Transaction Utility Theory and Consumer Pleasure from Deals

Classical microeconomic theory has historically posited that consumer choice is an exercise in rational utility maximization under strict budget constraints 123. In this traditional framework, consumers evaluate a potential purchase by comparing the absolute value of the product to the absolute value of the capital required to obtain it, operating solely on the principles of acquisition utility 234. However, this model routinely fails to explain pervasive market anomalies. Consumers frequently travel out of their way to save trivial amounts on inexpensive items, refuse to purchase highly desired items when the price feels unfair, and impulsively acquire unneeded goods simply because they are heavily discounted 5.

To resolve these contradictions, behavioral economics introduced the concept of transaction utility. Developed by Richard Thaler, transaction utility theory argues that the psychological value of a purchase consists of two distinct components: the value derived from the item itself and the value derived from the perceived quality of the financial deal 23569. By formalizing the psychological pleasure of securing a bargain independent of the product's functional utility, this framework provides a crucial lens for understanding modern consumer behavior, neurobiological reward processing, e-commerce pricing strategies, and the regulatory challenges of deceptive marketing 67.

Theoretical Framework of Value Perception

Acquisition Utility Versus Transaction Utility

The foundational premise of transaction utility theory is that consumers do not evaluate prices in a vacuum; they evaluate prices relative to internal expectations. Acquisition utility represents the economic concept of consumer surplus 23. It is calculated as the inherent value the consumer places on the good minus the actual price paid 23. If a consumer values a jacket at $100 and pays $100, the acquisition utility is neutral. If they value it at $100 and pay $80, there is a positive acquisition surplus.

Transaction utility, conversely, is entirely decoupled from the product's inherent value or the consumer's need for it. It is defined as the difference between the actual price paid and the consumer's expected or reference price 245. If the consumer expects the jacket to cost $150 based on a manufacturer's suggested retail price (MSRP) but finds it on sale for $80, the transaction utility is highly positive. The consumer experiences psychological pleasure from the perceived $70 saving, regardless of whether the jacket fulfills a functional need 45. Conversely, if the consumer expects to pay $50 but the price is $80, they experience negative transaction utility and may reject the purchase even if their internal valuation of the jacket exceeds $80 511.

| Feature | Acquisition Utility | Transaction Utility |

|---|---|---|

| Core Definition | The value derived from owning and utilizing a product or service. | The psychological value derived from the financial terms of the deal itself. |

| Classical Equivalent | Consumer surplus (subjective value minus opportunity cost). | No direct equivalent in standard neoclassical models. |

| Primary Calculation | Product Valuation minus Actual Price Paid. | Reference Price minus Actual Price Paid. |

| Behavioral Driver | Needs, functional benefits, and product quality. | Perceived fairness, discounts, and framing relative to expectations. |

| Potential Negative Outcome | Product fails to meet functional expectations. | Price feels exploitative or unfair relative to market norms. |

The Function of Reference Prices

Transaction utility relies entirely on the existence of a reference price, which acts as the psychological anchor against which the current price is judged 234. Reference prices are formed through a complex synthesis of past purchasing experiences, contextual cues within the retail environment, explicit MSRPs, and competitor pricing 458.

Because human cognition relies heavily on heuristics, consumers rarely maintain an accurate, objective database of market clearing prices for all goods. Instead, they rely on the immediate context provided by the retailer 4. The behavioral theory of arbitrary coherence demonstrates that initial price exposures shape the perception of future prices 4. If a consumer is consistently exposed to a high suggested retail price, a subsequent discount generates substantial positive transaction utility, rendering the deal highly attractive even if the final discounted price is mathematically identical to a competitor's standard everyday price 45.

This reliance on relative changes from a reference point aligns seamlessly with prospect theory, which dictates that individuals process economic outcomes as relative gains or losses rather than absolute states of wealth 259. Furthermore, prospect theory posits that losses are felt more intensely than equivalent gains. Applied to pricing, this means negative transaction utility (a markup above the reference price) deters purchasing more severely than an equivalent positive transaction utility (a discount) encourages it 29.

