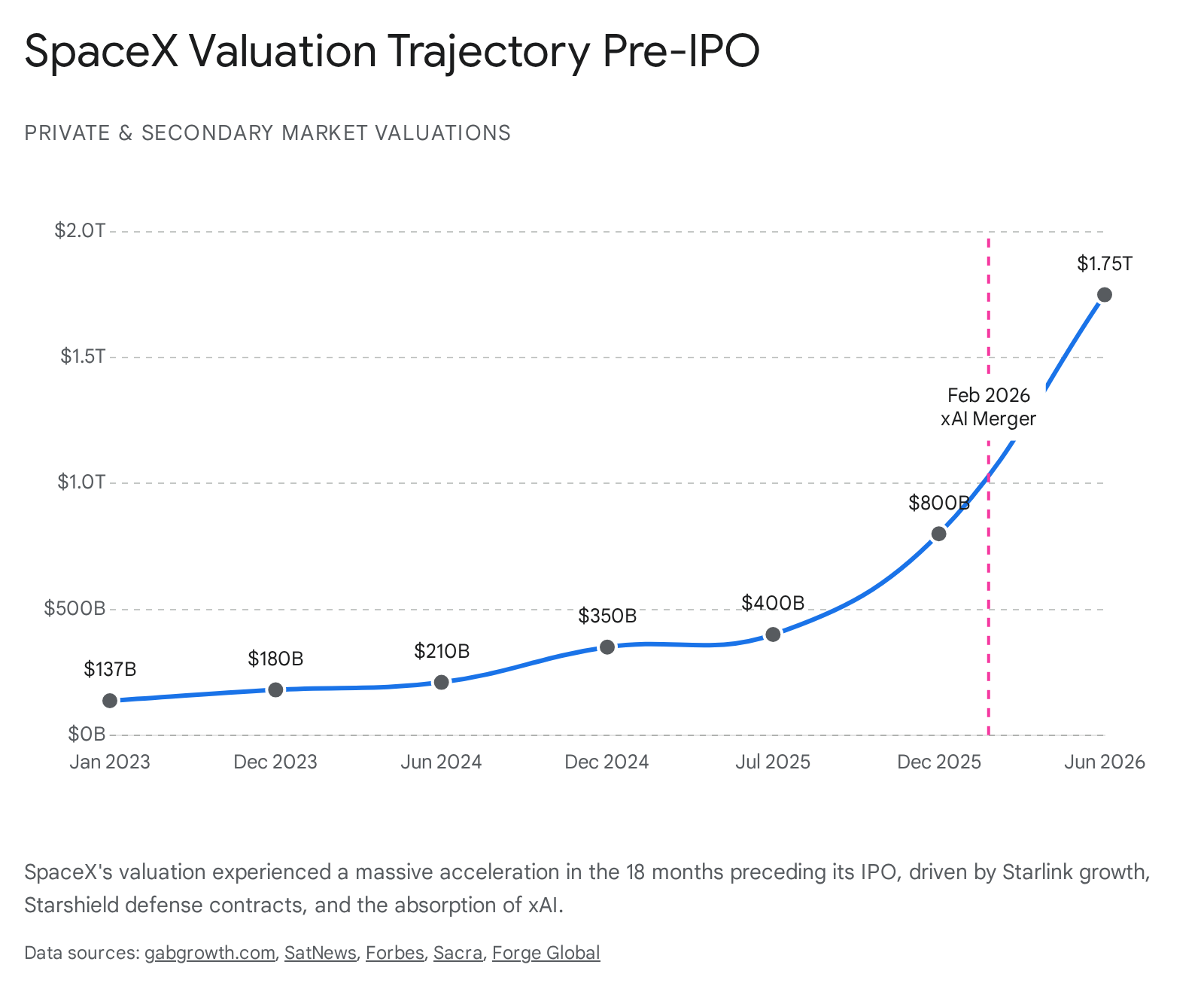

The $1.75 trillion IPO valuation represents the apex of an exponential appreciation curve in the secondary market over the preceding three years. For over two decades, SpaceX maintained its private status, utilizing periodic company-organized tender offers to provide liquidity for early investors and employees 45. This strategy allowed the company to establish progressively higher valuation benchmarks without subjecting its highly capital-intensive research and development programs to the short-term scrutiny of public equity markets 5.