Laboratory Evidence of Transaction Utility

Asymmetry of Gains and Losses in Pricing

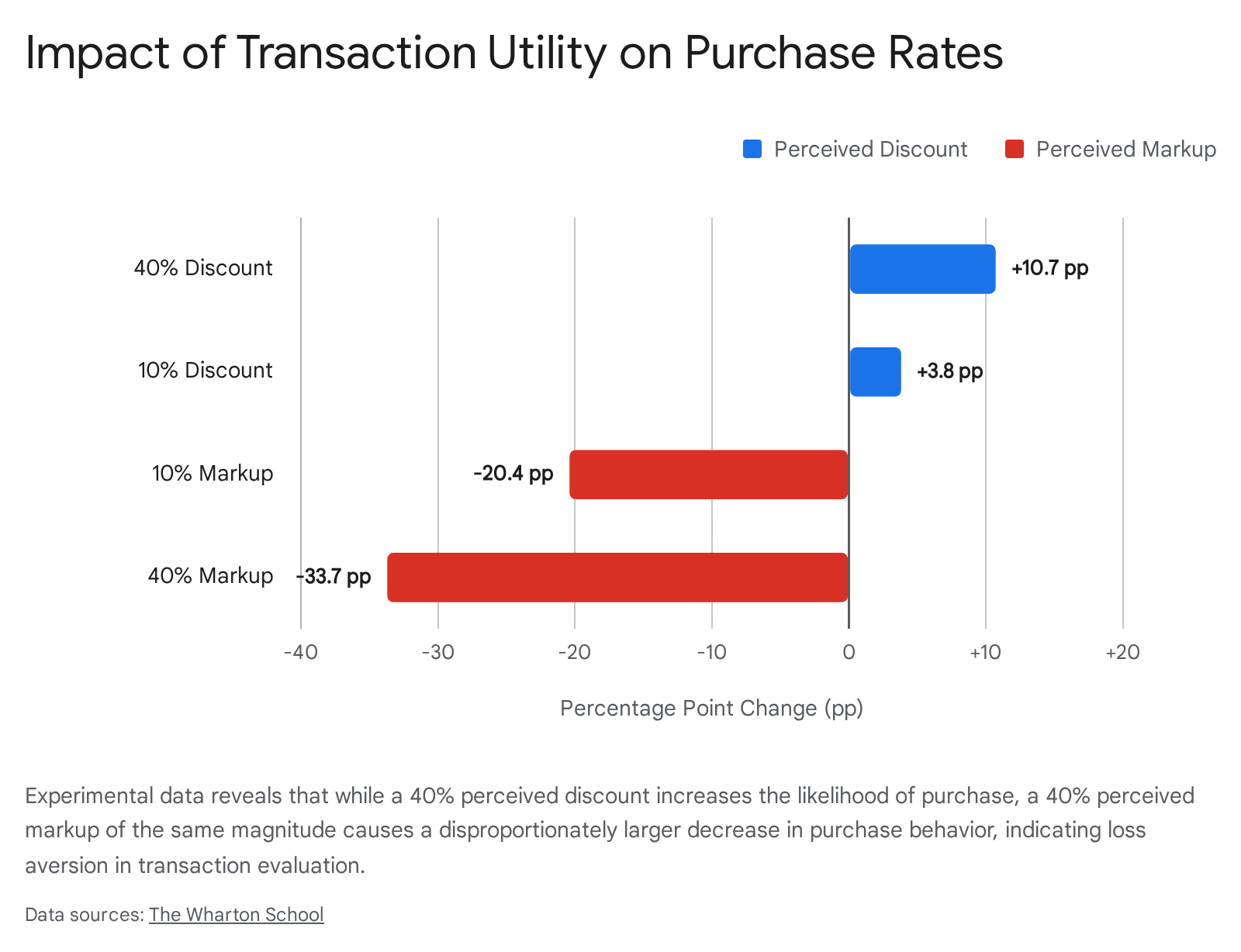

In laboratory paradigms designed to isolate variables related to value perception, the independent influence of transaction utility is pronounced. A prominent study utilizing a discount and markup game with virtual products demonstrated that consumers will actively sacrifice monetary payoffs specifically to maximize transaction utility 6. When an irrelevant original price was displayed above the selling price to suggest a discount, purchase rates increased significantly. In baseline assessments, a perceived 10% discount led to a 3.8 percentage point increase in purchasing, while a 40% perceived discount led to a 10.7 percentage point increase 6.

Conversely, the study quantified the asymmetric impact of loss aversion predicted by prospect theory. When the original price was below the selling price, suggesting a markup, the purchase rate dropped drastically. A 10% perceived markup caused a 20.4 percentage point decrease in purchasing, and a 40% perceived markup caused a 33.7 percentage point decrease 6.

Participants exhibited a calculable marginal rate of substitution where they were willing to sacrifice 37 to 57 cents in actual earnings to gain one dollar of perceived discount, and 37 to 78 cents to avoid a dollar of perceived markup 6.

The Coupon Trap Paradigm

Further isolating the psychological weight of a deal, researchers developed a coupon paradigm where participants were forced to choose between two virtual products. One product always generated higher total earnings but lower transaction utility, while the other generated higher transaction utility but lower overall earnings 6. Empirical results revealed that participants voluntarily sacrificed monetary earnings to purchase the product that created higher transaction utility thirty percent of the time 6.

Specifically, 28.5% of participants were willing to forfeit a dollar in actual earnings simply to gain an additional 50 cents in perceived discount 6. This phenomenon indicates that coupons and structured discounts can induce consumers to purchase suboptimal or more expensive products solely to maximize the usage of the coupon, even when this behavior actively diminishes their net consumption utility 6.

Diminishing Returns on Promotional Intensity

While transaction utility positively correlates with purchase intent, laboratory and field data demonstrate an eventual saturation point. The impact of discounts on consumer purchase intention follows an S-shaped response curve 8. Minor discounts fail to register meaningful transaction utility, while moderate discounts trigger rapid increases in purchase likelihood. However, once a discount exceeds a certain promotional saturation point, further price reductions yield minimal behavioral changes 8. This effect is compounded when retailers offer continuous, uninterrupted discounts. Over time, perpetual discounts recalibrate the consumer's internal reference price downward, permanently eroding the transaction utility and neutralizing the promotion's effectiveness 2.

Neurobiological Substrates of the Purchasing Decision

The behavioral phenomena described by transaction utility theory have been largely corroborated by neuroimaging and psychopharmacological research. The human brain processes the components of a purchase through distinct, competing neural pathways, encoding both the pleasure of the deal and the pain of the expenditure 101112.

Dopaminergic Anticipation and Reward Processing

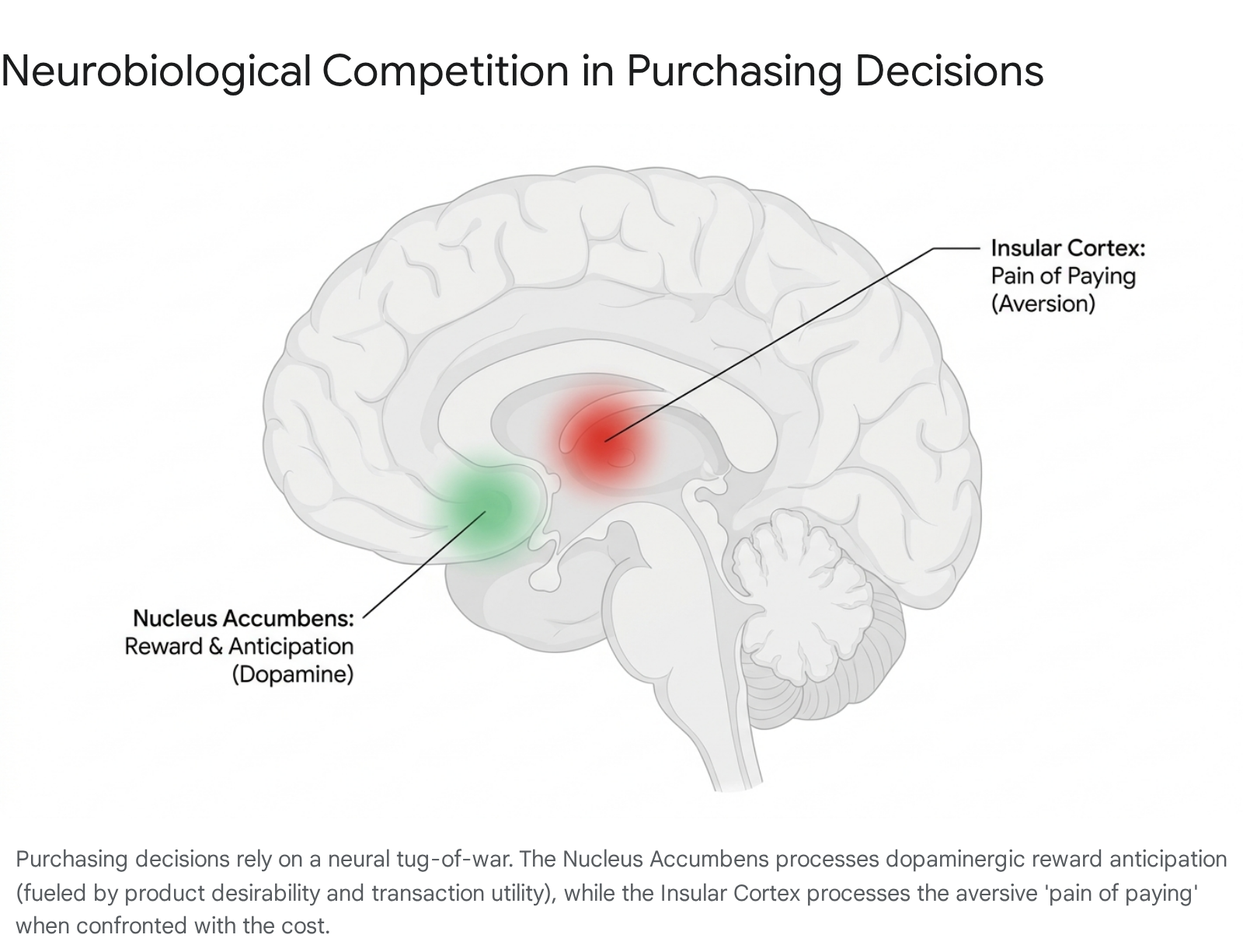

The psychological pleasure derived from securing a bargain is heavily mediated by the brain's dopaminergic reward system 1213. Functional magnetic resonance imaging (fMRI) studies demonstrate that when a consumer is exposed to a desirable product, the nucleus accumbens, a key node in the dopamine reward pathway associated with anticipated pleasure, shows significant activation 10. Importantly, dopamine release does not merely reflect the absolute magnitude of a reward, but rather the subjective value and the prediction error 121314.

Research utilizing the Becker-DeGroot-Marschak auction mechanism in primates has shown that midbrain dopamine neurons fire in direct correlation with trial-by-trial fluctuations in subjective reward value, confirming that the dopamine reward signal acts as an instantaneous utility prediction error signal 131516. When an outcome exceeds expectations, such as encountering a steep unexpected discount, the resulting positive prediction error triggers a burst of dopamine 1314. This dopaminergic surge biologically encodes transaction utility, providing an immediate neurochemical reward for navigating the financial interaction successfully 1521.