The valuation curve steepened notably throughout 2024 and 2025. In January 2024, SpaceX was valued at approximately $137 billion following a primary funding round 6. By June 2024, an internal tender offer valued the company at $210 billion 618. Just six months later, in December 2024, a subsequent tender offer pushed the valuation to $350 billion at $185 per share 187. As Starlink revenues compounded and the company's defense footprint expanded, a July 2025 tender offer priced the enterprise at $400 billion 520. This figure doubled again to $800 billion by December 2025 during an insider share sale priced at $421 per share 578.

The most profound structural valuation shift occurred in February 2026 with the absorption of xAI. Prior to the merger, xAI completed a heavily oversubscribed $20 billion Series E funding round in January 2026, which valued the independent AI startup at approximately $250 billion 91024. The all-stock acquisition combined the $1 trillion valuation of SpaceX with the $250 billion valuation of xAI, establishing a baseline combined entity worth roughly $1.25 trillion at the time of the transaction 10725. The IPO pricing of $1.75 trillion in June 2026 effectively added $500 billion in enterprise value in just four months, a premium attributed to institutional conviction in the synergies of vertical AI infrastructure 16.

Consolidated Financial Performance

The S-1 filing provides the first audited, transparent look into the financial mechanics of SpaceX. The disclosures reveal a highly bifurcated enterprise where a single profitable segment subsidizes massive, cash-burning capital expenditures across the company's experimental aerospace and computational divisions 59.

For the full year 2025, SpaceX reported consolidated revenues of $18.67 billion, representing a 33.2% year-over-year increase from $14.02 billion in 2024 69. However, the company posted a GAAP net loss of $4.94 billion for 2025, reversing a $791 million profit recorded the prior year 2811. This financial deterioration accelerated in the first quarter of 2026, with the company posting a net loss of $4.28 billion on $4.69 billion in quarterly revenue, bringing the total accumulated deficit to $41.3 billion 1011.

Despite these deep GAAP losses, SpaceX generated $6.58 billion in adjusted EBITDA in 2025 58. The disparity between the net loss and positive adjusted EBITDA stems from the heavy depreciation of the Starlink constellation, non-cash stock-based compensation, and the upfront expensing of Starship and xAI research and development 812.

The consolidated entity requires immense capital to sustain its operations. Capital expenditures totaled $20.7 billion in 2025 and accelerated to an astonishing $10.1 billion in Q1 2026 alone 810. If this quarterly pace is maintained, the company will spend more on capital expenditures in 2026 than it generated in gross revenue in 2025 8. The corporate balance sheet reflects this strain, showing $24.7 billion in cash and equivalents at the end of 2025, which declined to $15.9 billion by March 31, 2026 - an $8.8 billion cash burn over a single quarter 4. The company holds $12.1 billion in deferred revenue and an official backlog of $28.4 billion from multi-year launch and enterprise connectivity contracts 4. In a notable deviation from traditional corporate treasury management, the S-1 also disclosed that SpaceX holds 18,712 Bitcoin, valued at approximately $1.29 billion 1329.

Segment Economic Asymmetry

The fundamental financial narrative of SpaceX is rooted in segment asymmetry. The S-1 formally divides the company into three reporting segments: Connectivity, Space, and AI/Other. Only one of these segments is currently profitable.

| Segment | FY 2025 Revenue | FY 2025 Operating Income / (Loss) | Segment Role & Context |

|---|---|---|---|

| Connectivity (Starlink) | $11.39 Billion | $4.42 Billion | Represents 61% of total revenue. Generates 63% adjusted EBITDA margins. The sole profit engine subsidizing all other operations 4510. |

| Space (Launch & Starshield) | $4.09 Billion | $(0.66 Billion)* | High internal profitability on Falcon 9 is offset by $3.0B in Starship R&D. External launch revenue growth is maturing 91114. |

| AI (xAI & X Platform) | $3.20 Billion | $(6.36 Billion) | Revenue derived from X premium subscriptions and API access. Heavy losses driven by massive supercomputer capital expenditures 5811. |

*Space segment operating loss is an approximation based on the reported Q1 2026 operating loss of $662 million against $619 million in quarterly revenue, combined with the heavy annual R&D burden noted in S-1 disclosures 1114.