The Sunk Cost Mechanism and Effort Valuation

Dopamine pathways are intricately linked to the perception of effort and sunk costs 17. In environments with limited resources, achieving a reward after significant effort triggers higher dopamine secretion 17. Experimental mouse models demonstrate that acetylcholine is essential in linking the volume of dopamine released to the magnitude of the effort expended to obtain a reward 17.

This neurobiological mechanism explains why consumers often derive heightened transaction utility from deals that require active participation, such as hunting for a coupon, waiting in a digital queue for a flash sale, or negotiating a price 17. The exertion of effort amplifies the dopamine response upon securing the item, embedding the deal with greater subjective value and reinforcing the irrational adherence to sunk costs 17. Because dopamine reinforces previous behaviors, the release enables organisms to pay steep behavioral costs in the future, translating directly into the consumer habituation seen in bargain hunting 17.

Insular Cortex Activation and the Pain of Paying

While the nucleus accumbens processes the acquisition and transaction rewards, the actual transfer of capital triggers a competing neural mechanism. When consumers are exposed to price tags, particularly those perceived as unfairly high, fMRI scans reveal activation in the insular cortex and prefrontal cortex 1011. The insular cortex is heavily involved in processing aversive stimuli, including physical pain and nicotine withdrawal 1011.

This neurological reaction confirms the behavioral concept of the pain of paying 101118. If a price significantly exceeds the reference price, generating negative transaction utility, the insula activation functions as a distress signal that actively deters the purchase 11. This indicates that high prices do not deter spending purely through the rational calculation of foregone alternative pleasures, but through the immediate neurological induction of pain 1119. The final purchasing decision is the result of a neural competition: the dopaminergic anticipation of the product and the deal weighed against the aversive pain of the price 1011.

Recent functional positron emission tomography (fPET) studies incorporating 6-[18F]FDOPA uptake have further illuminated sex differences in these neurobiological responses 20. In a behavioral evaluation of reward processing, monetary gain induced stronger increases in ventral striatum dopamine synthesis in men, whereas the opposite effect was discovered in women, providing a neurobiological basis for differing sensitivities to reward and punishment during financial transactions 20.

Payment Modalities and Psychological Friction

Because the pain of paying directly opposes transaction utility, consumer behavior is heavily influenced by the format and timing of the transaction. Techniques that separate the act of consumption from the act of payment alter the consumer's mental accounting, mitigating the neurological pain of the transaction and allowing transaction utility to dictate the purchase 1819.

Mental Accounting and Resource Categorization

Mental accounting theory posits that individuals categorize funds into distinct, non-fungible mental accounts based on their origin and intended use 192122. When a transaction aligns with a predefined mental budget, it is processed differently than an unexpected expense. For instance, the house money effect illustrates that consumers are significantly more willing to take financial risks or make impulse purchases with perceived gains or found money than with their earned capital 2122.

Furthermore, double-entry mental accounting theory describes the reciprocal interactions between the pleasure of consumption and the pain of paying 1018. Through prospective accounting, consumption that has already been paid for is buffered against the pain of payment, freeing the consumer to enjoy the product entirely decoupled from its cost 18. The degree to which consumption reminds the consumer of their payment dictates the intensity of the pain experienced 18.

The Cashless Effect and Digital Transactions

The format of the payment drastically impacts loss aversion. Physical cash transactions require a tangible surrender of resources, generating acute pain of paying and functioning as a highly effective check against impulsive behavior 19. Tightwads, or individuals with high self-control, experience intense discomfort from spending physical cash, prompting them to adhere strictly to budgetary constraints 1922.

Conversely, credit cards, digital wallets, and mobile payments effectively anesthetize the pain of paying 101118. By decoupling the physical loss of money from the acquisition of the good, the insula response is measurably dampened 1018. When the pain of paying is minimized, the positive transaction utility of a perceived deal encounters less psychological resistance. Online cash transactions eliminate geographical constraints and reduce the tactile feedback of spending, rendering digital payments less painful than both cash and physical cards, which inherently fuels higher spending and impulsive purchases 1819.