Data indicates a stark reality: the Connectivity business generated nearly all of the consolidated EBITDA, masking the intense cash burn occurring in the Space and AI divisions 8. The financial viability of the entire $1.75 trillion valuation rests on Starlink's ability to continue funding the development of Starship and the build-out of xAI's computational infrastructure 4.

Connectivity Segment Analysis

The Connectivity segment, encompassing the Starlink low-Earth orbit (LEO) satellite internet constellation, operates as the primary anchor for the company's current valuation. In 2025, Starlink generated $11.39 billion in revenue, growing nearly 50% year-over-year 89.

Subscriber Growth and ARPU Compression

SpaceX's physical dominance in orbit is unmatched. The Starlink infrastructure consists of more than 9,600 active satellites, representing approximately 75% of all maneuverable satellites currently in low-Earth orbit 482. This network capacity has enabled aggressive subscriber acquisition. The active user base grew from 4.4 million in 2024 to 8.9 million by the end of 2025, reaching 10.3 million subscribers across 164 countries by the end of Q1 2026 41231.

However, the rapid expansion into international markets has exposed a critical vulnerability in the unit economics: Average Revenue Per User (ARPU) is experiencing severe compression.

| Metric | FY 2023 | FY 2024 | FY 2025 | Q1 2026 |

|---|---|---|---|---|

| Total Active Subscribers | 2.3 Million | 4.4 Million | 8.9 Million | 10.3 Million |

| Average Monthly ARPU | $99 | $91 | $81 | $66 |

Data derived from S-1 disclosures and historical subscriber reporting 10123233.

The Q1 2026 ARPU of $66 per month represents a 33% decline from 2023 levels 1032. In the S-1, management explicitly notes that ARPU is expected to continue declining as the subscriber base shifts away from early adopters in North America toward highly price-sensitive consumers in emerging markets, necessitating the introduction of lower-priced regional plans 3233.

To offset this consumer decay, SpaceX is heavily targeting the enterprise, aviation, and maritime sectors. While standard residential hardware kits typically cost a few hundred dollars, maritime and aviation services yield significantly higher margins. Maritime ARPU is estimated at $34,000 per month, while commercial aviation contracts can reach $300,000 per month, providing a high-margin counterweight to falling consumer subscription rates 534.

Direct-to-Device Expansion and Spectrum Policy

To dramatically expand its Total Addressable Market (TAM), SpaceX is developing Direct-to-Device (D2D) capabilities, allowing unmodified consumer smartphones to connect directly to Starlink satellites 35. Branded initially as Direct-to-Cell, the service officially launched commercial text messaging in July 2025 through a partnership with T-Mobile, with broadband data capabilities slated for subsequent rollout 3435.

This technological expansion has initiated intense regulatory disputes over radio spectrum allocation. In April 2026, the Federal Communications Commission (FCC) denied SpaceX's petition to operate in the 1.6/2.4 GHz Mobile Satellite Service bands, a ruling intended to protect incumbent spectrum holders such as Globalstar (which provides satellite services for Apple iPhones) and Iridium 351516. The FCC dismissed several operator requests, prioritizing regulatory certainty by enforcing exclusive spectrum rights 1516. To secure independent operational capacity and bypass these restrictions, SpaceX completed a $17 billion acquisition of wireless spectrum from EchoStar, enabling the company to negotiate with global cellular carriers more independently 535.

Concurrently, SpaceX has lobbied heavily for the modernization of satellite spectrum-sharing rules. In April 2026, FCC Chairman Brendan Carr proposed replacing the decades-old Equivalent Power Flux Density (EPFD) framework with a performance-based system 3839. The legacy EPFD rules forced low-Earth orbit constellations like Starlink to limit their transmission power to prevent interference with higher-orbit Geostationary (GSO) satellites 3839. If adopted, the new regulations will allow SpaceX to increase transmission power, effectively improving network capacity and reducing the total number of satellites required to maintain service speeds, despite significant resistance from legacy GSO operators such as SES and DirecTV 3839.

International Regulatory Friction

International expansion remains critical to sustaining Starlink's subscriber growth, but the company has encountered substantial geopolitical and regulatory hurdles in key emerging markets.

In India - a massive, underserved broadband market central to SpaceX's growth projections - the Ministry of Home Affairs froze final security clearances for Starlink just days before the June 2026 IPO 174118. Although the company secured a Global Mobile Personal Communication by Satellite (GMPCS) license in 2025, security agencies suspended commercial operations following reports that Starlink terminals were actively utilized in the Iran conflict, despite the service not being officially licensed in that jurisdiction 184319. Indian authorities expressed deep concerns regarding their ability to regulate a U.S.-controlled satellite network during geopolitical crises, demanding clarity on how SpaceX would handle conflicting demands from foreign governments 4319. This impasse has also stalled the approval of a national satellite-spectrum pricing framework, indefinitely delaying commercial rollout 1741.

In Africa, Starlink faces complex pricing dynamics and stringent local ownership laws. In Nigeria, macroeconomic inflation and currency devaluation forced the company to attempt a massive price hike in late 2024, raising monthly subscriptions from ₦38,000 to ₦75,000 2021. The Nigerian Communications Commission (NCC) initially blocked the unilateral increase, prompting Starlink to temporarily halt new residential orders in the country 2122. Following the NCC's broader approval of a 50% telecom tariff increase in early 2025, Starlink adjusted its monthly rate to ₦57,000 (approximately $35 to $39) 2349. Despite this adjustment, the recurring cost represents over 80% of the national minimum wage, restricting the service primarily to high-income earners and corporate entities 49.

In South Africa, despite being Elon Musk's country of birth, Starlink is entirely barred from operating 20. The nation's Black Economic Empowerment (BEE) policies mandate that foreign-owned telecommunications companies allocate at least 30% equity to historically disadvantaged groups, a requirement that SpaceX has thus far refused to accommodate 2022.

Space Launch and Defense Infrastructure

The Space segment, which encompasses the Falcon launch vehicles, Dragon capsules, Starship development, and the Starshield defense program, generated $4.1 billion in revenue in 2025, accounting for 22.5% of the consolidated top line 49.

Orbital Launch Monopoly

SpaceX currently operates a de facto monopoly in Western launch services. In 2025, the company executed 165 orbital launches, delivering 2,213 metric tons to orbit - representing over 80% of the world's total payload mass 431. The workhorse Falcon 9 is highly profitable on an internal unit-cost basis. Aided by boosters that have been successfully flown and recovered over 30 times, internal marginal costs are estimated to be as low as $17 million per launch, compared to commercial pricing of roughly $74 million 431.

Despite this dominance, external commercial launch revenue grew by only 8% year-over-year in 2025 431. This sluggish growth suggests that the traditional commercial satellite launch market is reaching maturity, and that a significant portion of Falcon 9's manifest is dedicated to internal Starlink deployments, which are eliminated in consolidated revenue reporting 49.

Starshield and Government Defense Contracts

To generate high-margin revenue beyond commercial launches, SpaceX developed Starshield, a militarized, secure variant of the Starlink bus designed specifically for government and intelligence applications 950. The defense sector has become highly lucrative; Starshield revenue reached approximately $1.8 billion in 2025, making it the company's second-fastest-growing sub-segment 9.

In May 2026, the U.S. Space Force awarded SpaceX a $2.29 billion fixed-price contract to build the Space Data Network (SDN) Backbone 50. The contract calls for a proliferated constellation of optically interconnected Starshield satellites to provide high-capacity, low-latency communications linking military sensors and weapons systems worldwide by 2027 50. This contract solidifies SpaceX's transition from a mere launch contractor to a foundational provider of national security satellite infrastructure 50.

Starship Development and Operational Risks

The core vulnerability, and the ultimate upside, of the Space segment rests entirely on the successful commercialization of Starship - a fully reusable, super-heavy launch vehicle. In the S-1 filing, management lists Starship as the single greatest execution risk facing the entire enterprise 48. The program is intensely capital-consuming, requiring $3.0 billion in R&D in 2025 and accelerating to an annualized pace of $3.7 billion by Q1 2026 9.

If successfully operationalized, Starship is designed to fundamentally alter the economics of space access. By recovering and reusing both the booster and the upper stage, payload costs to low-Earth orbit could fall from the Falcon 9's current ~$2,200/kg to between $200 and $300/kg 5124. This drastic cost reduction is a mechanical prerequisite for the company's most ambitious projections. The current Falcon architecture is physically incapable of lifting the heavier Starlink V3 satellites in sufficient volumes, nor can it deploy the massive infrastructure required for orbital data centers or planetary colonization 453.