Buy Now Pay Later Ecosystems

The psychological decoupling of payment and consumption has been aggressively formalized in the modern retail environment through Buy Now, Pay Later (BNPL) platforms 232425. BNPL services allow consumers to acquire goods immediately while dividing the cost into interest-free installments, typically distributed over a six-week period 2324. At roughly 9 percent adoption across the United States as of 2023, BNPL represents a systemic shift in how consumers process transaction costs 24.

Research indicates that BNPL fundamentally alters transaction utility by manipulating temporal framing and alleviating perceived financial constraints 23. By framing the initial outlay as a minor fraction of the total price, BNPL drastically reduces the immediate pain of paying 1823. A difference-in-difference analysis of customer transaction data revealed that introducing BNPL options at a major US retailer led to statistically significant increases in both purchase incidence and total basket size 23. Economic modeling indicates that BNPL effectively acts as a price-discrimination tool, offering subsidized loans that increase overall sales by roughly 20%, driven largely by low-creditworthiness consumers 26.

However, this systemic reduction in the pain of paying carries severe macroeconomic side effects. Studies matching retail purchasing with banking data across 10.6 million consumers show that BNPL adoption causes rapid deterioration in financial health metrics. Following BNPL adoption, users average a 4.0% increase in overdraft charges, a 1.1% increase in credit card interest, and a 2.3% increase in credit card late fees 2527. By subsidizing the acquisition of positive transaction utility through frictionless deferred payments, BNPL functionally facilitates overborrowing, demonstrating the hazard of manipulating transaction utility without absolute consumer transparency 242627.

Algorithmic Pricing and E-Commerce Strategies

The digitalization of retail has transformed transaction utility from a static pricing strategy into a dynamic, highly engineered environment. In e-commerce, retailers possess the technological infrastructure to actively manipulate reference prices and consumer effort to maximize the perception of a deal 2834.

Dynamic Pricing and Reference Volatility

In traditional brick-and-mortar retail, altering prices requires physical labor, resulting in relatively stable reference prices. In e-commerce, algorithmic dynamic pricing systems adjust prices continuously based on supply, competitor data, and individual consumer profiling 28342930. This practice effectively weaponizes transaction utility by injecting volatility into reference prices, creating artificial urgency 2931.

During major seasonal sales, algorithms rely on the heightened consumer expectation of discounts 3431. The aggregate price elasticity of demand in digital markets is highly variable across categories, estimated at -1.72 in electronics and -0.89 in fashion 28. Dynamic pricing has been shown to raise overall revenue by an average of 12.3% 28. However, this volatility introduces a threshold effect: excessive pricing intensity increases cart abandonment by 8.7%, indicating an inverted-U relationship between dynamic pricing activity and net revenue gains 28. Furthermore, promotional frequency exhibits diminishing returns; deploying more than three event sales per quarter exhausts the consumer base 28. When consumers detect hyper-frequent price shifts, the credibility of the reference price erodes, nullifying the transaction utility 62831.

Price Discrimination and Surveillance Pricing

To counteract expectation fatigue, retailers deploy surveillance pricing, where artificial intelligence algorithms adjust prices based on individual user data to match specific price sensitivities 3832. Investigations by regulatory bodies and consumer protection groups have found that algorithmic systems occasionally charge specific consumers up to 23% more for the identical item ordered from the same store at the exact same time 32.

By presenting a personalized price, the algorithm ensures that the individual consumer perceives just enough transaction utility to trigger a purchase. This tactic extracts maximum consumer surplus while maintaining the illusion of a bargain 2638. Recognizing the deceptive nature of personalized algorithmic pricing, states like New York have passed legislation requiring retailers to explicitly disclose when a price has been algorithmically generated using personal data, aiming to restore transparency to the reference price formulation 3832.