Starship development remains constrained by persistent technical anomalies and strict regulatory oversight. Following a mixture of successful milestones and explosive failures during the initial dozen test flights, the Federal Aviation Administration (FAA) subjected the program to rigorous safety and environmental reviews 254. The FAA mandates that engineering advancements must be continually gated by administrative licensing delays, particularly concerning booster recovery operations at the Boca Chica facility 254. For prospective investors, Starship is not yet a reliable operating system; it is a highly capital-intensive research program that must succeed to justify the company's $1.75 trillion valuation 54.

Artificial Intelligence and Orbital Compute

The most controversial element of the SpaceX IPO is its pivot into artificial intelligence. In February 2026, SpaceX acquired Elon Musk's independent AI laboratory, xAI (which had previously merged with the social media platform X), in an all-stock transaction 14109. This acquisition brought the Grok foundational language models, the proprietary data firehose of the X platform, and massive supercomputing infrastructure directly into the SpaceX corporate structure 1011.

Capital Expenditures and the Colossus Infrastructure

The newly formed AI segment is currently the primary driver of corporate cash burn. In 2025, the segment generated $3.2 billion in revenue - mostly derived from X platform advertising and premium subscriptions - but posted a staggering operating loss of $6.36 billion 45. In the first quarter of 2026 alone, AI operations burned an additional $2.5 billion 8.

Prior to the merger, xAI raised unprecedented capital to fund its hardware acquisition. Following a $10 billion raise in 2025, the company completed an upsized $20 billion Series E round in January 2026, backed by investors including Valor Equity Partners, Fidelity, the Qatar Investment Authority, Nvidia, and Cisco 91055. This round valued the standalone xAI entity at roughly $250 billion 924.

This capital is actively being deployed to construct the "Colossus" supercomputing clusters, primarily located in Memphis, Tennessee. By the end of 2025, xAI reported operating over one million Nvidia H100 GPU equivalents to train the advanced Grok 4 and Grok 5 models 1055. To secure future revenue against these massive hardware expenditures, the segment signed a landmark cloud services agreement with Anthropic in May 2026, contracting up to $1.25 billion per month in compute supply through 2029 (totaling up to $45 billion before adjustments) 832. Furthermore, the S-1 disclosed a pending $60 billion acquisition of the AI coding startup Cursor, a strategic outlay intended to merge developer workflows with SpaceX's underlying compute infrastructure 111132.

Orchestration Economics and Orbital Data Centers

The strategic logic of merging a rocket manufacturer with an AI lab centers on physical energy constraints and "Orchestration Economics." On Earth, the AI industry faces severe terrestrial power grid bottlenecks; U.S. data centers are projected to consume 470 terawatt-hours of electricity by 2030, constrained by land availability and grid capacity 25. SpaceX's long-term thesis aims to bypass these limitations by deploying 100-gigawatt AI data centers in low-Earth orbit starting in 2028 1157. These orbital facilities would be powered by uninterrupted, atmospheric-free solar energy, beamed or utilized directly in space to run inference workloads 2557.

Industry analysts suggest this strategy aligns with a structural shift in the software economy, often termed the "SaaSpocalypse" 58. As foundational Large Language Models (LLMs) commoditize, economic value is migrating from software applications toward the physical "orchestration layer" 585960. Bullish analysts argue that by owning the entire vertical stack - from silicon manufacturing and launch vehicles to satellite constellations and foundational models - SpaceX is building an insurmountable structural moat that software-only competitors like OpenAI or Anthropic cannot replicate 261.

Corporate Governance and the Ecosystem

SpaceX lists as a "controlled company" under Nasdaq regulations, utilizing a dual-class share structure 48. Class B shares carry 10 votes per share, granting CEO Elon Musk an estimated 85.1% of the total voting power 4107. This structure renders Musk immune to activist investor pressure or hostile removal, shielding the company's multi-decade vision from the short-term earnings demands typical of public markets, while simultaneously concentrating immense key-person risk 27.