Promotional Framing and Regulatory Focus Theory

The exact linguistic framing of a discount dictates how the transaction utility is neurologically received. Regulatory focus theory suggests that human motivation is rooted in the dual needs for advancement (promotion focus) and security (prevention focus) 33. E-commerce marketers match pricing language to these psychological states to trigger regulatory fit 33.

A sales promotion worded as "Get $1 Off" emphasizes achieving a gain, which appeals directly to promotion-focused consumers 33. Conversely, framing the exact same mathematical discount as "Save $1" emphasizes avoiding a loss, appealing to prevention-focused individuals 33. When the linguistic framing of the transaction utility matches the consumer's internal regulatory focus, it acts as a subtle behavioral nudge, stimulating broader purchasing behavior beyond the specific item on sale 33.

Gamification and Extrinsic Motivation

Beyond algorithmically shifting prices, retailers artificially inflate transaction utility through gamification. This involves integrating game mechanics, such as point scoring, limited-time challenges, and spin-to-win wheels, into non-game retail environments 2134423536.

Disguising Spending as Play

Gamification exploits the human desire for achievement and instant gratification, fundamentally altering the consumer's psychological state during the shopping journey 343537. From a neurobiological standpoint, winning a mystery discount or unlocking a reward tier triggers extrinsic motivation pathways, flooding the brain with dopamine prior to the actual purchase 213637. Because the consumer expended effort by spinning a virtual wheel or collecting digital tokens to earn the discount, the psychological value of the discount is magnified by the sunk cost effect 1738.

Self-determination theory clarifies that these psychological outcomes rely on fulfilling basic psychological needs: autonomy, competence, and relatedness 3638. By allowing a consumer to win a discount, the retailer fulfills the consumer's need for competence, making the resulting transaction utility feel earned rather than arbitrarily granted 3638. A study of 8,000 consumers revealed that nearly 90% are more likely to participate in online events when guaranteed a special offer 3747. By disguising the act of spending as an act of playing, gamified discounts shift the consumer's focus entirely away from acquisition utility, relying almost exclusively on the manufactured transaction utility to close the sale 3537.

Sunk Cost Amplification Through Engagement

The engagement required by gamified retail creates a habit-forming tendency 39. Repeated exposure to reward-based features, including points redemption and achievement badges, generates higher purchase rates and cultivates strong platform dependency 3539. The natural desire to win often overshadows the practical considerations of whether the purchase is financially sensible, leveraging the thrill of the game to override rational budget constraints 37. In some instances, consumers only realize they must spend capital to claim their newly won free items after the emotional high of the game has already manipulated their mental accounting 3537.

Cross-Cultural Variations in Market Interactions

While the neurological mechanisms underlying transaction utility are largely universal, the behavioral expression of price evaluation is heavily modulated by cultural frameworks and historical market norms. The perception of a fair deal varies significantly depending on societal trust levels and prevailing methods of price discovery 4940.

Haggling Protocols in Low-Trust Societies

In societies characterized by weaker institutional safety nets, high inflation, or a high prevalence of economic volatility, haggling and negotiation represent standard market practices 49. In these low-trust environments, fixed prices are viewed with skepticism; transaction utility must be actively negotiated to ensure fairness 49. The process of bargaining serves a dual purpose. First, it establishes the reference price dynamically in the absence of a trusted central authority. Second, it builds a social bond and tests reputational trust between the buyer and seller 49. In such cultures, accepting a first offer yields zero transaction utility and often implies the buyer has been exploited 49.

Fixed-Price Norms and Transaction Efficiency

Conversely, in high-trust societies, fixed pricing is the dominant paradigm. Historically popularized by department stores in the 19th century to democratize shopping, the fixed price tag acts as a social contract indicating transparency and consistent treatment 49. In cultures like Japan or Scandinavia, attempting to negotiate a marked price carries a high psychological cost and is often perceived as rude or indicative of deep distrust 49. In these environments, transaction utility is primarily communicated through formal sales events, transparent markdowns, and targeted couponing rather than interpersonal negotiation 49. By removing the anxiety of active negotiation, the fixed-price system allows consumers to base their transaction utility strictly on the retailer's advertised reference prices 49.