Executive compensation is heavily tied to the company's most extreme long-term ambitions. The S-1 details a 1-billion-share restricted stock grant to Musk that vests in 15 tranches 4. Vesting requires hitting sequential market capitalization milestones (scaling up to $7.5 trillion) combined with unprecedented operational achievements, culminating in the establishment of a self-sustaining human colony on Mars with at least one million people 410. A separate tranche is tied to the construction of non-Earth data centers capable of delivering 100 terawatts of compute 4.

The IPO has also catalyzed speculation regarding further consolidation of the "Musk ecosystem." Wedbush Securities analyst Dan Ives has publicly assigned an 80% to 90% probability that Tesla and SpaceX will formally merge by early 2027 6226. Proponents point to the joint "Terafab" facility in Austin, Texas, a shared manufacturing plant designed to produce custom silicon chips for both Tesla's autonomous vehicles/robotics and SpaceX's orbital infrastructure 256264. While purely speculative, the potential creation of a $3.4 trillion conglomerate spanning energy, robotics, automotive, aerospace, and AI adds a layer of highly complex optionality to the SPCX equity narrative 2627.

Institutional Valuation Projections

At an IPO valuation of $1.75 trillion against $18.67 billion in trailing 2025 revenue, SpaceX trades at a price-to-sales multiple of approximately 94x 152. This multiple vastly exceeds historical norms for mature aerospace contractors and implies growth trajectories rarely sustained by mega-cap technology equities 6. Consequently, Wall Street is sharply divided, with projections reflecting irreconcilable assumptions regarding execution risk, AI monetization, and the timeline for space commercialization 3.

Bullish Institutional Models

Bullish analysts view the 94x trailing multiple as a temporary artifact, arguing the current valuation serves as a discounted entry point into a company targeting a self-reported $28.5 trillion total addressable market 1451.

| Analyst / Firm | Target Price / Valuation | Core Thesis & Projections |

|---|---|---|

| Morgan Stanley | $3.4 Trillion (by 2040) | Estimates $3.4 trillion in revenue and $2.7 trillion in adjusted EBITDA by 2040, driven heavily by AI infrastructure and orbital compute 71329. |

| New Street Research | $165 / share ($2.3 Trillion) | Sum-of-the-parts model assigning $650B to Starlink, $100B to Launch, and $575B to xAI. Projects $195B in revenue by 2030 616628. |

| Oppenheimer | $190 / share | Focuses on vertical integration of the AI hardware/software stack. Forecasts $900 billion in revenue by 2035 253. |

| Goldman Sachs | IPO Lead Underwriter | Projects $474 billion in total revenue by 2030, with AI-related services accounting for $322 billion 7. |

Data aggregated from pre-IPO analyst notes and financial media disclosures 725366.

Firms like New Street Research assign a premium specifically for the physical infrastructure stack. Analyst Pierre Ferragu values xAI at $575 billion standalone - a 60% premium over pure-play AI software competitors like OpenAI - precisely because SpaceX owns the rockets and satellites necessary to deploy orchestration technology in orbit 6166.

Bearish Perspectives and Market Risks

Conversely, skeptics argue that the $1.75 trillion valuation represents a speculative bubble fueled by the scarcity of the asset and retail enthusiasm for Elon Musk's brand 2930.

Morningstar issued a highly cautious fair value estimate of just $63 per share - a 53% discount to the IPO price, valuing the enterprise at approximately $780 billion 2230. Morningstar's discounted cash flow analysis assigns roughly $40 per share to the core Space and Connectivity businesses, indicating that the IPO price fully bakes in what they term the "Moonshot scenario" 30. This scenario requires the flawless, rapid reusability of Starship and the highly profitable deployment of orbital data centers, an outcome Morningstar assigns only a 7% probability of success before 2028 30.

Prominent short-sellers and value investors echo these concerns. Investor Jim Chanos criticized the 90x sales multiple on a company that swung to a nearly $5 billion net loss in 2025, suggesting the market is irrationally discounting reality in favor of promises 213. Historical data from University of Florida finance researchers indicates that mega-cap IPOs priced above 40x sales trail the broader market over three-year horizons in the vast majority of cases 13. Should Starship face prolonged testing delays or xAI fail to generate returns on its massive supercomputing expenditures, public market participants may enforce a severe multiple contraction, particularly as insider lock-up periods expire 370.