Collectivist Versus Individualist Fairness Evaluations

Cultural dimensions, specifically the spectrum between collectivism and individualism, dictate how consumers evaluate the fairness of their transaction utility relative to others. Research comparing Chinese and American consumers highlights distinct reactions to price discrepancies among peers 4152.

Chinese consumers, rooted in collectivist structures and high power distance orientations, demonstrate high sensitivity to relationship contexts 4152. They react intensely if a friend or an in-group member receives a better price than they do, viewing it as a severe violation of fairness that deeply damages transaction utility 4152. In contrast, American consumers, operating in a highly individualistic framework, process price discrepancies more uniformly 4152. They evaluate the transaction strictly against their own reference point and are significantly less likely to alter their perception of transaction utility based on the social context of a referent customer receiving a different deal 4152.

Regulatory Environment and Market Failures

Because transaction utility holds powerful sway over consumer choice, retailers are heavily incentivized to inflate reference prices artificially to make deals appear more attractive. When this practice crosses from aggressive marketing into deception, it triggers regulatory intervention and generates long-term consumer backlash 424344.

Artificial Price Inflation and Deceptive Marketing

The practice of citing a high, fabricated original price, such as an inflated MSRP or a compare-at price that was never actually charged, is a common tactic to artificially generate transaction utility 424445. By establishing a falsely high psychological anchor, the retailer ensures the consumer perceives a massive discount, triggering the dopaminergic reward cycle 4445.

Under Section 5 of the Federal Trade Commission (FTC) Act, promotional pricing guidelines mandate that former prices cited in advertisements must be actual, bona fide prices offered to the general public on a regular basis for a reasonably substantial period 4446. The FTC, alongside various state attorneys general, has increasingly targeted these deceptive practices across multiple industries. Recent enforcement actions include multi-million dollar settlements with automotive dealers charging hidden add-on fees that destroyed advertised transaction utility, and major e-commerce platforms using unlawful comparison prices that did not match prevailing market rates 434458.

The regulatory landscape is continually adjusting to penalize these infractions, with the FTC recently adjusting the maximum civil penalty dollar amount for violations of Section 5 to $51,744 per incident to account for inflation 46. Recent class-action lawsuits against major retail conglomerates further allege that false reference pricing artificially inflates the true market price by manipulating the consumer's internal reference point, thereby illegally extracting consumer capital through the manufacture of illusory transaction utility 45.

Long-Term Repercussions of Negative Transaction Utility

When consumers discover that a reference price was fabricated, or when they are subjected to unexpected hidden fees, the anticipated positive transaction utility rapidly inverts into severe negative transaction utility 211. This psychological whiplash generates feelings of betrayal and injustice.

Marketing research demonstrates that negative experiences stemming from deceptive pricing lead directly to brand hate, an extreme psychological state where consumers cultivate profound negative emotions toward the offending entity 47. While acquisition utility failures, such as a product breaking, can often be resolved through returns or warranties, transaction utility failures directly damage underlying trust 4760. Studies show that approximately 70% of consumers will abandon a brand after just two negative experiences, and 24% will engage in permanent brand switching after a single highly negative encounter 48.

Furthermore, if a brand relies too heavily on frequent, aggressive discounting to drive short-term transaction utility, it risks inducing expectation fatigue 49. When the discounted price becomes the expected baseline in the consumer's mind, the transaction utility vanishes entirely 249. Any subsequent attempt to sell the product at its actual full price yields severe negative transaction utility, effectively destroying the firm's long-term profit margins and crippling customer lifetime value 249. Retailers must meticulously balance the immediate behavioral pull of transaction utility against the long-term sustainability of their pricing architecture to avoid permanently compromising their market position.